Fixed Income

Continued deterioration in labor demand underpins our expectation for a US recession, as it will lead to slower compensation growth, hobbling consumption spending’s main driver. We also previously highlighted that the outlook for bond yields currently hinges…

ECB Governing Council members unanimously voted in favor of lowering the deposit facility rate by 25 bps to 3.50% in September, marking the second cut this year. Moreover, expectations for weaker domestic demand led the ECB to downgrade its growth forecast…

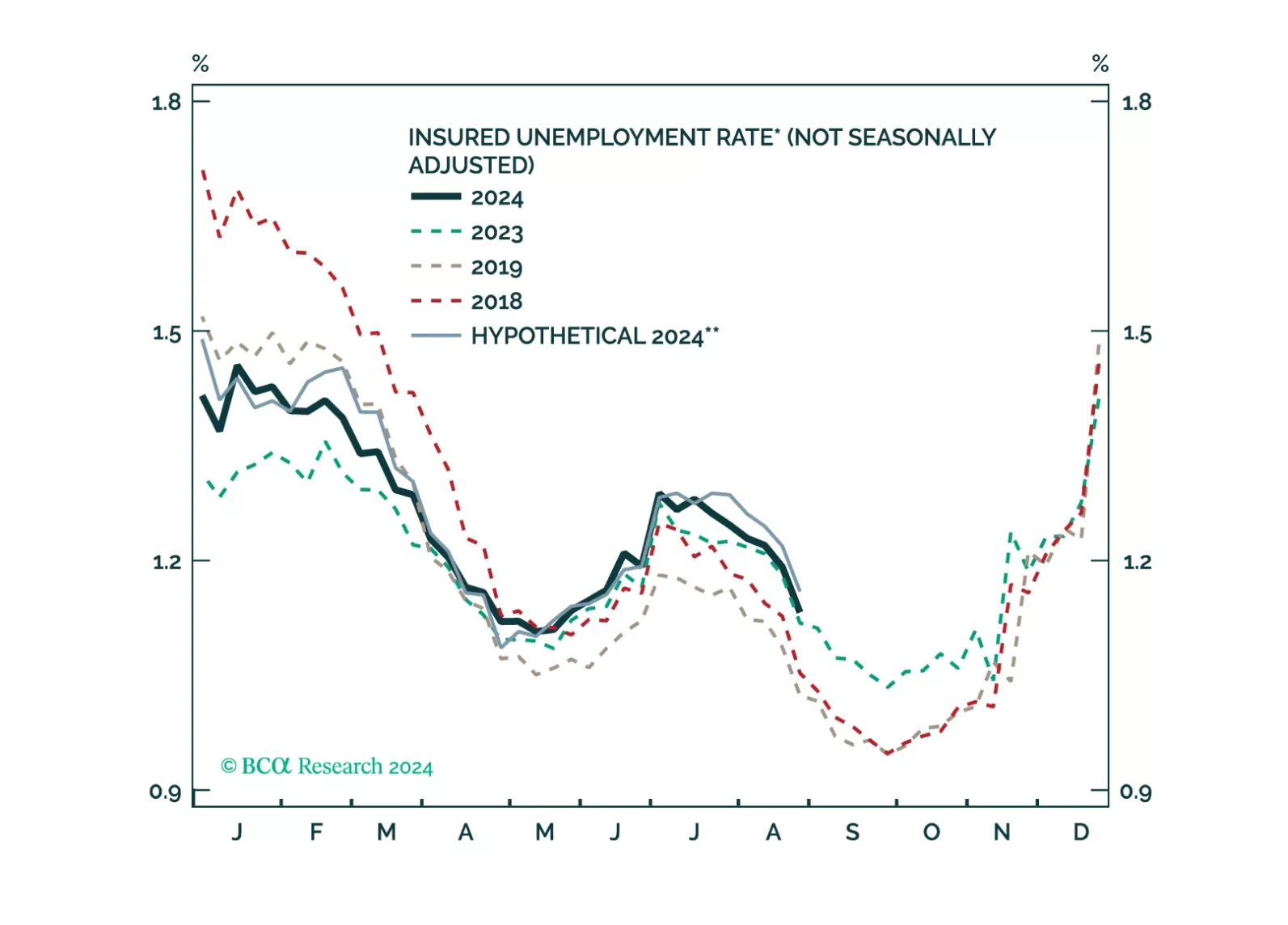

Some thoughts on this morning’s US claims report and a preview of next week’s FOMC meeting.

