Fixed Income

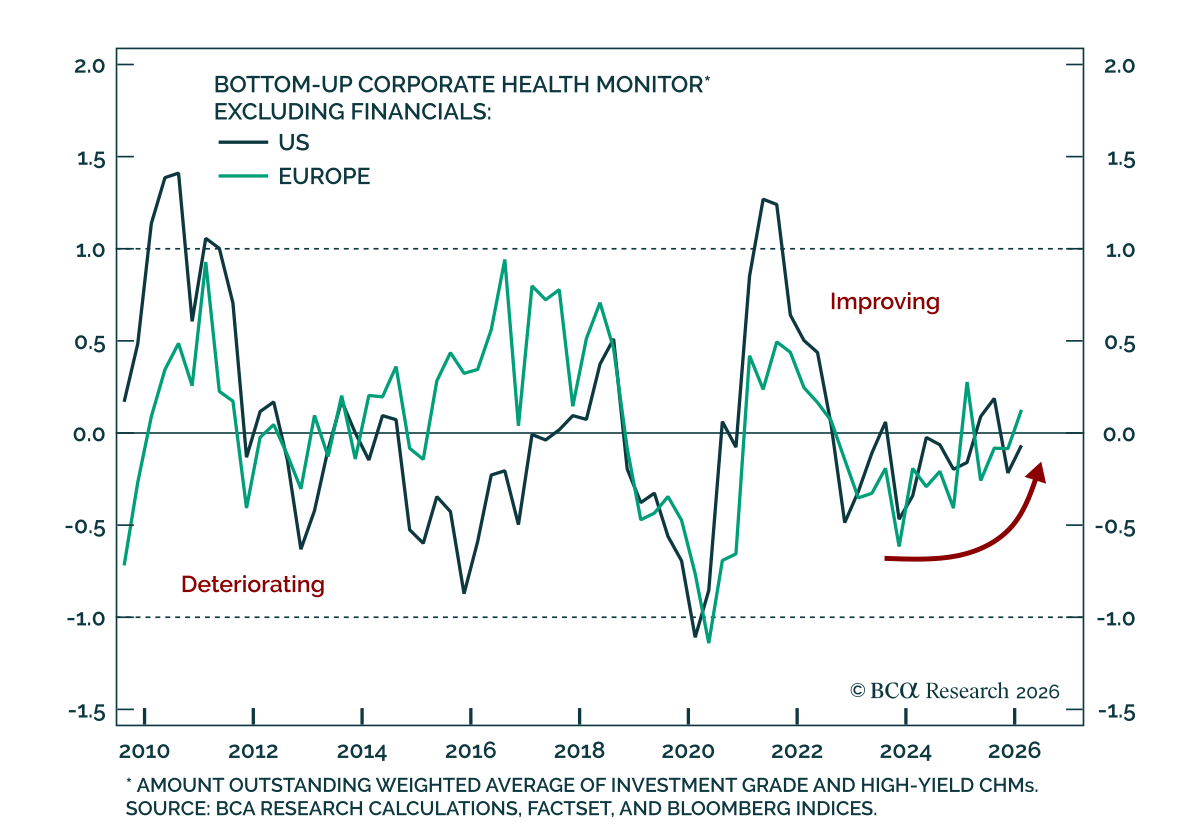

Our Global Fixed Income and European strategists find that improving corporate fundamentals continue to support tight credit spreads. However, a growing divide between stronger and weaker borrowers is emerging. Our Corporate Health Monitors show that balance…

We react to DM central bank meetings this week and highlight the opportunities emerging across global fixed income and currency markets.

Kevin Warsh announced an ambitious reform agenda for the Federal Reserve. We discuss the potential impact and the current outlook for interest rates.

