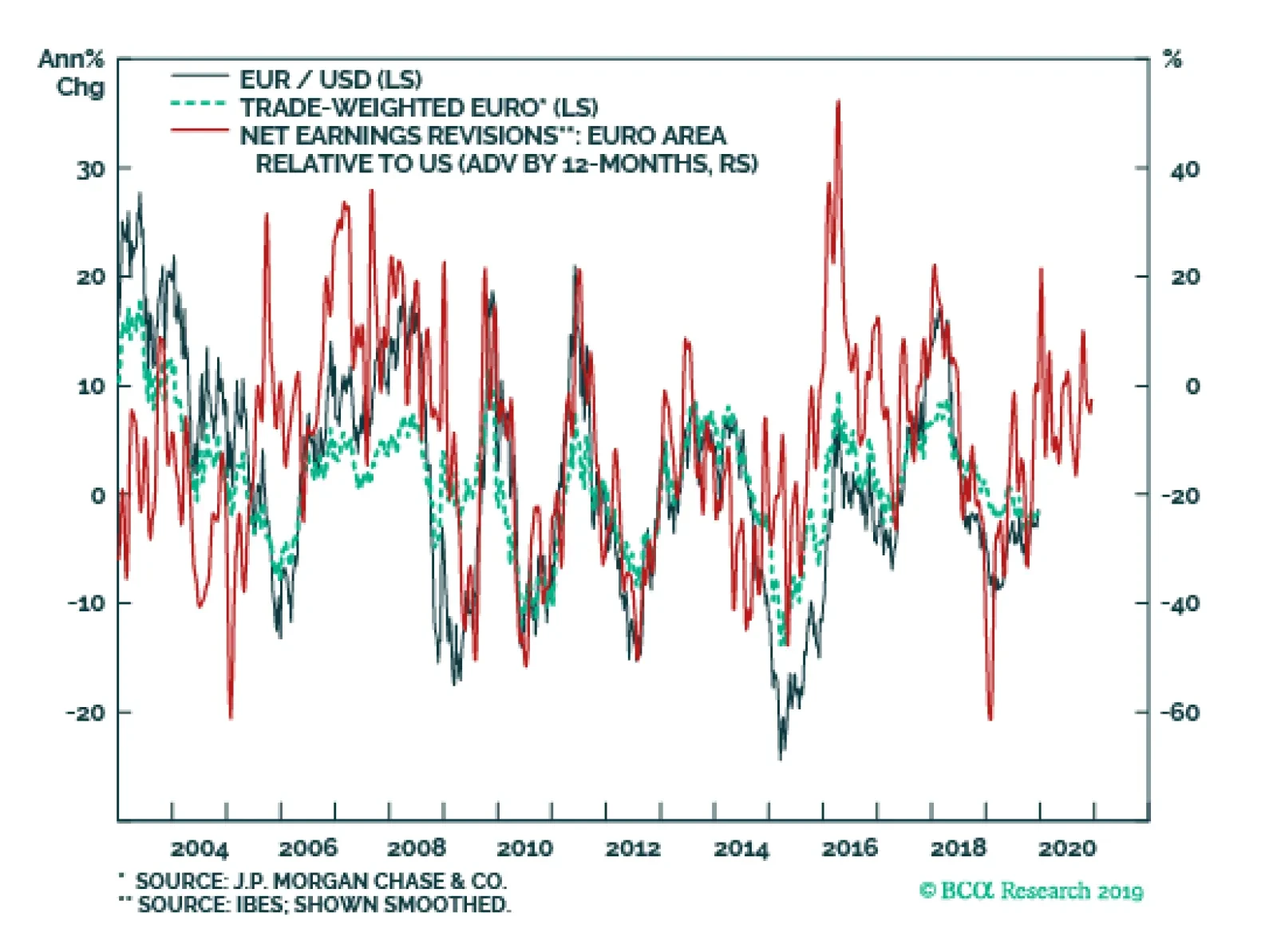

Euro Area

Our near-term target for EUR/USD is 1.18. This level will retest the downward sloping trendline in place since the Great Financial Crisis. The collapse in the euro since the financial crisis has been driven by falling growth differentials between the…

Highlights 2019 was a good year for our constraint-based method of political analysis. Trump was impeached, the trade war escalated, and China (modestly) stimulated – all as predicted. Nevertheless Trump caught us by surprise in Q2, with sanctions on Iran and tariffs on China. Our best trades were long defense stocks, gold, and Swiss bonds. Our worst trade was long rare earth miners. Feature Jean Buridan’s donkey starved to death because, faced with equal bundles of grain on both sides, it could not decide which to eat. So the legend goes. Investors face indecision all the time. This is especially the case when a geopolitical sea change is disrupting the global economy. Two or more political outcomes may seem equally plausible, heightening uncertainty. What is needed is a method for eliminating the options that require the farthest stretch. That’s what we offer in these pages, but we obviously make mistakes. The purpose of our annual report card is to identify our biggest hits and misses so we can hone our ability to combine fundamental macro and market analysis with the “art of the possible,” delivering better research and greater returns for clients. This is our last report for 2019. Next week we will publish a joint report with Anastasios Avgeriou of BCA Research’s US Equity Strategy. We will resume publication in early January. We wish all our clients a merry Christmas, happy holidays, and a happy new year! American Politics: Unsurprising Surprises Chart 1Our 2019 Forecast Held Up

Our 2019 Forecast Held Up

Our 2019 Forecast Held Up

On the whole our 2019 forecast held up very well. We argued that the global growth divergence that began in 2018 would extend into 2019 with the Fed hiking rates, a lack of massive stimulus from China, and an escalation in the US-China trade war. The biggest miss was that the Fed actually cut rates three times – addressed at length in our BCA Research annual outlook. But the bulk of the geopolitical story panned out: the US dollar, US equities, and developed market equities all outperformed as we expected (Chart 1). Geopolitical risk in the Trump era is centered on Trump himself. Beginning in 2017, we argued that the Democrats would take the House of Representatives in the midterm elections and impeach the president. Congress would not be totally gridlocked: while we argued for a government shutdown in late 2018, we expected a large bipartisan budget agreement in late 2019 and always favored the passage of the USMCA trade deal. Still, Congress would encourage Trump to go abroad in pursuit of policy victories, increasing geopolitical risks. We also argued that, barring “smoking gun” evidence of high crimes, the Republican-held Senate would acquit Trump – assuming his popularity held up among Republican voters themselves (Chart 2). These views either transpired or remain on track. The implication is that Trump-related risk continues and yet that Trump’s policies are ultimately constrained by the guardrails of the election. The latter factor helped propel the equity rally in the second half of the year. We largely sat out that rally, however. We overestimated the chances that Senator Bernie Sanders would falter and Senator Elizabeth Warren would swallow his votes, challenging former Vice President Joe Biden for the leading position in the early Democratic Party primary. We expected a significant bout of equity volatility via fears of a sharp progressive-populist turn in US policy (Chart 3). Instead, Sanders staged a recovery, Warren fell back, Biden maintained his lead, and markets rallied on other news. Chart 2Trump Will Be Acquitted

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

Chart 3Fears Of A Progressive Turn Did Not Derail The H2 Rally

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

Warren could still recover and win the nomination next year. But the Democratic Primary was not a reason to remain neutral toward equities, as we did in September and October. China’s Tepid Stimulus In recent years China first over-tightened and then under-stimulated the economy – as we predicted. But we misread the credit surge in the first quarter as a sign that policymakers had given up on containing leverage. In total this year’s credit surge amounts to 3.4% of GDP, about 1.2% short of what we expected (based on half of the 9.2% surge in 2015-16) (Chart 4). China’s credit surge was about 1.2% short of what we expected, but the direction was correct. While the government maintained easy monetary policy as expected, its actions combined with negative sentiment to snuff out the resurgence in shadow banking by mid-year (Chart 5). Chart 4China's Credit Surge Was Underwhelming

China's Credit Surge Was Underwhelming

China's Credit Surge Was Underwhelming

Still, China’s policy direction is clear – and fiscal policy is indeed carrying a greater load. The authorities are extremely unlikely to reverse course next year, so global activity should turn upward (Chart 6). Our “China Play Index” – iron ore prices, Swedish industrials, Brazilian stocks, and EM junk bonds, all in USD terms – has appreciated steadily (Chart 7). Chart 5China's Shadow Banking Remained Under Pressure

