Fixed Income

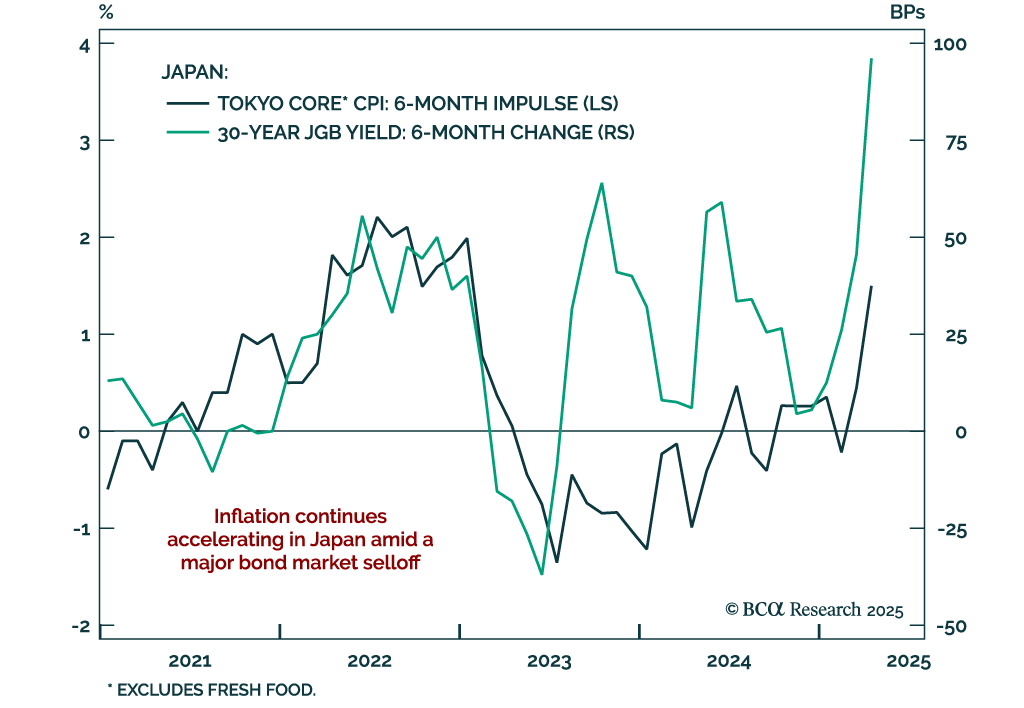

Tokyo CPI surprised to the upside in April, signaling that Japanese inflation shows no sign of deceleration and putting the Bank of Japan (BoJ) in a complicated position. Investors should remain maximum underweight in JGBs and overweight in…

