Fixed Income

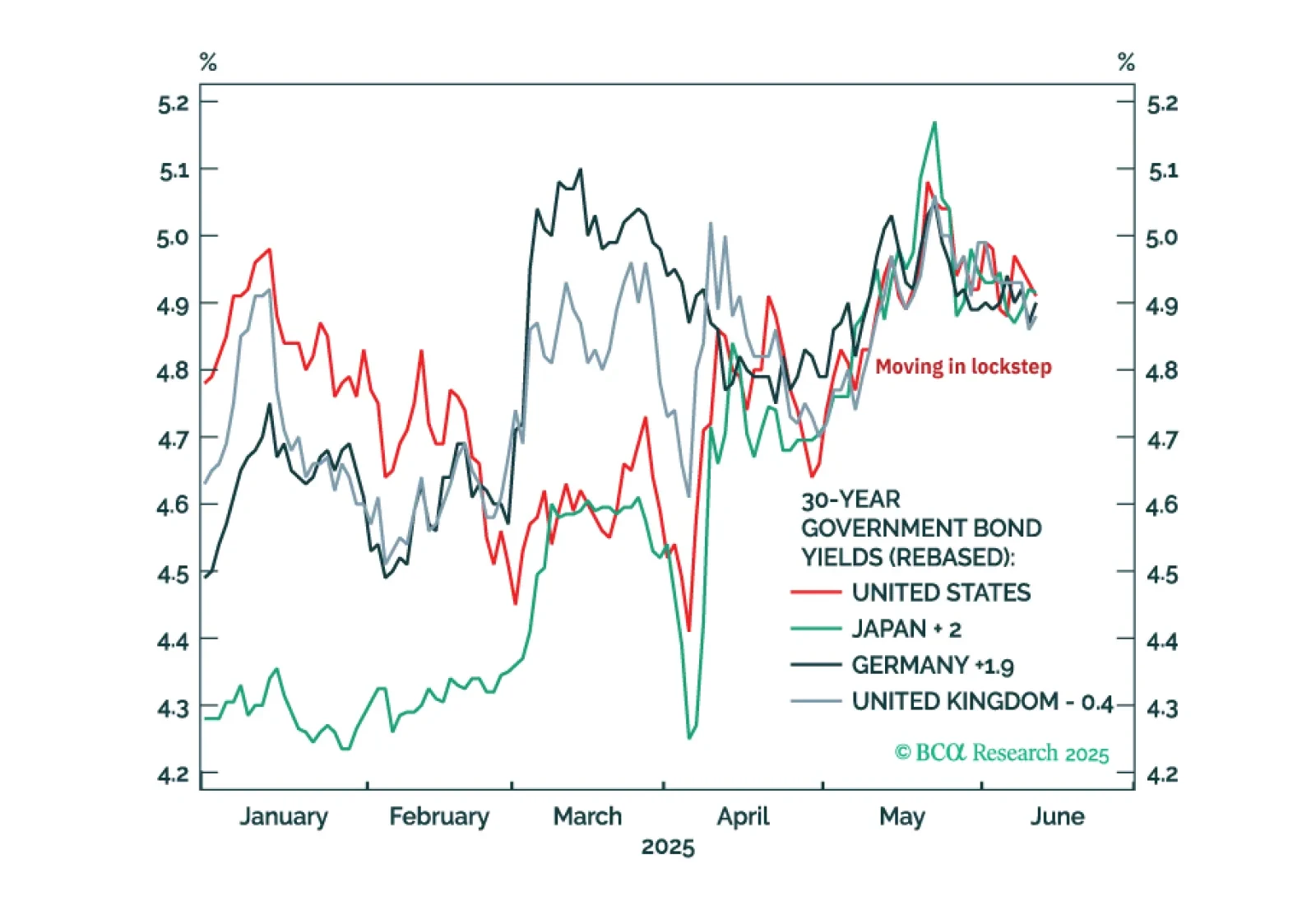

The perfectly synchronised moves in US, Japanese, German, and UK 30-year bond yields through the past two months are odd… and irrational. These irrational moves present compelling investment opportunities.

