Equities

Iran doesn’t need to sink a single US warship; it could inflict much more damage by sinking the US stock and bond markets by disrupting shipping, trade, and oil tankers with decentralised low-tech drone warfare. We discuss why it is not the direct pain of higher oil prices, but the knock-on repercussions for stock and bond markets that could inflict the greater damage. Plus, a new tactical trade is to underweight Materials.

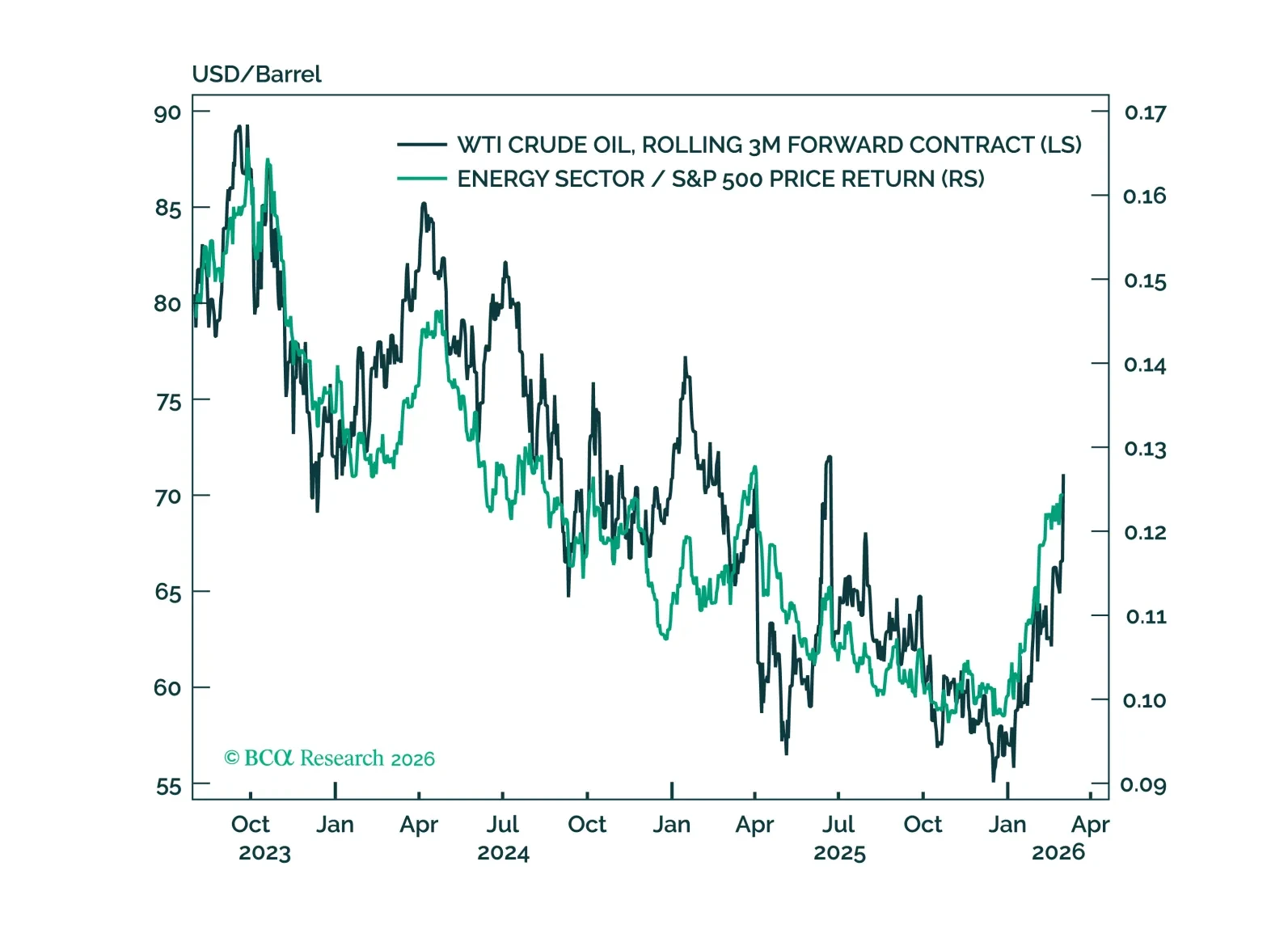

Middle East hostilities have triggered risk-off moves and pushed oil prices higher. Previous geopolitically driven oil price disruptions suggest that speed, persistence and equity market vulnerability relate to the degree of the market sell off. At the other end of the spectrum, energy stocks should benefit, but have already rallied significantly.

