Euro Area

The main risk confronting Europe’s major institutions such as the ECB, the EU Council, and the EU Commission is an existential risk. This is because the very existence of the pan-European project relies on the ongoing (largely) unanimous support of a…

Highlights Five risks to our bullish dollar stance need to be monitored: further weakness in the S&P 500; rebounding gold prices; stabilizing EM exchange rates and bond prices; Spanish bank stocks at multi-decade lows; and large, long-exposure by speculators to the greenback. However, China's lackluster response to stimulus and the U.S.'s domestic strength still favor the dollar. In fact, the key force likely to cause U.S. growth to converge toward weaker global growth will be a stronger U.S. dollar. Feature BCA has a positive bias toward the dollar for the coming six to nine months. Admittedly, the dollar is expensive, but cyclical determinants still favor a rally. The Federal Reserve is hiking rates as the U.S. economy is at full capacity and goosed up by fiscal injections. Yet global growth is very wobbly. This combination is a potent cocktail for USD strength. Despite these key sources of support, we cannot be dogmatic, especially as financial markets are anticipatory mechanisms, and therefore the dollar could have already priced in some of these developments. As such, this week we explore the key risks to our dollar view. While serious threats for the dollar exist over the upcoming two to three quarters, the key macro and financial drivers remain dollar bullish. The Threats 1) The S&P Sells Off Further The MSCI EAFE index, expressed in USD terms, is down nearly 20% since its January 2018 highs. Meanwhile, the S&P 500 has fallen 9% since its recent all-time high, or 7% vis-Ã -vis where it stood in late January. The risk is that as the global economic slowdown deepens, investors end up selling their good assets along with their bad ones. This means the S&P 500 could fall more. In fact, our colleague Peter Berezin writes in BCA's Global Investment Strategy that U.S. equities could fall an additional 6% from current levels before finding a durable support.1 The problem for the dollar is not whether stock prices fall. It is about what it means for the Fed. Until earlier this week, equity weakness had no impact at all on bonds. However, now, weak stock prices are dragging down U.S. bond yields. Moreover, while the U.S. yield curve slope steepened between August 24 and October 5, it is flattening anew (Chart I-1). All these market moves suggest investors are beginning to price out anticipated interest rate hikes. If U.S. stocks were to fall further, these dynamics would most likely deepen. However, since there is little monetary tightening to price out of the European or Japanese interest rate curves, such a move would likely lead to a dollar-bearish narrowing of interest rate differentials. Chart I-1It Took A Stock Market Rout For Investors To Reconsider The Fed's Path

It Took A Stock Market Rout For Investors To Reconsider The Fed's Path

It Took A Stock Market Rout For Investors To Reconsider The Fed's Path

2) Gold Is Rebounding Keynes might have called gold a barbarous relic of a bygone era, but as an extremely long-duration asset with no cash flow, the yellow metal remains an important gauge of global monetary and liquidity conditions. As the stock of dollar foreign-currency debt is large, a strong dollar is synonymous with tightening global liquidity conditions. Unsurprisingly, since 2017, gold and the dollar have been tightly negatively correlated (Chart I-2). However, since October, this correlation has been breaking down. Both the dollar and gold are moving up. This suggests that the recent increase in U.S. interest rates and in the dollar might not be as deleterious for the world as markets are currently anticipating. Chart I-2Is Gold Not Hating A Strong Dollar Anymore?

Is Gold Not Hating A Strong Dollar Anymore?

Is Gold Not Hating A Strong Dollar Anymore?

Moreover, gold prices often lead EM asset prices. Since gold prices are highly sensitive to global liquidity, this makes sense. When the yellow metal sniffs out whiffs of reflation, it is only a matter of time before EM assets do as well. Since a rally in EM assets would lead to an easing in EM financial conditions, this easing would improve the global growth outlook (Chart I-3). Hence, rising gold prices might be a sign that while investors are increasingly negative on global industrial activity, the light at the end of the tunnel could be around the corner. The dollar would suffer if the outlook for global growth were to improve. Chart I-3EM Financial Conditions Hold The Key To Global Growth

EM Financial Conditions Hold The Key To Global Growth

EM Financial Conditions Hold The Key To Global Growth

3) EM Currencies And EM High-Yield Bonds Stabilizing Something strange is happening. While EM equity prices are still falling, EM high-yield bonds and currencies are not. In fact, EM FX and EM debt prices bottomed at the beginning of September, despite rising U.S. interest rates. However, since then, EM stock prices denominated in USD terms have fallen nearly 10% (Chart I-4). EM exchange rates and yields are the most important determinants of EM financial conditions. This suggests that despite EM stock prices falling fast, EM financial conditions may not be deteriorating as quickly as assumed. Chart I-4Are EM Financial Conditions Easing?

Are EM Financial Conditions Easing?

Are EM Financial Conditions Easing?

This market action is in fact consistent with the development we highlighted in the gold market. We must therefore maintain a watchful eye on EM bonds and EM FX. Further meaningful improvement in these assets, while not BCA's base-case, would dangerously challenge our view that global industrial activity slows further, undermining our dollar-bullish view. 4) Spanish Banks Near Post-2008 Lows As we highlighted in August, Spanish banks are the most exposed major banks in the world to EM woes (Chart I-5).2 The exposure of the Spanish banking sector to the weakest EM economies represents 170% of capital and reserves, which is driving the entire euro area's exposure to these markets to 32% of Eurozone banks' capital and reserves. Chart I-5Who Has More Exposure To EM?

Risks To The Dollar View

Risks To The Dollar View

The weakening in EM expected growth and the fall in EM currencies is a risk for Spanish banks. However, Spanish banks also maintain a large chunk of their EM exposure in wholly or partly owned subsidiaries. This means that while an EM crisis will definitely have an important impact on Spanish bank earnings, the impact on the balance sheet of Spanish banks is likely to be more limited. However, Spanish banks now trade in line with the levels that prevailed in Q1 2009, Q3 2012 and Q1 2016 (Chart I-6). In other words, Spanish banks are already pricing in a crisis, especially after the Spanish Supreme Court ruled that banks - not customers - must pay mortgage duties. Chart I-6Spanish Banks Are Discounting Plenty Of Bad News

Spanish Banks Are Discounting Plenty Of Bad News

Spanish Banks Are Discounting Plenty Of Bad News

While markets may not be the most efficient mechanism when it comes to pricing future shocks, markets are very efficient at lateral pricing - i.e. the pricing of an event in one market, even if wrong, will be equally reflected in other markets. If the impact of an EM crisis is fully priced into Spanish banks, the impact of such a crisis is likely to also be reflected in the expectations of what the European Central Bank will do over the coming quarters, and thus it is also priced into the euro. The pessimism already present in Spanish banks and euro area financial equities may explain why the euro has not cracked below its August 17 lows, while global stock prices have. The bad news could simply already be baked into the cake! If Spanish bank stocks rebound, the dollar is likely to suffer; if they break down, the dollar will likely rally more. 5) Speculators Are Already Long The Dollar For the dollar to rise further, someone needs to buy it. The problem is that speculators have already been buying the greenback, and they are now aggressively long the dollar (Chart I-7). This means that it may become more difficult to find new buyers for U.S. dollars, especially as investors may be in the process of unloading their U.S. equities. To be fair, while it is true that the net speculative positions are elevated, they also can remain so for extended periods. Chart I-7Investors Are Long The Dollar

Investors Are Long The Dollar

Investors Are Long The Dollar

Bottom Line: There are important risks to our dollar-bullish view that we need to closely monitor. They are: the global stock selloff migrating to the U.S., which could prompt investors to price out Fed rate hikes; gold rebounding, which might indicate marginal improvement in global liquidity conditions; EM exchange rates and high-yield bonds not weakening anymore, which could result in an easing in financial conditions, ending the deterioration in global growth; Spanish banks potentially already pricing in a dire outcome in EM; and speculators being already long the dollar. Despite these Risks, Why Do We Still Like The Dollar? The first reason relates to global growth. Ultimately, the dollar is a counter-cyclical currency. When global growth weakens, the dollar strengthens. China continues to generate potent headwinds for the world economy. Beijing has been stimulating the Chinese economy, but this stimulus is having a muted impact. As Arthur Budaghyan writes in the week's Emerging Market Strategy report, China's monetary stimulus is falling flat.3 Not only are excess reserves in the banking sector rather meager, Chinese banks are not showing a deep propensity to lend. It is not just about the behavior of Chinese banks: Chinese firms are also not displaying a high propensity to spend and borrow, which is weighing on the velocity of money in China (Chart I-8). As a result, this means that liquidity injections are not generating much impact in terms of loan growth and economic activity. Chart I-8Chinese Stimulus Is Falling Flat Because Economic Agents Are Cautious

bca.fes_wr_2018_10_26_s1_c8

bca.fes_wr_2018_10_26_s1_c8

This is evident when looking at two variables. China's Li-Keqiang Index, our preferred measure of Chinese industrial activity, has stopped rebounding. In fact, it is currently weakening anew, which suggests that Chinese growth, despite all the supposed easing in monetary conditions, is not responding (Chart I-9, top panel). Moreover, Chinese infrastructure spending is also contracting at its fastest pace in 14 years (Chart I-9, bottom panel). Further, the slowing in Chinese real estate sales suggests that construction will not come to the rescue, especially as vacancy rates in Chinese major cities currently stand at elevated levels. Chart I-9Chinese Growth Outlook Is Deteriorating Anew

