Euro Area

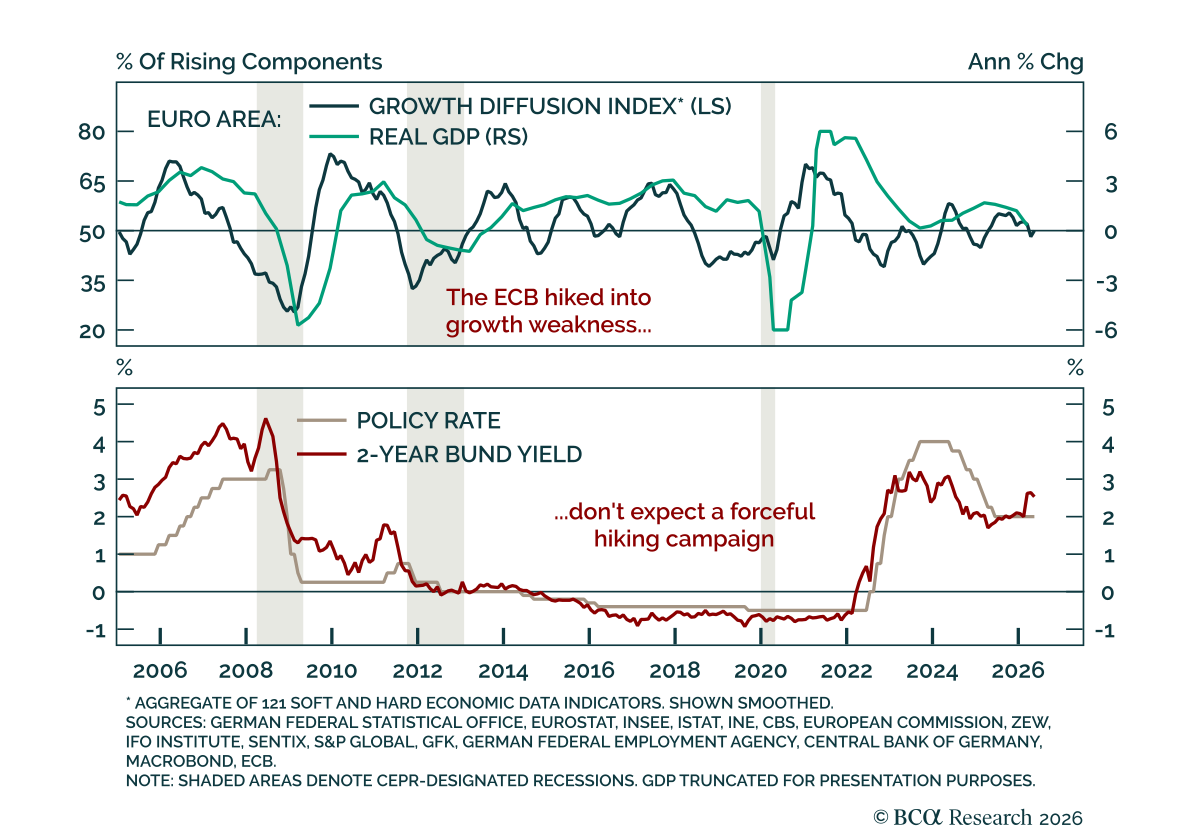

The ECB held rates at 2.25%, but kept the door open to further tightening in a near-term outlook still heavily shaped by energy prices. The hold was expected, but the ECB also signaled that every meeting remains upside risks to inflation, especially as the…

