Equities

According to BCA Research’s Global Investment Strategy service, the imbalances in the US economy are sizeable enough to generate a mild recession. Unfortunately for equity investors, a mild recession would not preclude a deep correction in stocks. …

Following a 12-year-long bear market, Greek equities have returned a whopping 186% in EUR terms from their 2016 lows. The Greek macroeconomic backdrop has indeed improved. Since 2021, Greece’s nominal GDP growth has exceeded the pace of growth in…

Despite global bond yields having trended lower since April, bonds have only started outperforming equities since July in US dollar terms. We expect this outperformance to persist going forward. Sentiment has largely driven the equity market rally this…

US small business optimism unexpectedly shed 2.5 points to 91.2 in August, the largest monthly decline since 2022, retracing nearly half of the index’s advance since March. The NFIB Small Business Optimism has oscillated in a tight range since 2022 but…

According to BCA Research’s Private Markets & Alternatives service, the Sports Franchise market presents a compelling opportunity for Private Equity due to its strong growth potential, evolving business models, and monopolistic properties. Sports team…

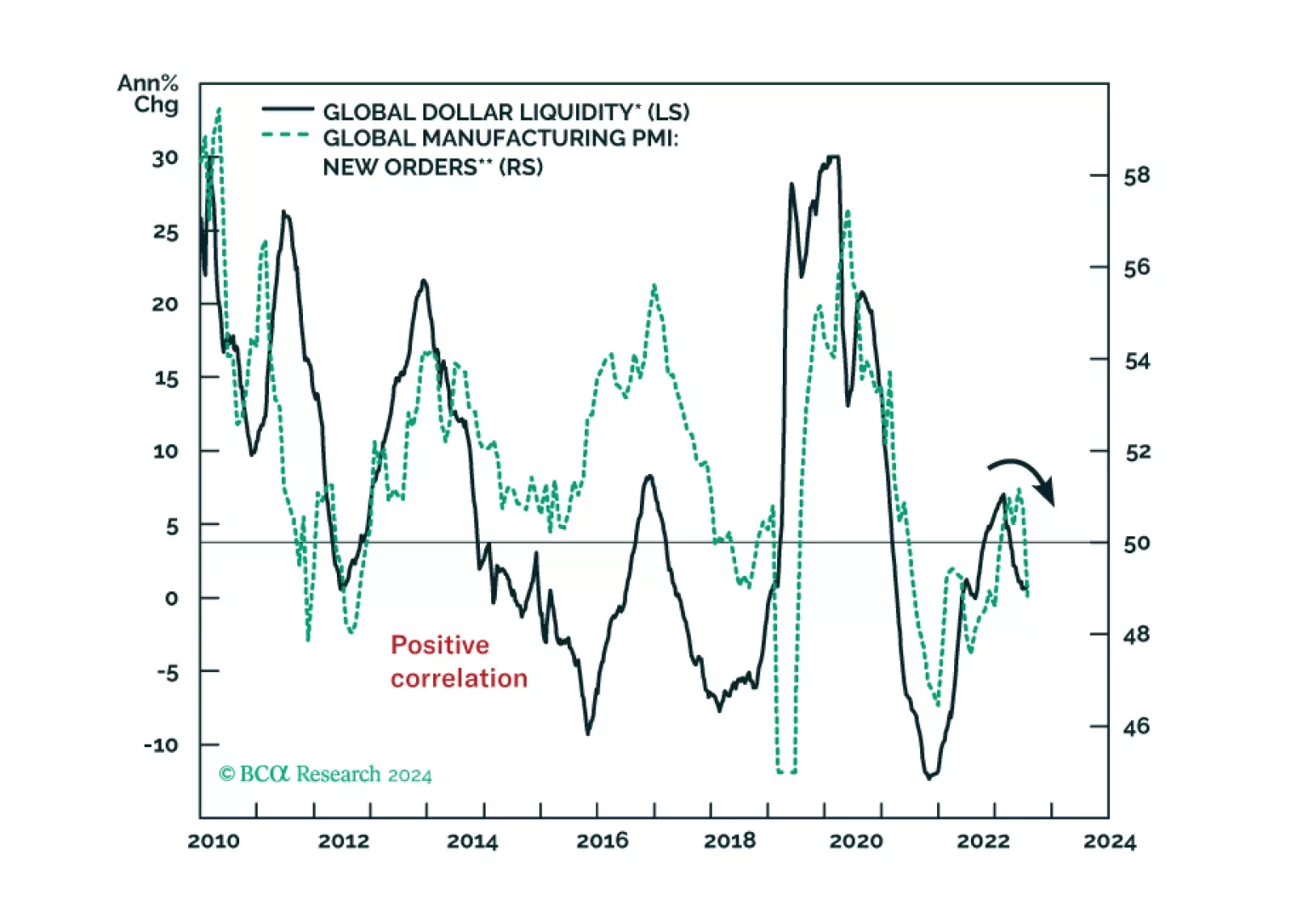

The undercurrents of global financial markets signal deteriorating global growth conditions. There is little cash on the sidelines in the US, the Euro Area, and Japan. If the budding bear market resembles the 2000-2003 one, EM stock prices are unlikely to outperform global equities in the initial leg but could outperform in the latter stage of the global selloff.

