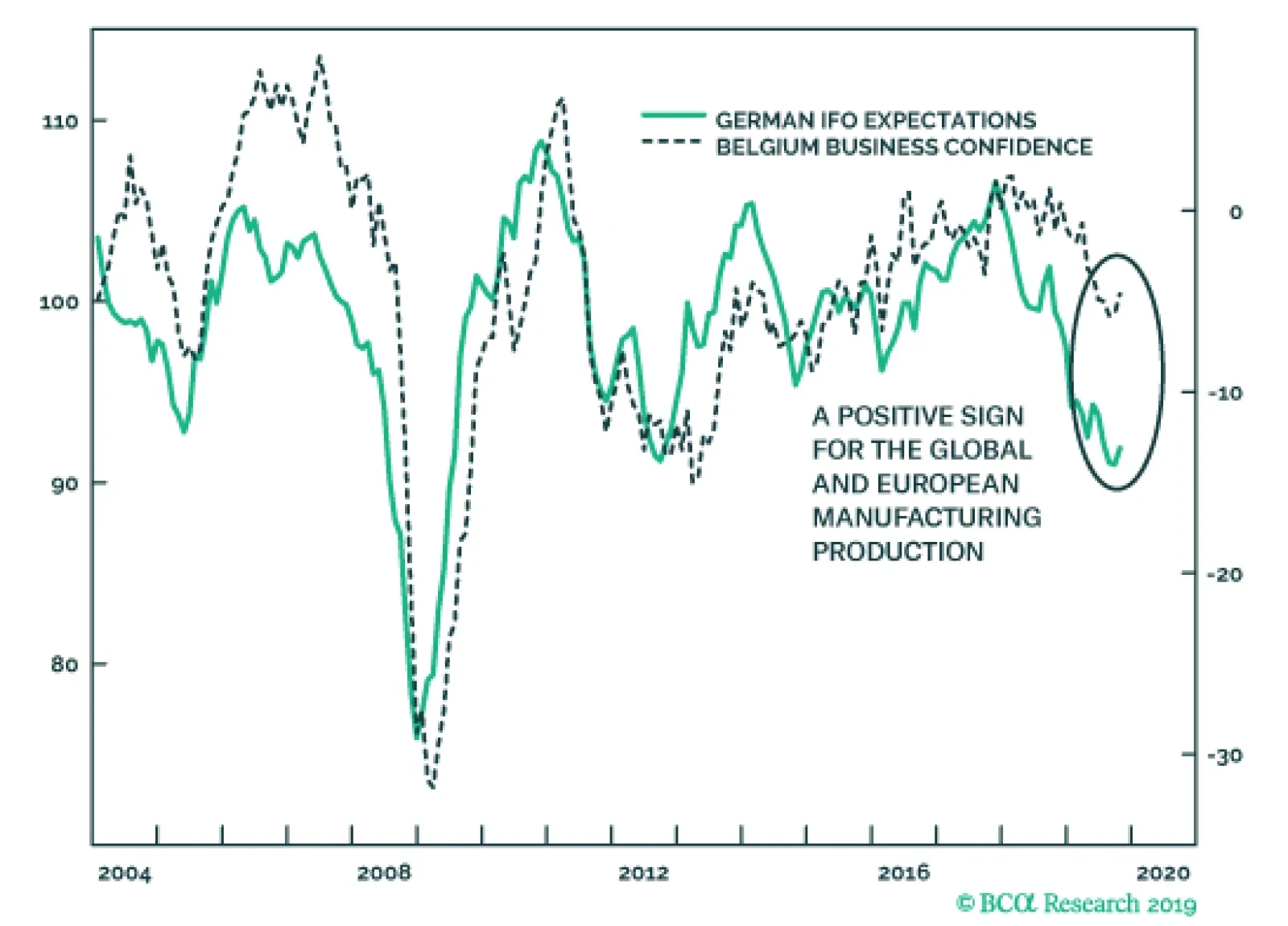

Europe

Highlights The Cold War is a limited analogy for the U.S.-China conflict; In a multipolar world, complete bifurcation of trade is difficult if not impossible; History suggests that trade between rivals will continue, with minimal impediments; On a secular horizon, buy defense stocks, Europe, capex, and non-aligned countries. Feature There is a growing consensus that China and the U.S. are hurtling towards a Cold War. BCA Research played some part in this consensus – at least as far as the investment community is concerned – by publishing “Power and Politics in East Asia: Cold War 2.0?” in September 2012.1 For much of this decade, Geopolitical Strategy focused on the thesis that geopolitical risk was rotating out of the Middle East, where it was increasingly irrelevant, to East Asia, where it would become increasingly relevant. This thesis remains cogent, but it does not mean that a “Silicon Curtain” will necessarily divide the world into two bifurcated zones of capitalism. Trade, capital flows, and human exchanges between China and the U.S. will continue and may even grow. But the risk of conflict, including a military one, will not decline. In this report, we first review the geopolitical logic that underpins Sino-American tensions. We then survey the academic literature for clues on how that relationship will develop vis-à-vis trade and economic relations. The evidence from political theory is surprising and highly investment relevant. We then look back at history for clues as to what this means for investors. Our conclusion is that it is highly likely that the U.S. and China will continue to be geopolitical rivals. However, due to the geopolitical context of multipolarity, it is unlikely that the result will be “Bifurcated Capitalism.” Rather, we expect an exciting and volatile environment for investors where geopolitics takes its historical place alongside valuation, momentum, fundamentals, and macroeconomics in the pantheon of factors that determine investment opportunities and risks. The Thucydides Trap Is Real … Speaking in the Reichstag in 1897, German Foreign Secretary Bernhard von Bülow proclaimed that it was time for Germany to demand “its own place in the sun.”2 The occasion was a debate on Germany’s policy towards East Asia. Bülow soon ascended to the Chancellorship under Kaiser Wilhelm II and oversaw the evolution of German foreign policy from Realpolitik to Weltpolitik. While Realpolitik was characterized by Germany’s cautious balancing of global powers under Chancellor Otto von Bismarck, Weltpolitik saw Bülow and Wilhelm II seek to redraw the status quo through aggressive foreign and trade policy. Imperial Germany joined a long list of antagonists, from Athens to today’s People’s Republic of China, in the tragic play of human history dubbed the “Thucydides Trap.”3 Chart II-1Imperial Overstretch

Imperial Overstretch

Imperial Overstretch

The underlying concept is well known to all students of world history. It takes its name from the Greek historian Thucydides and his seminal History of the Peloponnesian War. Thucydides explains why Sparta and Athens went to war but, unlike his contemporaries, he does not moralize or blame the gods. Instead, he dispassionately describes how the conflict between a revisionist Athens and established Sparta became inevitable due to a cycle of mistrust. Graham Allison, one of America’s preeminent scholars of international relations, has argued that the interplay between a status quo power and a challenger has almost always led to conflict. In 12 out of the 16 cases he surveyed, actual military conflict broke out. Of the four cases where war did not develop, three involved transitions between countries that shared a deep cultural affinity and a respect for the prevailing institutions.4 In those cases, the transition was a case of new management running largely the same organizational structure. And one of the four non-war outcomes was nothing less than the Cold War between the Soviet Union and the U.S. The fundamental problem for a status quo power is that its empire or “sphere of influence” remains the same size as when it stood at the zenith of power. However, its decline in a relative sense leads to a classic problem of “imperial overstretch.” The hegemonic or imperial power erroneously doubles down on maintaining a status quo that it can no longer afford (Chart II-1). The challenger power is not blameless. It senses weakness in the hegemon and begins to develop a regional sphere of influence. The problem is that regional hegemony is a perfect jumping off point towards global hegemony. And while the challenger’s intentions may be limited and restrained (though they often are ambitious and overweening), the status quo power must react to capabilities, not intentions. The former are material and real, whereas the latter are perceived and ephemeral. The challenging power always has an internal logic justifying its ambitions. In China’s case today, there is a sense among the elite that the country is merely mean-reverting to the way things were for many centuries in China’s and Asia’s long history (Chart II-2). In other words, China is a “challenger” power only if one describes the status quo as the past three hundred years. It is the “established” power if one goes back to an earlier state of affairs. As such, the consensus in China is that it should not have to pay deference to the prevailing status quo given that the contemporary context is merely the result of western imperialist “challenges” to the established Chinese and regional order. Chart II-2China’s Mean Reverting Narrative

November 2019

November 2019

In addition, China has a legitimate claim that it is at least as relevant to the global economy as the U.S. and therefore deserves a greater say in global governance. While the U.S. still takes a larger share of the global economy, China has contributed 23% to incremental global GDP over the past two decades, compared to 13% for the U.S. (Chart II-3). Chart II-3The Beijing Consensus

