Fixed Income

The latest Canadian data suggest that although demand is cooling down, the Canadian economy is not in freefall. The unemployment rate fell for the first time since December 2022, declining by 0.1 percentage points to 5.7%, compared to consensus…

Our Emerging Markets team believes that the risk-reward profile of the US dollar remains very attractive. First, if US growth stays robust, US interest rate expectations will rise because rate cuts priced in will not be realized. Rising interest rates will…

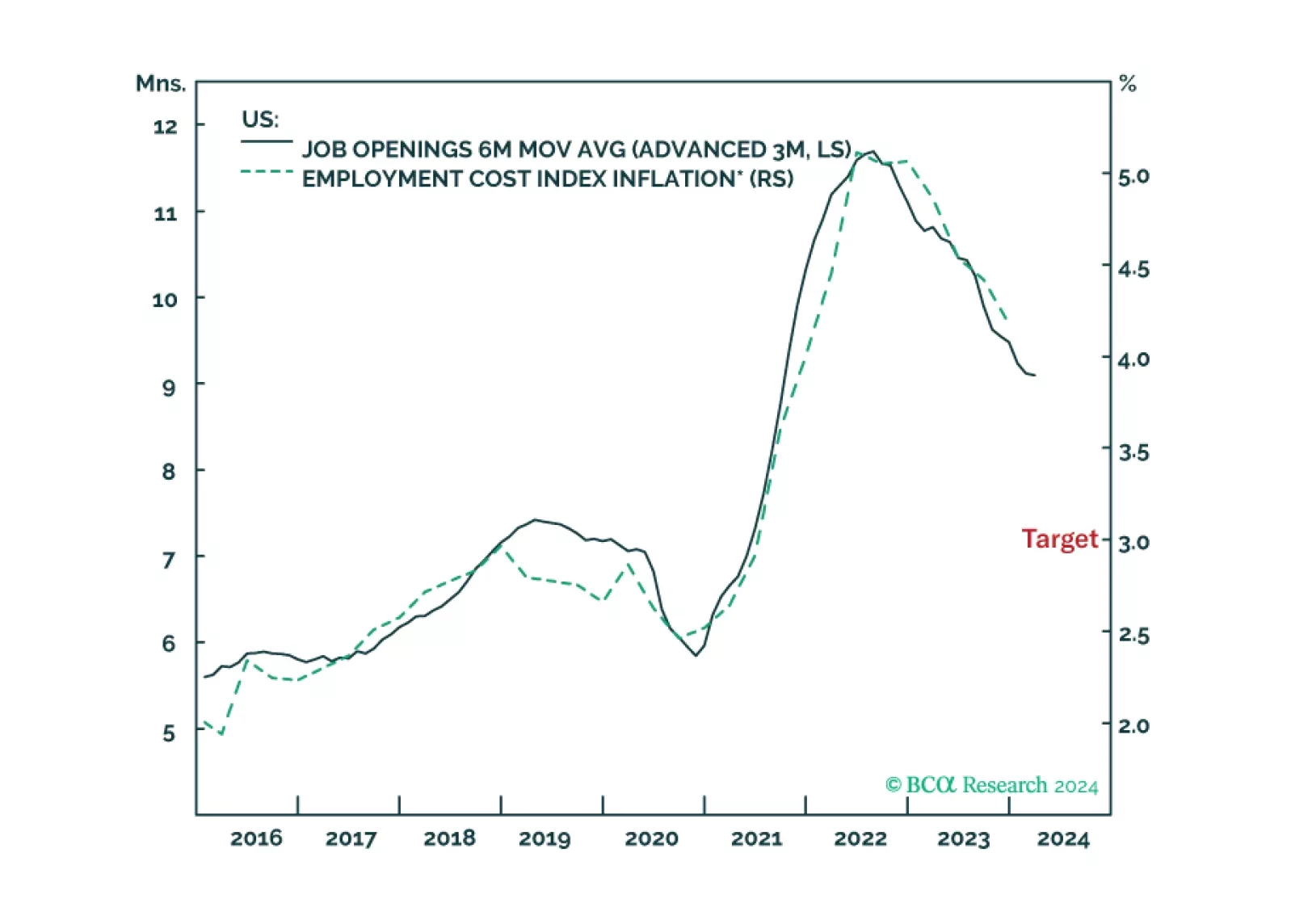

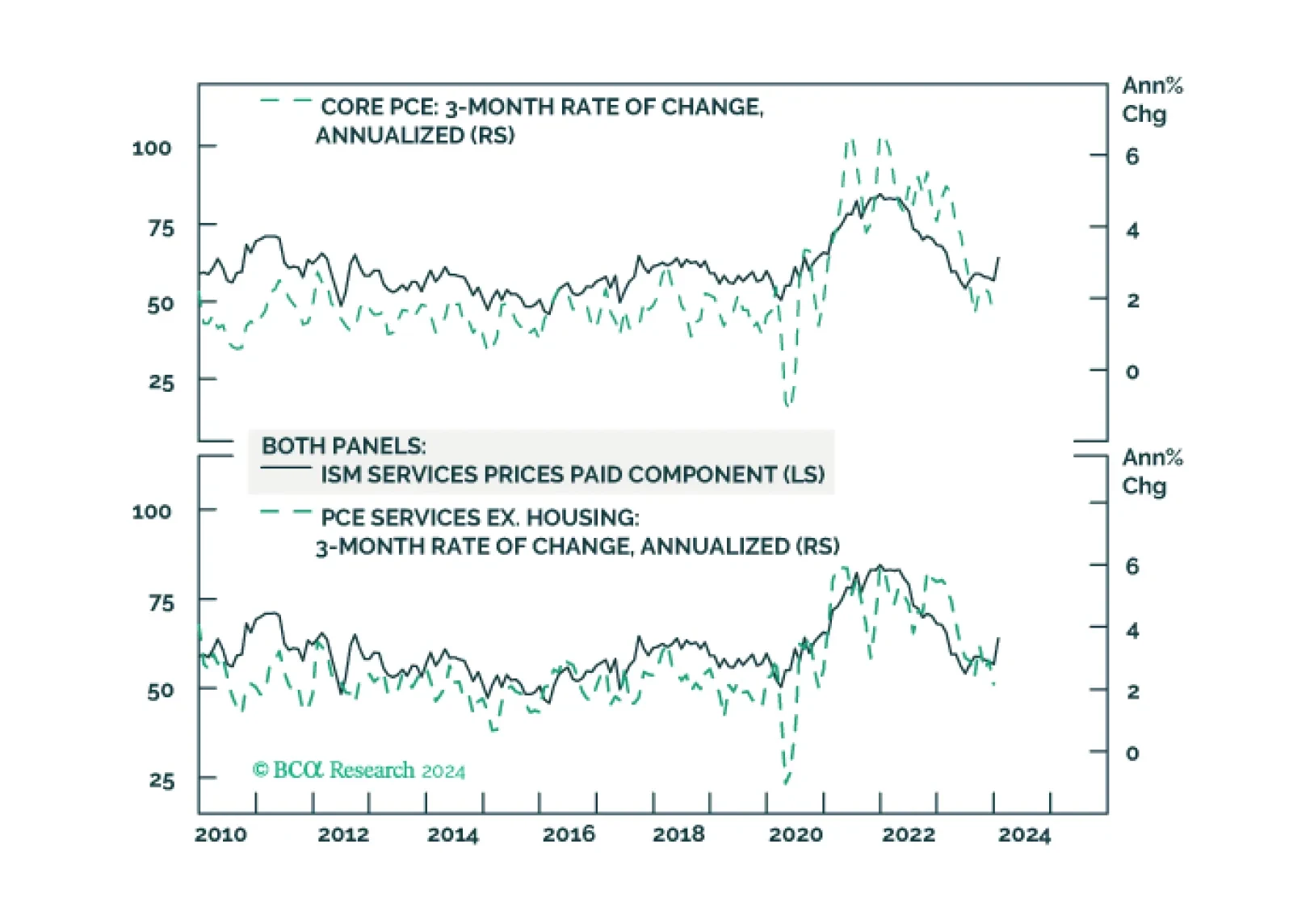

The disinflation to date has been benign because it has come almost entirely from improving supply. But the supply-side tailwind has exhausted, so the last mile of the journey to 2 percent inflation will be the hardest, especially in the US and the UK. We discuss the investment implications. Plus, we highlight an interesting sector pair-trade.

As expected, the Reserve Bank of Australia kept the policy rate unchanged at 4.35% on Tuesday. The updated economic forecasts show a downward revision to the growth outlook for this year versus the previous round of projections released in November. The…

Although our base case remains that a continuation of the disinflation process will allow policymakers to pivot to rate cuts this year, we continue to monitor risks to this outlook. On this front, some key indicators have recently moved in the wrong…

Our Portfolio Allocation Summary for February 2024.

