Equities

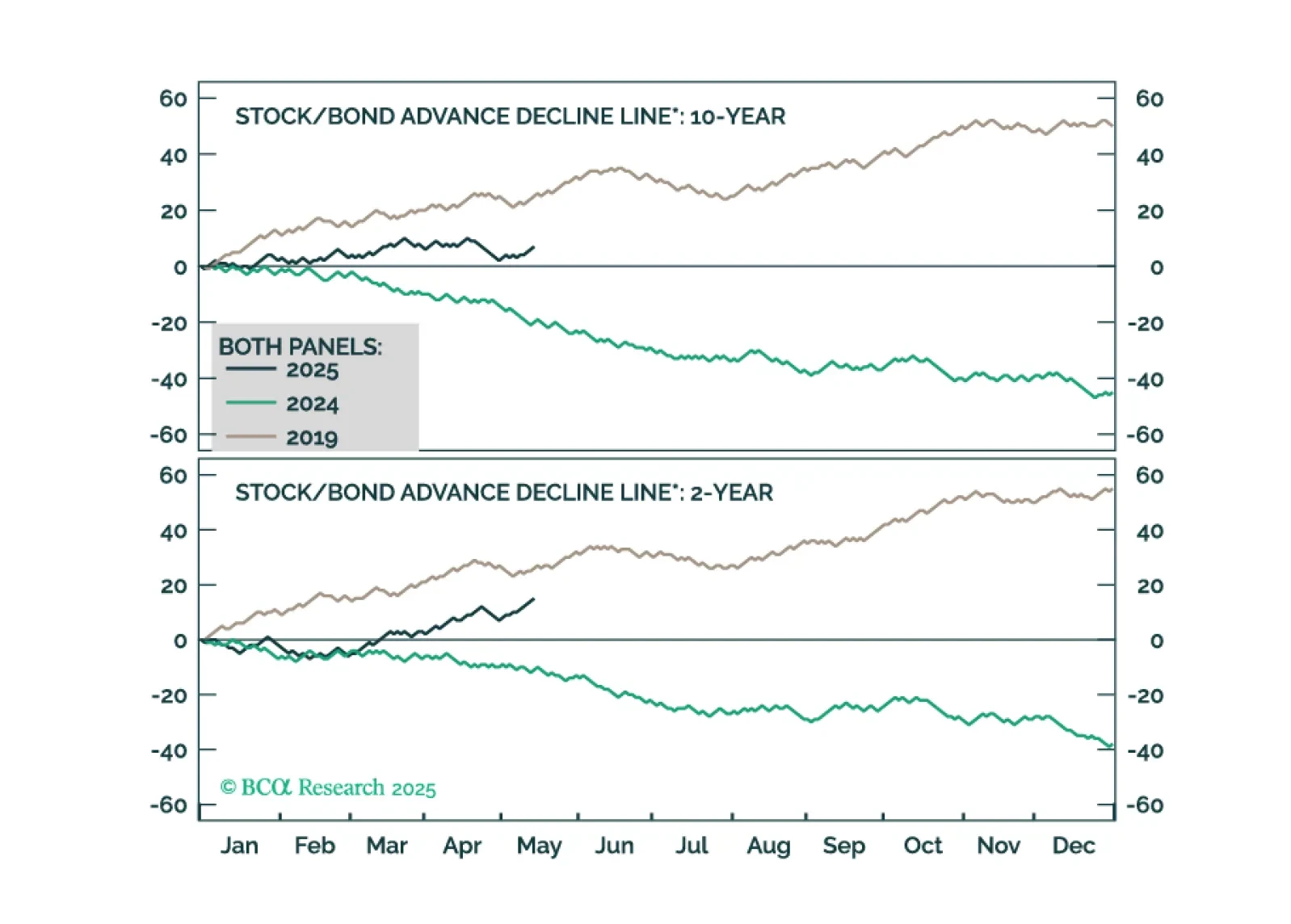

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.