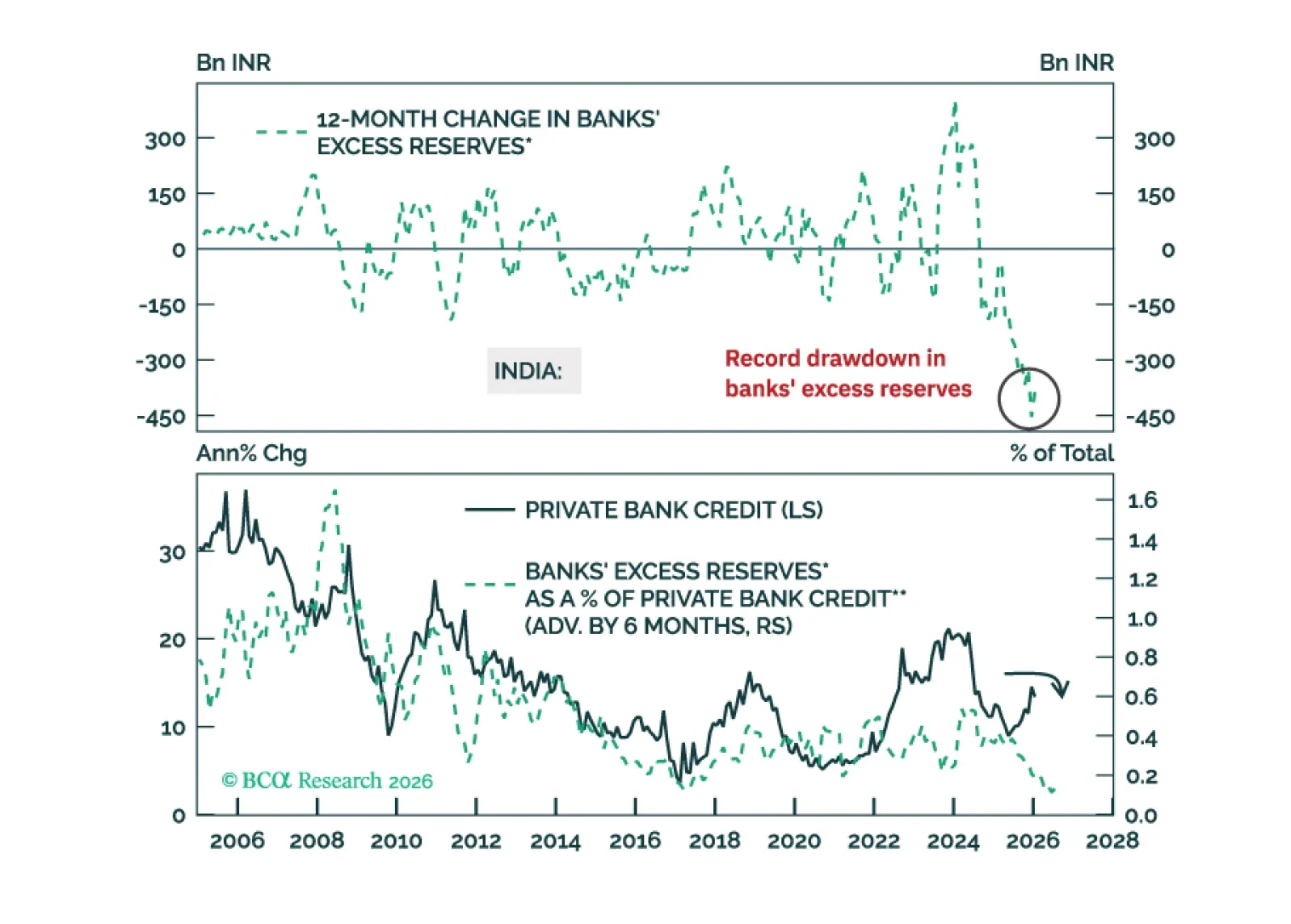

India is seeing net capital outflows for the first time in a generation. The central bank is selling foreign reserves to defend the rupee, which is draining banking system liquidity. The latter risks derailing the nascent credit revival. Indian stock prices remain vulnerable.

