Europe

Highlights European and global growth will rebound in the fourth quarter but the rebound will lack longevity. Bonds: Expect bond yields to edge modestly higher, especially for those yields that are deeply in negative territory. Underweight German bunds in a European or global bond portfolio. Currencies: Zero/negative yielding currencies have the most to gain, and our preference remains the yen. Equities: a tug of war between growth and valuation will leave the broad equity market index in a sideways channel. But with the higher yield, prefer equities over bonds. Equity sectors: Non-China cyclical plays will outperform China plays. Continue to overweight banks versus resources and/or industrials. Equity regions: Continue to overweight the Eurostoxx 50 versus the Shanghai Composite and/or the Nikkei 225. Feature Comfort and discomfort are not absolute, they are relative. Put your hand in cold water, and whether it feels comfortable or uncomfortable depends on where your hand has come from. If your hand has come from room temperature, the cold water will feel uncomfortable. But if your hand has come from an ice bucket, the cold water will feel like bliss! The same principle applies to how we, and the financial markets, perceive short-term economic growth. After a strong expansion, a pedestrian growth rate of 1 percent feels uncomfortable. But after an economic contraction, 1 percent growth feels very pleasant. This leads to two important points: In the short term, the market is less concerned about the rate of growth per se, it is more concerned about whether the rate of growth is accelerating or decelerating. When it comes to the short term drivers of growth – bond yields, credit, and the oil price – we must focus not on their changes, we must focus on their impulses, meaning the changes in their changes. This is because it is the impulses of bond yields, credit, and the oil price that drive the accelerations and decelerations of economic growth, often with a useful lead time of a few months. The Chart of the Week combined with Chart I-1-Chart I-4 should leave you in no doubt. In the euro area, United States, and China, the domestic bond yield 6-month impulses have led their domestic 6-month credit impulses with near-perfect precision. Chart of the WeekCredit Growth To Rebound In The Fourth Quarter, Then Fade

Credit Growth To Rebound In The Fourth Quarter, Then Fade

Credit Growth To Rebound In The Fourth Quarter, Then Fade

Chart I-2The Euro Area Bond Yield Impulse Leads Its Credit Impulse

The Euro Area Bond Yield Impulse Leads Its Credit Impulse

The Euro Area Bond Yield Impulse Leads Its Credit Impulse

Chart I-3The U.S. Bond Yield Impulse Leads Its Credit Impulse

The U.S. Bond Yield Impulse Leads Its Credit Impulse

The U.S. Bond Yield Impulse Leads Its Credit Impulse

Chart I-4The China Bond Yield Impulse Leads Its Credit Impulse

The China Bond Yield Impulse Leads Its Credit Impulse

The China Bond Yield Impulse Leads Its Credit Impulse

Based on this near-perfect precision, the credit impulses in the euro area and the U.S. should briefly rebound in the fourth quarter. But expect much less of a rebound, if any, in China. While bond yields have collapsed in the euro area and the U.S., resulting in tailwind credit impulses, they have moved much less in China. Indeed, China’s bond yield 6-month impulse has been moving deeper into headwind territory in the past few months (Chart I-5). Chart I-5Bond Yield Impulses Were Tailwinds In The Euro Area And U.S., But Not In China

Bond Yield Impulses Were Tailwinds In The Euro Area And U.S., But Not In China

Bond Yield Impulses Were Tailwinds In The Euro Area And U.S., But Not In China

It follows that a credit growth rebound in the fourth quarter will be sourced in Europe and the U.S. rather than in China. From a tactical perspective, this will favour non-China cyclical plays over China plays. But moving into the early part of 2020, expect the credit impulses to fade across all the major economies – unless bond yields now fall very sharply everywhere. Investing On Impulse Many people still find it confusing that it is the impulses – and not the changes – of bond yields, credit, and the oil price that drive the accelerations and decelerations of economic growth. To resolve this confusion, let’s clarify the point. The credit impulses in the euro area and the U.S. should briefly rebound in the fourth quarter. A bond yield decline will trigger new borrowing. For example, a given decline in the U.S. bond yield, say 0.5 percent, will trigger a given increase in the number of mortgage applications (Chart I-6). New borrowing will add to demand, meaning it will generate growth. But in the following period, a further bond yield decline of 0.5 percent will generate the same further new borrowing and growth rate. The crucial point is that, if the decline in the bond yield is the same, growth will not accelerate. Chart I-6A Given Decline In The Bond Yield Triggers A Given Increase In New Borrowing

A Given Decline In The Bond Yield Triggers A Given Increase In New Borrowing

A Given Decline In The Bond Yield Triggers A Given Increase In New Borrowing

Growth will accelerate only if the first 0.5 percent bond yield decline is followed by a bigger, say 0.6 percent, decline – meaning a tailwind impulse. Conversely and counterintuitively, growth will decelerate if the first 0.5 percent decline is followed by a smaller, say 0.4 percent, decline – meaning a headwind impulse. Don’t Blame Autos For A German Recession Chart I-7German Car Production Rebounded In The Third Quarter

German Car Production Rebounded In The Third Quarter

German Car Production Rebounded In The Third Quarter

If the German economy contracts in the third quarter and thereby enters a technical recession, the knee-jerk response will be to blame the troubles in the auto industry. But the evidence does not support this story. German new car production rebounded in the third quarter (Chart I-7). Begging the question: if not autos, what is the true culprit for the deceleration? The likely answer is that Germany recently suffered a severe headwind from the oil price impulse. Germany has one of the world’s highest volumes of road traffic per unit of GDP, second only to the U.S. (Table I-1). A possible explanation for Germany’s high traffic intensity is that, just like the U.S., Germany is a decentralised economy with multiple ‘hubs and spokes’ requiring a lot of criss-crossing of traffic. But unlike the U.S., German transport is highly dependent on oil imports, which tend to be non-substitutable and highly inelastic to price. As the value of German oil imports rise in lockstep with the oil price, Germany’s net exports decline, weighing on growth. Table I-1Germany Has A Very High Road Traffic Intensity

Growth To Rebound In The Fourth Quarter, But Fade In 2020

Growth To Rebound In The Fourth Quarter, But Fade In 2020

The upshot is that the oil price impulse has a major bearing on Germany’s short term growth accelerations and decelerations. The six month period ending around June 2019 constituted a severe headwind impulse. This is because a 30 percent increase in the oil price in that period followed a 40 percent decline in the previous six month period, equating to a headwind impulse of 70 percent.1 Germany has one of the world’s highest volumes of road traffic per unit of GDP. Allowing for typical lags of a few months, this severe headwind impulse was a major contributor to Germany’s recent deceleration. Oscillations in the oil price’s 6-month impulse have explained the oscillations in Germany’s 6-month economic growth with a spooky accuracy (Chart I-8). The good news is that the oil price’s severe headwind impulse has eased – allowing a rebound in German economic growth during the fourth quarter. Chart I-8The Oil Price Impulse Explains Oscillations In German Growth

The Oil Price Impulse Explains Oscillations In German Growth

The Oil Price Impulse Explains Oscillations In German Growth

Nevertheless, a putative rebound could be nullified by a wildcard: the ‘geopolitical risk impulse’. To be clear this is not an impulse in the technical sense, but it is a similar concept: are the number of potential tail-events increasing or decreasing? For the fourth quarter, our subjective answer is they are decreasing. In Europe, the formation of a new coalition government in Italy has removed Italian politics as a possible tail-event for the time being. Meanwhile, we assume that the Benn-Burt law in the U.K. has been drafted well enough to eliminate a potential no-deal Brexit on October 31. Elsewhere, the U.S/China trade war and Middle East tensions are most likely to be in stasis through the fourth quarter. How To Position For The Fourth Quarter After a disappointing third quarter for global and European growth, we expect a rebound in the fourth quarter. But at the moment, we do not have any conviction that the rebound’s momentum will take it deeply into 2020. Position for the fourth quarter as follows: Expect a rebound in the fourth quarter. Bonds: Expect bond yields to edge modestly higher, especially for those yields that are deeply in negative territory. Underweight German bunds in a European or global bond portfolio. Currencies: Zero/negative yielding currencies have the most to gain, and our preference remains the yen. With a Brexit denouement, the pound could be the biggest mover and our inkling is to the upside. But we await more clarity before pulling the trigger. Equities: a tug of war between growth and valuation will leave the broad equity market index in the sideways range in which it has existed over the past two years (Chart I-9). But with a higher yield than bonds, equities are the preferred asset-class in the ugly contest. Equity sectors: Non-China cyclical plays will outperform China plays. Continue to overweight banks versus resources and/or industrials. Equity regions: Continue to overweight the Eurostoxx 50 versus the Shanghai Composite and/or the Nikkei 225 (Chart I-10). Chart I-9Global Equities Have Gone Nowhere For Two Years

Global Equities Have Gone Nowhere For Two Years

Global Equities Have Gone Nowhere For Two Years

Chart I-10Stay Overweight Europe ##br##Versus China

Stay Overweight Europe Versus China

Stay Overweight Europe Versus China

Fractal Trading System* The recent surge in the nickel price is due to scares about supply disruption, specifically an Indonesian export ban. However, the extent of the rally appears technically stretched. We would express this as a pair-trade versus gold: long gold / short nickel. Chart I-11Nickel VS. Gold