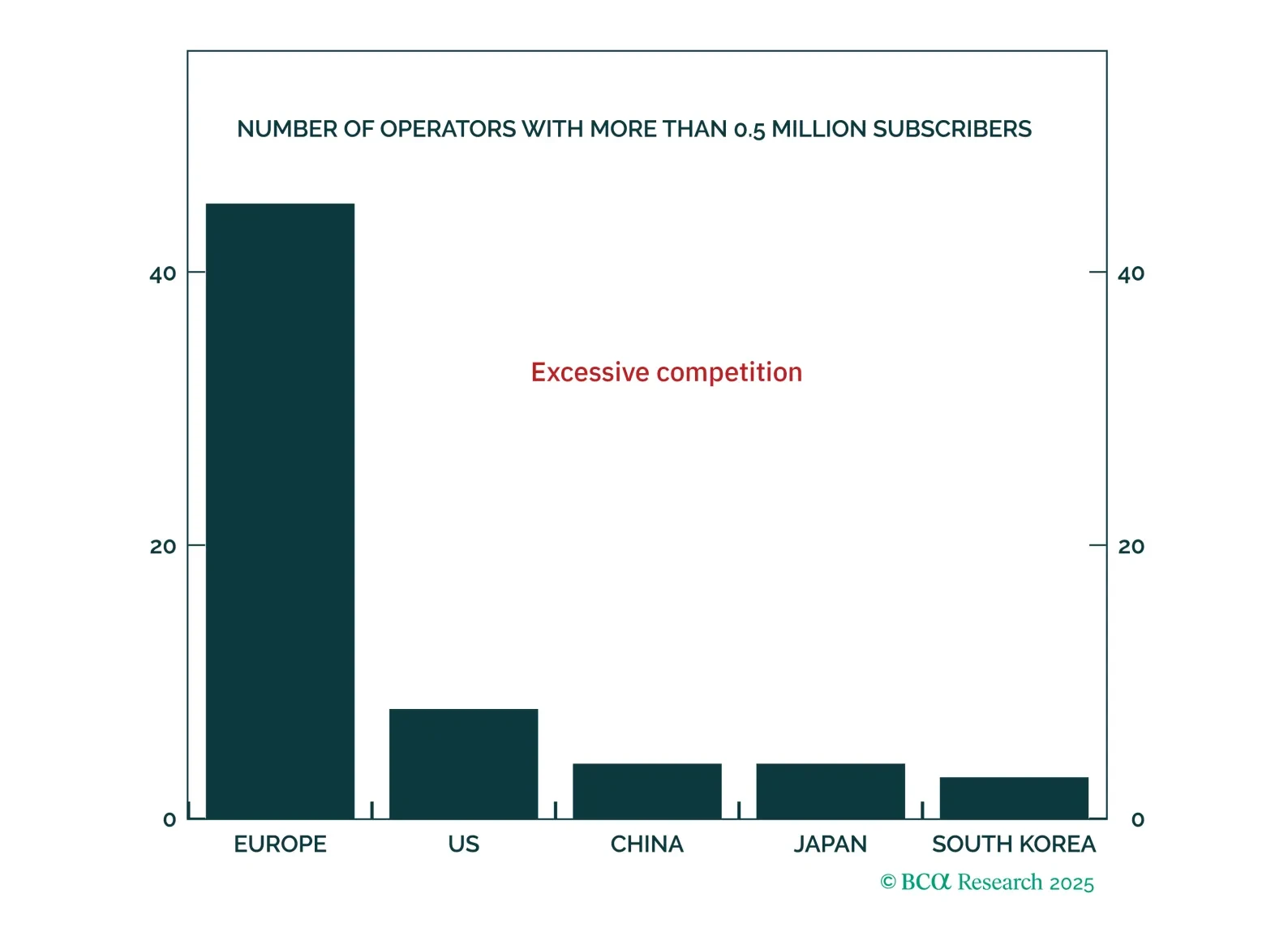

Europe’s telecoms are cheap just as Brussels moves to tear down barriers and spark cross border consolidation. Read why this blend of high yield, defensive earnings, and a powerful policy catalyst sets the stage for a major sector re rating.

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.