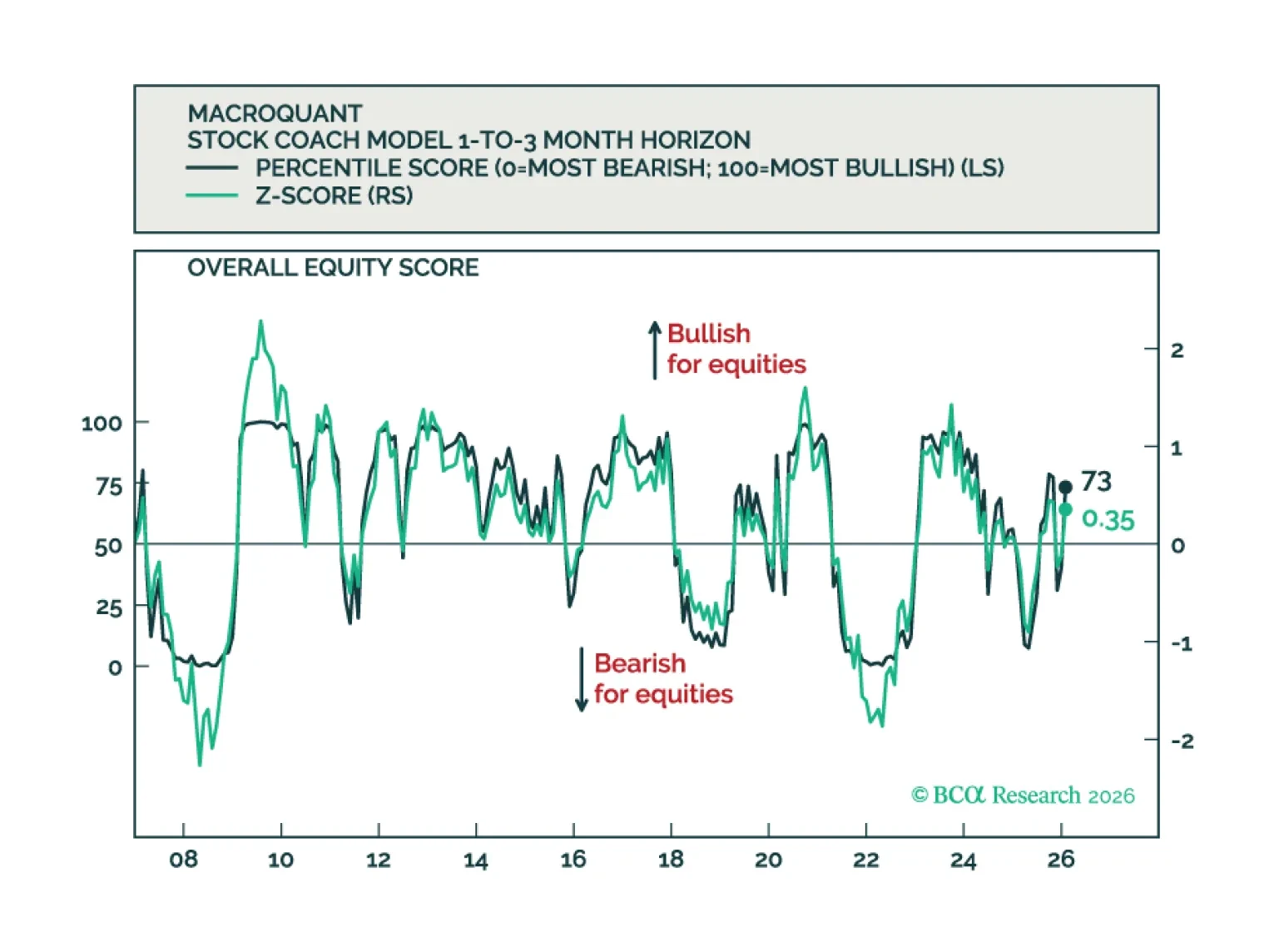

MacroQuant recommends a modest overweight position in equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has downgraded oil to neutral, and is bullish on copper and gold.

