Euro Area

Highlights The USD remains supported by fundamentals, especially now that its late-2016 excesses have been purged. Solid U.S. growth contrasts with weaker growth in the rest of the world, which will incentivize further inflows into the U.S. dollar. Despite this positive cyclical view, the tactical outlook remains risky for dollar bulls. In the immediate term, the euro will benefit from easing Italian tensions and as well as from the dollar's correction, but its six-month outlook remains poor. The AUD could also rebound right now, but any such rally should be used to build further short positions. Feature After a furious rally from February to August, the dollar has been weakening since the middle of last month. Since July, we have been worried that the dollar could stage a bit of a correction,1 but we remained committed to the view that ultimately the greenback would rise further in 2018. It is now time to review whether this thesis still holds. BCA believes that the USD's correction could run through the fall, but that the final quarter of 2018 should still prove a rewarding period for dollar bulls. Ultimately, policy divergences will remain a crucial support for the dollar, especially as EM weakness continues to affect the distribution of growth across the globe. USD: Not Yet Extended The dollar ultimately follows the path implied by its fundamental drivers - whether they are interest rate spreads, growth and inflation differentials, relative equity prices, or even relative money-supply growth. However, the path taken by the USD around its drivers is rather wide, and the dollar regularly overshoots and undershoots the equilibrium implied by the aggregation of all these fundamentals (Chart I-1). Academics call this the "band of agnosticism." Chart I-1The Dollar To Follow Fundamentals Higher

The Dollar To Follow Fundamentals Higher

The Dollar To Follow Fundamentals Higher

This cycle was no exception. BCA's Fundamentals Index for the dollar hooked up in 2011, a move associated with a turning point in the greenback itself. However, the dollar remained in undershoot territory for many years. Then suddenly, in 2014, the coiled spring was released and the dollar surged higher, moving above its "band of agnosticism" in 2015 - a moved exacerbated by the sudden rally that followed the election of Donald Trump in November 2016. Once the dollar had become over-loved, over-owned and expensive, it also became vulnerable. The pick-up in global growth that was so evident in 2017 caused a serious correction in this vulnerable currency. However, the selloff had a positive impact: U.S. growth, interest rates, equities and so on continued to move favorably, and the dollar is now positioned to rebound anew, having purged its most egregious excesses. The global economic backdrop is also positive for the dollar. For one, the theme of monetary divergences is still at play. Boosted by a healthy banking sector, healthy household balance sheets and an untimely fiscal stimulus of 1.7% of GDP, U.S. growth has hit 2.8%, well above potential. Moreover, growth has been above potential for eight years, and now U.S. capacity utilization is at its tightest level since the late 1980s. Historically, so large an absence of slack has been linked to higher U.S. interest rates (Chart I-2). Yet interest rate markets are pricing in roughly four increases over the next 24 months, even as Lael Brainard warned that the Federal Reserve could move beyond the hikes implied by its own forecast, the "dot plots." Chart I-2Tight Capacity Utilization Implies Higher U.S. Rates...

Tight Capacity Utilization Implies Higher U.S. Rates...

Tight Capacity Utilization Implies Higher U.S. Rates...

The U.S. economy continues to fare well, as U.S. real interest rates remain 60 basis points below neutral rates and the yield curve has yet to invert. However, U.S. rates matter for the rest of the world as well. There, the picture is less pretty. EM dollar debt stands near record levels (Chart I-3). Hence, EM financial conditions have been hit by the combined assault of higher U.S. rates and an appreciating dollar. Nowhere is this clearer than when looking at the interplay between U.S. bond yields and the South African rand or AUD/JPY, a cross highly correlated to EM currencies. This cycle, rising U.S. bond yields have most often been associated with a rising ZAR or a rising AUD/JPY (Chart I-4). However, this time around, as was the case during the May 2013 Taper Tantrum, rising bond yields are linked to these pro-cyclical currency pairs falling. This suggests that rising yields are not reflecting global growth anymore, and are in fact restrictive for the rest of the world, even if they are not a problem for the U.S. Chart I-3... Which Will Hurt EM Economies

... Which Will Hurt EM Economies

... Which Will Hurt EM Economies

Chart I-4Higher U.S. Rates Now Hurt Global Growth

Higher U.S. Rates Now Hurt Global Growth

Higher U.S. Rates Now Hurt Global Growth

This inference is underpinned by the decline in BCA's U.S. Financial Liquidity Index, which heralds additional weakness in global growth and commodity prices (Chart I-5). Already we are seeing symptoms of the malaise. Japanese foreign machine tool orders are contracting, and BCA's Asian Leading Economic Indicator is in deep contraction (Chart I-6). Chart I-5Dollar Liquidity Is A Problem For Growth

Dollar Liquidity Is A Problem For Growth

Dollar Liquidity Is A Problem For Growth

Chart I-6Signs That Global Growth Is Already Suffering

Signs That Global Growth Is Already Suffering

Signs That Global Growth Is Already Suffering

A rising fed funds rate and falling ex-U.S. growth is likely to continue to support the dollar. The dollar loves nothing more than falling global growth. The U.S. economy has low exposure to global trade and to the global industrial sector, and therefore when global growth slows, the U.S. economy is relatively insulated from foreign shocks. This means that U.S. rates of return do not suffer as much as foreign ones. This is even truer in the rare instances when global growth slows while U.S. economic activity continues to power ahead, especially when artificially inflated by untimely fiscal stimulus. This is a characterization of the current environment. Hence, money will continue to flow into the U.S. economy on a two- to three-quarter horizon. In fact, portfolio flows into the U.S. remain well below the levels that prevailed during the previous decade (Chart I-7). The current account deficit is also smaller, hence, if net foreign portfolio flows can increase due to the attraction of higher U.S. rates of return, the U.S. balance of payments will move into a greater surplus, creating a strong underpinning for the dollar. This positive cyclical backdrop for the greenback is not without impediments. Most crucially are the short-term dynamics. Since July, we have been warning clients that a tactical correction in the dollar was likely. While EUR/USD has indeed rebounded, most other currencies have displayed rather tepid performances. This does not mean that the tactical risks to the dollar have abated. Quite the opposite, they are rising. As Chart I-8 illustrates, a large buildup in dollar longs has materialized, yet the G10 economic surprise index is making a trough. Moreover, the diffusion index of the BCA Global Leading Economic indicator is also stabilizing. Additionally, USD /CNY has failed to make new highs and the Turkish central bank just raised rates to 24% - which if Argentina is any guide is likely to provide only temporary relief for the TRY. This means that a period of risk-on sentiment in EM could emerge. Stretched dollar positioning, a temporary stabilization in global growth and EM inflows could precipitate a serious correction in the dollar. Chart I-7Dollar Favorable Flows

Dollar Favorable Flows

Dollar Favorable Flows

Chart I-8Tactical Risks To The Dollar

Tactical Risks To The Dollar

Tactical Risks To The Dollar

Bottom Line: The dollar is still supported by potent cyclical tailwinds. The U.S. economy is roaring and at full employment, yet global growth is suffering because global liquidity conditions are deteriorating. Higher rates of return in the U.S. will therefore attract additional capital, supporting the greenback in the process. Despite this positive cyclical backdrop, the short-term outlook is murkier. Speculators have aggressively bought the dollar, leaving them vulnerable to any positive surprises in global growth, even temporary ones. Fade The Euro Rebound The euro has benefited from the cool-off in Italian politics. The populist Five Star Movement / Lega Nord coalition is backing away from a budget confrontation with Brussels, as Giovanni Tria, Italy's minister of finance, wants a 2% budget deficit, while Deputy Prime Minister Matteo Salvini is arguing for a 2.9% budget hole - well south of the 6% levels touted during the campaign. As a result, the spread between Italian BTPs and German bunds has fallen from 193 basis points at the beginning of the month to 150 basis points this week (Chart I-9). Since gyrations in Italian spreads reflect the evolution of the perceived probability that the euro area will fall apart, the fall in the spreads has implied a fall in the euro area-breakup risk premium. This has created a boon for the euro. Another support for the euro emerged yesterday. At his press conference, European Central Bank President Mario Draghi divulged that the ECB has curtailed its growth forecast for 2018 and 2019, but not its inflation forecast. In fact, Draghi went as far as mentioning that his confidence that euro area inflation would move back to target in the medium term has increased. There is no denying that the inflationary backdrop has improved as European wages and labor costs have indeed starting to recover (Chart I-10). However, the picture is not that straightforward. The lagged impact of the previous fall in euro area inflation relative to the U.S. is likely to continue to be felt in EUR/USD moving forward, as has been the case over the past 10 years (Chart I-11). Chart I-9The Euro Area Break Up Risk Premium Is Declining