November 2019

November 2019

Bottom Line: The emerging tensions between China and the U.S. fit neatly into the theoretical and empirical outlines of the Thucydides Trap. We do not see any way for the two countries to avoid struggle and conflict on a secular or forecastable horizon. What does this mean for investors? For one, the secular tailwinds behind defense stocks will persist. But what beyond that? Is the global economy destined to witness complete bifurcation into two armed camps separated by a Silicon Curtain? Will the Alibaba and Amazon Pacts suspiciously glare at each other the way that NATO and Warsaw Pacts did amidst the Cold War? The answer, tentatively, is no. … But It Will Not Lead To Economic Bifurcation President Trump’s aggressive trade policy also fits neatly into political theory, to a point. Realism in political science focuses on relative gains over absolute gains in all relationships, including trade. This is because trade leads to economic prosperity, prosperity to the accumulation of economic surplus, and economic surplus to military spending, research, and development. Two states that care only about relative gains due to rivalry produce a zero-sum game with no room for cooperation. It is a “Prisoner’s Dilemma” that can lead to sub-optimal economic outcomes in which both actors chose not to cooperate. Diagram II-1 illustrates the effects of relative gain calculations on the trade behavior of states. In the absence of geopolitics, demand (Q3) is satisfied via trade (Q3-Q0) due to the inability of domestic production (Q0) to meet it. Diagram II-1Trade War In A Bipolar World

November 2019

November 2019

However, geopolitical externality – a rivalry with another state – raises the marginal social cost of imports – i.e. trade allows the rival to gain more out of trade and “catch up” in terms of geopolitical capabilities. The trading state therefore eliminates such externalities with a tariff (t), raising domestic output to Q1, while shrinking demand to Q2, thus reducing imports to merely Q2-Q1, a fraction of where they would be in a world where geopolitics do not matter. The dynamic of relative gains can also have a powerful pull on the hegemon as it begins to weaken and rethink its originally magnanimous trade relations. As political scientist Duncan Snidal argued in a 1991 paper, When the global system is first set up, the hegemon makes deals with smaller states. The hegemon is concerned more with absolute gains, smaller states are more concerned with relative, so they are tougher negotiators. Cooperative arrangements favoring smaller states contribute to relative hegemonic decline. As the unequal distribution of benefits in favor of smaller states helps them catch up to the hegemonic actor, it also lowers the relative gains weight they place on the hegemonic actor. At the same time, declining relative preponderance increases the hegemonic state’s concern for relative gains with other states, especially any rising challengers. The net result is increasing pressure from the largest actor to change the prevailing system to gain a greater share of cooperative benefits.5 The reason small states are initially more concerned with relative gains is because they are far more concerned with national security than the hegemon. The hegemon has a preponderance of power and is therefore more relaxed about its security needs. This explains why Presidents George Bush Sr., Bill Clinton, and George Bush Jr. all made “bad deals” with China. Writing nearly thirty years ago, Snidal cogently described the current U.S.-China trade war. Snidal thought he was describing a coming decade of anarchy. But he and fellow political scientists writing in the early 1990s underestimated American power. The “unipolar moment” of American supremacy was not over, it was just beginning! As such, the dynamic Snidal described took thirty years to come to fruition. When thinking about the transition away from U.S. hegemony, most investors anchor themselves to the Cold War as it is the only world they have known that was not unipolar. Moreover the Cold War provides a simple, bipolar distribution of power that is easy to model through game theory. If this is the world we are about to inhabit, with the U.S. and China dividing the whole planet into spheres like the U.S. and Soviet Union, then the paragraph we lifted from Snidal’s paper would be the end of it. America would abandon globalization in totality, impose a draconian Silicon Curtain around China, and coerce its allies to follow suit. But most of recent human history has been defined by a multipolar distribution of power between states, not a bipolar one. The term “cold war” is applicable to the U.S. and China in the sense that comparable military power may prevent them from fighting a full-blown “hot war.” But ultimately the U.S.-Soviet Cold War is a poor analogy for today’s world. In a multipolar world, Snidal concludes, “states that do not cooperate fall behind other relative gains maximizers that cooperate among themselves. This makes cooperation the best defense (as well as the best offense) when your rivals are cooperating in a multilateral relative gains world.” Snidal shows via formal modeling that as the number of players increases from two, relative-gains sensitivity drops sharply.6 The U.S.-China relationship does not occur in a vacuum — it is moderated by the global context. Today’s global context is one of multipolarity. Multipolarity refers to the distribution of geopolitical power, which is no longer dominated by one or two great powers (Chart II-4). Europe and Japan, for instance, have formidable economies and military capabilities. Russia remains a potent military power, even as India surpasses it in terms of overall geopolitical power. Chart II-4The World Is No Longer Bipolar

The World Is No Longer Bipolar

The World Is No Longer Bipolar

A multipolar world is the least “ordered” and the most unstable of world systems (Chart II-5). This is for three reasons: Chart II-5Multipolarity Is Messy

Multipolarity Is Messy

Multipolarity Is Messy

Math: Multipolarity engenders more potential “conflict dyads” that can lead to conflict. In a unipolar world, there is only one country that determines norms and rules of behavior. Conflict is possible, but only if the hegemon wishes it. In a bipolar world, conflict is possible, but it must align along the axis of the two dominant powers. In a multipolar world, alliances are constantly shifting and producing novel conflict dyads. Lack of coordination: Global coordination suffers in periods of multipolarity as there are more “veto players.” This is particularly problematic during times of stress, such as when an aggressive revisionist power uses force or when the world is faced with an economic crisis. Charles Kindleberger has argued that it was exactly such hegemonic instability that caused the Great Depression to descend into the Second World War in his seminal The World In Depression.7 Mistakes: In a unipolar and bipolar world, there are a very limited number of dice being rolled at once. As such, the odds of tragic mistakes are low and can be mitigated with complex formal relationships (such as U.S.-Soviet Mutually Assured Destruction, grounded in formal modeling of game theory). But in a multipolar world, something as random as an assassination of a dignitary can set in motion a global war. The multipolar system is far more dynamic and thus unpredictable. Diagram II-2 is modified for a multipolar world. Everything is the same, except that we highlight the trade lost to other great powers. The state considering using tariffs to lower the marginal social cost of trading with a rival must account for this “lost trade.” In the context of today’s trade war with China, this would be the sum of all European Airbuses and Brazilian soybeans sold to China in the place of American exports. For China, it would be the sum of all the machinery, electronics, and capital goods produced in the rest of Asia and shipped to the United States. Diagram II-2Trade War In A Multipolar World

November 2019

November 2019

Could Washington ask its allies – Europe, Japan, South Korea, Taiwan, etc. – not to take advantage of the lucrative trade (Q3-Q0)-(Q2-Q1) lost due to its trade tiff with China? Sure, but empirical research shows that they would likely ignore such pleas for unity. Alliances produced by a bipolar system produce a statistically significant and large impact on bilateral trade flows, a relationship that weakens in a multipolar context. This is the conclusion of a 1993 paper by Joanne Gowa and Edward D. Mansfield.8 The authors draw their conclusion from an 80-year period beginning in 1905, which captures several decades of global multipolarity. Unless the U.S. produces a wholehearted diplomatic effort to tighten up its alliances and enforce trade sanctions – something hardly foreseeable under the current administration – the self-interest of U.S. allies will drive them to continue trading with China. The U.S. will not be able to exclude China from the global system; nor will China be able to achieve Xi Jinping’s vaunted “self-sufficiency.” A risk to our view is that we have misjudged the global system, just as political scientists writing in the early 1990s did. To that effect, we accept that Charts II-1 and II-4 do not really support a view that the world is in a balanced multipolar state. The U.S. clearly remains the most powerful country in the world. The problem is that it is also clearly in a relative decline and that its sphere of influence is global – and thus very expensive – whereas its rivals have merely regional ambitions (for the time being). As such, we concede that American hegemony could be reasserted relatively quickly, but it would require a significant calamity in one of the other poles of power. For instance, a breakdown in China’s internal stability alongside the recovery of U.S. political stability. Bottom Line: The trade war between the U.S. and China is geopolitically unsustainable. The only way it could continue is if the two states existed in a bipolar world where the rest of the states closely aligned themselves behind the two superpowers. We have a high conviction view that today’s world is – for the time being – multipolar. American allies will cheat and skirt around Washington’s demands that China be isolated. This is because the U.S. no longer has the preponderance of power that it enjoyed in the last decade of the twentieth and the first decade of the twenty-first century. Insights presented thus far come from formal theory in political science. What does history teach us? Trading With The Enemy In 1896, a bestselling pamphlet in the U.K., “Made in Germany,” painted an ominous picture: “A gigantic commercial State is arising to menace our prosperity, and contend with us for the trade of the world.”9 Look around your own houses, author E.E. Williams urged his readers. “The toys, and the dolls, and the fairy books which your children maltreat in the nursery are made in Germany: nay, the material of your favorite (patriotic) newspaper had the same birthplace as like as not.” Williams later wrote that tariffs were the answer and that they “would bring Germany to her knees, pleading for our clemency.”10 By the late 1890s, it was clear to the U.K. that Germany was its greatest national security threat. The Germany Navy Laws of 1898 and 1900 launched a massive naval buildup with the singular objective of liberating the German Empire from the geographic constraints of the Jutland Peninsula. By 1902, the First Lord of the Royal Navy pointed out that “the great new German navy is being carefully built up from the point of view of a war with us.”11 There is absolutely no doubt that Germany was the U.K.’s gravest national security threat. As a result, London signed in April 1904 a set of agreements with France that came to be known as Entente Cordiale. The entente was immediately tested by Germany in the 1905 First Moroccan Crisis, which only served to strengthen the alliance. Russia was brought into the pact in 1907, creating the Triple Entente. In hindsight, the alliance structure was obvious given Germany’s meteoric rise from unification in 1871. However, one should not underestimate the magnitude of these geopolitical events. For the U.K. and France to resolve centuries of differences and formalize an alliance in 1904 was a tectonic shift — one that they undertook against the grain of history, entrenched enmity, and ideology.12 Political scientists and historians have noted that geopolitical enmity rarely produces bifurcated economic relations exhibited during the Cold War. Both empirical research and formal modeling shows that trade occurs even amongst rivals and during wartime.13 This was certainly the case between the U.K. and Germany, whose trade steadily increased right up until the outbreak of World War One (Chart II-6). Could this be written off due to the U.K.’s ideological commitment to laissez-faire economics? Or perhaps London feared a move against its lightly defended colonies in case it became protectionist? These are fair arguments. However, they do not explain why Russia and France both saw ever-rising total trade with the German Empire during the same period (Chart II-7). Either all three states were led by incompetent policymakers who somehow did not see the war coming – unlikely given the empirical record – or they simply could not afford to lose out on the gains of trade with Germany to each other. Chart II-6The Allies Traded With Germany ...