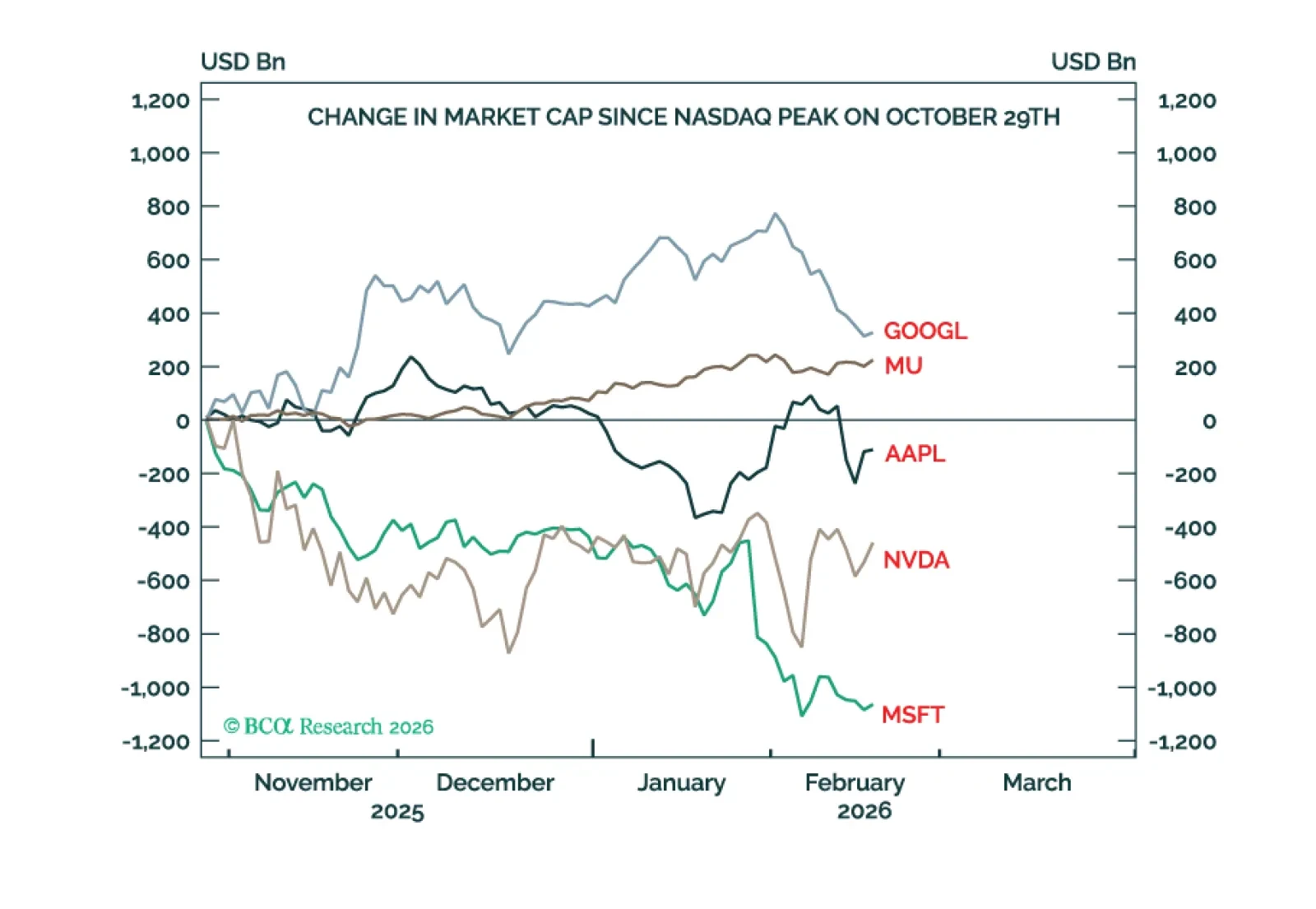

Tech has starkly underperformed other equity sectors and the tech-heavy US market has underperformed non-US markets, but global stocks are up and have comfortably outperformed bonds. This pattern of performances is likely to continue through the rest of 2026. Plus, two new tactical trades are: long coffee; and long ETH.