Nickel VS. Gold

Nickel VS. Gold

Set a profit target of 11 percent with a symmetrical stop-loss. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 The 6-month steps in the WTI crude oil price were $74.15, $45.21, and $58.24. The first change equated to a 40 percent decrease and the second change equated to a 30 percent increase. So the 6-month impulse was 70 percent. Fractal Trading Model Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights The global manufacturing cycle is likely to bottom soon, and consumption and services remain robust. The risk of recession over the next 12 months is low. This suggests that equities will continue to outperform bonds. But the risks to this optimistic scenario are rising. A denting of consumer confidence and worsening of geopolitical tensions could hurt risk assets. We hedge this by overweighting cash. China remains reluctant for now to use aggressive monetary easing. Until it does, the less cyclical U.S. equity market should outperform. We may shift into EM and European equities when China ramps up stimulus and the manufacturing cycle clearly bottoms. To hedge against this upside risk, we go tactically overweight Financials, and reiterate our overweight on Industrials and neutral on Australia. Bond yields should continue their rebound. We recommend an underweight on duration and favor TIPS. Credit should outperform on the cyclical horizon, but high corporate debt is a risk – we recommend a neutral position. Recommendations

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Feature Overview Hedges All Around This is a particularly uncertain time for the global economy – and so a tricky one for asset allocators. Will manufacturing activity bottom soon, or will it drag down the services sector and consumption with it? Will bond yields continue their strong rebound? Is the Fed done cutting rates? Will China now ramp up monetary stimulus? Will Iran escalate a confrontation with Saudi Arabia? What will President Trump tweet about next? This is the sort of environment in which portfolio construction comes into its own. We have our view on all these questions, but our level of conviction is somewhat lower than usual. The way for investors to react is to plan asset allocation in such a way that a portfolio is robust in all the most probable scenarios. We expect the global manufacturing cycle to bottom soon. The Global Leading Economic Indicator is already picking up, and the Global PMI shows some signs of bottoming (Chart 1). The shortest-term lead indicator, the Citigroup Economic Surprise Index, has recently jumped in every region except Europe (Chart 2). (See also What Our Clients Are Asking on page 7 for some more esoteric indicators of cycle bottoms.) The bottoming-out is due to easier financial conditions over the past nine months, a stabilization in Chinese growth, and simply time – the down-leg in manufacturing cycles typically last 18 months, and this one peaked in H1 2018. Chart 1First Signs Of Bottoming

First Signs Of Bottoming

First Signs Of Bottoming

Chart 2Surprisingly Strong Surprises

Surprisingly Strong Surprises

Surprisingly Strong Surprises

At the same time, government bond yields should have further to rise. The Fed may cut rates once more but, given the resilient U.S. economy, no more than that. This is less than the 59 basis points of cuts over the next 12 months priced in by the Fed Fund futures. The recent pick-up in economic surprises suggests that the 10-year U.S. Treasury yield should return at least to where it was six months ago, 2.3-2.4% (Chart 3). This might be delayed, however, if there is an increase in political tensions, for example a break-up of the U.S./China trade talks (Chart 4). Chart 3Long-Term Rates To Rebound Further...

Long-Term Rates To Rebound Further...

Long-Term Rates To Rebound Further...

Chart 4...But Geopolitical Tensions Remain A Risk

...But Geopolitical Tensions Remain A Risk

...But Geopolitical Tensions Remain A Risk

This implies that equities are likely to continue to outperform bonds over the next few quarters, and so we remain overweight global equities and underweight global bonds on the 12-month investment horizon. However, the risks to this rosy scenario are rising. We remain concerned about the inverted yield curve, which has accurately forecast every recession since World War II, usually about 18 months in advance (Chart 5). The 3-month/10-year curve inverted in the middle of this year. We also worry that the weakness in the manufacturing sector may dent consumer confidence. There are some signs of this in Europe and Japan – but none significant yet in the U.S. (Chart 6). Accordingly last month, as a hedge against an economic downturn, we went overweight cash, which we see as a more attractive hedge, from a risk/reward point-of-view, than bonds. Chart 5Can We Ignore The Message From The Yield Curve?

Can We Ignore The Message From The Yield Curve?

Can We Ignore The Message From The Yield Curve?

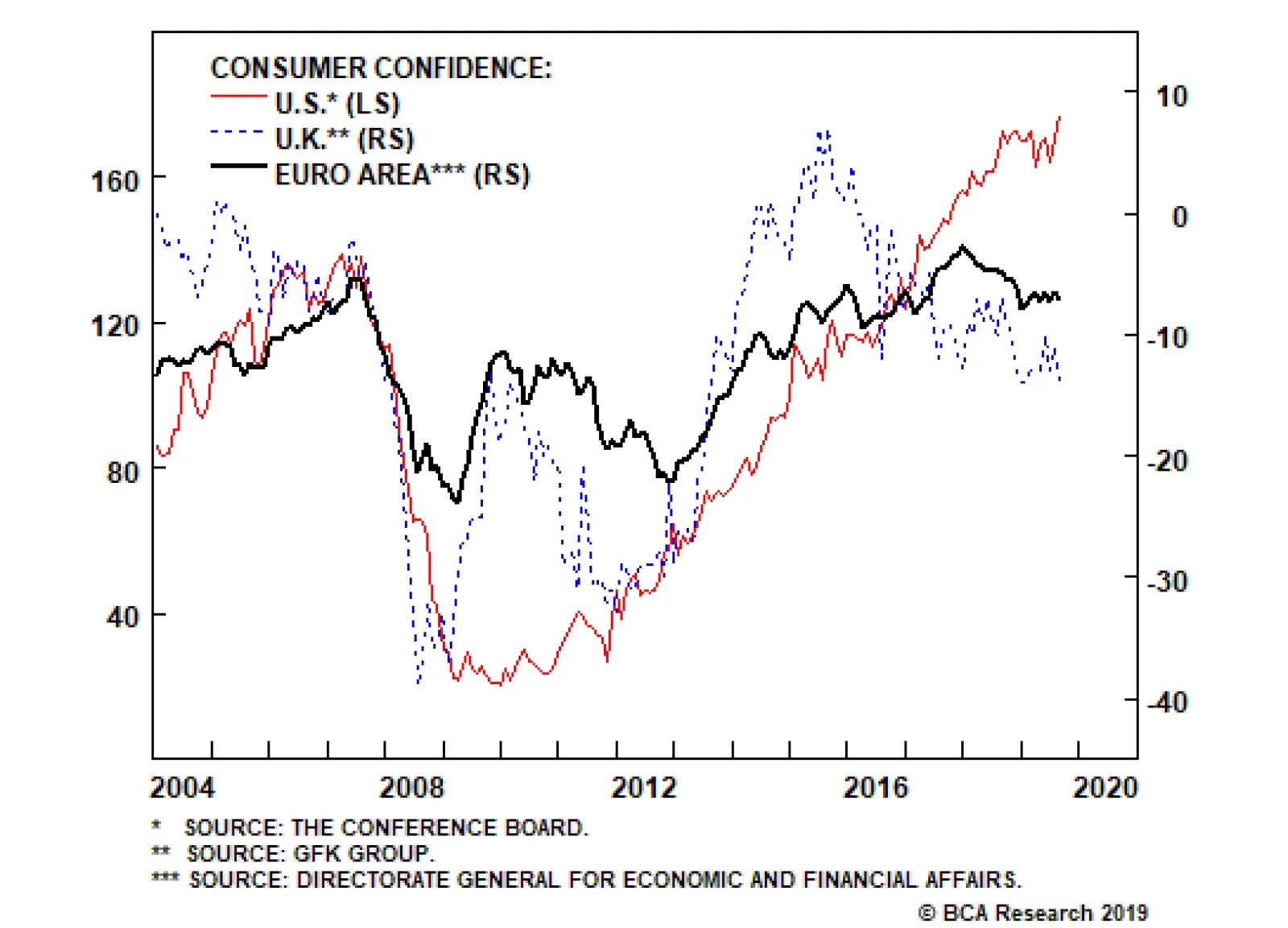

Chart 6Some Signs Of Weaker Consumer Confidence

Some Signs Of Weaker Consumer Confidence

Some Signs Of Weaker Consumer Confidence

We also remain overweight U.S. equities, which are lower-beta and have fewer structural headwinds than equities in other regions. However, we continue to look for an entry point into the more cyclical equity markets which would also be beneficiaries of bolder China stimulus. China’s monetary easing remains more tepid than in previous stimulus episodes. It has probably been enough to stabilize domestic activity (Chart 7) but not to trigger a rally in industrial commodity prices, EM assets, and euro area equities, as it did in 2016. A pick-up in global PMIs and signs of stronger Chinese credit growth would clearly help EM and Europe (Chart 8) but we need higher conviction that these things are indeed happening before making that move. In the meantime, we are hedging the upside risk by raising the global Financials sector tactically to overweight, since it would likely do well if euro area stocks started to outperform. Earlier this year, we raised the Industrials sector to overweight and Australian equities to neutral, also to hedge against the upside risk from more aggressive Chinese stimulus. Chart 7Chinese Stimulus Has Merely Stabilized Growth

Chinese Stimulus Has Merelyy Stabilized Growth

Chinese Stimulus Has Merelyy Stabilized Growth

Chart 8Europe And EM Are The Most Cyclical Markets

Europe And EM Are The Most Cyclical Markets

Europe And EM Are The Most Cyclical Markets

Chart 9Oil Price Spikes Often Precede Recessions

Oil Price Spikes Often Precede Recessions

Oil Price Spikes Often Precede Recessions

The biggest geopolitical risk to our sanguine scenario is the situation in the Middle East, after the attacks on Saudi oil refineries. Every recession in the past 50 years has been preceded by a 100% year-on-year spike in the crude oil price (though note that Brent would need to rise to over $100 a barrel by year-end, from $61 today, for that to eventuate (Chart 9)). A short-term oil shortage is not the problem since strategic reserves are ample. But the attack demonstrates the vulnerability of the Saudi installations. And a reprisal attack on Iran could lead it to block the Strait of Hormuz, through which more than 20% of global oil passes. We have an overweight on the Energy sector, partly as a hedge against these risks. BCA’s oil strategists expected Brent crude to rise to $70 this year, and average $74 in 2020, even before the recent attack. They argue that the risk premium in the oil price (the residual in Chart 10) is too low, given not only tensions with Iran, but also other potential supply disruptions in Iraq, Libya, Venezuela and elsewhere. Chart 10Is The Oil Risk Premium Too Low?

