Equities

On the surface, the US durable goods report delivered a negative surprise on Tuesday. The 6.1% m/m drop in new orders in January fell below expectations and the December figure was revised down to 0.3% m/m from 0.0% m/m. However, the details of the…

According to BCA Research’s China Investment Strategy service, the odds of a “Minsky Moment” are low for the Chinese banking sector. Chinese banks, however, will continue facing cyclical and structural headwinds, including a dismal asset quality and profit…

The FTSE 250 has been outperforming the FTSE 100 since late October 2023, with the former gaining 13.7% versus 3.9% in the case of the latter over this period. To the extent that UK small cap stocks are more exposed to domestic economic dynamics than…

At the headline level, US equity indices are on a tear with the S&P 500 forging a fresh all-time high last week and the NASDAQ on the verge of overtaking its November 2021 record close. However, the rally remains quite narrow, led by only a few stocks. As…

The 2023Q4 earnings season is drawing to a close with over 80% of S&P500 companies having reported results. However, the three main providers of aggregate earnings data are posting significant variations. Indeed, IBES Refinitiv reports a robust 9% y/y…

According to BCA Research’s European Investment Strategy service, Germany will likely drag the overall Euro Area into contraction, even if, individually, other countries manage to avoid a recession. This slightly better economic outcome will nonetheless…

Germany’s IFO Business Climate index ticked up 0.3 points to 85.5 in February, in line with consensus estimates. Expectations for the next 6 months explain the improvement in sentiment among German companies (up 0.6 points to 84.1), while their assessment of…

While efforts by policymakers to stabilize the stock market are buoying Chinese equities, domestic economic data remains soggy. Home prices declined further on both a monthly and annual basis in January, reinforcing the deflationary headwinds facing the…

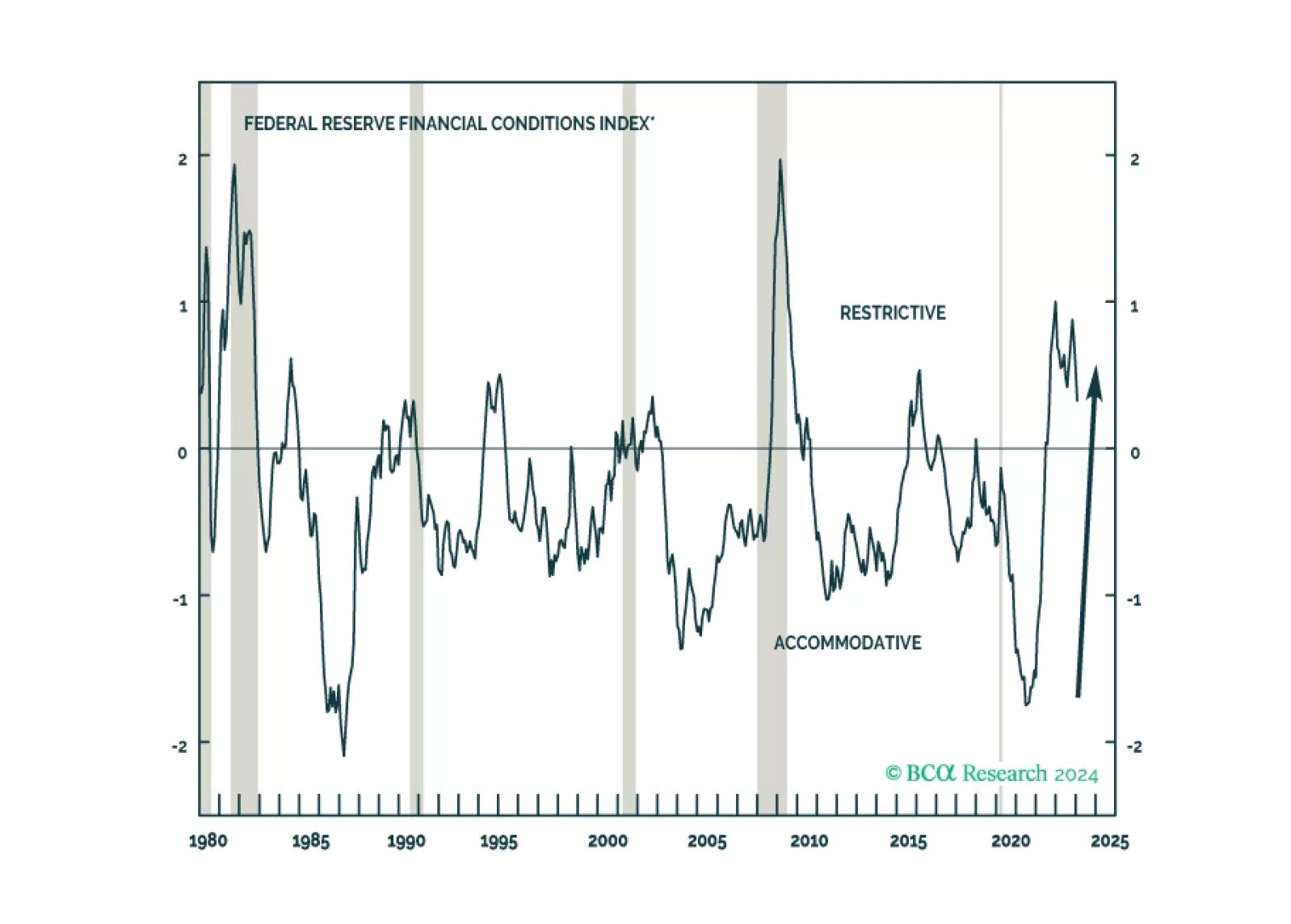

Clients have been pushing back on our recession call on the grounds that it is incompatible with the economy’s second-half acceleration and the more recent easing in financial conditions. We examine both of those points in the course of doing some pushing back of our own.

Preliminary PMI estimates suggest that service sector activity is expanding across DM economies in February. Most notably, services PMIs are back at or above 50 in Australia and the Eurozone from previously contracting levels. Meanwhile, the services sectors…