Fixed Income

The idea that rising interest rates benefit value at the expense of growth has become consensus amongst market participants. The rationale is simple: Most of the cashflow that shareholders will receive from growth stocks are farther into the future than…

In this report, we review our trade recommendations based on incoming data in the last month.

US initial jobless claims increased from 209 thousand last week to 231 thousand, surpassing expectations of 212 thousand. Moreover, continuing claims also surprised to the upside, increasing from 1.768 million to 1.785 million. Nearly half of the rise in…

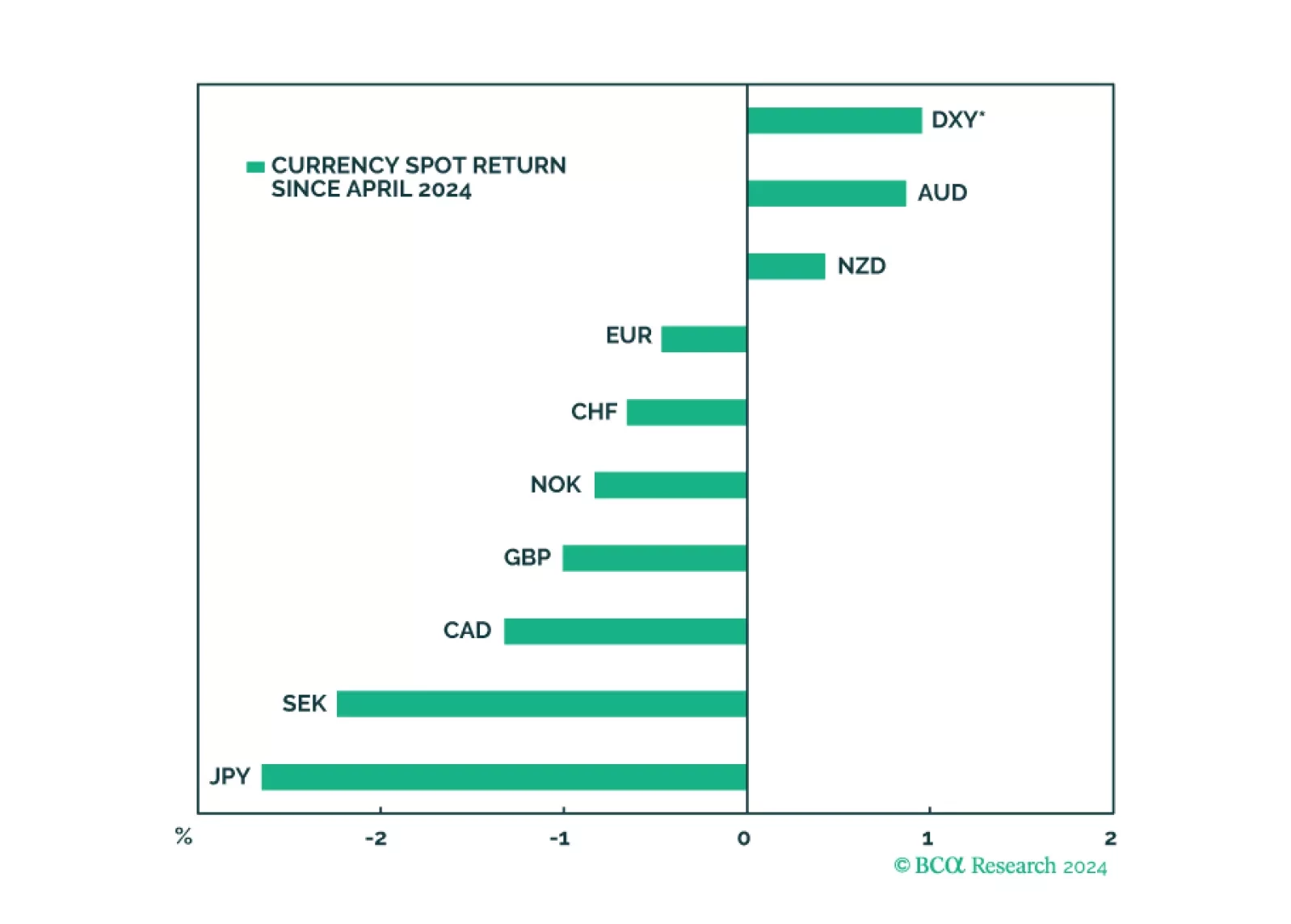

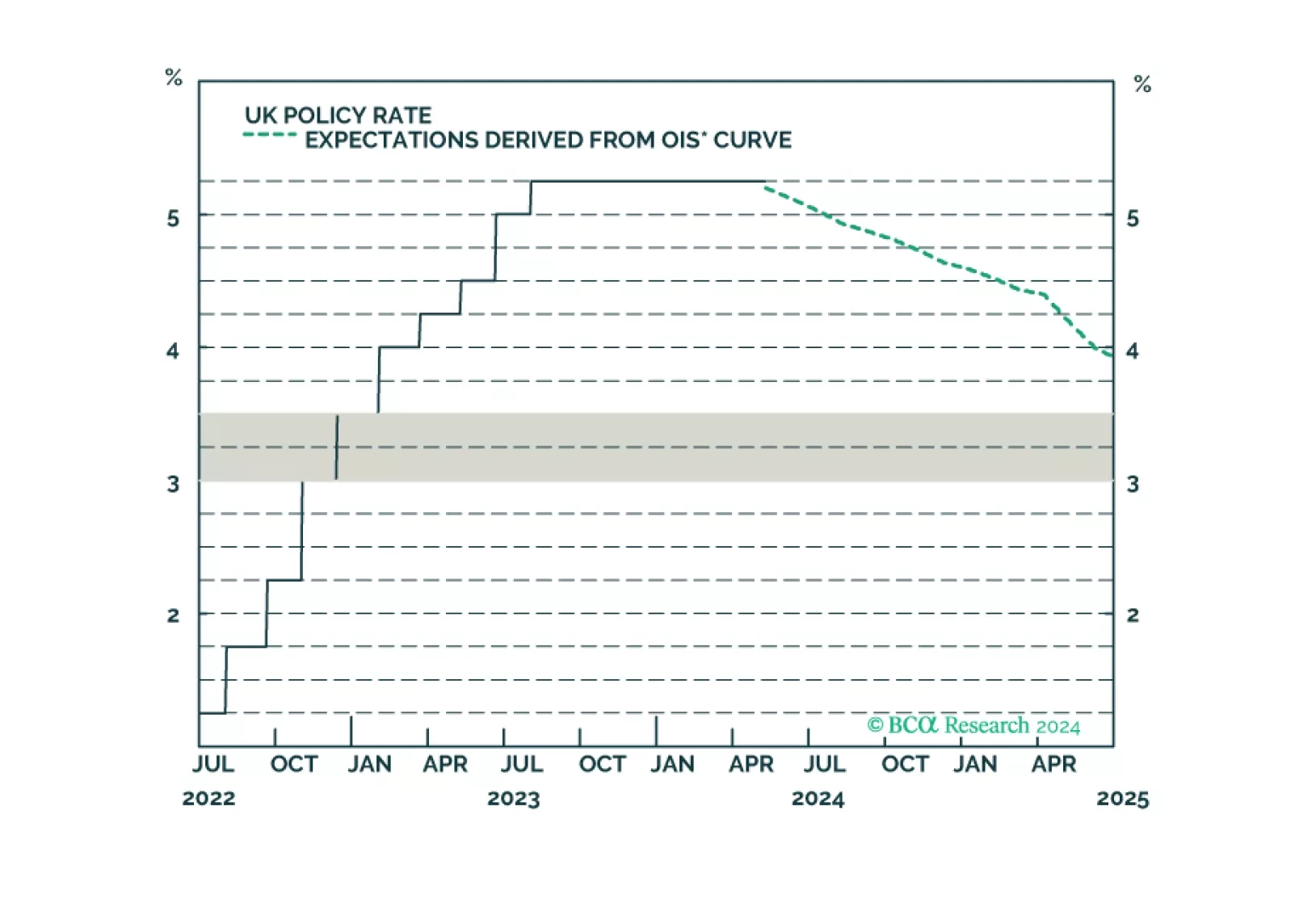

In a widely expected move, the Bank of England (BoE) maintained its policy rate at 5.25% in May. Nevertheless, two Committee Members voted in favor of cutting rates, one more than was anticipated. The tone of the report was overall dovish. The BoE…

An update to our views on UK rates and currency following today’s Bank of England meeting.

