Equities

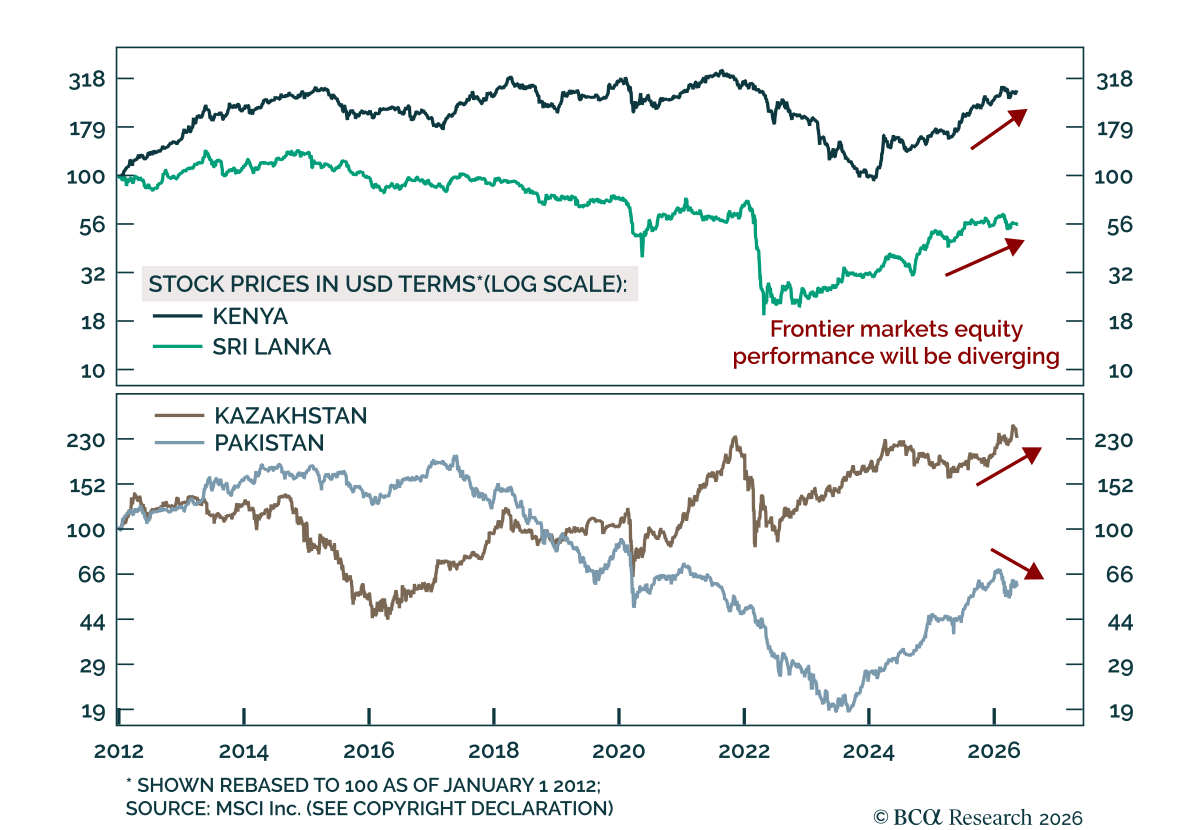

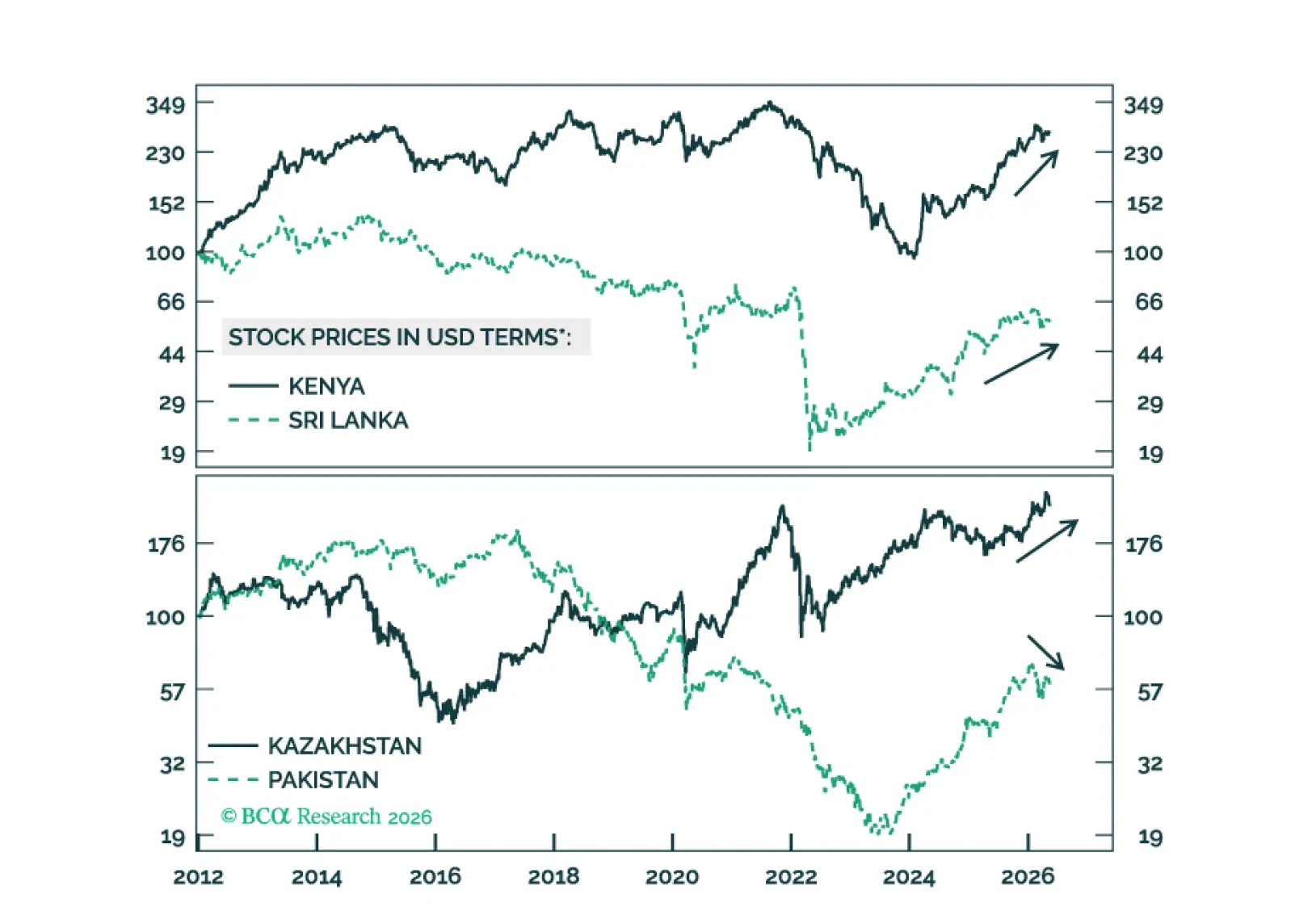

The divergence across frontier markets is likely to widen. Kenya, Kazakhstan, and Sri Lanka are well placed to outperform, while Pakistan is vulnerable. We offer several trade ideas to capture this divergence.