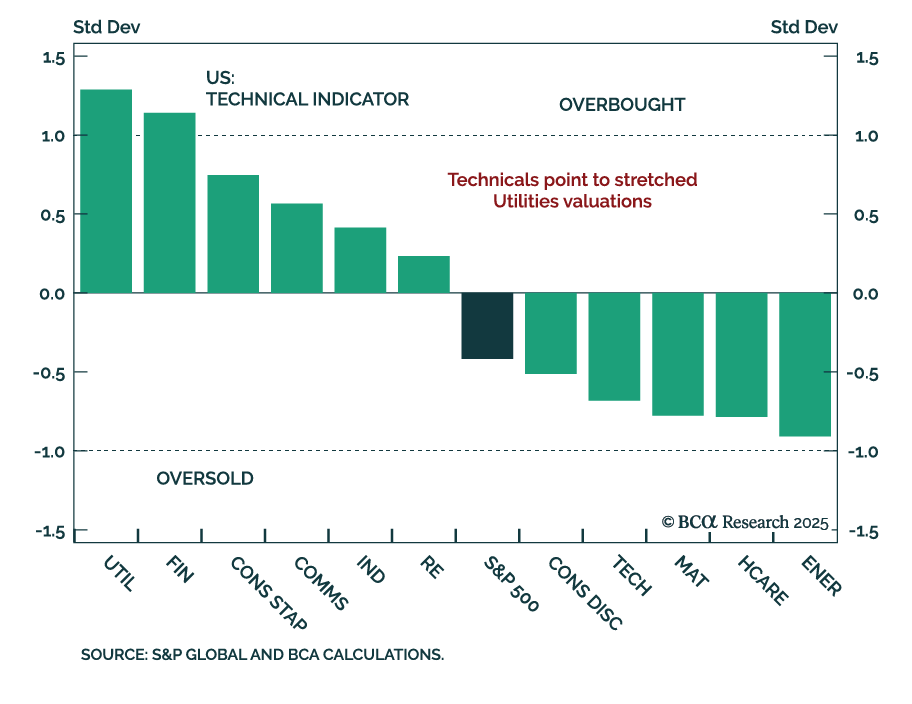

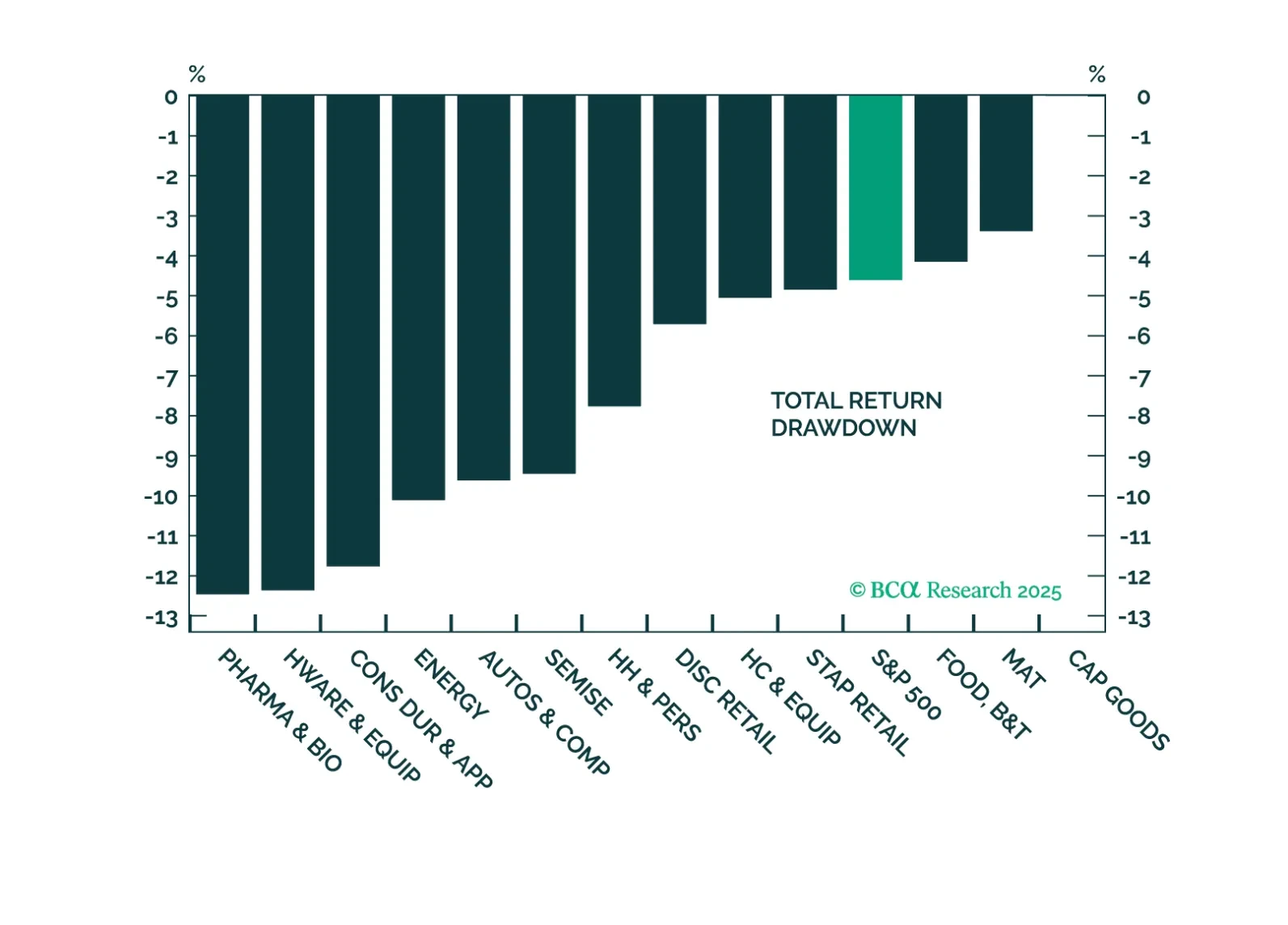

Markets are pricing out the worst trade policy fears, and while tariffs will still dent earnings, the impact looks smaller than initially feared. With sector rotation gaining traction and oversold names rebounding, we are adjusting our portfolio to reflect the rotation thesis.

A weakening economy will apply downward pressure to Treasury yields, but the Trump term premium will keep long-dated yields higher than they would otherwise be. This makes Treasury curve steepeners the most attractive trade in US fixed income.