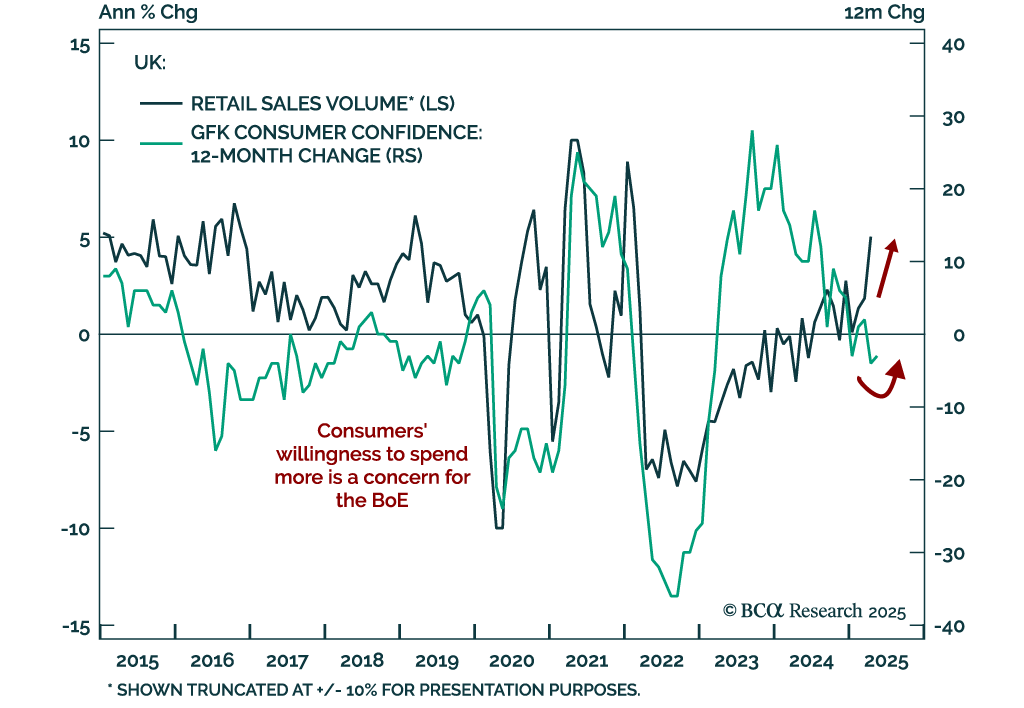

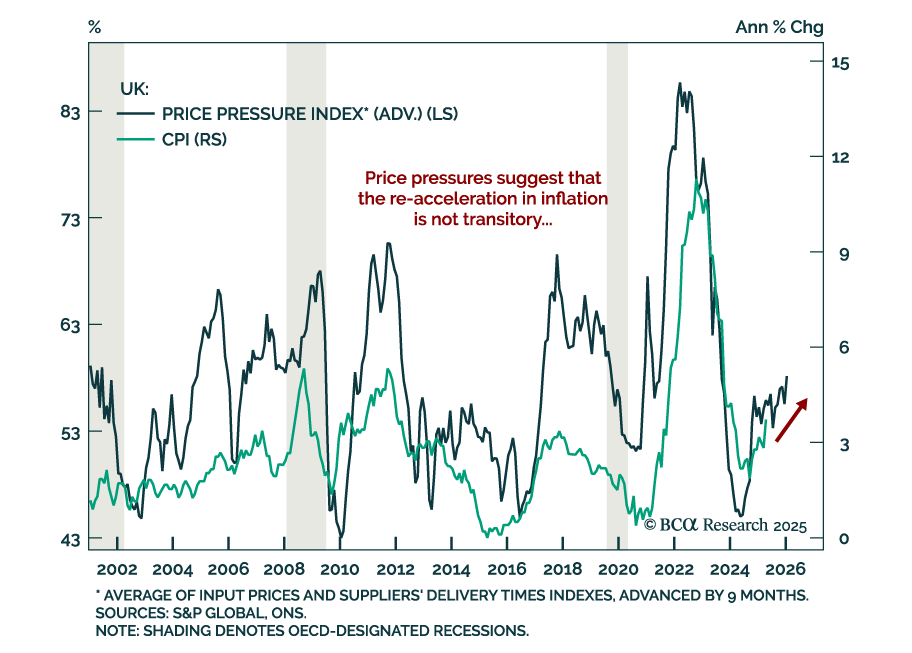

The rebound in UK retail sales and consumer confidence surprised to the upside, and suggests that the re-acceleration in inflation observed earlier this week may not be transitory. UK retail sales rose 1.2% m/m in April from 0.1% m/m, significantly…