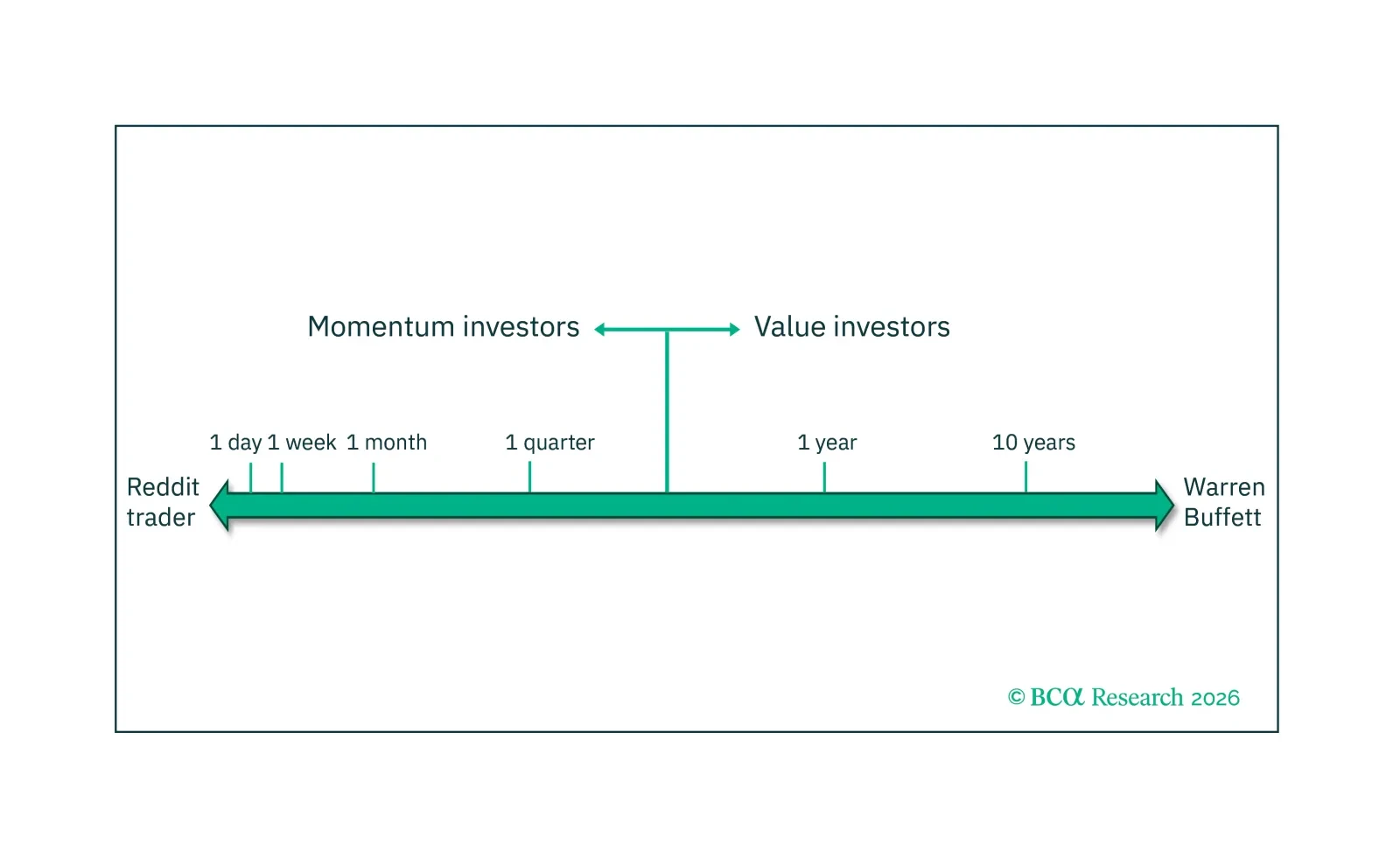

A market becomes inefficient, illiquid, and vulnerable to a phase transition when the ‘wisdom of crowds’ switches to the ‘madness of crowds.’ This switch from market wisdom to market madness may be the most significant recurring behavioural opportunity in active fund management and can be exploited in real-time by measuring the market’s complexity.