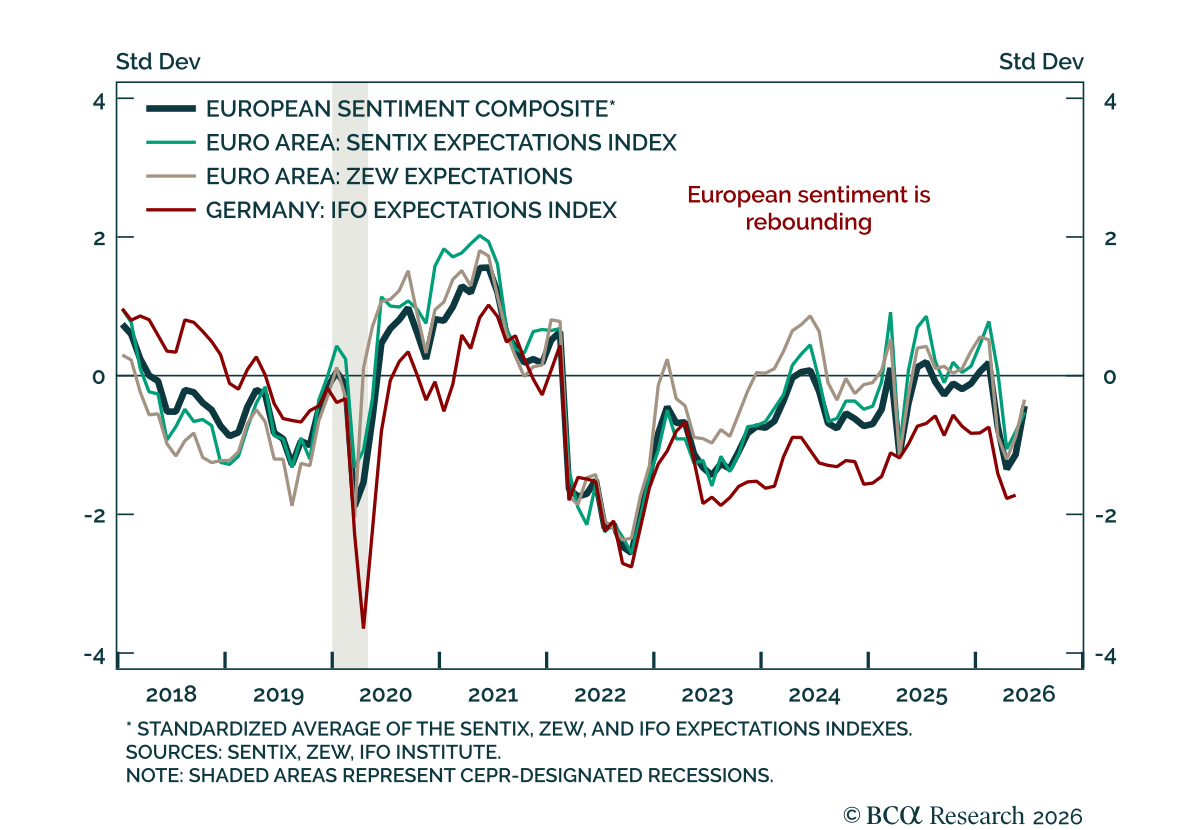

The recent European data improvement is unlikely to last. The July eurozone ZEW improved and beat estimates, but the positive impulse was likely energy-driven. Current conditions, however, remain depressed, weighing on macro momentum. Marginally tighter…

The Euro Area’s July ZEW survey pointed to a sharp improvement in sentiment alongside a lagging economy. The Euro Area expectations index rose to 23.4 from 9.5 in June, while Germany's beat estimates, climbing to 26.3 from 10.5. However, current conditions…

