Euro Area

Highlights The U.S. economy is slowing in a completely predictable manner. With inflationary pressures largely dormant, the Fed can afford to stay on hold for the next few FOMC meetings. Growth in the U.S. and the rest of the world should stabilize by mid-year. This will enable the Fed to resume raising rates in June. A bearish stance towards U.S. Treasurys is warranted over a 12-month horizon. As long as the Fed is hiking rates in response to above-trend GDP growth rather than accelerating inflation, risk assets will fare well. Investors should overweight global equities and spread product for now, but monitor inflation trends closely for signs of when to get out. Brexit fears are overdone. Stay long the pound versus the euro. We were stopped out of our short AUD/JPY trade for a gain of 10%. Feature A Predictable Slowdown Investors are misunderstanding the nature of the current slowdown in the United States and much of the world. Completely predictable slowdowns, such as this one, rarely morph into recessions. Real U.S. GDP rose at a blistering 3.8% average annualized pace in Q2 and Q3 of 2018. There is no way that sort of growth rate could have been sustained. Financial conditions also tightened sharply in Q4, which has inevitably weighed on growth. Given the stock market rout, it is actually surprising that the economy has not weakened more than it has. The New York Fed GDP Nowcast points to growth of 2.5% in Q4 of 2018 and 2.1% in Q1 of 2019. This is still above the Fed’s long-term estimate of potential GDP growth of 1.9%. Most of the slowdown has been concentrated in the manufacturing sector, but even there, the bloodletting may be ending. The latest Philadelphia Fed survey — arguably the most important of the regional Fed manufacturing reports — showed an uptick in activity, with the new orders component hitting the highest level since last July. Despite the tightening in financial conditions, bank lending to the business sector has accelerated over the past three months (Chart 1). The Conference Board’s Leading Credit Index remains in expansionary territory (Chart 2). While business capex intention surveys have come off their highs, they still point to robust spending plans over the next few quarters (Chart 3). Chart 1Credit Is Still Flowing To U.S. Businesses

Credit Is Still Flowing To U.S. Businesses

Credit Is Still Flowing To U.S. Businesses

Chart 2Little Sign Of A Looming Credit Crunch

Little Sign Of A Looming Credit Crunch

Little Sign Of A Looming Credit Crunch

Chart 3Capex Plans Still Solid

Capex Plans Still Solid

Capex Plans Still Solid

The labor market remains healthy, as evidenced by ongoing strong payroll growth and low initial unemployment claims. Faster wage growth is boosting consumer spending. Holiday sales rose by 5.1% from a year earlier according to the Mastercard SpendingPulse report, the fastest growth in six years. The Redbook same-store index tells a similar story (Chart 4). Chart 4Same-Store Sales Are Robust

Same-Store Sales Are Robust

Same-Store Sales Are Robust

The housing market struggled for much of 2018, but the recent stabilization in mortgage rates should help matters (Chart 5). Notably, mortgage applications for purchase have surged to their highest levels since 2010 (Chart 6). Homebuilder confidence improved in January, mirroring the rally in homebuilder shares (Chart 7). We are long homebuilders versus the S&P 500, a trade that is up 5.3% since we recommended it on November 1, 2018. Chart 5aThe U.S. Housing Sector Will Stabilize (I)

The U.S. Housing Sector Will Stabilize (I)

The U.S. Housing Sector Will Stabilize (I)

Chart 5BThe U.S. Housing Sector Will Stabilize (II)

The U.S. Housing Sector Will Stabilize (II)

The U.S. Housing Sector Will Stabilize (II)

Chart 6A Positive Signal For U.S. Housing

A Positive Signal For U.S. Housing

A Positive Signal For U.S. Housing

Chart 7U.S. Homebuilder Stocks Have Been Outperforming Recently

U.S. Homebuilder Stocks Have Been Outperforming Recently

U.S. Homebuilder Stocks Have Been Outperforming Recently

U.S. Government Shutdown: A Near-Term Hit To Growth The government shutdown poses a near-term risk to the U.S. economy. If it lasts until the end of March, it will shave about 1.7% off Q1 GDP based on White House estimates. While this represents a potentially significant hit to the economy, the effect is likely to be completely reversed once the shutdown ends. Moreover, the drag to growth from the shutdown pales in comparison to the overall stance of fiscal policy. According to the IMF, the cyclically-adjusted budget deficit is set to reach 5.7% of GDP this year, up from 3.2% of GDP in 2015. There is also a reasonable chance that any deal to end the shutdown will involve a commitment to increase spending beyond currently budgeted levels. This would increase the overall amount of fiscal stimulus the economy is receiving. Taking The Pulse Of Global Growth The slowdown in growth has been deeper and more protracted outside the United States. Nevertheless, rays of sunshine are emerging. Our global Leading Economic Indicator diffusion index, which measures the proportion of countries with rising LEIs compared to those with falling LEIs, has bottomed. The diffusion index leads the global LEI by a few months (Chart 8). Chart 8The Uptick In The LEI Diffusion Index Suggests Global Growth Could Stabilize

The Uptick In The LEI Diffusion Index Suggests Global Growth Could Stabilize

The Uptick In The LEI Diffusion Index Suggests Global Growth Could Stabilize

As is increasingly the case, the fate of the Chinese economy will be critical in determining when global growth begins to reaccelerate. The latest Chinese activity data has been disappointing, with this week’s downright awful export figures being the latest example. That said, credit growth may be starting to stabilize, as evidenced by stronger-than-expected loan growth for December. With credit growth now running only slightly above nominal GDP growth, the need for the authorities to maintain their deleveraging campaign has diminished. In an encouraging sign, the Market-Based China Growth Indicator developed by our China Investment Strategy service has been moving higher (Chart 9). Chart 9Encouraging Sign For The Chinese Economy