The Euro Area Break Up Risk Premium Is Declining

The Euro Area Break Up Risk Premium Is Declining

Chart I-10Rising Euro Area Labor Costs

Rising Euro Area Labor Costs

Rising Euro Area Labor Costs

Chart I-11Relative Inflation Backdrop Is Still Euro Bearish

Relative Inflation Backdrop Is Still Euro Bearish

Relative Inflation Backdrop Is Still Euro Bearish

This risk is compounded by developments in China. As we have often argued, the growth differential between the euro area and China can largely be explained by growth dynamics in China. As Chart I-12 illustrates, when Chinese monetary conditions tighten, or when China's marginal propensity to consume - as approximated by the gap between M1 and M2 - declines, this often leads to underperformance of European economic activity relative to the U.S. Chart I-12AChinese Economy Still Hurting Euro Area Vs U.S. (I)

Chinese Economy Still Hurting Euro Area Vs U.S. (I)

Chinese Economy Still Hurting Euro Area Vs U.S. (I)

Chart I-12BChinese Economy Still Hurting Euro Area Vs U.S. (II)

Chinese Economy Still Hurting Euro Area Vs U.S. (II)

Chinese Economy Still Hurting Euro Area Vs U.S. (II)

Today, Chinese monetary conditions have improved somewhat as the Chinese authorities try to combat the shock to the Chinese economy created by the growing trade war between the U.S. and China. However, Matt Gertken, BCA's Geopolitical Strategy service's expert on Chinese policy, believes that Chinese policymakers do not intent to actually cause economic growth to pick up. Indeed, they are committed to reform and deleveraging, and only want to limit downside to the Chinese economy.2 Thus, the large growth gap between the U.S. and the euro area is here to stay. As markets absorb news of Chinese stimulus, EUR/USD could rebound toward 1.19, but we are inclined to fade such a rebound. For one, the growth and inflation gap between the U.S. and the euro area remains euro bearish. Additionaly BCA's Central Bank Monitor for the Fed clearly points toward the need to tighten U.S. monetary policy, while our indicator for the ECB points to the need to maintain an extremely loose policy setting in Europe (Chart I-13). With the euro still trading above its intermediate-term fair value estimate (Chart I-14), beyond any short-term rally the euro still possesses ample downside in the fourth quarter. As such, we would use the current rebound in the euro as an opportunity to buy the dollar once again. Chart I-13The U.S. Needs More Tightening, Europe Does Not

The U.S. Needs More Tightening, Europe Does Not

The U.S. Needs More Tightening, Europe Does Not

Chart I-14The Euro Possesses Downside

The Euro Possesses Downside

The Euro Possesses Downside

Bottom Line: Falling risk premia in Italy, a pick-up in European wages and signs of stimulus in China are creating some support under the euro. However, European growth and inflation are set to continue to lag well behind the U.S. as China's stimulus is not designed to reverse its deleveraging campaign and boost growth, but instead to limit downside to growth created by the U.S.-China trade war. Hence, we will use the current rebound in the euro and correction in the USD to buy the greenback again in the coming weeks. What's Going On Down Under? In recent months, the Australian economy has managed to generate some impressive numbers on the employment front. However, until recently this was not enough to prompt investors to push the AUD higher. In fact, as recently as Monday, AUD/USD was trading at 0.71. Investors are skeptical about the Australian economy's underlying strength. The NAB Business Confidence for the Next Period has weakened sharply, while mortgage approvals and house prices have also sagged. This suggests that new orders, employment and consumption could follow lower (Chart I-15). This represents a big problem for the Aussie, as our central bank monitor for the Reserve Bank of Australia is already in "easing required" territory (Chart I-16). The RBA will therefore not be able to hike rates any time soon, despite the fact that U.S. interest rates are currently in an uptrend. As such, interest rate differentials between Australia and the U.S. will continue to deteriorate. Chart I-15Australia Is Set To Slowdown

Australia Is Set To Slowdown

Australia Is Set To Slowdown

Chart I-16China And Australia Are Joined At The Hip

China And Australia Are Joined At The Hip

China And Australia Are Joined At The Hip

Moreover, Australia has been hit directly by the decline in Chinese industrial activity. As Chart I-17 illustrates, Australian exports are a direct function of China's Li-Keqiang index. This has two implications. First, the current rebound in the Li-Keqiang index suggests that investors could bid up the AUD with great alacrity if the USD were to correct further, a thesis we espouse. However, since we do not anticipate the rebound in the Li-Keqiang indicator to have much longevity, nor do we anticipate the greenback's correction to morph into a bear market, this also means that we would use any rebound in the AUD to sell more of it. Beyond China, EM at large still constitutes a risk for AUD/USD. Arthur Budaghyan, our Chief EM strategist, argues that the period of weakness in EM assets has further to run. Our views on the U.S. dollar, on declining global liquidity and on Chinese policy corroborate this assessment. If EM economies slow further, the still-elevated expected long-term growth rate in EM earnings could decline further as well. Since growth expectations on EM EPS are indicative of expected interest rates and terms-of-trade for Australia, this also suggests that the AUD could suffer significant downside in the coming quarters (Chart I-18). Finally, the AUD remains a pricey currency. AUD/USD continues to trade significantly above its purchasing-power-parity fair value, and the real trade-weighted AUD remains above its long-term average (Chart I-19). As such, the AUD does not possess the required valuation cushion to make it a buy in this challenging context. Chart I-17RBA ##br##Cannot Hike

RBA Cannot Hike

RBA Cannot Hike

Chart I-18EM Has Yet To Be Fully Re-Rated, ##br##And So Does The AUD

EM Has Yet To Be Fully Re-Rated, And So Does The AUD

EM Has Yet To Be Fully Re-Rated, And So Does The AUD

Chart I-19No Valuation Cushion##br## In The AUD

No Valuation Cushion In The AUD

No Valuation Cushion In The AUD

Bottom Line: The Australian economy has posted some solid employment numbers, but the trends in business confidence and the housing market augur poorly. Australian monetary policy will have to remain very loose. Moreover, since China's stimulus is likely to be limited, any rebound in the AUD on the back of a dollar correction should be faded, especially as the Aussie does not offer any valuation cushion. Mathieu Savary, Vice President Foreign Exchange Strategy mathieu@bcaresearch.com 1 Please see Foreign Exchange Strategy Weekly Report, titled "Time To Pause And Breathe", dated July 6, 2018, available at fes.bcaresearch.com 2 Please see Foreign Exchange Strategy Special Report, titled "China: How Stimulating is The Stimulus?", dated August 24, 2018, available at fes.bcaresearch.com Currencies U.S. Dollar Recent data in the U.S. has been mixed: Average hourly earnings growth outperformed expectations significantly, coming in at 2.9%. Moreover, nonfarm payrolls also surprised to the upside, coming in at 201 thousand, but this was mitigated by large downward revisions to the previous two months. Additionally initial jobless claims surprised positively, coming in at 203 thousand. However, core inflation underperformed expectations, coming in at 2.2%. Finally, DXY has been flat for the past couple of weeks. We continue to be bullish on the dollar on a cyclical basis, as inflationary pressures will continue to accumulate in the U.S., causing the fed to hike more than expected, particularly in 2019. Moreover, high U.S. borrowing cost will likely weigh on global growth, giving an additional boost to the dollar, as the U.S. has a lower beta than other DM economies to the global economic cycle. Report Links: The Dollar And Risk Assets Are Beholden To China’s Stimulus - August 3, 2018 Rhetoric Is Not Always Policy - July 27, 2018 Time To Pause And Breathe - July 6, 2018 Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