Treasury yields continued to push higher on Monday, bringing the total increase over the past two trading days to 29bps. The move comes on the back of strong economic data releases indicating that conditions in the US are resilient. Notably, Friday’s…

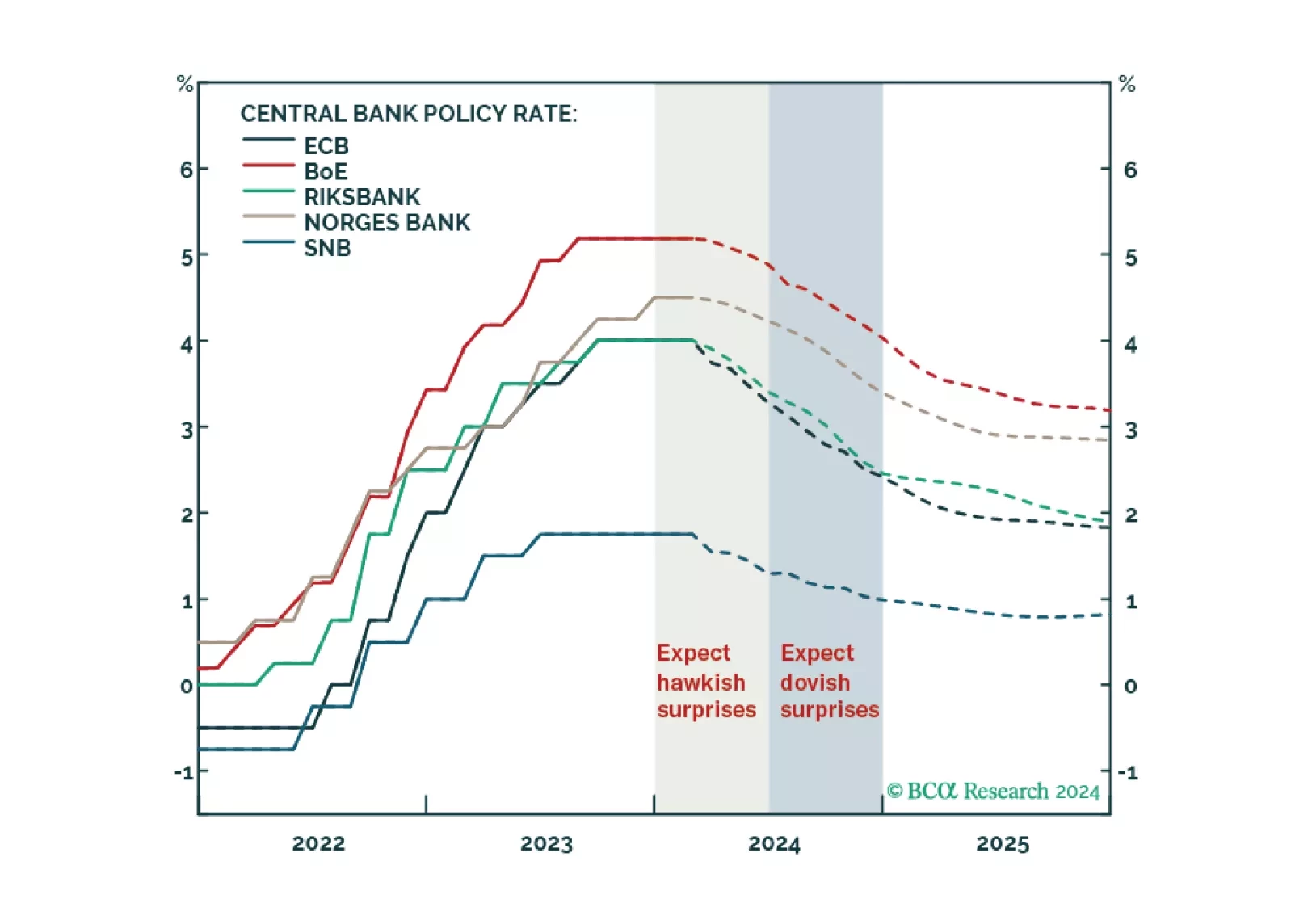

BCA Research’s European Investment Strategy service upgrades Swedish government bonds to neutral from underweight within European fixed-income portfolios. The Riksbank kept its policy rate steady at 4% last week. Governor Erik Thedéen and the Riksbank…

Our Central Bank Monitors support European central bankers’ decision to hold rates steady. Find out what it means for European fixed-income portfolio allocation.

The US Employment report came in well above consensus expectations on Friday, delivering a strong positive signal on labor market conditions in January. The 353 thousand increase in nonfarm payroll employment beat expectations of a slowdown to 185 thousand.…