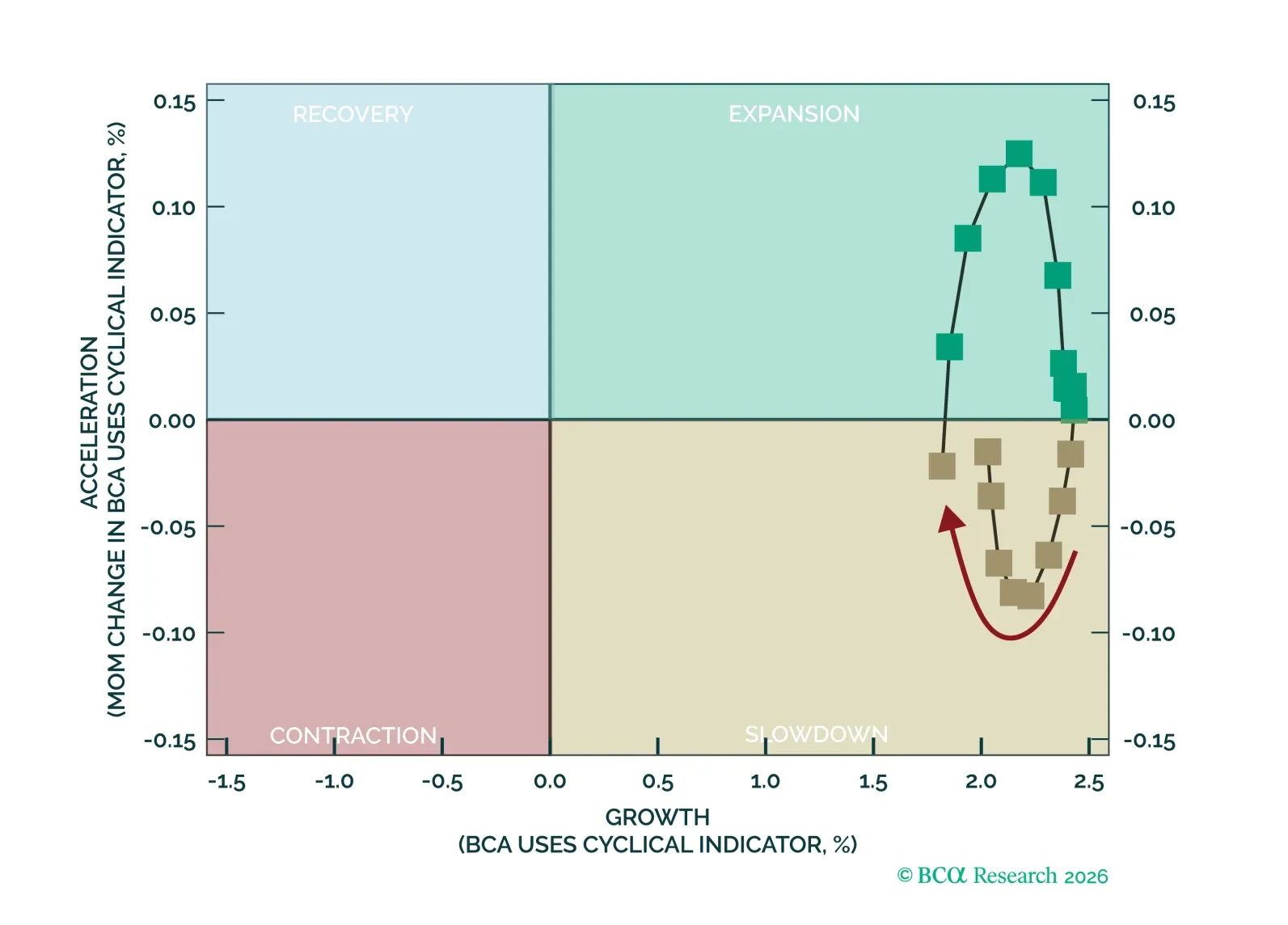

Equities

The S&P 500 rally is likely more than just risk-relief. Market internals reflect strengthening economic growth and higher inflation, with support coming from robust earnings. Tight financial conditions have compressed valuations, particularly within the Tech sector. We are initiating a long Software trade ahead of earnings season, given that multiples have declined and earnings growth is strong.

