Euro Area

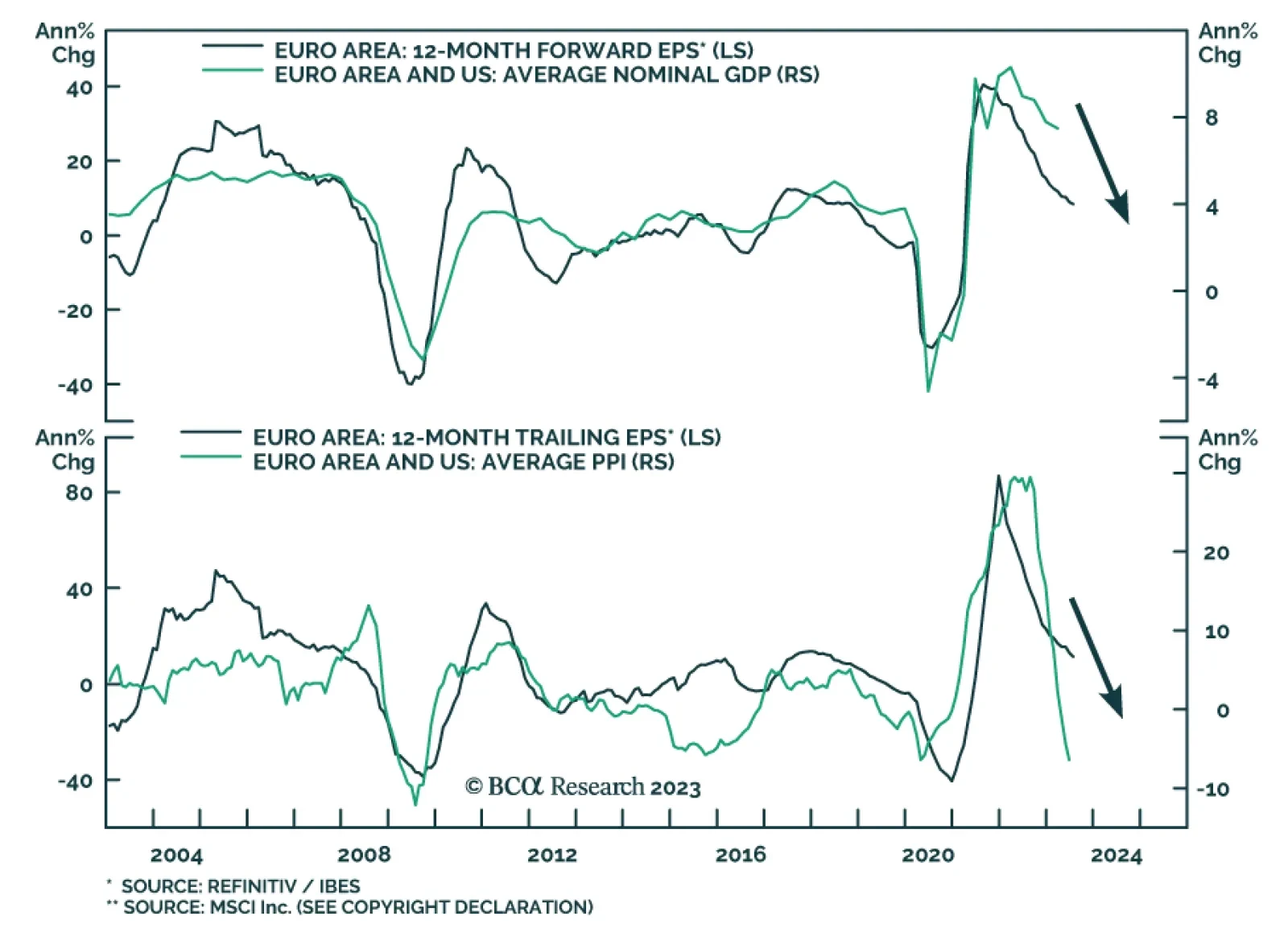

European real GDP growth is stabilizing, so why would European equities continue to trade sideways for the remainder of the year? The answer lies with nominal growth and its impact on earnings.

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.