China's Shadow Banking Remained Under Pressure

China's Shadow Banking Remained Under Pressure

Chart 6Global Activity Should Turn Upward In 2020

Global Activity Should Turn Upward In 2020

Global Activity Should Turn Upward In 2020

Chart 7Our 'China Play Index' Performed Well

Our 'China Play Index' Performed Well

Our 'China Play Index' Performed Well

US-China: Underestimating Trump’s Risk Appetite We have held a pessimistic assessment of US-China relations since 2012. We rejected the trade truces agreed at the G20 summits in December 2018 and June 2019 as unsustainable. Our subjective probabilities of Trump achieving a bilateral trade agreement with China have never risen above 50%. Since September we have expected a ceasefire but not a full-fledged deal. Nevertheless we struggled with the timing of the trade war ups and downs (Chart 8). In particular we accepted China's new investment law as a sufficient concession and were surprised on May 5 when talks collapsed and Trump increased the tariffs. The lack of constraints on tariffs prevailed in 2019 but in 2020 the electoral constraint will prevail as long as Trump still has a chance of winning. Our worst trade recommendation of the year emerged from our correct view that the June G20 summit would lead to trade war escalation. We went long rare earth miners based outside of China. We expected China to follow through on threats to impose a rare earth embargo on the US in retaliation for sanctions against Chinese telecom giant Huawei. Not only did the US grant Huawei a reprieve, but China’s rare earth companies outperformed their overseas rivals. The trade went deeply into the red as global sentiment and growth fell (Chart 9). Only with global growth turning a corner have these high-beta stocks begun to turn around. Chart 8Expect A Ceasefire, Not A Full-Fledged Trade Agreement

Expect A Ceasefire, Not A Full-Fledged Trade Agreement

Expect A Ceasefire, Not A Full-Fledged Trade Agreement

Chart 9Our Worst Call: Long Rare Earth Miners

Our Worst Call: Long Rare Earth Miners

Our Worst Call: Long Rare Earth Miners

Chart 10North Korean Diplomacy Has Not Collapsed (Yet)

North Korean Diplomacy Has Not Collapsed (Yet)

North Korean Diplomacy Has Not Collapsed (Yet)

Our sanguine view on North Korea was largely offside this year. Setbacks in US negotiations with North Korea have often preceded setbacks in US-China talks. This was the case with the failed Hanoi summit in February and the inconsequential summit at the demilitarized zone in June. This could also be the case in 2020, as Washington and Pyongyang are now on the verge of breaking off talks with the latter threatening a “Christmas surprise” such as a nuclear or missile test. It is not too late to return to talks. Beijing is the critical player and is still enforcing crippling sanctions on North Korea (Chart 10). Beijing would benefit if North Korea submitted to nuclear and missile controls while the US reduced its military presence on the peninsula. We view this year as a hiccup in North Korean diplomacy but if talks utterly collapse and military tensions break out then it would undermine our view on US-China talks, Trump’s reelection odds, and US Treasuries in 2020. Hong Kong, rather than Taiwan, became the site of the geopolitical “Black Swan” that we expected surrounding Xi Jinping’s aggressive approach to domestic dissent. We have never downplayed Hong Kong. The loss of faith in the governing arrangement with the mainland began with the Great Recession and shows no sign of abating (Chart 11). We shorted the Hang Seng after the protests began, but closed at the appropriate time (Chart 12). The problem is not resolved. Also, Taiwan can test its autonomy much farther than Hong Kong and we still expect Taiwan to become ground zero of Greater China political risk and the US-China conflict. Chart 11Hong Kong Discontent Is Structural

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

Chart 12Our Hang Seng Short Is Done

Our Hang Seng Short Is Done

Our Hang Seng Short Is Done

Chart 13Trump Needs A Trade Ceasefire

Trump Needs A Trade Ceasefire

Trump Needs A Trade Ceasefire

Trump is unlikely to seek another trade war escalation given the negative impact it would have on sentiment and the economy (Chart 13). He could engage in another round of “fire and fury” saber-rattling against North Korea, as the economic impact is small, but he will prefer a diplomatic track. Taiwan, however, cannot be contained so easily if tempers flare. As we go to press it is not clear if Trump will hike the tariff on China on December 15. Some investors would point to his tendency to take aggressive action when the market gives him ammunition (Chart 14). We doubt he will, as this would be a policy mistake – possibly quickly reversed or possibly fatal for Trump. Trump’s electoral constraint is more powerful in 2020 than it was in 2019. Chart 14Trump Ceasefire Will Last As Long As Economy Is At Risk

Trump Ceasefire Will Last As Long As Economy Is At Risk

Trump Ceasefire Will Last As Long As Economy Is At Risk

Chart 15Our 'Doomsday Basket' Captured Trump's First Three Years

Our 'Doomsday Basket' Captured Trump's First Three Years

Our 'Doomsday Basket' Captured Trump's First Three Years

Our best tactical trade of the year stemmed from the geopolitical risk in Asia (and the Fed’s pause): we recommended a long gold position this summer that gained 16%. We also closed out our “Doomsday Basket” of gold and Swiss bonds, initiated in Trump’s first year, for a gain of 14% (Chart 15). Now that the market has digested Trump’s tactical retreat, we have reinitiated the gold trade as a long-term strategic hedge against both short-term geopolitical crises and the long-term theme of populism. Iran: Fool Me Once, Shame On You … This is the second year in a row that we are forced to explain our analysis of Iran – we were only half-right. Our long-held view is that grand strategy will push the US to pivot to Asia to counter China while scaling back its military activity in the Middle East. Two American administrations have confirmed this trend. That said, there is still a risk that President Trump will get entangled in Iran and that risk is growing. Global oil volatility – which spiked during the market share wars of 2014 – declined through the beginning of 2018, until the Trump administration took clearer steps toward a policy of “maximum pressure” on Iran. The constraints on Trump are obvious: the US economy is still affected by oil prices, which are set globally, and Iran can damage supply and push up prices. Therefore Trump should back down prior to the 2020 election. Yet Trump imposed sanctions, waivered on them, and then re-imposed them in May 2019 – catching us by surprise each time (Chart 16). Chart 16Trump Flip-Flopped On Iran Policy

Trump Flip-Flopped On Iran Policy

Trump Flip-Flopped On Iran Policy

Chart 17Iran Tensions Backwardated Oil Markets

Iran Tensions Backwardated Oil Markets

Iran Tensions Backwardated Oil Markets

This saga is not resolved – we are witnessing what could become a secular bull market in Iran tensions. True, a Democratic victory in 2020 could lead to an eventual restoration of the 2015 nuclear deal. True, the Trump administration could strike a deal with the Iranians (especially after reelection). But no, it cannot be assumed that the US will restore the historic 2015 détente with Iran. Within Iran the regime hardliners are likely to regain control in advance of the extremely uncertain succession from Supreme Leader Ali Khamenei and this will militate against reform and opening up. We went long Brent crude Q1 2020 futures relative to Q1 2021 to show that tensions were not resolved (Chart 17) – the attack on Saudi Arabia in September confirmed this view. And yet the oil price shock was fleeting as global supply was adequate and demand was weak. Our current long Brent spot trade is not only about Iran. Global growth is holding up and likely to rebound thanks to monetary stimulus and trade ceasefire, OPEC 2.0 has strong incentives to maintain production discipline (driven by both Saudi Arabian and Russian interests), and the Iranian conflict has led to instability in Iraq, as we expected. The UK: Not Dead In A Ditch British Prime Minister Boris Johnson proclaimed this year that he would "rather be dead in a ditch” than extend the deadline for the UK to leave the EU. The relevant constraint was that a disorderly “no deal” exit would have meant a recession, which we used as our visual illustration of why Johnson would not actually die in a ditch (Chart 18). The test was whether parliament could overcome its coordination problems when it reconvened in September, which it immediately did, prompting us to go long GBP-USD on September 6 (Chart 19). This trade was successful and we remain long GBP-JPY. Chart 18The Reason We Rejected