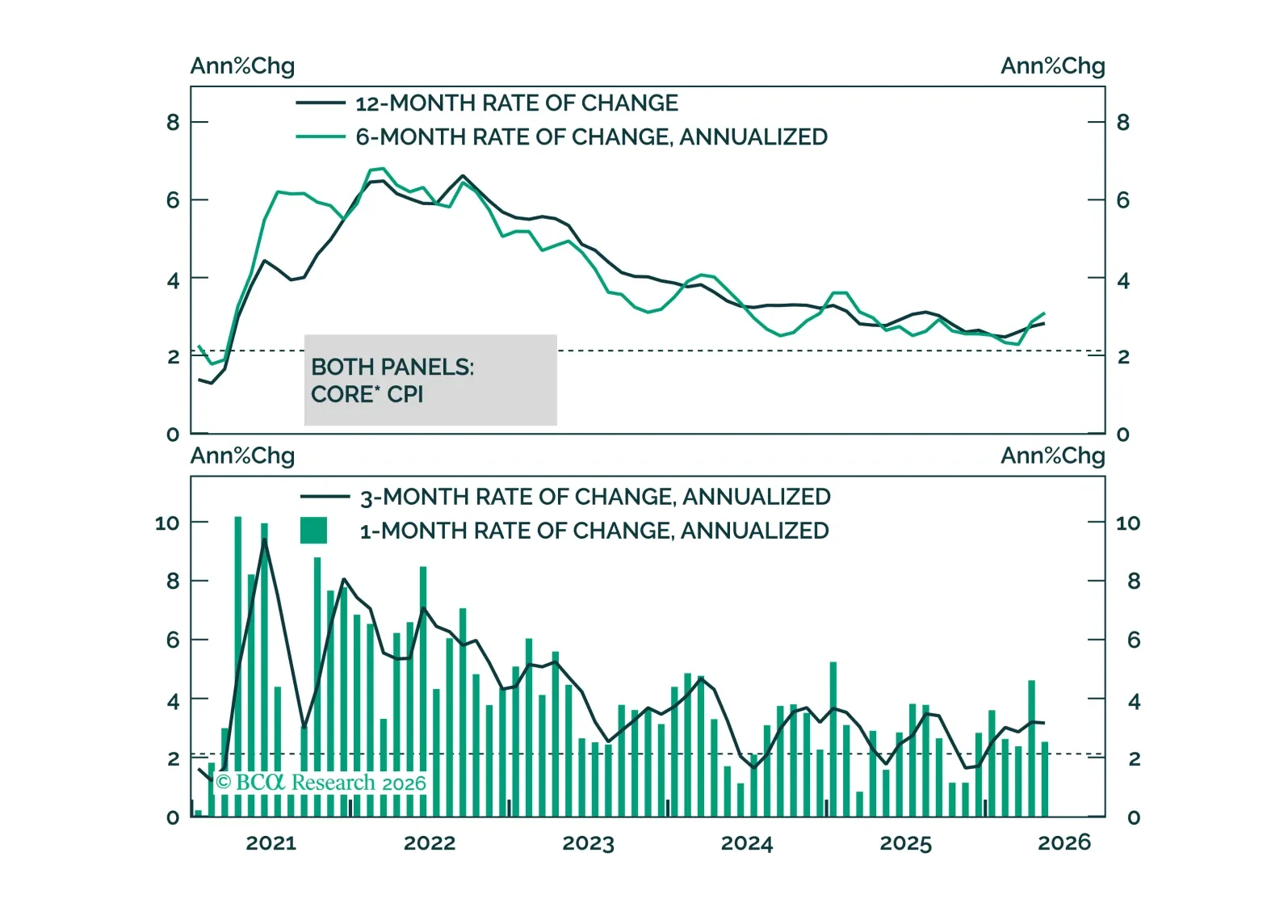

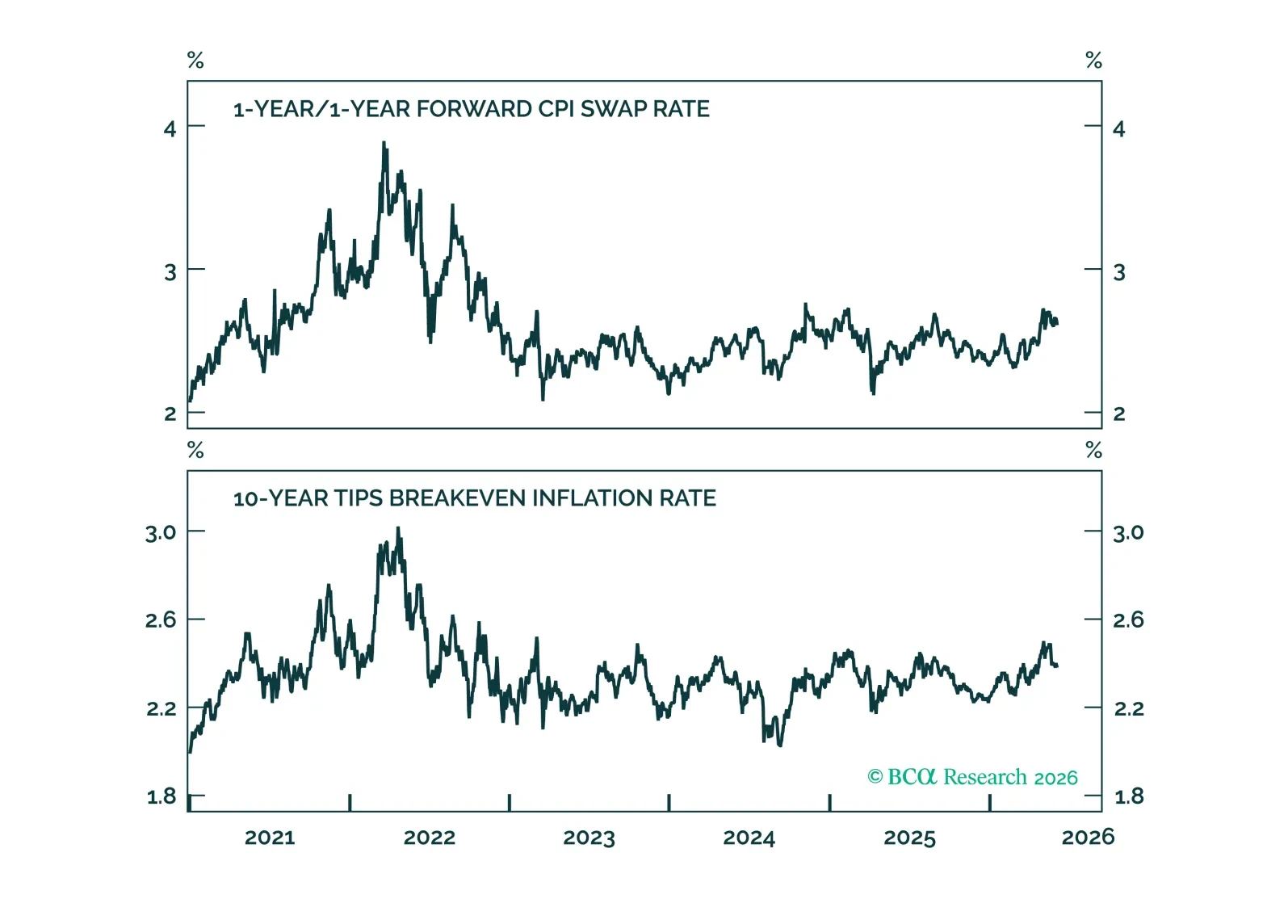

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

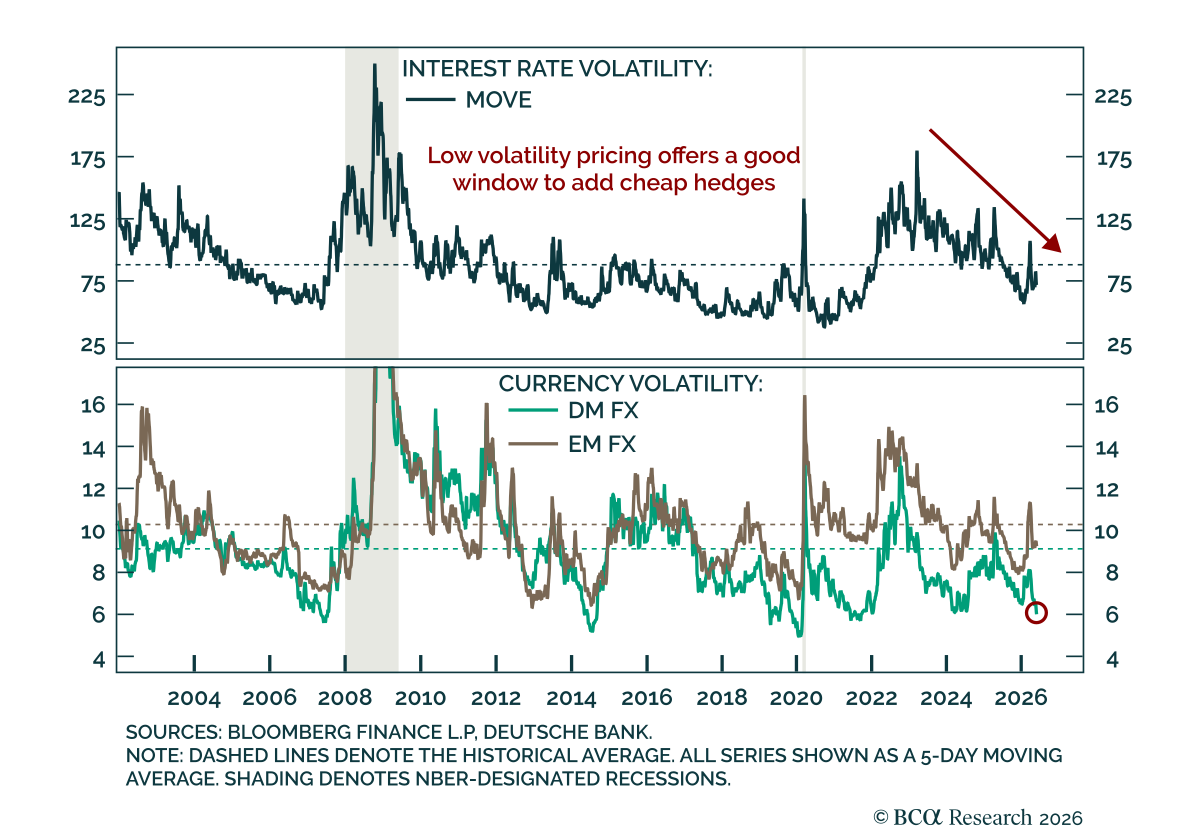

The collapse in FX volatility reinforces broader market optimism