Chinese Growth Outlook Is Deteriorating Anew

Chinese Growth Outlook Is Deteriorating Anew

We continue to monitor our China Play index (Chart I-10) to see if China is showing any underlying improvement, but the rally evident from June to October is now dissipating. The impact of stimulus thus looks like it is leaving investors wanting for more. Yet, as Matt Gertken and Roukaya Ibrahim argue in this week's Geopolitical Strategy service, additional stimulus will be limited as Xi Jinping is not yet abandoning his three battles against indebtedness, pollution and poverty.4 Hence, we expect China to remain a significant drag on global growth over the coming two to three quarters. Chart I-10China-Related Plays Are Losing Momentum

China-Related Plays Are Losing Momentum

China-Related Plays Are Losing Momentum

The second issue that supports our bullish-dollar stance is the mechanism required for U.S. and global growth to converge. As Ryan Swift argues in BCA's U.S. Bond Strategy service, U.S. growth will not be able to avoid the gravitational pull of a weaker global economy.5 The type of divergence currently on display between the global and U.S. Leading Economic Indicators (LEIs) is generally followed by a deteriorating U.S. growth outlook (Chart I-11). Chart I-11U.S. Growth Ultimately Converges With The Rest Of The World

U.S. Growth Ultimately Converges With The Rest Of The World

U.S. Growth Ultimately Converges With The Rest Of The World

However, this weakening in U.S. growth won't happen out of nowhere. Either there will be domestic vulnerabilities that prompt the U.S. to become more sensitive to foreign shocks, or the dollar will force this adjustment. Today, unlike in 2015 and 2016, the sales-to-inventory ratio does not point to any imminent decline in U.S. industrial activity; to the contrary, it suggests further improvements in the coming months (Chart I-12). This leaves the dollar as the main culprit to put the brakes on U.S. growth. Chart I-12U.S. Domestic Fundamentals Are Fine

U.S. Domestic Fundamentals Are Fine

U.S. Domestic Fundamentals Are Fine

Since 2009, the greenback has been very responsive to the relative growth outlook between the U.S. and the rest of the world. The accumulated gap between the U.S. and global LEIs shows the total impact of growth divergences. This indicator has done a good job at foretelling how the dollar will trade (Chart I-13). The dollar tends to respond to U.S. growth outperformance. Only once the dollar has rallied enough to meaningfully tighten U.S. financial conditions does the U.S. growth outlook deteriorate vis-Ã -vis the rest of the world. Currently, this chart suggests we are nowhere near having reached a chokepoint for U.S. growth. Chart I-13A Higher Dollar Needed For U.S. Growth To Resist The Gravitational Pull From The Rest Of The World

A Higher Dollar Needed For U.S. Growth To Resist The Gravitational Pull From The Rest Of The World

A Higher Dollar Needed For U.S. Growth To Resist The Gravitational Pull From The Rest Of The World

Since the Fed remains quite unconcerned by the weakness in global growth and global stock prices, we expect that world financial markets will have to plunge deeper, the dollar to rally higher and U.S. financial conditions to tighten further before the FOMC shows enough concern to hurt the dollar. We are not there yet. Bottom Line: The absence of a meaningful response by the Chinese economy to stimulus suggests that China may have hit a debt wall. This implies that Chinese growth remains fragile and therefore a drag on global growth. Hence, international economic activity and trade will continue to provide an important tailwind for the U.S. dollar. Meanwhile, the U.S. economy is not displaying enough domestic vulnerabilities to be overly sensitive to the softness in global growth. Instead, more rounds of dollar strength will be required to force U.S. growth to converge lower toward global economic activity. As such, these two forces remain powerful enough to overweight currency exposure to the USD within global portfolios. That said, the five risks described in the previous section must be kept in mind. At the current juncture, they only warrant buying a few hedges, such as our long NZD/USD recommendation, but they do not warrant underweighting the greenback. Mathieu Savary, Vice President Foreign Exchange Strategy mathieu@bcaresearch.com 1 Please see Global Investment Strategy Special Report, "Chinese Stimulus: Not so Stimulating", dated October 26, 2018, available at gis.bcaresearch.com 2 Please see Foreign Exchange Strategy Special Report, "The Bear And The Two Travelers", dated August 17, 2018, available at fes.bcaresearch.com 3 Please see Emerging Markets Strategy Weekly Report, "China: Stimulus, Deleveraging And Growth", dated October 25, 2018, available at ems.bcaresearch.com 4 Please see Geopolitical Strategy Special Report, "China Sticks To The "Three Battles", dated October 24, 2018, available at gps.bcaresearch.com 5 Please see U.S. Bond Strategy Weekly Report, "Waiting For Peak Divergence", dated October 23, 2018, available at usbs.bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. has been mixed: Markit Services PMI outperformed expectations, coming in at 54.7. This measure also increased from the previous month's reading of 53.5. However, durable good ex-defense month-on-month growth underperformed expectations, coming in at -0.6%. Finally, monthly new homes sales underperformed expectations, coming in at an annualized pace of 553 thousand. DXY has appreciated by 0.8% this week. We are bullish on the U.S. dollar on a cyclical basis. Furthermore, momentum, one of the strongest predictive factors for the dollar continues to be positive. Finally, global growth should continue to slowdown, as the monetary tightening by Chinese authorities starts to weigh on the global industrial cycle. Report Links: In Fall, Leaves Turn Red, The Dollar Turns Green - October 12, 2018 Policy Divergences Are Still The Name Of The Game - August 14, 2018 The Dollar And Risk Assets Are Beholden To China's Stimulus - August 3, 2018 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