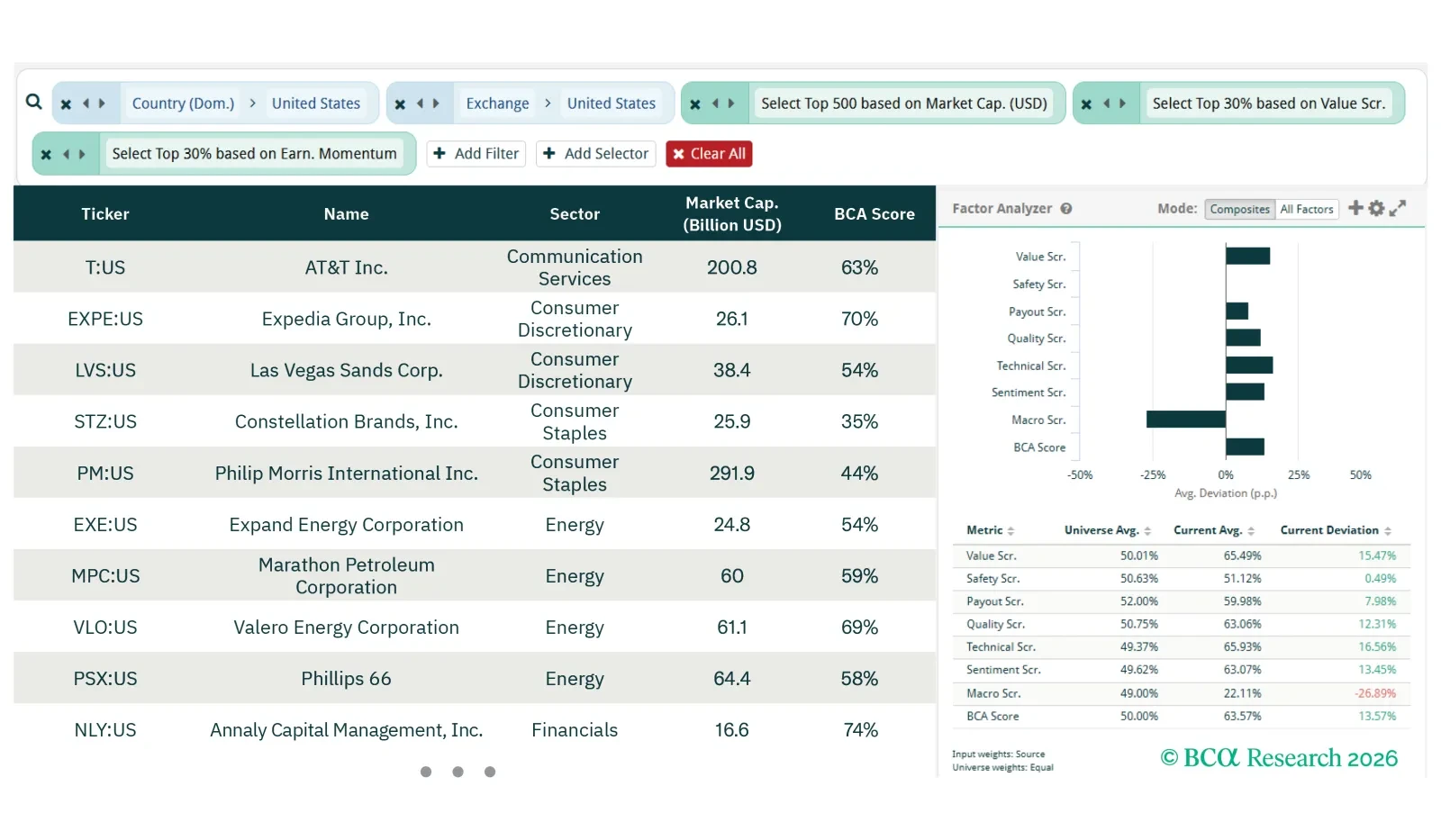

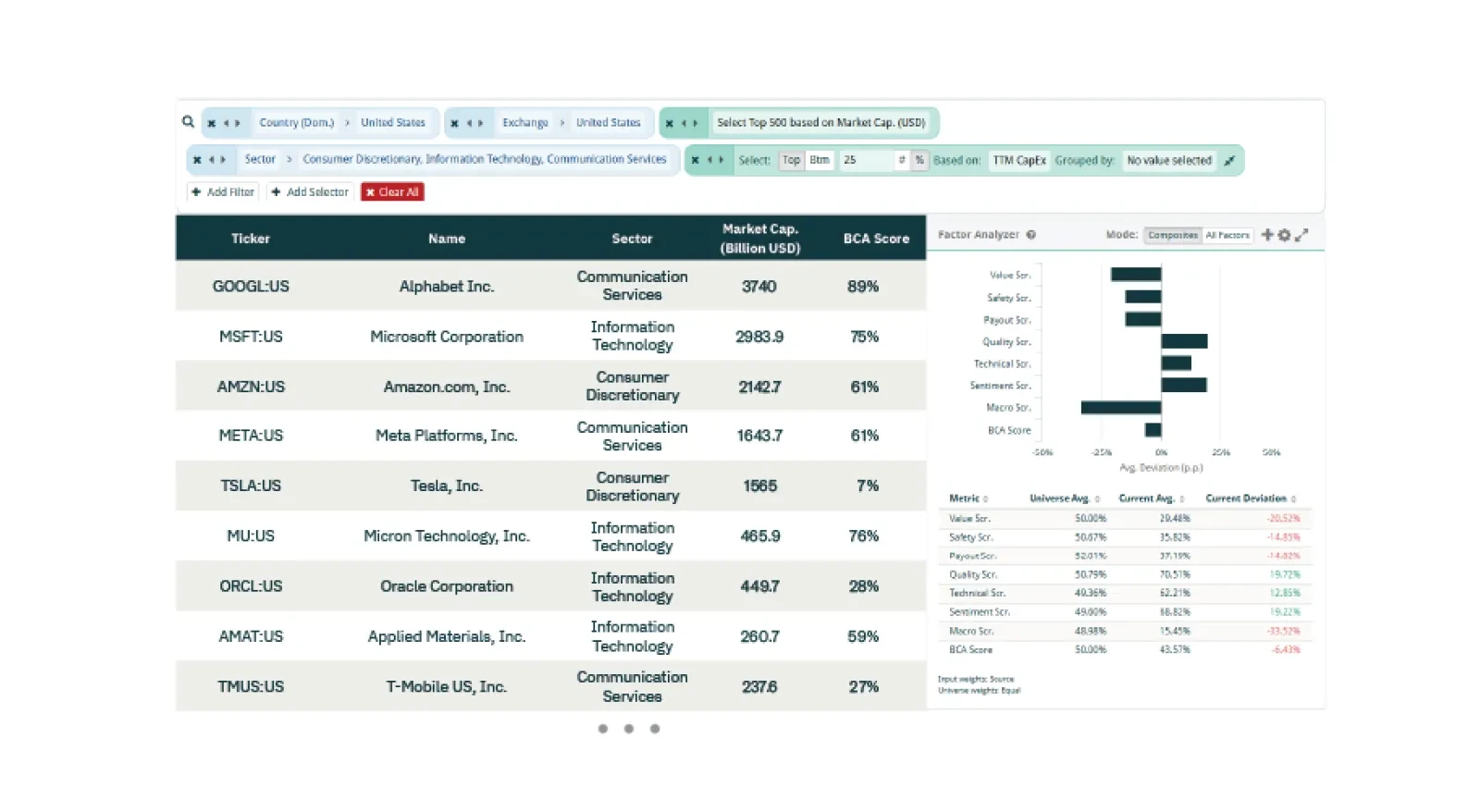

For this screener report, we explore opportunities in laggards with earnings momentum, Japanese semiconductors and US rate-sensitive stocks.