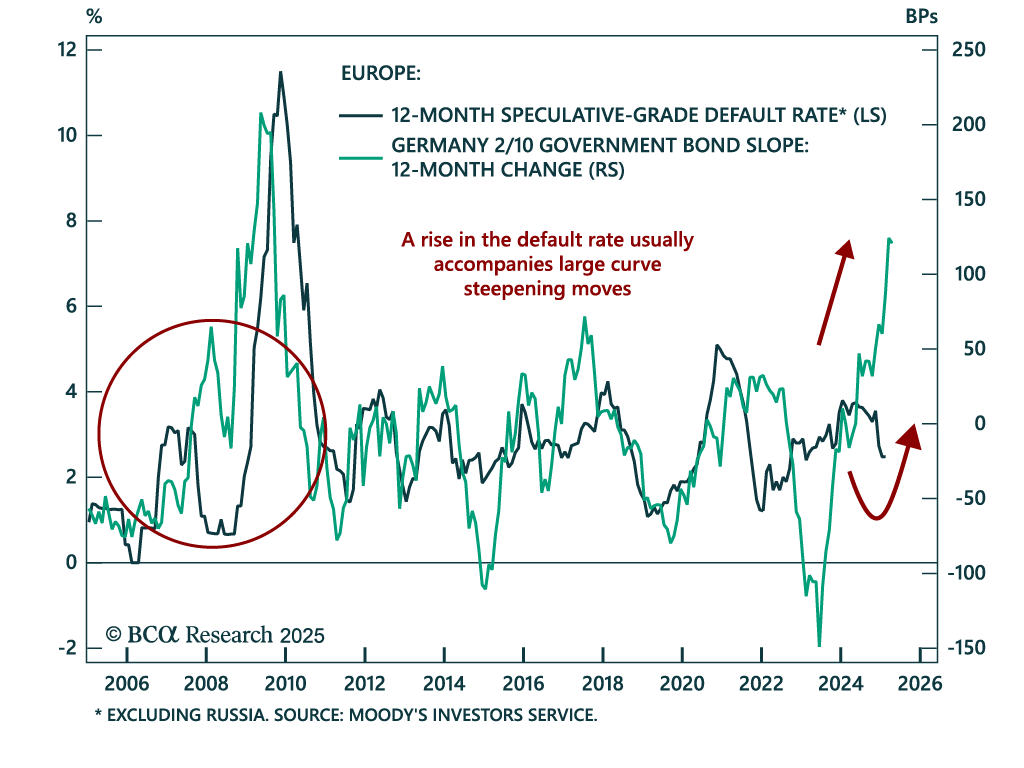

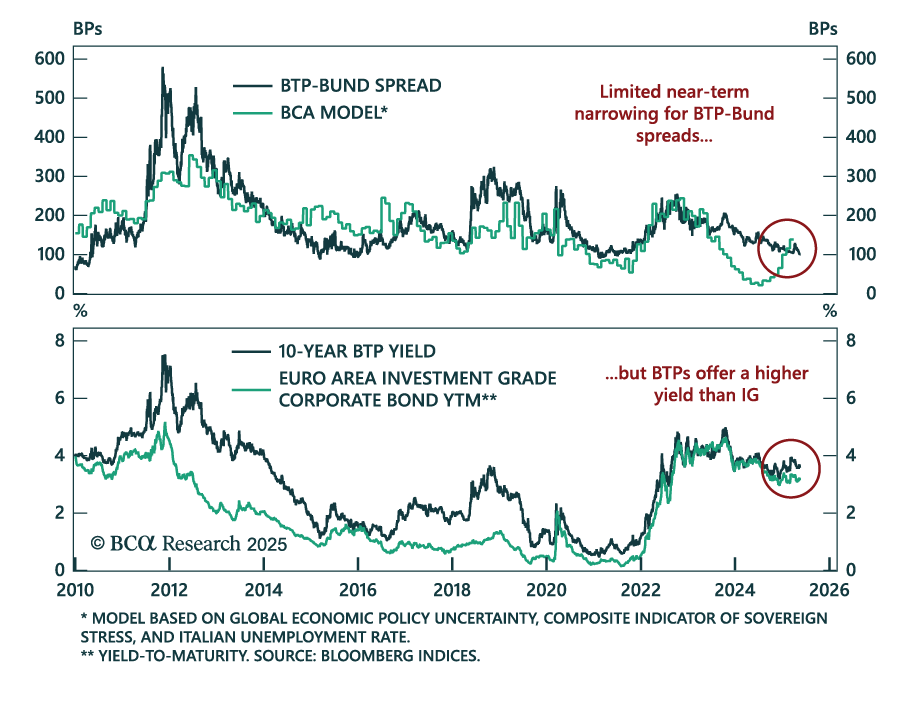

European corporate bond spreads have more room to narrow in the near term, but their next big leg is up. After a significant widening in option-adjusted spreads caused by stagflation fears in the US and “Liberation Day,” European spreads continue…

