Fixed Income

Our outlook for Fed policy in 2026.

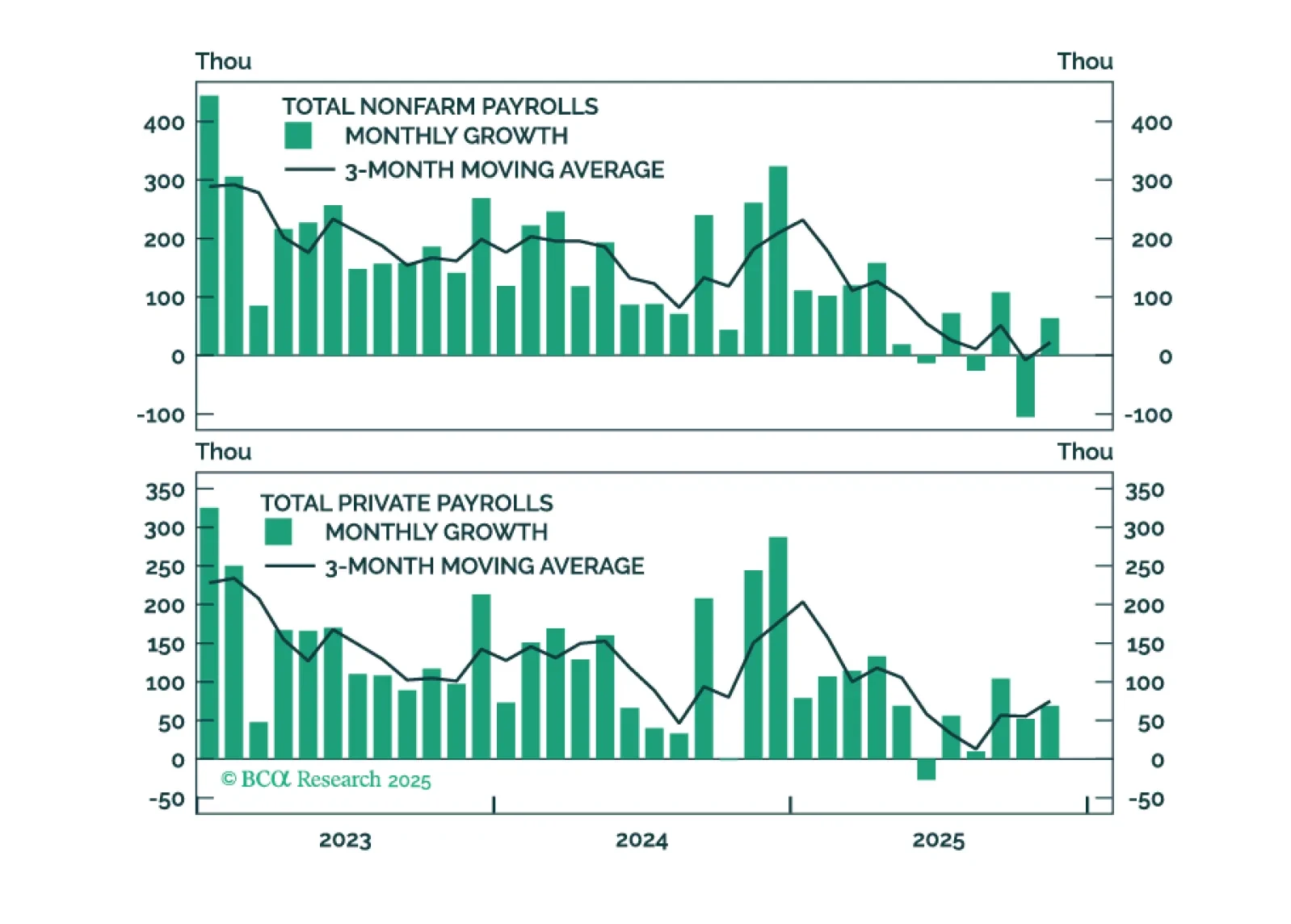

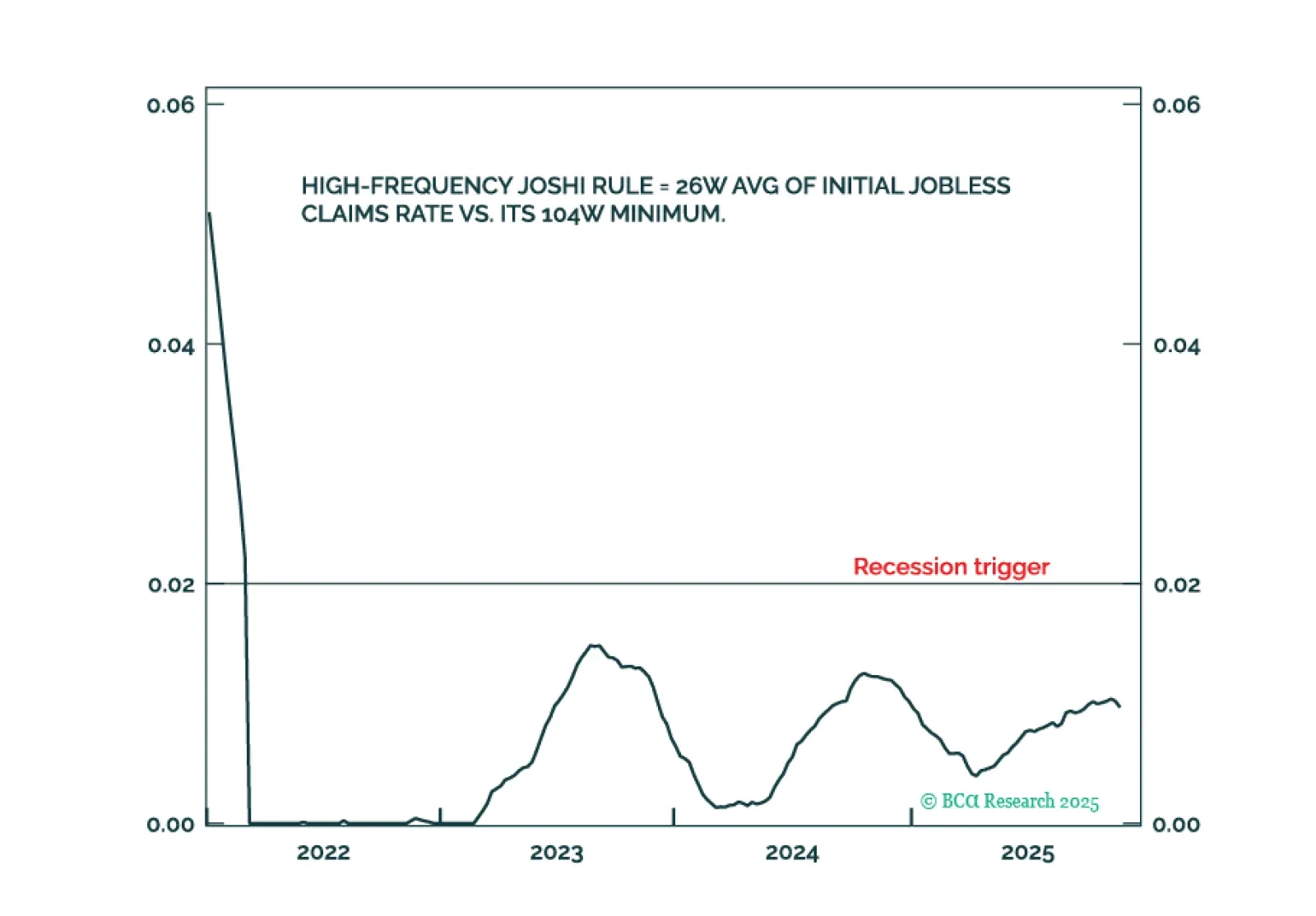

Employment Data Point To Dovish Policy Surprises In 2026

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

The bull versus bear battlelines are drawn for 2026: The friendliest Fed meets the most concentrated stock market rally ever. This last report of the year goes through the 10 key views for 2026 that emanate from this fascinating setup.

