Fixed Income

Our US Political Strategy colleagues now see 55% odds of a Trump victory, with odds of a Republican sweep at 47%. As odds of a contested election are rising, they built on their 2020 work to provide answers for next week’s election: Won’t the economy…

The main driver of global consumer sentiment in the past few years has been high inflation. Nowhere has this been the case more than in the US, where measures of animal spirits were depressed despite a roaring economy. Today, inflation worries have eased, but…

The “core core” (ex. fresh food & energy) segment of the Tokyo CPI basket beat expectations in October, printing at 1.8% year-over-year and accelerating from 1.6% in September after troughing at 1.5% in July. The Tokyo CPI is a timely indicator of…

Eurozone money and credit data beat expectations, with M3 accelerating to 3.2% year-over-year in September from 2.9% a month prior. Household and corporate lending both drove the improvement. This development echoes the latest ECB Bank Lending Survey,…

Savings must either flow into domestic investment, or abroad. Saving too much, with nowhere to funnel it, is breaking China’s economic model according to our Global Investment Strategy colleagues. As China's share of global manufacturing climbed to 30%,…

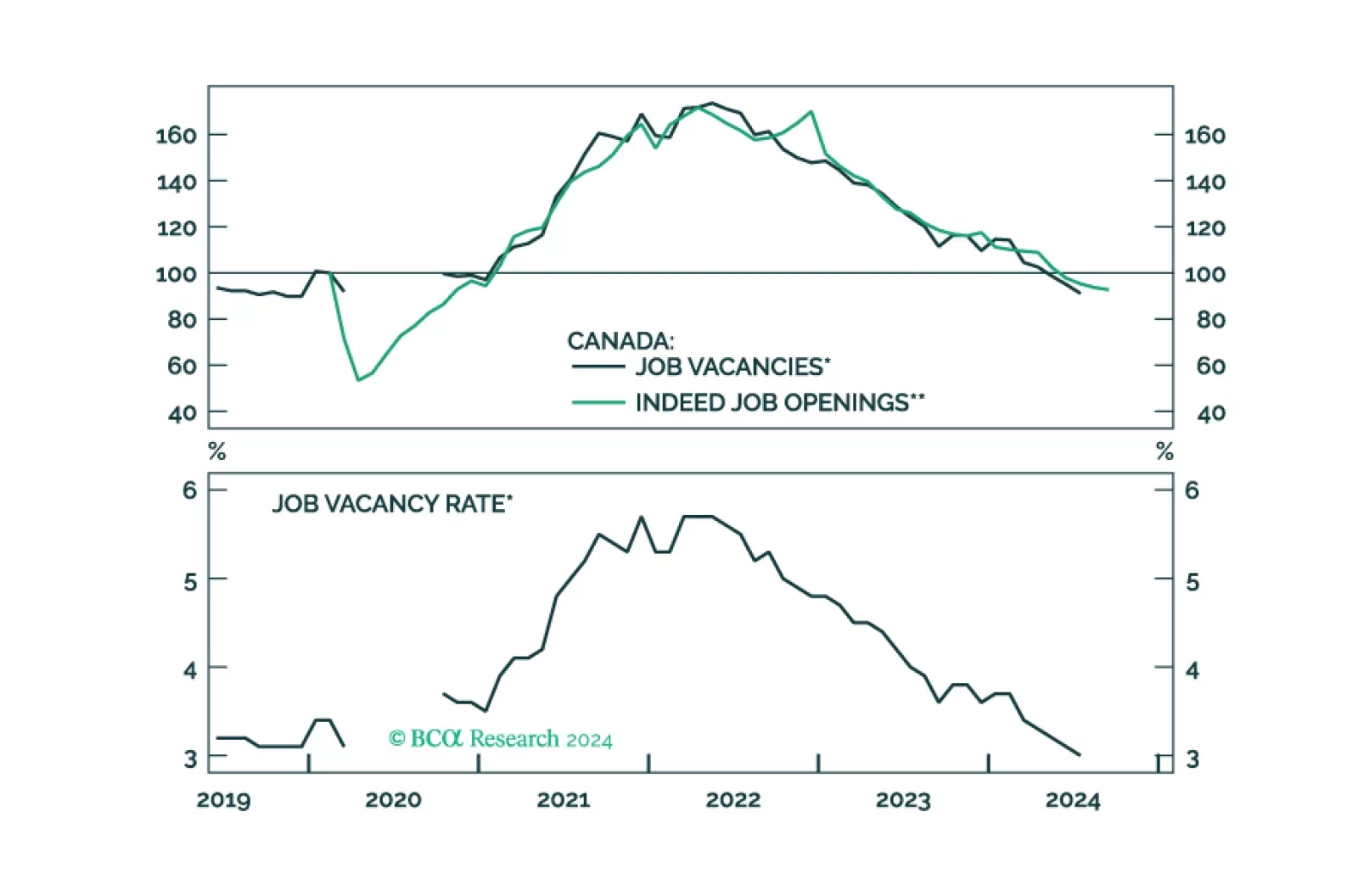

In this Insight, we evaluate if there is more juice in our macro bet of being long June 2025 CORRA versus SOFR futures, and correspondingly, being short the CAD, for investors with a 1-3 month horizon.

Flash estimates for European consumer confidence met expectations at -12.5 in October, rising from -12.9 in September. Despite this positive development, Euro Area sentiment remains poor. Consumer confidence remains below its long-term average and near the…

After cutting three times already since June, the Bank of Canada fulfilled market expectations and cut the overnight rate by 50 bps to 3.75%. The BoC sees risks around inflation as roughly balanced over its projection horizon, and is focused on “sticking the…

The Federal Reserve’s Beige Book, its survey of business contacts, shows an economy that has seen little growth since early September. The Fed’s contacts confirmed the manufacturing recession reflected in other data sources. Loan demand was mixed, as…

The US dollar had a strong October thus far, breaching its 20-,50- and 200-day moving averages with a 4% increase and only three trading days in the red. The DXY now sits above where it was before the August selloff in risk assets. What’s behind this…