November 2019

November 2019

Chart II-7… Right Up To WWI

November 2019

November 2019

Chart II-8Japan And U.S. Never Downshifted Trade

November 2019

November 2019

A similar dynamic was afoot ahead of World War Two. Relations between the U.S. and Japan soured in the 1930s, with the Japanese invasion of Manchuria in 1931. In 1935, Japan withdrew from the 1922 Washington Naval Treaty – the bedrock of the Pacific balance of power – and began a massive naval buildup. In 1937, Japan invaded China. Despite a clear and present danger, the U.S. continued to trade with Japan right up until July 26, 1941, few days after Japan invaded southern Indochina (Chart II-8). On December 7, Japan attacked the U.S. A skeptic may argue that precisely because policymakers sleepwalked into war in the First and Second World Wars, they will not (or should not) make the same mistake this time around. First, we do not make policy prescriptions and therefore care not what should happen. Second, we are highly skeptical of the view that policymakers in the early and mid-twentieth century were somehow defective (as opposed to today’s enlightened leaders). Our constraints-based framework urges us to seek systemic reasons for the behavior of leaders. Political science provides a clear theoretical explanation for why London and Washington continued to trade with the enemy despite the clarity of the threat. The answer lies in the systemic nature of the constraint: a multipolar world reduces the sensitivity of policymakers to relative gains by introducing a collective action problem thanks to changing alliances and the difficulty of disciplining allies’ behavior. In the case of U.S. and China, this is further accentuated by President Trump’s strategy of skirting multilateral diplomacy and intense focus on mercantilist measures of power (i.e. obsession with the trade deficit). An anti-China trade policy that was accompanied by a magnanimous approach to trade relations with allies could have produced a “coalition of the willing” against Beijing. But after two years of tariffs and threats against the EU, Japan, and Canada, the Trump administration has already signaled to the rest of the world that old alliances and coordination avenues are up for revision. There are two outcomes that we can see emerging over the course of the next decade. First, U.S. leadership will become aware of the systemic constraints under which they operate, and trade with China will continue – albeit with limitations and variations. However, such trade will not reduce the geopolitical tensions, nor will it prevent a military conflict. In facts, the probability of military conflict may increase even as trade between China and the U.S. remains steady. Second, U.S. leadership will fail to correctly assess that they operate in a multipolar world and will give up the highlighted trade gains from Diagram II-2 to economic rivals such as Europe and Japan. Given our methodological adherence to constraint-based forecasting, we highly doubt that the latter scenario is likely. Bottom Line: The China-U.S. conflict is not a replay of the Cold War. Systemic pressures from global multipolarity will force the U.S. to continue to trade with China, with limitations on exchanges in emergent, dual-use technologies that China will nonetheless source from other technologically advanced countries. This will create a complicated but exciting world where geopolitics will cease to be seen as exogenous to investing. A risk to the sanguine conclusion is that the historical record is applicable to today, but that the hour is late, not early. It is already July 26, 1941 – when U.S. abrogated all trade with Japan – not 1930. As such, we do not have another decade of trade between U.S. and China remaining, we are at the end of the cycle. While this is a risk, it is unlikely. American policymakers would essentially have to be willing to risk a military conflict with China in order to take the trade war to the same level they did with Japan. It is an objective fact that China has meaningfully stepped up aggressive foreign policy in the region. But unlike Japan in 1941, China has not outright invaded any countries over the past decade. As such, the willingness of the public to support such a conflict is unclear, with only 21% of Americans considering China a top threat to the U.S. Investment Implications This analysis is not meant to be optimistic. First, the U.S. and China will continue to be rivals even if the economic relationship between them does not lead to global bifurcation. For one, China continues to be – much like Germany in the early twentieth century – concerned with access to external markets on which 19.5% of its economy still depend. China is therefore developing a modern navy and military not because it wants to dominate the rest of the world but because it wants to dominate its near abroad, much as the U.S. wanted to, beginning with the Monroe Doctrine. This will continue to lead to Chinese aggression in the South and East China Seas, raising the odds of a conflict with the U.S. Navy. Given that the Thucydides Trap narrative remains cogent, investors should look to overweight S&P 500 aerospace and defense stocks relative to global equity markets. An alternative way that one could play this thesis is by developing a basket of global defense stocks. Multipolarity may create constraints to trade protectionism, but it engenders geopolitical volatility and thus buoys defense spending. Second, we would not expect another uptick in globalization. Multipolarity may make it difficult for countries to completely close off trade with a rival, but globalization is built on more than just trade between rivals. Globalization requires a high level of coordination among great powers that is only possible under hegemonic conditions. Chart II-9 shows that the hegemony of the British and later American empires created a powerful tailwind for trade over the past two hundred years. Chart II-9The Apex Of Globalization Is Behind Us

The Apex Of Globalization Is Behind Us

The Apex Of Globalization Is Behind Us

The Apex of Globalization has come and gone – it is all downhill from here. But this is not a binary view. Foreign trade will not go to zero. The U.S. and China will not completely seal each other’s sphere of influence behind a Silicon Curtain. Instead, we focus on five investment themes that flow from a world that is characterized by the three trends of multipolarity, Sino-U.S. geopolitical rivalry, and apex of globalization: Europe will profit: As the U.S. and China deepen their enmity, we expect some European companies to profit. There is some evidence that the investment community has already caught wind of this trend, with European equities modestly outperforming their U.S. counterparts whenever trade tensions flared up in 2019 (Chart II-10). Given our thesis, however, it is unlikely that the U.S. would completely lose market share in China to Europe. As such, we specifically focus on tech, where we expect the U.S. and China to ramp up non-tariff barriers to trade regardless of systemic pressures to continue to trade. A strategic long in the secularly beleaguered European tech companies relative to their U.S. counterparts may therefore make sense (Chart II-11). Chart II-10Europe: A Trade War Safe Haven

Europe: A Trade War Safe Haven

Europe: A Trade War Safe Haven

Chart II-11Is Europe Really This Incompetent?

Is Europe Really This Incompetent?

Is Europe Really This Incompetent?