The Euro Recent data in the euro area has been negative: Both headline and core inflation surprised to the downside, coming in at 2% and 1% respectively. Moreover, industrial production yearly growth also surprised to the downside, coming in at -0.1%. Finally, retail sales yearly growth also underperformed expectations, coming in at 1.1%. EUR/USD has been flat the past two weeks. Yesterday, however the market rallied as the ECB confirmed that it expects to wind down its bond-buying program. Nevertheless, it also lowered growth forecast for this year and next. We continue to believe that the euro will have downside until the end of the year, as a policy and regulatory tightening in China will weigh on the global industrial cycle, to which Europe is highly levered. Report Links: Time To Pause And Breathe - July 6, 2018 What Is Good For China Doesn’t Always Help The World - June 29, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

The Yen Recent data in Japan has been mixed: Tokyo ex fresh food inflation outperformed expectations, coming in at 0.9%. Moreover, overall household spending yearly growth also surprised positively, coming in at 0.1%. However, labor cash earnings yearly growth underperformed expectations substantially, coming in at 1.5%. Finally, Markit Services PMI surprised to the downside, coming in at 51.5. USD/JPY has been flat the past couple of weeks. Overall, we are bullish on the yen against the euro and the commodity currencies, as the tightening in monetary policy in the U.S. as well as in China should create a risk off environment where safe heavens like the yen benefits and cyclical currencies suffer. Report Links: Rhetoric Is Not Always Policy - July 27, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Rome Is Burning: Is It The End? - June 1, 2018 Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

British Pound Recent data in the U.K. has been mixed: Average hourly earnings yearly growth excluding and including bonuses both came in above expectations, at 2.9% and 2.6% respectively. Moreover, Markit Services PMI also outperformed expectations, coming in at 54.3. However, industrial production surprised to the downside, coming in at 0.9%. Finally, nationwide housing prices yearly growth also surprised negatively, coming in at 2%. GBP/USD has rallied by roughly 0.5% the past couple of weeks. We believe that the pound could have some short term upside, as positioning continues to be significantly bearish. That being said, we are bearish on the pound on a cyclical basis, particularly against the yen. At this moment, the pound does not appear to have much of a geopolitical risk premium embedded in its price. Thus, any turbulence in the Brexit negotiations could result in significant downside for the GBP. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Inflation Is In The Price - June 15, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Australian Dollar Recent data in Australia has been mixed: Gross domestic product yearly growth came in above expectations, at 3.4%. However, building permits month-on-month growth surprised to the downside, coming in at -5.2%. Finally, the RBA Commodity Index SDR yearly growth surprised positive, coming in at 6.7%. After a bout of pronounced weakness, AUD/USD has been flat for the past couple of weeks. We believe that the Australian dollar has further downside particularly against the yen and the dollar. Australia's economy is very sensitive to the Chinese industrial cycle, as iron ore is Australia's main commodity export. However, the overleveraged industrial complex is precisely the economic sector where Chinese policymakers want to rein in credit excesses. This will curb industrial activity in China, and hurt the economies of commodity supplies like Australia. Report Links: What Is Good For China Doesn’t Always Help The World - June 29, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

New Zealand Dollar Recent data in New Zealand has been mixed: Retail sales and retail sales ex autos yearly growth both outperformed expectations, coming in at 1.1% and 1.4% respectively. Moreover, the trade balance also surprised to the upside, coming in at -4.4 billion dollars/ However, the terms of trade Index underperformed expectations, coming in at 0.6%. NZD/USD has fallen by roughly 0.8% against the dollar for the past couple of weeks. We continue to be bearish on kiwi on a cyclical basis. The combination of high U.S. rates and deleveraging in China will weigh on carry currencies like the NZD. Furthermore, we also hold a bearish view on a structural basis, given that the new government has vowed to curb immigration and add an unemployment mandate to the RBNZ, both developments which are negative for the currency. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Canadian Dollar Recent data in Canada has been mixed: Both core and headline inflation outperformed expectations, coming in at 1.6% and 3% respectively. Moreover, manufacturing shipments month-on-month growth also outperformed expectations, coming in at 1.1%. However, retail sales month-on-month growth surprised to the downside, coming in at -0.2%. USD/CAD has been flat for the past couple of weeks. We are short this cross as a hedge to our dollar bullish view, as inflationary pressures in Canada remain strong. Moreover, the CAD will continue to outperform the AUD, as the divergence between Canada's and Australia's main export markets- China and the U.S. - will persist. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Inflation Is In The Price - June 15, 2018 Rome Is Burning: Is It The End? - June 1, 2018 Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Swiss Franc Recent data in Switzerland has been mixed: Gross domestic product yearly growth outperformed expectations, coming in at 3.4%. The SVME PMI also surprised to the upside, coming in at 64.8. However, the KOF leading indicator surprised negatively, coming in at 100.3. Finally, real retail sales growth also underperformed expectations, coming in at -0.3%. EUR/CHF has risen by roughly 0.5% this past two weeks. We continue to be bearish on the franc on a long-term basis, as inflationary pressures in Switzerland are still too weak for the SNB to remove its accommodative monetary policy, or stop its currency intervention. That being said, the CHF could experience some short term upside if the sell-off in emerging markets continues. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Norwegian Krone Recent data in Norway has been mixed: Both headline and core inflation outperform expectations, coming in at 3.4% and 1.9%. Moreover, the Labour Force survey also surprised to the upside, coming in at 3.9%. However, retail sales growth underperformed expectations, coming in at 0.7%. USD/NOK has fallen by nearly 2% over the last two weeks. We are bullish on the NOK against other commodity currencies like the AUD and the NZD. This is because oil will likely outperform within the commodity space. After all, Our commodity strategist have explained at length why political risk in Iraq and Venezuela could cause a shortage of supply in the oil markets, while Chinese deleveraging in the industrial sector will weigh on base metal demand. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Swedish Krona Recent data in Sweden has been mixed: Retail sales yearly growth surprised to the downside, coming in at -1.2%. However, consumer confidence outperformed expectations, coming in at 102.6. The krona has been the best performing currency during the past two weeks, with USD/SEK falling by roughly 2% over this period. At the moment we continue to be bullish USD/SEK, as the krona is the most sensitive currency to the dollar's strength. However, on a longer term basis, we believe that inflationary pressures in Sweden will ultimately force the Riskbank to hike more than the market expects, providing support for the SEK. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

Highlights An inflation scare would initially take bond yields higher. But the higher bond yields would undermine the valuation support of global risk-assets worth several times the size of the global economy. Thereby, an inflation scare could unleash a potentially much larger disinflationary scare. And the subsequent decline in yields would exceed the original rise. Using the 10-year T-bond yield for our roadmap (because it is least impacted by the lower bound to yields) a short trip to the uplands of 3.5% would precede a longer journey down to 2%. Feature The global long bond yield has been trapped within a tight sideways channel for almost two years (Chart of the Week); the global equity market has also lacked any clear direction in recent quarters (Chart I-2). The result is that this year's defining feature for asset-class returns is that there is no defining feature! Global equities, bonds and cash have delivered near-identical returns.1 Chart Of The WeekThe Global Long Bond Yield ##br##Has Been Trapped

The Global Long Bond Yield Has Been Trapped

The Global Long Bond Yield Has Been Trapped

Chart I-2World Equities Have Drifted ##br##Sideways This Year

At Higher Bond Yields, The Correlation With Equity Prices Has Flipped From Positive To Negative

At Higher Bond Yields, The Correlation With Equity Prices Has Flipped From Positive To Negative

This is not to say that 2018 has been a dull year for investors. Far from it. But all the action has been underneath the main asset allocation decision, across sectors, regions and countries. For example, European healthcare has outperformed European banks by 35 percent; and developed market equities have outperformed emerging market equities by 15 percent (Chart I-3 and Chart I-4). Chart I-3The Main Action Has Been Across Sectors...