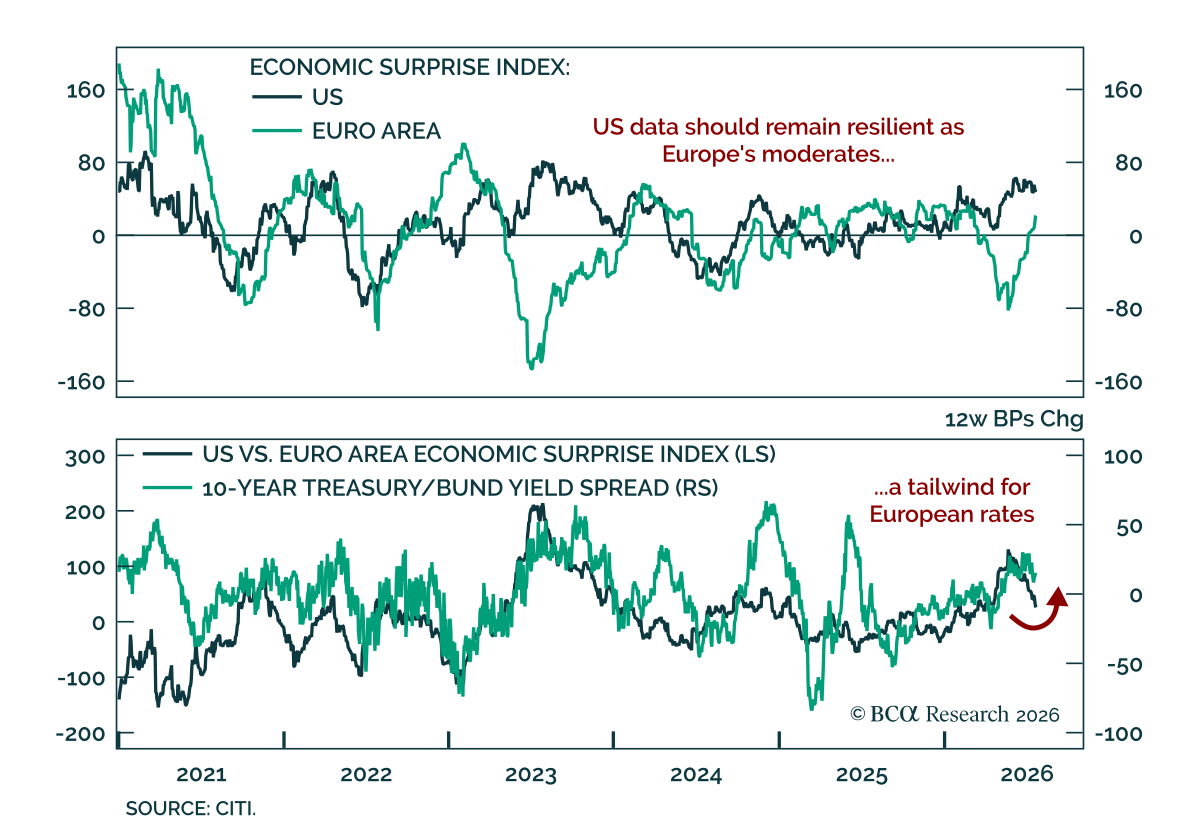

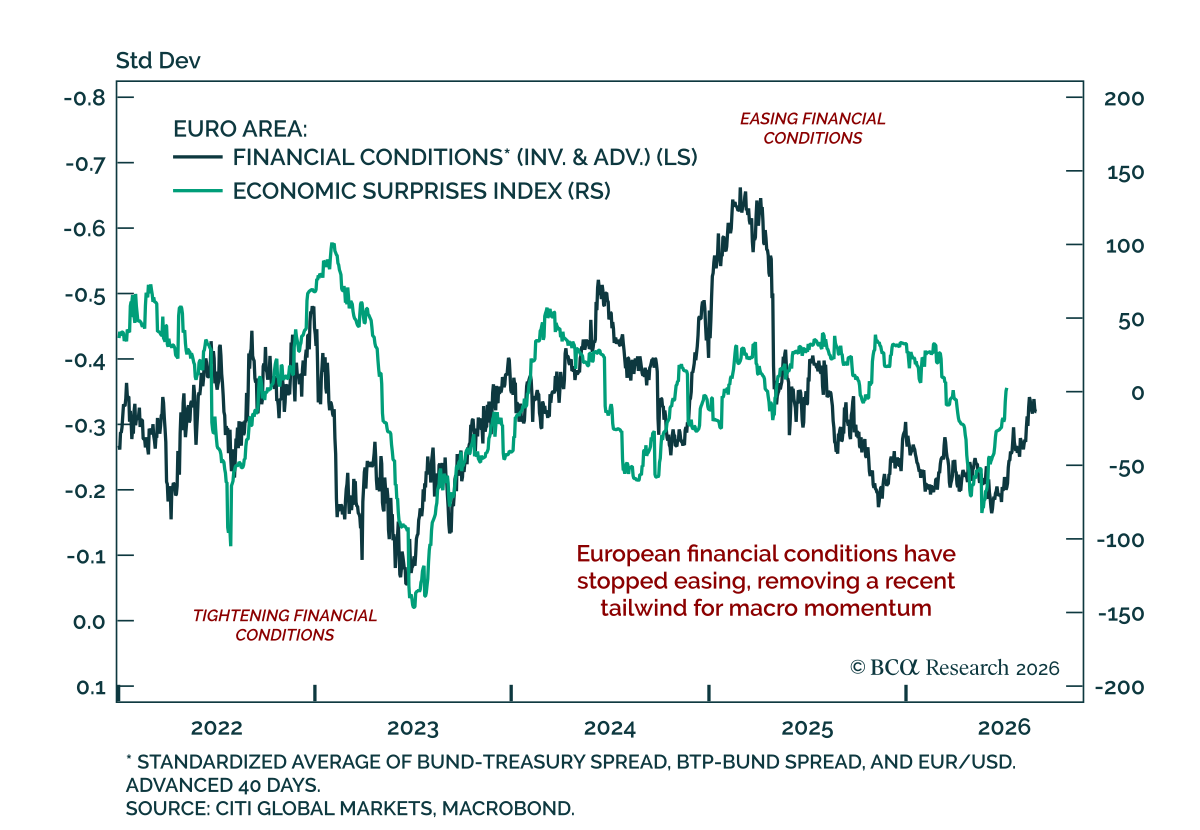

European data has stabilized, but a sustained improvement in momentum is unlikely. Our tactical framework is built around a reflexive loop between growth surprises and financial conditions. Positive surprises tighten financial conditions and eventually weigh…