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

Chart 19UK Parliament Voted Down No-Deal Brexit

UK Parliament Voted Down No-Deal Brexit

UK Parliament Voted Down No-Deal Brexit

Populism faltered in Europe, as expected. As we go to press, the UK Christmas election is reported to have produced a whopping Conservative majority. This year Johnson mounted the most credible threat of a no-deal Brexit that we are ever likely to see and yet ultimately delayed Brexit. The Conservative victory will produce an orderly Brexit. The trade deal that needs to be negotiated next year will bring volatility but it does not have a firm deadline and is not harder to negotiate than Brexit itself. The UK has passed through the murkiest parts of Brexit uncertainty. Moreover, our high-conviction view that more dovish fiscal policy would be the end-result of the Brexit saga is now becoming consensus. Europe: Not The Crisis You Were Looking For The European Union was a geopolitical “red herring” in 2019 as we expected. Anti-establishment feeling remained contained. Italy remains the weakest link in the Euro Area, but the political “turmoil” of 2018-19 is the populist exception that mostly proves the rule: Europeans are not as a whole rebelling against the EU or the euro. On France, Italy, and Spain our views were fundamentally correct. Even in the European parliament, where anti-establishment players have a better chance of taking seats than in their home governments, the true Euroskeptics who want to exit the union only make up about 16% of the seats (Chart 20). This is up from 11% prior to the elections in May this year. Chart 20Euroskepticism Was Overstated

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

Yet the European political establishment is losing precious time to prepare for the next wave of serious agitation, likely when a full-fledged recession comes. Chart 21Trump Did Not Pile Tariffs Onto Auto Sector

Trump Did Not Pile Tariffs Onto Auto Sector

Trump Did Not Pile Tariffs Onto Auto Sector

Germany is experiencing a slow transition from the long reign of Angela Merkel, whose successor has plummeted in opinion polls. The shock of the global slowdown – particularly heavy in the auto sector (Chart 21) – hastened Germany’s succession crisis. Chart 22Overstated EU Political Risk, Understated Chinese Risk

Overstated EU Political Risk, Understated Chinese Risk

Overstated EU Political Risk, Understated Chinese Risk

There is a silver lining: this shock is forcing the Germans to reckon with de-globalization. Attitudes across the country are shifting on the critical question of fiscal policy. Even the conservative Christian Democrats are loosening their belts in the face of the success of the Green Party and a simultaneous change in leadership among the Social Democrats to embrace bigger spending. The Trump administration refrained from piling car tariffs onto Europe amidst this slowdown in the automobile sector and overall economy. We expected this delay, as there is little support in the US for a trade war with Europe, contra China, and it is bad strategy to fight a two-front war. But if the US economy recovers robustly and Trump is emboldened by a China deal then this risk could reignite in future. With European political risk overstated, and Chinese mainland risk understated, we initiated a long European equities relative to Chinese equities trade (Chart 22), as recommended by our colleagues at BCA Research European Investment Strategy. And now we are initiating the strategic long EUR/USD recommendation that we flagged in September with a stop at 1.18. Japan: Shinzo Abe Has Peaked Japanese Prime Minister Shinzo Abe is still in power and still very popular, whether judged by the average prime minister in modern memory or his popular predecessor Junichiro Koizumi. But he is at his peak and 2019 did indeed mark the turning point – it is all downhill from here. First, he lost his historic double super-majority in the Diet by falling to a mere majority in the upper house (Chart 23). He is still capable of revising the constitution, but now it is now harder – and the high water mark of his legislative power has been registered. Chart 23Abe Lost His Double Super Majority

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

Chart 24Consumption Tax Hike Shows Limits Of Abenomics

Consumption Tax Hike Shows Limits Of Abenomics

Consumption Tax Hike Shows Limits Of Abenomics

Second, he proceeded with a consumption tax from 8% to 10% that predictably sent the economy into a tailspin given the global slowdown (Chart 24). We thought the tax hike would be delayed, but Abe opted to hike the tax and then pass a stimulus package to compensate. This decision further supports the view that Abe’s power will decline going forward. It is now incontrovertible that the Liberal Democrats are eschewing a radical plan of debt monetization in which they coordinate ultra-dovish fiscal policy with ultra-dovish monetary policy. “Abenomics” has not necessarily failed but it is a fully known quantity. Abe will next preside over the 2020 summer Olympics and prepare to step down as Liberal Democratic party leader in September 2021. It is conceivable he will stay longer, but the likeliest successors have been put into cabinet positions, including Shinjiro Koizumi, son of the aforementioned, whom we would not rule out as a future prime minister. Constitutional revision or a Russian peace deal could mark the high point of his premiership, but the peak macro consequences have been felt. Japan suffered a literal and figurative earthquake in 2011. Over the long run Tokyo will resort to more unorthodox economic policies and redouble its efforts at reflation. But not until the external environment demands it. This suggests that the JPY-USD is a good hedge against risks to the cyclically bullish House View in 2020 and supports an overweight stance on Japanese government bonds. Emerging Markets: Notable Mentions India: We were correct that Narendra Modi would be reelected as prime minister, but we did not expect that he would win a single-party majority for a second time (Chart 25). The risk is that this result leads to hubris – particularly in foreign policy and domestic social policy – rather than accelerating structural reform. But for now we remain optimistic about reform. Chart 25

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

How Are We Doing? ... Geopolitical Strategy 2019 Report Card

East Asia: We are optimistic on Southeast Asia in the context of US-China competition. But we proved overly optimistic on Malaysia and Indonesia this year, while we missed a chance to close our long Thai equity trade when it would have been very profitable to do so. Turkey: Domestic political challenges to President Recep Tayyip Erdoğan have led to a doubling down on unorthodox monetary policy and profligate fiscal policy, as expected. Early in the year we advised clients that Erdoğan would delay deployment of the Russian S-400 air defense system in deference to the US but it quickly became clear that this was not the case. Thus we correctly anticipated the sharp drop in the lira over the autumn (Chart 26). The US-Turkey relationship continues to fray and additional American sanctions are likely. Russia: President Vladimir Putin focused on maintaining domestic stability amid tight fiscal and monetary policy in 2019. This solidified our positive relative view of Russian currency and equities (Chart 27). But it also highlighted longer-term political risks. We expect this trend to continue, but by the same token Russia is a potential “Black Swan” risk in 2020. Chart 26The Lira's Autumn Relapse

The Lira's Autumn Relapse

The Lira's Autumn Relapse

Chart 27Russia's Eerie Quiet In 2019

Russia's Eerie Quiet In 2019

Russia's Eerie Quiet In 2019

Venezuela: Venezuela’s President Nicolas Maduro eked out another year of regime survival in 2019 despite our high-conviction view since 2017 that he would be finished. However, the economy is still collapsing and Russian and Chinese assistance is still limited (Chart 28). Before long the military will need to renovate the regime, even if our global growth and oil outlook for next year is positive for the regime on the margin. Chart 28Maduro Clung To Power

Maduro Clung To Power

Maduro Clung To Power

Chart 29Our 2019 Winner: Global Defense Stocks

Our 2019 Winner: Global Defense Stocks

Our 2019 Winner: Global Defense Stocks

Brazil: We were late to the Brazilian equity rally. While we have given the Jair Bolsonaro administration the benefit of the doubt, a halt to structural reforms in 2020 would prove us wrong. Our worst trade of the year was long rare earth miners, mentioned above. Our best trade was long global defense stocks (Chart 29), a structural theme stemming from the struggle of multiple powerful nations in the twenty-first century. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Ekaterina Shtrevensky Research Analyst ekaterinas@bcaresearch.com Jingnan Liu Research Associate jingnan@bcaresearch.com Marko Papic Consulting Editor marko@bcaresearch.com

Dear Client, In lieu of our regular report next week, I will be hosting a webcast on Wednesday, December 18th at 10:00 AM EST, where I will discuss the major investment themes and views I see playing out for 2020. This will be the last Global Investment Strategy report of 2019, with publication resuming early next year. On behalf of the entire Global Investment Strategy team, I would like to wish you a Merry Christmas, Happy Holidays, and a Healthy New Year! Best regards, Peter Berezin, Chief Global Strategist Overall Investment Strategy: Global growth should accelerate in 2020. Favor stocks over bonds. A more defensive stance will be appropriate starting in late 2021. Equities: Upgrade non-US equities to overweight at the expense of their US peers. Cyclical stocks, including financials, will outperform defensives. Fixed Income: Central banks will stay dovish, but bond yields will nevertheless rise modestly thanks to stronger global growth. Favor high-yield corporate credit over investment grade and sovereigns. Currencies: The US dollar will weaken in 2020 against EUR, GBP, CAD, AUD, and most EM currencies. The dollar will be flat against the yen and the Swiss franc. Commodities: Oil and industrial metals prices will move higher. Gold prices will be range-bound next year, but should rally in 2021 once inflation finally breaks out. GIS View Matrix

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Strategy Outlook – 2020 Key Views: Full Speed Ahead