The Main Action Has Been Across Sectors...

The Main Action Has Been Across Sectors...

Chart I-4...And Across Regions

...And Across Regions

...And Across Regions

Unshackling Bond Yields Might Be Difficult In the major developed economies, unemployment rates keep hitting new generational lows, implying that the main labour markets are tight. Yet policy interest rates range from a crisis-level negative 0.4 percent in the euro area to just 0.75 percent in the U.K. to a modest 2 percent in the U.S. This raises the potential for an inflation scare. At any moment, the bond market might panic that central banks are well behind the (Phillips) curve.2 The spike in bond yields would of course unleash a countervailing disinflationary feedback, by cooling credit growth and credit-sensitive sectors in the economy. But this feedback would take weeks or months to take effect and to show up in the economic data. Until then, it would liberate bond yields to reach higher ground. However, there would be a more powerful and immediate feedback which would keep the shackles on bond yields. That feedback would come not from the economy, but from the financial markets themselves. In Finance 101, all investment students learn that the valuations of risk-assets depend (inversely) on bond yields. But what is less well understood is that at very low bond yields this relationship becomes exponential. Approaching the lower bound of bond yields, bonds become doubly ugly. Not only do they offer feeble returns, but the bond returns take on an unattractive asymmetry. Specifically, you can no longer make a sudden large gain, but you can still suffer a sudden deep loss. In effect, bonds become much riskier investments.3 Confronted with this increased riskiness of bonds, 'risk-assets' becomes a misnomer because risk-assets are no longer riskier than bonds! This requires risk-asset returns to collapse to the feeble return offered by bonds with no additional 'risk-premium', giving their valuations an exponential uplift (Chart I-5). The big problem is that if bond yields normalise, the process goes into sharp reverse - the lofty valuations of risk-assets must decline as exponentially as they rose. Chart I-5At Low Bond Yields ##br##The Valuation Of Equities Changes Exponentially

Trapped: Have Equities Trapped Bonds?

Trapped: Have Equities Trapped Bonds?

The global bond yield appears close to this crossover point at which risk-asset valuations become vulnerable to an exponential derating. In the past year, whenever the global bond yield has reached the upper limits of its recent range - defined by the sum of 10-year yields on the U.S. T-bond, German bund, and JGB reaching 3.5 percent - the correlation between bond yields and equities has turned sharply negative (Chart I-6). And the subsequent sell-off in equities has eventually pegged back the rise in bond yields, effectively trapping them. Chart I-6At Higher Bond Yields The Correlation With Equity Prices Has Flipped From Positive To Negative

At Higher Bond Yields The Correlation With Equity Prices Has Flipped From Positive To Negative

At Higher Bond Yields The Correlation With Equity Prices Has Flipped From Positive To Negative

But what would happen if there were an inflation scare? The answer depends on the relative sizes of the inflationary impulse compared with the disinflationary impulse that resulted from sharply lower risk-asset prices. If central banks were more concerned about the inflationary impulse, they would have to keep tightening - in which case, bond yields would be liberated to reach elevated territory. Conversely, if the bigger worry was the disinflationary impulse, central banks would quickly reverse course, and bond yields would return to the lowlands. We now explain why the disinflationary impulse from lower risk-asset prices would end up as the bigger worry. An Inflation Scare Would Be Disinflationary The current episode of elevated risk-asset valuations is not unprecedented, but there is a crucial difference. Previous episodes of elevated risk-asset valuations tended to be localised, either by geography or sector: 1990 was focussed in Japan; 2000 was focussed in the dot com related sectors; 2008 was focussed in the U.S. mortgage and credit markets and preceded the emerging market credit boom (Chart I-7). Chart I-7The Emerging Market Boom Happened After 2008

The Emerging Market Boom Happened After 2008

The Emerging Market Boom Happened After 2008

By comparison, the post-2008 global experiment with quantitative easing, and zero and negative interest rate policy has boosted the valuations of all risk-assets across all geographies and all asset-classes - global equities (Chart I-8), global credit (Chart I-9), and global real estate. This makes it considerably more dangerous, because we estimate that the total value of global risk-assets is $400 trillion, equal to about five times the size of the global economy. Chart I-8Elevated Valuations On Global Equities

Elevated Valuations On Global Equities

Elevated Valuations On Global Equities

Chart I-9Elevated Valuations On Global Credit

Elevated Valuations On Global Credit

Elevated Valuations On Global Credit

Let's say you had an investment that was priced to generate 5 percent a year over the next decade. Now imagine that the valuation boost from ultra-accommodative monetary policy capitalises all of those future returns to today. For those future returns to drop to zero, today's price must surge by 63 percent.4 If you were prudent, you might amortise today's windfall to generate the original 5 percent a year over the next decade. But if you were imprudent, you might spend a large amount of the windfall today. Now let's imagine a valuation derating moves the investment's returns back to the future. For those that had prudently amortised the original windfall, nothing has really changed and future spending patterns would not be impacted. But not everybody is prudent. For those that had imprudently spent the original windfall, future spending would inevitably suffer a nasty recession. The key takeaway is that any inflationary impulse would - through higher bond yields - undermine the valuation support of global risk-assets worth several times the size of the global economy. Thereby, it could unleash a potentially much larger disinflationary impulse. A Roadmap For An Inflation Scare The high sensitivity of risk-asset valuations to bond yields is the genesis of our 'rule of 4' strategy for equity allocation, which is based on the sum of the 10-year yields on the U.S. T-bond, German bund and JGB: Above 3.5 is the level to go to a neutral exposure to equities; above 4 is the level to go underweight. Today, our metric stands at exactly 3.5 (Chart I-10). Chart I-10The 'Rule Of 4' Is At 3.5

10. The 'Rule Of 4' Is At 3.5

10. The 'Rule Of 4' Is At 3.5

For bonds, this means that 4 on this metric is also a good level to buy a mixed portfolio of high-quality 10-year government bonds. The equivalent level for high-quality 30-year government bonds is 5.5 (using the sum of the three 30-year yields). To sum up, an inflation scare would initially take bond yields higher. But this would threaten to unleash a much larger disinflation scare, causing the subsequent decline in yields to exceed the original rise. Using the 10-year T-bond yield as an illustration - as it is least impacted by the lower bound to yields - this would suggest the following roadmap: a short trip to the uplands of 3.5% would precede a longer journey down to 2%. Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com 1 The global long bond yield is captured by the simple average of the 30-year yields on the U.S. T-bond, German bund and Japanese government bond (JGB). The global equity market is captured by the MSCI All Country World Index in local currency terms. 2 The -0.4 percent refers to the ECB deposit rate. 3 Please see the European Investment Strategy Weekly Report "The Rule Of 4 For Equities And Bonds," August 2, 2018, available at eis.bcaresearch.com. 4 5 percent compounded over ten years. Fractal Trading Model* This week’s recommended trade is an intra-commodity pair trade: short palladium/long copper. The profit target is 6% with a symmetrical stop-loss. In other trades, short euro area energy versus financials was closed at the end of its 65 trading day holding period, albeit in loss. This leaves five open trades. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-11

