Fixed Income

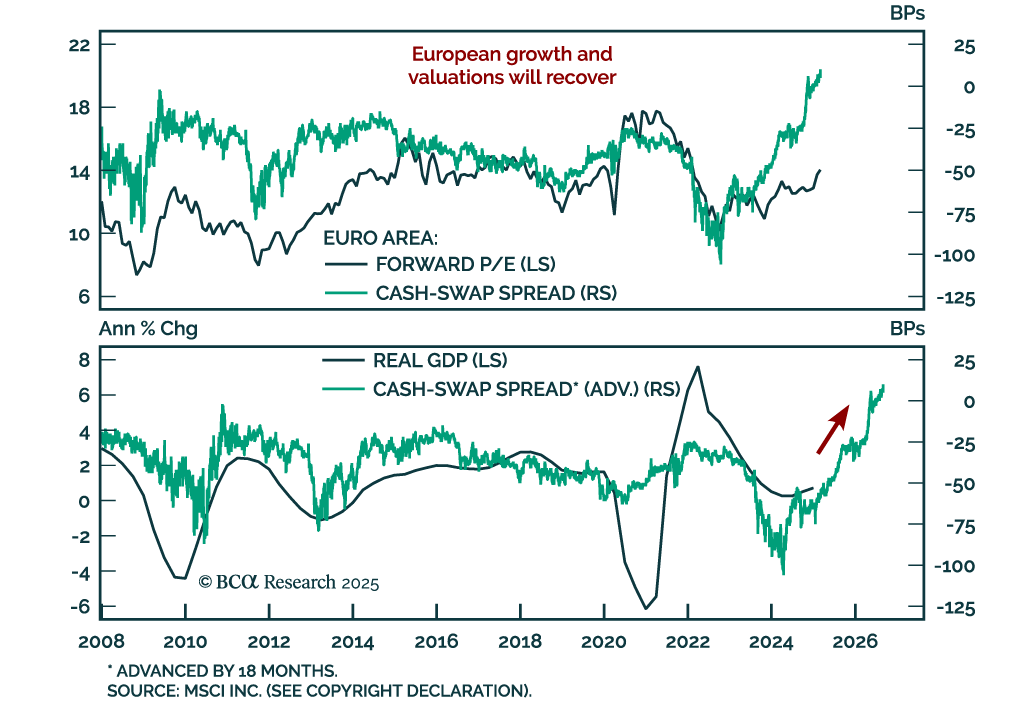

The ECB cut rates as expected, but rising yields and a stronger euro are tightening financial conditions just as fiscal policy shifts the macro landscape. With more rate cuts ahead and market positioning stretched, we outline the key risks, investment opportunities, and our updated call on the ECB’s terminal rate. Read our full report for actionable insights.

Our Portfolio Allocation Summary for March 2025.