Encouraging Sign For The Chinese Economy

Encouraging Sign For The Chinese Economy

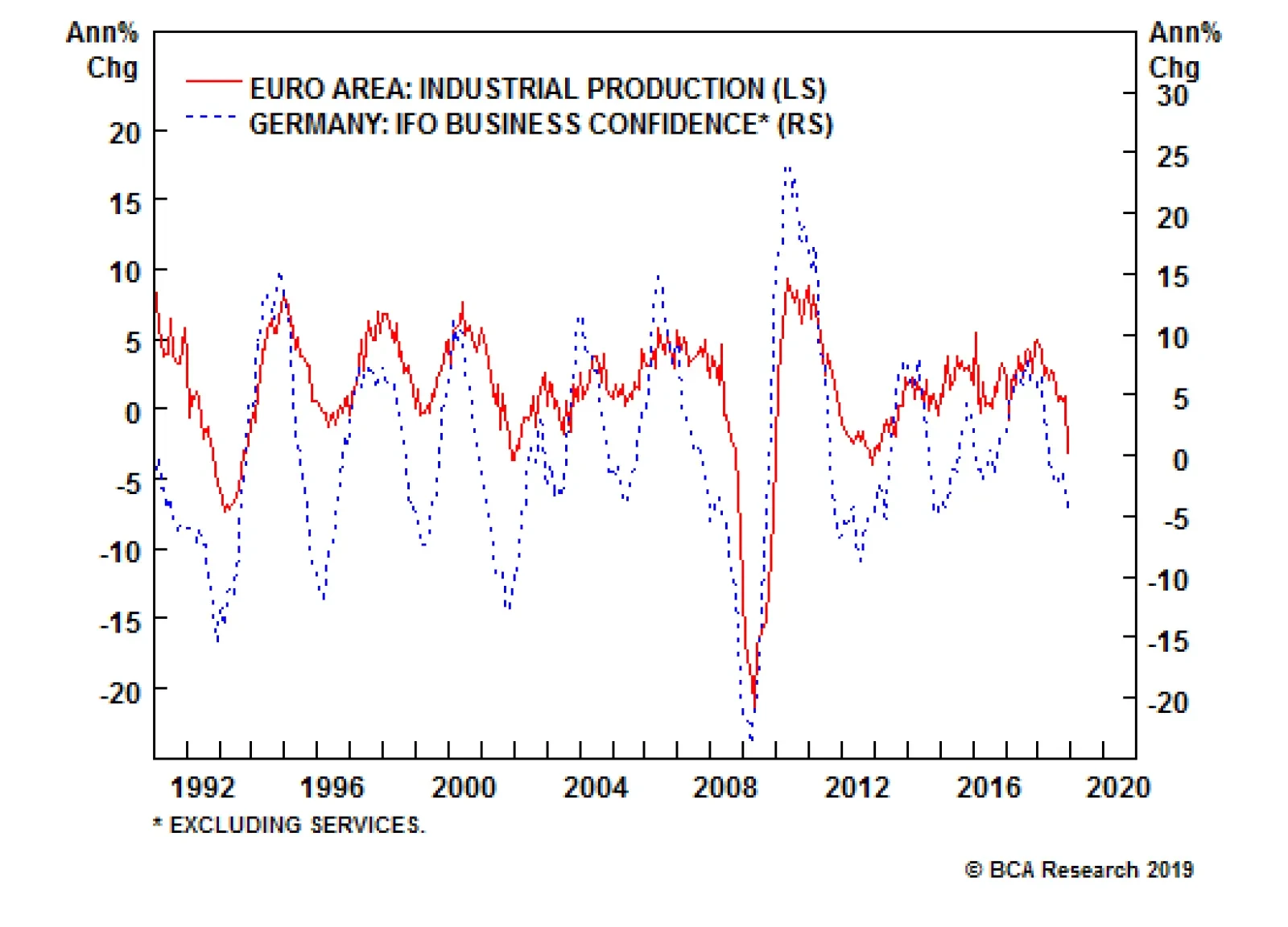

A revival in Chinese growth would aid trade-sensitive economies such as Japan and Germany. The former saw a decline in economic momentum in the second half of 2018, exacerbated by typhoons and an earthquake in Hokkaido. With the consumption tax set to increase from 8% to 10% in October, the Bank of Japan will need to maintain its yield curve control regime at least until 2020. This could weigh on the yen. With that in mind, we tightened the stop on our short AUD/JPY trade two weeks ago and subsequently exited the position with a gain of 10%. The German economy has taken it on the chin recently. Real GDP contracted in the third quarter and barely grew in the fourth quarter. The economy should rebound in 2019 as external demand improves. The drag on growth from the decline in automobile assemblies following the introduction of new emission standards should also turn into a modest tailwind as production resumes. In addition, fiscal policy is set to turn more stimulative, while robust wage growth, lower oil prices, and rising home prices should support consumption. Elsewhere in Europe, the Italian economy should recover as bond yields come down from their highs and confidence improves following the resolution of the impasse with the EU over budget targets. The modest easing in Italy’s fiscal policy of about 0.5% of GDP in 2019 should also benefit growth. It is too early to quantify the effect on the French economy from the “yellow vest” protests. France is no stranger to protests of this sort, so our guess is that the impact on the economy will be minimal. President Macron’s pledge to loosen fiscal policy in hopes of placating the protestors should also support demand. Brexit: A “No Deal” Outcome Looks Less Likely The Brexit saga could end in one of three ways: 1) A “no deal” where the U.K. leaves the EU with no alternative in place; 2) A “soft Brexit” involving an agreement to form a permanent customs union or some sort of “Norway plus” arrangement; 3) A decision to reverse the results of the original referendum and stay in the EU. In thinking about which of these three outcomes is most likely, one should keep the following in mind: Any course of action that the U.K. takes must have the support of the British parliament. A no deal outcome does not have parliament’s support. Not even close. Thus, it will not happen. This leaves options 2 and 3. This publication has argued since the day after the Brexit vote that the European establishment, following the example of the Irish and Danish referendums over various EU treaties, will keep insisting on do-overs until it gets the result it wants. If one referendum is good, two is even better – it’s twice as much democracy! The betting markets seem to be coming around to our view. As we go to press, PredictIt shows a one-in-three chance that a new referendum will be called by March 31 (Chart 10). Polling trends suggest that if another referendum were held, the remain side would probably prevail (Chart 11).

Chart 10

Chart 10

Chart 11U.K.: A Change Of Heart?

U.K.: A Change Of Heart?

U.K.: A Change Of Heart?

In some sense though, it does not matter for investors whether the original referendum is reversed or a soft-Brexit deal is reached. Either outcome would be welcomed by markets. We continue to advocate buying GBP/EUR. My colleague Dhaval Joshi, BCA’s Chief European strategist, also recommends that equity investors purchase the FTSE 250 index, which comprises from the 101st to the 350th largest companies listed on the London Stock Exchange. Unlike its large-cap counterpart, the FTSE 100, the FTSE 250 index is more geared to what happens in the U.K. than in the rest of the world. Investment Conclusions Global inflation remains subdued, which gives central banks the luxury of taking a wait-and-see approach to tightening monetary policy. Growth in the U.S. and the rest of the world should stabilize by mid-year. This will enable the Fed to resume raising rates in June. Given that the market is no longer pricing in any Fed hikes, a bearish stance towards U.S. Treasurys is warranted over a 12-month horizon (Chart 12). Outside of Japan, bond yields will also rise in the major developed economies. Chart 12Treasurys Will Underperform If The Fed Hikes Rates By More Than Expected

Treasurys Will Underperform If The Fed Hikes Rates By More Than Expected

Treasurys Will Underperform If The Fed Hikes Rates By More Than Expected

We downgraded global equities in June as our leading indicators began to point to slower growth ahead, but upgraded them back to overweight after stocks plunged following the December FOMC meeting. The rally over the past three weeks has reversed deeply oversold conditions and our tactical MacroQuant model is once again flagging some near-term risk to stocks. Nevertheless, if the global economy avoids a recession this year, as we expect, equities should fare well over a 12-month horizon. The MSCI All-Country World index is trading at a modest 13.6-times forward earnings (Chart 13). Profit estimates have been revised down meaningfully, suggesting that the bar for upward earnings surprises is now quite low. Chart 13A Lot Of Bad News Already Discounted?

A Lot Of Bad News Already Discounted?

A Lot Of Bad News Already Discounted?

Risk assets can tolerate higher rates as long as tighter monetary policy is the result of stronger growth. What risk assets cannot withstand is a stagflationary environment where growth is slowing but the Fed is hiking rates in order to bring down inflation. That is not the situation today, but could be the situation next year. Bottom line: Investors should overweight global equities and spread product for now, but monitor inflation trends closely for signs of when to get out. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Chart 14

Tactical Trades Strategic Recommendations Closed Trades

Highlights Global Corporates: The Fed is now clearly signaling a near-term capitulation to tightening financial conditions alongside slowing global growth and inflation. A pause in the U.S. rate hiking cycle, after credit spread valuations have cheapened up, opens up a window of opportunity for global corporate bond market outperformance versus government debt over the next 3-6 months. Country Allocation: Move to overweight (4 of 5) on both U.S. investment grade and high-yield corporates, while downgrading U.S. Treasuries to underweight (2 of 5). Upgrade euro area investment grade and high-yield corporates to neutral (3 of 5), while downgrading euro area governments to underweight (2 of 5). Upgrade emerging market U.S. dollar denominated debt (both sovereign and corporate) from maximum underweight to underweight (2 of 5). Feature We downgraded our overall recommended investment stance on global corporate debt to neutral on June 26 of last year.1 That decision reflected our concern at the time that less accommodative central banks, a rising U.S. dollar, weakening global growth momentum and intensifying U.S.-China trade tensions had all significantly worsened the near-term risk/reward tradeoff for owning corporate bonds. This accompanied a firm-wide call at BCA to pare back our recommended exposure to global equities for the same reasons. We now see an opportunity, driven by better value and diminished market volatility after the Fed has clearly signaled a pause on U.S. rate hikes (Chart of the Week), to go back to an overweight stance on corporate credit on a tactical basis (3-6 months). Chart of the WeekTime For A Pause In Corporate Spread Widening

Time For A Pause In Corporate Spread Widening

Time For A Pause In Corporate Spread Widening

To be clear, we still see medium-term risks for corporate credit once global growth stabilizes and a resilient U.S. economy forces the Fed to restart the rate hikes in the latter half of 2019. A move to a restrictive stance by the Fed toward year-end, signaled by an inversion of the U.S. Treasury yield curve, will raise recession risks and be the eventual death knell for this credit cycle. In the meantime, corporate debt is likely to outperform government bonds, justifying a tactical overweight position. This mirrors the recent change in the BCA House View, returning to a tactical overweight stance on global equities. On a regional basis, we prefer taking more of our upgraded credit risk in U.S. corporates over European and emerging market (EM) equivalents. The outlook for growth remains more favorable on a relative basis to Europe or China, the latter being most critical for the outperformance of EM assets. Why The Spread Widening Will Pause: A Patient Fed Is Taking A Break Global corporate bond spreads have widened since we did our downgrade in June, across all countries and credit tiers (Chart 2). Typically, some underperformance of corporate credit should occur when global growth momentum slows, as was the case throughout 2018. Yet the most violent period of spread widening only began once the Fed began signaling that it would continue with its interest hikes and balance sheet runoff, despite softening global growth.