USD bull market will end: A trade war is a very disruptive way to adjust one’s trade relationship. It opens one to retaliation and thus the kind of relative losses described in this analysis. As such, we expect that U.S. to eventually depreciate the USD, either by aggressively reversing 2018 tightening or by coercing its trade rivals to strengthen their currencies. Such a move will be yet another tailwind behind the diversification away from the USD as a reserve currency, a move that should benefit the euro. Bull market in capex: The re-wiring of global manufacturing chains will still take place. The bad news is that multinational corporations will have to dip into their profit margins to move their supply chains to adjust to the new geopolitical reality. The good news is that they will have to invest in manufacturing capex to accomplish the task. One way to articulate this theme is to buy an index of semiconductor capital companies (AMAT, LRCX, KLAC, MKSI, AEIS, BRIKS, and TER). Given the highly cyclical nature of capital companies, we would recommend an entry point once trade tensions subside and green shoots of global growth appear. “Non-aligned” markets will benefit: The last time the world was multipolar, great powers competed through imperialism. This time around, a same dynamic will develop as countries seek to replicate China’s “Belt and Road Initiative.” This is positive for frontier markets. A rush to provide them with exports and services will increase supply and thus lower costs, providing otherwise forgotten markets with a boon of investments. India, and Asia-ex-China more broadly, stand as intriguing alternatives to China, especially with the current administration aggressively reforming to take advantage of the rewiring of global manufacturing chains. Capital markets will remain globalized: With interest rates near zero in much of the developed world and the demographic burden putting an ever-greater pressure on pension plans to generate returns, the search for yield will continue to be a powerful drive that keeps capital markets globalized. Limitations are likely to grow, especially when it comes to cross-border private investments in dual-use technologies. But a completely bifurcation of capital markets is unlikely. The world we are describing is one where geopolitics will play an increasingly prominent role for global investors. It would be convenient if the world simply divided into two warring camps, leaving investors with neatly separated compartments that enabled them to go back to ignoring geopolitics. This is unlikely. Rather, the world will resemble the dynamic years at the end of the nineteenth century, a rough-and-tumble era that required a multi-disciplinary approach to investing. Marko Papic Consulting Editor, BCA Research Chief Strategist, Clocktower Group Footnotes 1 Please see BCA Research Geopolitical Strategy, “Power And Politics In East Asia: Cold War 2.0?,” September 25, 2012, “Sino-American Conflict: More Likely Than You Think,” October 4, 2013, “The Great Risk Rotation,” December 11, 2013, and “Strategic Outlook 2014 – Stay The Course: EM Risk – DM Reward,” January 23, 2014, “Underestimating Sino-American Tensions,” November 6, 2015, “The Geopolitics Of Trump,” December 2, 2016, “How To Play The Proxy Battles In Asia,” March 1, 2017, and others available at gps.bcaresearch.com or upon request. 2 Please see German Historical Institute, “Bernhard von Bulow on Germany’s ‘Place in the Sun’” (1897), available at http://germanhistorydocs.ghi-dc.org/ 3 See Graham Allison, Destined For War: Can America and China Escape Thucydides’s Trap? (New York: Houghton Miffin Harcourt, 2017). 4 The three cases are Spain taking over from Portugal in the sixteenth century, the U.S. taking over from the U.K. in the twentieth century, and Germany rising to regional hegemony in Europe in the twenty-first century. 5 Duncan Snidal, “Relative Gains and the Pattern of International Cooperation,” The American Political Science Review, 85:3 (September 1991), pp. 701-726. 6 We do not review Snidal’s excellent game theory formal modeling in this paper as it is complex and detailed. However, we highly encourage the intrigued reader to pursue the study on their own. 7 See Charles P. Kindleberger, The World In Depression, 1929-1939 (Berkeley: University of California Press, 2013). 8 Joanne Gowa and Edward D. Mansfield, “Power Politics and International Trade,” The American Political Science Review, 87:2 (June 1993), pp. 408-420. 9 See Ernest Edwin Williams, Made in Germany (reprint, Ithaca: Cornell University Press), available at https://archive.org/details/cu31924031247830. 10 Quoted in Margaret MacMillan, The War That Ended Peace (Toronto: Allen Lane, 2014). 11 Peter Liberman, “Trading with the Enemy: Security and Relative Economic Gains,” international Security, 21:1 (Summer 1996), pp. 147-175. 12 Although France and Russia overcame even greater bitterness due to the ideological differences between a republic founded on a violent uprising against its aristocracy – France – and an aristocratic authoritarian regime – Russia. 13 See James Morrow, “When Do ‘Relative Gains’ Impede Trade?” The Journal of Conflict Resolution, 41:1 (February 1997), pp. 12-37; and Jack S. Levy and Katherine Barbieri, “Trading With the Enemy During Wartime,” Security Studies, 13:3 (December 2004), pp. 1-47.

Highlights Declining uncertainty over policy, stabilizing growth in China and improvements in international liquidity, all will allow global economic activity to pick up in the months ahead. A weak dollar will reinforce this positive economic outlook; investors should favor pro-cyclical currencies such as the AUD, NZD and SEK. Bond yields will rise and stocks will outperform bonds on a 12- to 18-month basis. Cyclical stocks are more attractive than defensives. European stocks will outperform U.S. equities and European financials will shine. Copper is a promising buy; stay long the silver-to-gold ratio. Feature The outlook for risk assets and bond yields hinges on global economic activity. The S&P 500 has hit a new high, but our BCA Equity Scorecard Indicator remains non-committal towards stocks (Chart I-1). If global economic activity improves, the Scorecard will begin to flash a clear buy signal, but if growth deteriorates, the indicator will point towards sell. Chart I-1Stocks Could Go Either Way

Stocks Could Go Either Way

Stocks Could Go Either Way

Cautious optimism is in order. Politics, China, liquidity conditions and the dollar collectively will determine the global economic outlook. The liquidity backdrop has significantly improved, political uncertainty should recede and China will morph from a headwind to a modest tailwind. A weak dollar will indicate that the world is healing, and also will ease global financial conditions which will facilitate economic strength. We remain committed to a positive stance on equities on a 12- to 18-month horizon, and recommend below-benchmark duration in fixed-income portfolios. Cyclicals should outperform defensives, European banks offer an attractive tactical buying opportunity and European equities will outperform their U.S. counterparts. Heightened Risks… Chart I-2Risks To The Economy And Stocks

Risks To The Economy And Stocks

Risks To The Economy And Stocks

Many domestic indicators overstate the intrinsic fragility in the U.S. The Duncan LEI, which is the ratio of consumer durable spending and residential and business investment to final sales, has flattened. Therefore, the S&P 500 looks vulnerable and real GDP may contract (Chart I-2). CEO confidence and small business capex intentions warn of a looming retrenchment in household income (Chart I-2, bottom two panels). If consumer spending weakens, then a recession will be unavoidable. As worrisome as these indicators may be, we previously discussed that the major debt imbalances that often precede U.S. recessions are absent,1 the rebound in housing starts and homebuilding confidence is inconsistent with a restrictive monetary stance,2 and pipeline inflationary pressures are absent.3 Instead, business confidence and the Duncan LEI have been eroded by heightened political uncertainty and weak global manufacturing and trade. … Meet Receding Policy Uncertainty … The two biggest sources of policy uncertainty affecting markets, the Sino-U.S. trade war and Brexit, are diminishing. However, the U.S. election will continue to lurk in the background. Chart I-3Weaker Brexit Support = No Hard Brexit Support

Weaker Brexit Support = No Hard Brexit Support

Weaker Brexit Support = No Hard Brexit Support

Brexit Westminster and Britain’s Supreme Court have rebuked U.K. Prime Minister Boris Johnson’s threat of a “No-Deal” Brexit. Moreover, parliamentary support for his latest plan, which essentially keeps Northern Ireland’s economy within the EU, indicates that the probability of a “No-Deal” Brexit has collapsed to less than 5%. This assessment is reinforced by the delay of Brexit to January 31, 2020. An election is scheduled for December 12 and the chance of a new referendum to vet the deal is escalating. According to Matt Gertken, BCA’s Geopolitical Strategist, an election does not increase the risk of a hard Brexit. Meanwhile, support for Brexit is near its lowest point since the June 2016 referendum (Chart I-3). Thus, a new plebiscite would not favor a “No Deal” Brexit. Sino-U.S. Trade War Chart I-4Why The Trade-War Ceasefire?

Why The Trade-War Ceasefire?

Why The Trade-War Ceasefire?

The trade war truce will also greatly diminish economic uncertainty. Uncertainty created by the China-U.S. conflict accentuated the collapse in business confidence and capex intentions. The “phase one deal” announced earlier this month will likely materialize. The White House’s tactical retreat on trade is tied to U.S. President Donald Trump’s desire for a second term. He cannot risk inflicting further economic pain on his base of constituents. Weekly earnings are decreasing for workers in swing states located in the industrial rust belt, especially in those areas that Trump carried in 2016 (Chart I-4). Those swing states are most affected by the slowdown in the global manufacturing and trade sectors. Beijing is also motivated to agree to truce due to its soft economy and deflationary pressures. An easing in trade uncertainty will be positive for the domestic economy. China’s willingness to replace Carrie Lam, the embattled Chief Executive of Hong Kong, and to withdraw the extradition bill at the heart of the protests confirms its eagerness to come to an agreement with the U.S. China’s readiness to make a deal is also made evident by its increasing imports of U.S. agricultural products (Chart I-4, bottom panel). Ultimately, the U.S. will not implement tariffs in December on $160 billion of Chinese shipments. Consequently, investors and businesses should become less concerned about the chances of a worsening trade war. Moreover, chances are growing of a decrease (but not a complete annulation) of the previously imposed U.S. tariffs on China. … And A Q1 2020 Acceleration In Global Growth Global economic activity will improve in Q1 2020 because the drag from China will dissipate and global liquidity conditions will improve. Many activity indicators increasingly reflect these fundamental supports. China China’s economy has reached a new low point: Q3 annual GDP growth is at a 27-year low of 6%, capital spending is weak, industrial production and profits show little life, the labor market is soft, and imports and exports continue to contract. However, a turn in policy has materialized, which will protect the domestic economy. Moreover, this summer’s Politburo and State Council statements showed an increased willingness to reflate the economy. The global economy will accelerate in Q1 2020. Credit creation has stabilized and monetary conditions have eased (Chart I-5). Faced with producer price inflation of -1.2% and employment PMIs of 47.3 and 48.2 in the manufacturing and non-manufacturing sectors, respectively, authorities have allowed the credit impulse to improve to 26% of GDP from a low of 23.8%. In accordance with this new policy direction, the drag from the shadow banking system’s contraction will slow considerably, thanks to a stabilization in both the growth rate of deposits of non-depository financial institutions and the issuance of bonds by small financial institutions. Additionally, the emission of local government bonds will accelerate. Beijing has also meaningfully eased fiscal policy, which is its preferred reflationary tool. Policymakers have cut taxes by 2.8% of GDP in the past two years. The marginal propensity of households to consume is trying to bottom (Chart I-5, bottom). If history is a guide, the acceleration in the rate of change of public-sector capex will fuel this turnaround in China’s marginal propensity to consume, and push up BCA’s China Activity Indicator (Chart I-6). Chart I-5Overlooked Chinese Improvements