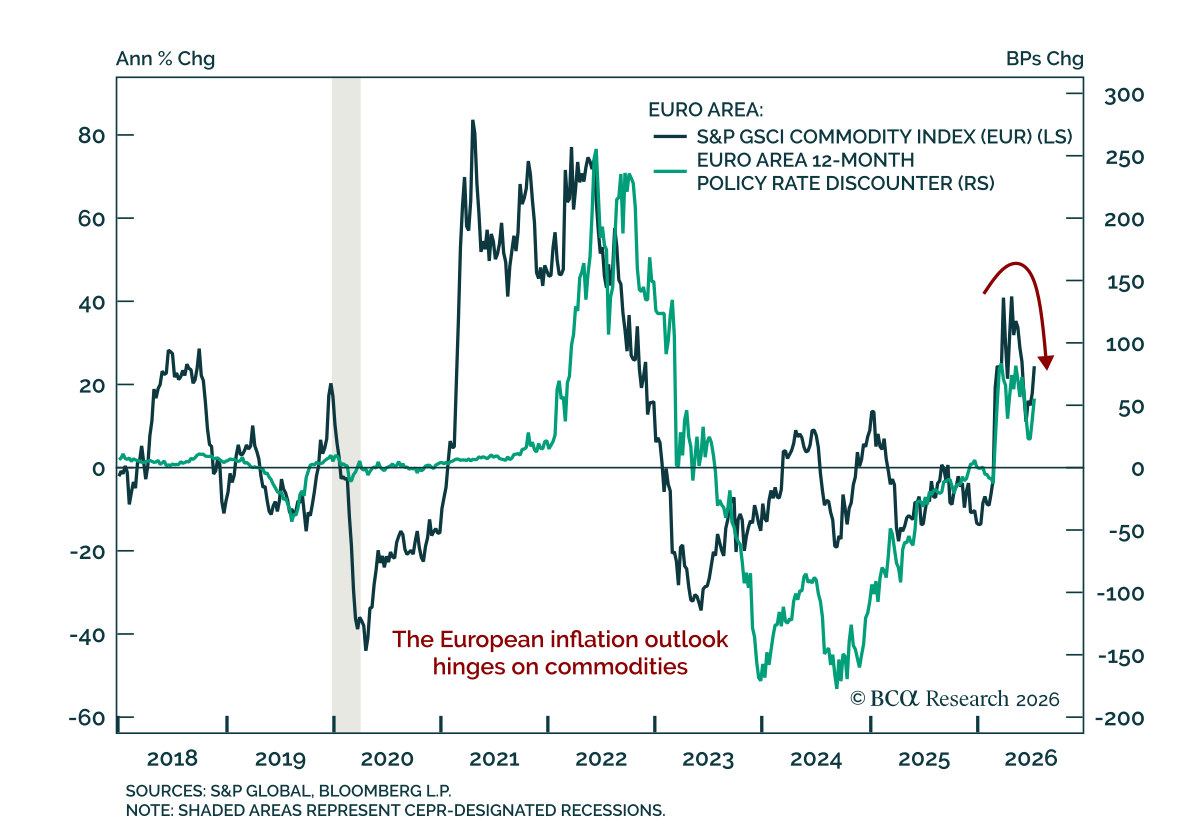

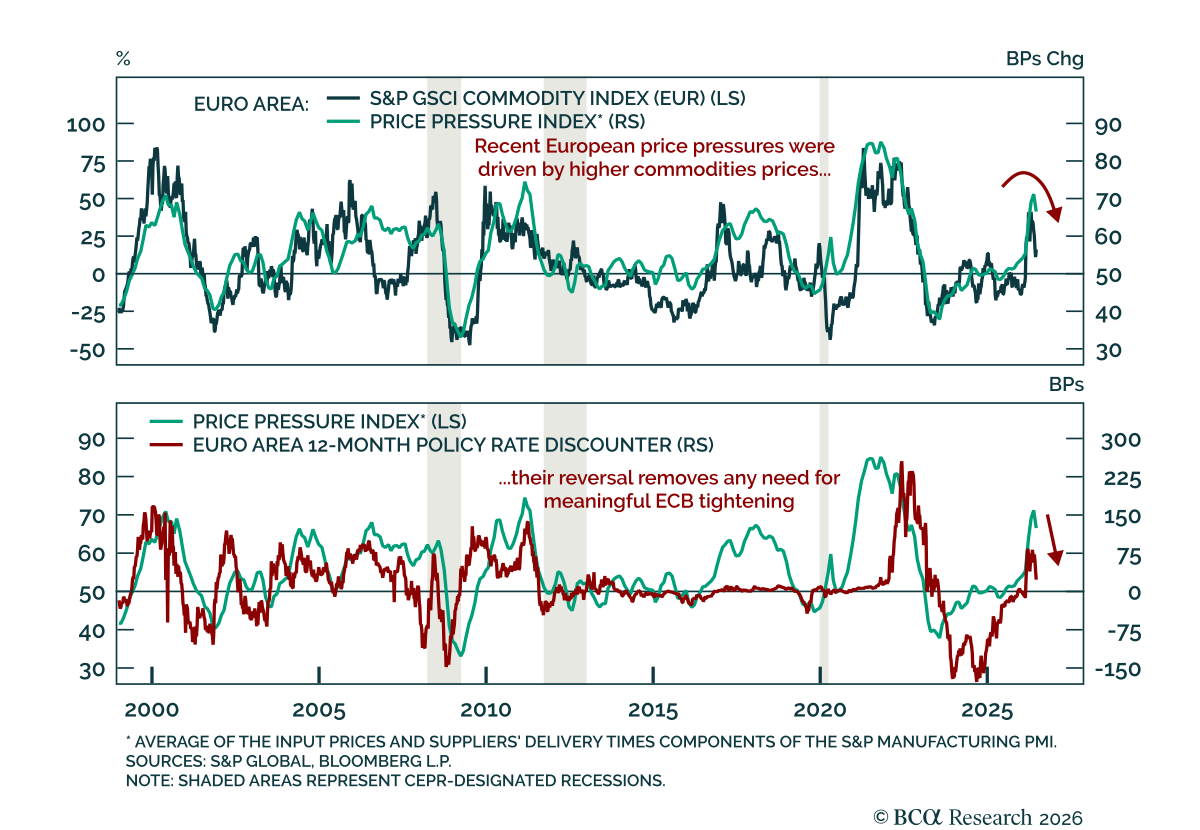

June inflation prints came in softer than expected across most major eurozone economies, reinforcing the case against further ECB tightening. Inflation undershot consensus in Germany, France, and Italy, while Spain was slightly above forecast but unchanged;…