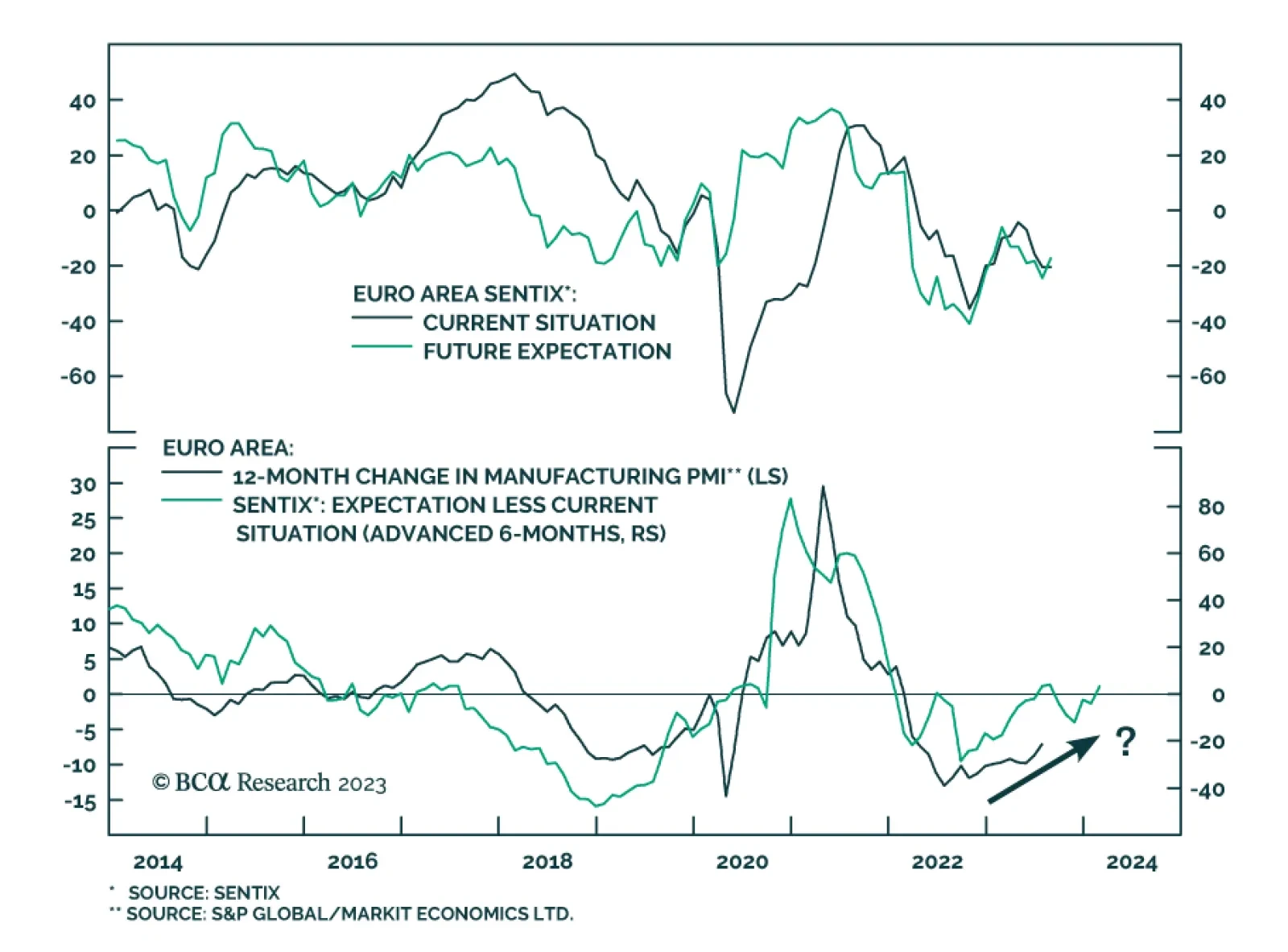

August offers an opportunity to review our key views. European growth is turning the corner and inflation is improving, but does it guarantee an imminent breakout in European stocks?