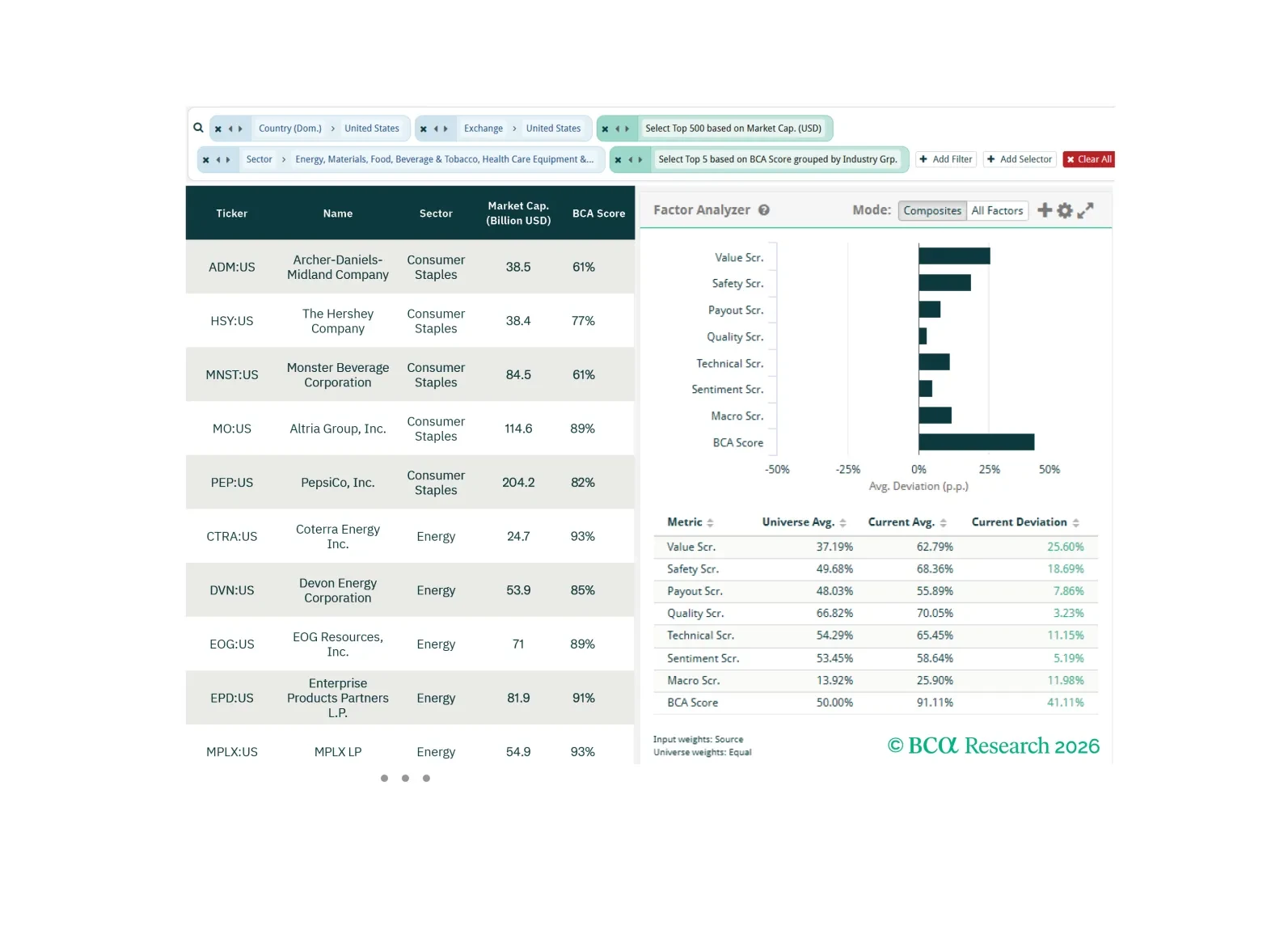

In this screener report, we explore opportunities in Inflation risk, supply-constrained Information Technology stocks, and old-economy cyclicals.