Despite global bond yields having trended lower since April, bonds have only started outperforming equities since July in US dollar terms. We expect this outperformance to persist going forward. Sentiment has largely driven the equity market rally this…

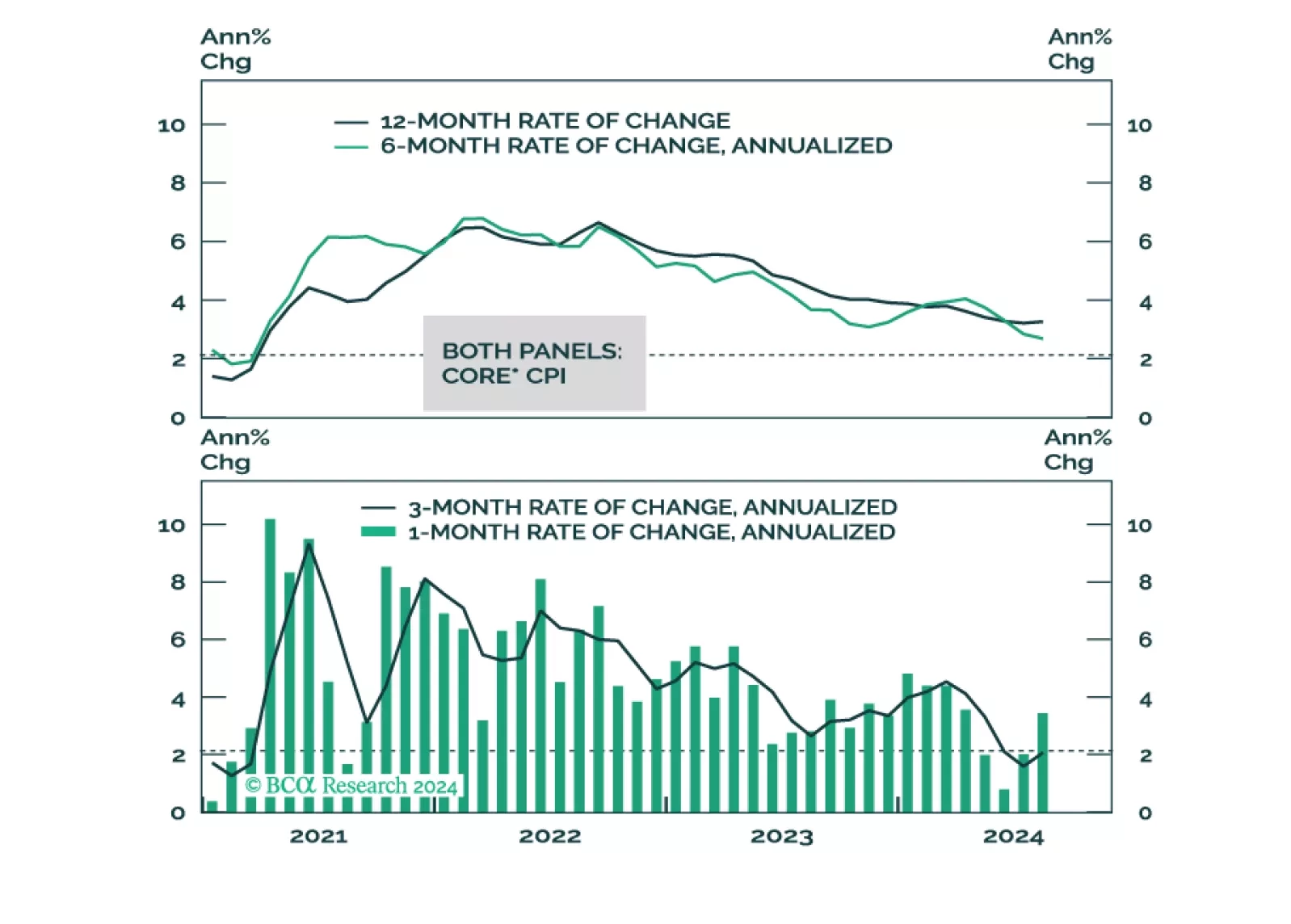

Our reaction to this morning’s CPI report and what it means for Fed policy.

