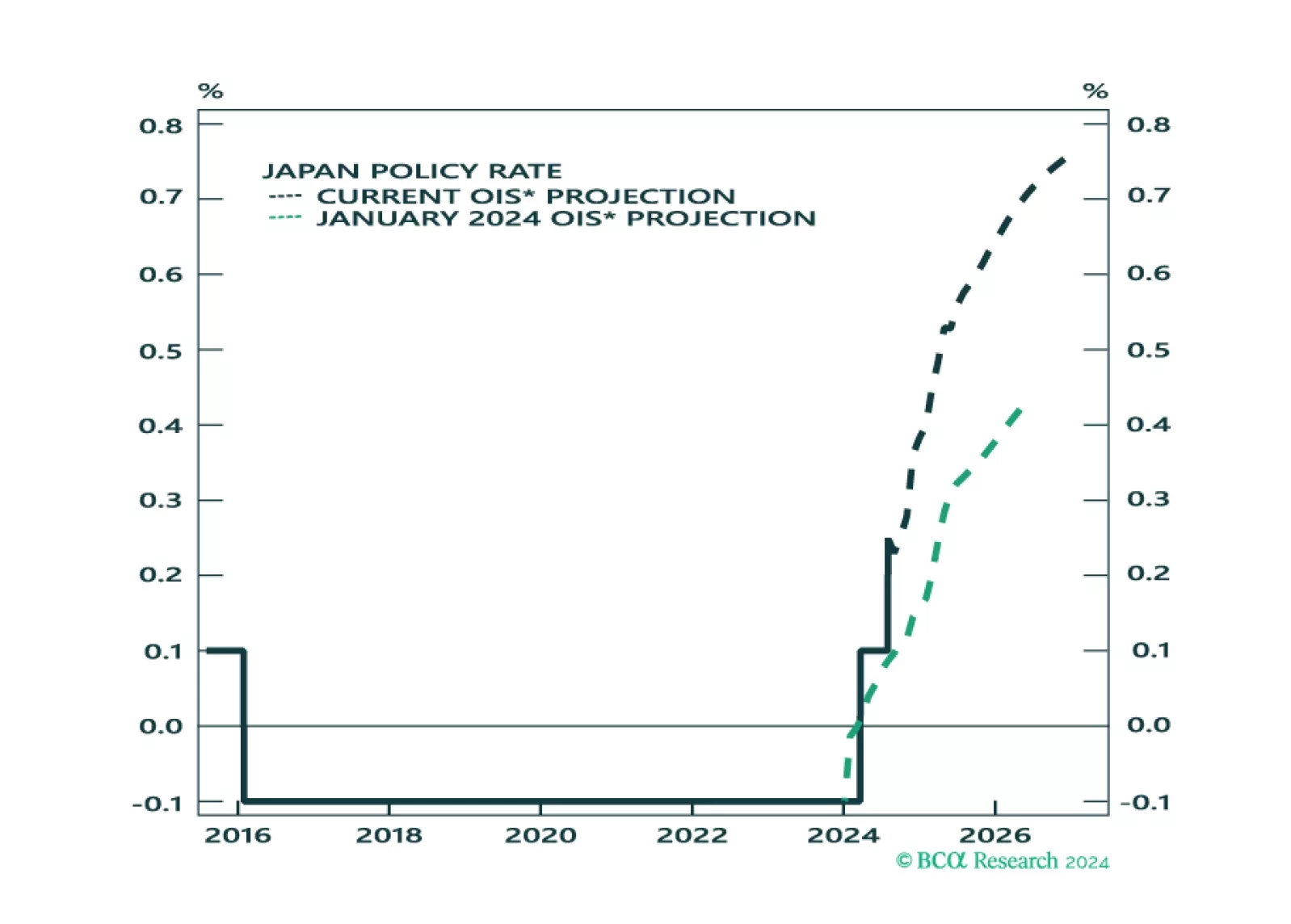

Fixed Income

We assess the investment implications of the BoJ and Fed meetings, and give our take on the next policy moves. We also assess the impact on asset markets.