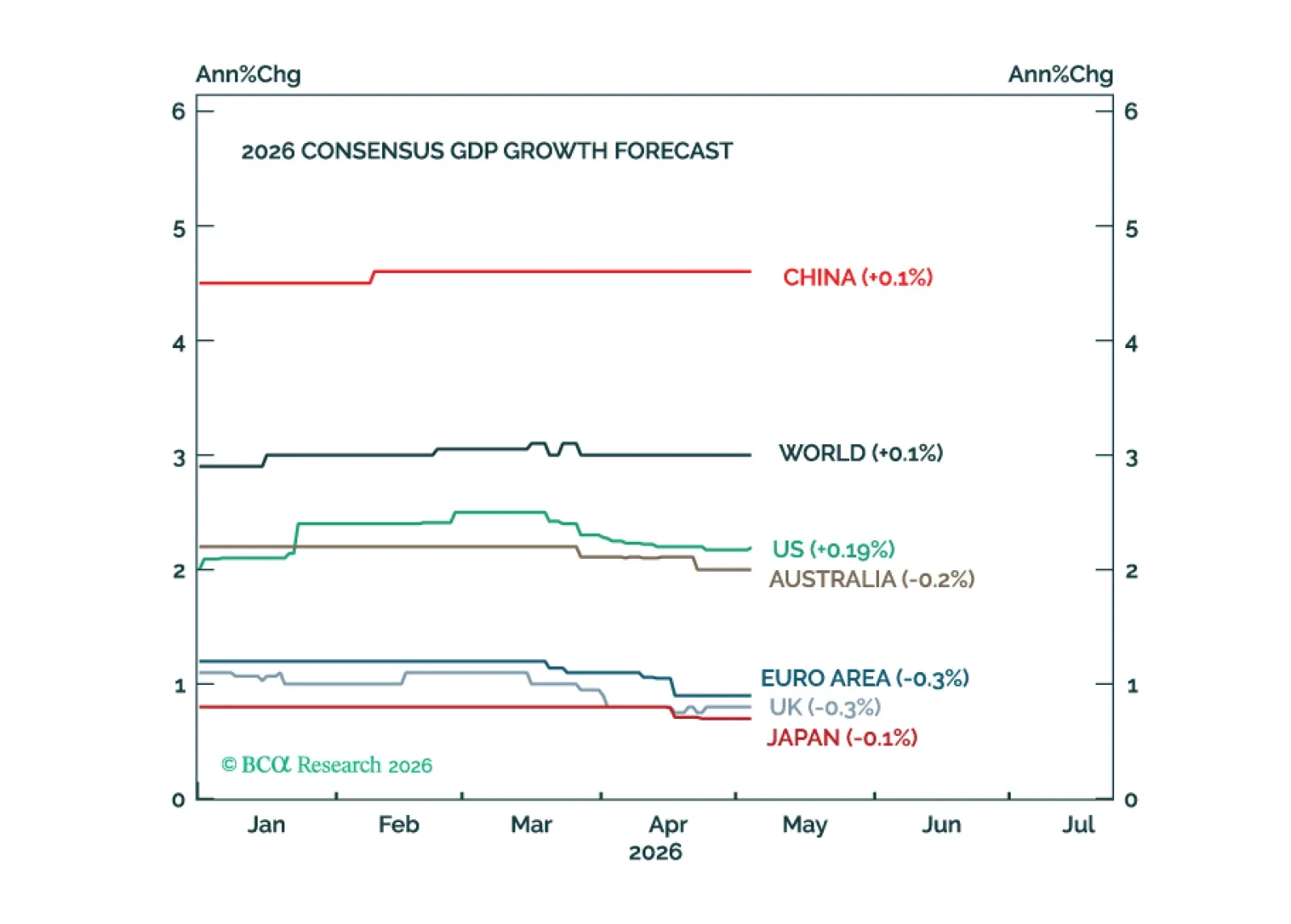

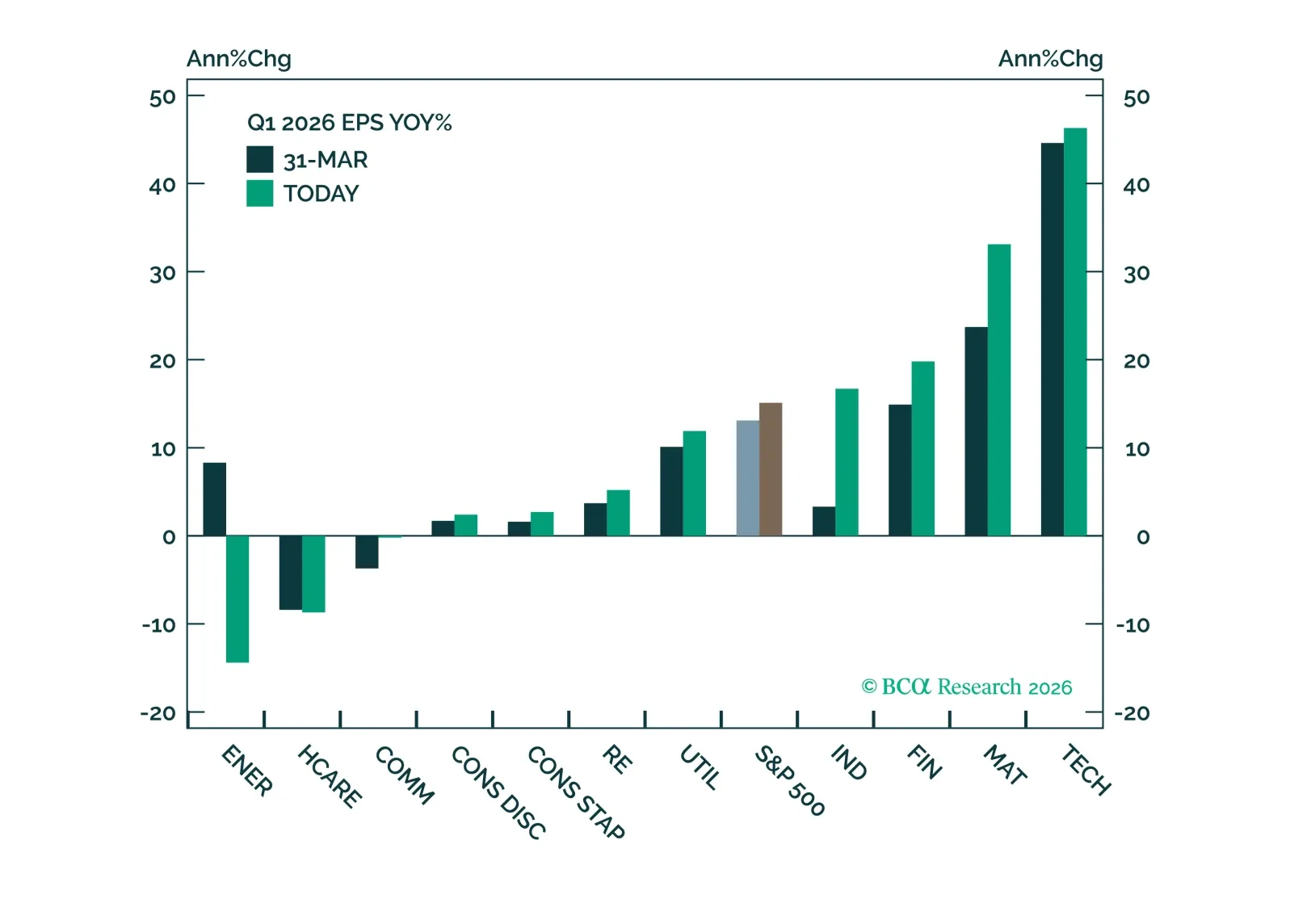

The investment cycle remains firmly intact, driving equity prices and fundamentals, as confirmed by both Q1 data and corporate commentary. Upside surprises, expanding margins, and rising capex expectations point to resilient demand. Companies confirm that AI-related demand is broad and visible, while geopolitical and credit risks remain contained and not yet systemic.