Long Global Basic Resources, Short Global Chemicals

Long Global Basic Resources, Short Global Chemicals

Fractal Trading Model Recommendations Equities Bond & Interest Rates Currency & Other Positions Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights German real estate and real estate equities remain a worthwhile multi-year position, especially in relative terms. The dominant stocks are Vonovia, Deutsche Wohnen, LEG, and GSW. Swedish real estate and real estate equities are likely to face harder times. The dominant stocks are Lundbergforetagen, Castellum, Fastighets, and Fabege. The structural pair-trade is long German real estate equities, short Swedish real estate equities. Italian real estate offers distressed opportunities. The long-term equity play is Covivio. We remain reluctant to own U.K. residential real estate or real estate equities. Chart of the WeekExtremes In European Real Estate

Extremes In European Real Estate

Extremes In European Real Estate

Feature Nowadays, the best way to play the relative performance of an individual economy is through real estate. Indeed, European real estate offers compelling structural opportunities for investors who want to go long, and for investors who want to go short. By contrast, the opportunities to play intra-European economic divergences through other asset-classes have become limited. Nineteen European countries share one currency and one policy interest rate; and the mega-cap companies that drive the major equity indexes are multinationals exposed to the global economy. Meaning that a stock market's relative performance is no longer defined by its home economy; it is now defined instead by its dominant sectors and stocks.1 This leaves real estate as the purest play on the domestic economy. The evidence comes from the huge divergences in real estate market performances across Europe through the past two decades (Chart I-2-Chart I-4). While house prices in Sweden and Norway have more than trebled in real terms, house prices in Germany and Italy are at the same real level today as in 1995 (Chart of the Week). Chart I-2Winners And Losers In##br## European Real Estate

Winners And Losers In European Real Estate

Winners And Losers In European Real Estate

Chart I-3Winners And Losers In##br## European Real Estate

Winners And Losers In European Real Estate

Winners And Losers In European Real Estate

Chart I-4Winners And Losers In##br## European Real Estate

Winners And Losers In European Real Estate

Winners And Losers In European Real Estate

How can German real estate be such a massive structural underperformer when the German economy has been one of Europe's star performers? The answer is that house prices take their cue from wages. German wages were suppressed for more than a decade, from which they are now playing a long catch up. A Tale Of Two Real Estate Markets: Germany And Sweden The two long-term drivers of house prices, assuming no supply bottlenecks, are: Real wages. The availability and price of bank credit. Real rents should trend higher to reflect the increasing quality of accommodation. For example, kitchens and bathrooms, heating and cooling systems and home security should all get better. In essence, the quality of accommodation benefits from productivity improvements. Of course, such improvements require investment expenditure. But a real estate investor requires a return on this investment. Therefore, rents - even after expenses - should increase in real terms. Given that house prices must maintain some long-term connection with rents, house prices should also trend higher in real terms, reflecting the improvements in home quality. But if real wages are not rising, it is impossible for tenants to absorb higher real rents, and so real rents and house prices stagnate. This describes the situation in Germany through 1995-2010 when labour market reforms resulted in real wages going nowhere, despite major gains in workers' real productivity (Chart I-5). Furthermore, as nominal adjustments to rents occur infrequently, German real rents and house prices actually fell through this extended period (Chart I-6). Chart I-5Through 1995-2010 German##br## Real Wages Stagnated...

Through 1995-2010 German Real Wages Stagnated...

Through 1995-2010 German Real Wages Stagnated...

Chart I-6...So German Real Rents And ##br##House Prices Declined

...So German Real Rents And House Prices Declined

...So German Real Rents And House Prices Declined

Since 2010, the dynamic has reversed. Needing to catch up with the economic fundamentals, German real wages, real rents and house prices have all rebounded very strongly. Nevertheless, based on the long-term connection with real productivity gains, German real rents and house prices have considerable further catch up potential. Just fifty miles across the Baltic Sea, the opposite is true. In Sweden - and Norway - house prices appear to have run well ahead of the economic fundamentals. For this, blame the central banks. In recent years, Sweden's Riksbank and the Norges Bank have had to shadow the ECB's ultra-loose policy to prevent a sharp appreciation of their currencies. The trouble is that the flood of bank credit has been absurdly inappropriate for the booming Scandinavian economies. So the ECB's policy may indeed have generated bank credit fuelled bubbles... albeit in Sweden and Norway. Real estate equities are just a leveraged play on rents - and thereby real estate capital values - because the companies take on debt to finance their property portfolios. This means that in the short term, they are (inversely) sensitive to bond yields, but in the long term the main driver is rental growth. Hence, in the German real estate market's post-2011 rebound, German real estate equities - now dominated by Vonovia, Deutsche Wohnen, LEG, and GSW - have trebled (Chart I-7), and the market relative trade is up a very pleasing 75 percent since we initiated it. Any rise in bond yields would be a short term drag, but given that real rents and house prices have further catch-up potential, the sector remains a worthwhile multi-year position, especially in relative terms. Chart I-7German Real Estate Equities ##br##Have Trebled Since 2012

German Real Estate Equities Have Trebled Since 2012

German Real Estate Equities Have Trebled Since 2012

Interestingly, Swedish real estate equities have also trebled in the post-2011 period (Chart I-8). But in Sweden's case, house prices are extended relative to the economic fundamentals. Swedish real estate equities - now dominated by Lundbergforetagen, Castellum, Fastighets, and Fabege - are likely to face harder times. Chart I-8Swedish Real Estate Equities ##br##Have Also Trebled Since 2012

Swedish Real Estate Equities Have Also Trebled Since 2012

Swedish Real Estate Equities Have Also Trebled Since 2012

Hence, the structural pair-trade is long German real estate equities, short Swedish real estate equities. Italian Real Estate Offers Distressed Opportunities Turning to Italian real estate, it has exhibited the mirror-image pattern of Germany. From the late nineties to 2008, Italian house prices almost doubled in real terms - only then to enter a ten year bear market. In recent years, Italian real wages have been growing again, raising the question: what is holding back Italian house prices? The answer is a banking system that will not lend, making it difficult for anybody to finance a house purchase (Chart I-9). Chart I-9Italian Banks Haven't Been Lending...

Italian Banks Haven't Been Lending...

Italian Banks Haven't Been Lending...

This lack of bank financing means that the natural flow of real estate that has to find a new owner is not receiving any bids. The upshot is that a long-term investor who can access financing can pick up property at highly distressed valuations, often at a fraction of the market price a few years ago. Some investors cannot remove a nagging fear about an 'Italexit' from the monetary union and the deep crisis that would follow. It is precisely because of the deep crisis that would ensue from a euro breakup that its likelihood remains low - though admittedly not zero. But even in that extreme eventuality, as long as Italy did not become an outlaw state in which property rights were dismantled, a long-term investor might still fare well. Because he would own a real asset bought at a very distressed price. Within the stock market, the real estate equity sector in Italy - just as in Germany and Sweden - has been a leveraged play on the house price cycle (Chart I-10). But there are two caveats: the sector is tiny with one dominant company, Beni Stabili; and Beni Stabili has just been taken over by the French property company Covivio. Still, now that Covivio owns a large portfolio of Italian real estate assets, it would be the appropriate equity to play this multi-year theme. And the bonus is that it offers a dividend yield of 5 percent. Chart I-10...Creating Distressed Opportunities In Italian Real Estate

...Creating Distressed Opportunities In Italian Real Estate

...Creating Distressed Opportunities In Italian Real Estate

U.K. Real Estate Faces Headwinds Finally, the recent pressure on U.K. house prices is likely to persist (Chart I-11) - with the housing market facing at least one of three potential headwinds: Chart I-11U.K. Real Estate Faces Headwinds

