Fixed Income

Global currency markets have entered a new era. This implies that the framework for analyzing exchange rates must also change. We introduce a new framework for analyzing EM currencies and classify them into resilient and vulnerable categories. Finally, we are adding more EM domestic bonds to our portfolio and making many changes to our currency trades.

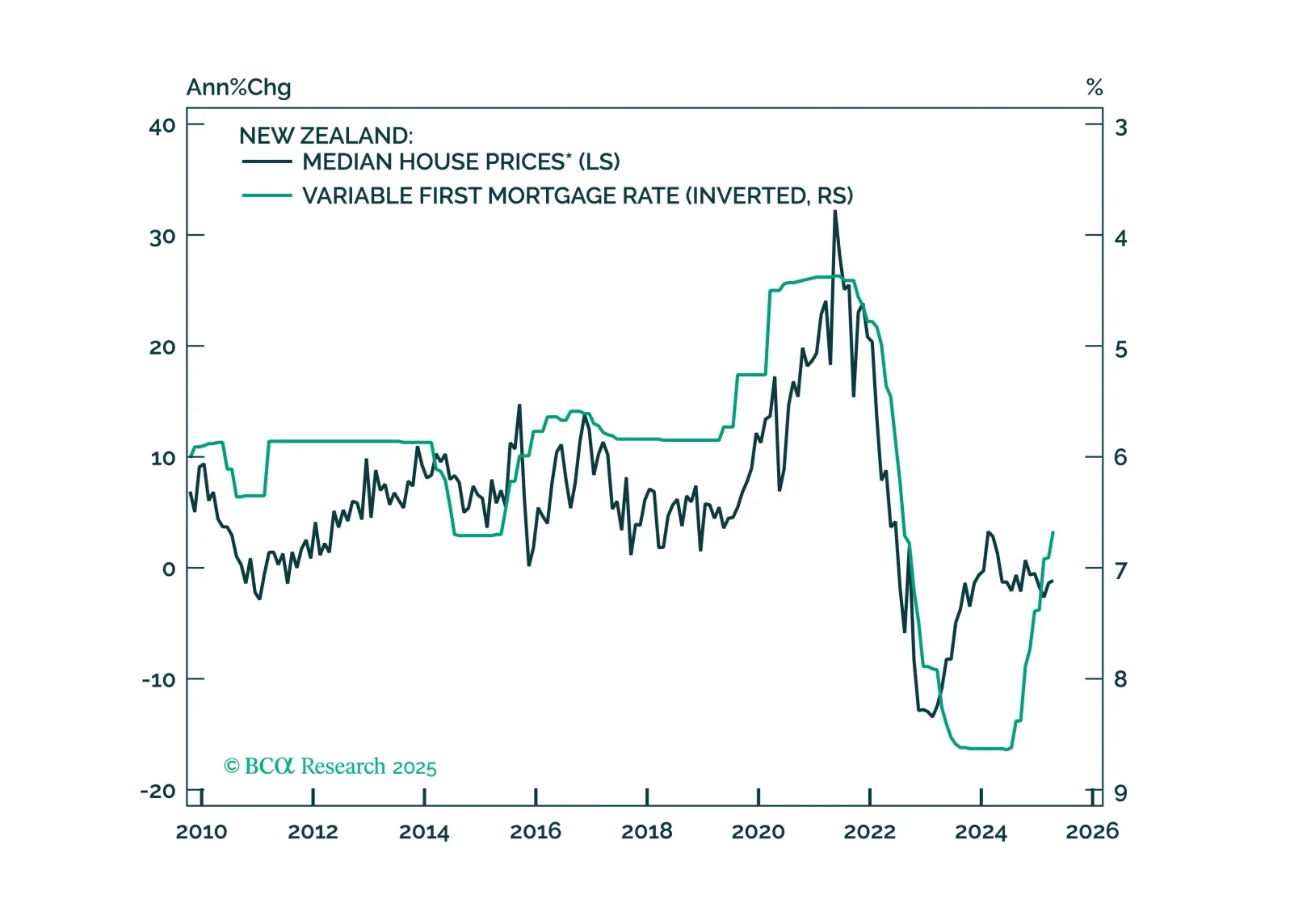

This Insight looks at the implications of the RBNZ’s rate cut on New Zealand assets.