I. Global Macro Outlook Stronger Global Growth Ahead We turned bullish on global equities last December after temporarily moving to the sidelines in the summer of 2018. Last month, we increased our procyclical bias by upgrading non-US stocks within our recommended equity allocation at the expense of their US peers. The decision to upgrade non-US equities stems from our expectation that global growth will strengthen in 2020. Global financial conditions have eased sharply this year, largely due to the dovish pivot by many central banks. Monetary policy affects the economy with a lag. This is one reason why the net number of central banks cutting rates has historically led global growth by about 6-to-9 months (Chart 1). Chart 1The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

In addition, there is mounting evidence that the global manufacturing cycle is bottoming out (Chart 2). The “official” Chinese PMI produced by the National Bureau of Statistics rose above 50 in November for the first time since May. The private sector Caixin manufacturing PMI has been improving for five consecutive months. The euro area manufacturing PMI increased over the prior month, led by gains in Germany and France. Chart 2A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

Chart 3The Auto Sector Is Showing Signs Of Life (I)

The Auto Sector Is Showing Signs Of Life (I)

The Auto Sector Is Showing Signs Of Life (I)

The PMI data for the US has been mixed. The ISM manufacturing index weakened in November. In contrast, the Markit PMI rose to a seven-month high. Despite its shorter history, we tend to give the Markit PMI more credence. It is based on a larger sample of companies and has sector weights that closely match the actual composition of US output. As such, the Markit PMI is better correlated with hard data on manufacturing production, employment, and factory orders. The auto sector has been particularly hard hit during this manufacturing downturn. Fortunately, the industry is showing signs of life. The Markit euro area auto sector PMI has rebounded, with the new orders-to-inventory ratio moving back into positive territory for the first time since the autumn of 2018. US banks stopped tightening lending standards for auto loans in the third quarter. They are also reporting stronger demand for vehicle financing (Chart 3). In China, vehicle production and sales are improving on a rate-of-change basis (Chart 4). Both automobile ownership and vehicle sales in China are still a fraction of what they are in most other economies, suggesting further upside for sales (Chart 5). Chart 4The Auto Sector Is Showing Signs Of Life (II)

The Auto Sector Is Showing Signs Of Life (II)

The Auto Sector Is Showing Signs Of Life (II)

Chart 5China: Structural Outlook For Autos Is Bright

China: Structural Outlook For Autos Is Bright

China: Structural Outlook For Autos Is Bright

Trade War Uncertainty The trade war remains the biggest risk to our sanguine view on global growth. As we go to press, rumors are swirling that the US and China have reached a “Phase One” trade deal that would cancel the scheduled December 15th tariff hike and roll back as much as half of the existing tariffs. If this were to occur, it would be consistent with our expectation of a trade truce. Nevertheless, it is impossible to be certain about how things will unfold from here. The best we can do is think through the incentives that both sides face and assume they will act in their own self-interest. For President Trump, the key priority is to get re-elected next year. Trump generally gets poor grades from voters on most issues. The one exception is the economy. Rightly or wrongly, the majority of voters approve of his handling of the economy (Chart 6). An escalation of the trade war would hurt the US economy, especially in a number of Midwestern states that Trump needs to win to remain president (Chart 7). Chart 6Trump Gets Reasonably High Marks On His Handling Of The Economy, But Not Much Else

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Chart 7Economic Health Of The US Midwest Matters For Trump

Economic Health Of The US Midwest Matters For Trump

Economic Health Of The US Midwest Matters For Trump

A resurgence in the trade war would also hurt Trump’s credibility. The point of the tariffs was not simply to raise revenue; it was to get China to the negotiating table. As a self-described master negotiator, President Trump now has to produce a “great” deal for the American people. If he had finalized an agreement with China a year or two ago, he would currently be on the hook for showing that it resulted in a smaller trade deficit. But with the presidential election only a year away, he can semi-credibly claim that the trade balance will only improve after he is re-elected. For their part, the Chinese would rather grapple with Trump now than face him after the election when he will no longer be constrained by re-election pressures. China would also like to avoid facing someone like Elizabeth Warren or Bernie Sanders, who may insist on including stringent environmental and human rights provisions in any trade deal. At least with Trump, the Chinese know that they are getting someone who is focused on commercial issues. Contrary to most media reports, there is a fair amount of overlap between what Trump wants and what the Chinese themselves would like to achieve. For example, as China has moved up the technological ladder, many Chinese companies have begun to complain about intellectual theft by their domestic rivals. Thus, strengthening intellectual property protection has become a priority for Chinese officials. Along the same vein, China aspires to transform the RMB into a reserve currency. A country cannot have a reserve currency unless it also has an open capital account. Hence, financial market liberalization must be part of China’s long-term reform strategy. These mutual interests between the US and China could provide the basis for a trade truce. The Changing Nature Of Chinese Stimulus Chart 8China: Credit Growth Is Only A Few Percentage Points Above Nominal GDP Growth

China: Credit Growth Is Only A Few Percentage Points Above Nominal GDP Growth

China: Credit Growth Is Only A Few Percentage Points Above Nominal GDP Growth

If a détente in the trade war is reached, will this prompt China to go back to its deleveraging campaign? We do not think so. For one thing, there can be no assurance that a trade truce will last. Thus, China will want to maintain enough stimulus as an insurance policy. In addition, credit growth is currently running only a few percentage points above nominal GDP growth (Chart 8). With the ratio of credit-to-GDP barely rising, there is little need to bring credit growth down much from current levels. This does not mean that the Chinese authorities will allow credit growth to increase significantly further. Instead, the authorities will continue shifting the composition of credit growth from the riskier shadow banking sector to the safer formal banking sector, while increasingly leaning on fiscal policy to buttress growth. One of the developments that has gone largely unnoticed by investors this year is that China’s general government deficit has climbed from around 3% of GDP in mid-2018 to 6.5% of GDP at present (Chart 9). Some of this stimulus has been used to finance tax cuts for households. Some of it has also been used to finance infrastructure spending, which requires imports of raw materials and capital goods. As a result of this fiscal easing, the combined Chinese credit/fiscal impulse has risen to a two-year high. It leads global growth by about nine months (Chart 10). Chart 9China Has Been Stimulating, Fiscally

China Has Been Stimulating, Fiscally

China Has Been Stimulating, Fiscally

Chart 10Chinese Stimulus Should Boost Global Growth

Chinese Stimulus Should Boost Global Growth

Chinese Stimulus Should Boost Global Growth

Europe On The Upswing Chart 11Euro Area Growth: The Good, The Bad, And The Ugly

Euro Area Growth: The Good, The Bad, And The Ugly

Euro Area Growth: The Good, The Bad, And The Ugly

Chart 12German Economy: Some Green Shoots

German Economy: Some Green Shoots

German Economy: Some Green Shoots

The weakness in euro area growth this year has been concentrated in Germany and Italy. France and Spain have actually grown at a trend-like pace (Chart 11). Germany should benefit from stronger global growth and a recovery in automobile production next year. The recent rebound in the German PMI, as well as improvements in the expectations components of the IFO, ZEW, and Sentix surveys are all encouraging in this regard (Chart 12). Italy should also gain from an easing in financial conditions and receding political risks (Chart 13). The Italian 10-year government bond yield has fallen from a high of 3.69% in October 2018 to 1.23% at present. Chart 13Easing Financial Conditions And Less Political Uncertainty Will Help Italy

Easing Financial Conditions And Less Political Uncertainty Will Help Italy

Easing Financial Conditions And Less Political Uncertainty Will Help Italy

Chart 14Euro Area Fiscal Thrust

Euro Area Fiscal Thrust

Euro Area Fiscal Thrust

Fiscal policy across the euro area is also turning more stimulative. The fiscal thrust in the euro area rose to 0.4% of GDP this year mainly due to a somewhat larger budget deficit in France (Chart 14). The thrust should remain positive in 2020. Even in Germany, fiscal policy should loosen. Faster wage growth in Germany is eroding competitiveness relative to the rest of the euro area (Chart 15). That could force German policymakers to ratchet up fiscal stimulus in order to support demand. Already, the Social Democrats are responding to poor electoral performance by adopting a more proactive fiscal policy, hoping to stop the loss of votes to the big spending Greens. Chart 15Germany: Faster Wage Growth Eroding Competitiveness Relative To The Rest Of The Euro Area

Germany: Faster Wage Growth Eroding Competitiveness Relative To The Rest Of The Euro Area

Germany: Faster Wage Growth Eroding Competitiveness Relative To The Rest Of The Euro Area