Overlooked Chinese Improvements

Overlooked Chinese Improvements

Chart I-6Public Investment Matters

Public Investment Matters

Public Investment Matters

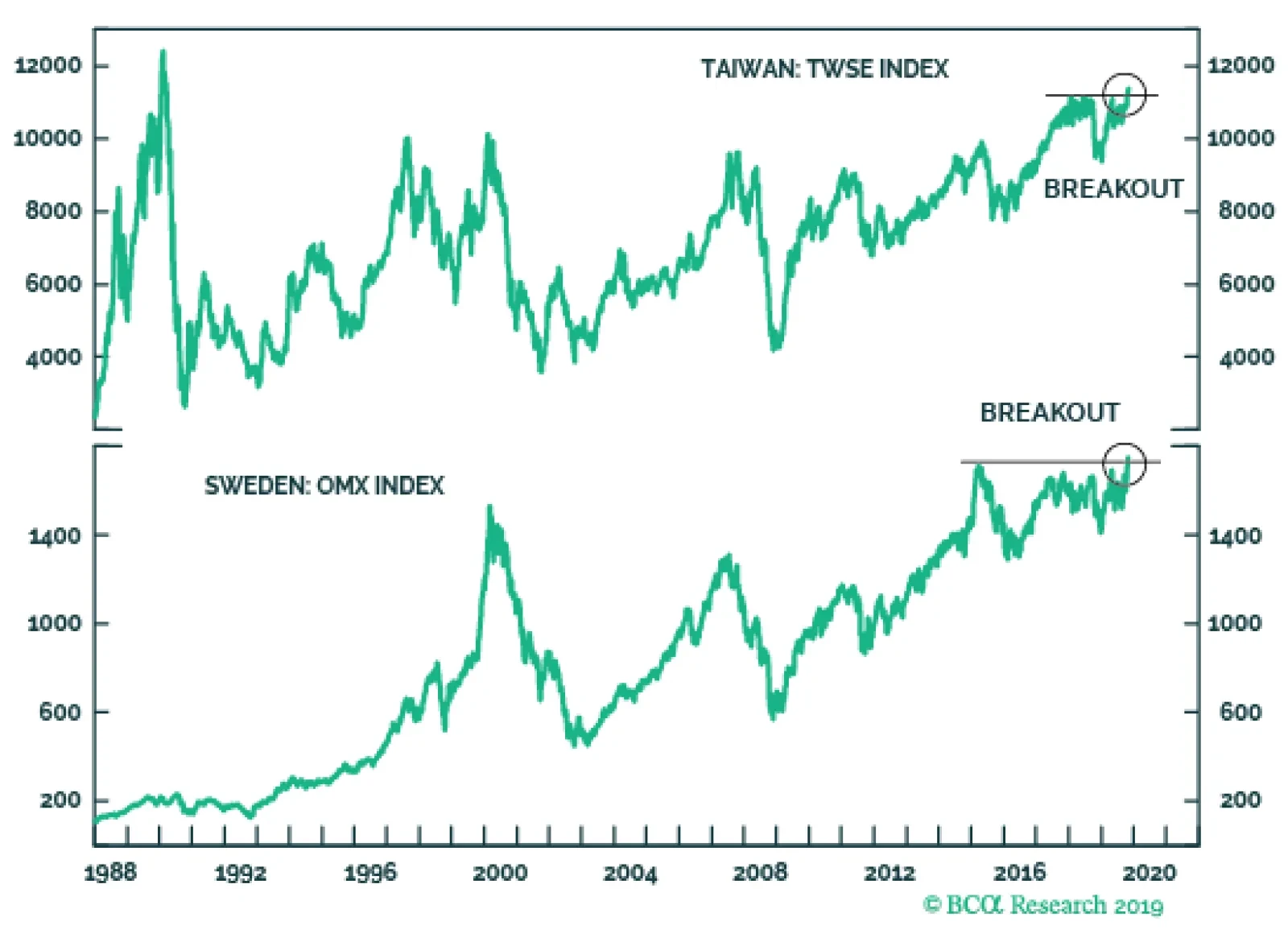

Chart I-7A Bottom In Chinese Exports Growth?

A Bottom In Chinese Exports Growth?

A Bottom In Chinese Exports Growth?

China’s economy is unlikely to bounce back as violently as in 2009, 2012 or 2016. Authorities are much more circumspect in their use of credit to reflate the economy than they were previously. Moreover, the regulatory environment will prevent a boom in the shadow banking system. Nonetheless, the fiscal push and the end of the decline in aggregate credit growth will allow the Chinese economy to stabilize and maybe pick up a bit. Therefore, China will move from a large headwind to a slight tailwind for global activity (Chart I-7, top panel). Mounting public capex also points toward a modest global recovery (Chart I-7, middle panel). Finally, the upturn in our Chinese reflation indicator, which incorporates both fiscal and monetary policy, points to a re-acceleration in U.S. capex intentions (Chart I-7, bottom panel). Global Liquidity Global liquidity conditions continue to improve and the global economy should soon respond within normal policy lags. 95% of central banks are loosening policy, which normally leads to an escalation in global activity (Chart I-8). The dominant central banks (the Federal Reserve, the European Central Bank and the Bank of Japan) will not tighten anytime soon. Inflation expectations in the U.S., the euro area and Japan stand at 1.9%, 1.1%, and 0.2%, respectively, well below levels consistent with a 2% inflation target. Moreover, U.S. core CPI has been perky, but both the ISM and the performance of transportation equities relative to utilities indicate that a deceleration in inflation is imminent (Chart I-9). Salaries are not yet inflationary either because U.S. real wages are growing in line with productivity (Chart I-9, bottom panel). In the euro area and Japan, realized core inflation remains at 1.0% and 0.5%, respectively, and supports the dovish message emanating from inflation expectations. Chart I-8Easier Global Policy Is Important

Easier Global Policy Is Important

Easier Global Policy Is Important

Chart I-9If Inflation Peaks, The U.S. Economy Will Breath A Sigh Of Relief

If Inflation Peaks, The U.S. Economy Will Breath A Sigh Of Relief

If Inflation Peaks, The U.S. Economy Will Breath A Sigh Of Relief

Liquidity indicators are reflecting this accommodative policy setting. The growth of U.S. and European bank deposits has reaccelerated from 2.5% to 6%, a development linked to the exit of a soft patch (Chart I-10). Moreover, BCA’s U.S. Financial Liquidity Indicator is still moving higher and flashing a resurgence in the BCA Global Leading Economic Indicator (LEI), the ISM Manufacturing Index, commodity prices, and EM export prices (Chart I-11). Finally, U.S. and global excess money reinforce the message of BCA’s U.S. Financial liquidity Indicator (Chart I-12). Chart I-10Deposits Suggest The Worst Of The Slowdown Is Behind Us

Deposits Suggest The Worst Of The Slowdown Is Behind Us

Deposits Suggest The Worst Of The Slowdown Is Behind Us

Chart I-11Continued Pick-Up In Financial Liquidity

Continued Pick-Up In Financial Liquidity

Continued Pick-Up In Financial Liquidity

The Fed will add to the supply of global liquidity by tackling the repo market’s seize-up. Depleting excess reserves and mounting financing needs among primary dealers resulted in the September surge in the Secured Overnight Financing Rate (SOFR). The Fed announced three weeks ago it would buy $60 billion per month of T-Bills and T-Notes, which will lead to a climbing stock of excess reserves. Higher excess reserves create a weaker dollar, stronger EM currencies and firming global PMIs (Chart I-13). Ultimately, EM currency strength eases EM financial conditions, which supports global growth (Chart I-13, bottom panel). Chart I-12Excess Liquidity Is Accelerating

Excess Liquidity Is Accelerating

Excess Liquidity Is Accelerating

Chart I-13U.S. Excess Reserves Will Grow Again

U.S. Excess Reserves Will Grow Again

U.S. Excess Reserves Will Grow Again

Borrowing activity in Advanced Economies is showing signs of life. Bank credit is already responding to the drop in global yields, and global corporate bond issuance in September 2019 rose to $434 billion. In the U.S., new issues of corporate bonds have also reaccelerated (Chart I-14). Global Growth Indicators Crucial indicators of global economic activity are picking up on this improving fundamental backdrop. The list includes: A sharp takeoff in the annualized three-month rate of change of capital goods orders in the U.S., the Eurozone and Japan (Chart I-15, top panel). Improvement in this indicator precedes progress in the annual growth rate of orders and in capex itself. Chart I-14Borrowers Are Responding To Easier Financial Conditions