U.K. Real Estate Faces Headwinds

U.K. Real Estate Faces Headwinds

A disorderly Brexit, though not our central case, would pose a huge risk for the U.K. economy. On the other hand, an orderly and smooth transition to Brexit would liberate the Bank of England to hike interest rates further in 2019. Bear in mind that in the U.K., wage pressures and CPI inflation are not dissimilar to those in the U.S., where the Federal Reserve has already hiked the policy rate seven times. So it is largely the uncertainties surrounding Brexit that are staying the BoE's hands. The precarious path to leaving the EU on March 29 2019 is littered with landmines for Theresa May. Any of these landmines could trigger a snap General Election, a Jeremy Corbyn led Labour government, and the spectre of a high-end 'land value' tax. Hence, we remain reluctant to own U.K. residential real estate or real estate equities. Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com 1 For the compelling evidence, please see Charts 1-6 in the European Investment Strategy Weekly Report 'The Eight Components Of Equity Market Allocation' July 26 2018 available at eis.bcaresearch.com. Fractal Trading Model* The 30% outperformance of India versus China during the recent EM shock is technically stretched, hitting a fractal dimension that signals a potential reversal, assuming no further deterioration in news flow. On this technical basis, the countertrend trade would be long China/short India with a profit target of 9% and symmetrical stop-loss. In other trades, long platinum/short nickel reached the end of its 65 day holding period very comfortably in profit. However, short consumer services versus consumer goods hit its stop-loss. This leaves five open trades. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment's fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-12

India vs. China

India vs. China

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report "Fractals, Liquidity & A Trading Model," dated December 11, 2014, available at eis.bcaresearch.com Fractal Trading Model Recommendations Equities Bond & Interest Rates Currency & Other Positions Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights 2018 YTD Summary: Investment grade corporate debt in the developed economies has performed poorly so far in 2018, led by lagging returns in Financials and some steepening of credit curves. U.S. credit has outperformed European equivalents. These trends are likely to continue over at least the next six months. Our Sector Portfolios: Our investment grade sector model portfolios have underperformed modestly so far in 2018 (-3bps each in the U.S., euro area & U.K.) - primarily due to our overweight stance on Financials which have performed poorly. Looking Ahead: We are maintaining a neutral level of target spread risk (i.e. duration-times-spread equal that of the benchmark index) in our sector model portfolios for the U.S., euro area and U.K. We will look to reduce that spread risk on signs of a deeper global growth slowdown, which we expect will unfold in 2019. Feature Chart of the WeekReversal Of Fortune

Reversal Of Fortune

Reversal Of Fortune

The performance of investment grade (IG) corporate bonds in the developed markets, as an asset class, has been underwhelming so far in 2018. Using the total return indices from Bloomberg Barclays, IG corporates in the U.S., euro area and U.K. - the regions with the three largest corporate bond markets among the developed economies - have lost -2.0%, -0.3% and -1.1%, respectively. The numbers do not look much better when shown on an excess return basis versus duration-matched government bonds: U.S. IG -0.8%, euro area -1.2% and the U.K. -1.3%. The sluggish performance for IG corporates is a mirror image of the strong showing in 2017 when looking at credit spreads, which reached very tight levels at the end of last year (Chart of the Week). The 2017 rally left global corporates exposed to any negative shocks, of which there have been many so far in 2018 (the February VIX spike, the Q1 global growth slowdown, intensifying U.S.-China trade tensions, ongoing Fed tightening, a strengthening U.S. dollar, less dovish non-U.S. central banks, Italian politics, emerging market turmoil). Given the more challenging environment for overall corporate bond performance, the role of sector selection as a way to generate alpha, by mitigating losses from beta, is critical. In this Weekly Report, we take a brief look at IG sector performance so far this year and update our sector allocations based on our relative value models for IG corporates in the U.S., euro area and U.K. 2018 YTD Global Corporates Performance: A Down Year The major IG sector groupings for the U.S., euro area and U.K. are presented in Table 1, ranked by the 2018 year-to-date excess returns (all are shown in local currency terms). The overall index return for each region is also shown (highlighted in gray) in the table, to highlight how individual sectors have performed relative to the overall IG index. Table 12018 Year-To-Date Investment Grade Sector Returns For The U.S., Euro Area & U.K.

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

As is always the case with IG corporates, the performance of the broad Financials grouping (which includes banks, insurance companies, REITs, etc.) heavily influences the returns of the overall IG index given the large weighting of Financials within the Corporates index across all three regions. In both the euro area and U.K., the sharp underperformance of Financials seen year-to-date (-1.3% and -1.4%, respectively) has created a somewhat odd situation where the majority of sectors have outperformed the overall index. That could only happen given the large weight of Financials in the euro area index (40%) and U.K. index (43%). Financials are also a big part of the U.S. index (32%), but there is more balance in the U.S. IG index which has helped boost the "beta" return from U.S. corporates. Specifically, the weightings of the top three largest U.S. broad sector groupings - Energy (9%), Technology (8%) and Communications (9%) - are a combined 26% of the overall U.S. IG index. Those three sectors are also among upper tier of the 2018 performance table in the euro area and U.K., but only represent a combined 15% and 8%, respectively, of each region's IG index. The conclusion is that index composition has flattered the performance of U.S. IG corporates versus European equivalents, given the latter's heavier weighting in Financials. The poor performance of Financials can be attributed to flattening global government bond yield curves (which is a negative for banks) and poor returns from global credit, especially in emerging markets (which is a negative for insurers that invest in spread product). We do not anticipate either of those trends reversing anytime soon - particularly the ongoing selloff in emerging market assets - thus Financials are likely to remain a drag on corporate bond performance for at least the next 3-6 months. One other factor that has weighed on overall IG corporate performance has been the steepening of credit spread curves. The gaps between credit spreads for Baa- and A-rated corporates have widened since the end of January, most notably in the euro area and the U.K. where growth has been slower than in the fiscal-policy fueled U.S. economy (Chart 2). With Baa-rated debt now representing one-half of the IG index for the U.S., euro area and U.K. (Chart 3) - a function of rising corporate leverage - continued underperformance of lower quality sectors will negatively impact the future overall returns from IG corporates. Chart 2Spread Curves Are##BR##Steepening In Europe

Spread Curves Are Steepening In Europe

Spread Curves Are Steepening In Europe

Chart 31/2 Of Investment Grade Corporate Indices##BR##Are Now Baa-Rated

1/2 Of Investment Grade Corporate Indices Are Now Baa-Rated

1/2 Of Investment Grade Corporate Indices Are Now Baa-Rated

Looking ahead, credit investors should be wary of the potential for downgrade risk in their portfolios given the high proportion of Baa-rated debt in the IG benchmark indices. This risk will become more acute when the global business cycle runs out of steam (a 2019 story, at the earliest, in our view). Bottom Line: Investment grade corporate debt in the developed economies has performed poorly so far in 2018, led by lagging returns in Financials and some steepening of credit curves. U.S. credit has outperformed European equivalents. These trends are likely to continue over at least the next six months. Our Corporate Sector Valuation Models: Winners & Losers Our recommended IG sector allocations come from our relative value model, which measures the valuation of each individual sector compared to the overall Bloomberg Barclays corporate bond index for each region. The methodology takes each sector's individual option-adjusted spread (OAS) and regresses it in a panel regression with all other sectors in each region. The dependent variables in the model are each sector's duration, convexity (duration squared) and credit rating - the primary risk factors for any corporate bond. Using the common coefficients from that panel regression, a risk-adjusted "fair value" spread is calculated. The difference between the actual OAS and fair value OAS is our valuation metric used to inform our sector allocation ranking. The latest output from the models can be found in the tables and charts in the Appendix starting on Page 13. We also show the duration-times-spread (DTS) for each sector in those tables, which we use as the primary way to measure the riskiness (volatility) of each sector. The scatterplot charts in the Appendix show the tradeoff between the valuation residual from our model and each sector's DTS. We then apply individual sector weights based on the model output and our desired level of overall spread risk in our recommended credit portfolio. The weights are determined at our discretion and are not the output from any quantitative portfolio optimization process. The only constraints are that all sector weights must add to 100% (i.e. the portfolio is fully invested with no use of leverage) and the overall level of spread risk (DTS) must equal our desired target. That target portfolio DTS is the first decision in our discretionary allocation process, which is informed by our strategic views on corporate credit in each region. For example, if we were recommending an overweight allocation to U.S. IG corporates, then we would target a portfolio DTS that was greater than the index DTS. If we then became a bit more cautious on U.S. corporates, we could reduce the target DTS (spread risk) of our model sector portfolio while maintaining an overall overweight allocation to U.S. corporates versus U.S. Treasuries. That is exactly what we did one year ago, when we began to target a weighted DTS of all our individual sector tilts that was roughly equal to the overall IG corporate index DTS for each region (U.S. euro area, U.K.) while maintaining an overall overweight stance on global corporate credit versus government debt. More recently, we have downgraded our stance on global spread product to neutral, while continuing to favor the U.S. over Europe, in response to growing tensions from emerging markets and the brewing U.S.-China trade war.1 Chart 4Performance Of Our IG Sector Allocations