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking Which Leading Indicators Should Investors Watch To Time The Rebound In Global Growth? Chart 11Positive Signals For Global Growth

Is Eurozone Manufacturing Close To A Bottom? Positive Signals For Global Growth

Is Eurozone Manufacturing Close To A Bottom? Positive Signals For Global Growth

During 2019, the global growth decline was a key driver of the bond rally and the outperformance of defensive assets. Thus, timing when this decline will reverse will be crucial, since it would also result in a change of leadership from defensive to cyclical assets. But how can this be done? Below we list three of our favorite indicators that have provided reliable leading signals on the global economy in the past: Carry-trade performance: The performance of EM currencies with very high carry versus the yen tends to be a leading indicator for global growth (Chart 11, panel 1). In general, carry trades distribute liquidity from countries where funds are plentiful but rates of return are low (like Japan), to places with savings shortfalls and high risk, but where prospective returns are high. Positive performance of these currencies tends to signal a positive shift in global liquidity, which usually fuels global growth. Swedish inventory cycle: The Swedish new-orders-to-inventories ratio is a leading indicator of the global manufacturing cycle (panel 2). Why? Sweden is a small open economy that is very sensitive to global growth dynamics. Moreover, Swedish exports are weighted towards intermediate goods, which sit early in the global supply chain. This makes the Swedish inventory cycle a good early barometer of the health of the global manufacturing cycle. G3 monetary trends: G3 excess money supply – measured as the difference between money supply growth and loan growth – is a leading indicator of global industrial production (panel 3). As base money and deposits become more plentiful in the banking system relative to the pool of existing loans, the liquidity position of commercial banks improves. This provides banks with the necessary fuel to generate more loan growth, a development which eventually provides a boon to economic activity. Importantly, all these leading indicators are sending a positive signal on the global economy. This confirms our view that rates should go up as global growth strengthens. Therefore, investors should remain overweight equities and underweight bonds in their portfolios. Is It Time To Buy Euro Area Banks? In a Special Report on euro area banks in December 2018, we noted that “Historically, when the relative P/B discount hits the lower band and the relative dividend yield hits the upper band, a rebound in relative return performance could be expected”.1 Our recommendation back then was that “long-term investors should avoid banks in the region, but investors with a more tactical mandate and much nimbler style could use the valuation indicators to ‘time’ their entry into and exit out of banks as a short-term trade.” Since then, banks have continued to underperform the overall market by over 10%, further pushing down relative valuation metrics. Currently, both relative P/B and relative dividend yield are at extreme levels that have historically heralded at least a short-term bounce. The euro area PMI is still below 50, but there are signs that the euro area economy could rebound later this year, which should be positive for banks’ relative earnings. Already, forward EPS growth has been stabilizing relative to the broad market (Chart 12, panel 4). In addition, two of the key concerns back in December 2018 were Italian government debt and the unwinding of QE. Now Italian debt is no longer in crisis and the ECB has relaunched QE. As such, investors with a tactical mandate and a nimble style should buy (overweight) banks in the euro area. Long-term investors should still avoid such a short-term trade because structural issues remain. Chart 12Tactically Upgrade Euro Area Banks

Tactically Upgrade Euro Area Banks

Tactically Upgrade Euro Area Banks

Is The Gold Rally Over? Spot gold prices have increased 17% year-to-date, on the back of global growth weakness, dovish central banks, and rising political tensions. Should investors now pare back their gold exposure? Common sense would suggest they should. However, these are not ordinary times. In the short term, gold prices might suffer from some profit-taking due to overbought technicals and excessively positive sentiment (Chart 13, panel 1). Moreover, gold prices have moved this year due to increased market expectations of central bank easing (panel 2). We expect that markets will be disappointed going forward by only limited rate cuts, which could put downward pressure on gold. On the other hand, with approximately 27%, or $14.9 trillion, of global debt with negative yields at the moment, investors will continue to shift to the next best asset – zero-yielding gold (panel 3). This is clear from the rise in holdings of gold over the past few years by both central banks and investors (panels 4 & 5). We expect this trend to persist as investors continue their search to avoid negative yields and focus on capital preservation. Geopolitical tensions have intensified since the beginning of the year: ongoing yet inconclusive trade negotiations between the U.S. and China, implementation of further tariffs, Brexit uncertainty, and the recent military attacks in the Middle East (panel 6). This environment should also continue to push gold prices higher. We continue to recommend gold as a hedge against inflation – which we see picking up over the next 12 months – as well as against any further deterioration in global growth and the geopolitical situation. Chart 13Gold: Sell Or Hold?

Gold: Sell Or Hold?

Gold: Sell Or Hold?

Risks to the rosy scenario are rising. We remain concerned about the inverted yield curve, which has accurately forecast every recession since World War II. How Low Can Rates Go? The zero lower bound is a thing of the past. Last month, Denmark’s central bank cut rates to -0.75%, and 10-year government bonds in Switzerland hit a historic low for any major country, -1.12%. In the next recession, how much further could interest rates theoretically fall? For individuals, cash rates might be limited by the cost of storing paper currency, which has a zero yield (unless governments find a way to ban cash or charge an annual fee on it). A bank safety deposit box costs about $300 a year, and a professional-quality safe big enough to store $1 million (which would be a pile of $100 bills 31 x 55 cms, weighing 10 kg) costs $2,000 with installation costs. Amortize the latter over 10 years, and the cost of storing $1 million is about 0.2%-0.3% a year. Swiss franc bills – maximum denomination CHF1,000 – would cost less to store. But storage costs for physical gold are around 2% a year. Since rates have fallen below this, there must be other constraints. Individuals would find storing money in cash possibly dangerous and certainly very inconvenient (imagine having to transport the cash to a bank to pay a tax bill). And the cost for a rich individual or company of storing, say, $1 billion (weighing 10 tonnes) would be much higher. Given the history in even low-rate countries (Chart 14, panel 1), we suspect around -1% is the level at which cashholders would seek alternatives to bank deposits of government bills. Chart 14How Low Can They Go?

How Low Can They Go?

How Low Can They Go?

Chart 15Yield Curves When Rates Are At Zero Or Below

Yield Curves When Rates Are At Zero Or Below

Yield Curves When Rates Are At Zero Or Below

At the long end, the yield curve does not typically invert much when short-term rates are zero or negative (Chart 15). The biggest 3-month/10-year inversion was in Switzerland earlier this year, -0.05%. This points then to the absolute lowest level for 10-year bonds anywhere, even in the middle of a nasty recession, at around -1.1%. That is a worry for asset allocators. It means that the maximum mathematical upside for Swiss government bonds from their current level (-0.8%) is 3% while it is 5% for German bonds (currently -0.5%). This is not much of a hedge. Only the U.S. looks better: if the 10-year Treasury yield falls to 0%, the total return is 18%. Global Economy Chart 16U.S. Growth Remains Solid

U.S. Growth Remains Solid

U.S. Growth Remains Solid

Overview: Industrial-sector growth globally has been weak, with the manufacturing PMI in most countries falling below 50. But consumption and services almost everywhere have remained resilient, even in the manufacturing-heavy euro area. And there are tentative signs of a bottoming-out in manufacturing. However, a full-scale rebound will depend on further monetary stimulus in China, where the authorities still seem cautious about rolling out easing on the scale of what was done in 2016. U.S.: U.S. manufacturing has now followed the rest of the world into contraction, with the ISM manufacturing index slipping below 50 in August (Chart 16, panel 2). However, consumption and services are holding up well. Employment continues to expand (albeit at a slightly slower pace than last year, perhaps because of a lack of jobseekers), there is no sign of a rise in layoffs, and consumer confidence remains close to a historical high (though it slipped slightly in September). Housing has recovered after last year’s slowdown, and the recent congressional budgetary agreement means fiscal policy will be mildly expansionary over the coming 12 months. Only capex (panel 5) has slowed, as companies postpone investment decisions due to uncertainty surrounding the trade war. The consensus expects U.S. real GDP growth of 2.2% this year, above most estimates of trend growth. Euro Area: Given its higher concentration in manufacturing, European growth is weaker than in the U.S. The manufacturing PMI has been below 50 since February, and fell further to 45.6 in August. Industrial production is shrinking by 2% year-on-year. Italy has experienced two negative quarters of growth, and Germany may also enter a technical recession in Q3 (GDP shrank by 0.1% in Q2). However, there are some tentative signs that manufacturing is bottoming: the ZEW survey in September, for example, surprised on the upside. And, like the U.S., consumption remains strong. Even in manufacturing-heavy Germany, employment continues to grow, and retail sales in July were up 4.4% year-on-year. In the U.K., however, uncertainty surrounding Brexit has damaged business investment, though employment has been strong.2 Chart 17First Signs Of A Rebound In The Rest Of The World?