Borrowers Are Responding To Easier Financial Conditions

Borrowers Are Responding To Easier Financial Conditions

Chart I-15Some Green Shoots Are Coming Through

Some Green Shoots Are Coming Through

Some Green Shoots Are Coming Through

Chart I-16Positive Market Signals

Positive Market Signals

Positive Market Signals

A significant upturn in the Philly Fed, Empire State, and Richmond Fed manufacturing surveys for October, which sends a positive signal for the ISM Manufacturing Index (Chart I-15, second panel). Moreover, the new orders and employment components of these surveys indicate that cyclical sectors of the economy will recover and the recent deterioration in employment conditions will be fleeting. A rebound in BCA’s EM economic diffusion index, which incorporates 23 variables. Such an increase usually precedes inflections in global industrial production (Chart I-15, bottom panel). An acceleration – both in absolute and relative terms - in the annual appreciation of Taiwanese stocks. A strong and outperforming Taiwanese equity market is a harbinger of firmer PMIs (Chart I-16, top two panels). A solid performance of EM carry trades financed in yen, European luxury equities, and the relative performance of global semiconductors, materials and industrial stocks, which signal stronger global PMIs (Chart I-16, bottom three panels). Bottom Line: The global economy will accelerate in Q1 2020. A melting probability of a “No-Deal” Brexit and a truce in the Sino-U.S. trade war will allow global uncertainty to recede. Concurrently, China’s economic slowdown is ending and global liquidity conditions are improving. The Dollar As The Arbiter Of Growth Chart I-17The Dollar Is A Counter-Cyclical Currency

The Dollar Is A Counter-Cyclical Currency

The Dollar Is A Counter-Cyclical Currency

The dollar faces potent headwinds. The greenback is a countercyclical currency; a business cycle upswing and a weak USD go hand in hand (Chart I-17). The tightness of this relationship results from a powerful feedback loop: weak growth boosts the dollar, but the dollar’s strength foments additional economic slowdown. Global liquidity and activity indicators signal a weaker dollar because they point toward an economic recovery. BCA’s U.S. Financial Liquidity Index, which foresaw a deceleration in the greenback’s rate of appreciation, is calling for an outright depreciation (Chart I-18, top panel). The expanding holdings of securities on U.S. commercial banks’ balance sheets (a key measure of liquidity) corroborates this message. According to a model based on the U.S., Eurozone, Japanese and Chinese broad money supply, the USD should significantly depreciate in the coming 12 months (Chart I-18, third panel). Finally, our EM Economic Diffusion Index validates pressures on the greenback, especially against commodity currencies (Chart I-18, bottom two panels). Chart I-18Liquidity And Growth Indicators Point To A Weaker Dollar

Liquidity And Growth Indicators Point To A Weaker Dollar

Liquidity And Growth Indicators Point To A Weaker Dollar

Growth differentials support this picture. Late last year, the stimulating effect of President Trump’s tax cuts allowed the U.S. to temporarily diverge from a weak global economy, but the U.S. manufacturing sector is now succumbing to the global slowdown. Once global growth snaps back, the U.S. is likely to lag behind as fiscal policy is becoming more stimulative outside the U.S. than in the U.S. Based on historical delays, this will continue to hurt the dollar (Chart I-19, top panel). Finally, the European economy generally outperforms the U.S. when China reflates, especially if Beijing’s push lifts the growth rate of M1 relative to M2, a proxy for China’s aggregate marginal propensity to consume (Chart I-20). Europe’s greater cyclicality reflects is larger exposure to both trade and manufacturing compared with the U.S. Chart I-19A Global Growth Convergence Will Hurt The Dollar

A Global Growth Convergence Will Hurt The Dollar

A Global Growth Convergence Will Hurt The Dollar

Chart I-20European Growth To Rise Vis-A-Vis The U.S.

European Growth To Rise Vis-A-Vis The U.S.

European Growth To Rise Vis-A-Vis The U.S.

The greenback is expensive and technically vulnerable, which compounds its cyclical risk. The trade-weighted dollar is at a 25% premium to its purchasing power parity equilibrium (PPP), an overvaluation comparable to its 1985 and 2002 peaks. Moreover, our Composite Technical Indicator is overextended and has formed a negative divergence with the price of the dollar (see page 54, Section III). Finally, speculators are massively long the U.S. Dollar Index (DXY). Balance-of-payment flows also flash a significant downside in the dollar (Chart I-21). The U.S. current account deficit stands at 2.5% of GDP, but it is widening in response to the dollar’s overvaluation and the White House’s expansive fiscal policy. Since 2011, foreign direct investments (FDI) have been the main driver of the dollar’s gyrations. Last year, net FDI surged in response to profit repatriations encouraged by the Tax Cuts and Jobs Act of 2017, while portfolio flows stayed in neutral territory. This regulatory change had a one-off impact and FDI will begin to dry out. Therefore, financing the widening current account deficit will become harder. Finally, after years in the red, net portfolio flows into Europe have turned positive (Chart I-21, bottom panel). The USD’s depreciation will ease global financial conditions and supports growth further. In this context, interest rate differentials are noteworthy. The two-year spread in real rates between the U.S. and the rest of the G-10 has fallen significantly since October 2018. Reversals in real rates herald a weaker dollar, especially when it faces valuation, technical and flow handicaps. Moreover, European five-year forward short rate expectations are near record lows. If global growth can stabilize, then the five-year forward one-month OIS will pick up, especially relative to the U.S. An uptick will boost the EUR/USD pair and hurt the dollar (Chart I-22). Chart I-21Balance-Of-Payments Dynamics Turning Against The USD

Balance-Of-Payments Dynamics Turning Against The USD

Balance-Of-Payments Dynamics Turning Against The USD

Chart I-22Relative Long-Term Rate Expectations And The Euro

Relative Long-Term Rate Expectations And The Euro

Relative Long-Term Rate Expectations And The Euro

The three most pro-cyclical currencies in the G-10 – the AUD, NZD and SEK - strengthen the most when BCA’s Global LEI bottoms but global inflation slows (Chart I-23). The GBP will likely generate a much stronger-than-normal performance next year. Cable trades at a 22% discount to PPP. It is also 19% cheap versus short-term interest rate parity models. The absence of a “No-Deal” Brexit should allow these risk premia to dissipate and the pound to recover. The CAD is also more attractive than Chart I-23 implies. The loonie is trading 10% below its PPP, and the USD/CAD often lags the EUR/CAD, a pair that has broken down (Chart I-24). Chart I-23Currency Performance As A Function Of Growth And Inflation

November 2019

November 2019

Chart I-24EUR/CAD Flashing A Bearish USD/CAD Signal

EUR/CAD Flashing A Bearish USD/CAD Signal

EUR/CAD Flashing A Bearish USD/CAD Signal

Bottom Line: A rebound in the global manufacturing sector next year will hurt the USD. The dollar is particularly vulnerable because growth differentials between the U.S. and the rest of the world have melted, the greenback is expensive, balance-of-payment dynamics are deteriorating and interest rate differentials are becoming less supportive. The USD’s depreciation will ease global financial conditions and supports growth further. Additional Investment Implications Bond Yields Have More Upside While the short-term outlook for bonds remains murky, the 12- to 18-month outlook is unambiguously bearish. The BCA Bond Valuation Index is still consistent with much higher U.S. yields in the next 12-18 months (see Section III, page 51). BCA’s Composite Technical Indicator for T-Notes is massively overbought and sentiment, as approximated by the Long-Term Interest Rates component of the ZEW survey, is overly bullish (Chart I-25). Thus, bonds represent an attractive cyclical sell. The Fed will not cut rates aggressively enough for bonds to ignore these valuation and technical risks. Treasurys have outperformed cash by 7.5% in the past year. Based on historical relationships, the Fed needs to cut rates to zero for bonds to beat cash in the coming 12 months (Chart I-26). After this week’s Fed cut to 1.75%, our base case is none to maybe one more rate cut. Chart I-25Sentiment Points To Yield Upside

Sentiment Points To Yield Upside

Sentiment Points To Yield Upside

Chart I-26The Fed Must Cut To Zero For T-Notes To Outperform Cash Further

The Fed Must Cut To Zero For T-Notes To Outperform Cash Further

The Fed Must Cut To Zero For T-Notes To Outperform Cash Further

Bond yields will need a recession to move lower. The deviation of 10-year Treasury yields from their two-year moving average closely tracks the Swedish Economic Diffusion Index (Chart I-27, top panel). Sweden, a small, open economy highly levered to the global industrial cycle, is a good gauge of the global business cycle. The broad weakness in the Swedish economy is unlikely to worsen unless the global slowdown morphs into a deep recession. Even if global growth remains mediocre, Sweden’s Economic Diffusion Index will rise along with yields. The expansion in securities holdings of U.S. commercial banks and the stabilization in China’s credit flows both support this notion (Chart I-27, bottom panel). Financial market developments also point to higher yields. Sectors that typically capture the momentum in the global economy are perking up. For example, bottoms in the annual performance of European luxury equities or Taiwanese stocks have preceded increases in yields (Chart I-28). Chart I-27Yields Have Upside