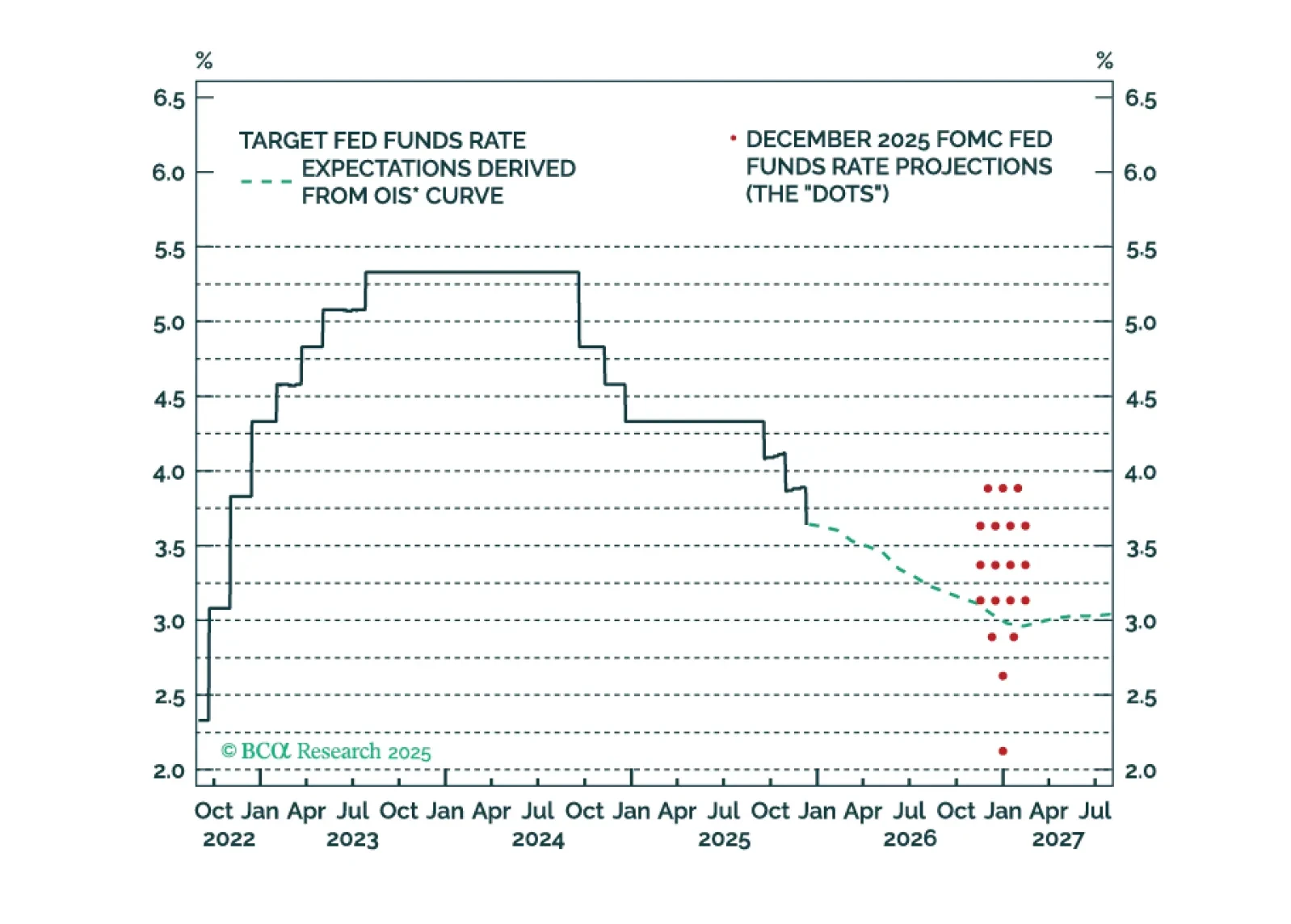

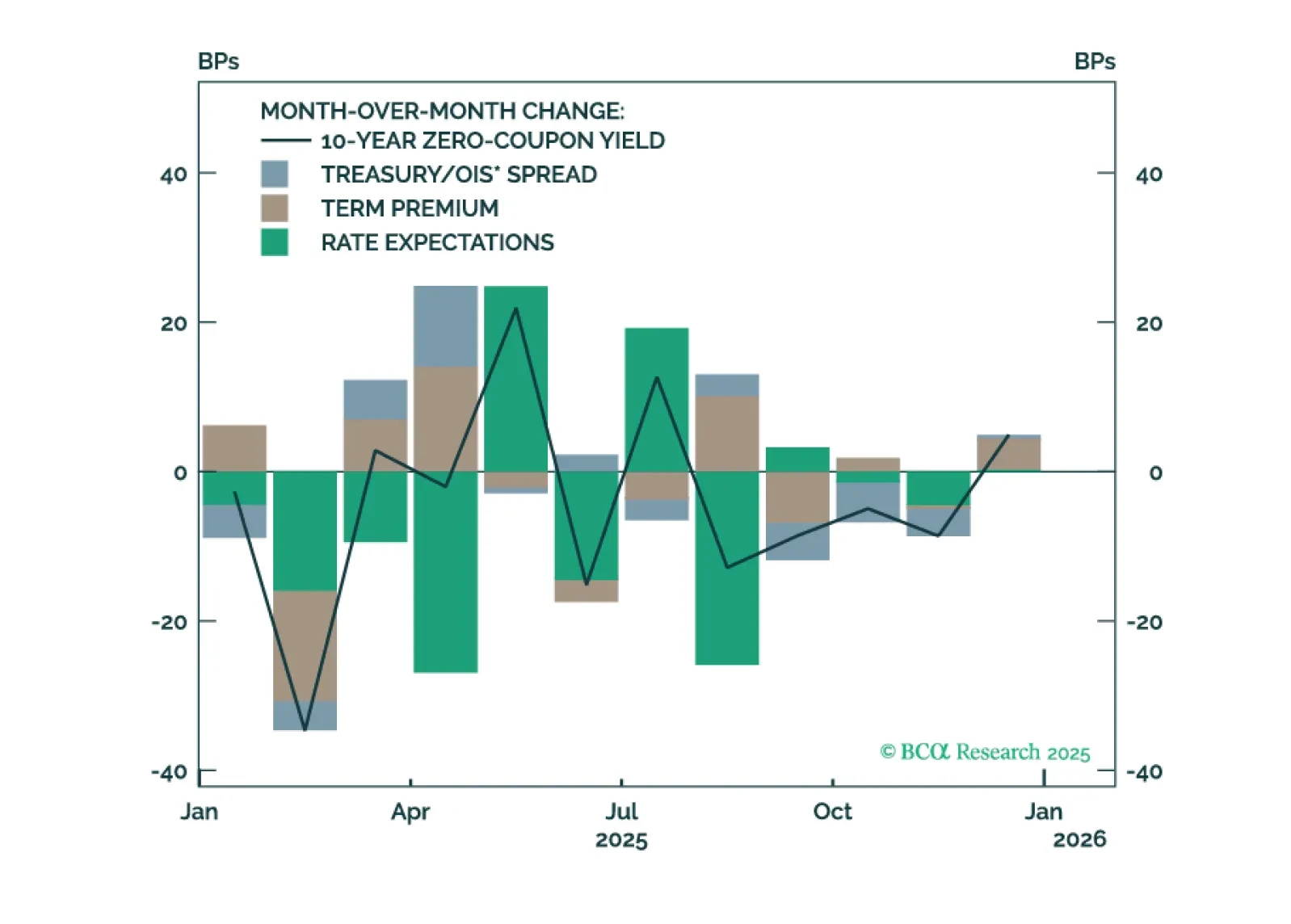

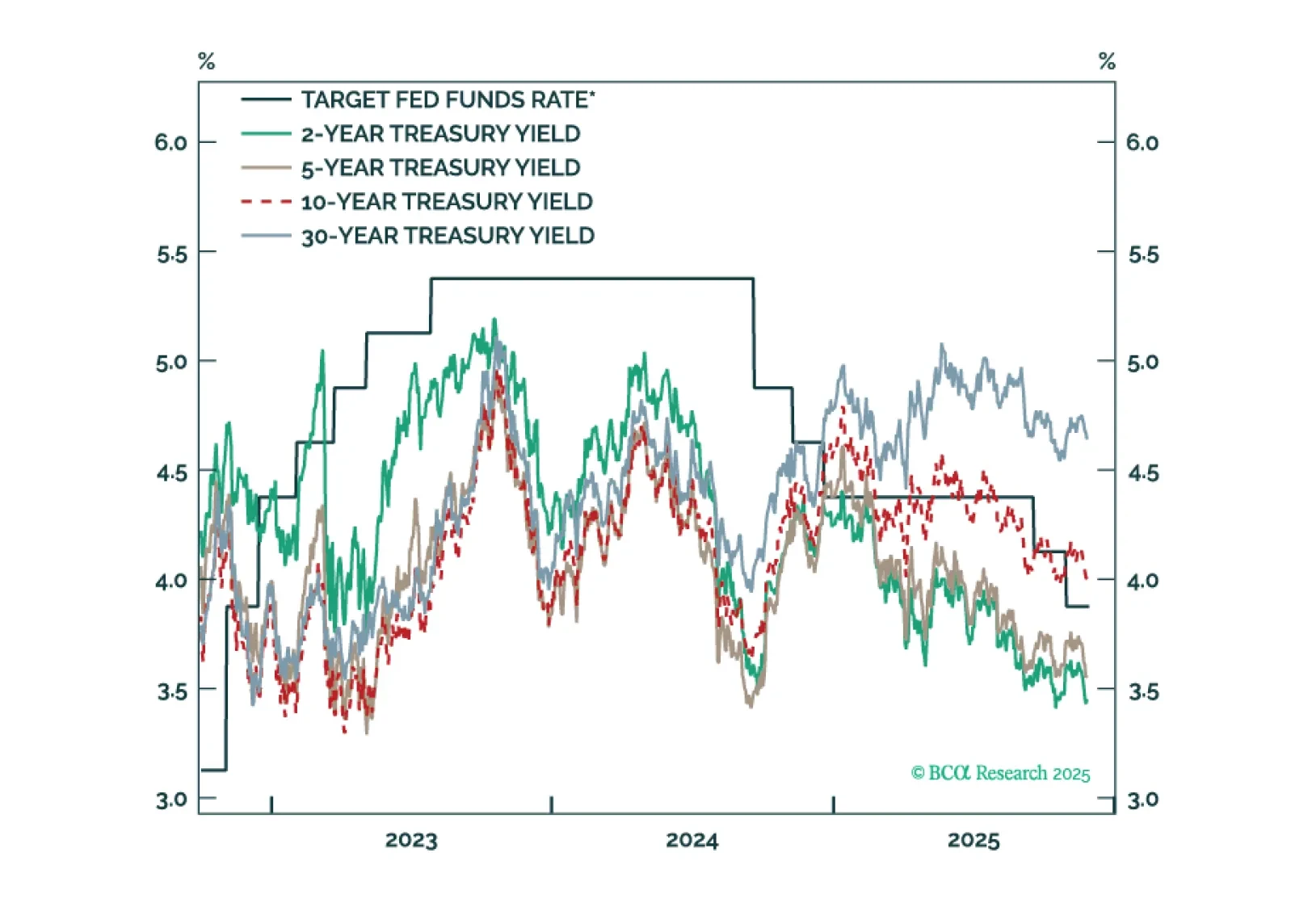

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