Chart 16Boris Johnson Won't Pursue A No-Deal Brexit

Boris Johnson Won't Pursue A No-Deal Brexit

Boris Johnson Won't Pursue A No-Deal Brexit

The UK economy should start to recover next year as Brexit uncertainty fades and fiscal policy turns more stimulative. Exit polls suggest that the Conservatives will command a majority government following today's election. There is not enough appetite within the Conservative party for a no-deal Brexit (Chart 16). As such, today's victory will allow Prime Minister Boris Johnson to push his proposed deal through Parliament. It will also allow him to fulfill his pledge to pass a budget that boosts spending. Japan: Own Goal Japan has been hard hit by the global growth slowdown, given its close ties to its Asian neighbors, namely China. Add on a completely unnecessary consumption tax hike, and it is no wonder the economy has been faltering. Despite widespread weakness, there have been some very preliminary signs of improvement of late: The manufacturing PMI ticked up in November, while the services PMI rose back above 50. Consumer confidence also moved up to the highest level since June. Furthermore, Prime Minister Abe announced a multi-year fiscal package worth approximately 26 trillion yen. The headline number grossly overstates the size of the stimulus because it includes previously announced measures as well as items such as land acquisition costs that will not directly benefit GDP. Nevertheless, the package should still boost growth by about 0.5% next year, offsetting part of the drag from higher consumption taxes. US: Chugging Along Despite the slowdown in global growth, a stronger dollar, and the trade war, US real final demand is on track to grow by 2.5% this year (Chart 17). This is above the pace of potential GDP growth of 1.7%-to-2%. Chart 17Underlying US Growth Remains Above Trend

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Strategy Outlook – 2020 Key Views: Full Speed Ahead

The Fed’s 75 basis points of rate cuts has moved monetary policy even further into accommodative territory. Not surprisingly, residential housing – the most interest rate-sensitive part of the economy – has responded favorably (Chart 18). While the tailwind from lower mortgage rates will dissipate by next summer, we do not anticipate much weakness in the housing market. This is because the inventory levels and vacancy rates remain near record-low levels (Chart 19). The shortage of homes should buttress both construction and prices. Chart 18US Housing: On Solid Ground (I)

US Housing: On Solid Ground (I)

US Housing: On Solid Ground (I)

Chart 19US Housing: On Solid Ground (II)

US Housing: On Solid Ground (II)

US Housing: On Solid Ground (II)

Strong labor and housing markets will support consumer spending, which represents nearly 70% of the economy. Business capital spending should also benefit from lower rates, receding trade tensions, and rising wages which are making firms increasingly eager to automate. II. Financial Markets Global Asset Allocation We argued in the section above that global growth should rebound next year thanks to easier financial conditions, an upturn in the global manufacturing cycle, a detente in the trade war, and modest Chinese stimulus. Chart 20 shows that stocks usually outperform bonds when global growth is accelerating. This occurs partly because corporate earnings tend to rise when growth picks up. BCA’s US equity strategy team expects S&P 500 EPS to increase by 5% next year if global growth merely stabilizes. An acceleration in global growth would surely lead to even stronger earnings growth. On the flipside, investors also tend to price out rate cuts (or price in rate hikes) when growth is on the upswing, resulting in lower bond prices (Chart 21). Chart 20Stocks Usually Outperform Bonds When Global Growth Is Accelerating

Stocks Usually Outperform Bonds When Global Growth Is Accelerating

Stocks Usually Outperform Bonds When Global Growth Is Accelerating

Chart 21Improving Global Growth Boosts Earnings Growth...And Expectations Of Rate Hikes

Improving Global Growth Boosts Earnings Growth...And Expectations Of Rate Hikes

Improving Global Growth Boosts Earnings Growth...And Expectations Of Rate Hikes

Relative valuations also favor stocks over bonds. Despite the stock market rally this year, the MSCI All-Country World Index currently trades at a reasonable 15.8-times forward earnings. This is below the forward PE ratio of 16.7 reached in January 2018 and even below the forward PE ratio of 16.4 hit in May 2015. Analysts expect global EPS to increase by 10% next year, below the historic 12-month expectation of 15% (Chart 22). In contrast to most years when analyst forecasts prove to be wildly overoptimistic, the current EPS forecast is likely to be met. Chart 22Analyst Expectations Are Not Wildly Optimistic

Analyst Expectations Are Not Wildly Optimistic

Analyst Expectations Are Not Wildly Optimistic

Chart 23Equity Risk Premium Remains Quite Elevated

Equity Risk Premium Remains Quite Elevated

Equity Risk Premium Remains Quite Elevated

If one inverts the PE ratio, one can calculate an earnings yield for global equities of 6.3%. One can then calculate the implied equity risk premium (ERP) by subtracting the real long-term bond yield from the earnings yield. As Chart 23 illustrates, the ERP remains quite elevated by historic standards. Some observers might protest that the ERP is elevated mainly because bond yields are so low. If low bond yields are discounting very poor economic growth prospects, perhaps today’s PE ratio should be lower than it actually is? The problem with this argument is that growth prospects are not so bad. The IMF estimates that global growth will be slightly above its post-1980 average over the next five years (Chart 24). While trend growth is falling in both developed and emerging economies, the rising share of faster-growing emerging markets in global GDP is helping to prop up overall growth. Chart 24The Trend In Global Growth Has Remained Steady Thanks To Faster-Growing EM

The Trend In Global Growth Has Remained Steady Thanks To Faster-Growing EM

The Trend In Global Growth Has Remained Steady Thanks To Faster-Growing EM

Sector And Regional Equity Allocation US stocks have outperformed their overseas peers by 10% year-to-date and by 137% since 2008. About half of the outperformance of US equities since the Great Recession was due to faster sales-per-share growth, a third was due to stronger margin growth, and the rest was due to relative PE expansion (Chart 25). Chart 25Faster Sales Growth, Rising Margins, And Relative PE Expansion Helped Drive US Outperformance Over The Past Decade

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Strategy Outlook – 2020 Key Views: Full Speed Ahead

It is worth noting that the outperformance of US stocks is a fairly recent phenomenon. Between 1970 and 2008, European equity prices and EPS actually rose slightly faster than in the US (Chart 26). EM stocks also outperformed the US in the decade leading up to the Global Financial Crisis. Chart 26US Earnings Have Not Always Outpaced Their Peers

US Earnings Have Not Always Outpaced Their Peers

US Earnings Have Not Always Outpaced Their Peers

We expect US stocks to rise in 2020 by about 5%-to-10%, but to lag their foreign peers in common-currency terms. There are four reasons for this: Sector skews favor non-US equities. Cyclical stocks tend to outperform defensives when global growth is strengthening and the US dollar is weakening (Chart 27). Cyclical sectors are overrepresented outside the US. We would include financials in our definition of cyclicals. Faster global growth next year will lift long-term bond yields. Since central banks are unlikely to raise rates, yield curves will steepen. Steeper yield curves will boost net interest margins, thus helping bank shares (Chart 28). European banks are more dependent on the spread between lending and borrowing rates than US banks, since the latter derive more of their profits from fees. Non-US stocks are quite a bit cheaper than their US peers. The forward PE for US equities currently stands at 18.1, well above the forward PE of 13.6 for non-US equities. Other valuation measures reveal an even bigger premium on US stocks (Chart 29). Differences in sector weights account for about a quarter of the valuation gap between the US and the rest of the world. The rest of the gap is due to cheaper valuations within sectors. Financials, for example, are notably less expensive in the rest of the world, particularly in Europe (Chart 30). The valuation gap between the US and the rest of the world is even starker if we compare earnings yields with bond yields. Since bond yields are lower outside the US, the implied equity risk premium is significantly higher for non-US stocks. Profit margins have less scope to rise in the US than in the rest of the world. According to MSCI data, net operating margins currently stand at 10.3% in the US compared to 7.9% abroad. Unlike in the US, margins in Europe and EM are still well below their pre-recession peaks (Chart 31). While US margins are unlikely to fall next year thanks to stronger global growth, rising wage growth will negatively impact profits in some labor-intensive industries. Labor slack is generally greater abroad, which should limit cost pressures. Uncertainty over the US election is likely to limit the gains to US equities. All of the Democratic frontrunners have pledged to roll back the 2017 Tax Cuts and Jobs Act to one degree or another. A full repeal of the Act would reduce S&P 500 EPS by about 10%. While such a dramatic move is far from guaranteed – for starters, it would require that the Democrats gain control of both the White House and the Senate – it does pose a risk to investors. The same goes for increased regulatory actions, which Senators Sanders and Warren have both vocally championed. Chart 27Cyclicals Do Well Versus Defensives When Global Growth Is Strengthening And The US Dollar Is Weakening