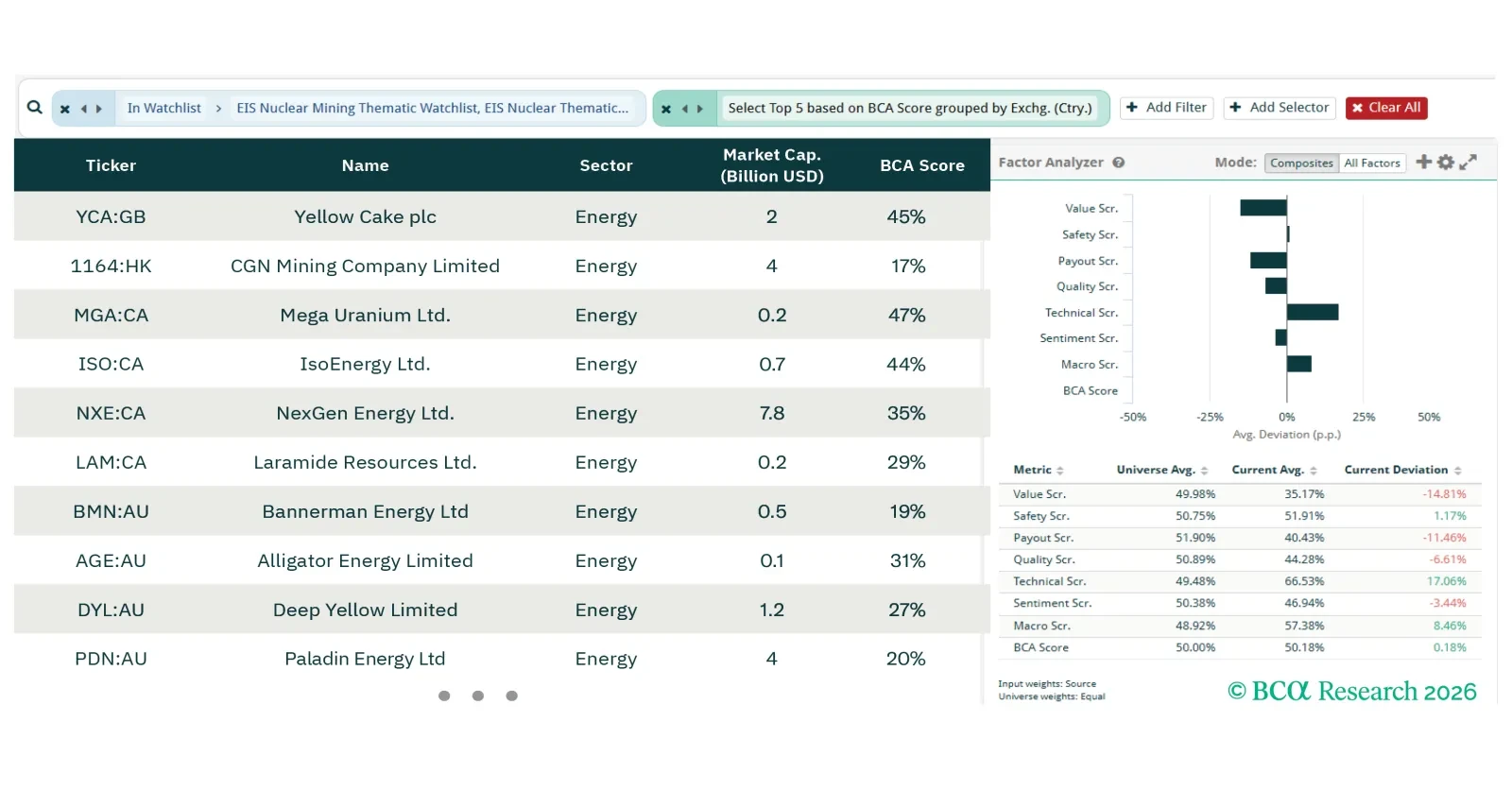

In this screener report, we explore opportunities in nuclear theme, geopolitical hedge, and winners from AI productivity boom.

