Fixed Income

Gold prices reached $2300 per ounce for the first time on Wednesday. They have now rallied by more than 12% so far this year. To a degree the furious rally in gold has been puzzling. Who has been buying? It certainly has not been private investors. Global…

Our reaction to this morning’s employment report and bond market moves.

It is too early for the RBA to begin cutting rates. Inflation remains above target, with core CPI currently standing at 3.4%, one of the highest numbers amongst major economies. The labor market is also fundamentally strong. Australia’s unemployment rate…

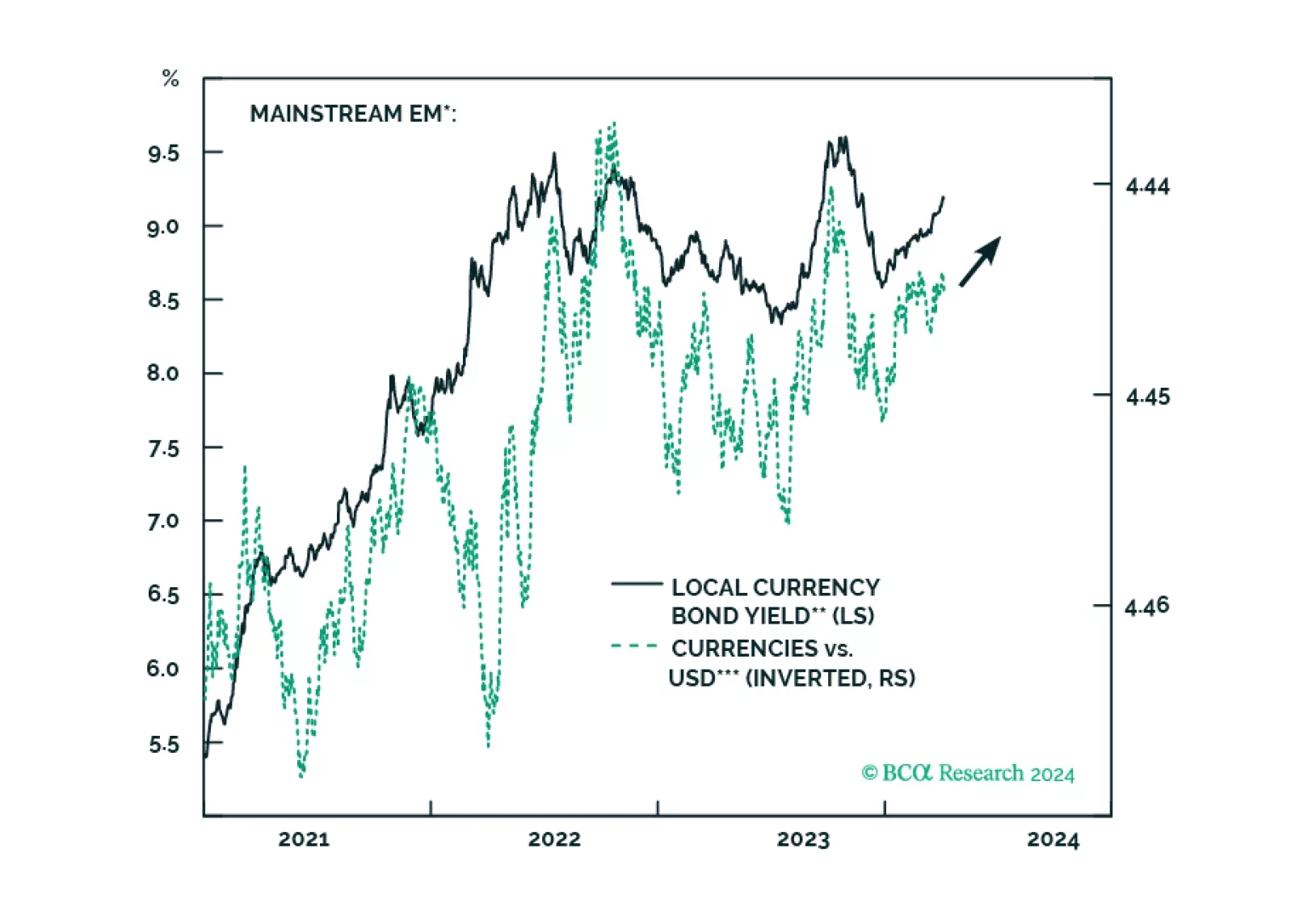

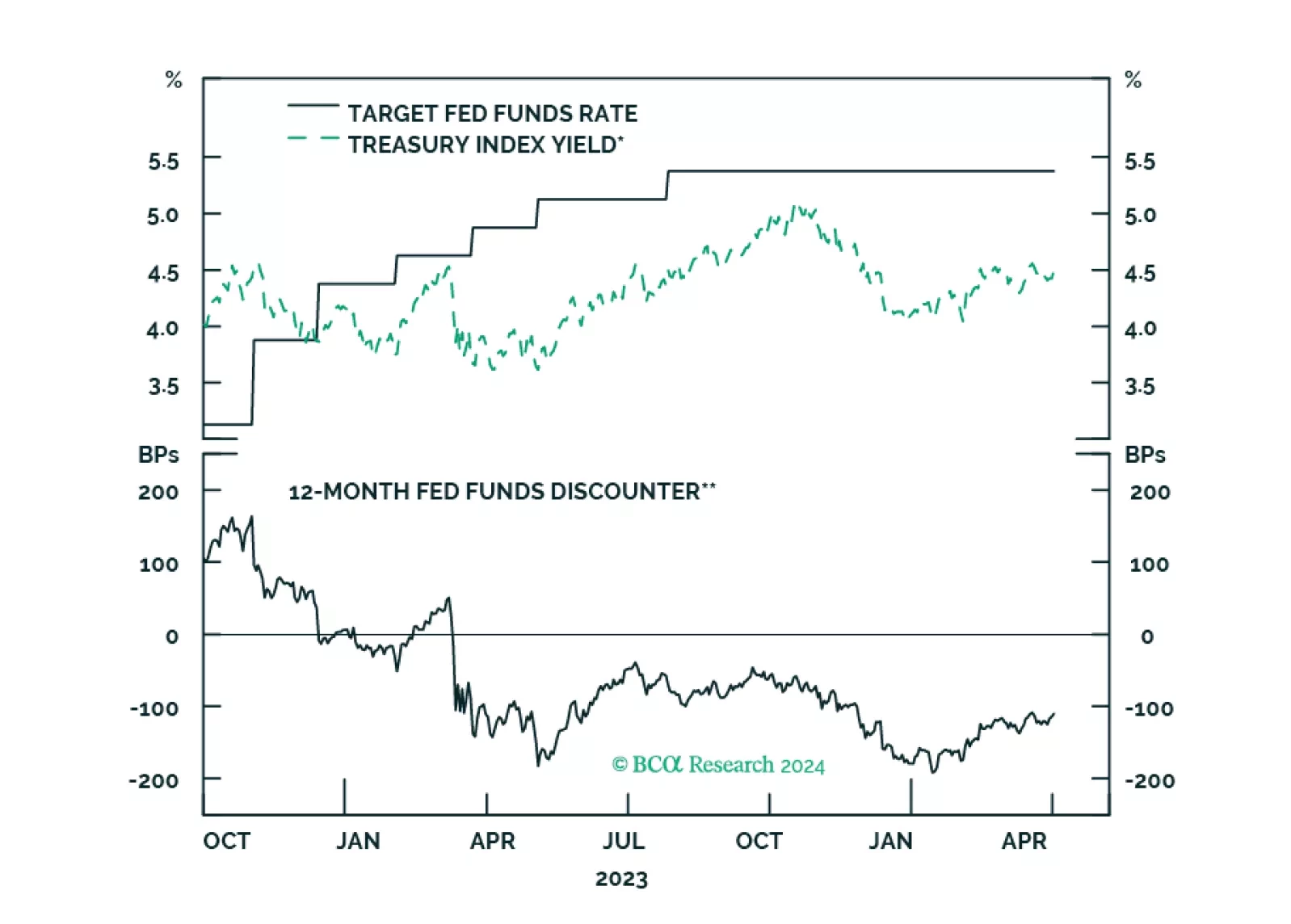

Climbing US bond yields, alongside higher oil prices, might spoil the party for global risk assets. There are budding cracks in EM domestic bonds, and even though we like this asset class in the long run, investors exposed to it should reduce their positions for now.