Yields Have Upside

Yields Have Upside

Chart I-28Key Financial Market Signals For Yields

Key Financial Market Signals For Yields

Key Financial Market Signals For Yields

Stocks Will Outperform Bonds Our conviction is strengthening that equities will outperform bonds. The total return of the stock-to-bond ratio has upside. BCA’s Global Economic and Financial Diffusion Index has rallied sharply, which often precedes an ascent in the stock-to-bond ratio, both in the U.S. and globally (Chart I-29). Bonds are much more expensive than stocks, therefore, only a recession will allow stocks to underperform in the coming 12 to 18 months. The environment is positive for equities. BCA’s Monetary Indicator is very elevated and our Composite Sentiment Indicator shows little complacency toward stocks among investors (see Section III, page 47). Finally, the strength in the U.S. Financial Liquidity Indicator supports the S&P 500’s returns (Chart I-30). Chart I-29Cyclical Indicators Argue In Favor Of Stocks Over Bonds

Cyclical Indicators Argue In Favor Of Stocks Over Bonds

Cyclical Indicators Argue In Favor Of Stocks Over Bonds

Chart I-30Liquidity Tailwind For The S&P 500

Liquidity Tailwind For The S&P 500

Liquidity Tailwind For The S&P 500

A few market developments are noteworthy. 55.6% of the S&P 500’s constituents have reported Q3 earnings, and 74% of those firms are beating estimates. Moreover, the market is generously rewarding firms with the largest positive earnings surprises. Additionally, the Value Line Geometric Index is forming a reverse head-and-shoulder pattern, while the relative performance of the Russell 2000 has formed a double bottom (Chart I-31). The environment also favors cyclicals relative to defensive equities. By lifting bond yields, stronger economic activity leads to a contraction in the multiples of defensives relative to cyclicals. The latter’s earnings expectations respond more positively to reviving economic activity, which creates an offset to climbing discount rates. As a result, cyclicals often outperform defensives when the stock-to-bond ratio increases, or after Taiwanese equities gain momentum (Chart I-32). Chart I-31Improving Equity Market Dynamics

Improving Equity Market Dynamics

Improving Equity Market Dynamics

Chart I-32Favor Cyclicals Over Defensives

Favor Cyclicals Over Defensives

Favor Cyclicals Over Defensives

Compared to other equity markets, the U.S. faces the most challenges. Our model forecasts a 3% annual drop in the S&P 500’s operating earnings in June 2020, and the deviation of U.S. equities from their 200-day moving average has greatly diverged from net earnings revisions (Chart I-33). U.S. equities have already discounted a turnaround in earnings. Moreover, the S&P 500’s margins have downside, a topic covered by BCA’s Chief Equity Strategist Anastasios Avgeriou.4 Our Composite Margin Proxy, Operating Margins Diffusion Index and Corporate Pricing Power Indicator all remain weak (Chart I-34). Downward pressure on margins will limit how rapidly earnings respond when a rebound in global economic activity lifts revenues. Finally, the S&P 500 trades at a historically elevated forward P/E ratio of 18.4, the MSCI EAFE trade at a much more reasonable 14-times forward earnings. Chart I-33Headwinds For U.S. Stocks

Headwinds For U.S. Stocks

Headwinds For U.S. Stocks

Chart I-34Headwinds For U.S. Margins

Headwinds For U.S. Margins

Headwinds For U.S. Margins

The tech sector will also weigh on the performance of U.S. equities relative to international stocks. Tech stocks represent 22.5% of the U.S. benchmark, compared with 9.7% for the euro area. Anastasios recently argued that software spending has remained surprisingly resilient despite the global economic slowdown; it will likely lag spending on machinery and structures when the cycle picks up.5 Consequently, tech earnings will lag other traditional cyclical sectors. Moreover, tech multiples will suffer when the dollar depreciates and bond yields rise (Chart I-35). As high-growth stocks, tech equities derive a large proportion of their intrinsic value from long-term deferred cash flows and their terminal value. Thus, tech multiples are highly sensitive to discount factors. Unaffected by those negatives, European equities will benefit most from the outperformance of stocks relative to bonds. A weak dollar will be the first positive for the common-currency returns of European equities. Valuations are the second tailwind. The risk premium for European equities is 300 basis points higher than for U.S. stocks. Moreover, U.S. margins will likely diminish relative to the Eurozone’s because of stronger unit labor costs in the U.S. Sector composition will also dictate the performance of European equities. Compared with the U.S., Europe is underweight tech and healthcare stocks, a defensive sector (Table I-1). Investors who favor Europe will also bet against these two sectors. Europe is a wager on the other cyclical sectors: materials, industrials, energy and financials. Chart I-35Tech P/Es Are At Risk

Tech P/Es Are At Risk

Tech P/Es Are At Risk

Table I-1Europe Overweights The Correct Cyclicals

November 2019

November 2019

European financials are particularly attractive. Negative European yields are a major handicap for European financials, but this handicap is already reflected in their price. European banks trade at a price-to-book ratio of 0.6 versus 1.3 for the U.S. This discount should be narrowing, not widening. Yields are bottoming and European loan growth is contracting at a -2% annual rate relative to the U.S. versus -8.6% five years ago. Meanwhile, the annual rate of change of European deposits is in line with the U.S. The attraction of European banks comes from the outlook for their return on tangible equity. A model shows that three variables govern European banks’ ROE: German yields, Italian spreads and the momentum of the silver-to-gold ratio (SGR). German yields impact net interest margins, Italian spreads drive peripheral financial conditions and thus, loan generation in the European periphery, and the SGR tracks the global manufacturing cycle (silver has more industrial uses than gold, but is equally sensitive to real yields), which affects loan flows in the European core. This model logically tracks the performance of European banks and financials (Chart I-36). Our positive outlook on global growth and yields, along with the fall in Italian spreads, augurs well for cheap European financial equities and banks in particular. Commodities Our constructive stance on the global business cycle and yields, plus our negative view on the greenback, is consistent with higher industrial commodity prices. Copper looks particularly attractive. Speculators are aggressively selling the metal, whose price stands at an important technical juncture (Chart I-37). Chart I-36The Drivers Of RoE Point To Higher European Bank Stock Prices

The Drivers Of RoE Point To Higher European Bank Stock Prices

The Drivers Of RoE Point To Higher European Bank Stock Prices

Chart I-37Cooper Is An Attractive Play On Global Growth

Cooper Is An Attractive Play On Global Growth

Cooper Is An Attractive Play On Global Growth

Chart I-38Favorable Technical Backdrop For Silver-To-Gold Ratio

Favorable Technical Backdrop For Silver-To-Gold Ratio

Favorable Technical Backdrop For Silver-To-Gold Ratio

Finally, we have favored the SGR since late June. Silver is deeply oversold and under-owned relative to the yellow metal (Chart I-38). Consequently, silver’s greater industrial usage should be a potent tailwind for the SGR.6 Mathieu Savary Vice President The Bank Credit Analyst October 31, 2019 Next Report: November 22, 2019 - Outlook 2020 II. Back To The Nineteenth Century The Cold War is a limited analogy for the U.S.-China conflict; In a multipolar world, complete bifurcation of trade is difficult if not impossible; History suggests that trade between rivals will continue, with minimal impediments; On a secular horizon, buy defense stocks, Europe, capex, and non-aligned countries. There is a growing consensus that China and the U.S. are hurtling towards a Cold War. BCA Research played some part in this consensus – at least as far as the investment community is concerned – by publishing “Power and Politics in East Asia: Cold War 2.0?” in September 2012.7 For much of this decade, Geopolitical Strategy focused on the thesis that geopolitical risk was rotating out of the Middle East, where it was increasingly irrelevant, to East Asia, where it would become increasingly relevant. This thesis remains cogent, but it does not mean that a “Silicon Curtain” will necessarily divide the world into two bifurcated zones of capitalism. Trade, capital flows, and human exchanges between China and the U.S. will continue and may even grow. But the risk of conflict, including a military one, will not decline. In this report, we first review the geopolitical logic that underpins Sino-American tensions. We then survey the academic literature for clues on how that relationship will develop vis-à-vis trade and economic relations. The evidence from political theory is surprising and highly investment relevant. We then look back at history for clues as to what this means for investors. The U.S.-China conflict will not lead to complete bifurcation of the global economy. Our conclusion is that it is highly likely that the U.S. and China will continue to be geopolitical rivals. However, due to the geopolitical context of multipolarity, it is unlikely that the result will be “Bifurcated Capitalism.” Rather, we expect an exciting and volatile environment for investors where geopolitics takes its historical place alongside valuation, momentum, fundamentals, and macroeconomics in the pantheon of factors that determine investment opportunities and risks. The Thucydides Trap Is Real … Speaking in the Reichstag in 1897, German Foreign Secretary Bernhard von Bülow proclaimed that it was time for Germany to demand “its own place in the sun.”8 The occasion was a debate on Germany’s policy towards East Asia. Bülow soon ascended to the Chancellorship under Kaiser Wilhelm II and oversaw the evolution of German foreign policy from Realpolitik to Weltpolitik. While Realpolitik was characterized by Germany’s cautious balancing of global powers under Chancellor Otto von Bismarck, Weltpolitik saw Bülow and Wilhelm II seek to redraw the status quo through aggressive foreign and trade policy. Imperial Germany joined a long list of antagonists, from Athens to today’s People’s Republic of China, in the tragic play of human history dubbed the “Thucydides Trap.”9 Chart II-1Imperial Overstretch