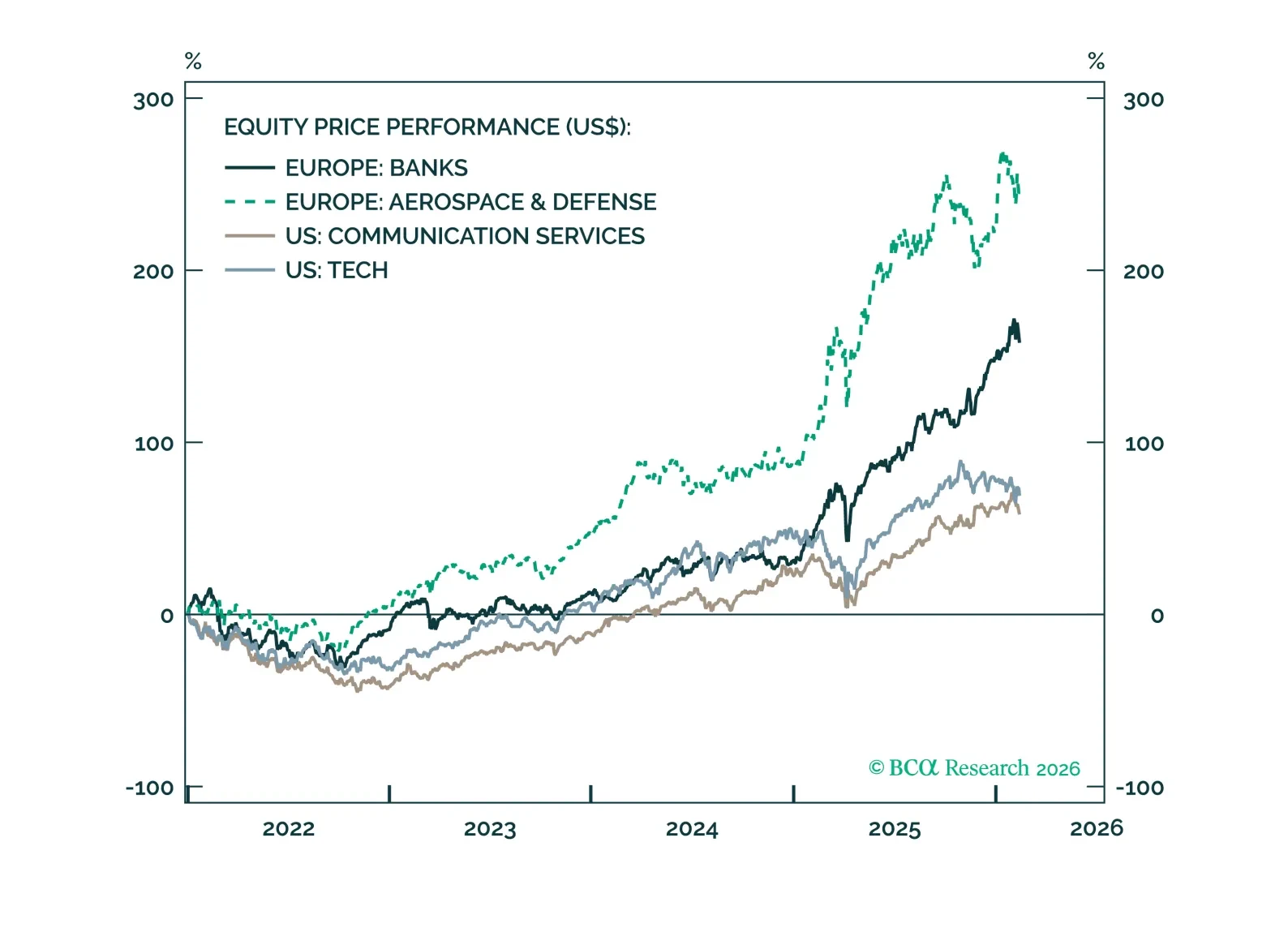

The near-term outlook is less supportive for European banks and defense equities. We downgrade banks to neutral and continue to expect defense stocks to trade in a “sell the rumor, buy the news” pattern.