and repricing of tail risks, while cheap volatility pricing offers investors a good window of opportunity to add hedges. DM FX implied volatility has continued to drop precipitously despite…

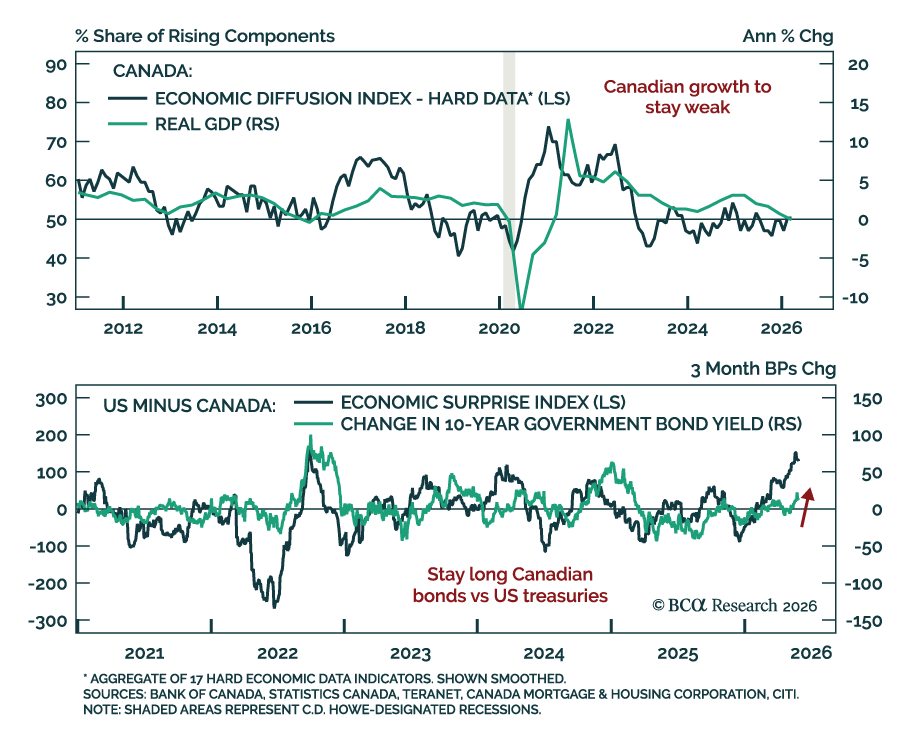

Canada’s growth backdrop has weakened sharply. Q1 GDP fell 0.1% on a quarterly annualized basis, missing expectations for 1.5% growth, after Q4 was revised down to a 1% contraction. The drag is broadening. Business capital investment fell 0.7% q/q, its…