Cyclicals Do Well Versus Defensives When Global Growth Is Strengthening And The US Dollar Is Weakening

Cyclicals Do Well Versus Defensives When Global Growth Is Strengthening And The US Dollar Is Weakening

Chart 28Steeper Yield Curves Help Financials

Steeper Yield Curves Help Financials

Steeper Yield Curves Help Financials

Chart 29US Equities Are More Expensive Than Stocks Abroad

US Equities Are More Expensive Than Stocks Abroad

US Equities Are More Expensive Than Stocks Abroad

Chart 30European Financials Trade At A Substantial Discount To Their US Peers

European Financials Trade At A Substantial Discount To Their US Peers

European Financials Trade At A Substantial Discount To Their US Peers

Chart 31Profit Margins Have Less Scope To Rise In The US Than In The Rest Of The World

Profit Margins Have Less Scope To Rise In The US Than In The Rest Of The World

Profit Margins Have Less Scope To Rise In The US Than In The Rest Of The World

Within the non-US universe, euro area stocks have the most upside potential. In contrast, we see less scope for Japanese stocks to outperform the global benchmark because of uncertainties over the impact of the consumption tax hike on domestic demand. In addition, a weaker trade-weighted yen next year will annul the currency translation gains that unhedged equity investors can expect to receive from other non-US stock markets. Lastly, the passage of a new investment law that requires investors wishing to “influence management” to receive prior government approval could cast a pall over recent efforts to improve corporate governance in Japan. Fixed Income Chart 32Inflation Excluding Shelter Has Been Muted

Inflation Excluding Shelter Has Been Muted

Inflation Excluding Shelter Has Been Muted

Chart 33Long-Term Bond Yields Will Move Higher As Faster Growth Pushes Up Estimates Of The Neutral Rate

Long-Term Bond Yields Will Move Higher As Faster Growth Pushes Up Estimates Of The Neutral Rate

Long-Term Bond Yields Will Move Higher As Faster Growth Pushes Up Estimates Of The Neutral Rate

Central banks will remain on the sidelines next year. Inflation is still running well below target in most economies. Even in the US, where slack has largely been absorbed and wage growth has risen, core inflation excluding housing has averaged only 1.2% over the past five years (Chart 32). Nevertheless, long-term bond yields will still move higher next year as investors revise up their estimate of the neutral rate in response to faster growth (Chart 33). On a regional basis, BCA’s fixed-income experts favor low-beta bond markets (Chart 34). Japanese bonds have a very low beta to the overall Barclays Global Treasury index because inflation expectations are quite depressed and the Bank of Japan will actively intervene to prevent yields from rising. On a USD currency-hedged basis, the Japanese 10-year yield stands at a relatively decent 2.38%, above the yield of 1.79% on comparable maturity US Treasurys (Table 1). Chart 34Favor Lower-Beta Government Bond Markets In 2020

Favor Lower-Beta Government Bond Markets In 2020

Favor Lower-Beta Government Bond Markets In 2020

Table 1Bond Markets Across The Developed World

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Strategy Outlook – 2020 Key Views: Full Speed Ahead

In contrast to Japan, the beta of US Treasurys to the overall global bond index is relatively high, implying that Treasurys will underperform other sovereign bond markets in a rising yield environment. The beta for Germany, UK, Australia, and Canada lie somewhere between Japan and the US. Consistent with our bullish view on global equities, we expect corporate bonds to outperform sovereign debt in 2020 (Chart 35). Despite the weakness in manufacturing, US banks further eased terms on commercial and industrial loans in Q3, according to the Fed’s Senior Loan Officer Survey. Chart 35Stronger Growth Causes Corporate Spreads To Tighten

Stronger Growth Causes Corporate Spreads To Tighten

Stronger Growth Causes Corporate Spreads To Tighten

At the US economy-wide level, neither interest coverage nor debt-to-asset ratios are particularly stretched (Chart 36). Admittedly, the picture looks less flattering if we focus solely on high-yield issuers (Chart 37). That said, a wave of defaults is very unlikely to occur in 2020, so long as the Fed is on hold and economic growth is on the upswing. Chart 36Corporate Debt: A Benign Top-Down View

Corporate Debt: A Benign Top-Down View

Corporate Debt: A Benign Top-Down View

Chart 37Corporate Debt: More Concerning Picture Among High-Yield Issuers

Corporate Debt: More Concerning Picture Among High-Yield Issuers

Corporate Debt: More Concerning Picture Among High-Yield Issuers

Chart 38US Corporates: Focus On High-Yield Credit

HY Spread Targets US Corporates: Focus On High-Yield Credit

HY Spread Targets US Corporates: Focus On High-Yield Credit

Moreover, despite narrowing this year, high-yield spreads still remain above our fixed-income team’s estimate of fair value (Chart 38). They recommend moving down the credit curve and increasing the weight in Caa-rated bonds. These have underperformed this year largely because of technical factors such as their large exposure to the energy sector and relatively short duration. As oil prices rise next year, energy sector issuers will feel some relief. Moreover, unlike this year, rising long-term government bond yields in 2020 should also make shorter-duration credit more attractive. In contrast to high-yield spreads, investment-grade spreads have gotten quite tight. Investors seeking high-quality bond exposure should shift towards Agency MBS, which still carry an attractive spread relative to Aa- and A-rated corporate bonds. European IG bonds should also outperform their US peers thanks to faster growth in Europe next year and ongoing support from the ECB’s asset purchase program. Looking beyond the next 12-to-18 months, there is a strong chance that inflation will increase materially from current levels. The unemployment rate across the G7 has fallen to a multi-decade low, while the share of developed economies reaching full employment has hit a new cycle high (Chart 39). Chart 39ADeveloped Markets: Unemployment Rates Keep Trending Lower... And Full Employment Reaching New Cycle Highs

Developed Markets: Unemployment Rates Keep Trending Lower... And Full Employment Reaching New Cycle Highs

Developed Markets: Unemployment Rates Keep Trending Lower... And Full Employment Reaching New Cycle Highs

Chart 39BDeveloped Markets: Unemployment Rates Keep Trending Lower... And Full Employment Reaching New Cycle Highs

Developed Markets: Unemployment Rates Keep Trending Lower... And Full Employment Reaching New Cycle Highs

Developed Markets: Unemployment Rates Keep Trending Lower... And Full Employment Reaching New Cycle Highs

Chart 40The Phillips Curve Is Alive And Well

The Phillips Curve Is Alive And Well

The Phillips Curve Is Alive And Well

For all the talk about how the Phillips curve is dead, wage growth remains well correlated with labor market slack (Chart 40). Rising wages will boost real disposable incomes, leading to more spending. If economies cannot increase supply to meet higher demand, prices will rise. It simply does not make sense to argue that the price of apples will increase if the demand for apples exceeds the supply of apples, but that overall prices will not increase if the demand for all goods and services exceeds the supply of all goods and services. It will take at least until mid-2021 for inflation to rise above the Fed’s comfort zone. It will take even longer for rates to reach restrictive territory, and longer still for tighter monetary policy to make its way through the economy. However, at some point in 2022, the interest-rate sensitive sectors of the US economy will buckle, setting off a global economic downturn and a deep bear market in equities and credit. Enjoy it while it lasts. Currencies And Commodities The US dollar is a countercyclical currency, meaning that it usually moves in the opposite direction of the global business cycle (Chart 41). This countercyclicality stems from the fact that the US, with its large service sector and relatively small manufacturing base, is a “low beta economy.” Strong global growth does help the US, but it benefits the rest of the world even more. Thus, capital tends to flow out of the US when global growth strengthens, which puts downward pressure on the dollar. As global growth picks up in 2020, the dollar will weaken. EUR/USD should increase to around 1.15 by end-2020. GBP/USD will rise to 1.40. USD/CNY will move to 6.8. The Australian and Canadian dollars, along with most EM currencies, will strengthen as well. However, the Japanese yen and Swiss franc are likely to be flat-to-down against the dollar, reflecting the defensive nature of both currencies. Today's rally in the pound has raised the return on our short EUR/GBP trade to 10.5%. For now, we would stick with this position. Chart 42 shows that the pound should be trading near 1.30 against the euro based on real interest rate differentials, which is still well above the current level of 1.20. Chart 41The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Chart 42Interest Rate Differentials Suggest More Upside For The Pound