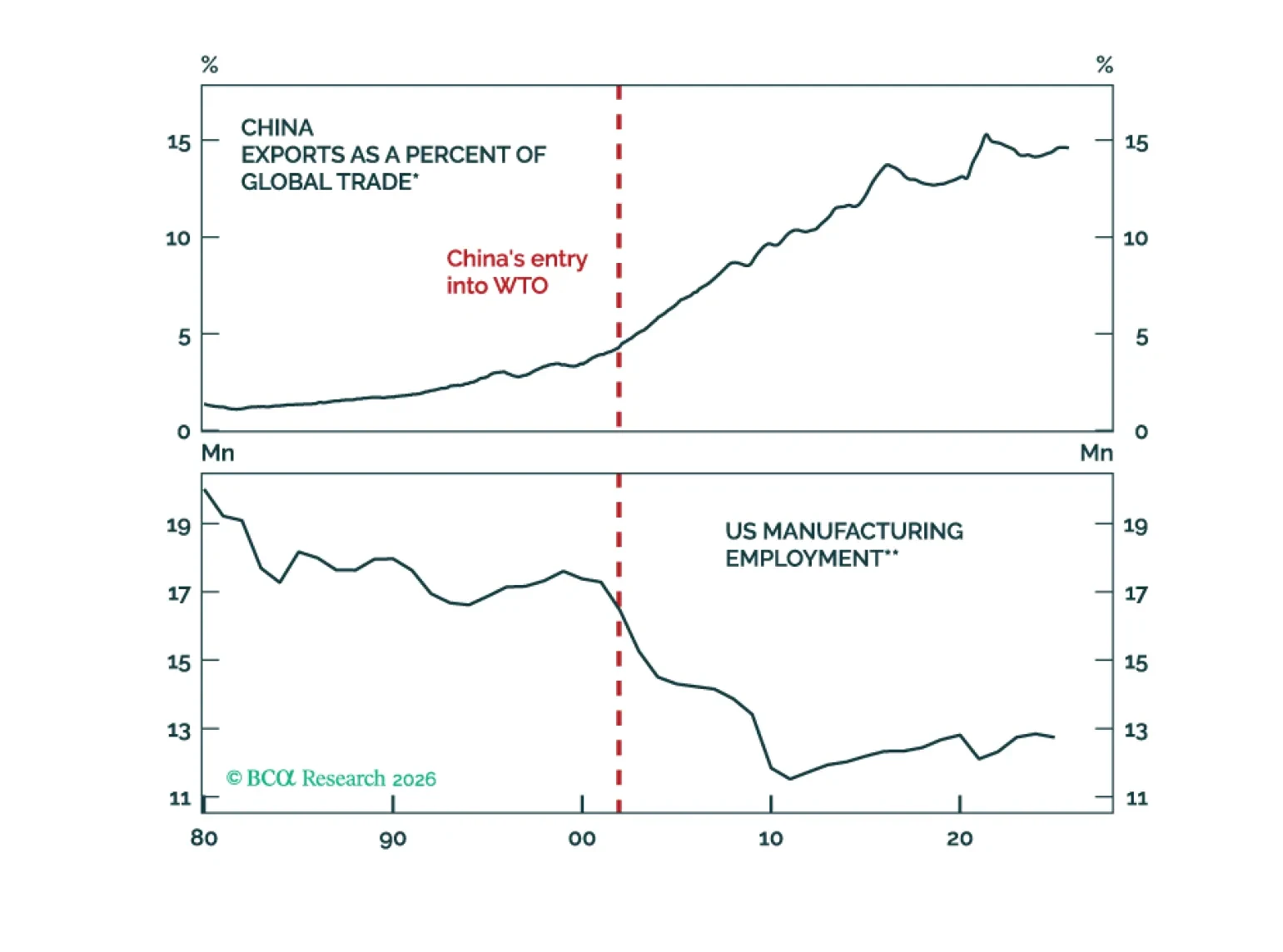

If humanoid robots were to become substitutable for workers, the AI age could lead to rapid growth in the size of the effective global labor force. The result could be a larger version of the “China shock,” which followed China’s entry into the global economy.