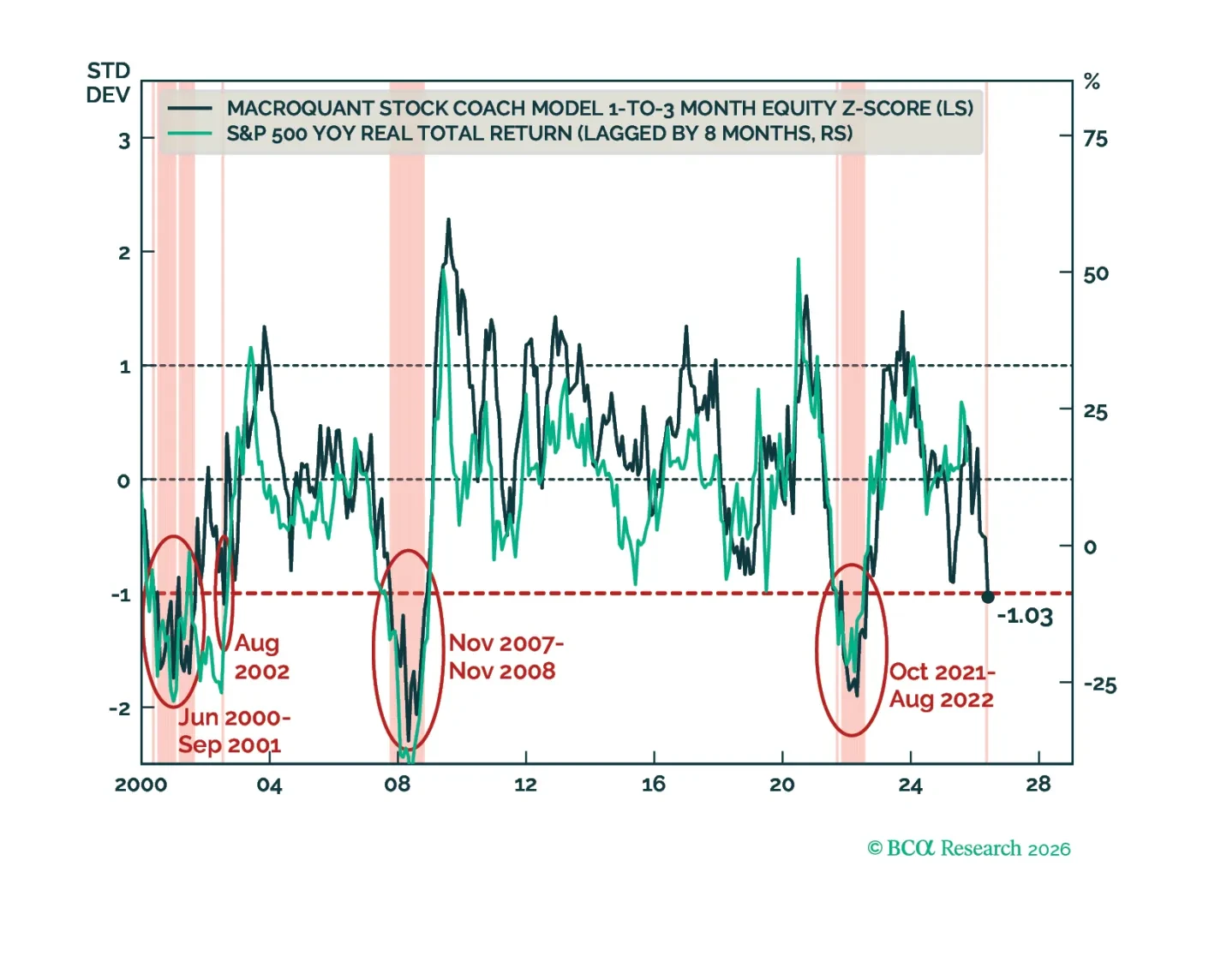

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

The June ZEW was mixed, with Germany’s expectations beating estimates while current-conditions measures worsened further. The survey period included Monday, June 15, when the US-Iran deal was announced. That split between European expectations and…