The BoE embarked on its easing cycle in August, delivering its first 25 bps rate cut. The decision was nowhere near unanimous, with 5 MPCs out of 9 voting in favor of lowering policy rates. Indeed, while headline inflation is sitting right on the central…

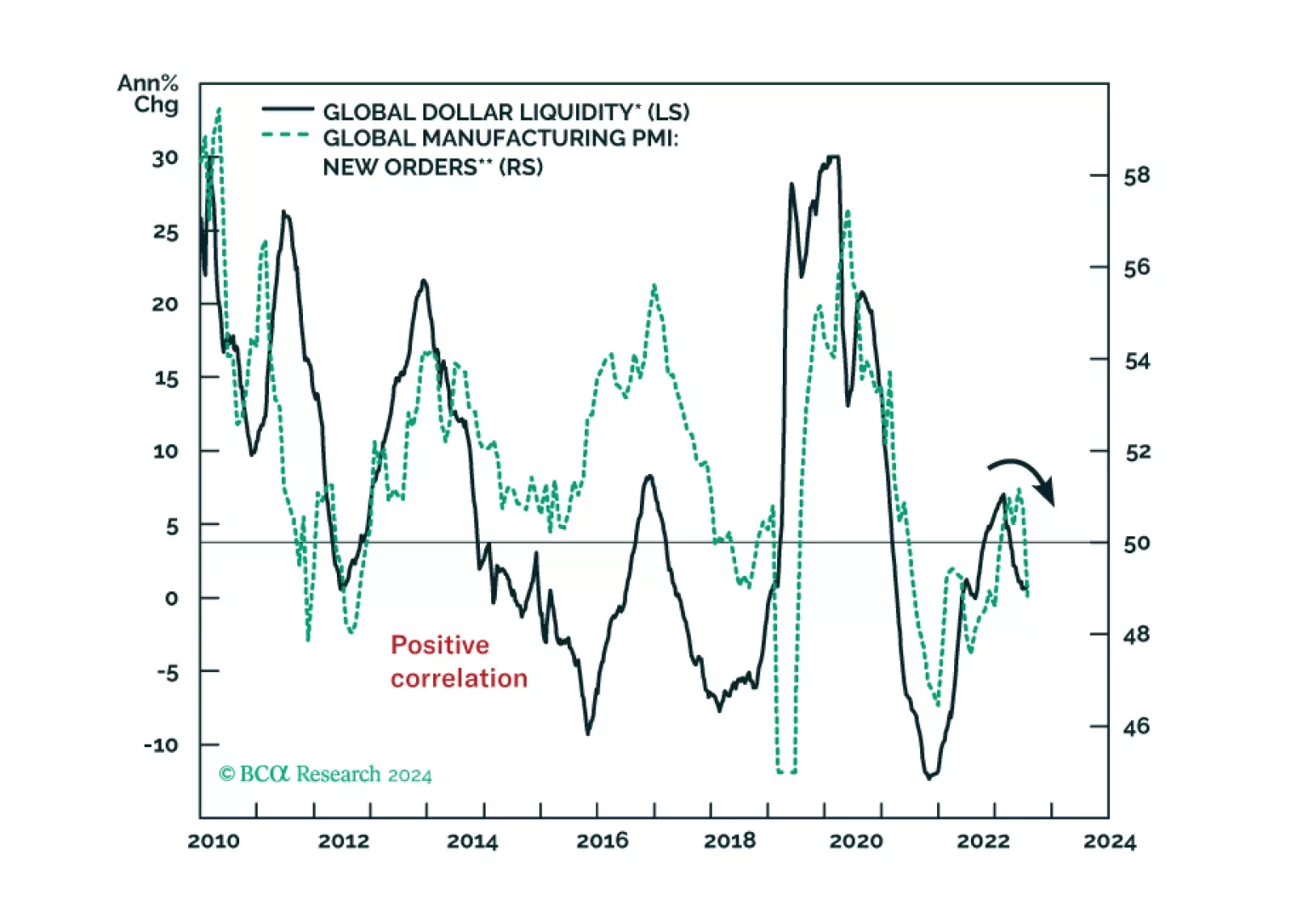

The undercurrents of global financial markets signal deteriorating global growth conditions. There is little cash on the sidelines in the US, the Euro Area, and Japan. If the budding bear market resembles the 2000-2003 one, EM stock prices are unlikely to outperform global equities in the initial leg but could outperform in the latter stage of the global selloff.