First Signs Of A Rebound In The Rest Of The World?

First Signs Of A Rebound In The Rest Of The World?

Japan: Consumption has already slipped, even before the consumption tax hike scheduled in October. Retail sales in July fell 2% year-on-year, due to negative wage growth and consumer sentiment falling to a five-year low. Manufacturing continues to suffer from China’s slowdown and the strong yen (up 6% over the past 12 months), with exports falling 6% and industrial production down 2% year-on-year over the past three months. The effect of the consumption tax hike may be cushioned by government measures (lowering taxes on autos and making high-school education free, for example). And a pickup in Chinese growth would boost exports. But there are scant signs yet of a bottoming in activity. Emerging Markets: China’s growth appears to have stabilized, with both manufacturing and non-manufacturing PMIs above 50 (Chart 17, panel 3). But confidence remains fragile, with retail sales growth slowing to a 20-year low and car sales down 7% in August, despite the introduction of cars compliant with new emissions standards. The authorities have responded with further easing measures (including a further cut in the reserve requirement in September) but seem reluctant to launch a full-scale monetary stimulus, similar to what they did in 2016. Elsewhere in EM, growth has slowed in countries with structural issues (latest year-on-year real GDP growth in Argentina is -5.7%, in Turkey -1.5% and in Mexico -0.8%) but remains fairly resilient elsewhere (India 5%, Indonesia 5%, Poland 4.2%, Colombia 3.4%). Interest Rates: Central banks almost everywhere have turned dovish, with the Fed cutting rates for a second time, the ECB restarting asset purchases, and the Bank of Japan signaling it will ease in October. But further monetary accommodation will probably be less than the market expects. The Fed signaled that its cuts were just a mid-cycle correction and that further easing is unlikely. And the ECB and BoJ have little ammunition left. With signs of growth bottoming, and the market understanding that central banks’ dovish turn is reaching its end, long-term rates, which have already risen in the U.S. from 1.45% to 1.72% in September, are likely to move higher. Investors should also carefully watch U.S. inflation, which is showing signs of underlying strength, with core CPI inflation rising 2.4% year-on-year in August (and as much as 3.4% annualized over the past three months). Global Equities Chart 18Has Earnings Growth Bottomed?

Has Earnings Growth Bottomed?

Has Earnings Growth Bottomed?

Still Cautious, But Adding An Upside Hedge: Global equities registered a small loss of 8 basis points in Q3 (Chart 18) despite all the headline risks from geopolitics and weakening economic data. Overall, our defensive country allocation worked well in Q3, since DM equities outperformed EM by 4.5%, and the U.S. outperformed the euro area by 2.8%. Our sector positioning did not do as well since underweights in Utilities and Consumer Staples and overweights in Industrials, Energy and Health Care all went in the wrong direction, even though the underweight in Materials did help to offset the loss. During the quarter, however, both sector and country rotations were evident within the global equity universe, in line with the wild swings in bond yields. September saw some reversals in DM/EM, U.S./euro area and cyclical/defensives. Going forward, BCA’s House View remains that global economic growth will begin to recover over the coming months, albeit a little later than we previously expected. As such, our defensive country allocation remains appropriate. We did put euro area and EM equities on upgrade watch in April,3 but the delay in the global recovery also implies that it is still not the time to trigger this call. With our view that bond yields have hit bottom,4 we are making one adjustment in our global sector allocation by upgrading Financials to overweight from neutral. We are financing this by cutting in half the double overweight in Health Care to overweight (see next page for more details). This adjustment also acts as a hedge against two possible outcomes: 1) that the euro area outperforms the U.S., and 2) that Elizabeth Warren wins in the upcoming U.S. presidential election.5 Upgrade Global Financials To Overweight From Neutral Chart 19Upgrade Global Financials

Upgrade Global Financials

Upgrade Global Financials

The relative performance of global Financials to the overall equity market has been hugely affected by the movements in global bond yields (Chart 19, panel 1). As bond yields made a sharp reversal in September, so did the relative performance of Financials, even though it is barely evident on the chart given how much Financials have underperformed the broad market over recent years. It’s not clear how sustainable the sharp reversal in bond yields will be, but BCA’s House View is that bond yields will move higher over the next 9-12 months. As such, we are upgrading Financials to overweight from neutral, for the following additional reasons: Valuations are extremely attractive as shown in panel 2. More importantly, the relative valuation is now at an extreme level that historically heralded a bounce in Financials’ relative performance. Loan quality has improved. The U.S. non-performing loan (NPL) ratio is nearing the lows reached before the Global Financial Crisis (GFC). Even in Spain and Italy, NPL ratios have fallen significantly, though they remain higher than they were prior to the GFC (panel 3). U.S. consumption has been strong, housing has rebounded, and demand for loans is getting stronger (panel 4), in line with data such as the Citi Economic Surprise Index, suggesting that economic data may have hit bottom. To finance this upgrade, we cut the double overweight of Health Care to overweight, as a hedge against Elizabeth Warren winning next year’s U.S. presidential election and tightening rules on drug pricing. Government Bonds Maintain Slight Underweight On Duration. Our below-benchmark duration call was severely challenged by the global bond markets in the first two months of the third quarter. The U.S. 10-year Treasury yield hit 1.43% on September 3 in response to the weaker-than-expected ISM manufacturing index in the U.S., 57 bps lower than the level at the end of previous quarter, and just a touch higher than the historical low of 1.32% reached on July 6, 2016. The rebound in bond yields since September 5, however, was driven not only by the ebb and flow in the U.S./China trade policy dynamics, but also by the positive surprises in economic data releases, as shown in Chart 20. BCA’s Global Duration Indicator, constructed by our Global Fixed Income Strategy team using various leading economic indicators, is also pointing to higher yields globally going forward. Investors should maintain a slight underweight on duration over the next 9-12 months. Favor Linkers Vs. Nominal Bonds. Global inflation expectations have also rebounded after continuing their downtrend in the first two months of the quarter. This largely reflects the acceleration in August in realized inflation measures such as core CPI, core PCE, and average hourly earnings. In addition, historically, the change in the crude oil price tends to have a good correlation with inflation expectations. The oil price jumped initially by 20% following the attack on the Saudi Arabian oil production facilities. While it’s not clear how the geopolitical tensions will evolve in the Middle East, a conservative assumption of a flat oil price until the end of the year still points to much higher inflation expectations, supporting our preference for inflation-linked bonds over nominal bonds. We also favor linkers in Japan and Australia over their respective nominal bonds (Chart 21). Chart 20Bond Yields Have Hit Bottom

Bond Yields Have Hit Bottom

Bond Yields Have Hit Bottom

Chart 21Favor Inflation Linkers

Favor Linkers

Favor Linkers

We continue to look for an entry point into more cyclical markets which would benefit from a bolder Chinese stimulus. Corporate Bonds Since we turned cyclically overweight on credit within a fixed-income portfolio, investment-grade bonds and high-yield bonds have produced 220 and 73 basis points, respectively, of excess return over duration-matched government bonds. We remain bullish on the outlook for credit over the next 12 months, as we expect global growth to accelerate before the end of the year. Historically, improving global growth has resulted in sustained outperformance of credit over government bonds. Moreover, default rates should remain subdued over the next year given that lending standards continue to ease (Chart 22, panel 1). How long will we remain overweight credit? High levels of leverage, declining interest coverage ratios, and the high share of Baa-rated debt in the U.S. corporate debt market continue to make credit a risky proposition on a structural basis. However, with inflation expectations still very low, the Fed has a strong incentive to keep monetary policy easy. This dovish monetary policy should keep interest costs at bay, helping credit outperform over the next year. That said, we believe that there are some credit categories that are more attractive than others. Specifically, we recommend investors favor Baa-rated and high yield securities, given that there is still room for further credit compression in these credit buckets (panel 2 and panel 3). On the other hand, investors should stay away from the highest credit categories, as they no longer offer value (panel 4). Chart 22Baa-rated And High-Yield Credit Offer The Most Value