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

We last presented a performance update for our global IG corporate sector allocations back on April 12th of this year. Since then, our recommended tilts have modestly underperformed the benchmark index in excess return terms by a combined -3bps (Chart 4). This came entirely from the euro area, with both the U.S. and U.K. sector allocations simply matching the benchmark index. Year-to-date, our IG sector allocations have underperformed the benchmark by a combined -9bps in excess return terms, split equally among the U.S., euro area and U.K. This is a result entirely consistent with our long-standing stance to overweight Financials in all three regions, which continue to appear cheap in our valuation framework. Also, an increasing number of sectors had become expensive within that framework, in all three regions, so some portion of that overweight to global Financials was "by default" given that our model portfolios must be fully invested (finding value has been a persistent problem for credit investors over the past year). The return numbers for our U.S. sector allocations can be found in Table 2. Since our last update in April, the best performing sectors (in excess return terms) within our recommended tilts have all been underweights: Pharmaceuticals (+1.2bps), Electric Utilities (+1.1bps), Retailers (+0.6bps), Health Care (+0.6bps), Diversified Manufacturing (+0.5bps) and Chemicals (+0.4bps). These were fully offset, however, by underperformance from our large overweights to Energy (-4.1bps) and Financials (-2.7bps). Table 2U.S. Investment Grade Performance

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

The return numbers for our euro area sector allocations - shown here hedged into U.S. dollars as is the case when we present all our model portfolio returns - can be found in Table 3. Since our last update in April, the best performing sectors (in excess return terms) within our recommended tilts have been underweights to Transportation (+2.0bps) and Electric Utilities (+0.6bps), with underperformance coming from our underweight to Food/Beverage (-2.4bps) and overweight to Life Insurers (-3.1bps). Table 3Euro Area Investment Grade Performance

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

The return numbers for our U.K. sector allocations (again, hedged into U.S. dollars) can be found in Table 4. Since our last update in April, the best performing sectors (in excess return terms) within our recommended tilts have been our underweight to Utilities (+2.0bps) and Consumer Non-Cyclicals (+0.9bps), but this was nearly fully offset by our large overweight to Financials (-2.6bps). Table 4U.K. Investment Grade Performance

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

Despite the underperformance of our sector portfolios year-to-date, the cumulative alpha from the portfolios since we began tracking the performance of the recommendations remains positive (+2bps in the U.S., +9bps in the euro area, +42bps in the U.K.). Bottom Line: Our investment grade sector model portfolios have underperformed modestly so far in 2018 (-3bps each in the U.S., euro area & U.K.) - primarily due to our overweight stance on Financials which have performed poorly. Changes To Our Sector Model Portfolios As mentioned earlier, the first choice we make when determining the recommended sector allocations within our model portfolios is how much spread risk (DTS) to take. For the U.S., euro area and U.K., we have already been maintaining a portfolio DTS that is close to the index DTS since August 2017. After our recent decision to downgrade global spread product allocations to neutral versus government bonds, we do not feel a need to further reduce our spread risk by targeting a below-index DTS. That would likely be our next decision when we wish to get more defensive on credit, which would await evidence that global leading economic indicators are sharply slowing and/or global monetary policy is becoming restrictive. Within that neutral level of spread risk, we are making the following portfolio changes based on the updated output from our valuation models presented in the Appendix Tables on pages 13-18. The goal is to favor sectors that have a DTS close the index DTS but have positive valuation residuals from our model: U.S.: We downgrade Tobacco and Wireless to Neutral; we downgrade Paper to Underweight. Euro Area: We upgrade Transportation, Other Industrials, Natural Gas, Brokerages/Asset Managers and Finance Companies to Overweight; we upgrade Automotive, Retailers and Tobacco to Neutral; we downgrade Wireless to Neutral; we downgrade Diversified Manufacturing & Media Entertainment to Underweight. U.K.: We upgrade Health Care, Transportation and Other Industrials to Overweight; we upgrade Integrated Energy to Neutral; we downgrade Technology & Wireless to Neutral; we downgrade Metals & Mining and Supermarkets to underweight. Robert Robis, Senior Vice President Global Fixed Income Strategy rrobis@bcaresearch.com 1 Please see BCA Global Fixed Income Strategy Weekly Report, "Time To Take Some Chips Off The Table: Downgrade Global Corporate Bond Exposure To Neutral", dated June 26th 2018, available at gfis.bcaresearch.com. Appendix Appendix Table 1U.S. Corporate Sector Valuation And Recommended Allocation*