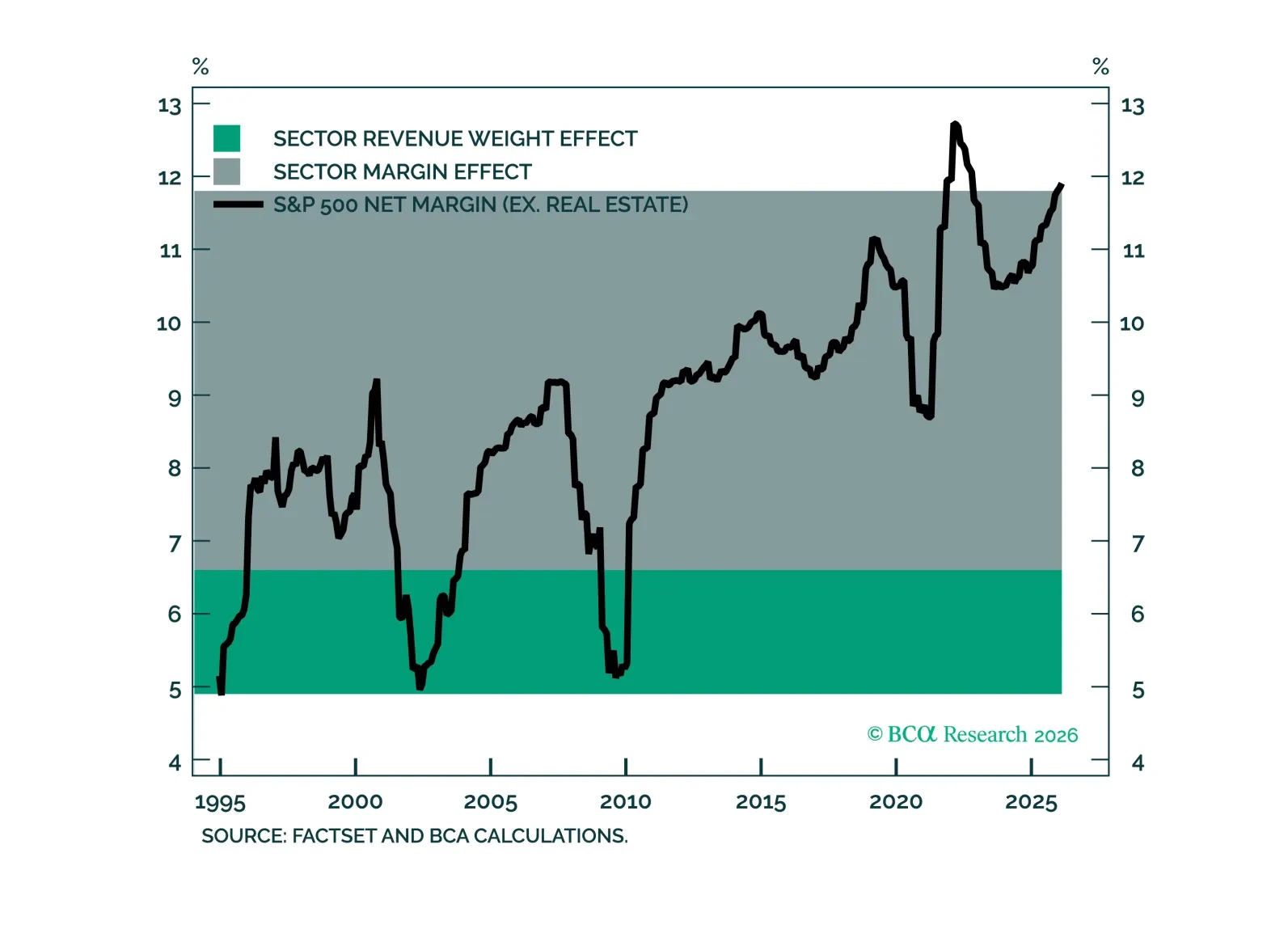

The long-run rise in S&P 500 margins reflects more than a shift toward higher-margin sectors. Most of the increase has come from higher profitability within sectors, supported by favorable mix of macro forces. Looking ahead, many of those tailwinds are likely to fade, with AI-driven productivity gains as a potential offsetting upside driver of margins.

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.

