Fixed Income

Consistent with the risk-on environment that has dominated markets so far this year, high yield bonds have returned 4.9% YTD on a total return basis, outperforming both Treasuries (2.9%) and investment grade (3.1%). Nevertheless, our US Bond strategists…

US producer prices rose by a softer-than-expected 0.1% m/m in July, from 0.2% in June. The core measure remained unchanged, the tamest reading in four months. Notably, the index for final demand services fell 0.2% m/m. Our US Bond strategists have…

Subdued demand for credit among Chinese private-sector businesses and households persisted through July. Aggregate financing missed expectations, growing CNY 0.8bn to CNY 18.9bn in July on a YTD basis. New loans grew CNY 0.2bn to CNY 13.5bn, below the CNY…

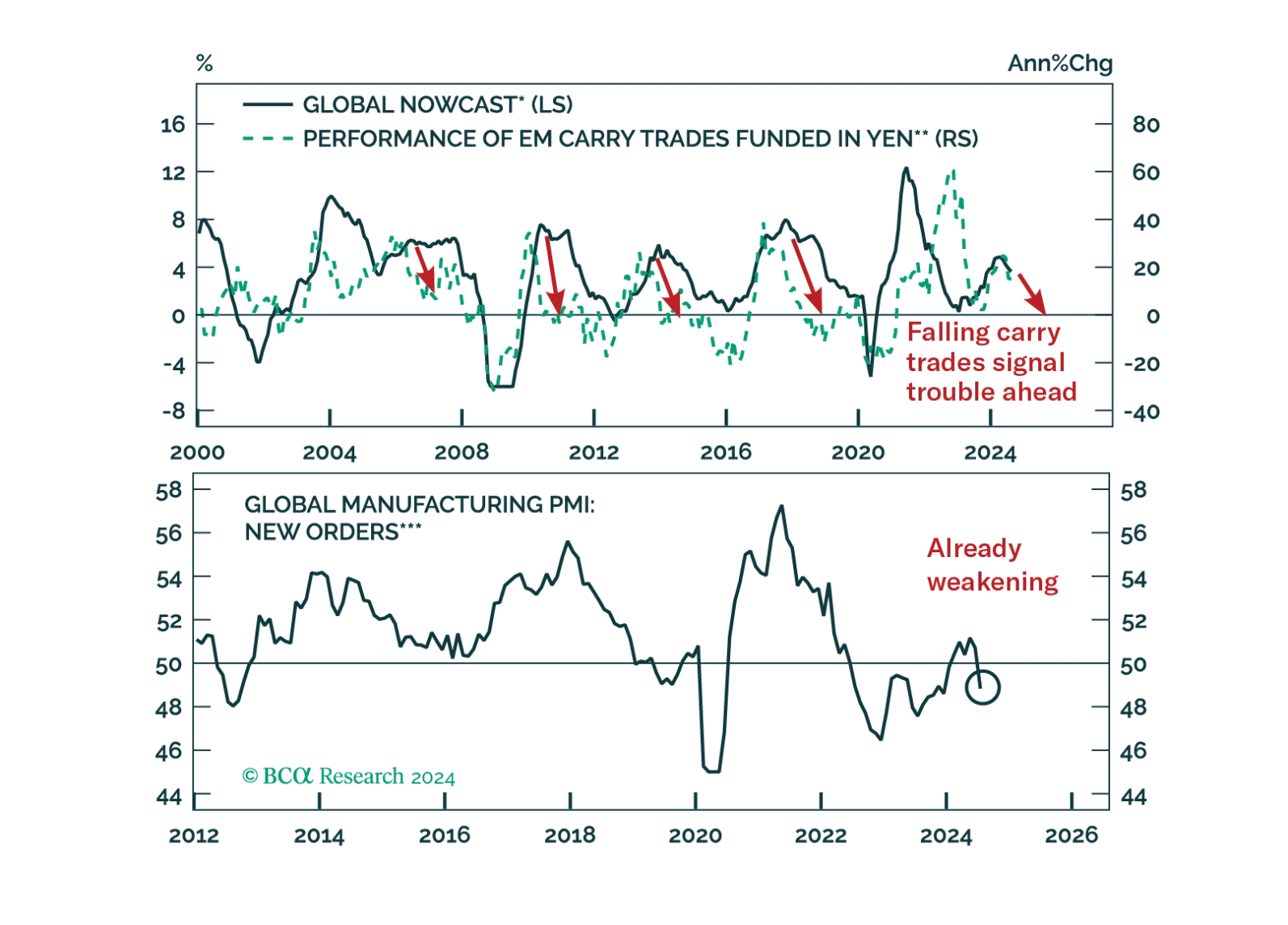

According to BCA Research’s European Investment Strategy service, investors should fade the rebound in European equities and bond yields as the euro is also at risk. Last week’s bounce in global equities is temporary. The pause in the carry trades unwound,…

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

The market backdrop changed a lot between the preparation and the publication of our equity downgrade report. We publish this companion Insight to help investors navigate the new environment.

German Industrial production and factory orders continued their slump in June. The usual powerhouse of the Euro Area economy has been trailing its peers throughout 2024. While both industrial production and factory orders surprised to the upside in June,…

The prices of multiple financial assets have failed to break above their technical resistances. When this occurs, a breakdown ensues. In brief, global risk assets remain vulnerable. We are upgrading Chinese onshore stocks from neutral to overweight and offshore ones from underweight to neutral within EM and global equity portfolios.

According to BCA Research’s US Bond Strategy service, Friday’s employment report caused financial markets to price-in some recession risk for the first time in months. The Treasury curve bull-steepened in July, a move that accelerated after Friday’s negative…

Our Portfolio Allocation Summary for August 2024.