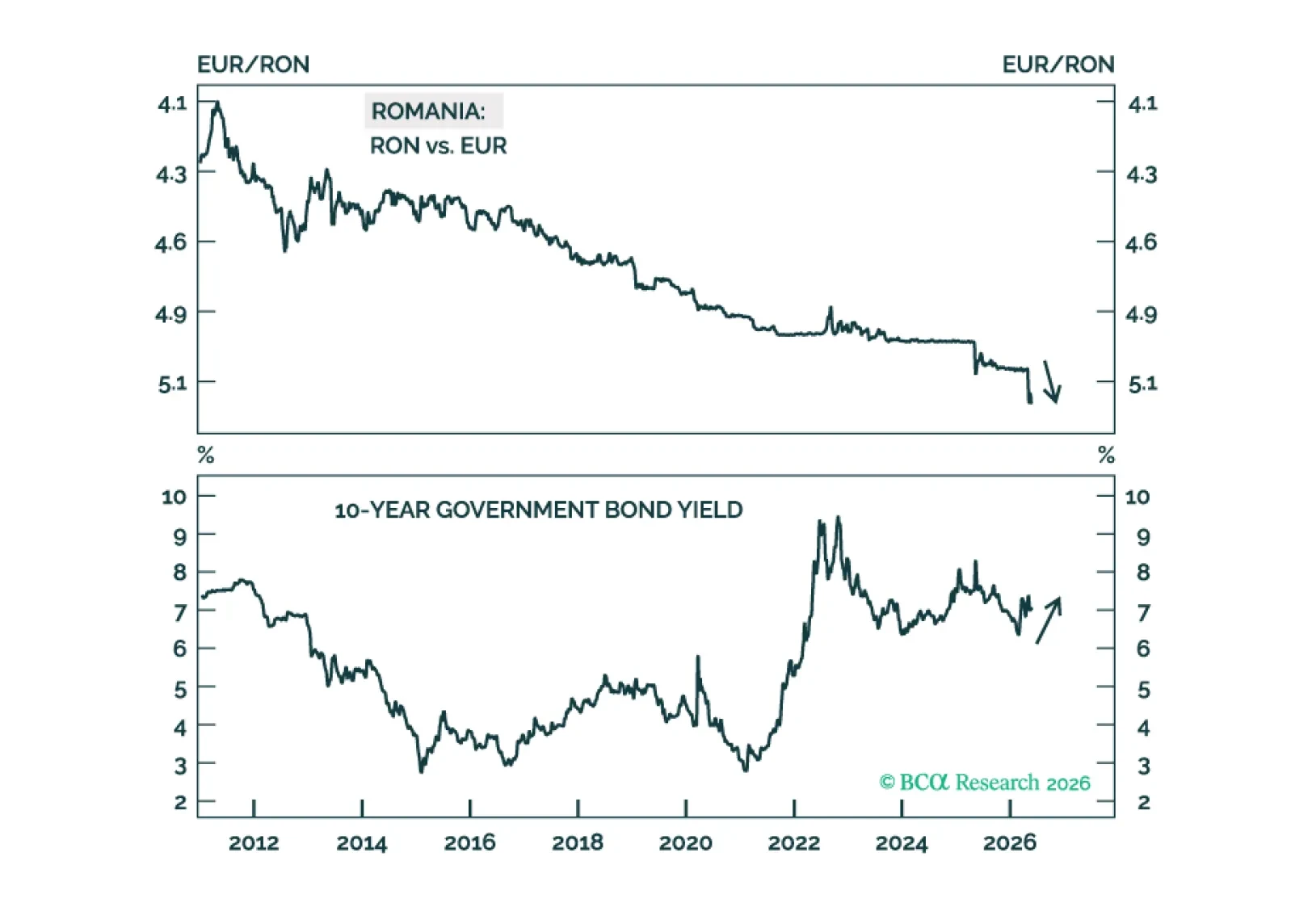

In Romania, large fiscal and current account deficits, high inflation, negative real rates, an overvalued exchange rate, and deteriorating growth point to budding currency devaluation. Investors should short the Romanian currency versus the euro and underweight Romanian local bonds, equities, and sovereign credit.