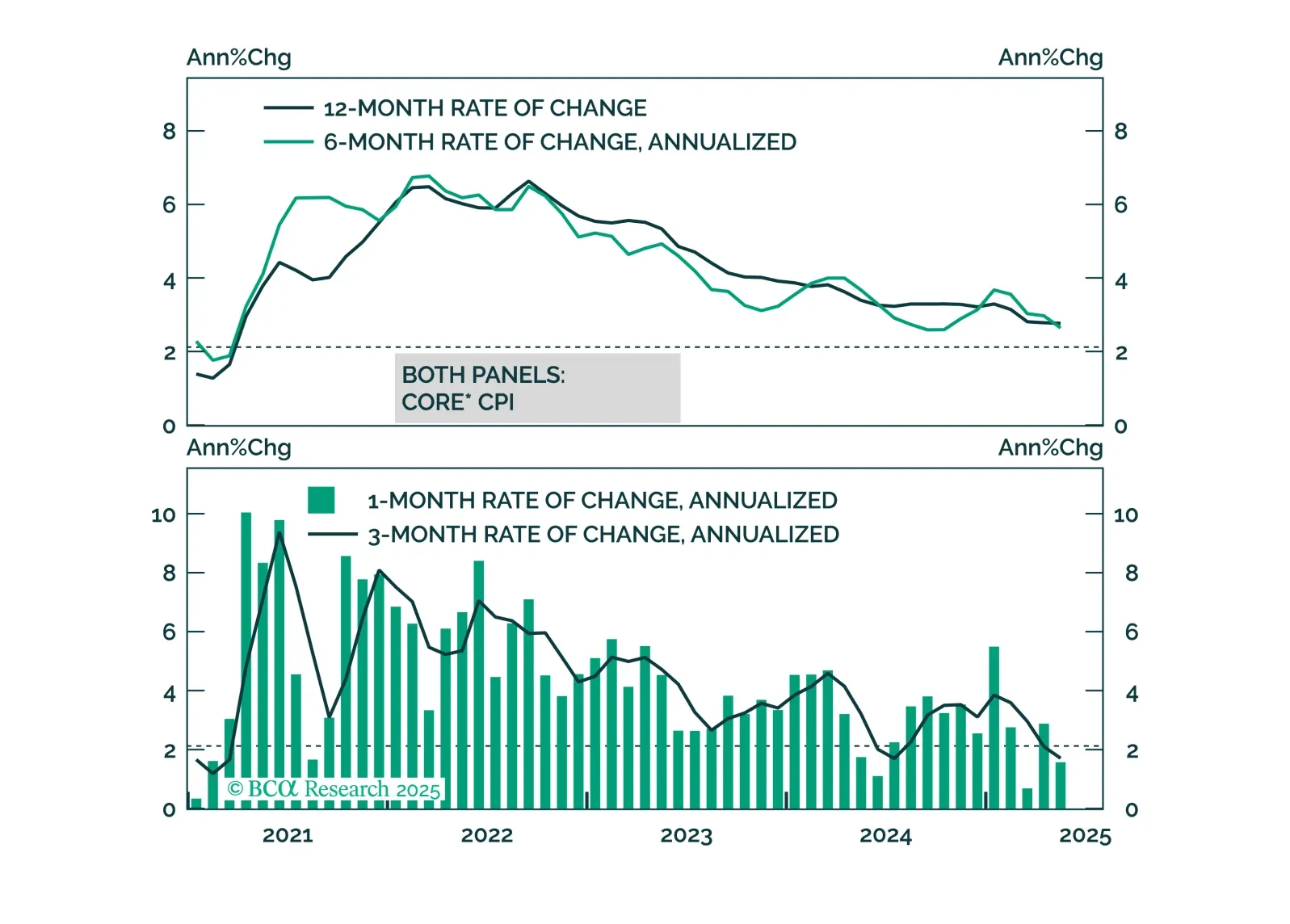

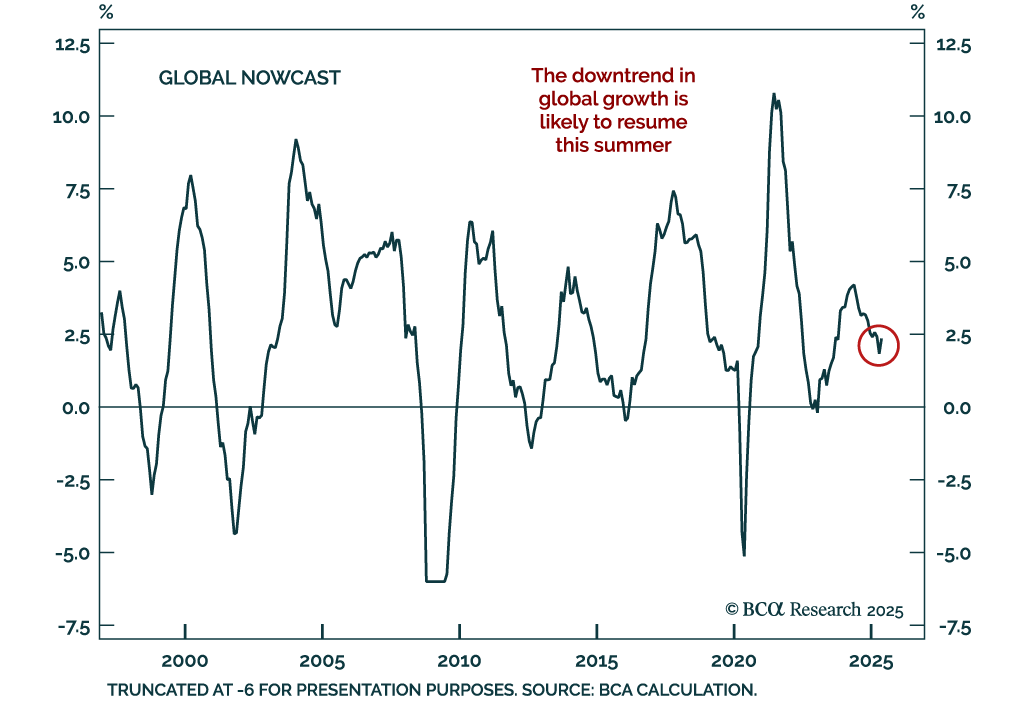

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