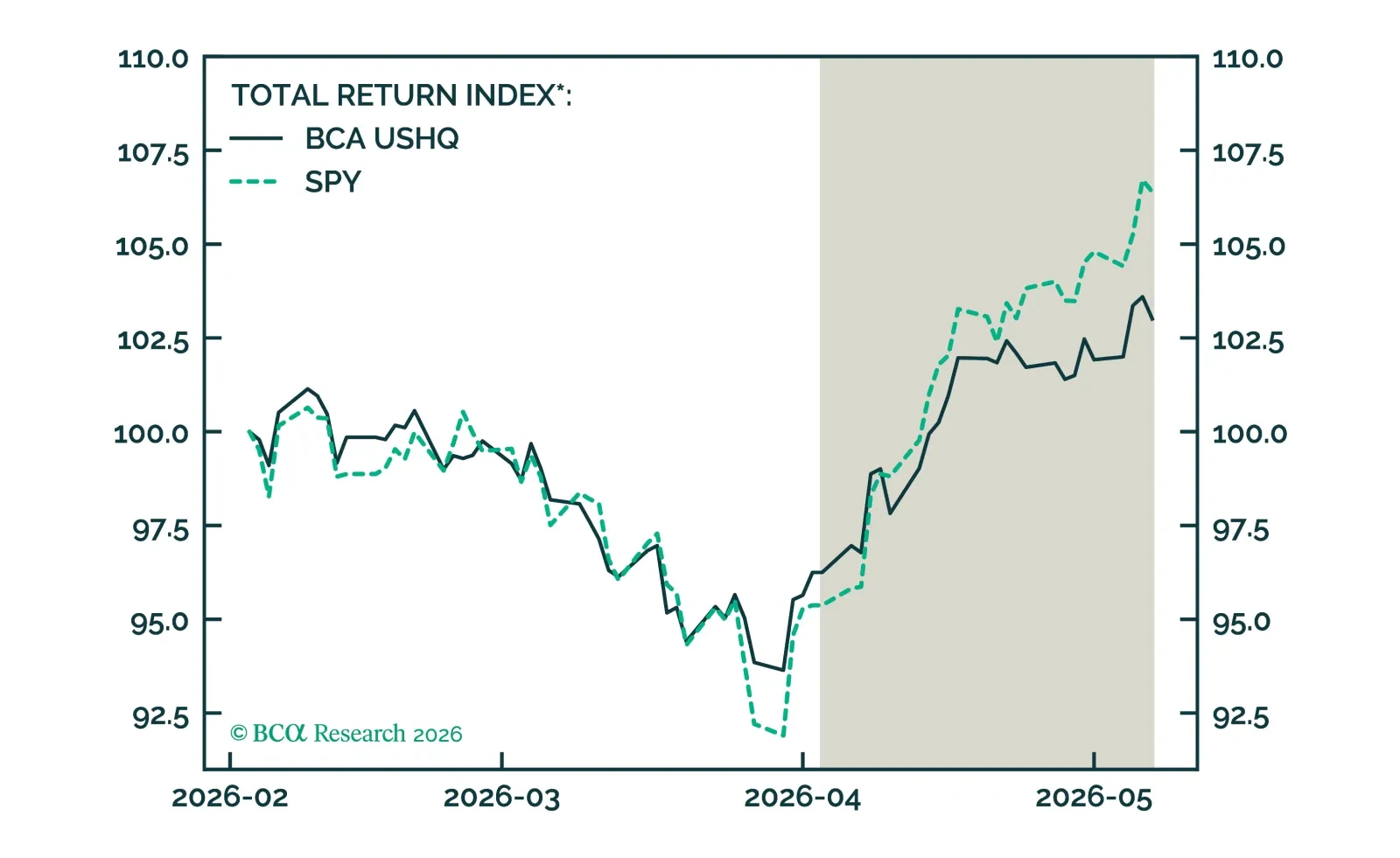

The US High Quality (USHQ) portfolio underperformed its benchmark through April, returning 7.02%, while its SPY benchmark returned 11.55%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark as well, with USHQ underperforming by approx. 338bps.