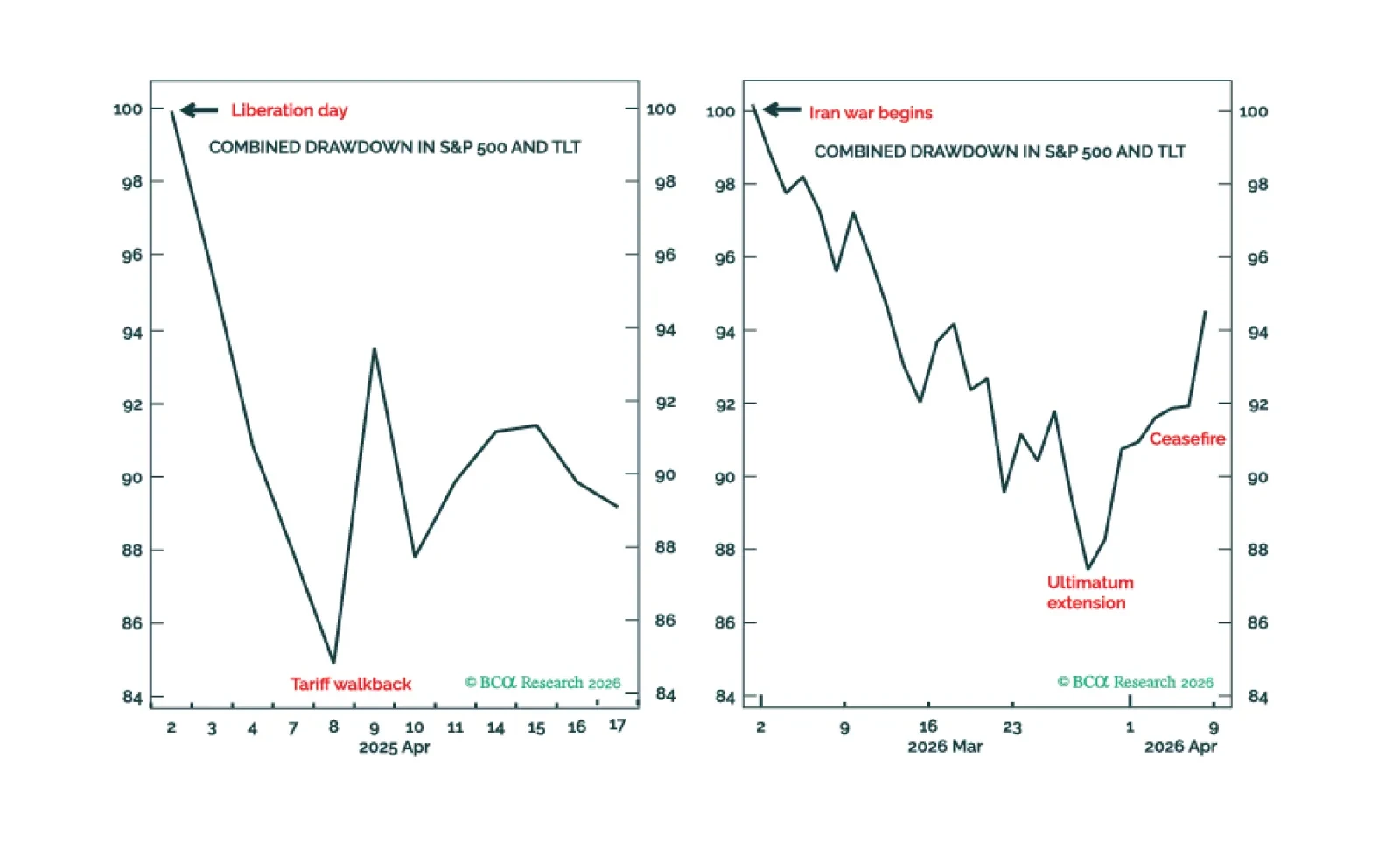

Trump’s breaking point is encapsulated by the combined drawdown in stocks plus bonds reaching 12-15 percent. On this basis, we describe how to ‘trade Trump’. Plus, we highlight three positions that should do well independent of Trump’s actions, including a new trade.

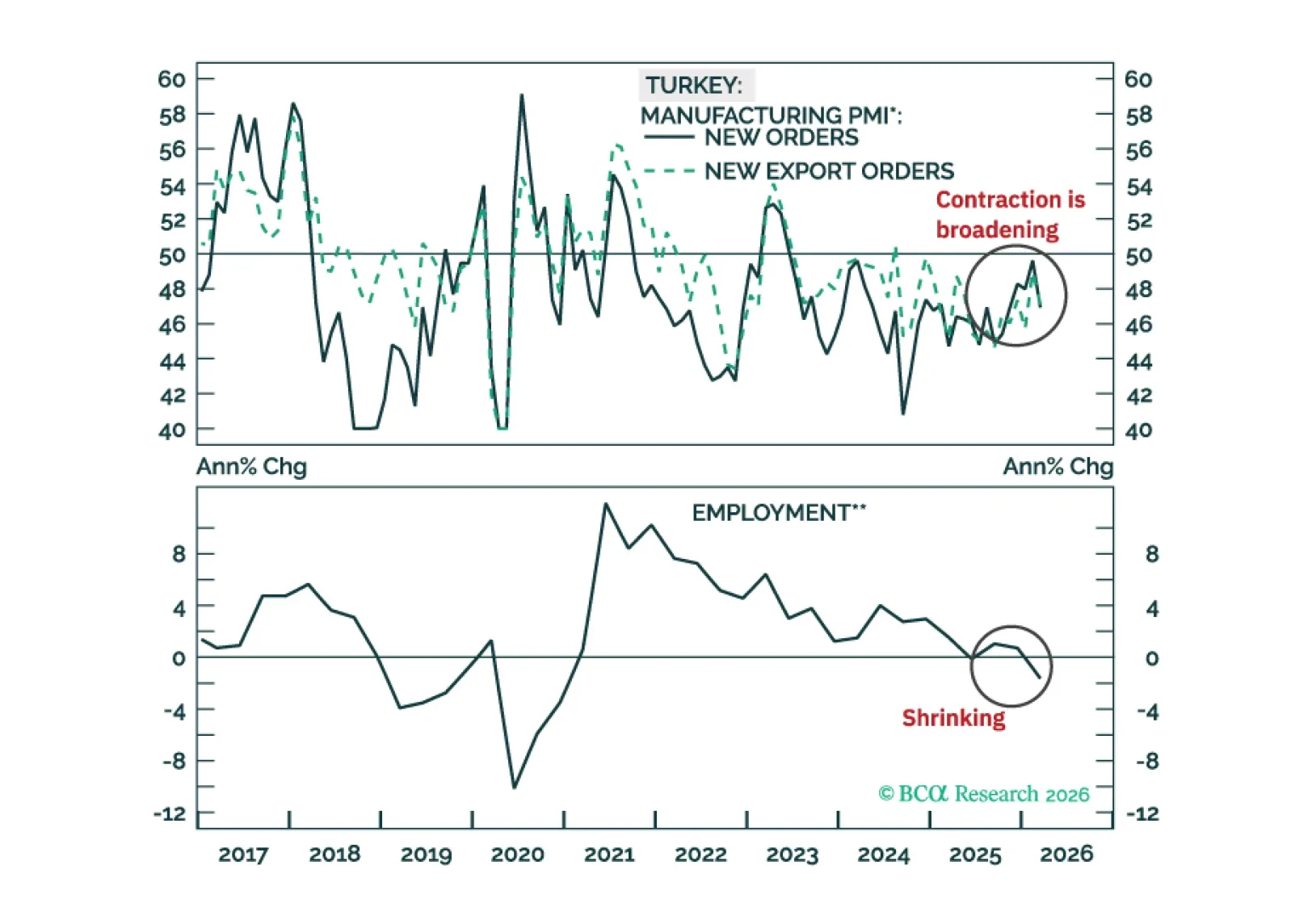

The Turkish financial markets will struggle in the very near term, but beyond that, the cyclical disinflation process will resume. Fixed-income investors should put Turkish 2-year local currencybonds on a ‘buy’ watch list.