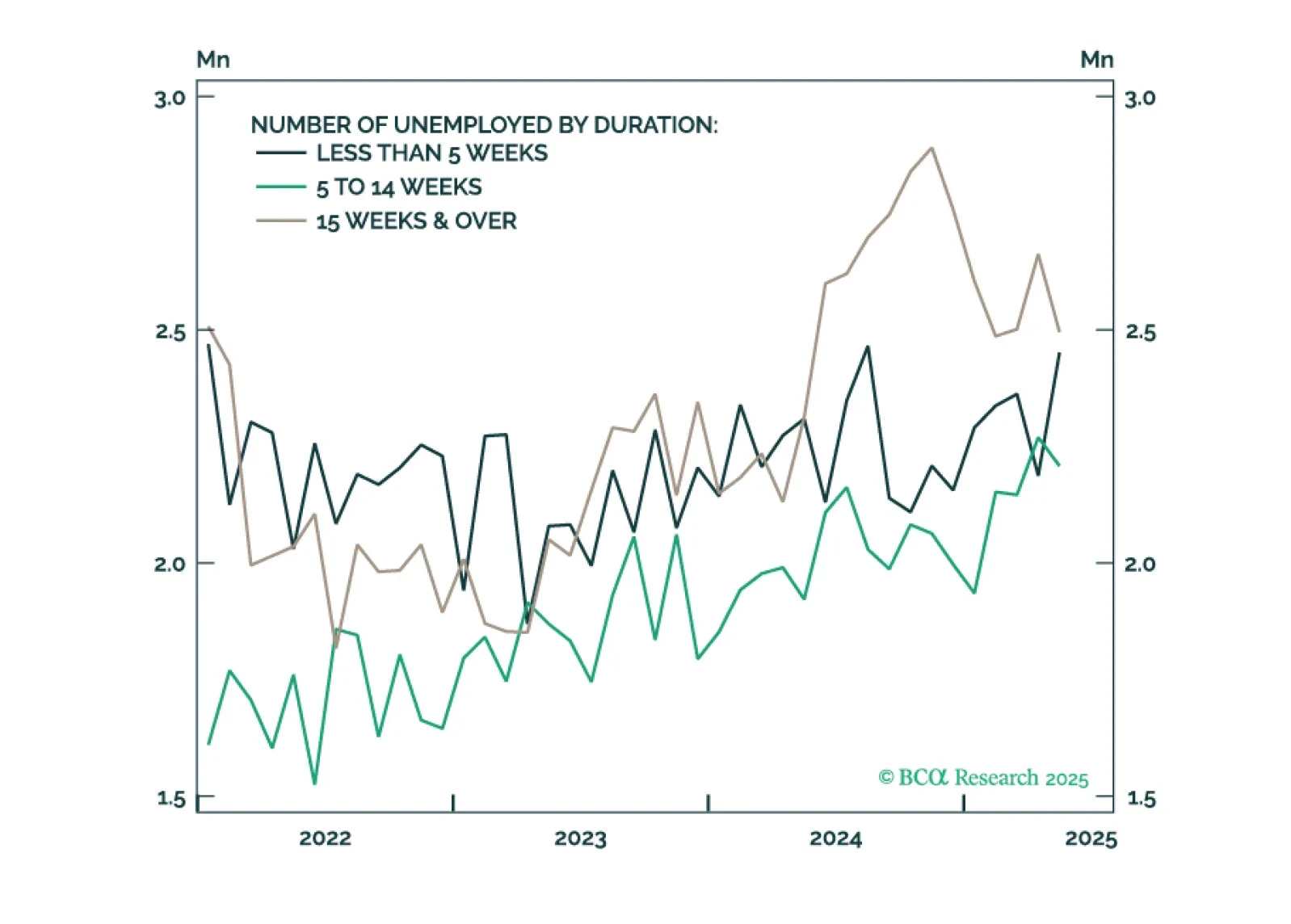

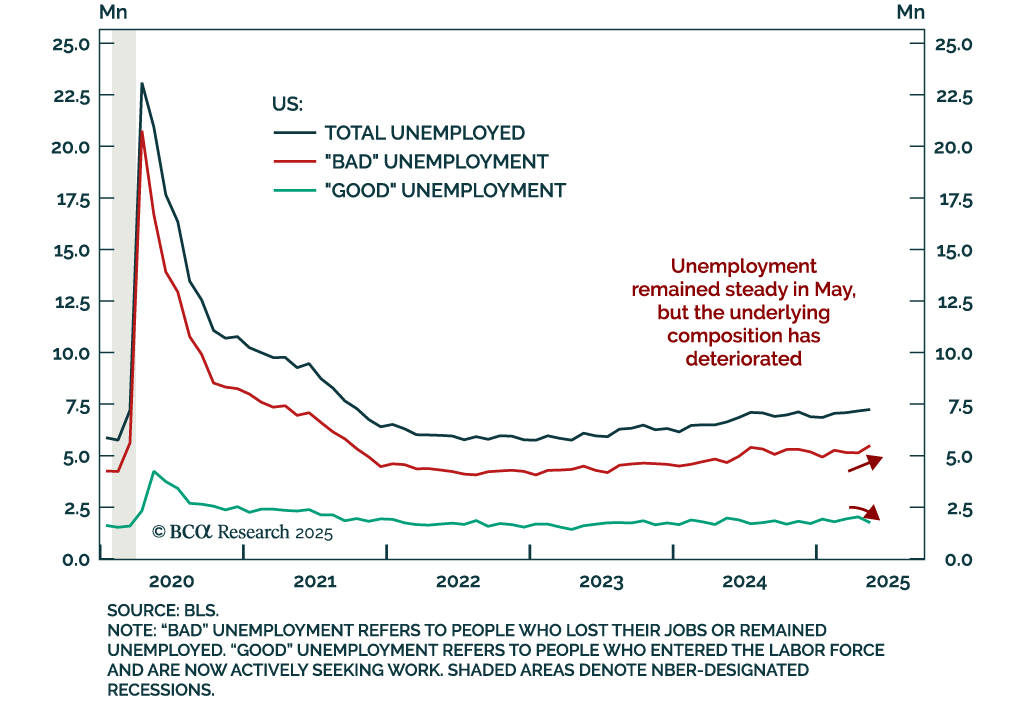