Baa-rated And High-Yield Credit Offer The Most Value

Baa-rated And High-Yield Credit Offer The Most Value

Commodities Chart 23No Supply Shock In The Oil Market

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Energy (Overweight): September’s drone attack on Saudi crude facilities sent oil prices soaring as much as 20% in the days following, before falling back to pre-attack levels. Initial estimates estimated the supply disruption at 5.7 million barrels a day – approximately 5.5% of global supply – making it the largest crude supply outage in history. However, assuming the Saudis can return 70% of the lost output back online as they claim, OPEC’s spare capacity, approximately 1.8 million barrels a day, should be able to balance the market and cover the remaining lost production.6,7 In the longer-term, a pick-up in global oil demand, as economic growth rebounds, plus supply tightness should keep oil price elevated, with Brent reaching $70 this year and averaging $74 in 2020 (Chart 23, panels 1 & 2). Industrial Metals (Neutral): A combination of half-hearted year-to-date stimulus by Chinese authorities and a stronger USD in the second and third quarters of 2019 have driven industrial metals spot prices lower. However, the Chinese government announced additional stimulus in September, with further bond issuance to finance infrastructure projects and an easing of monetary policy (panel 3). This should give some upside for industrial metal prices over the coming six-to-12 months. Precious Metals (Neutral): We remain positive on gold, despite its strong performance year-to-date, since we see it as a good hedge against recession, inflation, and geopolitical risks. We discuss gold in detail in the What Our Clients Are Asking section on page 9. Silver also looks attractive in the short term. The nature of the use of silver has changed over the past two decades, from being mostly a base metal for industrial fabrication to becoming more of a precious metal viewed as a safe haven. The correlation between gold and silver prices has increased since the Global Financial Crisis from an average of 0.5 pre-crisis to 0.8 post-crisis (panels 4 & 5). Global growth and political uncertainty should support silver prices in the coming months. Currencies U.S. Dollar: The trade-weighted dollar has appreciated by 2.5% since we turned neutral in April. We expect that the steep drop in yields will continue to ease financial conditions and help global growth in the last quarter of the year. Given that the dollar is a counter-cyclical currency, an environment where global growth rallies have historically been negative for the greenback. Euro: Since we turned bullish in April, EUR/USD has depreciated by 2.7%. Overall, we continue to be positive on EUR/USD on a cyclical timeframe. After the ECB cut rates by 10 basis points and announced further rounds of quantitative easing, there is not much room left for the euro area to keep easing relative to the U.S. (Chart 24, panel 1). Moreover, improving expectations of profit growth in the euro area vis-à-vis the U.S. will drive money flows towards Europe, pushing EUR/USD up in the process (panel 2). Emerging Market Currencies: We remain bearish on emerging market currencies for the time being. That being said, they remain on upgrade watch for the end of the year. There are multiple signs that global growth is turning up, a consequence of the easy financial conditions caused by some of the lowest bond yields on record. Moreover, the marginal propensity to spend (proxied by M1 growth relative to M2 growth) in China, the main engine of EM growth, continues to point to further appreciation in emerging market currencies (panel 3). Chart 24Interest Rate And Profit Expectation Differentials Favor The Euro

The Euro Might Soon Pop Interest Rate And Profit Expectations Differentials Favor The Euro

The Euro Might Soon Pop Interest Rate And Profit Expectations Differentials Favor The Euro

Alternatives Chart 25Favor Hedge Funds Untill Global Growth Bottoms

Favor Hedge Funds Untill Global Growth Bottoms

Favor Hedge Funds Untill Global Growth Bottoms

Return Enhancers: Over the past 12 months, we have recommended investors pare back on private equity and increase allocations to hedge funds – macro hedge funds in particular. This was due to our judgement that we are late in the economic cycle. While we expect growth to pick up over the coming months, this is not yet clear in the data (Chart 25, panel 1). This uncertain macro outlook will prove tough for private equity funds, especially given an environment of rising multiples and increasing competition for deals. We continue to see global macro hedge funds as the best hedge ahead of the next recession and would advise investors to allocate funds now, given the time it takes to move allocations in the illiquid space. Inflation Hedges: In the current environment, TIPS are likely a better inflation hedge than illiquid alternative assets. Our May 2019 Special Report 8 showed that TIPS produce a particularly attractive risk-adjusted return during times when inflation is rising, but still fairly low (below 2.3%). TIPS should do well, therefore, in the environment we expect over the next few months, where the Fed remains dovish, cutting rates perhaps once more, while condoning a moderate acceleration of inflation (panel 2). Volatility Dampeners: Structured products – mostly Mortgage-Backed Securities (MBS) – have had an excellent record of reducing portfolio volatility (panel 3). Despite that, we do not recommend more than a neutral allocation to MBS currently due to a less-than-attractive valuation picture. Despite Treasury yields falling by more than 100 basis points this year and refinancing activity picking up, nominal MBS spreads remained near their all-time lows. However, as Treasury yields bottom, we expect refinancing to slow, putting downward pressure on spreads. Risks To Our View The most likely upside risk comes from the Fed being too dovish and falling behind the curve. Underlying inflation pressures in the U.S. remain strong (with core CPI up 3.4% annualized over the past three months). After two rate cuts, the Fed Funds rate is now comfortably below the neutral rate: 0.1% in real terms compared to a Laubach-Williams r* of 0.8% (Chart 26). Tightness in the money markets have pushed the Fed to start expanding its balance sheet again. If manufacturing growth accelerates next year, and wages and profits begin to rise, a stock market melt-up, similar to that in 1999, would be possible. Eventually, though, the Fed would need to raise rates (perhaps sharply) to kill inflation, which could usher in the next recession. There are a broader range of possible downside risks. As argued throughout this Quarterly, there are various possible triggers of recession: failure of China to stimulate, and a loss of confidence by consumers, in particular. Some models of recession put the risk over the next 12 months as high as 30% (Chart 27). Structurally, the biggest risk is probably the high level of corporate debt in the U.S. (Chart 28). A breakdown in the junk bond market, as seen briefly last December, could lead to companies failing to refinance the large amount of debt maturing over the next 18 months. Geopolitical risks also remain elevated and are, by nature, hard to forecast. The outcome of Brexit remains highly uncertain – though we see low risk of a no-deal exit. We expect trade talks between the U.S. and China to drag on, without a comprehensive deal, while a clear breakdown would be negative. Impeachment of President Trump is probably not a significant market event, but might hurt market sentiment briefly (particularly if it makes the election of Elizabeth Warren more likely). The Iran/Saudi conflict could escalate. Risk premiums may need to rise to take into account these threats. Chart 26Is The Fed Turning Too Dovish?

Is The Fed Turning Too Dovish?

Is The Fed Turning Too Dovish?

Chart 27What Risk Of Recession?

What Risk Of Recession?

What Risk Of Recession?

Chart 28Is Corporate Debt The Biggest Risk?

Is Corporate Debt The Biggest Risk?

Is Corporate Debt The Biggest Risk?

Footnotes 1Please see Global Asset Allocation Special Report, titled "Euro Area Banks: Value Play Or Value Trap?" dated December 14, 2018, available at gaa.bcaresearch.com. 2 Please see Foreign Exchange Strategy Special Report, “United Kingdom: Cyclical Slowdown Or Structural Malaise?”, dated 20 September 2019, available at fes.bcaresearch.com. 3Please see Global Asset Allocation Quarterly, titled "Quarterly - April 2019" dated April 1, 2019, available at gaa.bcaresearch.com. 4Please see Global Investment Strategy Weekly Report, titled "Bond Yields Have Hit Bottom," dated September 6, 2019, available at gis.bcaresearch.com. 5Please see Global Investment Strategy Weekly Report, titled "Elizabeth Warren And The Markets," dated September 13, 2019, available at gis.bcaresearch.com. 6Dmitry Zhdannikov and Alex Lawler “Exclusive: Saudi oil output to return faster than first thought - sources,” Reuters, dated Sepetmber 17, 2019. 7Please see Geopolitical Strategy Special Alert titled, “Attacks On Critical Infrastructure In KSA Raises Questions About U.S. Response,” dated September 16, 2019, available at gps.bcaresearch.com. 8Please see Global Asset Allocation Special Report, titled “Investors’ Guide To Inflation Hedging: How To Invest When Inflation Rises,” dated May 22, 2019, available at gaa.bcaresearch.com GAA Asset Allocation

The ECB’s tiering of reserves might prevent euro zone banks from teetering over the edge, but unless the manufacturing recession ends soon and firms start to borrow to invest, banks will continue to have a demand problem. Meanwhile, Norwegian bonds…

Sometimes, the best ideas are the simplest ones. The Norges bank is the most hawkish G-10 central bank, while the European Central Bank restarted QE at its latest meeting. This is a powerful catalyst for a short EUR/NOK trade. The Eurozone slowdown has been…

Highlights The world remains mired in a manufacturing recession. As such, it is still too early to put on fresh pro-cyclical trades. Focus on the crosses rather than outright U.S. dollar bets. Two new trade ideas: sell EUR/NOK and buy GBP/JPY. Also consider selling the gold/silver ratio. Feature Currency markets tend to trade into and out of various regimes. This means that to be an effective FX manager, you have to be extremely fluid. For example, interest rate differentials might dominate FX moves during a particular period, pivoting your job to a central bank monitor. Other times, flows dominate, perhaps even equity flows, like when a disruptive technology is developed in a specific market. The outperformance of U.S. equities, specifically technology stocks, is a case in point. Balance-of-payments dynamics usually matter mostly at critical turning points, making them not very useful as timing indicators. The exorbitant privilege of the U.S. dollar we discussed a fortnight ago is also a case in point. But more often than not, being able to identify whether the investment climate is about to become more hostile or not could be the key difference between being a successful FX manager or a relic. There has been no shortage of news for investors to digest over the last few days, from the Brexit imbroglio, to the Fed, to the drone attacks in Saudi Arabia and finally to U.S. President Donald Trump’s possible impeachment. But the most perplexing (and perhaps the most important) has been the German manufacturing flash PMI print for the month of September of 41.4, the lowest in over a decade (Chart I-1). If the country with the “cheapest currency” cannot manage to pull itself out of a manufacturing recession, then the message to the periphery is clearly that they have an impending problem. In short, our contention that the euro was close to a bottom might be offside by a few months, based on the latest manufacturing data release (Chart I-2). Chart I-1A Eurozone Manufacturing Recession