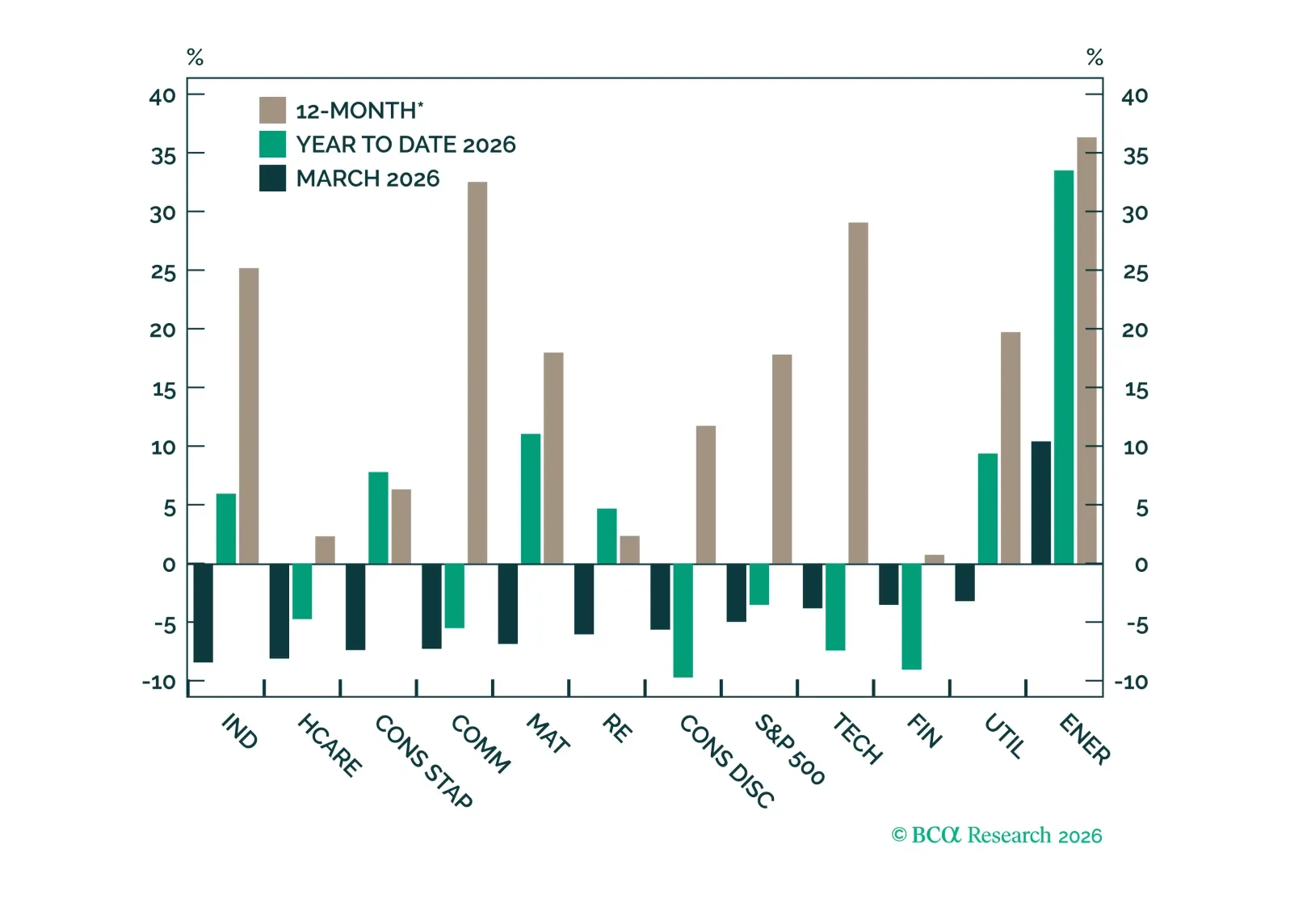

We expect the S&P 500 to deliver $308 of EPS in 2026, with a year-end target of 7700. Revenue growth drives upside, with little margin or multiple expansion. With economic growth tilted toward investment, we are overweight Technology, Industrials, and Materials, market-weight Financials, Energy, Health Care, Communication Services, and Real Estate, and underweight Consumer Staples, Consumer Discretionary, and Utilities.

While the Middle East conflict’s inflationary impact is likely to persist, US recession risk is contained whereas non-US recession risk is more elevated. We discuss what this means for investment strategy. Plus, a new tactical trade is to underweight Utilities.