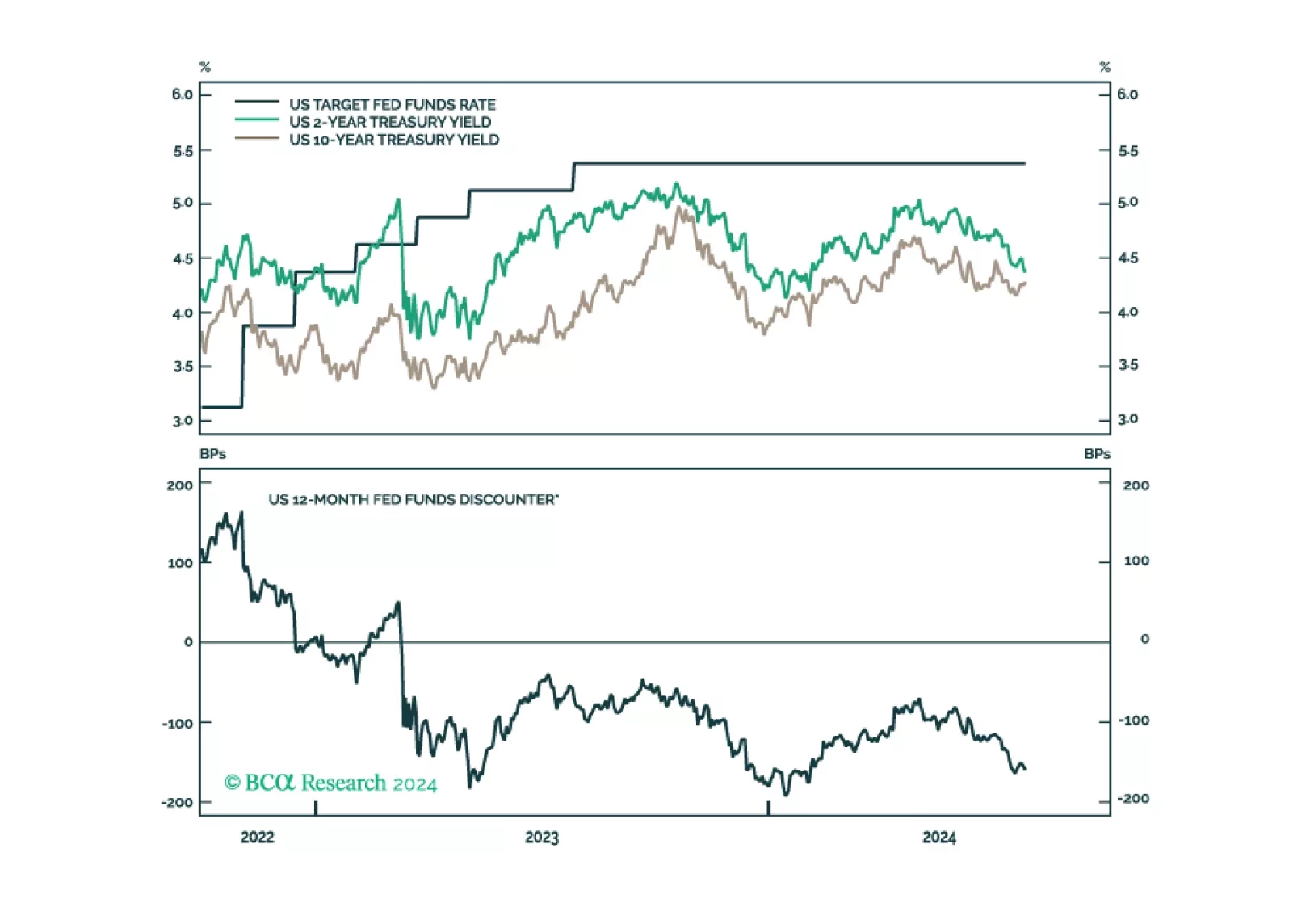

The Fed kept rates steady today, but teed up an initial rate cut in September while putting more emphasis on the employment side of its dual mandate.