Flash estimates for Euro Area inflation in March surprised to the downside. Headline inflation slowed from 2.6% to 2.4% versus expectations of 2.5% and core inflation eased from 3.1% to 2.9% versus expectations of 3%. While the stickiness of services…

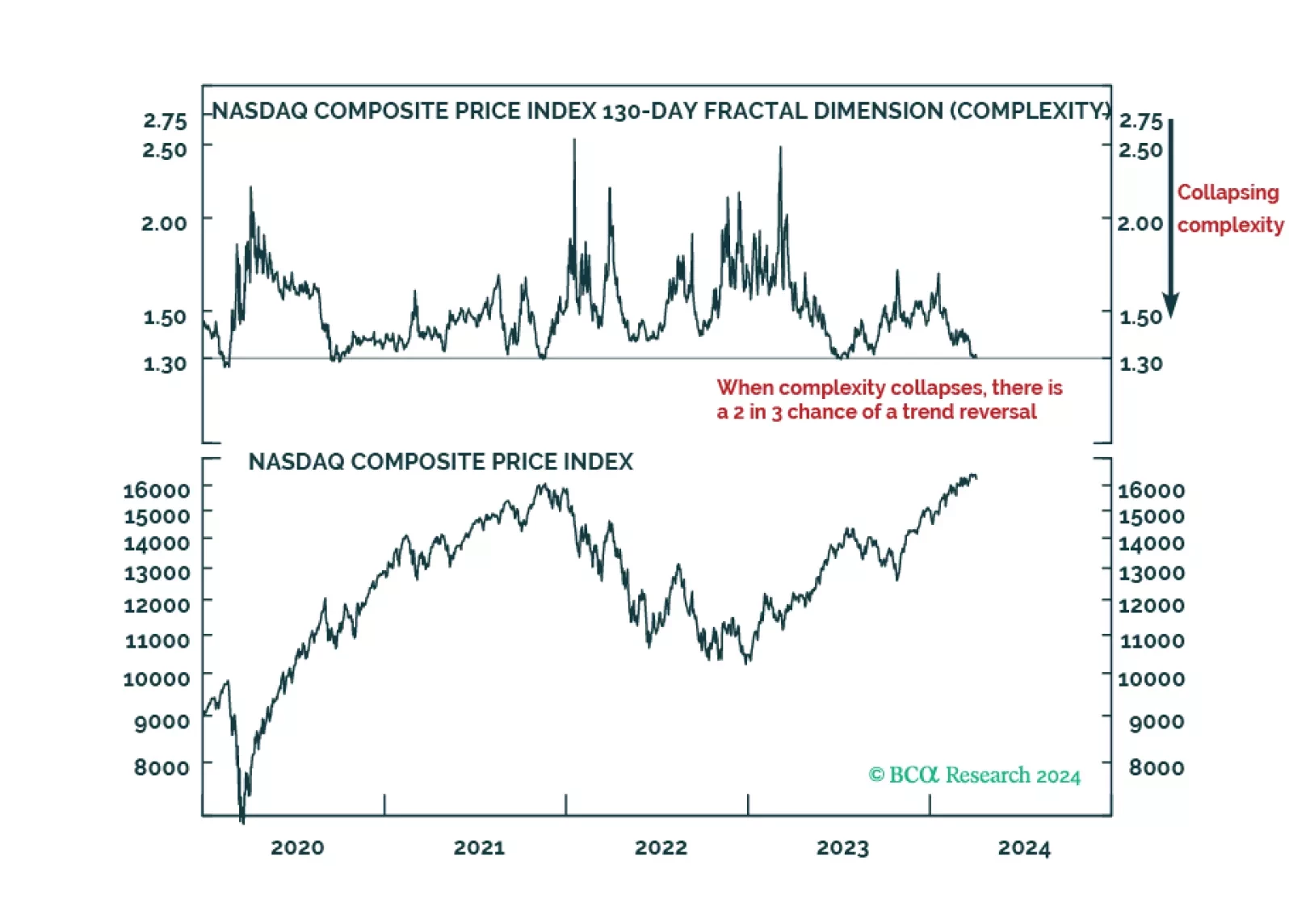

The analysis of complexity is a massive competitive advantage in investing, and from today, clients will be able to monitor the complexities of the world’s 17 major investments on our webpage in real-time.

The Dallas Fed released its trimmed mean PCE inflation rate for February on Friday. The trimmed mean PCE is a measure of underlying inflation which excludes the top 31% and the bottom 25% of the PCE basket and then uses a weighted average of the remaining…

Our Portfolio Allocation Summary for April 2024.

The Bank of Canada released its Business Outlook Survey for the first quarter of this year on Monday. While there are some early signs of stabilization, overall demand continues to be weak. The indicator for future sales growth remains well below its…

The soft-landing narrative dominated the behavior of financial markets in March, with most major global risk assets posting above average returns. In particular, the burgeoning ‘risk on’ sentiment led to a rally across global equity markets. On this front,…