Equities

The Q2 reporting season underscores the resilience of corporate earnings, supporting our bullish outlook for equities, an outlook further bolstered by expectations of fiscal and monetary easing. However, for now, we are booking profits, closing overweights in Technology and Growth, and initiating a new overweight in Real Estate.

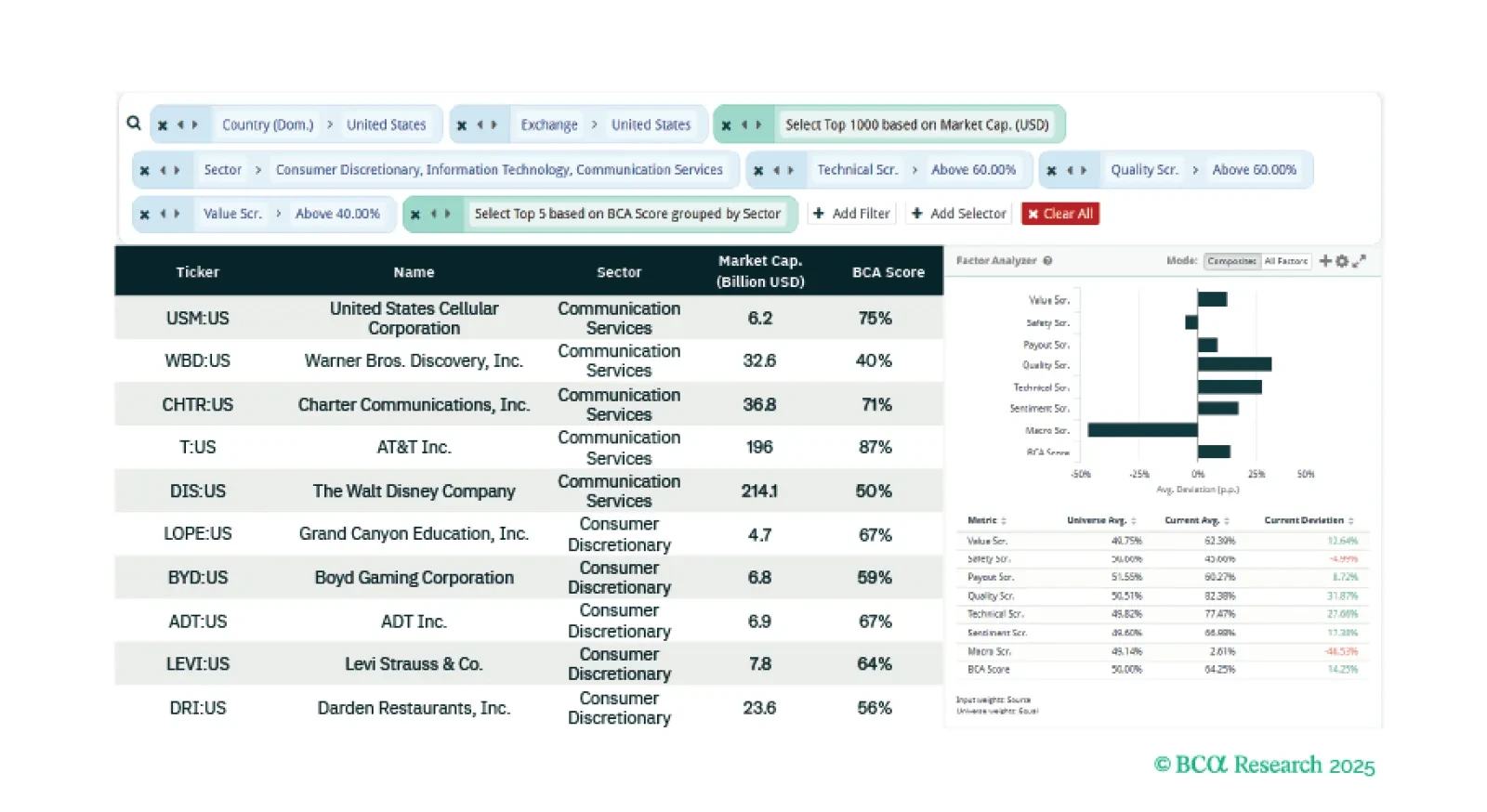

This week our three screeners identify: Broader and more accessible tech-driven equities, US equities exposed to cryptocurrencies, and doubling-down on top-decile stocks.