Chart 2

This set off yet another clash between policy and the markets – one of BCA’s key investment themes for 2018 that still applies in 2019 – resulting in a sharp selloff in global risk assets, including corporate debt. The result was a tightening of U.S. financial conditions, first through a stronger U.S. dollar (supported by rate hike expectations) and later through lower equity prices and wider corporate spreads. This echoed the 2014/15 period when the Fed was trying to lift rates off the zero bound after ending its quantitative easing program. The Fed was only able to deliver a single rate hike in December 2015 before pausing because of severely slumping global growth (most notably in China) and a sharp tightening in financial conditions, both of which knocked the wind out of the U.S. economy. Turning to 2019, the downturn in cyclical growth indicators like manufacturing purchasing managers indices (PMI) and the global leading economic indicator (LEI) has reached levels last seen after that 2014/15 episode (Chart 3). Importantly, our global LEI diffusion index, which measures the number of countries with rising LEIs compared to falling LEIs and is itself a reliable leading indicator of the global LEI, is bottoming out at the same level that preceded the 2016 LEI revival (middle panel). This suggests that a stabilization of the global LEI could unfold in the next few months, which would also signal a potential rebound in corporate credit returns (bottom panel). Chart 3Credit Returns Already Reflect Slowing Growth

Credit Returns Already Reflect Slowing Growth

Credit Returns Already Reflect Slowing Growth

Given the many similarities between today and the 2014/15 backdrop, it is sensible to look for other indicators that accurately heralded the end of that period of spread widening to help time a potential increase in recommended exposure to corporates. Over the past several weeks, our colleagues at our sister BCA service, U.S. Bond Strategy, have been following a checklist of market-based signals to determine the timing of a potential peak in U.S. credit spreads.2 These are grouped into two categories: signals of rebounding global growth and signals of Fed capitulation on rate hikes. For global growth, the indicators monitored are shown in Chart 4: Chart 4Checklist For Peak U.S. Spreads: Global Growth

Checklist For Peak U.S. Spreads: Global Growth

Checklist For Peak U.S. Spreads: Global Growth

the CRB raw industrials index of commodity prices (a broader measure that excludes highly volatile oil prices) the BCA Market-Based China Growth Indicator (created by our China Investment Strategy team as a proxy of investor expectations of Chinese growth3) the Global Industrial Mining equity price index For Fed capitulation, the indicators monitored are shown in Chart 5: Chart 5Checklist For Peak U.S. Spreads: Fed Capitulation

Checklist For Peak U.S. Spreads: Fed Capitulation

Checklist For Peak U.S. Spreads: Fed Capitulation

our 12-month fed funds discounter, which measures the amount of expected Fed rate hikes over the next year discounted in the U.S. Overnight Index Swap (OIS) curve the price of gold in dollars (a higher price correlating with perceptions of easier U.S. monetary policy and vice versa) the nominal trade-weighted U.S. dollar index Among the growth-focused elements of the checklist, only the China Growth Indicator is in a clear uptrend. Non-oil commodity prices had been stabilizing at the end of 2018 but appear to be rolling over, while it is not yet clear if the downturn in Mining stocks has ended. With momentum in global PMIs and LEIs still having not yet bottomed out, it may be too early to expect a cyclical rebound in non-oil commodities and related equities. At a minimum, that will require even greater signs that China’s economy is regaining some vigor. However, as we discussed last week, Chinese policymakers’ options to stimulate growth are far more limited now than they were in 2015 and 2016 when a rebounding China boosted commodity demand and EM asset performance.4 Within the Fed-focused components of the “Peak Spreads Checklist”, the near-term bullish signal for credit is much stronger. Our fed funds discounter has rapidly priced out all rate hikes for 2019. Since November, gold is up nearly 8% and the nominal trade-weighted U.S. dollar is down 2%. The shift in recent Fed messaging from signaling a “gradual pace” of tightening to exhibiting “patience” on any future policy moves was a highly dovish signal for investors. This alone has been enough to stabilize equity and credit markets, which had been discounting that Fed tightening in 2019 would drive the U.S. into a possible recession. In the constant battle between financial conditions and the Fed, the former has won this latest round. How long will this Fed pause last? Continuing with the comparison to the 2014/15 episode, a critical difference is that underlying trends in U.S. economic growth and inflation are firmer today. This is evident in the BCA Fed Monitor, which is comprised of economic and financial data that indicate pressure on the Fed to tighten or ease monetary policy. Chart 6 shows a “cycle-on-cycle” comparison of the Fed Monitor (and its subcomponents) today versus 2014/15. The Fed Monitor is still signaling a need for the Fed to continue tightening because the Economic Growth and Inflation Components remain elevated. Yet the Monitor has declined from its recent peak thanks entirely to the plunge in the Financial Conditions Component, which has fallen even faster than it did in 2014/15. Chart 6BCA Fed Monitor: Today Vs 2014/15

BCA Fed Monitor: Today Vs 2014/15

BCA Fed Monitor: Today Vs 2014/15

The implication from our Fed Monitor is that there needs to be more evidence of slowing U.S. economic growth and reduced inflation pressures for the Fed to stay on hold for longer. If the data stay firm, but financial conditions ease because investors expect a prolonged pause from the Fed, then the Fed could quickly return to a hawkish bias later this year. This is now our base case scenario for how 2019 will play out. This is also why we are only upgrading corporate debt on a tactical basis. We do not expect U.S. growth or inflation to slow enough to prevent more Fed tightening later this year – an outcome that will weigh on credit returns as the Fed moves to a restrictive policy stance. Yet even if we are wrong and the U.S. economy decelerates more sharply, that is also a bad outcome for credit because it means weaker corporate profits and rising downgrades and defaults. For bond investors with longer-time horizons than 3-6 months, the credit rally that we are anticipating can actually provide an opportunity to reduce credit exposure for the final leg of the Fed’s monetary policy cycle and the multi-year corporate credit cycle. In other words, selling into the rally rather than chasing it. For now, we are choosing to play for the shorter-term move by upgrading our recommended global credit allocations. Yet we do not envision this turning into a long-term position. The medium-term outlook for corporates is far more challenging given the advanced age of the monetary, business and credit cycles. Bottom Line: The Fed is now clearly signaling a near-term capitulation to tightening global financial conditions alongside slowing global growth and inflation. A pause in the U.S. rate hiking cycle, after credit spread valuations have cheapened up, opens up a window of opportunity for global corporate bond market outperformance versus government debt over the next 3-6 months. The Specific Changes To Our Recommended Asset Allocation As part of our tactical upgrade of global corporate debt, we are making the following changes to our recommended portfolio allocation tables (see Page 13): Upgrade overall global credit exposure to overweight (4 out of 5) Upgrade both U.S. investment grade and high-yield corporate exposure to overweight (4 out of 5), while downgrading U.S. Treasury exposure to underweight (2 out of 5) Upgrade euro area investment grade and high-yield corporate exposure to neutral (3 out of 5) and downgrade euro area government bond exposure to underweight (2 out of 5) Upgrade EM U.S. dollar denominated debt from maximum underweight to underweight (2 out of 5), both for sovereign and corporate debt. The changes all represent a one-notch upgrade from our previous allocations, based on our more positive tactical view on overall global credit risk, while still maintaining our relative preference for U.S. corporates over non-U.S. equivalents. We prefer U.S. credit not only because we expect better relative economic growth momentum in the U.S., but also because our preferred valuation metrics indicate that U.S. corporate bond spreads now look relatively attractive. Our estimate of the default-adjusted spread on U.S. high-yield corporates, which is simply the current spread minus losses from defaults, has risen to 302bps, well above the long-run average of 268bps (Chart 7). That is a function of the high-yield spread now discounting a 2019 default rate of nearly 6%, well above our forecasted default rate of 2.5%.5 Chart 7Too Much Default Risk Priced Into U.S. Junk

Too Much Default Risk Priced Into U.S. Junk

Too Much Default Risk Priced Into U.S. Junk

Corporate credit spreads in the U.S. also look attractive on a volatility-adjusted basis. Our estimates of Breakeven Spreads – the amount of spread widening required for corporate returns to break-even with duration-matched U.S. Treasuries on a one-year horizon – shows that credit spreads have cheapened to levels that are in the upper end of the historical range for both investment grade and high-yield debt (Charts 8 & 9). Chart 8Vol-Adjusted IG Spreads Have Cheapened

Vol-Adjusted IG Spreads Have Cheapened

Vol-Adjusted IG Spreads Have Cheapened

Chart 9Vol-Adjusted HY Spreads Are Cheap

Vol-Adjusted HY Spreads Are Cheap

Vol-Adjusted HY Spreads Are Cheap

Credit spreads have also cheapened up in Europe and EM, and a “risk-on” rally from a Fed pause will likely benefit spread product in those regions. However, the performance of U.S. credit versus non-U.S. credit remains largely determined by relative growth trends (Charts 10 & 11). Given our more positive view on U.S. growth on a relative basis, we are maintaining a higher recommended allocation to U.S. corporates versus euro area and EM equivalents, even as we upgrade overall global corporate exposure. This is also a way to provide a partial hedge to the specific risks in the latter regions coming from: Chart 10Global Corporates: Continue Favoring U.S. Over Europe