Bank Indonesia raised its policy rate by 50 bps to 5.25% last week, 25 bps above expectations, as a response to persistent rupiah weakness. The recent sell-off in the rupiah and local bonds was partly triggered by the finance minister's plan to spend an…

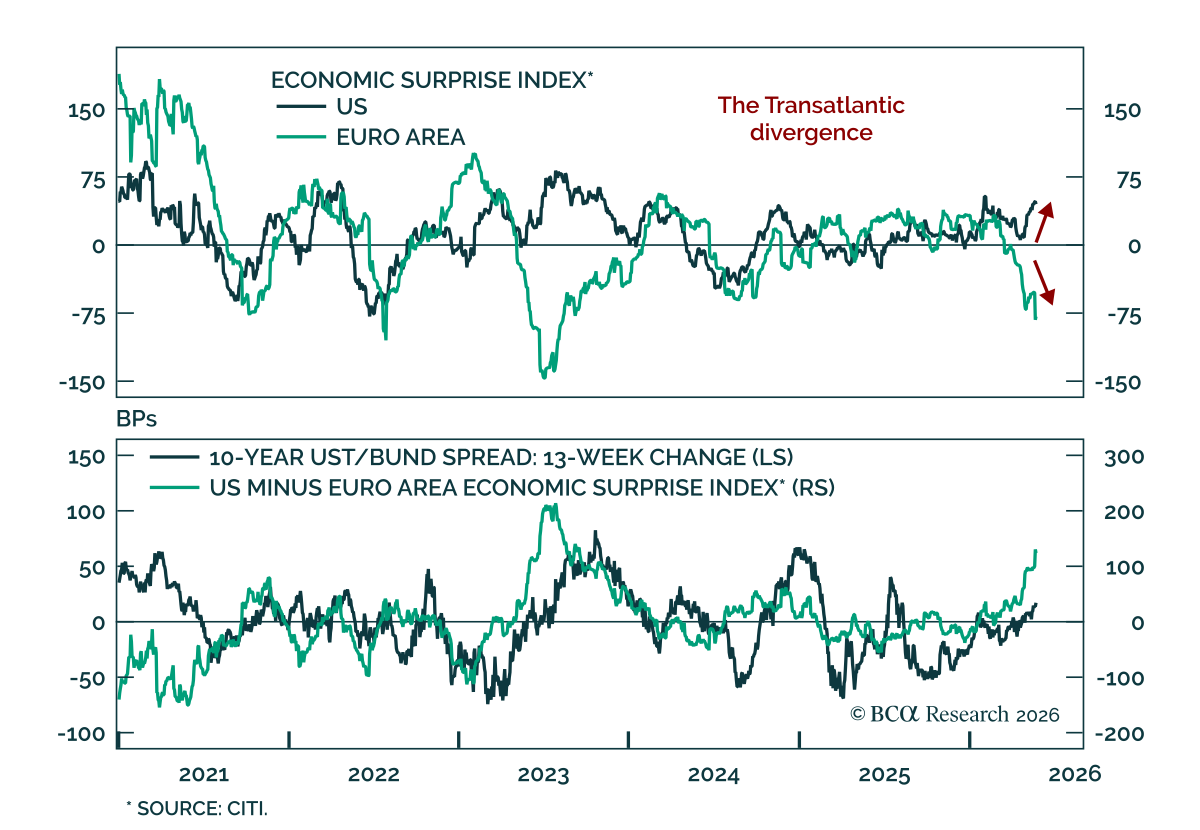

Go long German 10-year Bunds versus US 10-year Treasuries as US resilience diverges from euro area weakness. The trade is backed by a widening growth gap, with the US better insulated from rising oil prices and the euro area losing momentum. The US…