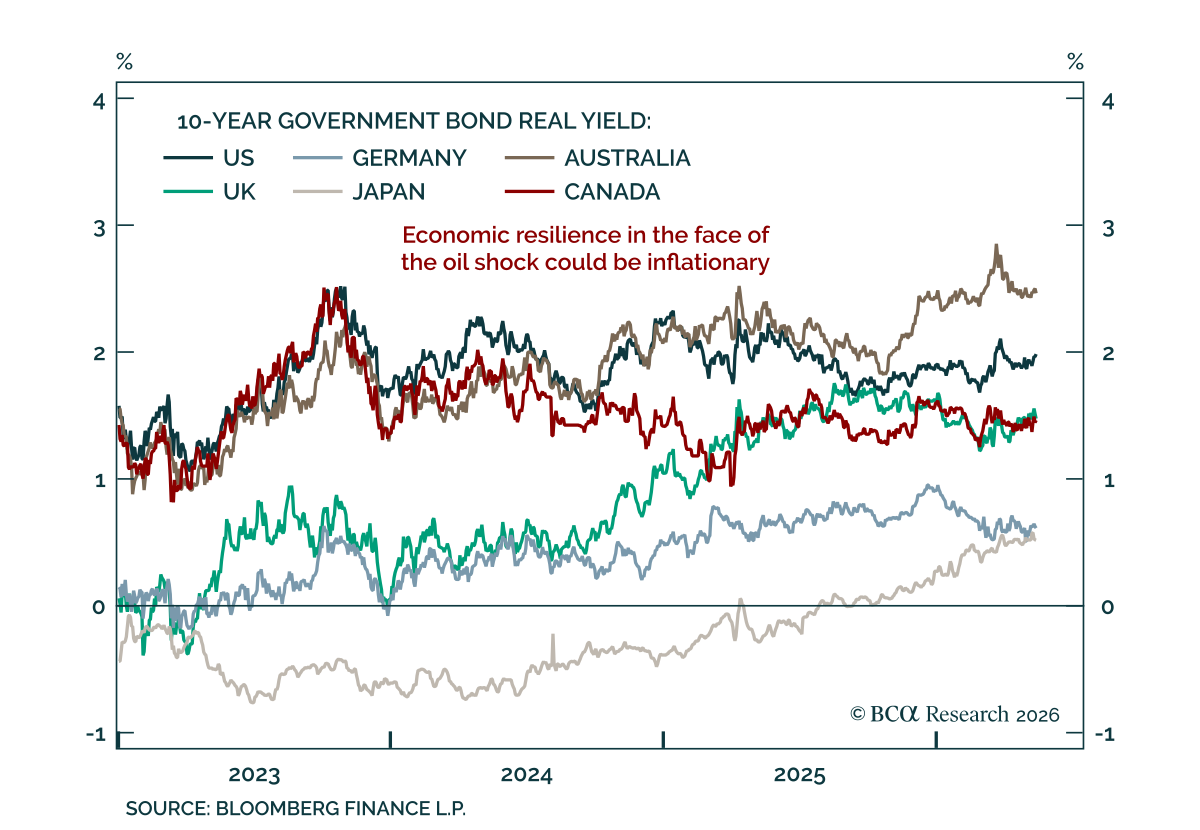

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

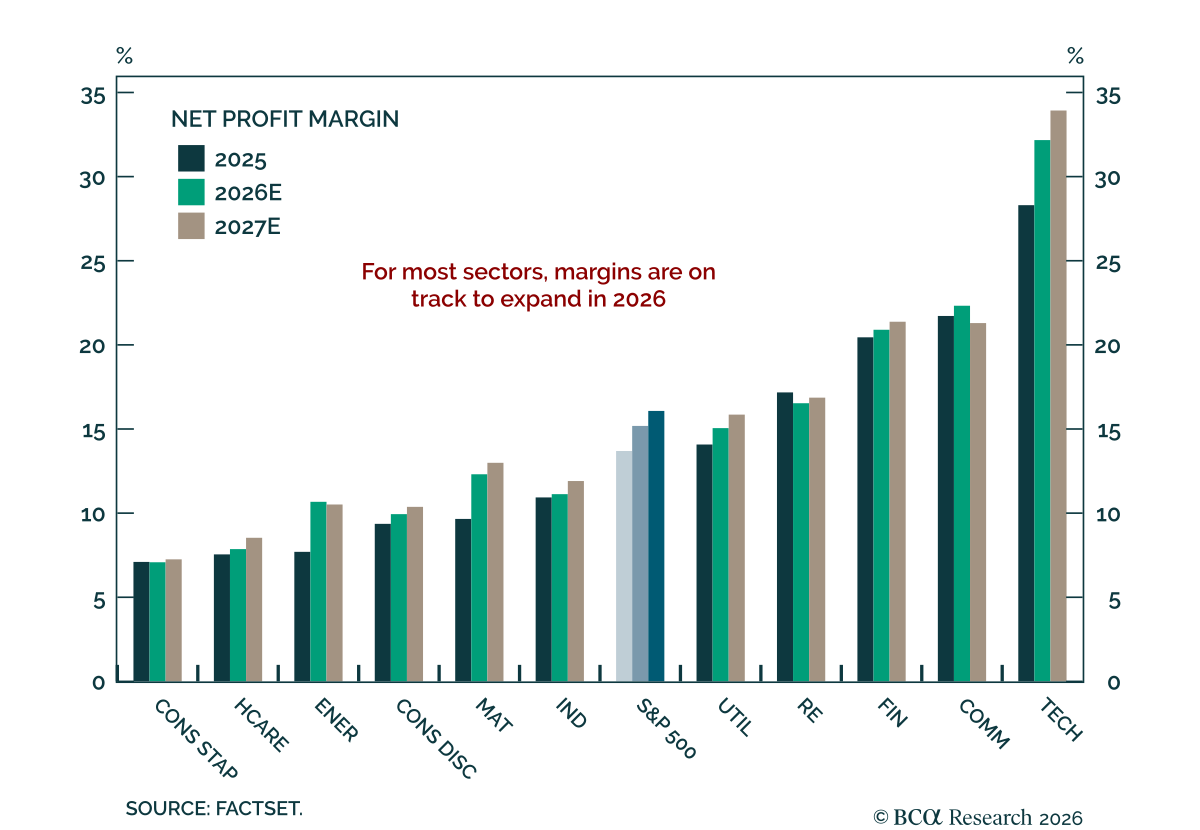

Leadership has rotated toward investment-driven sectors, reflected in both EPS growth and price performance. Expanding margins suggest the cycle may have longer to run, as productivity gains start to work their way through fundamentals. We continue to see upside for the S&P 500, with no change to our sector outlook.