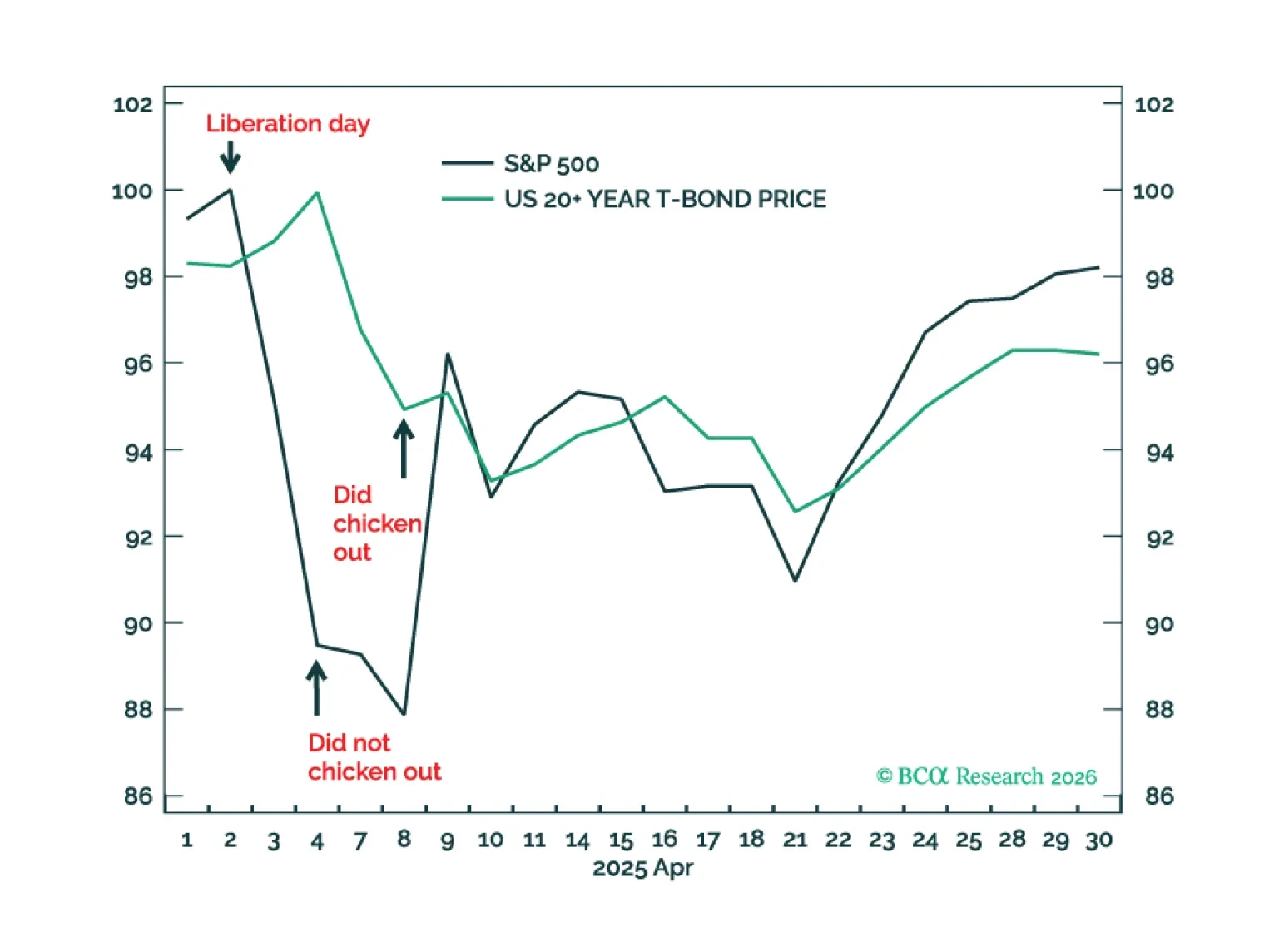

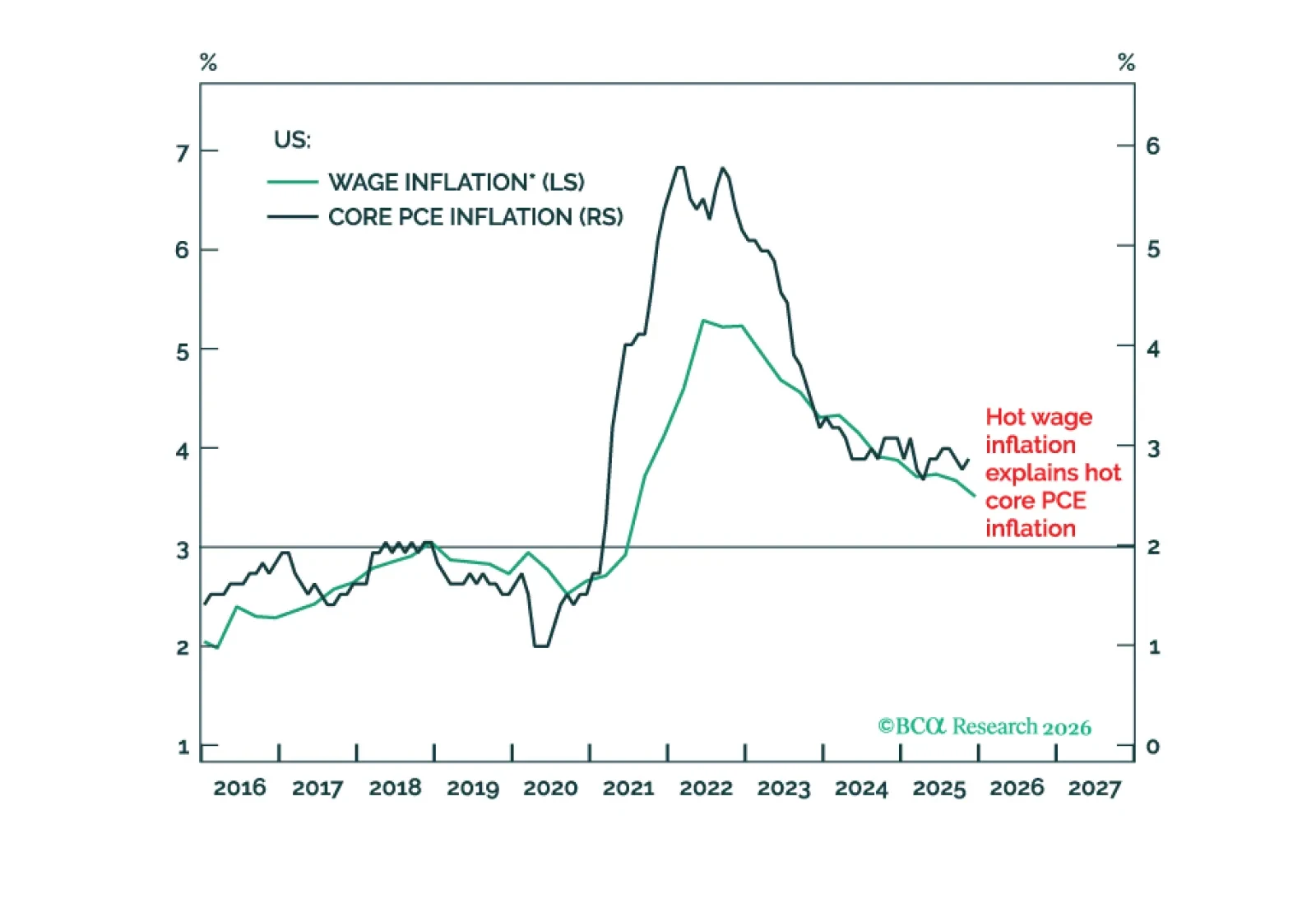

The Warsh Fed will run the US economy hot. This is bad for T-bonds and the dollar, but good for stocks. Plus, a new tactical trade is overweight Consumer Discretionary (RXI) versus Industrials (EXI).

For this screener report, we explore opportunities in a CapEx premium divergence trade, a valuation convergence trade, and European Defense Stocks.