Equities

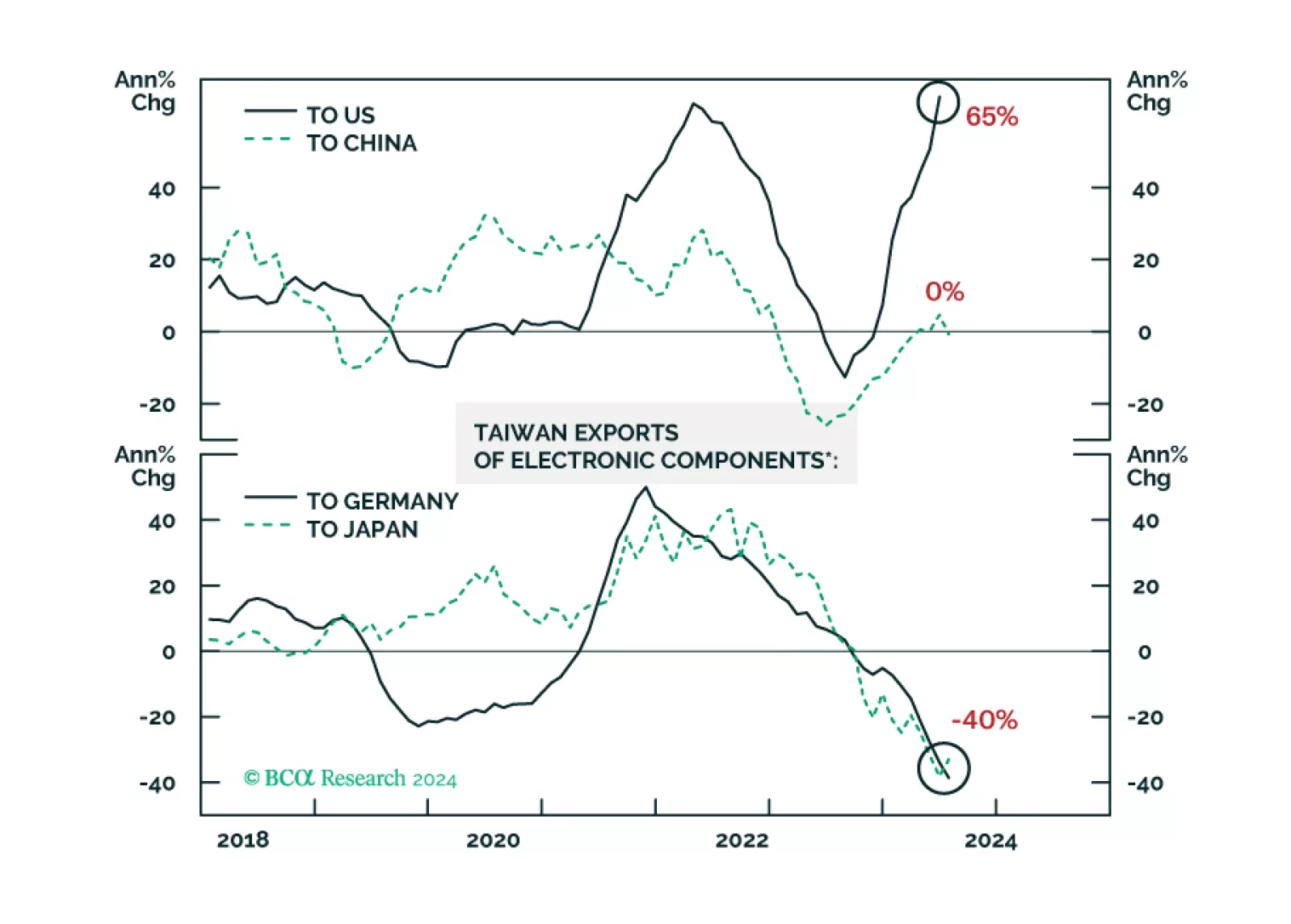

There has been a decoupling within the global semiconductor industry. Demand for AI and advanced chips has been booming. Yet, sales of legacy and non-AI semiconductors have failed to recover. Given their spectacular run-up, share prices of high-end and AI-chip producers might continue selling off even if their sales continue to grow rapidly.