A Eurozone Manufacturing Recession

A Eurozone Manufacturing Recession

Chart I-2The Euro Needs Stronger Growth

The Euro Needs Stronger Growth

The Euro Needs Stronger Growth

Which FX Regime? Chart I-3A Recession Will Be Dollar Bullish

A Few Trade Ideas

A Few Trade Ideas

The performance of the dollar since the 10/2 yield curve inverted is instructive. So far, we are tracking both the 2005 and 1998 roadmaps, meaning the window for cautious optimism on risk assets could still pan out (Chart I-3). Specifically, the dollar tends to rally during recessions but the window before the dollar bull market takes hold can be quite long. In both 2006 and 1998, the dollar eventually catapulted higher, but it took longer than 12 months. Having an accurate recession probability-timing model is therefore crucial for strategy. Historically, domestic flows have been a very timely indicator, since repatriation by residents occurs during episodes of severe capital flight. In 2005, domestic individuals were deploying funds outside the U.S., which suggested patience before positioning for dollar strength. This made sense, since the return on capital was higher outside the U.S. with the EM and commodity bull market in full swing. More often than not, FX markets tend to favor regions with the highest return on capital. These tend to be the most difficult to bet against, but potentially the most potent blindside at turning points. If economic data continues to deteriorate due to much larger endogenous factors, a defensive strategy is clearly warranted. One way to tell will be an emerging divergence between our leading indicators and actual underlying data as is occurring so far in September. On the flip side, any specter of positive news could light a fire under sectors, currencies and countries that have borne the brunt of the slowdown. Both are highly risky bets. For now, we prefer to focus on the crosses rather than outright U.S. dollar bets. Sell EUR/NOK Sometimes, the best ideas are the simplest ones. The Norges bank is the most hawkish G-10 central bank, while the European Central Bank restarted QE at its latest meeting. This is a powerful catalyst for a short EUR/NOK trade: The dollar tends to rally during recessions but the window before the dollar bull market takes hold can be quite long. The slowdown in the euro zone has been concentrated in the manufacturing sector, but the deflationary impulse is starting to shift to other parts of the economy. Euro area overall core CPI continues to blast downwards, which has historically been a bad omen for the euro (Chart I-4). We expect euro zone inflation expectations to eventually rise, in part helped by the recovery in oil prices (Chart I-5), but this will also benefit the Norwegian krone. EUR/NOK has historically tracked the performance of relative stock prices between Europe and Norway, but a gaping wedge opened up in 2018 (Chart I-6). This divergence is unsustainable. In short, it is a bet on oil fields in Norway versus European banks. The ECB’s tiering of reserves might prevent euro zone banks from teetering over the edge, but unless the manufacturing recession ends soon and firms start to borrow to invest, banks will continue to have a demand problem. Meanwhile, the flareup in the Middle East means that oil prices will remain bid in the near term. This should favor Norwegian equities over those in the euro zone, and be negative for EUR/NOK (Chart I-7). 10-year German bunds are yielding -0.57% while the yield pickup on Norwegian bonds is a positive carry of 1.8%, despite liquidity concerns. In their latest policy meeting, Central Bank Governor Øystein Olsen stressed that Norway had much more fiscal room to maneuver in the event of a downturn, meaning the supply of Norwegian paper could increase, easing the liquidity premium. Chart I-4Deflation Remains Predominant In The Eurozone