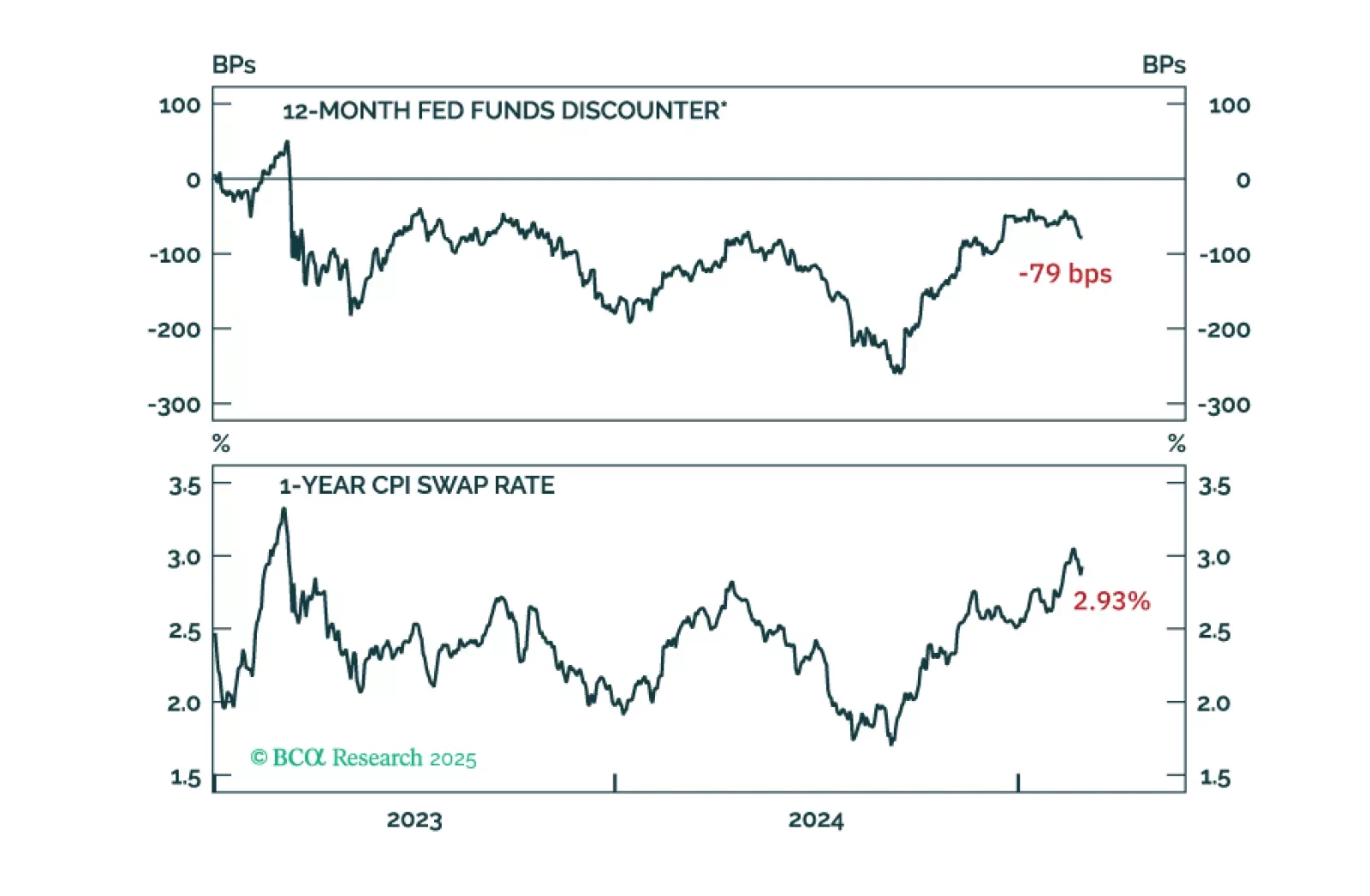

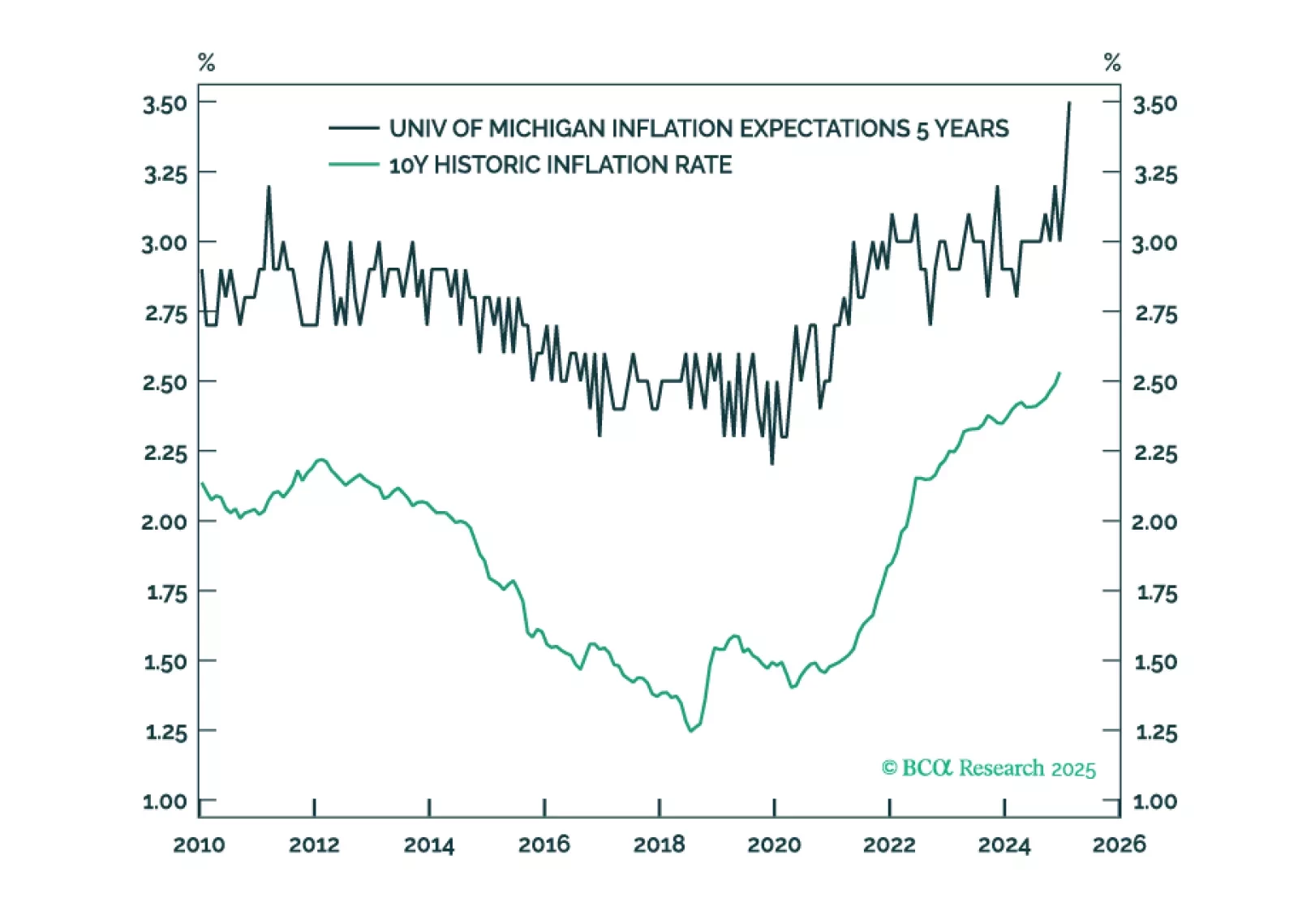

Core PCE inflation was tame this morning, but with large tariffs looming we anticipate loftier inflation readings in the months ahead.

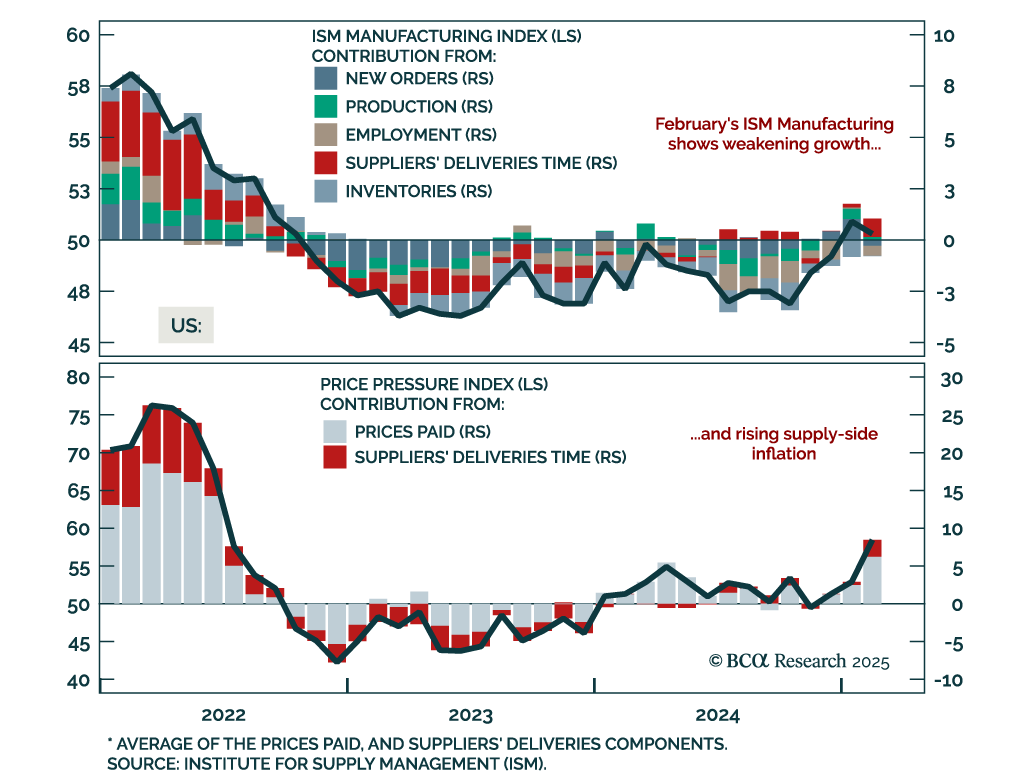

The US (and the UK) is staring down the barrel of a ‘mini-stagflation’ until a deflationary shock arrives to neutralise it. We describe a likely source for the deflationary shock and list three investment conclusions that are valid irrespective of how long it takes for the deflationary shock to arrive. Plus: RCI.B is deeply oversold and ripe for a rebound.