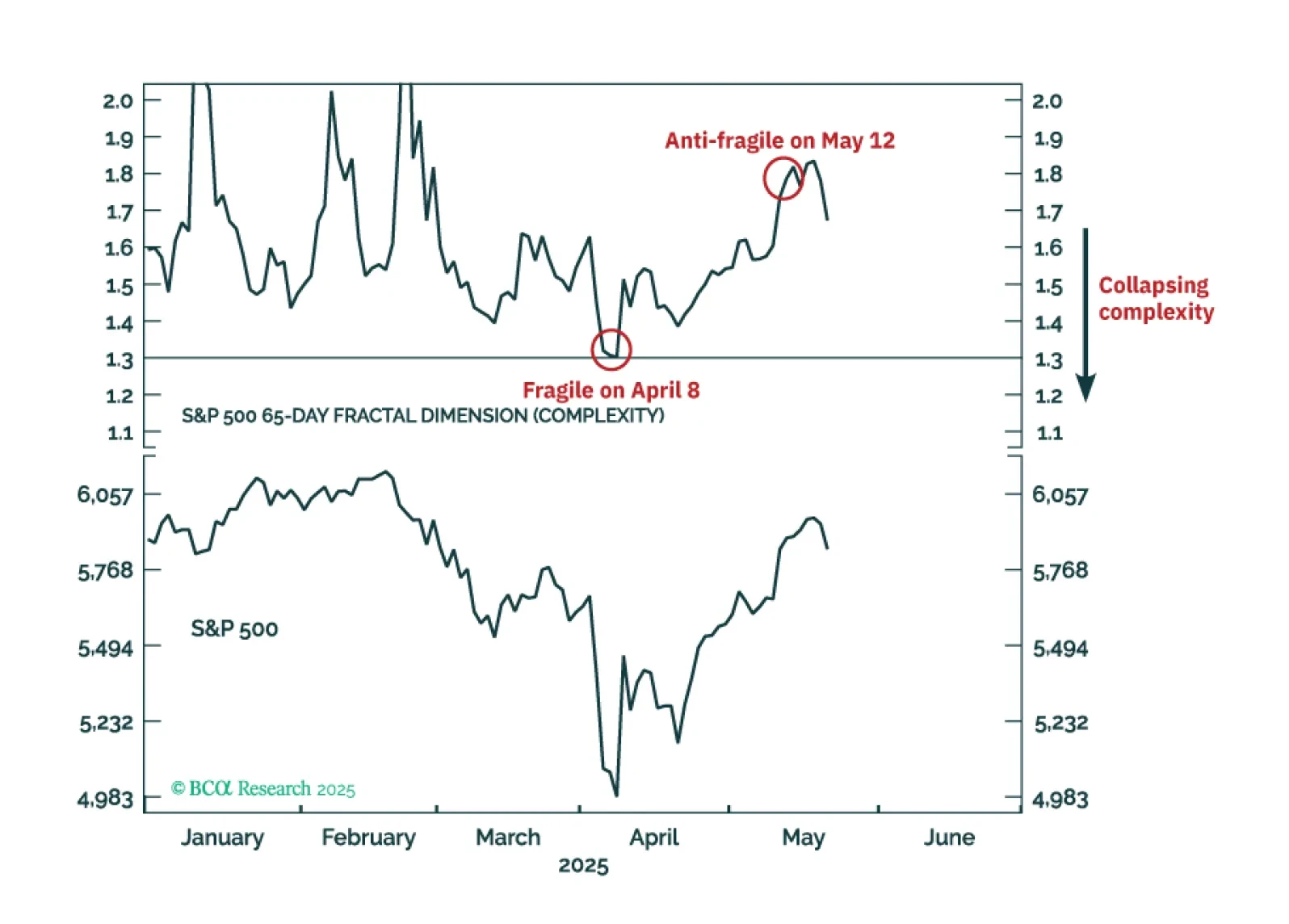

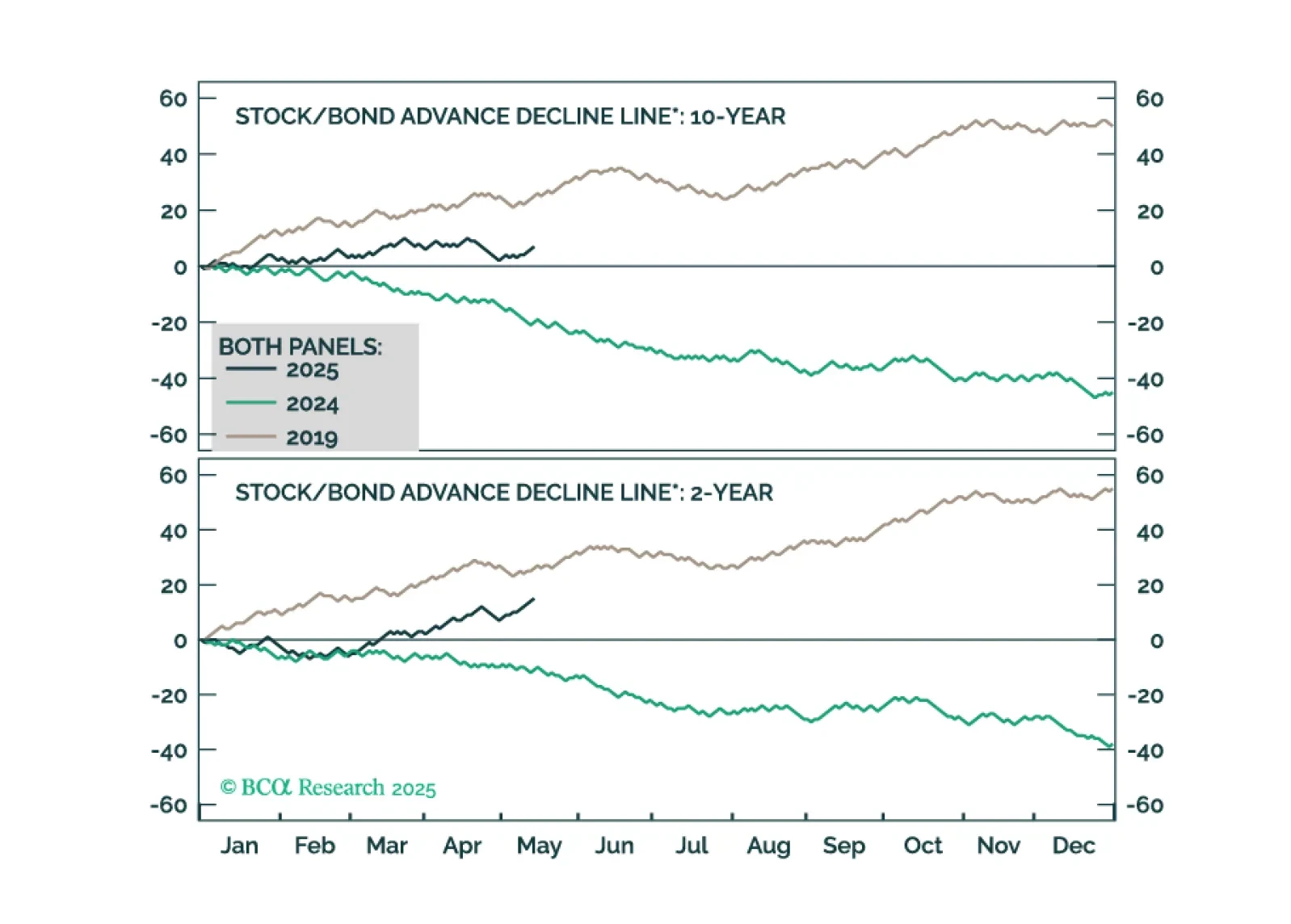

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.