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

Appendix Chart 1U.S. Corporate Sector Risk Vs. Reward*

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

Appendix Table 2Euro Area Corporate Sector Valuation And Recommended Allocation*

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

Appendix Chart 2Euro Area Corporate Sector Risk Vs. Reward*

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

Appendix Table 3U.K. Corporate Sector Valuation And Recommended Allocation*

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

Appendix Chart 3U.K. Corporate Sector Risk Vs. Reward*

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

A Performance Update On Global Corporate Bond Sectors

A Performance Update On Global Corporate Bond Sectors

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

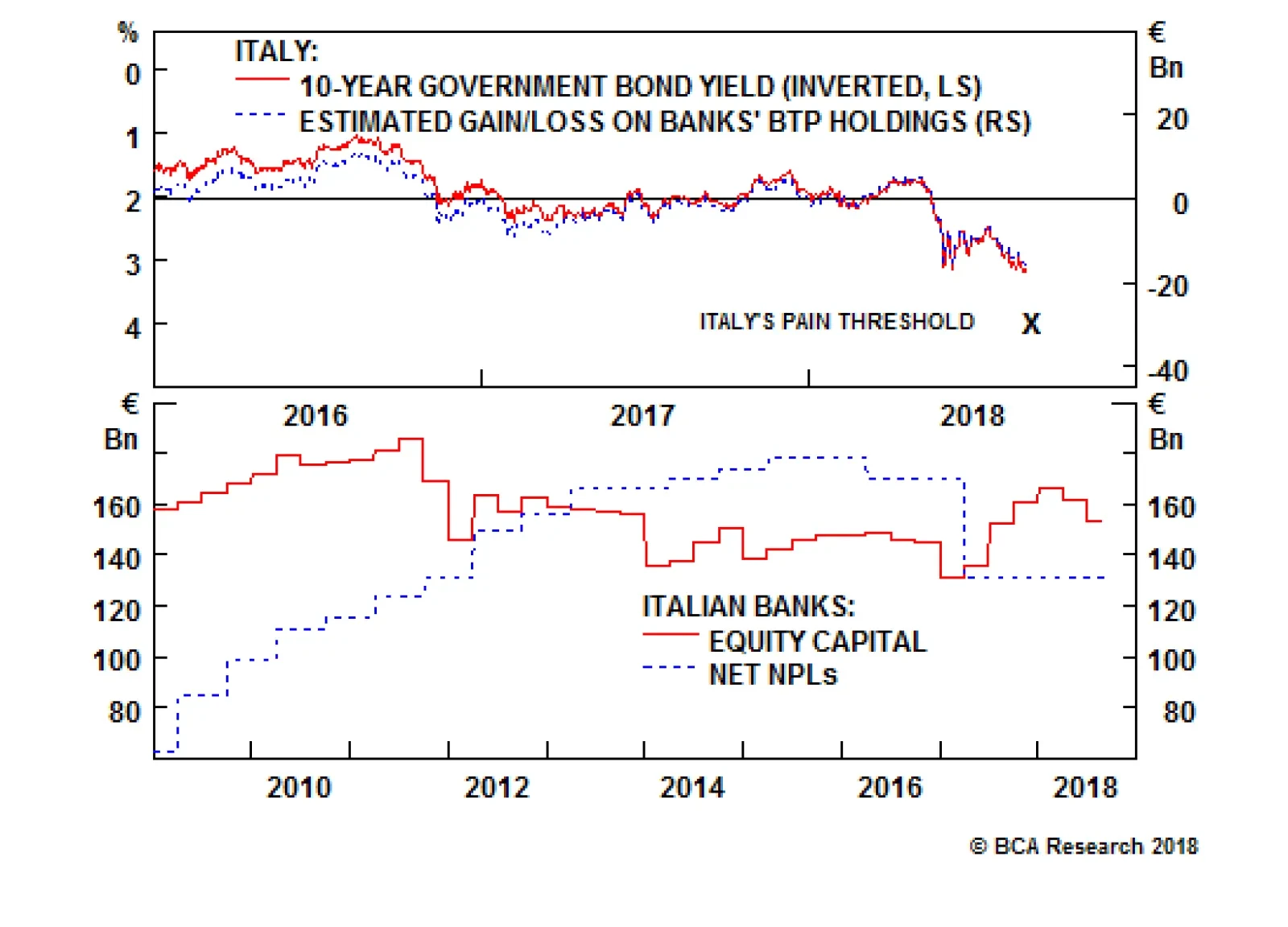

When Italian bond prices decline, it erodes the value of the €350 billion of BTPs held by Italian banks and also weakness their balance sheets. Investors start to get nervous about a bank's solvency when equity capital no longer covers net non-performing…

Highlights We remain bullish on the dollar, but no longer think that being long the greenback is the "slam-dunk" trade that it was earlier this year. A reacceleration in growth outside the U.S. and an overly dovish Fed represent the biggest risks to our constructive dollar view. China is likely to stimulate its economy, but concerns about high debt levels and malinvestment will limit the scale of any fiscal/credit stimulus. Letting the RMB slide may prove to be the preferable option. Worries about debt sustainability in Italy and EM contagion to European banks will constrain credit growth in the euro area, thus keeping the ECB in a highly dovish mode. For the time being, we favor developed market stocks over their EM peers. At the sector level, we would overweight defensives relative to deep cyclicals. U.S. stocks will outperform European stocks in dollar terms, although the performance is likely to be much more balanced in local-currency terms. The longer-term path for Treasury yields is to the upside. Nevertheless, a stronger dollar, coupled with safe-haven flows into the Treasury market, could temporarily push the 10-year yield down to 2.5% over the next few months. Feature The Dollar At A Crossroads After surging by 10% between February 1st and August 15th, the broad trade-weighted dollar has fallen by 0.9% over the past two weeks. Despite the latest setback, the greenback is still 23.2% above its 2014 lows and only 2.8% below its December 28, 2016 high (Chart 1). BCA continues to maintain a bullish view on the dollar. However, given recent market action, it is useful to stress-test our thesis in order to explore what could go wrong with it. As we discuss below, a key risk to the dollar is that global growth reaccelerates, with the U.S. once again going from leader to laggard in the global growth horserace. Global Growth And The Dollar The dollar tends to strengthen when global growth is deteriorating. Since the U.S. is a "low-beta" economy dominated by services rather than manufacturing and primary industries, an environment in which the global economy is slowing is usually one where the U.S. is outperforming the rest of the world. Chart 2 shows that there is a strong correlation between the value of the trade-weighted dollar and the difference between The Conference Board's U.S. Leading Economic Indicator (LEI) and the non-U.S. LEI. The gap between the U.S. and the non-U.S. LEI is still quite large. However, it has started to shrink recently, reflecting both a dip in the U.S. LEI as well as a small improvement in the non-U.S. LEI. The implication is that the U.S. economy is outshining the rest of the world, but the magnitude of outperformance has begun to narrow. Looking forward, the fate of the dollar will hinge on whether growth in the rest of the world can catch up with the United States. By definition, this can happen either if U.S. growth falls or non-U.S. growth rises. We examine each possibility in turn. Chart 1Despite Recent Pullback, ##br##The Dollar Is Still Close To Its 2016 High

Despite Recent Pullback, The Dollar Is Still Close To Its 2016 High

Despite Recent Pullback, The Dollar Is Still Close To Its 2016 High

Chart 2The U.S. Economy Is Still Outperforming The Rest Of The World, But The Gap Is Starting To Narrow

The U.S. Economy Is Still Outperforming The Rest Of The World, But The Gap Is Starting To Narrow

The U.S. Economy Is Still Outperforming The Rest Of The World, But The Gap Is Starting To Narrow

U.S. Growth: As Good As It Gets? The second quarter was probably the high watermark for U.S. growth for the rest of this cycle. Real GDP expanded by 4.2%, more than double most estimates of trend growth. The deceleration in payroll growth in July, a string of weak housing data releases, and the drop in the national ISM surveys alongside declines in a number of regional surveys such as the Philly Fed PMI, all point to a somewhat softer third quarter GDP growth reading. How worried should dollar bulls be? We see three reasons to downplay the negative impact on the dollar from the recent string of softer economic data. While the U.S. economy has slowed, it is still quite strong. The Bloomberg consensus forecast suggests that real GDP will increase by 3% in Q3. The Atlanta Fed's GDPNow model predicts 4.1% growth, while the New York Fed's Nowcast anticipates a more modest growth rate of 2%. The underlying drivers of aggregate demand remain supportive. U.S. financial conditions have loosened recently, thanks mainly to narrower credit spreads and higher equity prices (Chart 3). The effects of fiscal stimulus have also yet to make their way fully through the economy, especially with respect to government spending. The consumer is in great shape. The unemployment rate is near a 20-year low and the savings rate stands at a comfortable 6.7%, well above the level that the current ratio of household net worth-to-disposable income would predict (Chart 4). The housing vacancy rate is close to all-time lows, which limits the downside risk both to home prices and construction activity (Chart 5). Chart 3U.S. Financial Conditions Have Eased Recently

U.S. Financial Conditions Have Eased Recently

U.S. Financial Conditions Have Eased Recently

Chart 4The Savings Rate Has Room To Fall

The Savings Rate Has Room To Fall

The Savings Rate Has Room To Fall

Some of the apparent slowdown in U.S. growth appears to be due to intensifying supply-side constraints rather than faltering demand (Chart 6). This is important because slower growth resulting from weaker demand should, in principle, cause the Fed to moderate the pace of rate hikes, whereas slower growth resulting from an overheated economy should prompt the Fed to accelerate the pace of rate hikes. The latter is much better for the dollar than the former. Chart 5Low Housing Inventories Will ##br##Support Home Prices And Construction

Low Housing Inventories Will Support Home Prices And Construction

Low Housing Inventories Will Support Home Prices And Construction

Chart 6U.S. Economy Is Hitting Supply-Side ##br##Constraints

U.S. Economy Is Hitting Supply-Side Constraints

U.S. Economy Is Hitting Supply-Side Constraints