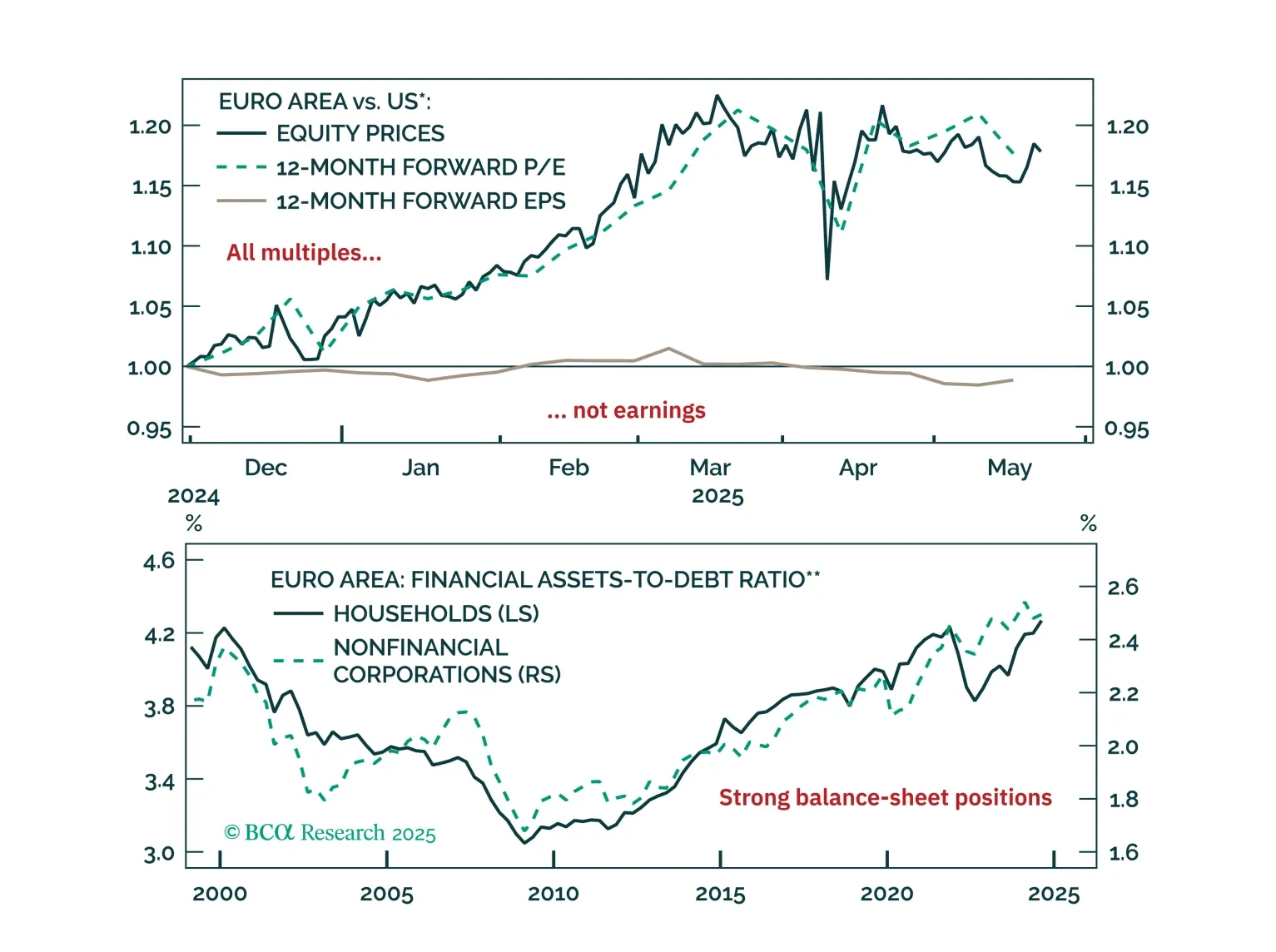

Five questions, five answers from the road. We unpack what Europe’s biggest investors are worried about right now, from trade‑war whiplash to bund‑versus‑Treasury positioning; and where the real opportunities still lie.