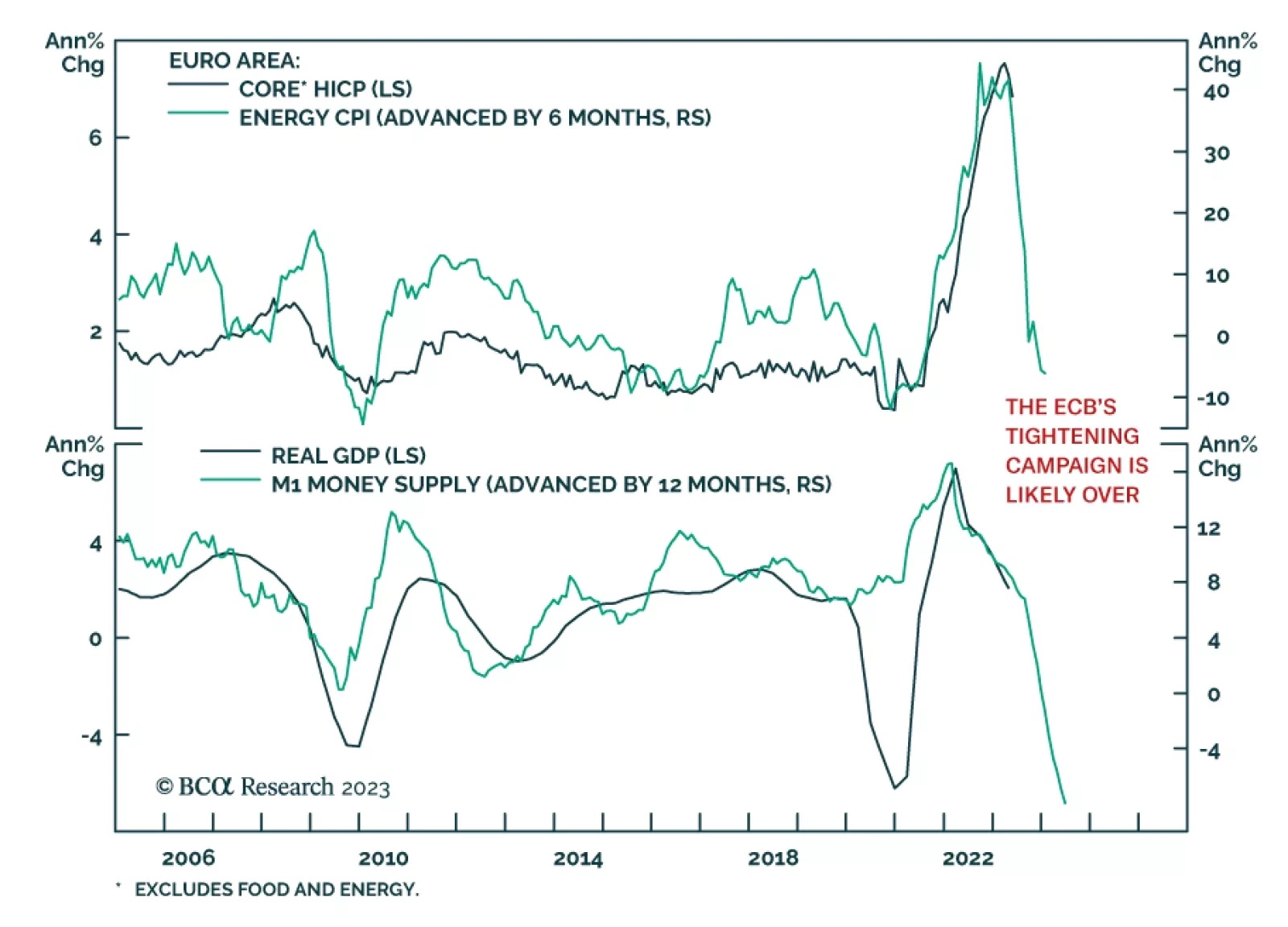

The ECB’s tone has changed decisively. Intransigent forward guidance is gone; data dependency is in. What does this transition mean for the path of European interest rates and the euro?

The DXY will continue to have near-term upside, as economic growth holds up in the US, while it deteriorates in other parts of the world. Remain constructive on the DXY at current levels, but pivot to a short position on evidence US growth is boosting the rest of the world.