Global Corporates: Continue Favoring U.S. Over Europe

Global Corporates: Continue Favoring U.S. Over Europe

Chart 11Global Corporates: Continue Favoring U.S. Over EM

Global Corporates: Continue Favoring U.S. Over EM

Global Corporates: Continue Favoring U.S. Over EM

a) an end of the ECB’s corporate bond buying as part of its Asset Purchase Program, which takes a major buyer out of the euro area corporate market b) a more persistent slowing of Chinese growth momentum and softer non-oil commodity prices, both of which would be negatives for EM assets On a final note, we are also changing the specific weighting in our Model Bond Portfolio on Page 12 to reflect all of the above changes. The allocations to all U.S., euro area and EM corporates are increased – with bigger allocation changes in the U.S. – funded out of reduced weightings in U.S., German and French government bonds. Note that we are not making any changes to our relative U.K. exposures this week, given the unique risk for U.K. financial markets from the Brexit uncertainty. Thus, we are maintaining an overweight stance on U.K. Gilts in the government bond portion of the model portfolio, while remaining underweight U.K. corporates on the credit side. Robert Robis, CFA, Senior Vice President Global Fixed Income Strategy rrobis@bcaresearch.com Footnotes 1 Please see BCA Global Fixed Income Strategy Weekly Report, “Time To Take Some Chips Off The Table: Downgrade Global Corporate Bond Exposure To Neutral”, dated June 26th 2018, available at gfis.bcaresearch.com. 2 Please see BCA U.S. Bond Strategy Weekly Report, “A Checklist For Peak Credit Spreads”, dated November 27th 2018, available at usbs.bcaresearch.com. 3 Please see BCA China Investment Strategy Weekly Report, “Trade Is Not China’s Only Problem”, dated November 21st 2018, available at cis.bcaresearch.com. 4 Please see BCA Global Fixed Income Strategy Weekly Report, “Three Big Questions To Start Off 2019”, dated January 8th 2019, available at gfis.bcaresearch.com. 5 That forecasted default rate is taken from Moody’s, who have a similarly positive outlook on 2019 U.S. growth as BCA. Therefore, we see no reason to use a different default rate assumption in our high-yield valuation estimate. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Enough With The Gloom: Upgrade Global Corporates On A Tactical Basis

Enough With The Gloom: Upgrade Global Corporates On A Tactical Basis

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Today’s Industrial production in the euro area dropped to -3.3% on a year-on-year basis, much worse than expectations. The month-over-month number is -1.7%. This grim result raises concerns on the growth conditions in Europe. First, political tensions in…

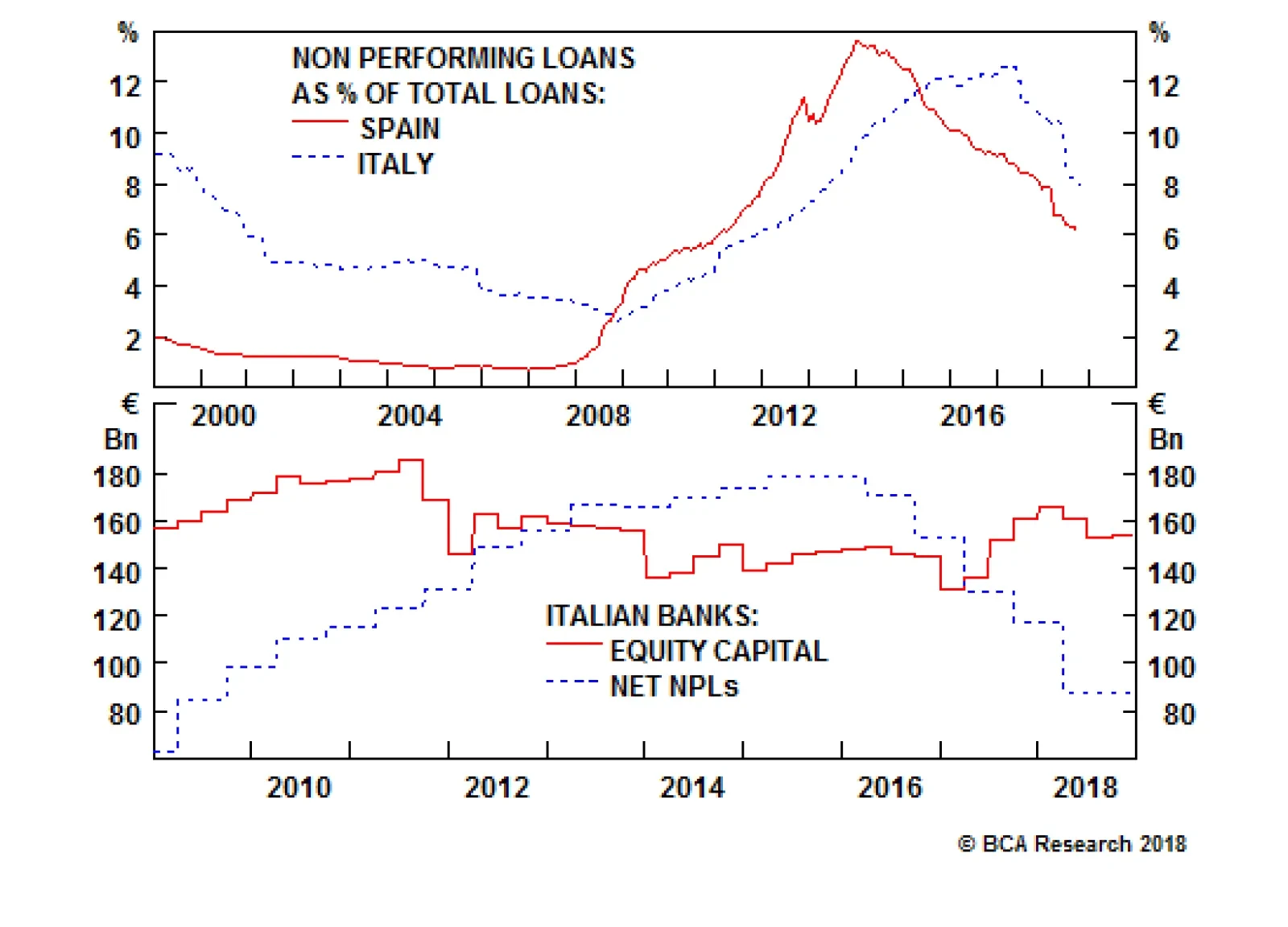

Highlights All of our recent investment recommendations have performed very strongly but have further to go: 1. Own a combination of European banks plus U.S. T-bonds. 2. Overweight EM versus DM. 3. Overweight European versus U.S. equities. 4. Overweight Italian assets versus European assets. 5. Overweight the JPY. Feature Chart of the WeekBank Outperformance Corroborates A Growth Rebound

Bank Outperformance Corroborates A Growth Rebound

Bank Outperformance Corroborates A Growth Rebound

2019 will be the investment mirror-image of 2018. Last year started with growth fading and inflation on the cusp of picking up, both in Europe and around the world. This year has started with the European and global economies in the mirror-image configuration: growth likely to rebound, albeit modestly, and inflation set to fade (Chart I-2). Chart I-2Why 2019 Is The Mirror-Image Of 2018

Why 2019 Is The Mirror-Image Of 2018

Why 2019 Is The Mirror-Image Of 2018

However, as 2019 unfolds, the configuration will reverse, requiring a flip from a pro-cyclical to a pro-defensive investment tilt later in the year. This contrasts with 2018 which started pro-defensive and ended pro-cyclical. In this regard, the economic and investment shape of 2019 will be the mirror-image of 2018. Growth To Rebound, Inflation To Fade A tell-tale sign of a growth rebound is the recent outperformance of banks. Around the world, yield curves have flattened – or even inverted – meaning that banks’ net interest margins have compressed. This compression of bank profit margins is normally bad news for bank equities. Yet banks have been outperforming, not just in Europe but globally (Chart I-3). If margins are compressing, the plausible explanation for outperformance would be an improved outlook for asset growth, reflecting both a reduction in bad debt provisioning and a pick-up in bank credit growth. Chart I-3Banks Have Been Outperforming Since October

Banks Have Been Outperforming Since October

Banks Have Been Outperforming Since October

Independently and reassuringly, our proprietary credit impulse analysis supports this thesis (Chart of the Week). Six-month credit impulses have been rebounding not only in Europe, but also in the United States and very impressively in China (Chart I-4). Chart I-46-Month Credit Impulses Have Rebounded Everywhere

6-Month Credit Impulses Have Rebounded Everywhere

6-Month Credit Impulses Have Rebounded Everywhere

At the same time, inflation is set to disappoint as the recent near-halving of the crude oil price feeds into both headline and core consumer price indexes. With central banks now promising even greater “dependence on the incoming data”, this unfolding dynamic will force them to temper any hawkish intentions and rhetoric, limiting the extent of upside in bond yields. In this configuration, the combination of European banks plus U.S. T-bonds which we first recommended in November is still appropriate (Chart I-5). The position is up 3 percent in little more than a month and has further to go.1 Chart I-5Own A Combination Of Banks And Bonds

Own A Combination Of Banks And Bonds

Own A Combination Of Banks And Bonds

Europe’s largest economy, Germany, should benefit from another support to growth. Last year, the auto sector – a major engine of the German economy – spluttered as it absorbed the new WLTP emissions testing standard. Through the middle of 2018 German motor vehicle exports suffered a €20 billion hit which shaved 0.6 percent from Germany’s €3.4 trillion economy (Chart I-6). Now, if auto exports stabilize, this drag will disappear. And if auto exports recover to the pre-WLTP level after this one-off and temporary shock, Germany will receive a 0.6% mirror-image boost to growth.2 Chart I-6German Auto Exports Suffered A WLTP Hit

German Auto Exports Suffered A WLTP Hit

German Auto Exports Suffered A WLTP Hit

Regional Allocation Is Always And Everywhere About Sectors The European equity earnings cycle is tightly connected with global growth oscillations (Chart I-7). The simple reason is that the European equity market is over-exposed to classically growth-sensitive sectors such as banks and industrials. Chart I-7The European EPS Cycle Is Tightly Connected With Global Growth Oscillations

The European EPS Cycle Is Tightly Connected With Global Growth Oscillations

The European EPS Cycle Is Tightly Connected With Global Growth Oscillations

The emerging market earnings cycle is also connected with global growth oscillations (Chart I-8) because emerging markets have a very high exposure to banks. But the much less understood reason is that emerging markets have a near-zero exposure to healthcare (Table I-1). In sharp contrast, the U.S. equity earnings cycle has almost no connection with global growth oscillations (Chart I-9) because the U.S. equity market is over-exposed to technology and healthcare, neither of which are classically cyclical sectors. Chart I-8The EM EPS Cycle Is Also Connected With Global Growth Oscillations...