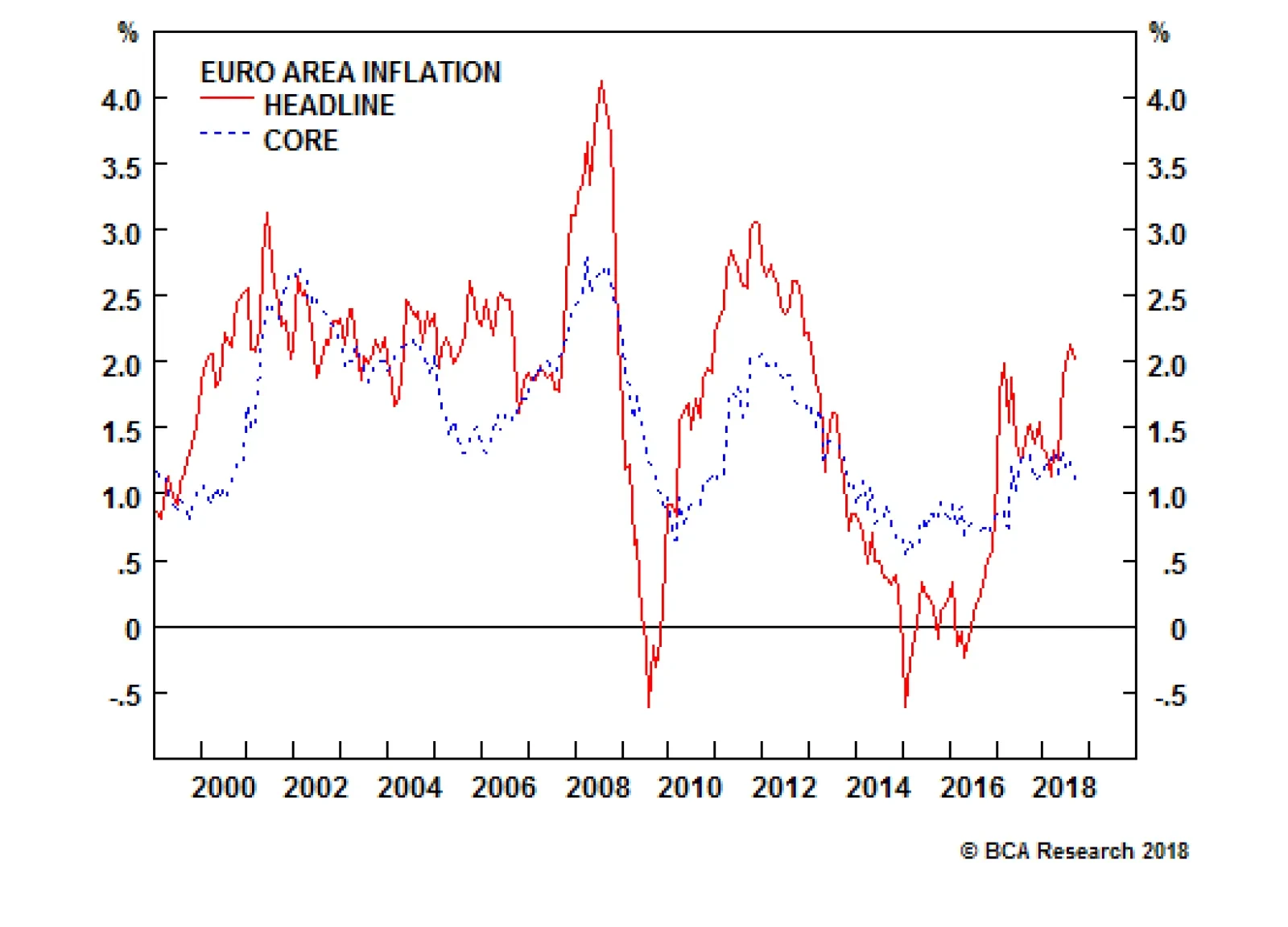

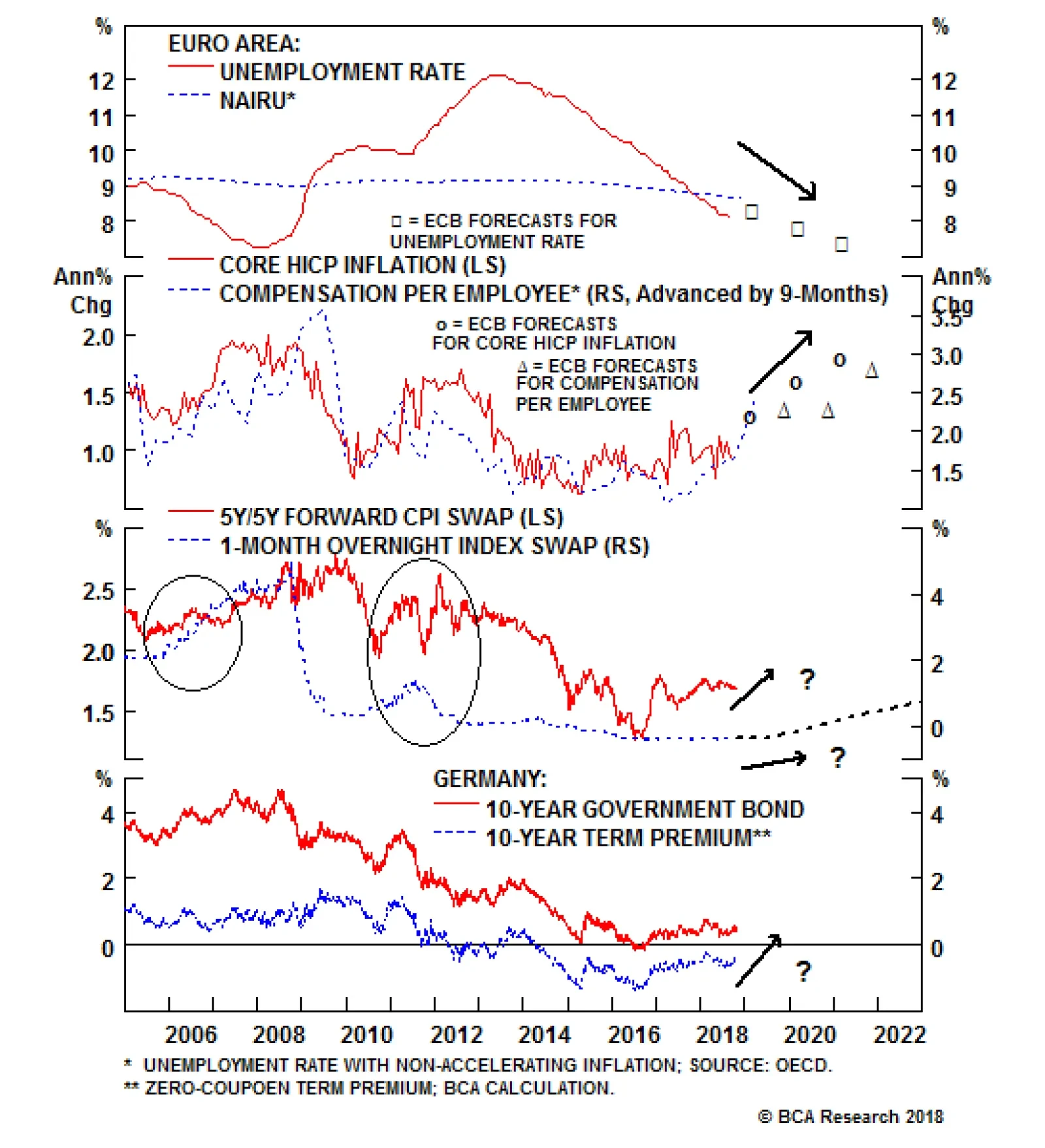

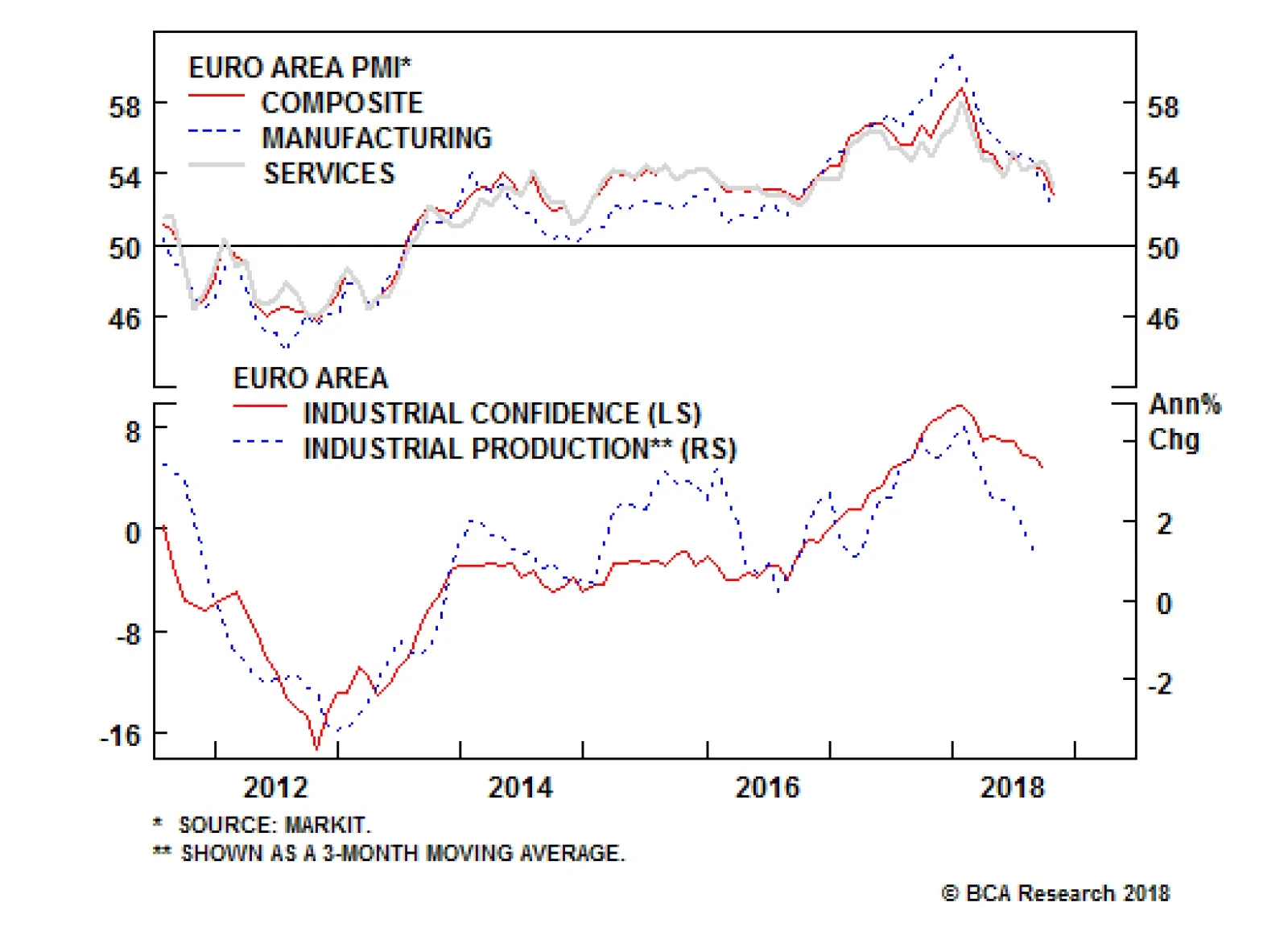

Recent data in the euro area has been negative: Markit Manufacturing PMI surprised to the downside, coming in at 52.1. Moreover, Markit Services PMI also underperformed expectations, coming in at 53.3. Finally, private loan yearly growth surprised negatively, coming in at 3.1%. EUR/USD has fallen by 0.8% this week. We are bearish on the euro on a cyclical basis, as inflationary pressures continue to be too weak in the euro area for the ECB to start raising rates. Moreover, the fact that the euro area's economy is highly dependent on exports, makes it very sensitive to global growth and emerging markets. This means that the tightening by Chinese authorities should impact the euro area economy negatively, and consequently, put downward pressure on EUR/USD. Report Links: Will Rising Wages Cause An Imminent Change In Policy Direction In Europe And Japan? - October 5, 2018 Policy Divergences Are Still The Name Of The Game - August 14, 2018 Time To Pause And Breathe - July 6, 2018 The Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan has been mixed: The leading economic Index outperformed expectations, coming in at 104.5. However, the coincident index surprised to the downside, coming in at 116.7. USD/JPY has been flat this week. We are neutral on the yen on a tactical basis, given that the current risk-off environment should continue to help safe havens like the yen. However, we are bearish on the yen on a cyclical basis, as inflation expectations are not well anchored in Japan. This means that the BoJ will continue to conduct ultra-dovish monetary policy for the foreseeable future, putting a cap on how high the yen can rise. Report Links: Will Rising Wages Cause An Imminent Change In Policy Direction In Europe And Japan? - October 5, 2018 Rhetoric Is Not Always Policy - July 27, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

GBP/USD has decreased by 1.5% this week. Given the lack of a geopolitical risk premium embedded into the pound, we expect GBP volatility to remain elevated. This means that any hiccups in Brexit negotiations could bring about some downside for the pound. Furthermore, inflation should remain contained, even amid a tight labour market. This is mainly because inflation dynamics in the U.K. are much more driven by the external sector, as imports represent a very large portion of British final demand. Given that the pound has remained stable this year, inflation will remain subdued. We are currently short GBP/NZD in our portfolio, to take advantage of the dynamics mentioned above. Report Links: Clashing Forces: The Fed And EM Financial Conditions - October 19, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Inflation Is In The Price - June 15, 2018 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

AUD/USD has been flat this week. We are most bearish on this currency within the G10, given that the AUD is highly sensitive to the Chinese industrial cycle, which will continue to slow down, as Chinese authorities keep cleaning credit excesses in the economy. Moreover, policy tightening by the Fed will provide a further headwind to cyclical plays like the AUD. We are short AUD/CAD within our portfolio, as we believe that the oil currencies should fare better than other commodity currencies, given that OPEC supply cuts, as long as Iranian sanction in oil will keep upward pressure on oil prices. Report Links: Policy Divergences Are Still The Name Of The Game - August 14, 2018 What Is Good For China Doesn't Always Help The World - June 29, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