China’s CPI and PPI both surprised to the downside in August. Consumer prices grew from 0.5% y/y to 0.6%, below the 0.7% anticipated. However, a 2.8% y/y surge in food prices (the fastest pace so far this year) overstates this headline figure. Core CPI…

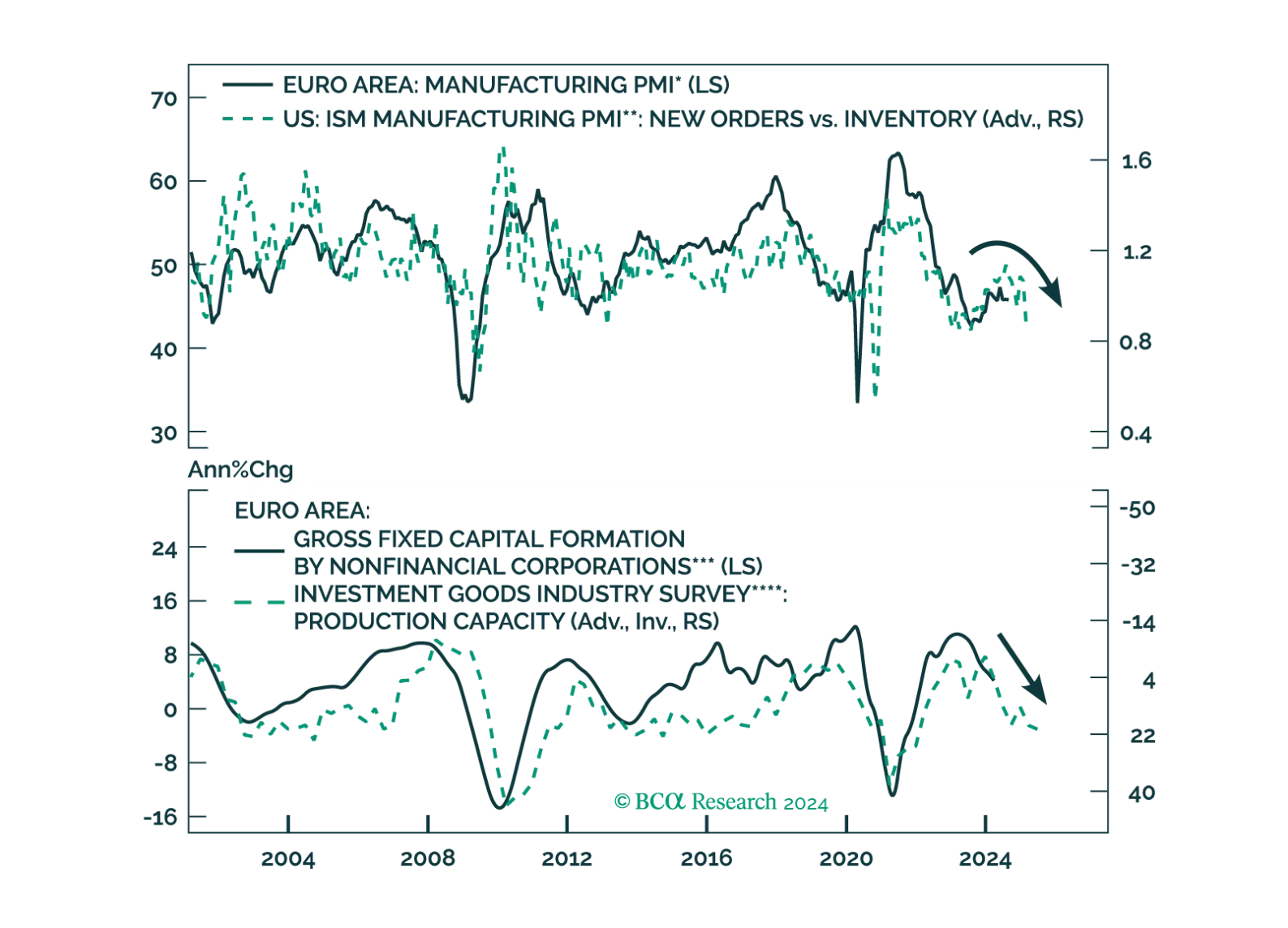

Eurozone GDP’s final estimate indicates that growth was slower than expected in Q2. Output grew 0.2% q/q in Q2, compared to 0.3% previously reported. A significant downward revision to capex (2.2% contraction against 1.8% previously estimated) drove the…

The Swedish economy’s cyclicality and sensitivity to global trade make it a reliable bellwether for global growth. Sweden is facing significant domestic weakness. Employment growth declined by 0.14% y/y in July and households’ debt burden stands at 155% of…

Crucial leading indicators of the global and European economies continue to deteriorate. How should investors position their European portfolios to benefit from these trends?