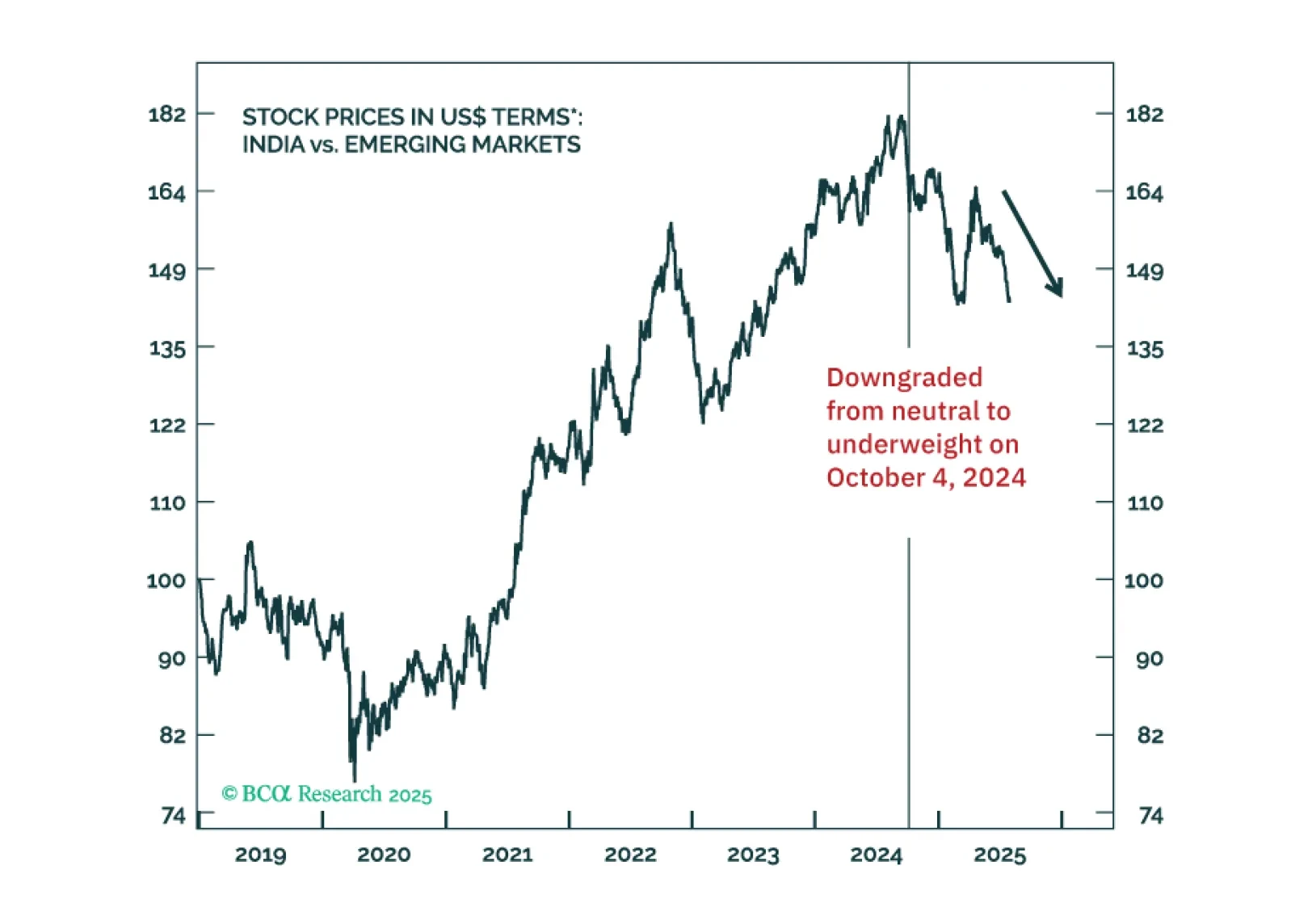

A high US tariff and the lingering uncertainties on the US-India trade deal will hurt investors sentiment. This and contracting corporate profits will push share prices lower. Stay underweight Indian stocks.