NZD/USD has been flat this week. We are positive on the New Zealand dollar, particularly against the GBP, as there is very little room for kiwi rate expectations to fall. Moreover, this currency should also outperform the Australian dollar, given that New Zealand is less exposed to the Chinese industrial cycle than Australia. Nevertheless, we remain bearish on the NZD on a long-term basis, given that the new government proposals to reduce immigration and add an unemployment mandate to the RBNZ will lower the neutral rate in New Zealand, which will limit the central bank's ability to tighten monetary policy. Report Links: Clashing Forces: The Fed And EM Financial Conditions - October 19, 2018 In Fall, Leaves Turn Red, The Dollar Turns Green - October 12, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada has been negative: Core inflation underperformed expectations, coming in at 1.5%. This measure also decreased form 1.7% last month. Headline inflation also surprised to the downside, coming in at 2.2%. This measure decreased significantly, coming down from 2.8% the previous month. The Bank of Canada increased rates to tk% on Wednesday, and highlighted the potential for additional rate hikes over the coming 12 months. USD/CAD has been mostly flat this week. The upside in the CAD versus the USD is likely to be limited as the policy tightening by the BoC now seems well anticipated by market participants. To take advantage of this reality, we went short CAD/NOK in our portfolio. This cross also serves as a hedge to our long dollar view, given its positive correlation to the DXY. Despite some headwinds, the CAD should outperform the AUD, as we expect that oil will do better than base metals within the commodity complex. Report Links: Clashing Forces: The Fed And EM Financial Conditions - October 19, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Inflation Is In The Price - June 15, 2018 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

EUR/CHF has fallen by 0.5% this week, as investors have grown worried with the recent sell off in equities. We are bearish on the franc on a cyclical basis, given that inflation in Switzerland is still too weak for the SNB to move away from their ultra-dovish monetary policy. Moreover, Helvetic real estate prices should continue to fall, as the restrictions on immigration put forth by the Swiss government since 2014 should continue to weigh on housing demand. This will further hamper the ability of the SNB to tighten its extraodinarly accommodative monetary policy. That being said, EUR/CHF could continue to fall in the near term, as money flows into safe heaven assets amid the current sell off in equities. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

USD/NOK has risen by 0.9% this week. As expected, yesterday the Norges Bank left rates unchanged at 0.75%. In its report, the Norwegian central bank highlighted that although economic growth has been a little lower than anticipated, inflation has been somewhat higher than expectations. We are bullish on the krona against the Canadian dollar, given that rate hike expectation in Canada are much more fully priced in than in Norway even though the inflationary backdrop is very similar. Moreover, we are positive on the krone relatively to other commodity currencies like the AUD or the NZD, as we expect oil to outperform other commodities thanks to supply cuts by OPEC and sanctions against Iran. Report Links: Clashing Forces: The Fed And EM Financial Conditions - October 19, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

USD/SEK has rallied by 1% this week. We are positive on USD/SEK on a short-term basis, given that the SEK is the currency which is most negatively affected by the strength of the U.S. dollar. Furthermore, tightening by Chinese authorities should also weigh on the krona, given that the Swedish economy is very levered to the global industrial cycle, as many of its exports are intermediate goods that are then re-exported to emerging markets. That being said, we are bullish on the krona on a longer-term basis, as the Riksbank is on the verge of beginning a tightening cycle as imbalances in the Swedish economy are only growing more dangerous. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