The EM EPS Cycle Is Also Connected With Global Growth Oscillations...

The EM EPS Cycle Is Also Connected With Global Growth Oscillations...

Chart I-9...But The U.S. EPS Cycle Is Not Connected With Global Growth Oscillations

...But The U.S. EPS Cycle Is Not Connected With Global Growth Oscillations

...But The U.S. EPS Cycle Is Not Connected With Global Growth Oscillations

Chart I-

Hence the allocation to emerging market (EM) versus developed market (DM) equities, and to Europe versus the U.S. reduce to simple equity sector calls. A quick glance at Chart I-10 and Chart I-11 will reveal two fundamental and inescapable truths: Chart I-10EM Outperforms DM When Global Banks Outperform Healthcare

EM Outperforms DM When Global Banks Outperform Healthcare

EM Outperforms DM When Global Banks Outperform Healthcare

Chart I-11European Equities Outperform U.S. Equities When Global Banks Outperform Technology

11. European Equities Outperform U.S. Equities When Global Banks Outperform Technology

11. European Equities Outperform U.S. Equities When Global Banks Outperform Technology

EM outperforms DM when global banks outperform global healthcare. European equities outperform U.S. equities when global banks outperform global technology. But is this just about so-called ‘beta’? No, banks can outperform in a rising market by going up more or, as recently, in a falling market by going down less. So this is always and everywhere about head-to-head sector relative performances. My colleague Arthur Budaghyan, our chief emerging market strategist, remains steadfastly pessimistic on the structural outlook for EM versus DM. We agree with Arthur, albeit we arrive at the structural conclusion from a completely different perspective. To reiterate, for EM to outperform DM global banks must outperform global healthcare. However, over an extended period this will prove to be an extremely tall order. As detailed in European Banks: The Case For And Against, blockchain is a long-term extinction threat to banks’ business models and profitability. Whereas healthcare is still a major growth sector as people focus more spending on improving the quality and quantity of their lifespans.3 Nevertheless, from a purely tactical perspective, the growth up-oscillation phase that started in October can continue for a little while longer allowing the recent countertrend moves to persist – especially as the recent decline in bond yields could further spur credit growth in the near term. So for the moment stay overweight: EM versus DM. European equities versus U.S. equities. Italian assets versus European assets. Bargain Basement Currencies Another of my colleagues Doug Peta, our chief U.S. strategist, has coined a lovely metaphor: “you cannot get hurt falling out of a basement window”. The metaphor beautifully captures the asymmetry when you are near the floor or ‘zero-bound’. Doug uses it to explain that small contributors to an economy have a limited capacity to damage economic growth because they cannot fall very far. We think the metaphor applies equally to interest rates when they are at or near their lower bound, which is to say, in the basement. This begs the obvious question: if interest rates are in the basement, then what is it that cannot get hurt much? The answer is: the exchange rate. The payoff profile for exchange rates just tracks expected long-term interest rate differentials. This means that when the expected interest rate is in or near the basement, the currency possesses a highly attractive payoff profile called positive skew. In essence, for any central bank already at the realistic limit of ultra-loose policy – such as the BoJ and ECB – policy rate expectations are effectively in the basement. They cannot go significantly lower. In contrast, policy rate expectations for the Federal Reserve are somewhere between the seventh and twelfth storey of the building (Chart I-12). From which you can get seriously hurt if you fall out of the window! Chart I-12You Cannot Get Hurt Falling Out Of A Basement Window

You Cannot Get Hurt Falling Out Of A Basement Window

You Cannot Get Hurt Falling Out Of A Basement Window

The upshot is that currency investors should always own at least one currency whose interest rate is in the basement against one whose interest rate is high up in the building, susceptible to fall out at some point, and get seriously hurt. The near term complication is the risk, albeit low, of a no-deal Brexit which would hurt European economies and currencies to a greater or lesser extent. Until the Brexit fog shows some signs of clearing, we would prefer the currency whose interest rate is in the basement to be a non-European currency. So for the moment, our favourite major currency remains the JPY. Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System* We are pleased to report that the 50:50 combination of Litecoin and Ethereum has surged by 42 percent in just two weeks! Also, long EUR/NZD achieved its 2.5 percent profit target and is now closed. This week’s trade is in line with the recommendation in the main body of this report to become pro-cyclical. Go long global industrials versus global utilities with a profit target of 3 percent and a symmetrical stop-loss. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-13

Long Global Industrials Vs. Global Utilities

Long Global Industrials Vs. Global Utilities

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com Footnotes 1 The European banks position is relative to the broader equity market, and the recommended combination is 25 cents in the banks and 75 cents in the bonds. 2 German auto net exports and GDP are quoted at annualized rates. The Worldwide Harmonized Light Vehicle test Procedure (WLTP) is a new standard for auto emissions that took effect on September 1, 2018. 3 Please see the European Investment Strategy Special Report “European Banks: The Case For And Against”, November 8, 2018 available at eis.bcaresearch.com. Fractal Trading System Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Dear Client, In lieu of next week’s report, I will be hosting a webcast on Wednesday, January 9th at 10 AM EST, when I will be discussing the economic and financial market outlook for 2019 and answering your questions. Best regards, Peter Berezin, Chief Global Strategist Highlights The lack of major financial and economic imbalances in the U.S., as well as the Fed’s ability to moderate the pace of rate hikes, reduce the risk of a vicious cycle where tighter financial conditions lead to slower economic growth and even tighter financial conditions. The scope for central banks to cut rates is more limited outside the United States. Imbalances are also greater abroad. Nevertheless, the news is not all bleak, with the recent rebound in China’s credit impulse being a case in point. We turned more bullish on risk assets following December’s post-FOMC equity sell-off. A moderately overweight position in global equities over a 12-month horizon is currently justified. While we continue to favor the U.S. over other bourses in dollar terms, our conviction level in this regional bias has decreased. Treasury yields are likely to rise in an environment where U.S. growth is strong enough to enable the Fed to continue raising rates. Outside Japan, global government bond yields will also increase in 2019. We are removing our long June-2019 Fed funds futures contract hedge, and we are now solely outright short the December-2020 contract. We are also taking profits on our March-2019 EEM ETF put for a gain of 104%. Feature Merry Crisis And A Happy New Fear Santa arrived early this year. The plunge in stocks allowed investors to buy some of the world’s premier companies at a mouthwatering 20%-to-30% discount to what they would have paid just a few months earlier. What a gift! Needless to say, most investors would not regard last month’s stock market performance in such a favorable light. But why not? One answer is that investors must mark their portfolios to market. Thus, even if the decline in equity prices raised future returns, it still implied a decline in present net worth. Yet, this cannot be the whole explanation, because if all investors expected stocks to bounce back quickly, they would not have sold in the first place. Clearly, many investors must have come to the conclusion that the stock market would not only go down but stay down. However, this presents a puzzle. The economic environment did not change that much in the weeks leading up to the October sell-off. Growth has slowed more recently (Chart 1), with this morning’s disappointing ISM manufacturing report being the latest example, but this appears to have been mainly a response to the souring market climate rather than the cause of it. Chart 1Tighter Financial Conditions Have Led To Slower Growth

Tighter Financial Conditions Have Led To Slower Growth

Tighter Financial Conditions Have Led To Slower Growth

Reverse Causality? This raises an intriguing possibility: What if the drop in stock prices and jump in credit spreads that began in late September hurt expectations of economic growth by enough to justify a further discount in risk asset valuations? Such a “Financial Conditions Index (FCI) doom loop” is not just a theoretical construct. The last two U.S. recessions were both the products of burst asset bubbles — first the dotcom bubble and then the housing bubble. Could such a self-fulfilling vicious cycle be erupting again? If so, any rally in stocks or credit should be sold into, just as was the case in both 2001 and 2007. U.S. Fairly Resilient To A Doom Loop Fortunately, there are two reasons to think that such an outcome will not reoccur, at least not in the United States. First, as Box 1 explains, an FCI doom loop is more likely to unfold when economic growth becomes very sensitive to changes in financial conditions. This normally happens when economic and financial imbalances are elevated. That does not appear to be the case today. Unlike in the lead-up to the last two recessions, the U.S. private sector is a net saver whose income outstrips spending by 2.1% of GDP (Chart 2). Cyclical spending – the sum of residential investment, business capex, and expenditures on consumer durable goods – is also far below prior business-cycle peaks as a share of GDP (Chart 3). Chart 2The U.S. Private Sector Is A Net Saver