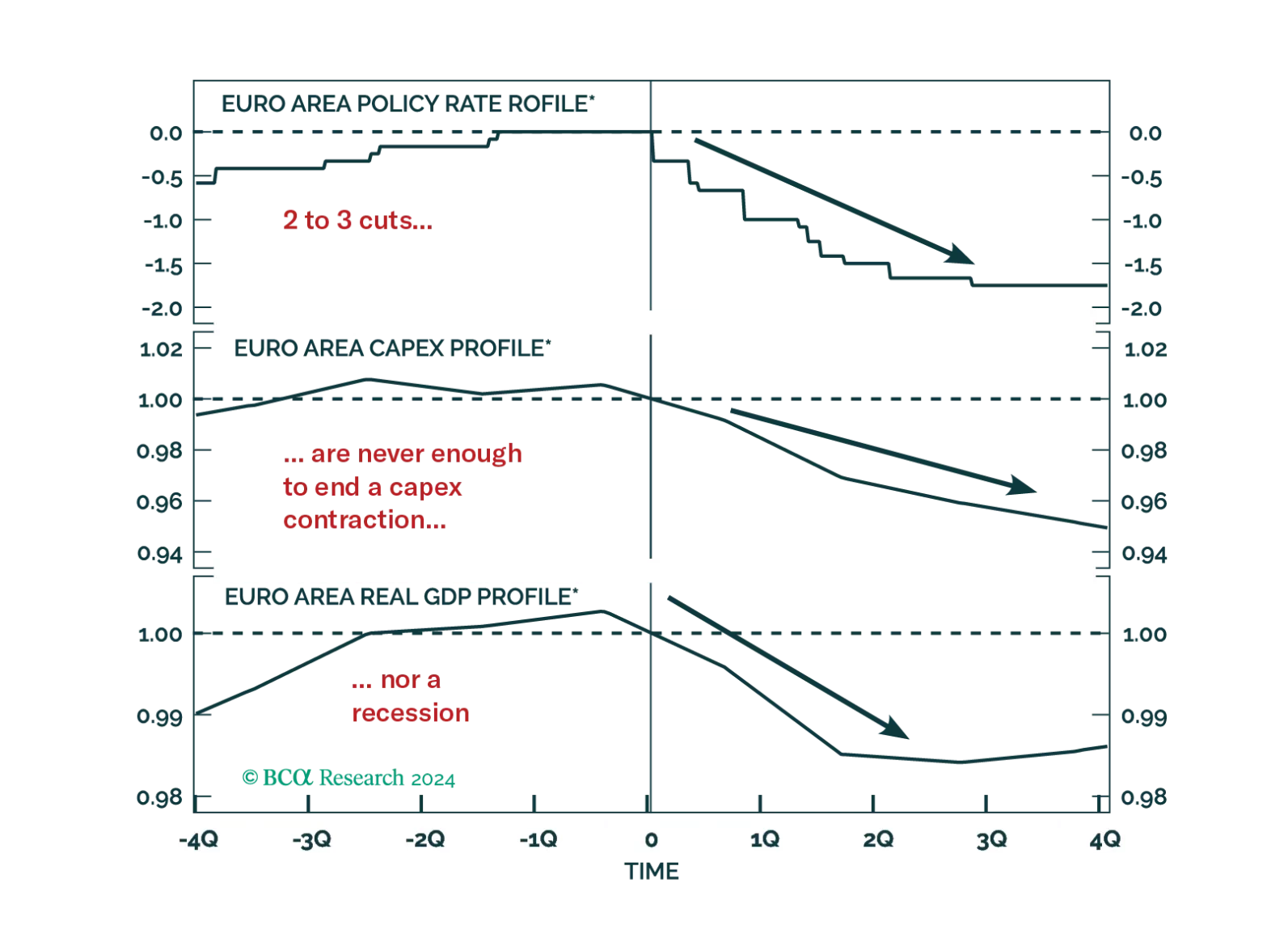

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

This report takes a look at bond and FX market technical indicators and calibrates the decision to increase portfolio duration and get long the US dollar.