Highlights We do not view October's equity downdraft as a signal to further trim risk assets to underweight. Nonetheless, stocks have not yet fallen enough to justify buying either. The economic divergence between the U.S. and the rest of the world is intensifying and showing up in relative EPS trends. We believe earnings growth is set to drop sharply in the Eurozone and Japan. The viciousness of the bond selloff in October is worrying. The good news is that the Treasury curve steepened and the selloff mostly reflected higher real yields, rather than inflation expectations. Both facts suggest that the Treasury rout was reflective of strong U.S. growth, rather than a signal that the Fed is overly restrictive. Our sense is that the fed funds rate has not yet reached the economic choke point, but it is critical to watch for signs of trouble. This month we focus on key monetary indicators. Our "R-Star" indicator is deteriorating, but is not yet in the danger zone for risk assets. It is possible that we will upgrade risk assets back to overweight if stocks in the developed markets cheapen further, as long as our monetary indicators are not flashing red and the U.S. earnings backdrop remains upbeat. However, the risks are formidable and show no signs of abating. Indeed, our global economic indicators continue to deteriorate and we might be headed for a brief manufacturing recession outside of the U.S. A Democratic win in the U.S. mid-terms might spark a knee-jerk equity selloff, but Congress is unlikely to unravel any of the fiscal stimulus currently in place through 2019. The Administration's foreign policy remains a larger risk for equities. Our high conviction view is that President Trump will continue to use a "maximum pressure" approach for Iran and China that will spark additional fireworks. Another growing risk is an oil price spike above US$100/bbl in early 2019, causing significant economic damage. Chinese policy stimulus is underwhelming and the credit impulse remains weak. In the absence of real policy action in China, the prospect of continuing Fed tightening means that it is too early to bottom-fish in emerging markets. The market is still underestimating the U.S. inflation outlook and the amount of Fed tightening over the next 12-18 months. We continue to recommend a neutral stance on global equities (with a preference for developed over emerging markets), a below-benchmark duration bias, and an overweight allocation in cash. Feature October's market action confirmed that we have entered a period of elevated volatility as investors digest the inevitability of rising U.S. interest rates. We do not view the downdraft in equity markets as a signal to further trim risk asset exposure to underweight. Nonetheless, stocks have not yet fallen enough to justify buying either. We took profits and downgraded risk assets to benchmark in June, placing the proceeds into cash. Our primary motivation was the advanced nature of the U.S. economic cycle, stretched valuations, heightened geopolitical tensions, the risk of a Chinese "hard landing" and upside potential for U.S. inflation and global bond yields. We did not foresee a recession either in the U.S. or the other major economies in the near future. Nonetheless, we concluded that the risk/reward balance did not favor staying overweight risk assets. A number of culprits could be blamed for October's pullback, but in reality the market has been primed for some profit-taking for a long while and so any little excuse could have been used by investors to sell. Fed Chair Powell's "long way to go" comment seemed to push the teetering equity market over the edge. He challenged the market's view that the fed funds rate is getting close to neutral, implying that the Fed is not close to pushing the pause button. The Treasury curve steepened as the market discounted a higher cyclical peak in the fed funds rate. Could it be that bond yields have reached a "choke point" where tightening financial conditions are derailing the economic expansion? The global economic deceleration is intensifying, but the U.S. economy still appears to be enjoying solid momentum outside of housing. We do not yet see any major dark clouds forming in the U.S. corporate earnings picture either, as discussed below. Moreover, the bond selloff in October mostly reflected rising real yields (rather than inflation expectations), and the curve steepened. Both facts suggest that the Treasury selloff was reflective of U.S. strong growth, rather than a signal that the Fed is now outright restrictive. Nonetheless, the issue is particularly tricky in this cycle because the equilibrium, or neutral, fed funds rate is undoubtedly somewhat lower than in past expansions. Given the uncertain level of the neutral rate, investors must be on the lookout for signs that interest rates are beginning to bite. Markets And The Fed Cycle BCA has long viewed financial markets through the lens of money and credit. This includes a framework that involves the Fed policy cycle. We begin by decomposing the fed funds rate cycle into four phases based on the interaction between the level of rates and their direction, as follows (Chart I-1 and Chart I-2): Phase I begins with the first rate hike of a new tightening cycle and ends when the fed funds rate crosses above our estimate of the equilibrium rate (shown as a dashed line in Charts I-1 and I-2). Phase II represents the latter stages of the tightening cycle, when the Fed hikes its target rate above equilibrium in a deliberate effort to cool an overheating economy. Phase III represents the early stage of the easing cycle. It begins with the first rate cut from the peak and lasts until the Fed cuts its target rate below equilibrium. Phase IV represents the late stage of the easing cycle. It encompasses both the period when the fed funds rate breaks below its equilibrium level until it bottoms. Chart I-1Stylized Fed Rate Cycle

November 2018

November 2018

Chart I-2Fed Funds Rate And Equilibrium

Fed Funds Rate And Equilibrium

Fed Funds Rate And Equilibrium

The tough part is estimating the neutral level of the fed funds rate. It is a theoretical concept - the level that is consistent with an economy at full employment with no upward or downward pressure on inflation or growth. The Fed lifts the fed funds rate above neutral when it wishes to dampen the economy and temper inflationary pressure. Economic theory ties the equilibrium interest rate to the pace of expansion of the supply side of the economy, or potential GDP growth. Our approach is to combine the CBO's estimate of potential GDP growth with a smoothed version of the actual fed funds rate, to account for the fact that the equilibrium rate periodically deviates from potential growth. The historical track record of this framework is compelling. The latest update of our analysis of equity returns during the four phases was published by BCA's U.S. Investment Strategy Service.1 The level of the fed funds rate relative to its equilibrium has mattered much more than the direction of rates for historical S&P 500 price returns (Table I-1 and I-2). Price returns during Phases I and IV (when the fed funds rate is below equilibrium) trounce returns during Phases II and III (when the funds rate is in restrictive territory). This is especially the case after adjusting returns for inflation. Table I-1Tight Policy Is Hazardous To Stocks' Health, ...

November 2018

November 2018

Table I-2...Especially In Real Terms

November 2018

November 2018

Further breaking down the historical returns into 12-month forward EPS estimates and 12-month forward multiples, it turns out that multiples usually contract when the Fed is tightening. However, during Phase I this is more than offset by the increase in forward earnings estimates, such that equity investors enjoy positive returns until rates move into restrictive territory in Phase II. Our sense is that we are still in Phase I, implying that it is too early to expect more than a correction in risk assets based solely on the U.S. monetary policy cycle. The fed funds rate has been rising, but so too has the equilibrium rate according on our measure. Powell's latest comments suggest that the Fed agrees. That said, it is a cliche to say that this cycle has been different in many ways. Nobody knows exactly where the neutral rate is today. This means that we must be on watch for signs that the fed funds rate has already crossed into restrictive territory. We looked at the behavior of a raft of monetary and credit indicators around the time that the fed funds rate broke above the estimated neutral rate in the past. None of them have been reliable across all business cycles since the 1970s, but the best ones are shown in Chart I-3: Growth in M1 generally begins to decelerate as the fed funds rate approaches neutral and falls into negative territory shortly thereafter. Bank liquidity is defined as short-term assets as a percent of total bank credit. It usually peaks just before rates become restrictive, and begins to fall quickly as the fed funds rate surpasses the equilibrium level. We interpret bank liquidity as a proxy for banks' willingness to provide funding liquidity that enables institutional investors to take positions. The peak level of bank liquidity differs across tightening cycles, but it is never a good sign when it begins to trend lower. Consumer credit growth has a somewhat spotty track record as an indicator of monetary restraint, but it has often peaked around the time that the Fed enters Phase II. The BCA Fed Monitor is an indicator designed to gauge the pressure on the Fed to adjust policy one way or the other. It generally peaks in "tight money required" territory just before, or coincident with, the shift from Phase I to Phase II. A shift of the Monitor into "easy money required" territory would suggest that policy has become outright restrictive, and that a peak in the fed funds rate is approaching. Chart I-3BCA R-Star Indicator And Its Components

BCA R-Star Indicator And Its Components

BCA R-Star Indicator And Its Components

Combining the four into one indicator removes some of the noise of the individual series. The BCA "R-Star" Indicator is shown in the top panel of Chart I-3. A dip in this indicator below the zero line would warn that we have entered Phase II and that the equity bull market is out of time. Chart I-4 shows the BCA R-Star indicator again, along with the S&P 500, EPS growth and profit margins. It is shaded for periods when the R-Star indicator is below zero. The lead time has varied across the economic cycles and it is far from a perfect predictor. Nonetheless, when the indicator is negative it has generally been associated with falling stock prices, decelerating profit growth and eroding profit margins. The indicator has edged lower this year, but is not yet in the danger zone. Chart I-4BCA R-Star Indicator And The U.S. Profit Cycle