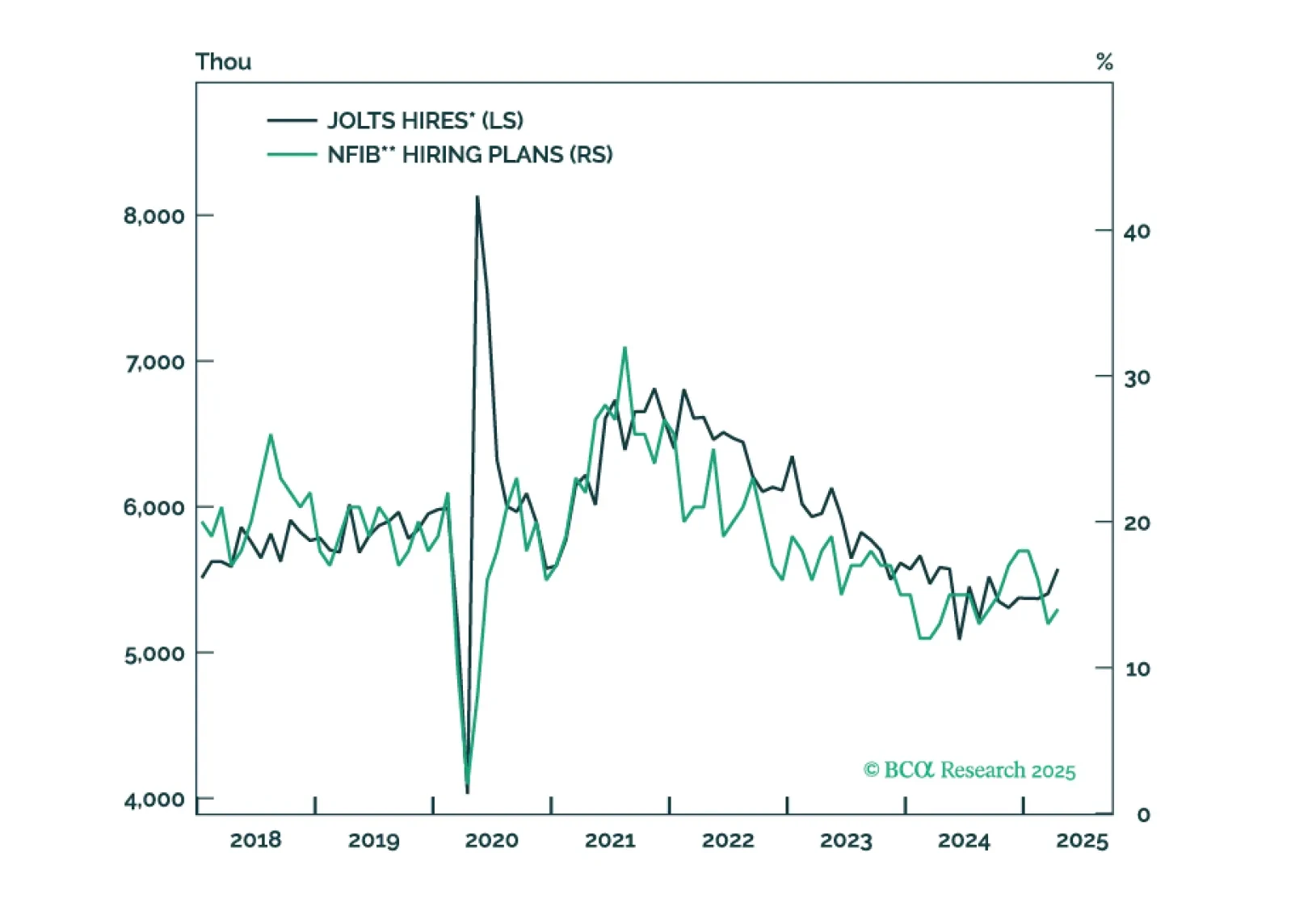

For now, measures of labor market utilization (like the unemployment rate) are only gradually weakening. But we know from history that these trends have a habit of quickly accelerating in advance of recession.