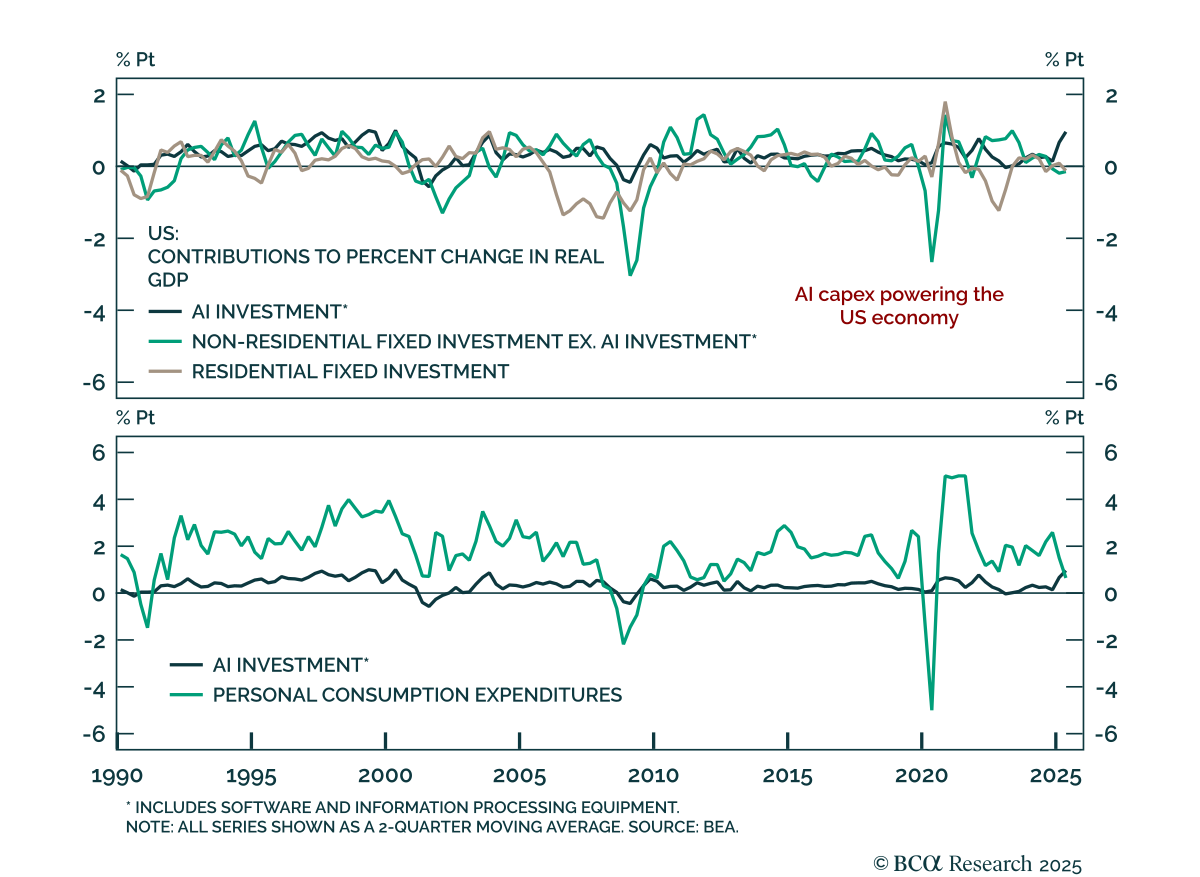

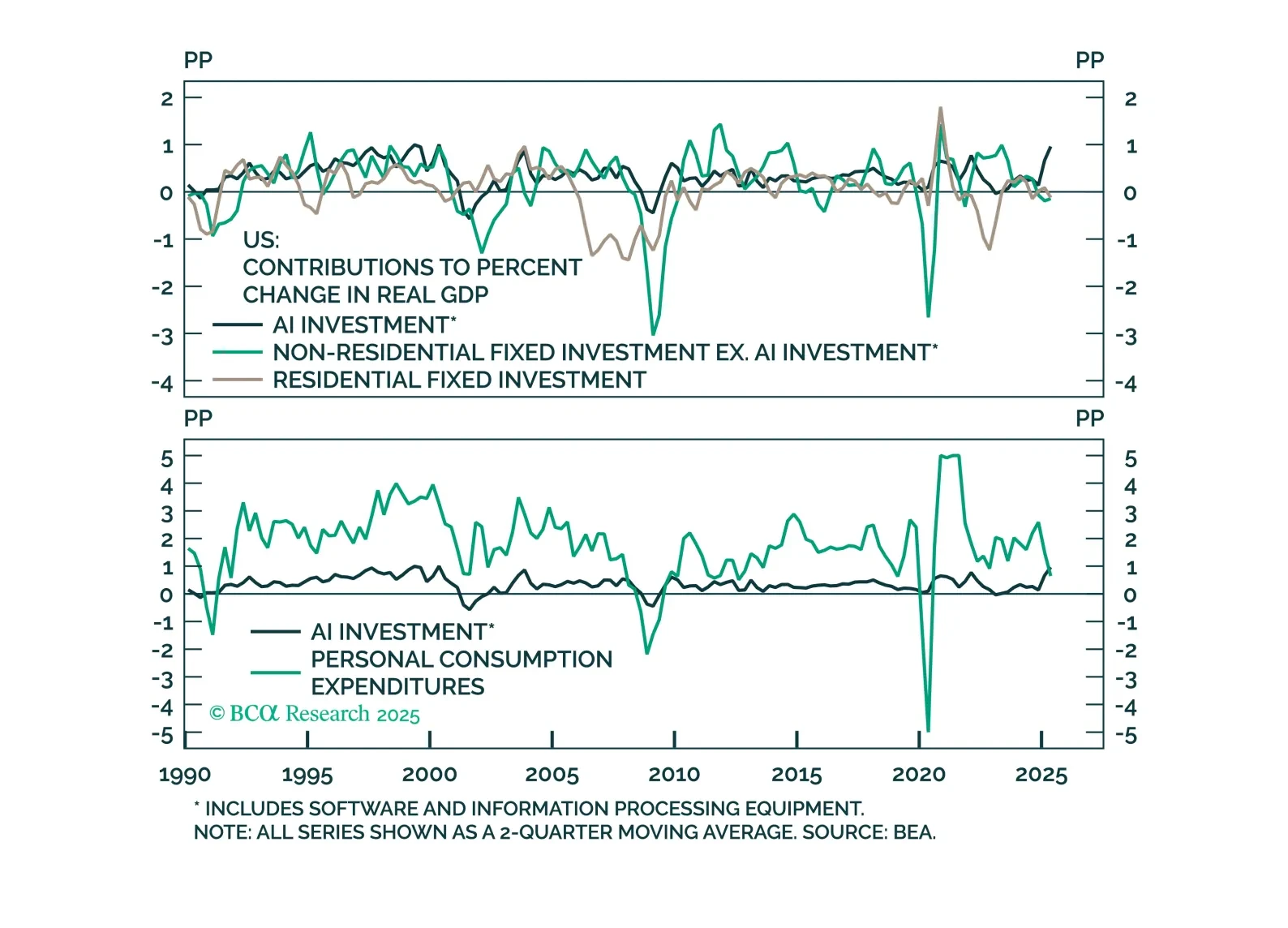

Over the first half of 2025, AI capex outpaced both consumption and all other investments in its contribution to US growth. Like all other capex cycles this one will end in tears. However, the indicators we track suggest that AI capex can continue supporting growth and markets for now. Remain Neutral on equities. Upgrade Health Care to Overweight and downgrade Consumer Staples to Neutral. Buy tail risk protection.