The U.S. Private Sector Is A Net Saver

The U.S. Private Sector Is A Net Saver

Chart 3U.S. Economy: Cyclical Spending Is Still Restrained

U.S. Economy: Cyclical Spending Is Still Restrained

U.S. Economy: Cyclical Spending Is Still Restrained

Despite recent releveraging in some categories, U.S. household debt has continued to decline in relation to the size of the economy. The ratio of personal debt-to-disposable income is now 34 percentage points below pre-crisis levels (Chart 4). Chart 4Household Leverage Is Below Its Peak

Household Leverage Is Below Its Peak

Household Leverage Is Below Its Peak

U.S. corporate debt has moved in the opposite direction. Nevertheless, while the ratio of U.S. corporate debt-to-GDP has climbed to a record high, it is still quite low by global standards (Chart 5). Perhaps more importantly, corporate debt is generally held by non-leveraged institutions. If corporate defaults were to rise unexpectedly, the losses to lenders would not pose the same systemic risk to the financial sector as mortgage defaults did during the Global Financial Crisis. Chart 5U.S. Corporate Debt Is High, But It Is Higher Elsewhere

U.S. Corporate Debt Is High, But It Is Higher Elsewhere

U.S. Corporate Debt Is High, But It Is Higher Elsewhere

The Fed’s Reaction Function It is not surprising that the stock market sell-off accelerated in early October following Fed Chairman, and failed golfer, Jay Powell’s comment that interest rates were “far from neutral.” We think that worries that the Fed will tighten too quickly are misplaced. Yes, monetary policy operates with “long and variable lags.” However, financial conditions, which lead growth, can be observed in real time (Chart 6). Chart 6Global Financial Conditions Have Tightened

Global Financial Conditions Have Tightened

Global Financial Conditions Have Tightened

Most of the tightening in financial conditions since late September has been due to falling equity prices. Our baseline scenario envisions a gain of roughly 10% in the S&P 500 in 2019. A rebound in stocks of this magnitude will reverse most of the recent FCI tightening, thereby allowing the Fed to raise rates three times this year. But if equities continue to sag, the Fed will scale back further monetary tightening or even cut rates. The mere possibility of such a policy response reduces the odds of an FCI doom loop. A Mixed Bag Outside The U.S. The economic outlook is murkier outside the United States. Economic and financial imbalances are greater in the EM space and parts of Europe. Non-U.S. central banks also have less scope to respond to adverse shocks, either because of fears that looser monetary policy will spark capital outflows (as is the case in many emerging markets) or because of the presence of the zero-bound constraint on interest rates (as is the case in the euro area and Japan). Nevertheless, the situation is not that bad. EM assets have been fairly resilient over the past few months, at least in comparison to their developed economy counterparts (Chart 7). China’s credit impulse has actually perked up, an indication that while credit growth is falling, it is doing so at a slower pace. Chart 8 shows that the Chinese credit impulse is highly correlated with global industrial commodity prices. We still expect global growth to slow in the first half of 2019, but at this point, much of the slowdown has been discounted in asset markets. With that in mind, we are raising the stop on our short AUD/JPY trade to 10% and instituting a profit target of 15%. Chart 7EM Assets Have Been Outperforming Recently

EM Assets Have Been Outperforming Recently

EM Assets Have Been Outperforming Recently

Chart 8The Increase In China's Credit Impulse Bodes Well For Industrial Commodity Prices

The Increase In China's Credit Impulse Bodes Well For Industrial Commodity Prices

The Increase In China's Credit Impulse Bodes Well For Industrial Commodity Prices

The Perils Of Discrete Decision-Making One of the annoyances of being an investment strategist is that you often feel compelled to take discrete views on where the markets are heading. Are you bullish, bearish, or neutral? Actually, it is usually just bullish or bearish because most people regard neutral views as lacking in conviction and insight. This incentive structure is counterproductive. Not only does it cause analysts to turn a blind eye to incoming data that may challenge their thesis, it disregards how professional investors actually operate. Successful investors scale into positions as the market gets cheaper and scale out as it becomes more expensive. Trying to time the bottom (or the top) with exact precision is futile. With that in mind, we are going to tweak the way we make recommendations going forward in order to improve transparency, accountability, and accuracy. Rather than simply stating whether we are bullish, bearish, or neutral, we will assign the main asset classes a subjective score between zero and one hundred, with 0-to-40 being bearish, 40-to-60 being neutral, and 60-to-100 being bullish. We will adjust the score in every publication. To add analytic rigor to this framework, we will also compare our subjective model score with that of our MacroQuant model. Where Things Now Stand We downgraded global equities last June, but moved back to overweight following December’s post-FOMC meeting sell-off, as valuations reached that rather blurry line at which a modest equity overweight was warranted. Our subjective score for global equities currently stands at 65%, above the model’s estimate of 50%. Our moderately bullish view reflects our expectation that global growth will stabilize by mid-year and monetary policy will remain accommodative, even if the Fed raises rates by more than what the markets are currently discounting. Tempering our enthusiasm is the recognition that the business cycle is getting long in the tooth – especially in the U.S. – and that global equity valuations, while far cheaper than they were a few months ago, are still significantly less favorable than they were near past market bottoms (Chart 9). Chart 9Global Equity Valuations Have Improved

Global Equity Valuations Have Improved

Global Equity Valuations Have Improved

Regionally, we continue to favor U.S. stocks over other developed markets, and DM over EM more broadly. However, our conviction level on this view is not high, and we are prepared to revise it if it looks like global growth is accelerating, an outcome that would limit any further dollar strength (our subjective dollar score currently stands at 70%, below the model’s estimate of 92%). Reflecting our expectation of decent global equity returns in 2019 and our waning conviction to be underweight EM, we are taking profits on in our March-2019 EEM ETF put for a gain of 104%. Please note that our view on EM is more optimistic than that of Arthur Budaghyan, BCA’s chief emerging markets strategist, who continues to see considerable downside risks to EM assets. For now, Treasury yields are likely to rise in an environment where U.S. growth is strong enough to enable the Fed to continue raising rates. We assign the 10-year yield a score of 30%, which is close to our model estimate of 32%. Accordingly, we are removing our long June-2019 Fed funds futures contract hedge, and we are now solely outright short the December-2020 contract. Core European bond yields will increase, reflecting diminished excess capacity in the euro area and the end of ECB net asset purchases. U.K. yields should also grind higher, as the odds of a soft Brexit (or no Brexit) improve. Only in Japan will yields remain contained, thanks to the BoJ’s ongoing yield curve control regime. We do not expect spread product to have a banner year, but the current yield pick-up should be sufficient to ensure that risky credit outperforms cash. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Box 1 The Analytics Of Doom Loops When will a tightening in financial conditions stemming from lower equity prices and higher borrowing costs lead to a vicious circle of slower economic growth and even tighter financial conditions? The answer depends on how sensitive economic growth is to financial conditions in relation to how sensitive financial conditions are to growth. Figure 1 shows two equilibrium schedules, one for the economy (EE) and one for asset markets (AA). Both schedules slope downward. The EE schedule is downward-sloping because easier financial conditions boost growth. If growth is too strong given the prevailing level of financial conditions, economic activity will slow (Panel A). The AA schedule is downward-sloping because equity prices tend to fall and credit spreads rise when growth slows. If equity prices are too high and credit spreads are too narrow for a certain level of growth, then financial conditions will tighten (Panel B). Suppose economic growth is not very sensitive to changes in financial conditions, perhaps because imbalances in the economy are limited (Panel C). Then changes in financial conditions will be fleeting: A decline in equity prices or a widening in credit spreads will not hurt growth very much, allowing the stock market and credit market to quickly normalize. In contrast, suppose that economic growth is very sensitive to financial conditions, so much so that the EE schedule is flatter than the AA schedule. In this case, the economy will be vulnerable to self-reinforcing booms and busts (Panel D). In particular, a small random jump from U to UI will send the economy careening towards a doom loop of ever-weaker growth and tighter financial conditions.

Chart 10

Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Chart 11

Tactical Trades Strategic Recommendations Closed Trades

GAA DM Equity Country Allocation Model Update The GAA DM Equity Country Allocation model is updated as of December 31, 2018. The quant model reduced Spain’s large overweight to a slight overweight, and further downgraded the U.S. allocation. As a result, the model now has assigned overweight allocations to Germany, Switzerland, the Netherlands, Canada and Italy, with underweight allocations to the U.S., Japan, France and U.K. Australia and Sweden are now in the neutral zone, as shown in Table 1. Table 1Model Allocation Vs. Benchmark Weights

GAA Quant Model Updates

GAA Quant Model Updates

As shown in Table 2 and Chart 1, Chart 2 and Chart 3, the overall model outperformed the MSCI world benchmark by 38 bps in December, with a 48 bps of outperformance from Level 1 model offset by a 21 bps of underperformance from Level 2. Since going live, the overall model has outperformed by 96 bps, with Level 2 outperforming by 120 bps and level 1 outperforming by 57 bps. Table 2Performance (Total Returns In USD %)

GAA Quant Model Updates

GAA Quant Model Updates

Chart 1GAA DM Model Vs. MSCI World

GAA DM Model Vs. MSCI World

GAA DM Model Vs. MSCI World

Chart 2GAA U.S. Vs. Non U.S. Model (Level 1)

GAA U.S. Vs. Non U.S. Model (Level 1)