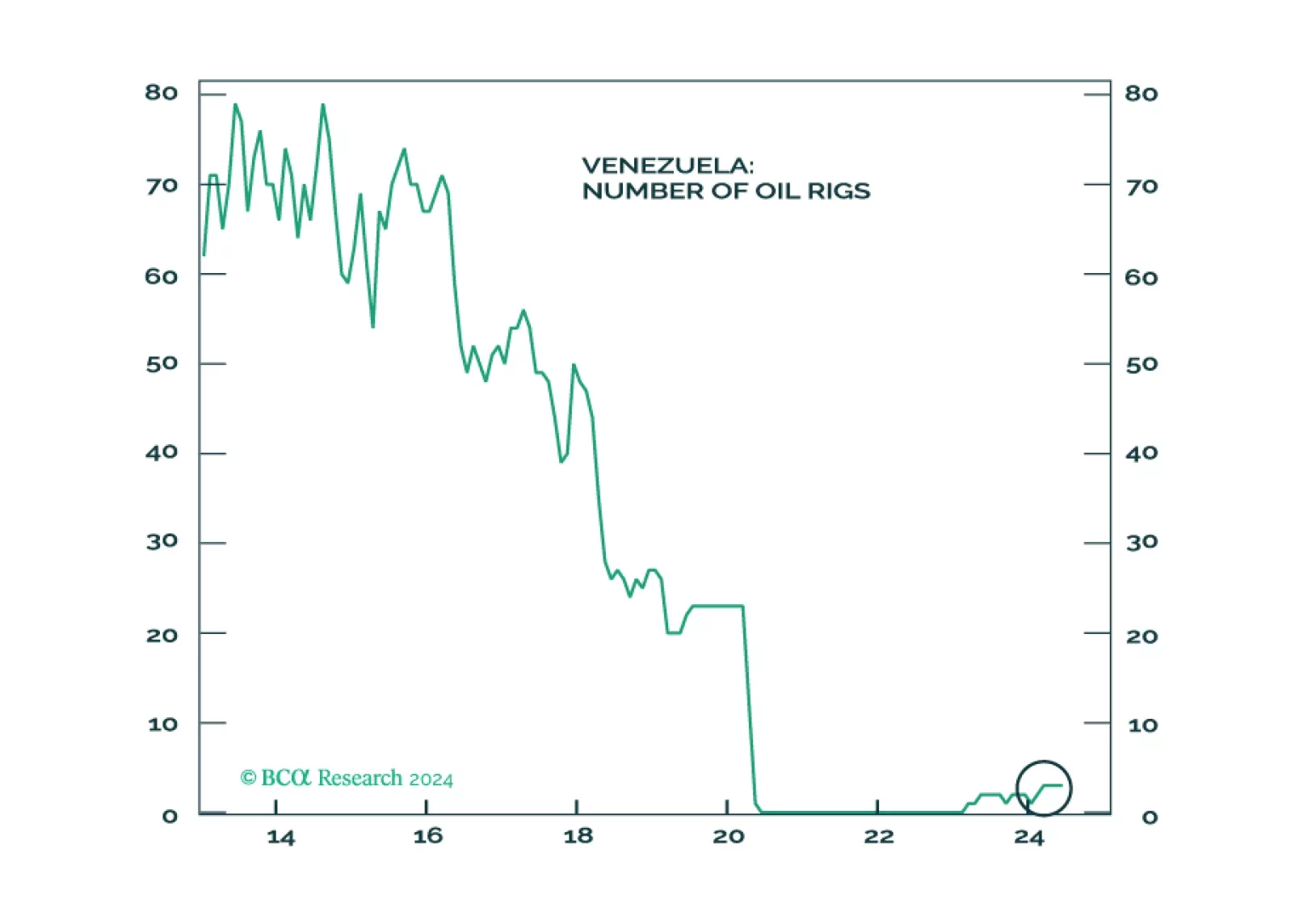

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

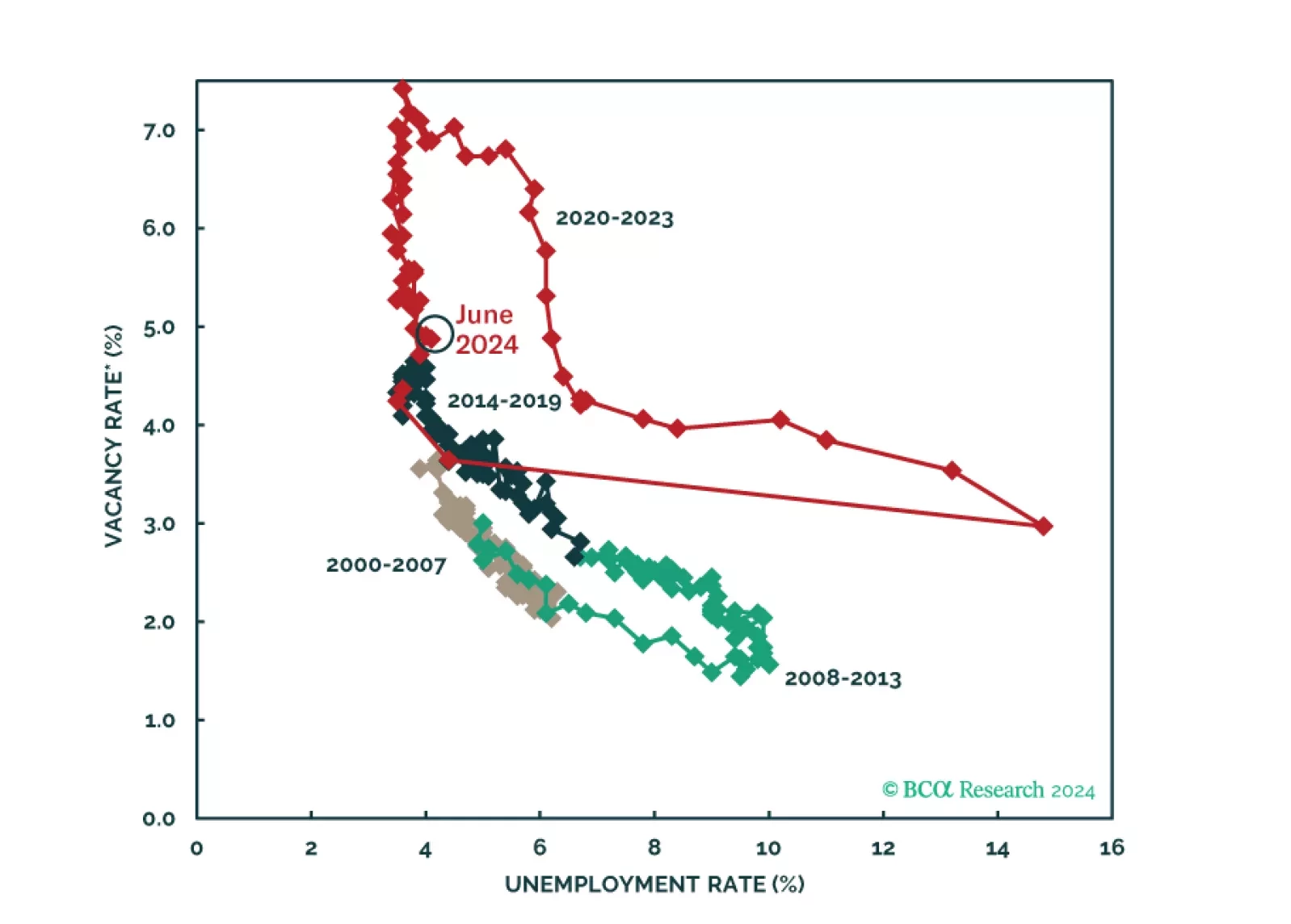

After this morning’s jobless claims number, we have now seen enough deterioration in our preferred labor market indicators to increase portfolio duration from “at benchmark” to “above benchmark”.