BCA R-Star Indicator And The U.S. Profit Cycle

BCA R-Star Indicator And The U.S. Profit Cycle

Finally, we are of course watching the yield curve. Its recent steepening suggests that U.S. growth justifies higher bond yields and that policy has not yet become outright restrictive. Global Growth Divergence Continues... We do not see compelling evidence from the flow of U.S. economic data that higher rates are derailing the expansion, although there are a couple of worrying signs, suggesting that growth has peaked. The backdrop is quite supportive for consumer spending: tax cuts, robust employment gains, rising wages and elevated confidence. The fact that the household saving rate is relatively high means that consumers have the wherewithal to boost the pace of spending if they wish. Motor vehicle sales have moderated, but this is to be expected when the economic cycle is advanced. The replacement cycle for U.S. business investment still has further to run. The average age of the non-residential housing stock is the highest since 1963. Both capex intention surveys and the recent easing in lending standards for commercial and industrial loans suggest that U.S. capital expenditures will be well supported, although there has been some softness in the former recently (Chart I-5). Chart I-5U.S. Capex Outlook Is Bright

U.S. Capex Outlook Is Bright

U.S. Capex Outlook Is Bright

That said, the soft U.S. housing data are a concern, especially because a peak in residential investment as a share of GDP has been a good (albeit quite early) leading indicator of recessions. It is difficult to fully explain why housing is losing altitude given all the tailwinds supporting demand, including solid household formation (see last month's Overview). Mortgage rates have increased but affordability is still favorable. It could be that the supply side, rather than demand, is the problem: tight lending standards, zoning restrictions and the high cost of building. Still, a continued housing downtrend relative to GDP would be a challenge to our view that there will be no recession in 2019. While the U.S. economy is enjoying strong momentum, the same cannot be said for the rest of the global economy. A raft of items has weighed on CEO confidence outside of the U.S., including trade wars, a strong dollar, rising oil prices, emerging market turbulence, the return of Italian debt woes and the continuing slowdown in the Chinese economy. The global PMI is beginning to erode from a high level (Chart I-6). The softening in world activity appears to be concentrated in capital spending. Growth in capital goods imports for an aggregate of 20 countries continues to decelerate, along with industrial production for capital goods and machinery & electrical equipment in the major advanced economies. Chart I-6Global Capex Is Softening

Global Capex Is Softening

Global Capex Is Softening

Meanwhile, our favorite global leading indicators are flashing red (Chart I-7). BCA's Global LEI has broken below the boom/bust line and its diffusion index suggests further downside. The Global ZEW and the BCA Boom/Bust indicator are holding just below zero. The global credit impulse is also still pointing down. Chart I-7Global Leading Indicators Flashing Red

Global Leading Indicators Flashing Red

Global Leading Indicators Flashing Red

Among the advanced economies, Europe and Japan are most vulnerable to the slowdown in global trade and capital spending. Industrial production growth has already stalled in both economies and their respective LEIs are heading south fast (Chart I-8). Chart I-8Global Divergence

Global Divergence

Global Divergence

...Affecting Relative Earnings Trends It is thus not surprising that corporate EPS growth has peaked in the Eurozone and Japan. The macro data that drive our top-down EPS growth models suggest that the profit situation is going to deteriorate quickly in the coming quarters. The peak in industrial production growth suggests that the corporate top line will lose more steam. Meanwhile, nominal GDP growth has decelerated sharply in both economies, in absolute terms and relative to the aggregate wage bill (Chart I-9). These trends suggest that profit margins are coming under significant downward pressure. Even when we build in a modest growth pickup and slight rebound in margins in 2019, EPS growth falls close to zero by year-end according to our model (Chart I-10). Chart I-9Diverging Macro Trends...

Diverging Macro Trends...

Diverging Macro Trends...

Chart I-10...Implies Different EPS Outlook

...Implies Different EPS Outlook

...Implies Different EPS Outlook

The earnings situation is completely different in the U.S. It is still early in Q3 earnings season, but company reports have been upbeat so far. The macro variables that feed into our top-down U.S. EPS model point to both continuing margin expansion and robust top line growth (Chart I-9). Nominal GDP growth has surged to more than 5% on a year-ago basis, while the expansion in the economy's wage bill has been steady at under 5%. It is also very impressive that industrial production growth continues to accelerate, bucking the global trend. We assume that U.S. GDP growth moderates from this year's hectic pace in 2019, but stays well above-trend because of the lingering fiscal tailwind. Impressively, the indicators we are following suggest that S&P 500 profit margins still have some upside potential, at least in the next quarter or two (Chart I-11). Nonetheless, we make the conservative assumption that margins will narrow somewhat in 2019. Plugging this macro scenario into our model, it suggests that EPS growth will decelerate to a still-solid 10% pace by the end of 2019. The impact on corporate profits from the rise in bond yields so far will be minimal. It is only now that the yield on the average corporate bond has reached the average coupon on outstanding debt. This means that it will require further increases in yields from here to have any meaningful impact on corporate interest expense. Chart I-11U.S. Margin Indicators Still Upbeat

U.S. Margin Indicators Still Upbeat

U.S. Margin Indicators Still Upbeat

The U.S. economic and earnings backdrop is robust enough that we would be tempted to upgrade our risk asset allocation back to overweight if the S&P 500 moves even lower in the near term. Nonetheless, a number of key risks keep us at benchmark for now. (1) U.S. Foreign Policy The U.S. mid-term election is less than two weeks away as we go to press. Our geopolitical team places the odds of a Democratic House takeover at 65%, and the odds of a Senate takeover at 40%. Investors should expect a knee-jerk equity selloff if the Democrats manage to grab both parts of Congress. However, any damage to risk assets should be fleeting because the Democrats would not be able to unravel any of President Trump's main economic policies. Voters are not demanding budget discipline from either party, despite the surging federal deficit (Chart I-12). We highlighted in a recent Special Report that we foresee little political backlash against fiscal profligacy because of the shift-to-the-left by the median voter.2 The Trump tax cuts are here to stay. Chart I-12No Political Backlash To Big Deficits

No Political Backlash To Big Deficits

No Political Backlash To Big Deficits

In fact, our geopolitical team argues that the odds would increase for an infrastructure plan and even of an immigration deal, if President Trump comes to the middle ground on some of his demands.3 The implication is that fiscal policy will remain highly stimulative in 2019, before the initial thrust begins to wear off in 2020. The Administration's foreign policy, however, remains a key risk for equities. Our high conviction view is that President Trump will continue pursuing unorthodox foreign and trade policies regardless of the midterm outcome. The just-announced 10% tariff on $200 billion of Chinese imports confirms our alarmist view on trade tensions. President Trump has threatened to lift the tariff to 25% by the end of the year in order to pile even more pressure on Beijing. This would represent a significant escalation in the trade war, one that we do not expect Chinese policymakers to simply roll over and accept. The risk is that the Chinese government not only hikes tariffs on U.S. exports, but also retaliates against U.S. firms with operations in China. Even more dangerously, a trade war with China could escalate into a military conflict in the South China Sea. Meanwhile, the U.S. embargo on Iranian oil exports will officially begin on November 4, just two days before the midterm election. We expect President Trump to turn the screws on Iranian exports in ways that President Obama did not. Once the election is out of the way, President Trump will refocus on his "maximum pressure" tactic, which he believes led to a breakthrough with North Korea. Unfortunately for the markets, we do not expect that this tactic will work as smoothly with Iran and China. (2) Rising Probability Of An Oil Shock The Administration's pressure on Iran adds to the already high risk of an oil price spike above US$100 per barrel in early 2019. While oil demand growth is slowing somewhat, exports from two of OPEC's largest producers - Iran and Venezuela - are falling precipitously. Global oil inventories are drawing down, while spare capacity is perilously low, leaving little in the way of readily available backup supply to deal with an unplanned production outage. The confluence of these factors is setting the global oil market up for a supply shock according to our energy experts (Chart I-13). Chart I-13Increasing Risk Of An Oil Spike

Increasing Risk Of An Oil Spike

Increasing Risk Of An Oil Spike

It is important to differentiate between a steady demand-driven rise in the price of oil and a rapid supply-driven oil price spike. The former can be bond-bearish by forcing inflation expectations higher at a time when strong economic growth is also pushing up real bond yields. Nonetheless, equity prices could continue rising in this scenario as the robust economic backdrop outweighs the impact of higher yields. In contrast, an oil price spike that is driven by supply restrictions might initially be negative for bond prices, but ultimately would produce a deflationary impulse by depressing real economic activity. It could even be the catalyst for a recession. A supply-driven oil spike would be outright bearish for risk assets and may prove to be the trigger for a shift from benchmark to underweight for global stocks and corporate bonds. The risk facing corporates in the next economic downturn is one of the topics covered in this month's Special Report, beginning on page 21. The report looks at the structural changes to the economy and financial markets that have occurred because of the Great Recession and financial crisis. (3) EM Pain Is Not Over In the absence of policy stimulus in China, the prospect of continuing Fed tightening means that it is too early to bottom-fish in emerging markets. Emerging Asia is at the epicenter of the global trade and capital spending slowdown. The sharp deceleration in Taiwanese and Korean export growth rates suggests that growth in world industrial production and forward earnings estimates are not yet near a bottom (Chart I-14). Chart I-14Asian Exports Softening...