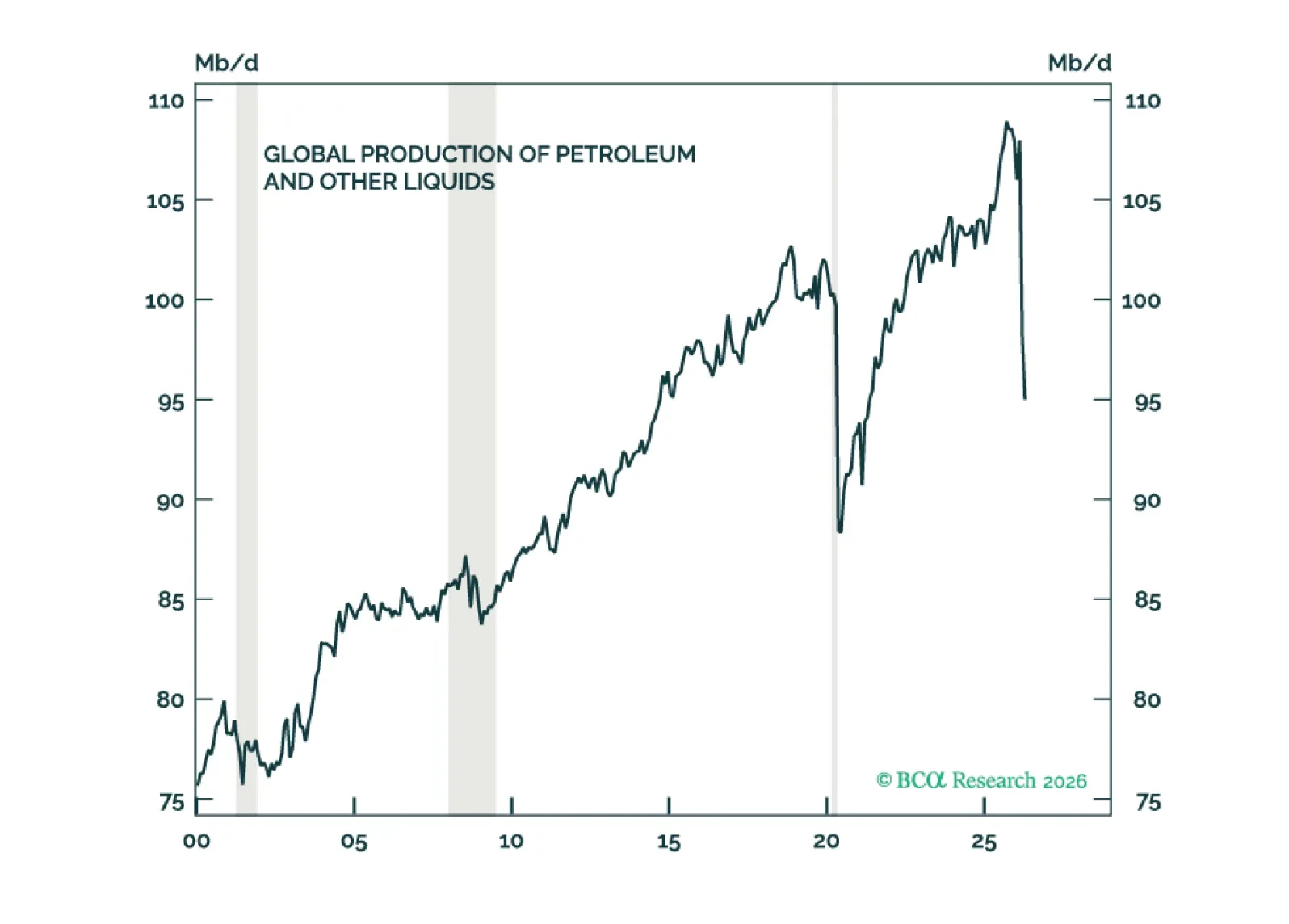

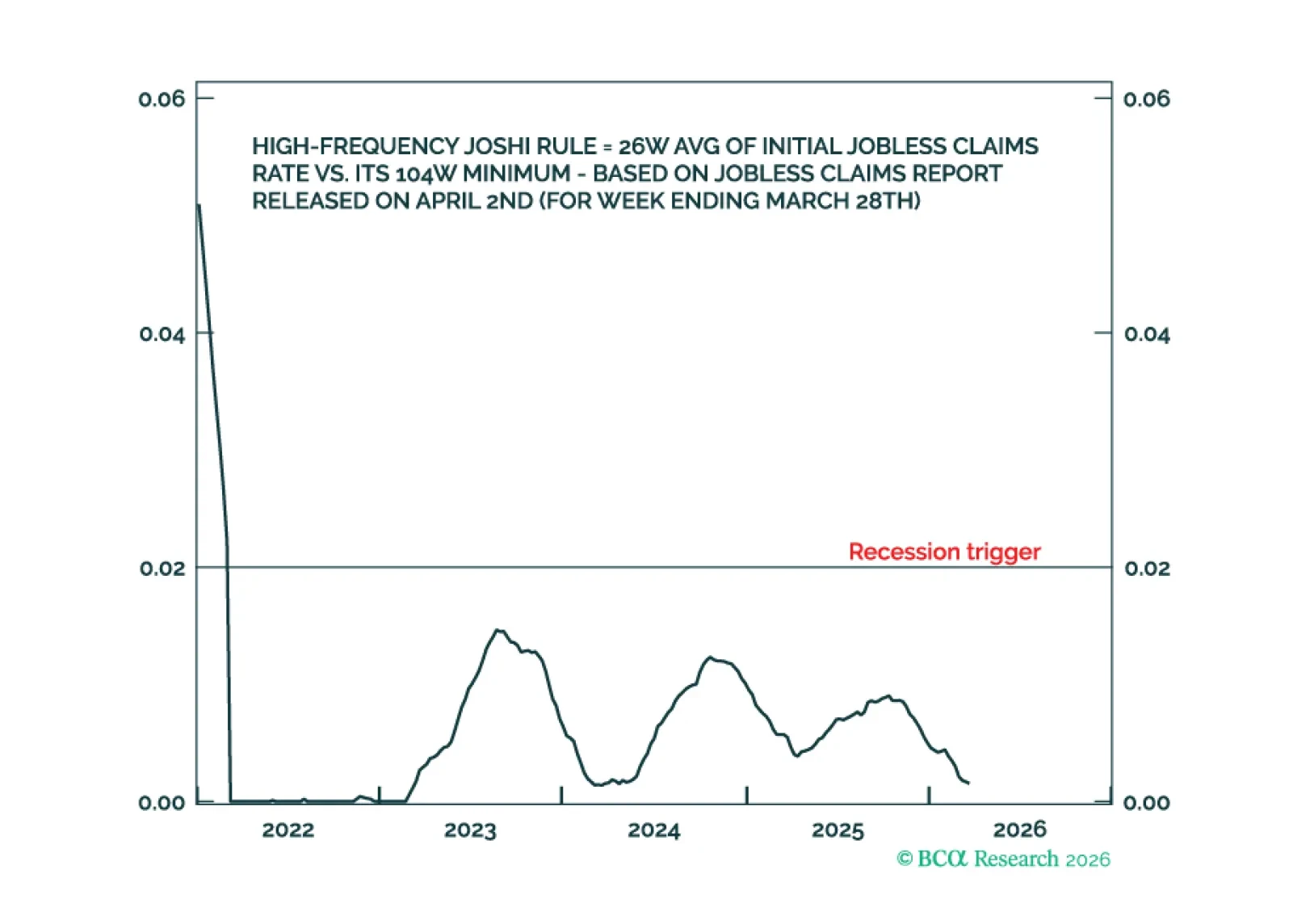

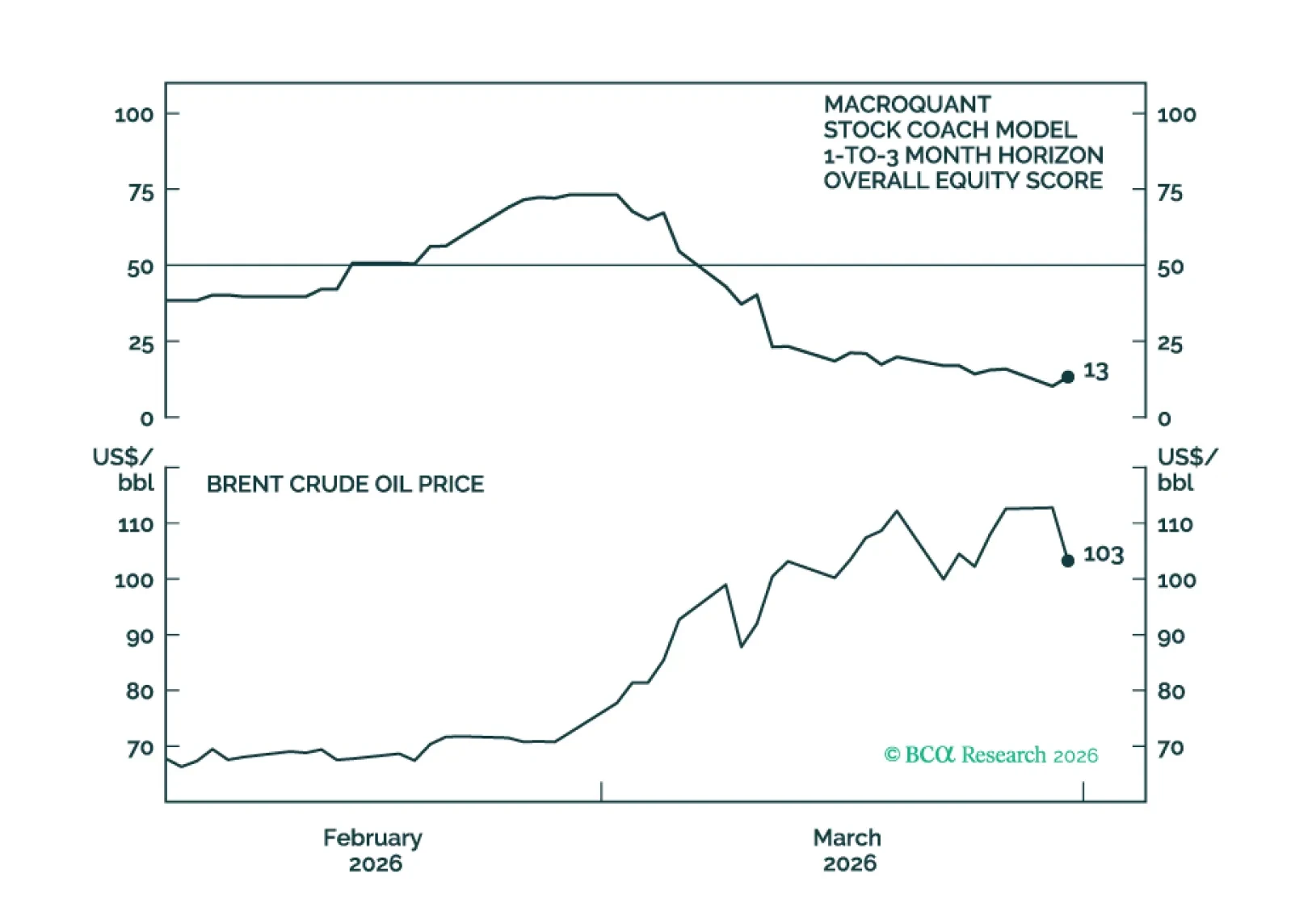

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.