Interest Rate Differentials Suggest More Upside For The Pound

Interest Rate Differentials Suggest More Upside For The Pound

The trade-weighted dollar will continue to depreciate until late-2021, and then begin to strengthen again as the Fed turns more hawkish and global growth starts to falter. Commodity prices tend to closely track the global growth/dollar cycle (Chart 43). Industrial metal prices will fare well next year. Oil prices will also move up. Globally, the last of the big projects sanctioned prior to the oil-price collapse in late 2014 are coming online in Norway, Brazil, Guyana, and the US Gulf. Our commodity strategists expect incremental oil supply growth to slow in 2020, just as demand reaccelerates. Gold is likely to be range-bound for most of next year reflecting the crosswinds from a weaker dollar on the one hand (bullish for bullion), and receding trade war risks and rising bond yields on the other hand. Gold will have its day in the sun starting in 2021 when inflation finally breaks out. Our key market charts are shown on the following page. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Chart 43Dollar Weakness Is A Boon For Commodities

Dollar Weakness Is A Boon For Commodities

Dollar Weakness Is A Boon For Commodities

Key Financial Market Forecasts

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Strategy Outlook – 2020 Key Views: Full Speed Ahead

MacroQuant Model And Current Subjective Scores

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Strategy Outlook – 2020 Key Views: Full Speed Ahead

Strategic Recommendations Closed Trades

Highlights Structurally overweight US T-bonds versus core European bonds. Our preferred expression is long T-bonds versus Swiss bonds. US yields can fall a lot more than European yields, and European yields can rise a lot more than US yields. Structurally underweight the overvalued dollar versus undervalued European currencies. Our preferred expression is long SEK/USD. Structurally underweight price-sensitive European export sectors. Undervalued European currencies cannot fall much further, and those European exporters that depend on price competitiveness will struggle to outperform. But structurally overweight soft luxuries. Despite President Trump’s threat to tariff French products, soft luxuries retain very strong pricing power and sustainable long term demand growth from rising female labour participation rates globally. Fractal trade: The 65-day fractal structure of global equities suggests that they are vulnerable to a near-term countertrend move. Feature Chart of the WeekLike-For-Like, Structural Inflation Is Lower In the US Than In Europe

Like-For-Like, Structural Inflation Is Lower In the US Than In Europe

Like-For-Like, Structural Inflation Is Lower In the US Than In Europe

A seemingly trivial disagreement between Europeans and Americans on how to measure inflation turns out to be the culprit for three major distortions in the world right now: Deeply divergent monetary policies across the developed economies. Huge valuation anomalies in the foreign exchange markets. President Trump’s threat of a trade war to counter the huge trade surpluses that Europe and China are running against the US. The inflation measurement disagreement wouldn’t really matter if inflation were running in the mid-single digits. But when inflation is near zero, the seemingly trivial difference in inflation measurement methodologies has ended up generating massive distortions. European And American Inflation Are Not The Same European inflation excludes the maintenance and upkeep costs associated with owning your home, whereas US inflation includes these costs at a hefty 25 percent weighting, making owner occupied housing by far the largest single item in the US inflation basket. By omitting the largest item in the US inflation basket, European inflation is subtly yet crucially different to American inflation. The European statisticians argue that unlike all the other items in the inflation basket, there is no independent market price for the ongoing cost of home ownership, and therefore this cost should be excluded. The American statisticians argue that the ongoing cost of home ownership is the single largest expense for most people and, as such, it should be ‘imputed’ from a concept known as ‘owner equivalent rent’ – essentially, asking homeowners how much it would cost to rent their own home. Different definitions of inflation will trigger very different policy responses from central banks. Both the European and American approaches have their merits and drawbacks, and it is not our intention to endorse one approach over the other. Our intention is simply to point out that the two approaches can give very different results for inflation – and therefore trigger very different policy responses from inflation-targeting central banks, with their consequent economic and political repercussions. If Americans used the European definition of inflation, then headline inflation in the US today would be running at the same sub-par rate as in the euro area, 1 percent, and well below the Fed’s 2 percent target (Chart I-2 and Chart I-3). More important, the five year annualised rate of inflation – let’s call it US structural inflation – would have been stuck below 1 percent since 2016 (Chart I-1 and Chart I-4). Under these circumstances, it would have been impossible for the Fed to hike the funds rate eight times, as it did through 2017-18. Chart I-2Like-For-Like, Headline Inflation Is Identical In The US And The Euro Area...

Like-For-Like, Headline Inflation Is Identical In The US And The Euro Area...

Like-For-Like, Headline Inflation Is Identical In The US And The Euro Area...

Chart I-3...And Core Inflation Is ##br##Very Similar

...And Core Inflation Is Very Similar

...And Core Inflation Is Very Similar

Chart I-4Using The European Definition Of Inflation, The Fed Couldn't Have Hiked Rates

Using The European Definition Of Inflation, The Fed Couldn't Have Hiked Rates

Using The European Definition Of Inflation, The Fed Couldn't Have Hiked Rates

Instead, what if Europeans used the American definition of inflation? European inflation does not include owner equivalent rent, but it does include housing rent for those that do rent their homes. In the US, these two items tend to move in lockstep (Chart I-5). If we assume the same for Europe, we can deduce that a US type weighting for owner equivalent rent would have boosted the headline inflation rate in the euro area by 0.3-0.4 percent through 2014-16, and by a possible 0.5 percent in Sweden through 2013-15 (Chart I-6 and Chart I-7). Under these circumstances, it would have been very difficult for the ECB and Riksbank to take and maintain policy rates deeply in negative territory, as they did through 2015-19. Chart I-5Owner Equivalent Rent Tracks ##br##Housing Rent

Owner Equivalent Rent Tracks Housing Rent

Owner Equivalent Rent Tracks Housing Rent

Chart I-6Using The American Definition Of inflation, Euro Area Inflation Would Have Been Higher...

Using The American Definition Of inflation, Euro Area Inflation Would Have Been Higher...

Using The American Definition Of inflation, Euro Area Inflation Would Have Been Higher...

Chart I-7...And Swedish Inflation Would Have Been Much Higher

...And Swedish Inflation Would Have Been Much Higher

...And Swedish Inflation Would Have Been Much Higher

The Different Definitions Of Inflation Have Created Dangerous Distortions If Europeans and Americans were using the same definition of inflation then, one way or the other, their monetary policies would not be as deeply divergent as they are now. One important implication is that European currencies would not be as undervalued as they are now. If Europeans and Americans were using the same definition of inflation then their monetary policies would not be as deeply divergent as they are now. Based on the ECB’s own analysis, the euro area is over-competitive versus its top 19 trading partners – meaning the euro is undervalued – by at least 10 percent. Moreover, the ECB admits that this sizable undervaluation only appeared after the ECB and Fed started taking their monetary policies in opposite directions in 2015 (Chart I-8). Chart I-8The Euro Is Undervalued By More Than 10 Percent

The Euro Is Undervalued By More Than 10 Percent

The Euro Is Undervalued By More Than 10 Percent

Put the other way, the dollar would not be as overvalued as it is now. In turn, the stronger dollar has created its own dangerous spill-overs. As we explained last week in The Hidden Sales Recession Of 2015… And Why It Matters Now, the surging dollar in 2015 could not have come at a worse time for China. Given that the Chinese economy was already slowing sharply, and the yuan was pegged to the dollar, the resulting loss of Chinese competitiveness just exacerbated the slump. Forcing China to loosen the dollar peg in August 2015. All of which brings us neatly to the hot topic of 2019, and likely 2020 too – President Trump’s threat of a trade war to counter the huge trade imbalances that Europe and China are running against the US. As it happens, President Trump has a good point. Trade wars almost always stem from trade imbalances; and trade imbalances almost always stem from exchange rate manipulations or, at least, exchange rate distortions that advantage one economy to the detriment of another. The euro's undervaluation only happened after monetary policies diverged in 2015. Most of the euro area’s €150 billion trade surplus with the US appeared after 2015, so it cannot be a structural issue. In fact, the evolution of the trade imbalance has tracked relative monetary policy between the Fed and ECB almost tick for tick (Chart I-9), via the exchange rate channel and the over-competitiveness of the euro which the ECB fully admits. Chart I-9Excessively Divergent Monetary Policies Caused The Euro Area's Huge Trade Surplus With The US

Excessively Divergent Monetary Policies Caused The Euro Area's Huge Trade Surplus With The US

Excessively Divergent Monetary Policies Caused The Euro Area's Huge Trade Surplus With The US

Of course, neither the ECB nor the Fed are deliberately targeting trade or the exchange rate; they are targeting inflation. But to repeat, they are targeting different definitions of inflation. Crucially, with a backdrop of near zero inflation, small definitional differences in inflation can generate huge economic and financial distortions, with dangerous political consequences. The Compelling Structural Opportunities The definitional difference between European and American inflation explain many of the economic and financial distortions we are witnessing now, as well as the dangerous political consequences. The main counterargument is that the inflation definitions are what they are; neither the ECB nor the Fed are likely to change them anytime soon. Nevertheless, there are compelling structural opportunities. Since 2015, American inflation has outperformed European inflation for one reason and one reason only: owner equivalent rents have surged by almost 20 percent relative to other prices (Chart I-10 and Chart I-11). The historic evidence suggests that such a pace of outperformance is unsustainable structurally and, absent this tailwind, US and European headline inflation rates have to converge, one way or the other. Chart I-10An Unsustainable Surge In US Owner Equivalent Rent...