Asian Exports Softening...

Asian Exports Softening...

Softening Chinese domestic demand is adding to the gloom. Chart I-15 shows that efforts by the Chinese authorities to curtail corporate debt have been bearing fruit. In response to the regulatory and administrative tightening, smaller financial institutions are not building up the working capital required to expand their loan book. As a result, the Chinese credit impulse remains weak and shows no sign of a bottom, despite the uptick in the latest reading on M3 growth. Chinese policy stimulus is underwhelming, confirming the view we expressed in the September BCA Overview. Xi Jinping has not yet abandoned his structural goals and shadow bank crackdown, which are weighing on overall credit expansion. Chart I-15...And No Growth Impulse From China

Chinese Policy Tightening In Action ...And No Growth Impulse From China

Chinese Policy Tightening In Action ...And No Growth Impulse From China

Second, EM financial conditions continue to tighten (Chart I-15). Our currency strategists point out that many factors lie behind this deterioration in the EM financial conditions index, including the collapse in performance of carry trades, the dollar's ascent, and rising U.S. interest rates that are boosting the cost of servicing foreign currency EM debt. In turn, tighter EM financial conditions are contributing to the global manufacturing slowdown in a self-reinforcing negative feedback loop. EM Asia is particularly at risk to this loop, but Europe, Japan and commodity producers are also vulnerable. Some market commentators have argued that the Fed will soon have to back off its rate hike campaign in the face of global financial market stress. However, the FOMC's pain threshold is higher than at any time since the Great Recession because the domestic economy is showing signs of overheating. The correction in risk assets would have to get a lot worse before the Fed blinks. Meanwhile, the U.S. again passed on the chance to label China a currency manipulator. This opens the door to another downleg in the RMB, especially if the U.S./China trade war escalates. Additional RMB weakness would spell more trouble for EM assets. The implication is that any bounce in EM currencies or asset prices represents a selling opportunity for those investors not already short. Our EM strategists expect at least another 15% drop in share prices before the risk-reward profile of this asset class improves. (4) Italian Debt Crisis The main problem with the Italian economy is that the private sector saves too much and spends too little. A shrinking population has reduced the need for firms to invest in new capacity. Unlike Germany, Italy cannot export its savings to the rest of the world through a large trade surplus because it does not have a hypercompetitive economy. Nor can the Italian government risk running afoul of the bond vigilantes by emulating Japan's strategy of absorbing private-sector savings with large budget deficits. The implication is that Italy is stuck in a low-growth trap that is feeding political pressure to shed the EU's fiscal straight jacket. We believe that the populist government will be the first to blink, but it may require more bouts of financial stress to force capitulation. A 4% level on the 10 year BTP yield is a likely threshold for a compromise. Above that level, Italian banks become insolvent based on the market value of their holdings of Italian debt. In the meantime, rising global bond yields worsen Italy's tenuous financial situation, with possible contagion into global financial markets. Investment Conclusions: The U.S. bond market is waking up to the likelihood that U.S. short-term rates are going higher than previously expected, suggesting that recent investment themes will persist for a while longer. We continue to recommend a neutral stance on global equities (with a preference for developed over emerging markets), a below-benchmark duration bias, and an overweight allocation in cash. The bond market is only priced for the Fed to maintain its quarterly rate hike pace until June of next year (Chart I-16). Investors judge that some combination of tepid global economic momentum and tame U.S. core inflation temper the Fed's need or ability to take rates much higher. We disagree, based our own assessment of the U.S. economy and our out-of-consensus inflation view (see this month's Special Report). Rising volatility and/or a weaker global growth pulse are unlikely to prompt the Fed to bail out of its tightening campaign as quickly as it did in early 2016. Chart I-16Market Expectations For The Fed Still Too Complacent

Market Expectations For The Fed Still Too Complacent

Market Expectations For The Fed Still Too Complacent

Meanwhile, our indicators suggest that the divergence between the red-hot U.S. economy and cooling global activity will continue, implying more upside potential for the U.S. dollar. We expect another 5-10% rise against most currencies, with the possible exception of the Canadian dollar. It is difficult to identify a "choke point" for bond yields in advance. A 10-year Treasury yield north of 3.7% might cause us to call the peak in yields and to become even more defensive on risk assets, but it will be critical to watch our monetary indicators. Indeed, we would be tempted to upgrade stocks back to overweight if the global selloff progresses much further, in the absence of negative reading from the monetary indicators or an inverted yield curve. The earnings backdrop will continue to be a tailwind for the U.S. equity market at least into early 2019. In contrast, profit growth in the Eurozone and Japan is set to disappoint market expectations. The U.S. equity market will therefore outperform, particularly in unhedged terms. Stay at benchmark on corporate bonds versus governments in the U.S. and Eurozone. Avoid emerging market assets and commodities. The main exception is oil, which is increasingly at risk of a spike above $100/bbl. Mark McClellan Senior Vice President The Bank Credit Analyst October 25, 2018 Next Report: November 29, 2018 1 Please see U.S. Investment Strategy Special Report "Revisiting The Fed Funds Rate Cycle," dated September 3, 2018, available at usis.bcaresearch.com 2 Please see The Bank Credit Analyst "U.S. Fiscal Policy: An Unprecedented Macro Experiment," dated July 2018, available at bca.bcaresearch.com 3 Please see BCA Geopolitical Strategy Weekly Report "A Story Told Through Charts: The U.S. Midterm Election," dated September 19, 2018, available at gps.bcaresearch.com II. The Long Shadow Of The Financial Crisis The Great Recession and financial crisis cast a long shadow that will affect economies, policymakers and investors for years to come. The roots of the crisis are already well known. The first of a two-part series looks forward by examining the areas where we believe structural change has occurred related to the economy or financial markets. First, the financial crisis transformed the corporate bond market in several ways that heighten the risk for quality spreads in the next downturn. Debt and market liquidity are two key concerns. Corporate leverage will not cause the next recession. Nonetheless, when one does occur, corporate spreads in the U.S. and (to a lesser extent) the Eurozone will widen by more for any given degree of recession. This reflects a low interest coverage ratio, poor market liquidity, the downward trend in credit quality and covenant erosion. Second, the shock of the Great Recession and its aftermath appears to have affected the relationship between economic slack and inflation. Firms have been extra reluctant to grant wage gains. However, we argue that the "shell shock" effect will wane. The fact that inflation has been depressed for so long may actually cultivate the risk that inflation will surprise on the upside in the coming years. Investors should hold inflation-protection in the inflation swaps market, or by overweighting inflation-linked bonds versus conventional issues. Third, the events of the last decade have left a lasting impression on monetary policymakers. They will err on the side of allowing the economy to overheat and inflation to modestly overshoot the target in the major economies, despite signs of financial froth. The Fed will respond only with a lag to the current fiscally-driven surge in U.S. growth, leading to a boom/bust economic scenario. Central bankers will have no trouble employing unorthodox policies again in the future, and will be willing to push the boundaries even further during the next recession. Expect aggressive manipulation of the long-end of the yield curve when the time arrives to ease policy. We may also observe more coordination between monetary and fiscal policies. Fourth, global bond yields fell to unprecedented levels, reflecting both structural and cyclical headwinds to demand growth. A dismal productivity performance is another culprit. Productivity growth is poised to recover to some extent, while some of the growth headwinds have reached an inflection point. We do not expect nominal bond yields to return to pre-Lehman norms, and yields could even fall back to previous lows in the case of a recession. Nonetheless, we expect a yield pattern of higher lows and higher highs over the coming business cycles. The 10-year anniversary of the Lehman shock this autumn sparked an avalanche of analysis on the events and underlying causes of the Great Recession and financial crisis. It is a woeful story of greed, a classic bubble, inadequate regulation, new-fangled financial instruments, and a globalized financial system that spread the shock around the world. The crisis cast a long shadow that will affect economies, policymakers and investors for many years to come. The roots of the crisis are well known, so we will not spend any time going over well-trodden ground. Rather, this Special Report looks forward by examining the areas where we believe structural change has occurred related to the economy or financial markets. In Part I, we cover the corporate bond market, the inflation outlook, central bank policymaking and equilibrium bond yields. Part II will look at the debt overhang, systemic risk in the financial sector, asset correlations, the cult of equity and the rise of populism. While not an exhaustive list, we believe these are the key areas of structural change. (1) Corporate Bond Market: Leverage And Downgrade Risk The financial crisis transformed the corporate bond market in several ways that heighten the risk for quality spreads in the next downturn. Debt and market liquidity are two key concerns. An extraordinarily long period of extremely low interest rates was too much for corporate CEOs to pass up. However, because the durability of the economic recovery was so uncertain, it seemed more attractive to hand over the borrowed cash to shareholders than to use it to aggressively expand productive capacity. The ongoing equity bull market rewarded CEOs for the financial engineering, serving to create a self-reinforcing feedback loop. And so far, corporate bondholders have not policed this activity. The result is that the U.S. corporate bond market has grown in leaps and bounds since 2009 (Chart II-1A and Chart II-1B). The average duration of the Bloomberg Barclays index has also risen as firms locked in attractive financing rates. The same is true, although to a lesser extent, in the Eurozone. Chart II-1AU.S. BBB-Rated Share Rising...