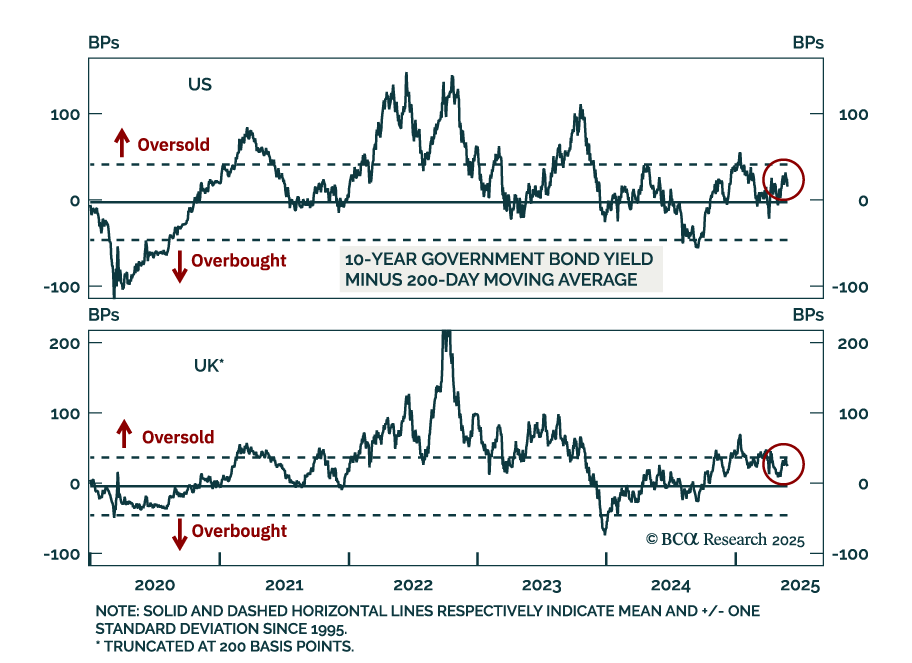

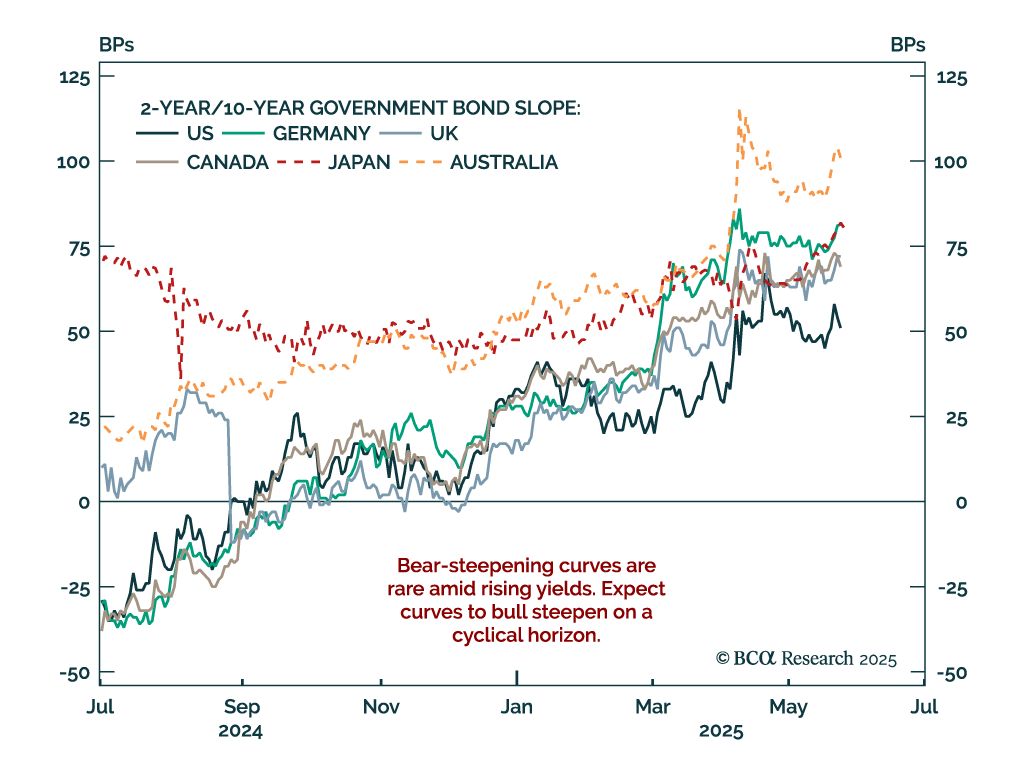

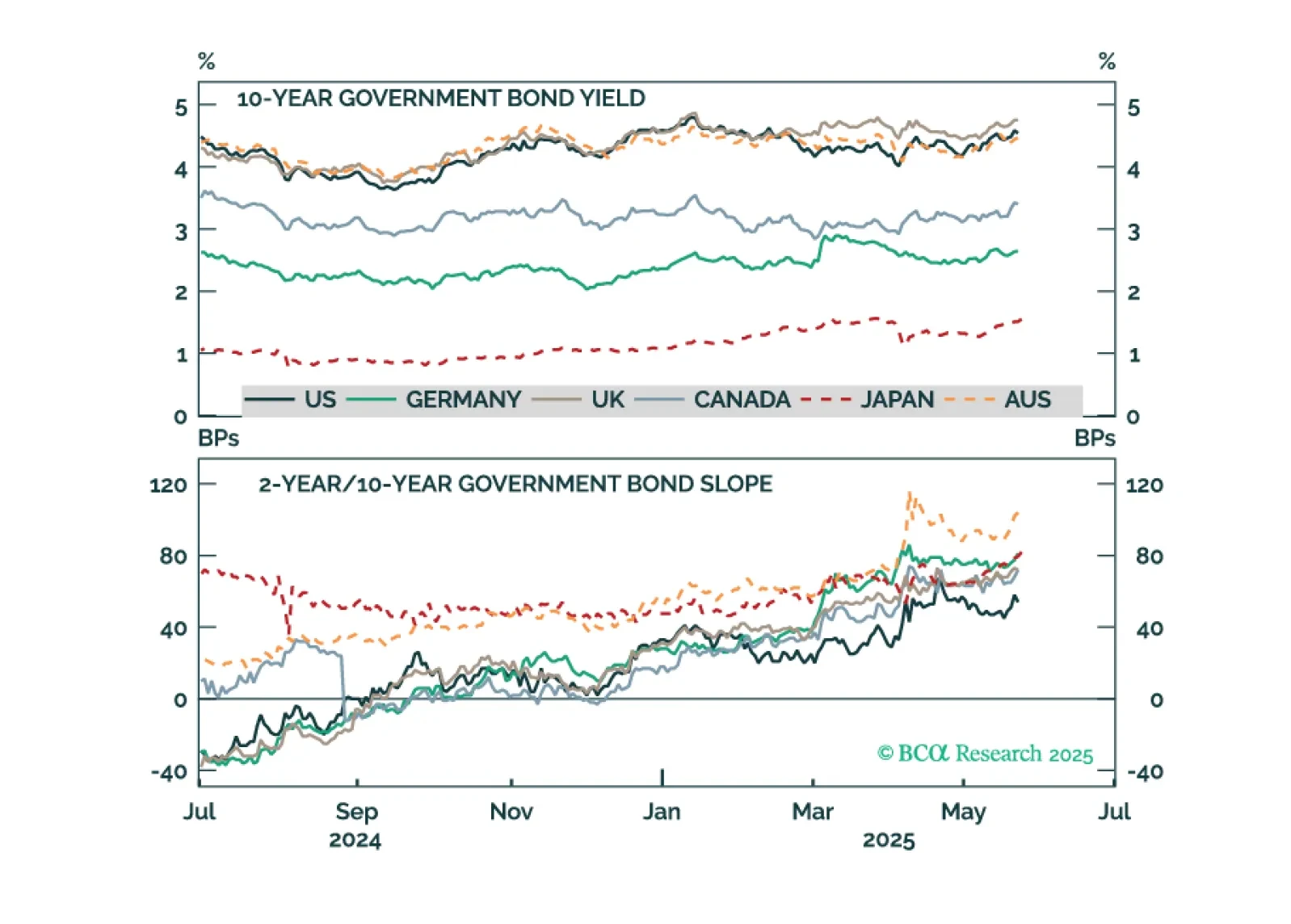

We perform a decomposition of yields moves across six major developed government bond markets to get to the bottom of what’s been driving the global bond selloff of the past eight months.