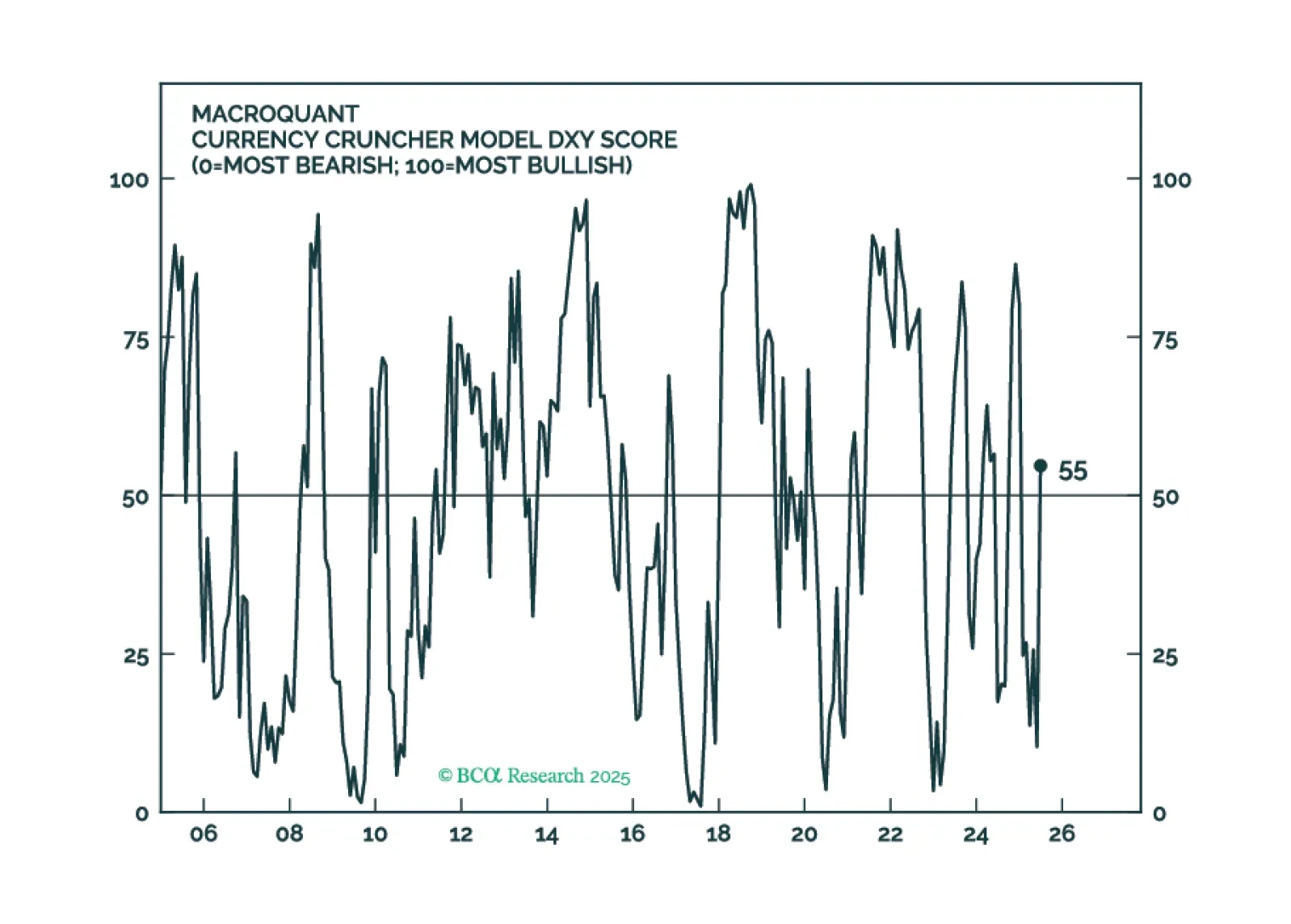

MacroQuant is recommending that equity investors keep their finger near the eject button but avoid pressing it for now. The model is warming up to the dollar again and sees scope for oil prices to rise.