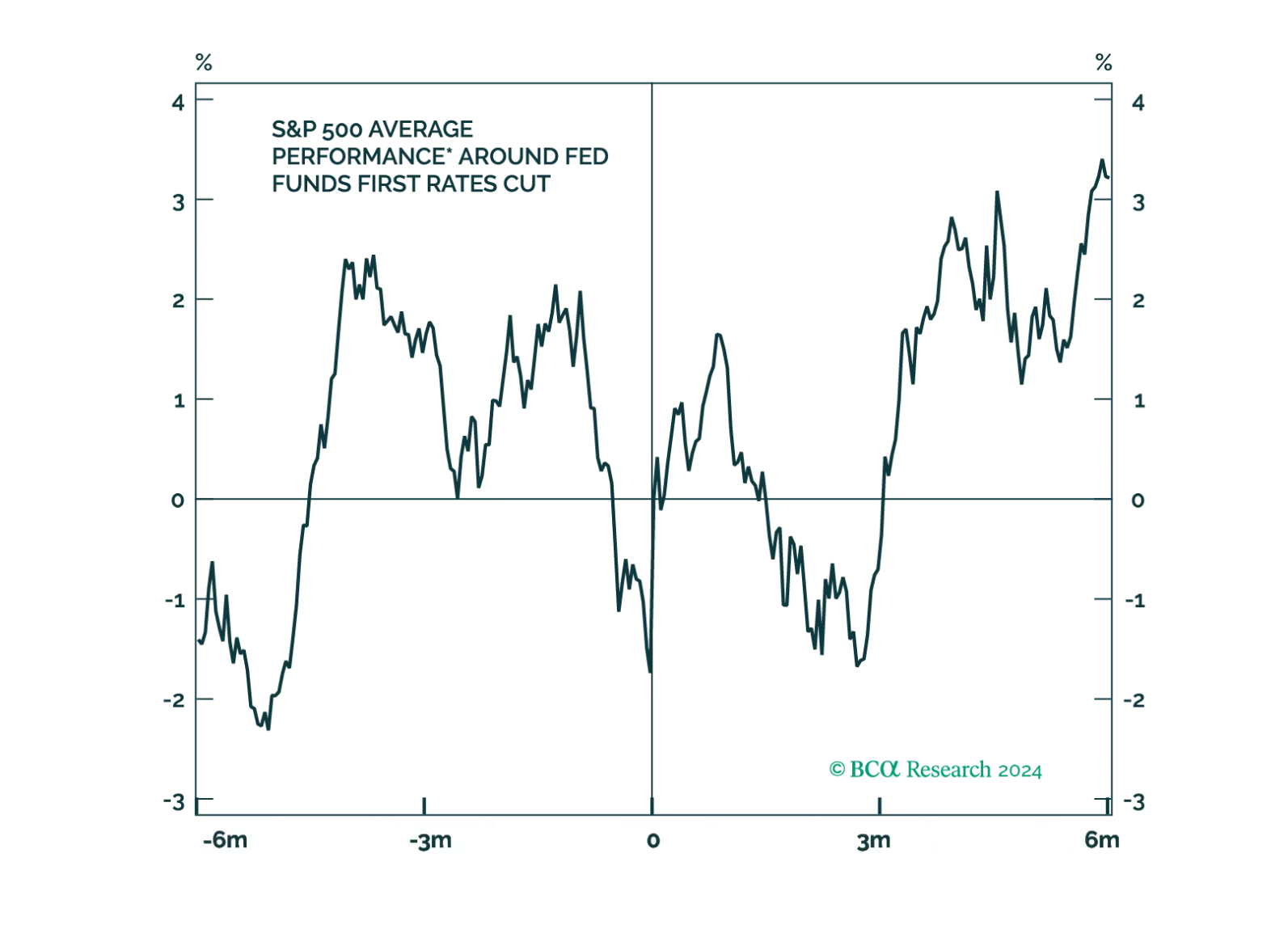

Even after the Fed cuts rates, policy will remain restrictive for some time. Moreover, in history, stocks have tended to fall around the first rate cut. We remain cautious on the outlook for the economy and risk assets.