An Unsustainable Surge In US Owner Equivalent Rent...

An Unsustainable Surge In US Owner Equivalent Rent...

Chart I-11...Has Lifted US Headline ##br##Inflation

...Has Lifted US Headline Inflation

...Has Lifted US Headline Inflation

In this inevitable convergence, the asymmetric starting point of bond yields favours a long US T-bonds, short core European bonds structural position. Because, if the inflation convergence is downwards, T-bond yields will fall much further than European yields; whereas if the inflation convergence is upwards, European yields will likely rise more than T-bond yields. Our preferred structural expression is: long US T-bonds, short Swiss bonds. For currencies it is the opposite message. The overvalued dollar is likely to underperform, at least versus other developed market currencies. Given that Swedish inflation has been the most understated by the exclusion of owner equivalent rents, combined with the Riksbank’s intention to exit negative interest rate policy imminently, our preferred structural expression is: long SEK/USD. American inflation has outperformed European inflation for one reason and one reason only: owner equivalent rents have surged by almost 20 percent relative to other prices. Lastly, European export growth – even in Germany – has been heavily reliant on a cheapening euro (Chart I-12). Undervalued European currencies cannot fall much further, and those European exporters that depend on price competitiveness will struggle to outperform. Even those multinationals that sell their products in dollars will lose out in the accounting translation back into a strengthening domestic currency. Hence, structurally underweight price-sensitive European export sectors. Chart I-12Without A Weaker Euro, Most European Exporters Will Struggle To Outperform

Without A Weaker Euro, Most European Exporters Will Struggle To Outperform

Without A Weaker Euro, Most European Exporters Will Struggle To Outperform

The one exception to this is the soft luxuries sector. Despite President Trump’s threat to tariff French products, soft luxuries retain very strong pricing power and sustainable long term demand growth from rising female labour participation rates globally. Stay structurally overweight soft luxuries. Fractal Trading System* The 65-day fractal structure of global equities suggests that they are vulnerable to a near-term countertrend move. Accordingly, this week’s recommended trade is to short the MSCI All Country World versus the global 10-year bond (simple average of US, euro area, and China), setting a profit target and symmetrical stop-loss at 2.5 percent. In other trades, long NZD/JPY and long SEK/JPY both achieved their profit targets of 3 percent and 1.5 percent respectively. Against this, long Poland versus World reached its 4 percent stop-loss. The rolling 1-year win ratio now stands at 65 percent. Chart I-13MSCI All-Country World Vs. Global 10-Year Bond

MSCI All-Country World Vs. Global 10-Year Bond

MSCI All-Country World Vs. Global 10-Year Bond

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

Cyclical Recommendations Structural Recommendations

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

How Low Inflation Has Distorted The World

Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Feature Recommended Allocation

Monthly Portfolio Update: How To Position For The End Game

Monthly Portfolio Update: How To Position For The End Game

In late November, BCA Research published its 2020 Outlook titled Heading Into The End Game, an annual discussion between BCA’s managing editors and the firm’s longstanding clients Mr. and Ms X.1 We recommend GAA clients read that document for a full analysis of the macro and investment environment we expect in 2020. In this Monthly Portfolio Outlook, we focus on portfolio construction: how we would recommend positioning a global multi-asset portfolio for the 12-month investment horizon in light of that analysis. First, a brief summary of the BCA macro outlook. We believe the global manufacturing cycle is starting to bottom out, partly because of its usual periodicity of 18 months from peak to trough, and also because of easier financial conditions, and some moderate fiscal and credit stimulus from China (Chart 1). Central banks will remain dovish next year despite accelerating growth. The Fed, in particular, worries that inflation expectations have become unanchored (Chart 2) and, moreover, will be reluctant to raise rates ahead of the US presidential election. This environment implies a moderate rise in long-term interest rates, with the US 10-year Treasury yield rising to 2.2-2.5%. Chart 1Reasons To Expect A Rebound

Reasons To Expect A Rebound

Reasons To Expect A Rebound

Chart 2Unanchored Inflation Expectations Worry The Fed

Unanchored Inflation Expectations Worry The Fed

Unanchored Inflation Expectations Worry The Fed

For an asset allocator, this combination of an improving manufacturing cycle and easy monetary policy looks like a very positive environment for risk assets (Chart 3). We, therefore, remain overweight equities and underweight fixed income. We have discussed over the past few months the timing to turn more risk-on and pro-cyclical in our recommendations.2 Since we are increasingly confident about the probability of the manufacturing cycle turning up, this is the time to make that change. Consequently, the shifts we are recommending in our global portfolio, shown in the Recommended Allocation table and discussed in detail below, add to its beta (Chart 4). Chart 3A Positive Environment For Risk Assets

A Positive Environment For Risk Assets

A Positive Environment For Risk Assets

Chart 4Raising The Beta Of Our Portfolio

Raising The Beta Of Our Portfolio

Raising The Beta Of Our Portfolio

Chart 5Some Signs Of Risk-On Still Missing

Some Signs Of Risk-On Still Missing

Some Signs Of Risk-On Still Missing

Nonetheless, we still have some concerns. China’s stimulus (particularly credit growth) remains half-hearted compared to previous cyclical rebounds in 2012 and 2016. We expect a “phase one” ceasefire in the trade war. But even that is not certain, and it would not anyway solve the long-term structural disputes. To turn fully risk-on, we would want to see signs of a clear rebound in commodity prices and a depreciation of the US dollar, which have not yet happened (Chart 5). The 2020 Outlook proposed some milestones to monitor whether our scenario is playing out and whether we should turn more or less risk-on. We summarize these milestones in Table 1. Given these uncertainties, to hedge our pro-cyclical positioning we continue to recommend an overweight in cash, and we are instituting an overweight position in gold. Table 1Milestones For 2020

Monthly Portfolio Update: How To Position For The End Game

Monthly Portfolio Update: How To Position For The End Game

Chart 6Recessions Are Caused By Inflation Or Debt

Recessions Are Caused By Inflation Or Debt

Recessions Are Caused By Inflation Or Debt

How will this cycle end? All recessions in modern history have been caused either by a sharp rise in inflation, or by a debt-fueled asset bubble (Chart 6). The Fed will likely fall behind the curve at some point as, after further tightening in the labor market, inflation starts to pick up. How the Fed reacts to that will determine what triggers the recession. If – as is most likely – it lets inflation run, that could blow up an asset bubble (and it was the bursting of such bubbles which caused the 2000 and 2007 recessions); if it decides to tighten monetary policy to kill inflation, the recession would look more like those of the 1970s and 1980s. But it is hard to see either happening over the next 12-18 months. Equities: As part of our shift to a more pro-risk, pro-cyclical stance, we are cutting US equities to underweight, and raising the euro zone to overweight, and Emerging Markets and the UK to neutral. US equities have outperformed fairly consistently since the Global Financial Crisis (Chart 7) – except during the two periods of accelerating global growth, in 2012-13 (when Europe did better) and 2016-17 (when EM particularly outperformed). The US today is expensive, particularly in terms of price/sales, which looks more expensive than the P/E ratio because the profit margin is at a record high level (Chart 8). The upside for US stocks in 2020 is likely to be limited. In 2019 so far, US equities have risen by 29% despite earnings growth close to zero. Multiples expanded because the Fed turned dovish, but investors should not assume further multiple expansion in 2020. Our rough model for US EPS growth points to around 8% next year (sales in line with nominal GDP growth of 4%, margins expanding by a couple of points, plus 2% in share buybacks). Add a dividend yield of 2%, and US stocks might give a total return of 10% or so. Chart 7US Doesn't Always Outperform

US Doesn't Always Outperform

US Doesn't Always Outperform

Chart 8US Equities Are Expensive

US Equities Are Expensive

US Equities Are Expensive