UK inflation surprised to the upside in April. Headline inflation rose to a 15-month high of 3.5%, from 2.6% the month before. Core inflation also surprised above estimates, printing 3.8% vs. 3.4% in March. Services inflation climbed to 5.4% from 4.7%. Higher…

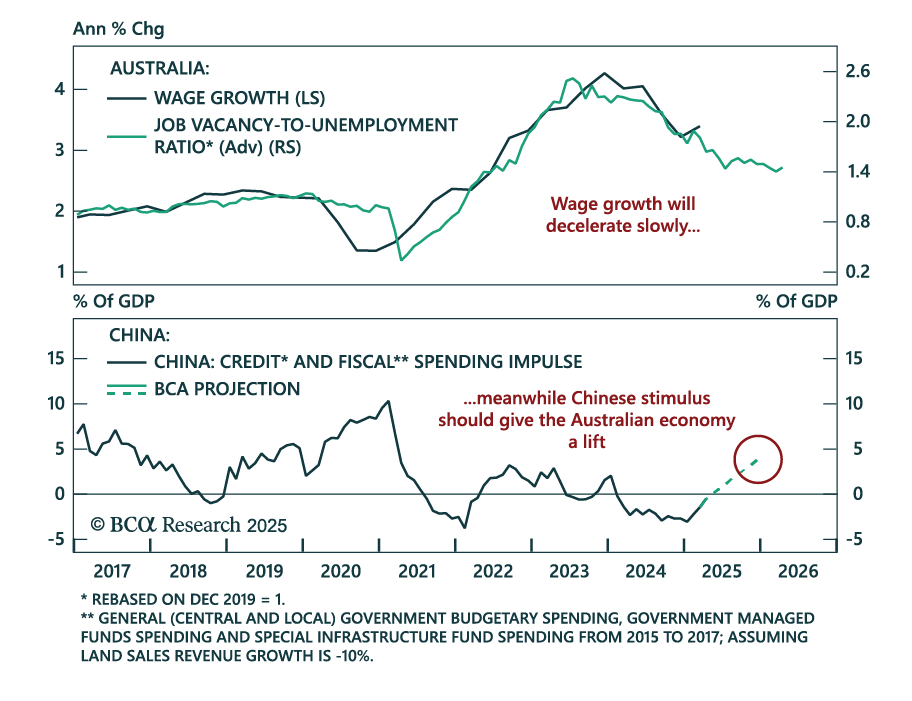

Overnight, the Reserve Bank of Australia (RBA) cut the cash rate target by 25bps to 3.85%, as widely expected. After this cut, the market still prices in about 50bps of easing over the next six months. According to our Global Fixed-Income strategists,…

The European bond market is pricing in a more optimistic outlook. The BTP-Bund spreads have narrowed 30bps since April 9 and are now within reach of their pre-Ukraine war level. BCA’s European strategists do not share this optimism, at least not in the…