The Swedish economy’s cyclicality and sensitivity to global trade make it a reliable bellwether for global growth. Sweden is facing significant domestic weakness. Employment growth declined by 0.14% y/y in July and households’ debt burden stands at 155% of…

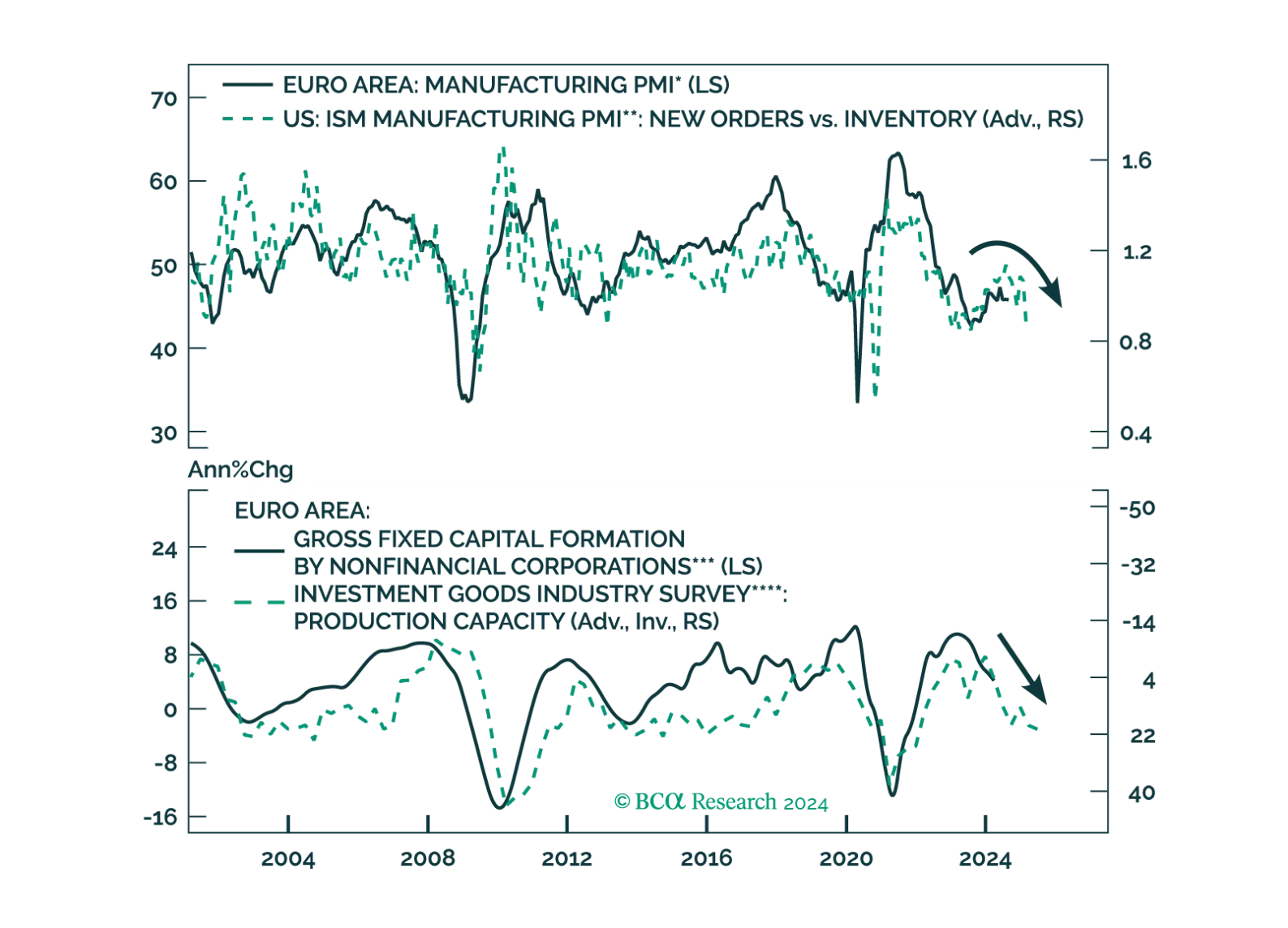

Crucial leading indicators of the global and European economies continue to deteriorate. How should investors position their European portfolios to benefit from these trends?

The pro-cyclical Eurozone economy is highly exposed to a global downturn, which we expect will materialize by early 2025. The ECB is behind the curve and we thus expect it to ease more aggressively than markets expect next year. A dovish surprise in 2025…