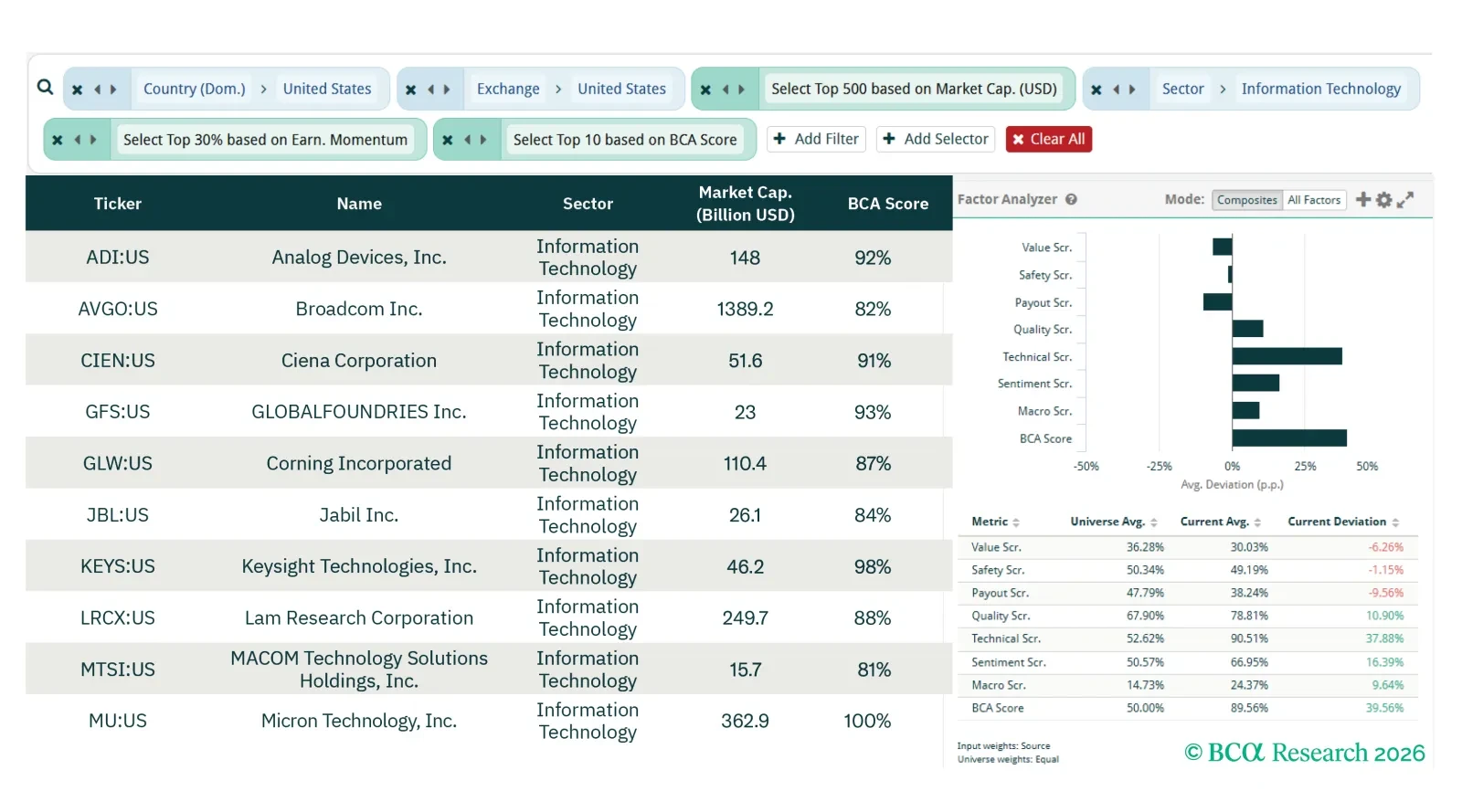

This screener report builds on the US Equity Strategy team's sector view published on 30 March 2026, where the team overweights Information Technology, Industrials, and Materials on a 3- to 12-month horizon. Here we utilize our screening tools to layer bottom-up stock selection onto their top-down sector views.