Deflation Remains Predominant In The Eurozone

Deflation Remains Predominant In The Eurozone

Chart I-5A Rise In Oil Prices Will Help Inflation Expectations

A Rise In Oil Prices Will Help Inflation Expectations

A Rise In Oil Prices Will Help Inflation Expectations

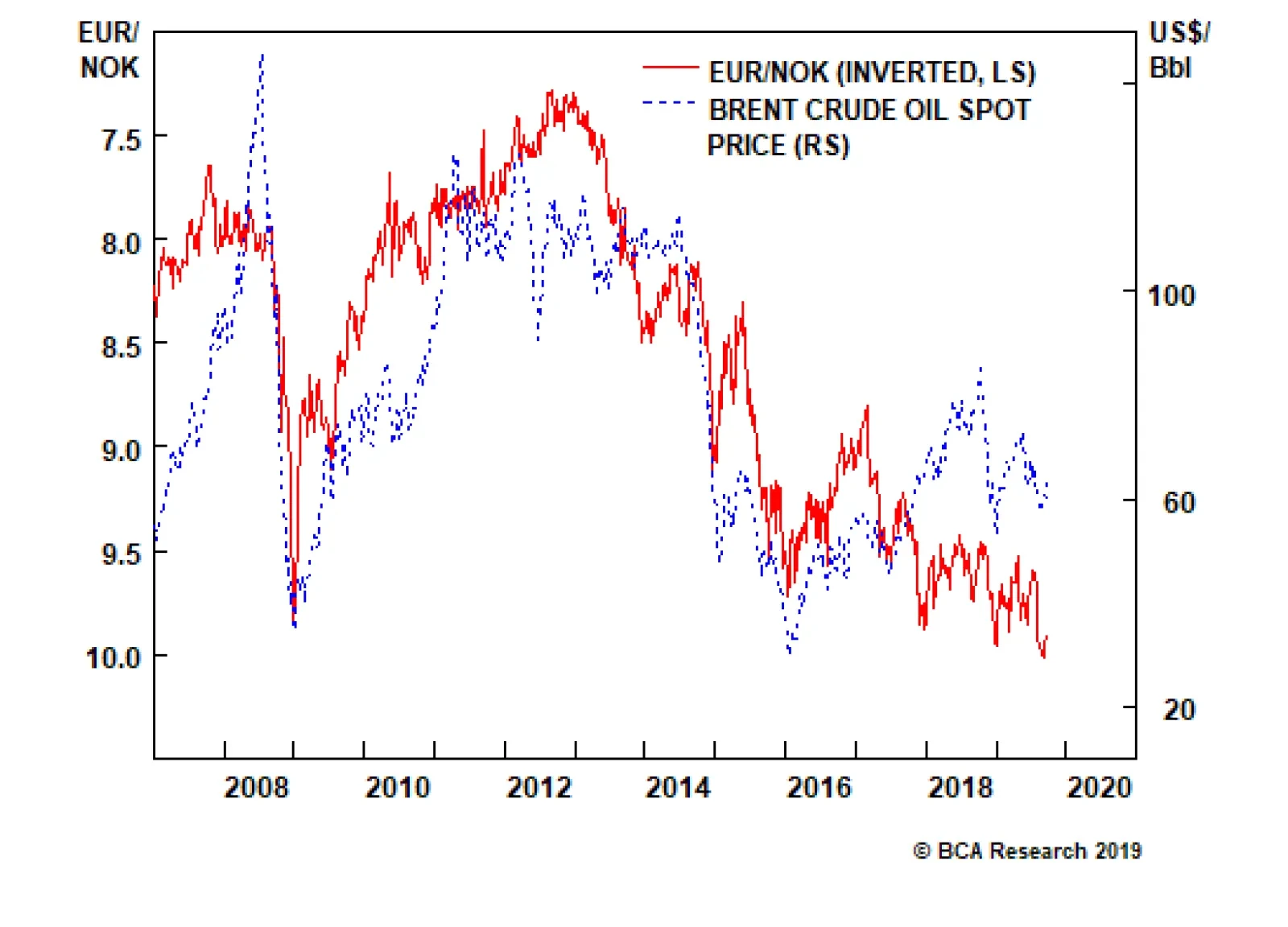

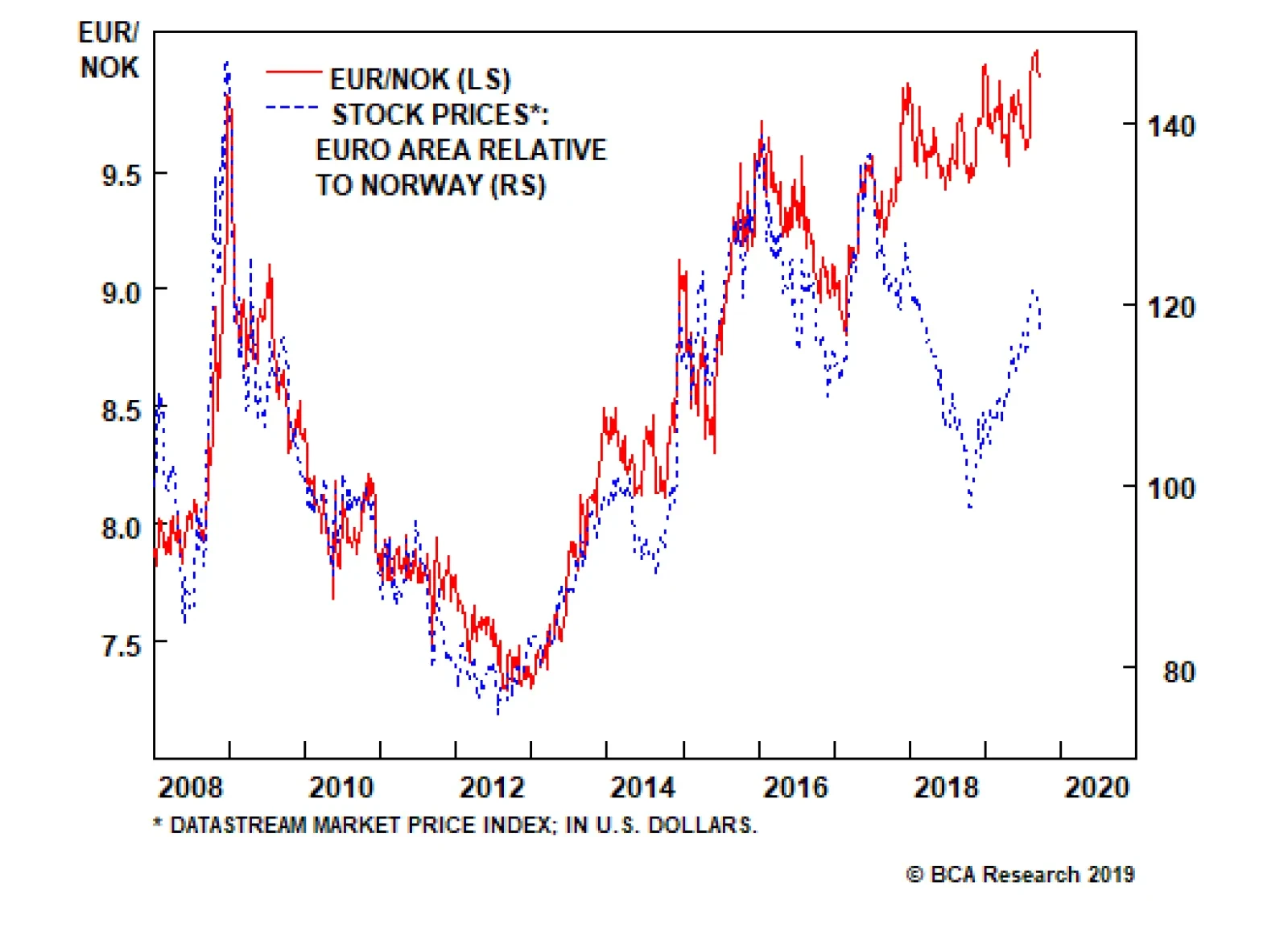

Chart I-6Stocks And Currencies: An Unsustainable Divergence

Stocks And Currencies: An Unsustainable Divergence

Stocks And Currencies: An Unsustainable Divergence

Chart I-7Higher Oil is Negative ##br##For EUR/NOK

Higher Oil is Negative For EUR/NOK

Higher Oil is Negative For EUR/NOK

Bottom Line: Sell EUR/NOK at 9.937. Buy GBP/JPY Last week’s Special Report made the case for a cyclical recovery in the U.K., even though structural factors remain a headwind. This week, we are re-attempting to buy cable versus the yen: Most importantly, the Bank of England stood pat at its latest policy meeting while the Bank of Japan is likely to introduce more stimulus or stronger guidance. Real interest rate differentials favor a stronger pound. Most importantly, the Bank of England stood pat at its latest policy meeting while the Bank of Japan is likely to introduce more stimulus or stronger guidance (Chart I-8). Chart i-8A Tactical Bounce In GBP/JPY Is Likely

A Tactical Bounce In GBP/JPY Is Likely

A Tactical Bounce In GBP/JPY Is Likely

Chart I-9The Benefit Of A Weaker Pound

The Benefit Of A Weaker Pound

The Benefit Of A Weaker Pound

Speculators are very short the pound while they have been covering their short bets on the yen, as the investment environment has become more uncertain. The fall in the pound should begin to improve the U.K.’s balance-of-payment dynamics relative to Japan (Chart I-9). Bottom Line: Buy GBP/JPY at 132.6. Concluding Thoughts We continue to track various indicators for the dollar, from interest rate differentials, balance-of-payment dynamics, valuations, portfolio flows and positioning – and none of them are sending a bullish signal at the moment. Global growth remains in a funk, which has been supercharging dollar bulls. However, long-dollar bets remain susceptible should global growth stabilize. Our strategy is to continue focusing on the crosses until categorical evidence emerges that global growth has bottomed. In our trading portfolio, we continue to favor the NOK, SEK, petrocurrencies and the AUD. So far, these trades have been implemented at the crosses to limit downside risk, should our view on the dollar be offside. We intend to eventually start placing outright dollar bets once evidence emerges that global growth has bottomed and the world has skidded a recession. Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. have been relatively strong: The Markit flash manufacturing PMI rebounded to 51 in September from 50.3. Flash services PMI increased to 50.9. The Chicago Fed national activity index increased to 0.1 from -0.4 in August. The Richmond Fed manufacturing index fell to -9 in September from 1. The Conference Board consumer confidence fell to 125.1 in September from 135.1. On the housing front, home prices grew by 0.4% month-on-month in July. Mortgage applications decreased by 10% for the week ended September 20th, but new home sales increased by 7% month-on-month in August. Initial jobless claims increased to 213,000 for the week ended September 20th. Annualized GDP growth was unchanged at 2% quarter-on-quarter in Q2. Trade deficit of goods was little changed at $72.8 billion. Headline and core PCE increased to 2.4% and 1.9% quarter-on-quarter, respectively in Q2. The DXY index appreciated by 0.6% this week. The recent data from the U.S. have been holding up quite well compared with the rest of the world. Net speculative positions on the greenback remain elevated due to U.S. relative strength. While we see dollar resilience in the near term, declining net foreign purchases of U.S. securities, diminishing interest rate differentials and the plunging bond-to-gold ratio all suggest the path of least resistance for the dollar is down. Report Links: Preserving Capital During Riot Points - September 6, 2019 Has The Currency Landscape Shifted? - August 16, 2019 USD/CNY And Market Turbulence - August 9, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area continue to deteriorate: The Markit flash manufacturing and services PMIs for the euro area both fell to 45.6 and 52, respectively in September. In France, the Markit flash manufacturing PMI fell to 50.3; services PMI decreased to 51.6. In Germany, the manufacturing PMI collapsed to 41.4; services PMI fell to 52.5. German IFO current assessment increased to 98.5 in September. However, the IFO expectations fell to 90.8. Monetary supply (M3) grew by 5.7% year-on-year in August. German Gfk consumer confidence nudged up to 9.9 in October. The EUR/USD fell by 0.8% this week. The recent data from the euro area has unfortunately showed no signs of global growth bottoming. The manufacturing PMI in Germany is now at its lowest level since the Great Financial Crisis. A major concern faced by investors is that weak activity in manufacturing may have already begun to infiltrate the service sectors. That said, the services PMIs in major economies, though falling, still remain in expansionary territory above 50. Report Links: Battle Of The Central Banks - June 21, 2019 EUR/USD And The Neutral Rate Of Interest - June 14, 2019 Take Out Some Insurance - May 3, 2019 Japense Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been negative: National headline inflation fell from 0.5% year-on-year to 0.3% year-on-year in August. Core inflation was unchanged at 0.6% year-on-year. The Markit flash manufacturing PMI fell to 48.9 in September from 49.3. Services PMI also fell to 52.8 from 53.3. The leading index and coincident index were both little changed at 93.7 and 99.7, respectively, in July. The USD/JPY has been flat this week. Japanese exports have been weak, weighed by the global trade war and manufacturing slowdown. However, accordingly to the BoJ, domestic demand has remained firm, and capex also continues to increase. Moreover, the consumption tax hike next month will probably have a marginal impact compared with previous tax hikes. In a speech this week, BoJ Governor Haruhiko Kuroda emphasized that the central bank will ease without hesitation if the economy loses momentum. Report Links: Has The Currency Landscape Shifted? - August 16, 2019 Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 Battle Of The Central Banks - June 21, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