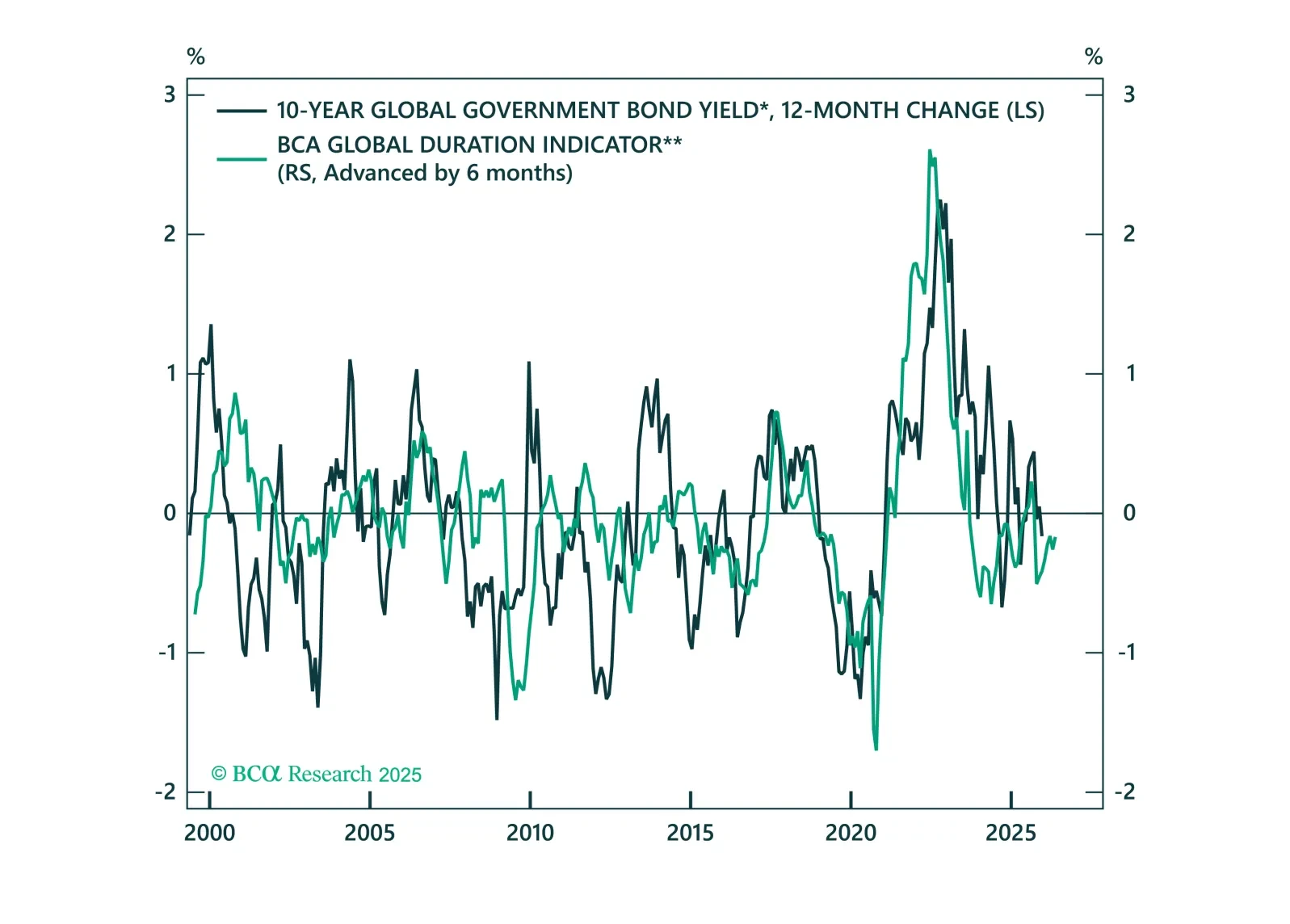

We present our five key views for global fixed income markets in 2026. A year that will see the global easing cycle come to an end.

Our Portfolio Allocation Summary for December 2025.

The high-frequency Joshi Rule confirms that the US labour market is holding up. Equity investors should regard 5-10 percent selloffs as tactical buying opportunities. Bond investors should stay underweight US duration. Plus, a new high-conviction trade is to go overweight the 30-year German bund versus the 30-year US T-bond.

Our key US fixed income views for 2026.