GAA U.S. Vs. Non U.S. Model (Level 1)

Chart 3GAA Non U.S. Model (Level 2)

GAA Non U.S. Model (Level 2)

GAA Non U.S. Model (Level 2)

Please see also the website http://gaa.bcaresearch.com/trades/allocation_performance. For more details on the models, please see Special Report, “Global Equity Allocation: Introducing The Developed Markets Country Allocation Model,” dated January 29, 2016, available at https://gaa.bcaresearch.com. Please note that the overall country and sector recommendations published in our Monthly Portfolio Update and Quarterly Portfolio Outlook use the results of these quantitative models as one input, but do not stick slavishly to them. We believe that models are a useful check, but structural changes and unquantifiable factors need to be considered too in making overall recommendations. GAA Equity Sector Selection Model Dear Client, As advised in our October 2018 Special Alert, we have suspended the GAA Equity Sector Selection Model due to the significant changes in the GICS sector classifications, implemented at the end of September. We will rebuild the model using the newly constituted sectors once full back data is available from MSCI, which we understood would be in December but which we have not received yet. We thank you for your understanding. Xiaoli Tang, Associate Vice President xiaoliT@bcaresearch.com Amr Hanafy, Research Associate amrh@bcaresearch.com

The Brexit tension remains high and may even intensify in early 2019 before a resolution arrives. Hence, while 2019 will offer a great opportunity to buy the pound, it will require a little patience. In contrast, Italy is de-escalating its brinkmanship…

Dear Client, We are sending you our last issue of the year, which contains a lighter fare than usual, highlighting 10 charts we find important. The first three charts tackle questions of Chinese growth, global activity and the outlook for the Federal Reserve. The other seven relate directly to the currency market. We will resume our regular publishing schedule on January 4th, 2019. The Foreign Exchange Strategy team would like to thank you for your continued readership and wish you and yours a joyful holiday season as well as a healthy, happy and prosperous 2019. Warm Regards, Mathieu Savary, Vice President Foreign Exchange Strategy mathieu@bcaresearch.com Feature 1) Chinese Growth Outlook Since the 19th National Congress of the Communist Party of China, Beijing has been focused on controlling debt growth. The Chinese leadership is worried that too much debt will lead to the dreaded middle-income trap, whereby a country’s development stalls once it achieves middle-income status. Because of Beijing’s laser focus on debt, Chinese growth, especially in the industrial sector, has slowed. Yet in the second half of 2018, Chinese policymakers have grown concerned by the deepening malaise in the domestic economy. Consequently, they have loosened policy, accelerating the issuance of local government bonds, letting the repo rate fall to 2.7% and cutting the reserve requirement ratio to 14.5%. Despite these measures, credit growth has continued to slow, hitting 16-year lows, and crucially, the shadow banking system is still contracting (Chart 1, left panel). While the supply of credit remains tepid, declining demand for credit is more concerning. China’s marginal propensity to save, as approximated by the gap between the growth of M2 and M1 money supply, is still rising. Historically, a rising marginal propensity to save leads to slowing industrial activity and slowing import growth (Chart 1, right panel). This implies that China will continue to weigh on global trade and global industrial activity. Thus, to turn growth around, Chinese policymakers will need to ease policy further. Chart 1AChinese Growth Will Slow Further (I)

Chinese Growth Will Slow Further (I)

Chinese Growth Will Slow Further (I)

Chart 1BChinese Growth Will Slow Further (II)

Chinese Growth Will Slow Further (II)

Chinese Growth Will Slow Further (II)

2) Global Growth And Inflation Outlook Already, the outlook for Chinese growth points to additional downside to global growth – something EM carry trades financed in yen are already sniffing out (Chart 2, left panel). The deterioration in the performance of those carry trades further amplifies the negative impulse emanating from China. If high-yielding EM currencies depreciate versus funding currencies like the yen, money is leaving those economies. Hence, EM liquidity conditions are tightening and financial conditions are deteriorating, reinforcing the leading property of EM carry trades vis-à-vis global industrial activity. Chart 2ASlowing Global Growth And Inflation (I)

Slowing Global Growth And Inflation (I)

Slowing Global Growth And Inflation (I)

Chart 2BSlowing Global Growth And Inflation (II)

Slowing Global Growth And Inflation (II)

Slowing Global Growth And Inflation (II)

Moreover, as telegraphed by the relative performance of EM bonds to EM equities, global inflation is set to peak soon, and then decelerate (Chart 2, right panel). This is a natural consequence of the deflationary impact of slowing Chinese growth and tightening EM liquidity conditions – the two most crucial factors lying behind the softness in global growth. Thus, financial markets are likely to remain volatile, at least until global policymakers have changed their tune enough to reverse global growth and inflation dynamics. 3) The Fed Is On Track To Hike More Than The Market Believes In its latest set of forecasts, the Federal Reserve may have been forced to adjust how much it will hike interest rates over the coming years. Nonetheless, by the end of 2020, the FOMC still anticipates having to increase interest rates by more than the -8 basis points currently priced into the futures curve. We are inclined to side with the Fed. U.S. growth may be slowing, but it will remain above trend in 2019. Additionally, the U.S. economy is most likely already at full employment, thus inflationary pressures are building. For the Fed, the labor market remains the fulcrum of potential inflation. As the left panel of Chart 3 shows, both the Atlanta Fed Wage Tracker and BLS average hourly earnings are growing at an accelerating pace, giving the Fed ammo to hike rates further. Moreover, the highly interest-sensitive housing sector has been a great source of concern for U.S. growth. However, now that this year’s surge in mortgage rates is being digested, mortgage applications are once again rebounding (Chart 3, right panel). This suggests that real estate activity will stabilize. Hence, even if the Fed pauses, it will still surprise markets to the upside over the coming 24 months. Chart 3AGood Reasons To Keep Hiking In 2019

Good Reasons To Keep Hiking In 2019

Good Reasons To Keep Hiking In 2019

Chart 3BGood Reasons To Keep Hiking In 2019

Good Reasons To Keep Hiking In 2019

Good Reasons To Keep Hiking In 2019

4) The Dollar Can Rally Even If U.S. Growth Falls Off A Cliff In our assessment, U.S. growth will slow next year, but will nonetheless remain above trend. However, if we are wrong and U.S. growth weakens much more, the dollar is unlikely to crater. As Chart 4 illustrates, periods of broad growth weakness – as measured by our U.S. economic diffusion index – often generate a strong – not weak – dollar. U.S. growth weakness often happens as global growth deteriorates. Since the U.S. economy exhibits a low beta to global industrial activity – the segment of the economy that contributes most to the variance in GDP growth – it follows that if a shock is global, the U.S. is likely to perform better than the rest of the world, leading to a strong dollar. Today, the downside risk is that the U.S. catches the cold that has hit the global economy. Hence, if U.S. growth has significantly more downside, it would suggest that economies outside the U.S. would suffer even more. The dollar should perform well in this environment. Chart 4The Dollar Doesn't Really Care If U.S. Growth Slows

The Dollar Doesn't Really Care If U.S. Growth Slows

The Dollar Doesn't Really Care If U.S. Growth Slows

5) The Dollar Versus Global Growth And Global Inflation The most important question to forecast the path of the dollar is where we stand in the global growth and inflation cycle. As Chart 5 shows, the dollar tends to perform most poorly early in the business cycle, when global growth is picking up but inflation remains muted (bottom-right quadrant), and late in the cycle when global growth has begun to weaken but inflation remains perky (top-left quadrant). The best time to hold the greenback is during global downturns, when both global growth and inflation are decelerating (bottom-left quadrant). With global industrial activity on a downtrend and inflation set to roll over soon, we are entering the bottom-left quadrant. As a result, the greenback should continue to rally on a trade-weighted basis, gaining most against the commodity currency complex. The yen may be the one currency bucking this trend, as in recent years it has become even more counter-cyclical than the dollar.

Chart 5

6) The Dollar Is A Momentum Currency One of the defining characteristics of the greenback is that from an investment-style perspective, it is a momentum currency. As the left panel of Chart 6 illustrates, among G-10 currencies, momentum continuation strategies work best for the USD. This is because of feedback loops present in the global economy.