U.S. BBB-Rated Share Rising...

U.S. BBB-Rated Share Rising...

Chart II-1B...Same In The Eurozone

...Same In The Eurozone

...Same In The Eurozone

Balance sheet health is obviously not the key driver of corporate bond relative returns at the moment. Nonetheless, investors will begin to worry about the growth outlook if interest rates continue to rise. The U.S. national accounts data suggest that interest coverage remains relatively healthy, but this includes large companies such as some of the FAANGs that have little debt and a lot of cash. The national accounts data are unrepresentative of the companies that are included in the Bloomberg Barclays corporate bond index, which are heavy debt issuers. To gain a clearer picture, we calculated a bottom-up Corporate Health Monitor (CHM) for a sample of U.S. companies that provides a sector and credit-quality composition that roughly matches the Bloomberg Barclay's index. The CHM is the composite of six critical financial ratios. Chart II-2 highlights that the investment-grade (IG) CHM has improved over the past two years due to the profitability sub-components. However, the debt/equity ratio has been in a steep uptrend. Interest coverage does not appear alarming by historical standards at the moment, but one can argue that it should be much higher given the extremely low average coupon on corporate bonds, and given that profit margins are extraordinarily high in the U.S. The rapid accumulation of debt has overwhelmed these other factors. Evidence of rising leverage is broadly based across sectors and ratings. Chart II-2U.S. IG Corporate Health

U.S. IG Corporate Health

U.S. IG Corporate Health

Unfortunately, the profit tailwind won't last forever. At some point, earnings growth will stall and this cycle's debt accumulation will start to bite in the context of rising interest rates. To gauge the risk, we estimate the change in the interest coverage ratio over the next three years for a 100 basis-point rise in interest rates across the corporate curve, taking into consideration the maturity distribution of the debt.1 For our universe of Investment-grade U.S. companies, the interest coverage ratio would drop from a little over 7 to under 6, which is close to the lows of the Great Recession (denoted as "x" in Chart II-3). Of course, the decline in interest coverage will be much worse if the Fed steps too far and monetary tightening sparks a recession. The "o" in Chart II-3 denotes the combination of a 100 basis-point interest rate shock and a mild recession in which the S&P 500 suffers a 25% peak-to-trough decline in EPS. The overall interest coverage ratio plunges close to all-time lows at 4½. Chart II-3Interest Coverage To Plunge...

Interest Coverage To Plunge...

Interest Coverage To Plunge...

These simulations imply that, for any given size of recession, the next economic downturn will have a larger negative impact on corporate health than in the past. Rating agencies have undertaken some downgrading related to shareholder-friendly activity, but downgrades will proliferate when the agencies realize that the economy is turning and the profit boom is over (Chart II-4). Banks will belatedly tighten lending standards, adding to funding pressure for the corporate sector. Chart II-4...And Ratings To Be Slashed

...And Ratings To Be Slashed

...And Ratings To Be Slashed

Fallen Angels The potential for a large wave of fallen angels means that downgrade activity will be particularly painful for corporate bond investors. The surge in lower-quality issuance has led to a downward trend in the average credit rating and has significantly raised the size of the BBB-rated bonds relative to the IG index and relative to the broader universe of corporate bonds including high yield (Chart II-5, and Chart II-1A).2 The downward trend in credit quality predates Lehman, but events since the Great Recession have likely reinforced the trend. Chart II-5Lower Ratings And Longer Duration

Lower Ratings And Longer Duration

Lower Ratings And Longer Duration

Studies show that bonds that get downgraded into junk status can perform well for a period thereafter, suggesting that investors holding a fallen angel should not necessarily sell immediately. Nonetheless, the process of transitioning from investment-grade to high-yield involves return underperformance as the spread widens. Poor market liquidity and covenant erosion will intensify pressure for corporate spreads to widen when the bear market arrives. Market turnover has decreased substantially since the pre-Lehman years, especially for IG (Chart II-6). The poor liquidity backdrop appears to be structural, reflecting regulation that has curtailed banks' market-making activity and prop trading, among other factors. Chart II-6Poor Market Liquidity

Poor Market Liquidity

Poor Market Liquidity

The Eurozone corporate bond market has also seen rapid growth and a deterioration in the average credit rating. Liquidity is an issue there as well. That said, the Eurozone corporate sector is less advanced in the leverage cycle than the U.S. Interest coverage ratios will fall during the next recession, but this will be concentrated among foreign issuers - domestic issuers are much less at risk to rising interest rates and/or an economic downturn.3 Bottom Line: Corporate leverage will not cause the next recession. Nonetheless, when one does occur, corporate spreads in the U.S. and (to a lesser extent) Eurozone will widen by more for any given degree of recession. Current spreads do not compensate for this risk. (2) Inflation Undershoot Breeds Overshoot Inflation in the U.S. and other developed economies has been sticky since the financial crisis. First, inflation did not fall as much in the recession and early years of the recovery as many had predicted, despite the worst economic contraction in the post-war period. Subsequently, central banks have had trouble raising inflation back to target. In the U.S., core PCE inflation has only recently returned to 2%. Several structural factors have been blamed, but continuing tepid wage growth in the face of a very tight labor market raises the possibility that the inflation-generating process has been fundamentally altered by the Great Recession. In other words, the relationship between slack in the labor market (or market for goods and services) and inflation has changed. In theory, inflation should rise when the economy's output is above its potential level or when the unemployment rate is below its full-employment level. Inflation should fall when the reverse is true. This means that the change (not the level) in inflation should be positively correlated with the level of the output gap or the labor market gap. Chart II-7 presents the change in U.S. core inflation with the output gap. Although inflation appears to have become less responsive to shifts in the output gap after 1990, it has been particularly insensitive in the post-Lehman period. Chart II-7The U.S. Phillips Curve: RIP?

The U.S. Phillips Curve: RIP?

The U.S. Phillips Curve: RIP?

One reason may be that the business sector was shell-shocked by the Great Recession and financial crisis to such an extent that business leaders have been more reluctant to grant wage gains than in past cycles. Equally-unnerved workers felt lucky just to have a job, and have been less willing to demand raises. Dampened inflation expectations meant that low actual inflation became self-reinforcing. We have some sympathy with this view. Long-term inflation expectations have been sticky at levels that are inconsistent with the major central banks meeting their inflation targets over the long term. This suggests that people believe that central banks lack the tools necessary to overwhelm the deflationary forces. The lesson for investors and policymakers is that, while unorthodox monetary policies helped to limit the downside for inflation and inflation expectations during and just after the recession, these policies have had limited success in reversing even the modest decline that did occur. That said, readers should keep in mind a few important points: One should not expect inflation to rise much until economies break through their non-inflationary limits. The major advanced economies have only recently reached that point to varying degrees; Inflation lags the business cycle (Chart II-8). This is especially the case in long 'slow burn' economic expansions, as we have demonstrated in previous research; and The historical relationship between inflation and economic slack has been non-linear. As shown in Chart II-9, U.S. inflation has tended to accelerate quickly when unemployment drops below 4½%. Chart II-8U.S. Inflation Lags The Cycle

November 2018

November 2018

Chart II-9A Kinked Phillips Curve

November 2018

November 2018