There is little data from the U.K. this week: Mortgage approvals decreased slightly to 42,576 in August from 43,303 in July. The GBP/USD fell by 1.4% this week. British Prime Minister Boris Johnson has now lost his majority in Westminster after large profile defections from the so-called rebels, thus another election is highly likely by year-end. Besides, a further delay of Brexit is almost certain. We have downgraded the probability for a no-deal Brexit. We remain positive on the pound and are buying GBP/JPY this week. Report Links: United Kingdon: Cyclical Slowdown Or Structural Malaise? - September 20, 2019 Battle Of The Central Banks - June 21, 2019 A Contrarian View On The Australian Dollar - May 24, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been mixed: The preliminary commonwealth manufacturing PMI fell to 49.4 in September from 50.9 in August. On the other hand, the services PMI rebounded to 52.5 from 49.1, back to above-50 expansionary territory. Consumer confidence increased to 110.1 from 109.3 this week. The AUD/USD fell by 1% this week. Reserve Bank of Australia Governor Philip Lowe commented on Tuesday that the Australian economy is picking up, and is now at a “gentle turning point.” The previous rate cuts have allowed the property markets in big cities like Sydney and Melbourne to regain some strength, but will likely take longer to flow through the whole economy. In terms of monetary policy, Governor Lowe reiterated his commitment to ease monetary conditions when needed, though he did not signal an imminent move for next week. Australia has a large beta to global shifts as a small, open economy. Should the global manufacturing recession come to an end, the positive fundamentals will continue to lift the Australian economy through the rest of the year and into 2020. Report Links: A Contrarian View On The Australian Dollar - May 24, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been negative: Imports increased by NZ$30 million to NZ$5.69 billion in August, while exports fell by NZ$830 million to NZ$4.13 billion. The total trade deficit widened from NZ$700 million to NZ$1.57 billion. The NZD/USD appreciated by 1% initially, then plunged after the Reserve Bank of New Zealand’s policy meeting, returning flat this week. As widely expected, the RBNZ kept its official cash rate unchanged at 1% this Wednesday while signaling that there is more scope to ease if necessary amid a global slowdown. The market is currently pricing an 80% probability of a rate cut for the next policy meeting in November, reflecting weak business confidence. We are playing the kiwi weakness through the Australian dollar and Swedish krona, which are 1.9% and 1.95% in the money, respectively. Report Links: USD/CNY And Market Turbulence - August 9, 2019 Where To Next For The U.S. Dollar? - June 7, 2019 Not Out Of The Woods Yet - April 5, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been resilient: Bloomberg Nanos confidence increased to 57.4 this week from 56.7. Retail sales increased by 0.4% month-on-month in July, lower than the expectations of a 0.6% monthly growth. The USD/CAD has been flat this week. Oil prices have been on a wild ride this year. Since the drone attack a fortnight ago, Saudi Arabia has claimed that it is recovering faster than expected, beating its own targets. Brent crude oil spot prices have fallen by 6% from their September 16th peak, while Western Canada Select (WCS) oil prices have dropped by 12.3%, dampening the loonie’s upside potential. Report Links: Preserving Capital During Riot Points - September 6, 2019 Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 On Gold, Oil And Cryptocurrencies - June 28, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been mostly negative: The trade balance narrowed to CHF 1.2 billion in August from CHF 2.6 billion in July. Credit Suisse survey expectations came in at -15.4 in September, up from the last reading of -37.5 in August. The USD/CHF has been flat this week. As a small, open economy, Switzerland belongs to those countries with highest foreign trade-to-GDP share. The trade balance in August has been the lowest since January 2018, with lower exports of main goods including chemical and pharmaceutical products. Among trading partners, exports to Germany, Italy, and France all declined, reflecting the recent manufacturing slowdown in Europe. That said, we remain positive on the safe-haven Swiss franc during the risk-off period amid trade war uncertainties, Brexit chaos, Middle-East tensions, and more recently, the Trump Impeachment imbroglio. Report Links: What To Do About The Swiss Franc? - May 17, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Balance Of Payments Across The G10 - February 15, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

There is scant data from Norway this week: The unemployment rate increased to 3.8% in July, 0.6 percentage points higher than in April, accordingly to the recent Labour Force Survey. The USD/NOK appreciated by 0.5% this week. The Norges Bank, the one and only hawkish central bank among the G-10, raised its interest rate by 25 basis points to 1.5% last week. Since last September, the Norges Bank has hiked rates four times in total, resulting in a one-percentage-point increase in rates. The central bank stated that “the Norwegian economy has been solid; Employment has risen; Capacity utilization appears to be somewhat above a normal level; Inflation is close to target.” A higher interest rate would also help take the wind out of skyrocketing house prices and household debt levels. In addition, the central bank lowered its projection path for the krone, stating that the factors it outlined, including weaker activity in the petroleum sector, would probably keep weighing on the krone in the years ahead. Report Links: Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 On Gold, Oil And Cryptocurrencies - June 28, 2019 Currency Complacency Amid A Global Dovish Shift - April 26, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been negative: Consumer confidence fell to 90.6 in September. PPI yearly growth fell from 2% in July to 1.4% in August. Trade balance shifted to a deficit of SEK 5.4 billion in August. USD/SEK has been flat this week. We are closely monitoring the Swedish foreign trade as a leading indicator for global growth. The Swedish trade balance has shifted to a deficit for the first time this year. However, compared to last August, the deficit was narrowed by SEK 2.6 billion. Year to date, the Swedish trade surplus amounted to SEK 27 billion. Notably, the trade in goods with non-EU countries resulted in a surplus of SEK 6.6 billion, while the trade with EU resulted in a deficit of SEK 12 billion. Report Links: Where To Next For The U.S. Dollar? - June 7, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights President Trump’s support among Republicans and lack of smoking gun evidence will prevent his removal from office. Trade risk will increase if Trump’s approval benefits from impeachment proceedings and the U.S. economy is resilient. Political risk on the European mainland is falling. However, watch out for Russia and Turkey, and short 10-year versus 2-year gilts. A new election in Spain may not resolve the political deadlock. Book gains on our Hong Kong Hang Seng short. Feature Impeachment proceedings against U.S. President Donald Trump, the brazen Iranian attack on Saudi Arabia, the persistence of trade war risk, and additional weak data from China and Europe all suggest that investors should remain risk averse for now. Specifically, Trump’s impeachment could drive him to seek distractions abroad – abandoning the tactical retreat from aggressive foreign and trade policy that had only just begun. Geopolitical risk outside of the hot spots is falling, especially in Europe. The risk of a no-deal Brexit has collapsed in line with our expectations. Italy and Germany have pleased markets by providing some fiscal stimulus sans populism. In France, President Emmanuel Macron’s popularity is recovering. And – as we discuss in this report – Spain’s election will not add any significant fear factor. In what follows we introduce a new GeoRisk Indicator, review the signal from all of our indicators over the past month, and then focus on Spain. Fear U.S. Politics, Not Impeachment The House Democrats’ decision to impeach Trump gives investors another reason to remain cautious on risk assets. Why not be bullish? It is true that impeachment without smoking gun evidence increases Trump’s chances of reelection, which is market positive relative to a Democratic victory. President Trump is virtually invulnerable to Democratic impeachment measures as long as Republicans continue to support him at a 91% rate (Chart 1). Senators will not defect in these circumstances, so Trump will not be removed from office. Trump is invulnerable to impeachment measures as long as GOP support remains high. Moreover the transcript of his phone conversation with Ukrainian President Volodymyr Zelenskiy did not produce a bombshell: there is no explicit quid pro quo in which President Trump suggests he will withhold military aid to Ukraine in exchange for an investigation into former Vice President Joe Biden’s and his son Hunter’s doings involving Ukraine. Any wrongdoing is therefore debatable, pending further evidence. This includes evidence beyond the “whistleblower’s complaint,” which suggests that the Trump team attempted to stifle the transcript of the aforementioned phone call. The point is that the grassroots GOP and Senate are the final arbiters of the debate. The problem is that scandal and impeachment will still likely feed equity market volatility (Chart 2). The House Democrats could turn up new evidence now that they are fully focused on impeachment and hearing from whistleblowers in the intelligence community. Chart 1GOP Not Yet Willing To Impeach Trump

Impeachment, Trade War, And A Sojourn To Spain – GeoRisk Update: September 27, 2019

Impeachment, Trade War, And A Sojourn To Spain – GeoRisk Update: September 27, 2019

Impeachment also has a negative market impact via the Democratic Party’s primary election. Elizabeth Warren has not dislodged Biden in the early Democratic Primary yet. Chart 2Impeachment Proceedings Likely To Raise Vol

Impeachment Proceedings Likely To Raise Vol

Impeachment Proceedings Likely To Raise Vol

If she does, it will have a sizable negative impact on equity markets, as President Trump will still be only slightly favored to win reelection. Under any circumstances, this election will be extremely close, it has significant implications for fiscal policy and regulation, and therefore it will create a lot of uncertainty between now and November 2020. The whistleblower episode has if anything aggravated this uncertainty. As mentioned at the top of the report, if impeachment proceedings ever gain any traction they could drive Trump to seek distractions abroad – abandoning the tactical retreat from aggressive foreign and trade policy that had only just begun. Finally, Trump’s reelection, while more market-friendly than the alternative and likely to trigger a relief rally, is not as bullish as meets the eye. Trump’s policies in the second term will not be as favorable to corporates as in the first term. Unshackled by electoral concerns yet still facing a Democratic House, Trump will not be able to cut taxes but he will be likely to conduct his foreign and trade policy even more aggressively. This is not a market-positive outlook, regardless of whether it is beneficial to U.S. interests over the long run. Bottom Line: President Trump’s approval among Republican voters is the critical data point. Unless they abandon faith, the senate will not turn, and Trump’s support may even go up. But this is not a reason to turn bullish. The coming year will inevitably see a horror show of American political dysfunction that will lead to volatility and potentially escalating conflicts abroad. Introducing … Our Sino-American Trade Risk Indicator This week we introduce a new GeoRisk Indicator for the U.S.-China trade war (Chart 3). The indicator is based on the outperformance of overall developed market equities relative to those same equities that have high exposure to China, and on China’s private credit growth (“total social financing”). As our chart commentary shows, the indicator corresponds with the course of events throughout the trade war. It also correlates fairly well with alternative measures of trade risk, such as the count of key terms in news reports. Chart 3Trade Risk Will Go Up From Here

Impeachment, Trade War, And A Sojourn To Spain – GeoRisk Update: September 27, 2019

Impeachment, Trade War, And A Sojourn To Spain – GeoRisk Update: September 27, 2019