Microsoft has gone up in a worryingly near-perfect straight line with dimension 1.098. Take August off before making a big commitment to stocks. Plus: a new tactical trade is to go long USD/HUF.

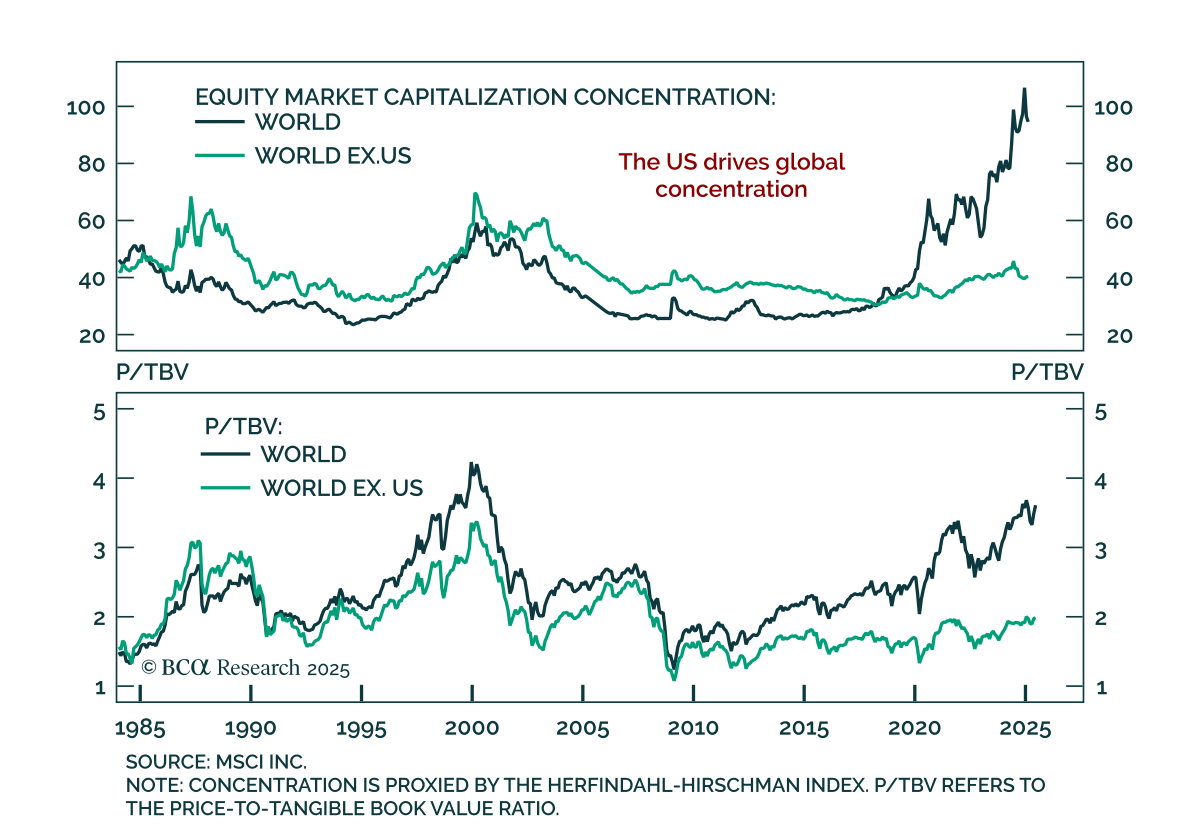

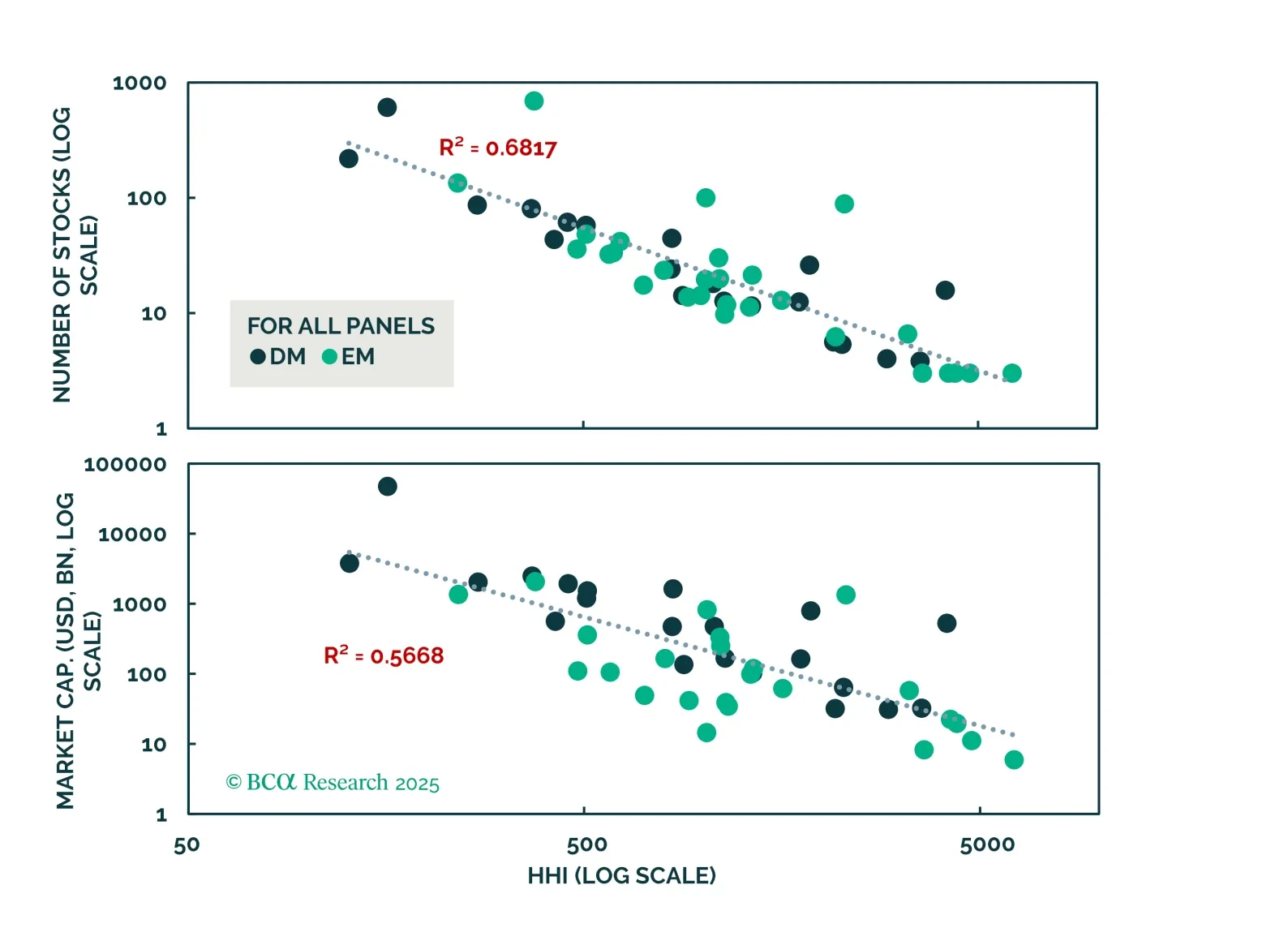

Using stock-level data for MSCI ACWI country indices going back to 1984 for Developed markets and 1988 for Emerging markets, we find that market concentration adds little predictive power for long term forward returns. Whatever predictive power it has disappears once we include traditional metrics like value and size. The same is true for idiosyncratic index risk. Index concentration is just not very important for determining risk and return in equity markets.