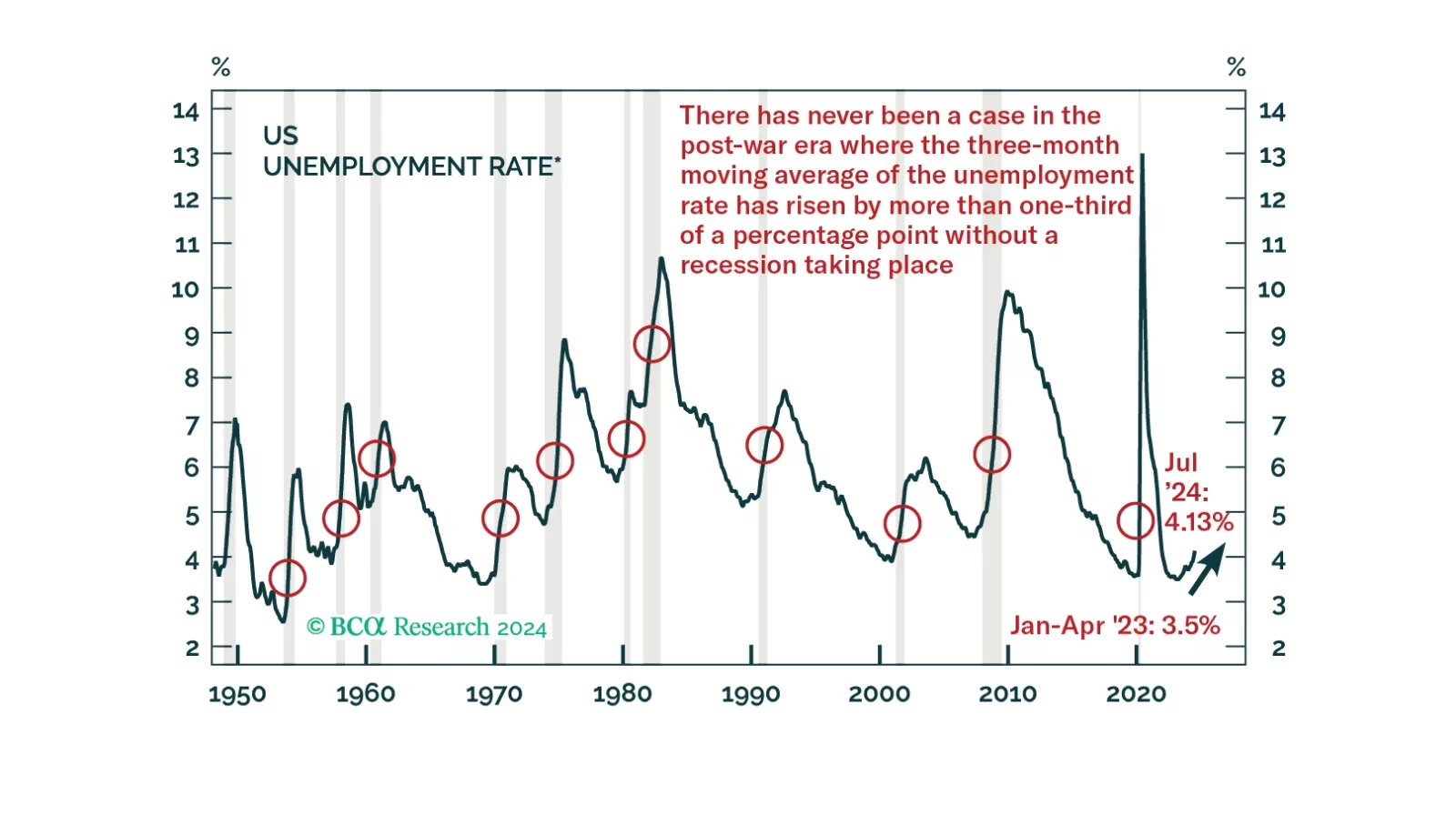

Our annual end-of-summer chartbook report traces the labor market deterioration that led us to downgrade equities at the beginning of August. It also highlights the soft-landing expectations that the credit and equity markets are discounting. We like the risk-reward profile of our newly defensive stance.