Chart 6

Chart 6BMomentum Still Flashing A Greenlight For The Greenback (II)

Momentum Still Flashing A Greenlight For The Greenback (II)

Momentum Still Flashing A Greenlight For The Greenback (II)

Of the major economies, the U.S. is the least sensitive to global trade and global investment – a consequence of the low share of exports and manufacturing in GDP and employment. As a result, when global growth deteriorates, the U.S. economy experiences less of a slowdown and American rates of return decline less. Thus, money comes back into the U.S., lifting the dollar in the process. However, since there is USD 14-trillion in dollar-denominated foreign-currency debt, a rising dollar increases the cost of capital for these borrowers. The ensuing tightening in financial conditions hurts global growth, further enhancing the greenback’s appeal. The relationship goes in reverse once global growth improves. These powerful feedback loops explain why when the dollar strengthens, it remains stronger for longer than anyone anticipated, and vice versa when it weakens. Today, the momentum signal for the dollar remains positive (Chart 6, right panel). Along with slowing global growth, momentum was one of the key factors behind the dollar’s strength this year. If, as we expect, global inflation also weakens in the first half of 2019, the dollar will likely experience a beautiful first six months of the year. 7) Keep An Eye On Sino-U.S. Rate Differentials When one-year interest rate differentials between the U.S. and China widen, the DXY tends to strengthen (Chart 7, left panel). This is a reflection of global growth dynamics. U.S rates tend to rise relative to China when Chinese growth is decelerating. Since a slowing Chinese economy implies less intake of machinery and raw materials, a weaker China hurts Europe, Japan, EM and commodity producers a lot more than it affects the U.S. This lifts the dollar in the process. Moreover, so long as Chinese one-year interest rates keep falling versus the U.S., it also signals that any reflationary efforts by China have not yet had any impact on growth. Chart 7AU.S.-China Rate Differentials Point To A Stronger Dollar (I)

U.S.-China Rate Differentials Point To A Stronger Dollar (I)

U.S.-China Rate Differentials Point To A Stronger Dollar (I)

Chart 7BU.S.-China Rate Differentials Point To A Stronger Dollar (II)

U.S.-China Rate Differentials Point To A Stronger Dollar (II)

U.S.-China Rate Differentials Point To A Stronger Dollar (II)

This same rate differential between the U.S. and China also drives fluctuations in USD/CNY (Chart 7, right panel). Since falling relative Chinese rates are a symptom of a weaker Chinese economy, this relationship makes sense. Moreover, in recent years, more than against the dollar, Chinese policymakers have targeted the value of the CNY on a trade-weighted basis. Mechanically, if slowing Chinese growth flatters the trade-weighted dollar, it also forces USD/CNY up. This can further reinforce the strength in the broad trade-weighted dollar as a falling CNY is deflationary for the global economy. Because Chinese growth remains weak, we expect U.S. rates to continue to move higher vis-à-vis Chinese ones, lifting both the DXY and USD/CNY in the process. 8) EUR/USD: More Downside And A Complex Bottoming Process Ahead EUR/USD will suffer if global growth weakens and the dollar strengthens. On one hand, the European economy is much more sensitive to the Chinese and global industrial cycle than U.S. activity is. Our outlook for global growth therefore implies that the European Central Bank will find it difficult to raise rates in the fall of 2019, while the Fed is likely to surprise markets on the hawkish side. On the other hand, the simplest vehicle to bet on a strengthening dollar is to sell EUR/USD. Our fair-value model for EUR/USD currently pegs its equilibrium at 1.11 (Chart 8, left panel). However, EUR/USD never ends its downdrafts at its fair value – a consequence of its negative correlation with the dollar, a momentum currency that easily over- and under-shoots fair value. Thus, we expect the euro to find stability closer to 1.08. Chart 8AEUR/USD Will Bottom Later Next Year (I)

EUR/USD Will Bottom Later Next Year (I)

EUR/USD Will Bottom Later Next Year (I)

Chart 8BEUR/USD Will Bottom Later Next Year (II)

EUR/USD Will Bottom Later Next Year (II)

EUR/USD Will Bottom Later Next Year (II)

Moreover, inflationary dynamics do not suggest that EUR/USD is yet ripe for the taking. Since 2008, the gap between euro area and U.S. core CPI has been a reliable leading indicator for EUR/USD (Chart 8, right panel). In fact, this chart suggests that EUR/USD is more likely to bottom towards the second half of 2019; so as long as European inflation remains tepid, it will be hard for this currency to suddenly rebound and recoup the losses it has experienced this year. A complex bottom is more likely than a V-shaped one. 9) EUR/JPY: All About Bond Yields Even more so than USD/JPY, EUR/JPY remains beholden to trends in global bond yields (Chart 9). BCA’s view is that on a cyclical horizon of nine to 12 months, bond yields have upside. However, with global growth and inflation likely to decelerate further in the first half of 2019, safe haven assets could remain well bid over that timeframe. This implies the time to buy EUR/JPY is not now, and that a better buying opportunity will emerge once global growth stabilizes. Thus, we remain short EUR/JPY for the time being, a view we have held since the beginning of 2018. Chart 9Risks To Global Growth Equals EUR/JPY Downside

Risks To Global Growth Equals EUR/JPY Downside

Risks To Global Growth Equals EUR/JPY Downside

10) EUR/GBP Is At Risk At the current juncture, EUR/GBP is a binary bet: Either a hard Brexit comes to fruition, in which case U.K. real rates plummet and British inflation rises above 5%, creating a deeply pound-bearish environment. Alternatively, a soft Brexit (or even no Brexit) materializes, in which cases British real rates have upside, the Bank of England has a freer hand to combat inflationary pressures, and the pound can rally. With EUR/GBP currently trading toward the top of its historical distribution, we believe it is an attractive shorting opportunity (Chart 10). Marko Papic, BCA’s chief geopolitical strategist, assigns a less than 10% probability of a hard Brexit. As such, the pound is more likely to exist in a soft/no-Brexit world in 12 months than otherwise. This means the pound should be-revalued. Chart 10Sell EUR/GBP

Sell EUR/GBP

Sell EUR/GBP

We prefer playing the pound’s strength against the euro rather than the dollar, as we expect the dollar to rally further in the first half of 2019, so cable would be swimming against the tide. Moreover, when the dollar strengthens, historically EUR/GBP weakens, as the GBP has a lower beta to the dollar than the euro does. Hence, our dollar view is also consistent with a lower EUR/GBP. Mathieu Savary, Vice President Foreign Exchange Strategy mathieu@bcaresearch.com Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

Highlights Asset allocation: Start 2019 with an overweight to industrial commodities versus equities. Await an oversold sell-off signal on the 65-day fractal dimension to go tactically overweight equities versus cash. Equities: Start 2019 with a cyclical equity sector tilt, but become more defensive as the global economy inevitably flips into a down-oscillation later in 2019. Start tactically overweight Italy’s MIB versus the Eurostoxx. Bonds: Initiate a bond yield convergence play: long 10-year Italian BTPs versus Spanish Bonos. Currencies: Start 2019 short EUR/JPY combined with long EUR/USD. There will be a great opportunity to buy the GBP, but not yet. Alternatives: A compelling buying opportunity for the cryptocurrencies Litecoin and Ethereum. Feature 2019 will present investors a mirror-image pattern to 2018. Through most of 2018, global growth was decelerating while inflation was accelerating. Now this configuration is flipping: global growth is rebounding while inflation is set to collapse. Growth To Rebound, Then Fade Global growth has entered an up-oscillation, for which the evidence is irrefutable: Industrial (non-oil) commodities are strongly outperforming equities, and rising even in absolute terms (Chart of the Week and Chart 2). Emerging markets are strongly outperforming developed markets (Chart 3). Financials are outperforming the broad equity market (Chart 4). Sweden’s manufacturing PMI – a bellwether of global activity – is rebounding strongly (Chart 5). Perhaps most importantly, China’s 6-month credit impulse has gone vertical (Chart 6). Chart of the WeekNon-Oil Commodities Are Strongly Outperforming Equities

Non-Oil Commodities Are Strongly Outperforming Equities

Non-Oil Commodities Are Strongly Outperforming Equities

Chart I-2Non-Oil Commodities Are Recovering In Absolute Terms Too

Non-Oil Commodities Are Recovering In Absolute Terms Too

Non-Oil Commodities Are Recovering In Absolute Terms Too

Chart I-3Emerging Markets Are Strongly Outperforming Developed Markets

Emerging Markets Are Strongly Outperforming Developed Markets

Emerging Markets Are Strongly Outperforming Developed Markets

Chart I-4Financials Are Outperforming

Financials Are Outperforming

Financials Are Outperforming

Chart I-5Sweden’s Manufacturing PMI Is Up Sharply

Sweden's Manufacturing PMI Is Up Sharply

Sweden's Manufacturing PMI Is Up Sharply

Chart I-6China’s 6-Month Credit Impulse Has Gone Vertical

China's 6-Month Credit Impulse Has Gone Vertical

China's 6-Month Credit Impulse Has Gone Vertical

Taken together, this is compelling evidence of a growth rebound, even if it is modest. Crucially, such up-oscillations tend to last at least six to eight months. Hence, equity sector performances, which always take their cue from global growth, will follow a mirror-image pattern in 2019 to that in 2018. Bottom Line: Start the year with an overweight to industrial commodities versus equities and a cyclical equity sector tilt, but prepare to fade to a more defensive tilt as the global economy inevitably flips into a down-oscillation later in 2019. Inflation Is The Dog That Will Not Bark There are not many things that are certain in the economy, but a racing certainty for early 2019 is that headline inflation will collapse. This is because the plunge in the crude oil price – 40 percent so far and getting worse by the day – is about to feed through into headline consumer price indexes (Chart 7 and Chart 8). Inevitably, it will seep through into core inflation too, via the impact on energy dependent prices such as transport costs. Chart I-7Headline Inflation Will Collapse In Europe

Headline Inflation Will Collapse In Europe

Headline Inflation Will Collapse In Europe

Chart I-8Headline Inflation Will Collapse In The U.S.

Headline Inflation Will Collapse In The U.S.

Headline Inflation Will Collapse In The U.S.