The ECB hiked as expected, but further tightening would be a mistake that ultimately supports European bonds. The policy rate was raised by 25 bps to 2.25%, as expected. The ECB also revised its inflation forecasts higher and its growth forecasts lower. It…

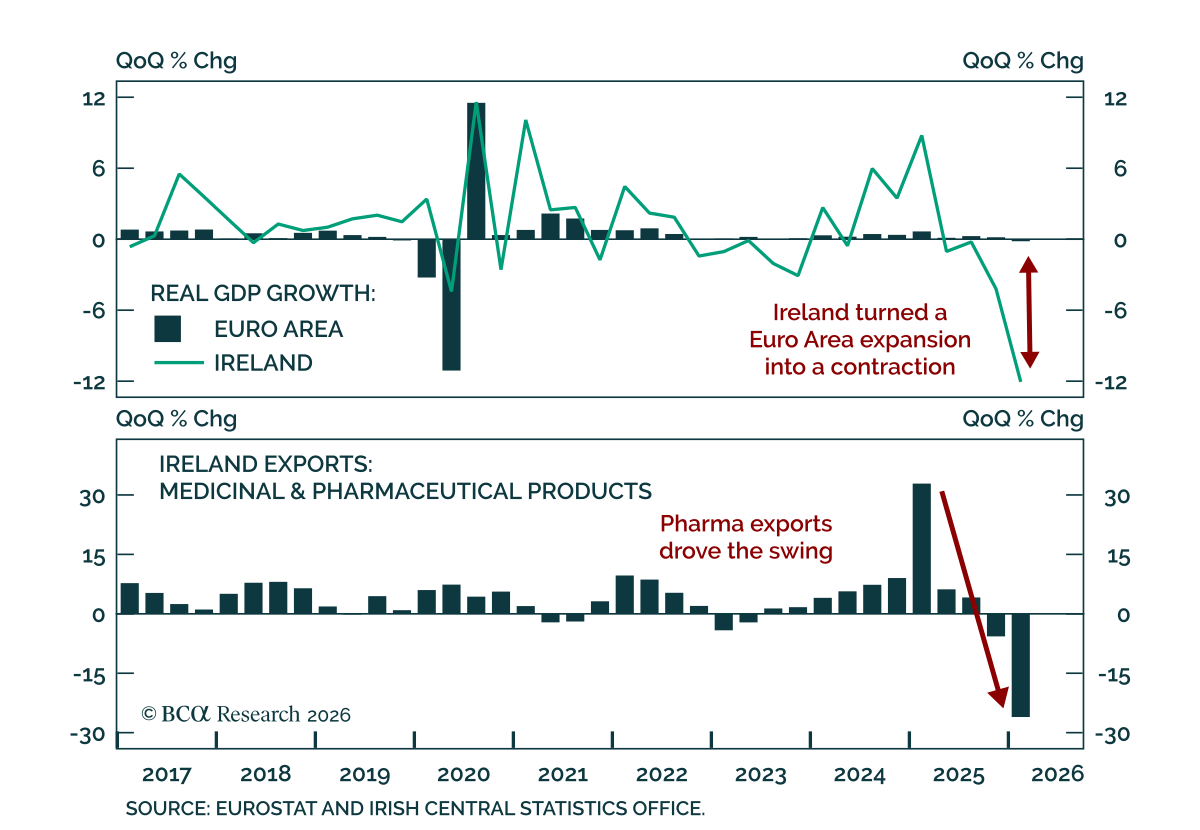

Ireland is making the Euro Area look weaker than it is. The bloc reportedly contracted 0.2% in Q1 2026, but stripping out Ireland would have shown a 0.3% expansion. That reversal can be traced back to a dramatic downward revision in Irish GDP, from -2% to…

Euro area core inflation jump to 2.5% strengthens the case for a near-term ECB insurance hike, but investors should not extrapolate hawkish policy over the next 12 months. The move from 2.2% to 2.5% in May exceeded expectations of 2.4%, but core HICP remains…