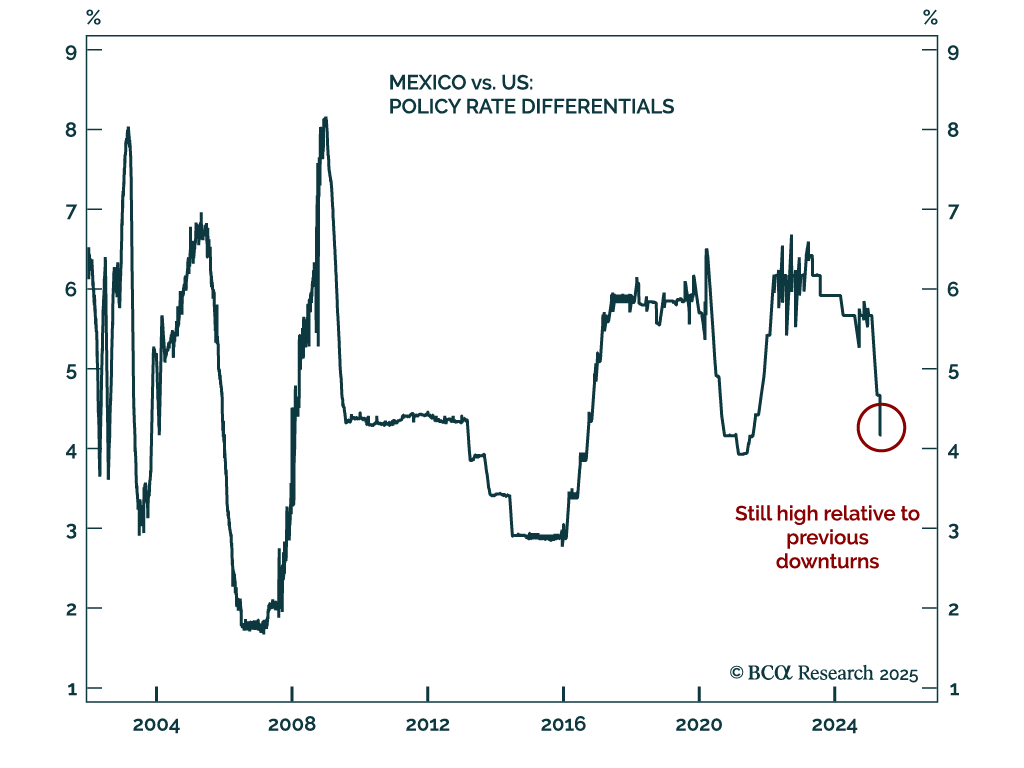

Banxico’s 50 bps rate cut reinforces our bullish view on Mexican bonds, with easing likely to continue as inflation falls and growth slows. The central bank unanimously lowered its policy rate to 8.5%, and we expect further cuts ahead as Mexico heads toward a…

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.

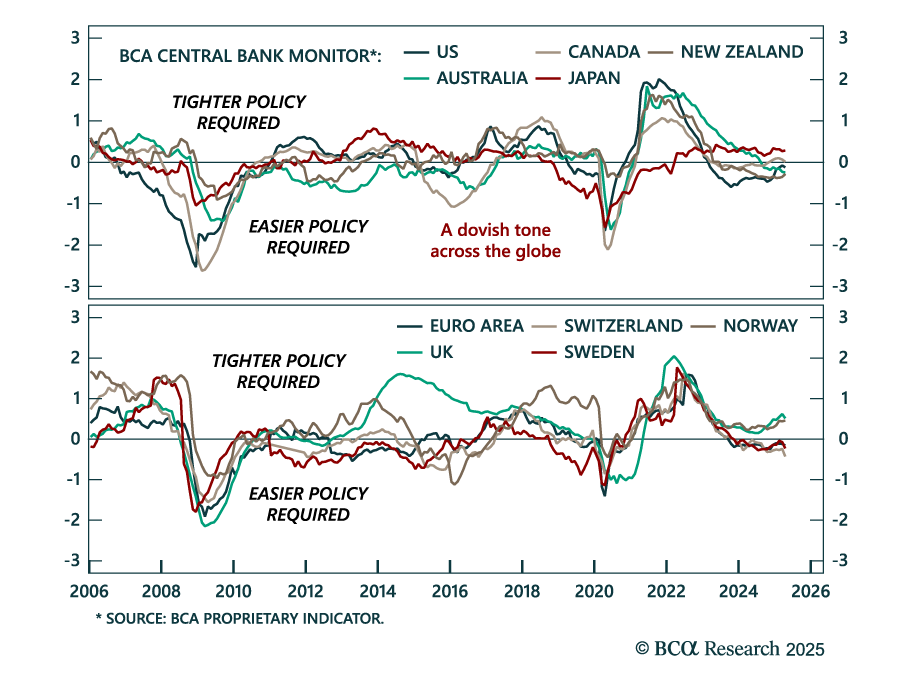

Expect broad-based dovish surprises from major central banks, and stay overweight UK and euro area government bonds. Our Global Fixed Income, European, and FX strategists published a joint update of BCA’s Central Bank Monitors. They expect the Bank of…