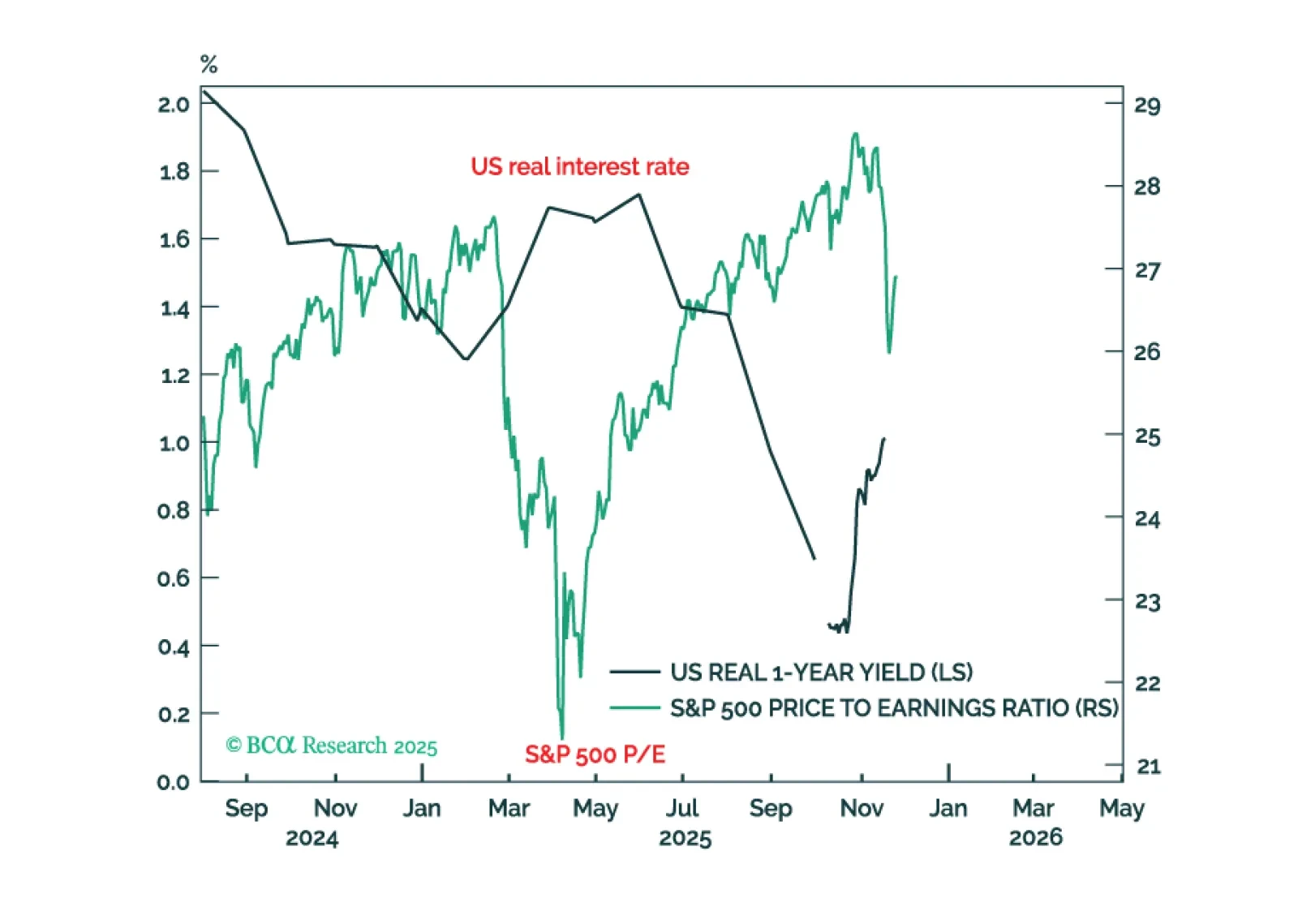

Stock market valuations are moving as a near-perfect mirror image of the US real interest rate, meaning that the Fed is underpinning the stock market. But if the market stopped believing in AI-driven profits growth, valuations would collapse, irrespective of the Fed’s efforts to underpin them. When might this happen? Plus, two new tactical trades are: long BTC versus gold; and overweight industrials.