The revival in global growth momentum continued in April. The JPM Global Manufacturing PMI came in at 50.3, marking its third consecutive month of expansion. Details underscored solid demand conditions. Output and new orders continued to rise and new…

According to BCA Research’s US Bond Strategy service, investors should look to the stock-to-bond ratio to time the breakout in yields. The strong positive correlation between stock and bond returns has been a consistent feature of the inflationary…

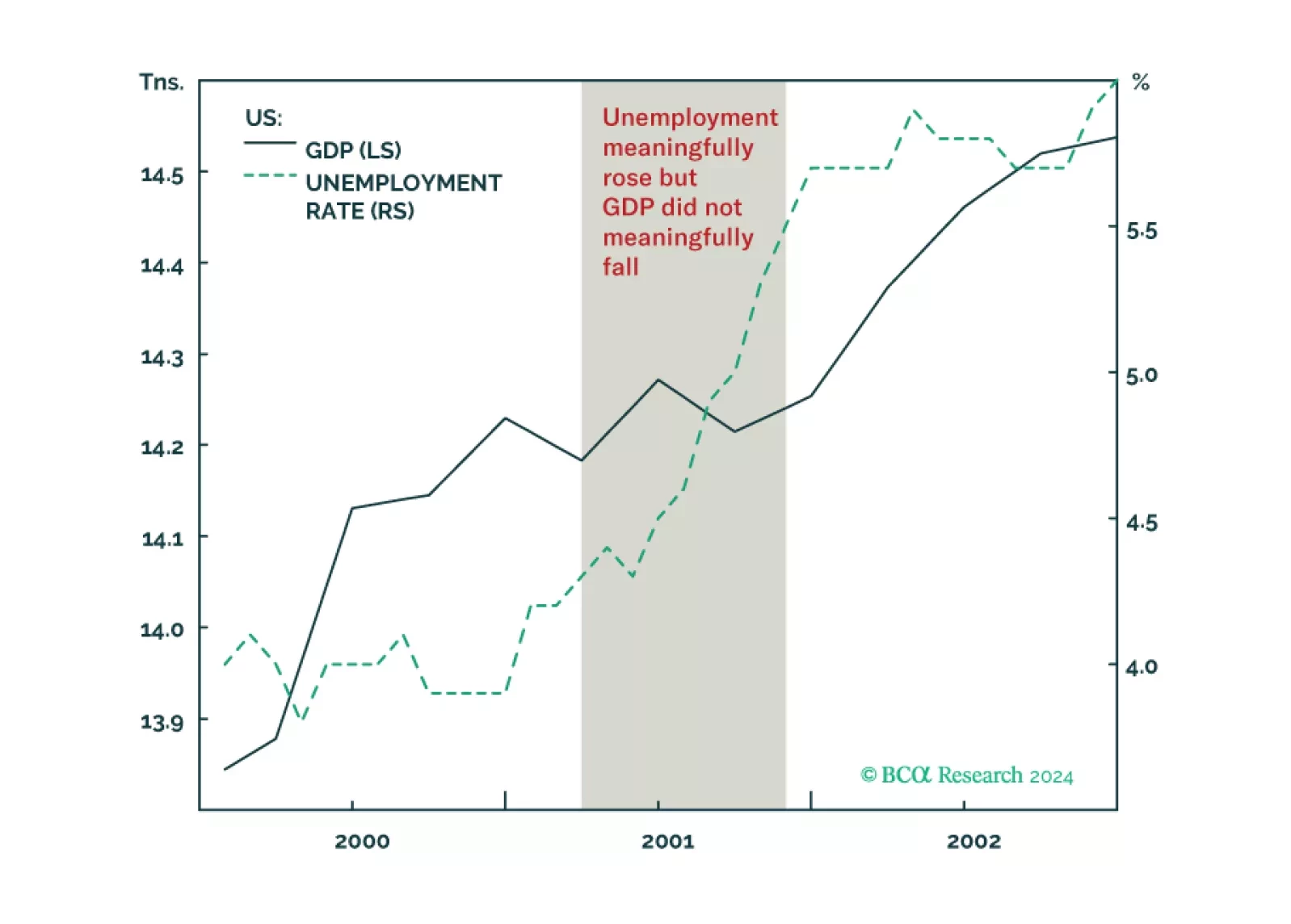

Why the US could get a jobs recession without a GDP recession, as happened in 2001, and what it means for stocks and bonds. Plus, an update on the Joshi rule.

The Reserve Bank of Australia (RBA) left its policy rate unchanged at 4.35% at its May meeting, in line with expectations. The statement highlighted that inflation continues to moderate, though at a slower-than-expected pace. Board members also pointed out…

Transit through the Suez Canal has hit a new low. The 7-day moving average of daily ship transit calls is currently at 30, less than half of what it was at the end of 2023. The decline in volume has been even more severe, with metric tons passing through the…