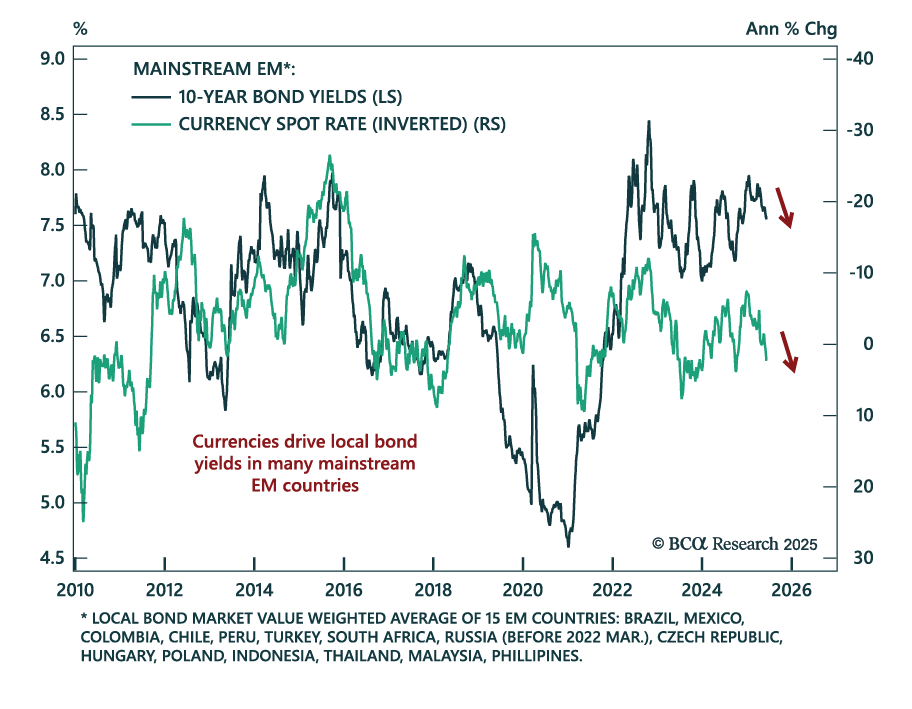

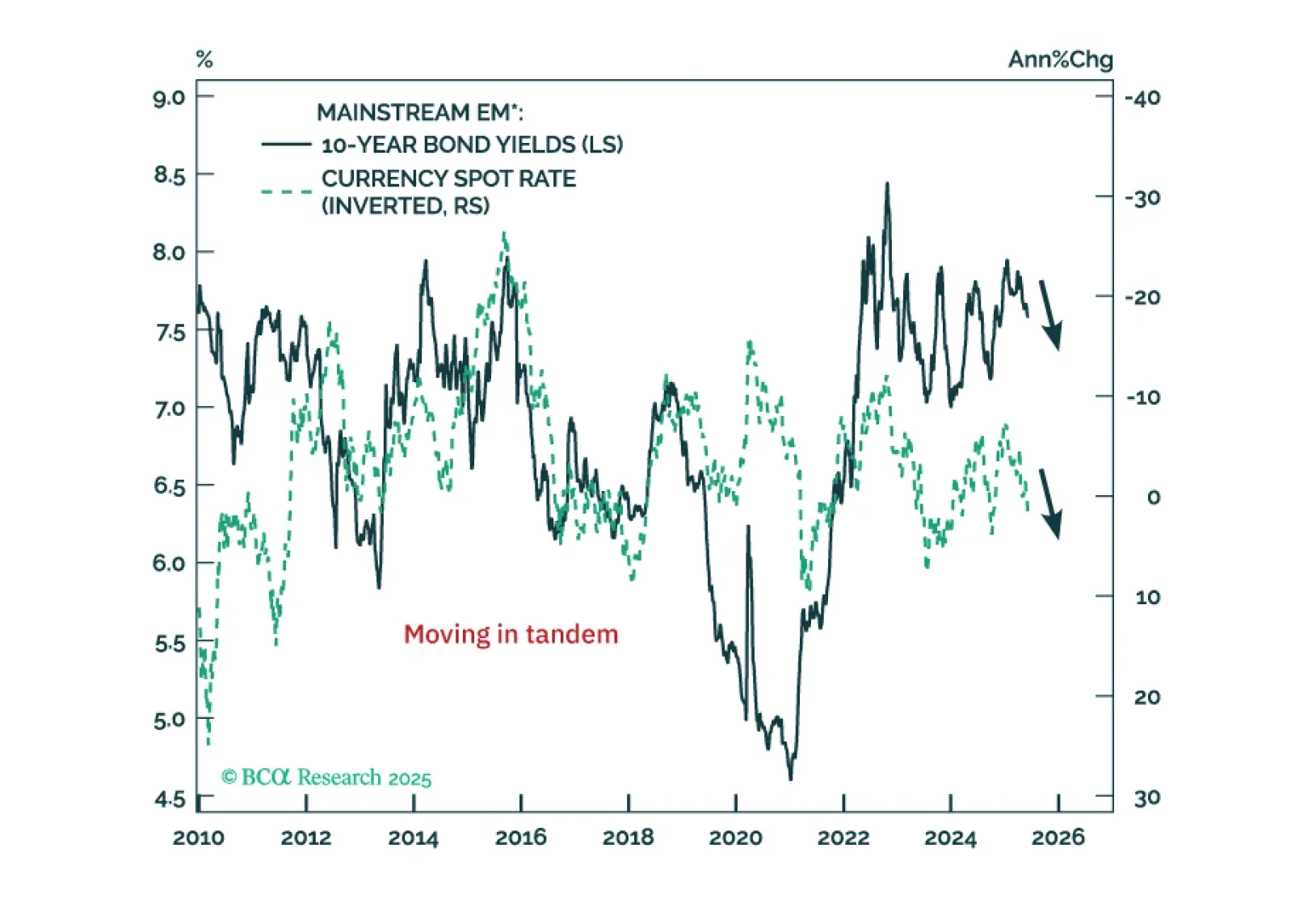

Unlike in past episodes, US dollar weakness will be deflationary, not reflationary, for the rest of the world. In this context, EM local currency bonds offer a superior risk-reward profile. Stay long domestic bonds in select EM countries.

Our Portfolio Allocation Summary for June 2025.