Imperial Overstretch

Imperial Overstretch

The underlying concept is well known to all students of world history. It takes its name from the Greek historian Thucydides and his seminal History of the Peloponnesian War. Thucydides explains why Sparta and Athens went to war but, unlike his contemporaries, he does not moralize or blame the gods. Instead, he dispassionately describes how the conflict between a revisionist Athens and established Sparta became inevitable due to a cycle of mistrust. Graham Allison, one of America’s preeminent scholars of international relations, has argued that the interplay between a status quo power and a challenger has almost always led to conflict. In 12 out of the 16 cases he surveyed, actual military conflict broke out. Of the four cases where war did not develop, three involved transitions between countries that shared a deep cultural affinity and a respect for the prevailing institutions.10 In those cases, the transition was a case of new management running largely the same organizational structure. And one of the four non-war outcomes was nothing less than the Cold War between the Soviet Union and the U.S. The fundamental problem for a status quo power is that its empire or “sphere of influence” remains the same size as when it stood at the zenith of power. However, its decline in a relative sense leads to a classic problem of “imperial overstretch.” The hegemonic or imperial power erroneously doubles down on maintaining a status quo that it can no longer afford (Chart II-1). The challenger power is not blameless. It senses weakness in the hegemon and begins to develop a regional sphere of influence. The problem is that regional hegemony is a perfect jumping off point towards global hegemony. And while the challenger’s intentions may be limited and restrained (though they often are ambitious and overweening), the status quo power must react to capabilities, not intentions. The former are material and real, whereas the latter are perceived and ephemeral. In a multipolar world, the U.S. will not be able to exclude China from the global system. The challenging power always has an internal logic justifying its ambitions. In China’s case today, there is a sense among the elite that the country is merely mean-reverting to the way things were for many centuries in China’s and Asia’s long history (Chart II-2). In other words, China is a “challenger” power only if one describes the status quo as the past three hundred years. It is the “established” power if one goes back to an earlier state of affairs. As such, the consensus in China is that it should not have to pay deference to the prevailing status quo given that the contemporary context is merely the result of western imperialist “challenges” to the established Chinese and regional order. Chart II-2China’s Mean Reverting Narrative

November 2019

November 2019

In addition, China has a legitimate claim that it is at least as relevant to the global economy as the U.S. and therefore deserves a greater say in global governance. While the U.S. still takes a larger share of the global economy, China has contributed 23% to incremental global GDP over the past two decades, compared to 13% for the U.S. (Chart II-3). Chart II-3The Beijing Consensus

November 2019

November 2019

Bottom Line: The emerging tensions between China and the U.S. fit neatly into the theoretical and empirical outlines of the Thucydides Trap. We do not see any way for the two countries to avoid struggle and conflict on a secular or forecastable horizon. What does this mean for investors? For one, the secular tailwinds behind defense stocks will persist. But what beyond that? Is the global economy destined to witness complete bifurcation into two armed camps separated by a Silicon Curtain? Will the Alibaba and Amazon Pacts suspiciously glare at each other the way that NATO and Warsaw Pacts did amidst the Cold War? The answer, tentatively, is no. … But It Will Not Lead To Economic Bifurcation President Trump’s aggressive trade policy also fits neatly into political theory, to a point. Realism in political science focuses on relative gains over absolute gains in all relationships, including trade. This is because trade leads to economic prosperity, prosperity to the accumulation of economic surplus, and economic surplus to military spending, research, and development. Two states that care only about relative gains due to rivalry produce a zero-sum game with no room for cooperation. It is a “Prisoner’s Dilemma” that can lead to sub-optimal economic outcomes in which both actors chose not to cooperate. Diagram II-1 illustrates the effects of relative gain calculations on the trade behavior of states. In the absence of geopolitics, demand (Q3) is satisfied via trade (Q3-Q0) due to the inability of domestic production (Q0) to meet it. Diagram II-1Trade War In A Bipolar World

November 2019

November 2019

However, geopolitical externality – a rivalry with another state – raises the marginal social cost of imports – i.e. trade allows the rival to gain more out of trade and “catch up” in terms of geopolitical capabilities. The trading state therefore eliminates such externalities with a tariff (t), raising domestic output to Q1, while shrinking demand to Q2, thus reducing imports to merely Q2-Q1, a fraction of where they would be in a world where geopolitics do not matter. The dynamic of relative gains can also have a powerful pull on the hegemon as it begins to weaken and rethink its originally magnanimous trade relations. As political scientist Duncan Snidal argued in a 1991 paper, When the global system is first set up, the hegemon makes deals with smaller states. The hegemon is concerned more with absolute gains, smaller states are more concerned with relative, so they are tougher negotiators. Cooperative arrangements favoring smaller states contribute to relative hegemonic decline. As the unequal distribution of benefits in favor of smaller states helps them catch up to the hegemonic actor, it also lowers the relative gains weight they place on the hegemonic actor. At the same time, declining relative preponderance increases the hegemonic state’s concern for relative gains with other states, especially any rising challengers. The net result is increasing pressure from the largest actor to change the prevailing system to gain a greater share of cooperative benefits.11 History teaches us that trade occurs even amongst rivals and during wartime. The reason small states are initially more concerned with relative gains is because they are far more concerned with national security than the hegemon. The hegemon has a preponderance of power and is therefore more relaxed about its security needs. This explains why Presidents George Bush Sr., Bill Clinton, and George Bush Jr. all made “bad deals” with China. Writing nearly thirty years ago, Snidal cogently described the current U.S.-China trade war. Snidal thought he was describing a coming decade of anarchy. But he and fellow political scientists writing in the early 1990s underestimated American power. The “unipolar moment” of American supremacy was not over, it was just beginning! As such, the dynamic Snidal described took thirty years to come to fruition. When thinking about the transition away from U.S. hegemony, most investors anchor themselves to the Cold War as it is the only world they have known that was not unipolar. Moreover the Cold War provides a simple, bipolar distribution of power that is easy to model through game theory. If this is the world we are about to inhabit, with the U.S. and China dividing the whole planet into spheres like the U.S. and Soviet Union, then the paragraph we lifted from Snidal’s paper would be the end of it. America would abandon globalization in totality, impose a draconian Silicon Curtain around China, and coerce its allies to follow suit. But most of recent human history has been defined by a multipolar distribution of power between states, not a bipolar one. The term “cold war” is applicable to the U.S. and China in the sense that comparable military power may prevent them from fighting a full-blown “hot war.” But ultimately the U.S.-Soviet Cold War is a poor analogy for today’s world. In a multipolar world, Snidal concludes, “states that do not cooperate fall behind other relative gains maximizers that cooperate among themselves. This makes cooperation the best defense (as well as the best offense) when your rivals are cooperating in a multilateral relative gains world.” Snidal shows via formal modeling that as the number of players increases from two, relative-gains sensitivity drops sharply.12 The U.S.-China relationship does not occur in a vacuum — it is moderated by the global context. Today’s global context is one of multipolarity. Multipolarity refers to the distribution of geopolitical power, which is no longer dominated by one or two great powers (Chart II-4). Europe and Japan, for instance, have formidable economies and military capabilities. Russia remains a potent military power, even as India surpasses it in terms of overall geopolitical power. Chart II-4The World Is No Longer Bipolar

The World Is No Longer Bipolar

The World Is No Longer Bipolar

A multipolar world is the least “ordered” and the most unstable of world systems (Chart II-5). This is for three reasons: Chart II-5Multipolarity Is Messy

Multipolarity Is Messy

Multipolarity Is Messy

Math: Multipolarity engenders more potential “conflict dyads” that can lead to conflict. In a unipolar world, there is only one country that determines norms and rules of behavior. Conflict is possible, but only if the hegemon wishes it. In a bipolar world, conflict is possible, but it must align along the axis of the two dominant powers. In a multipolar world, alliances are constantly shifting and producing novel conflict dyads. Lack of coordination: Global coordination suffers in periods of multipolarity as there are more “veto players.” This is particularly problematic during times of stress, such as when an aggressive revisionist power uses force or when the world is faced with an economic crisis. Charles Kindleberger has argued that it was exactly such hegemonic instability that caused the Great Depression to descend into the Second World War in his seminal The World In Depression.13 Mistakes: In a unipolar and bipolar world, there are a very limited number of dice being rolled at once. As such, the odds of tragic mistakes are low and can be mitigated with complex formal relationships (such as U.S.-Soviet Mutually Assured Destruction, grounded in formal modeling of game theory). But in a multipolar world, something as random as an assassination of a dignitary can set in motion a global war. The multipolar system is far more dynamic and thus unpredictable. Diagram II-2 is modified for a multipolar world. Everything is the same, except that we highlight the trade lost to other great powers. The state considering using tariffs to lower the marginal social cost of trading with a rival must account for this “lost trade.” In the context of today’s trade war with China, this would be the sum of all European Airbuses and Brazilian soybeans sold to China in the place of American exports. For China, it would be the sum of all the machinery, electronics, and capital goods produced in the rest of Asia and shipped to the United States. Diagram II-2Trade War In A Multipolar World

November 2019

November 2019