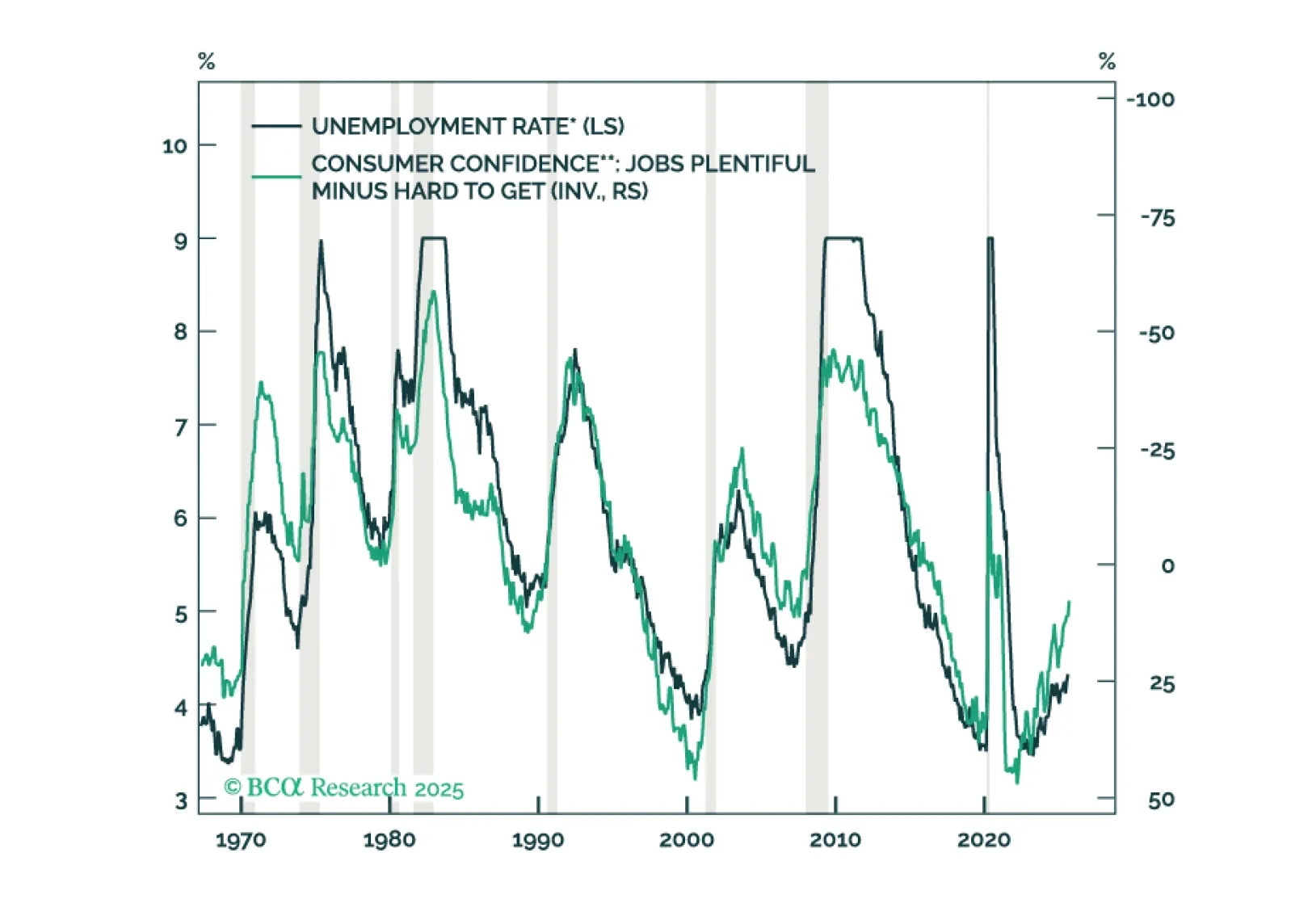

Fixed Income

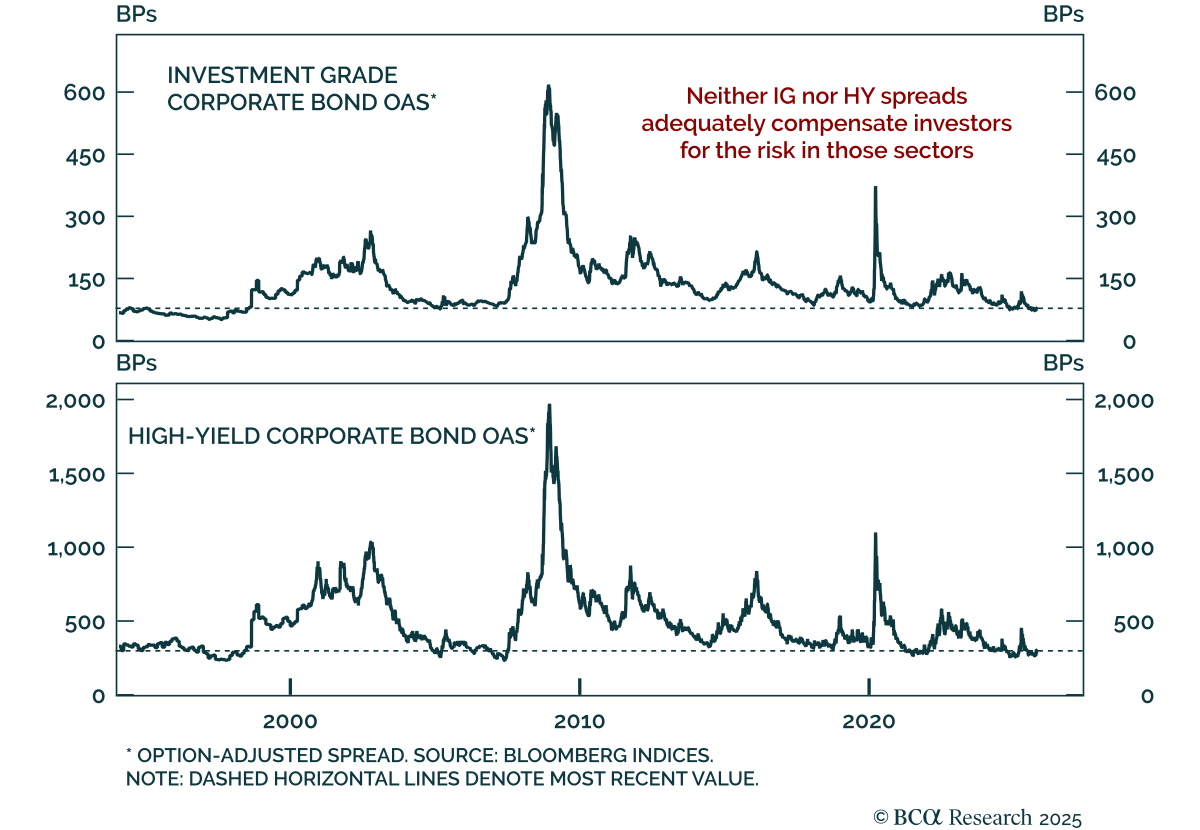

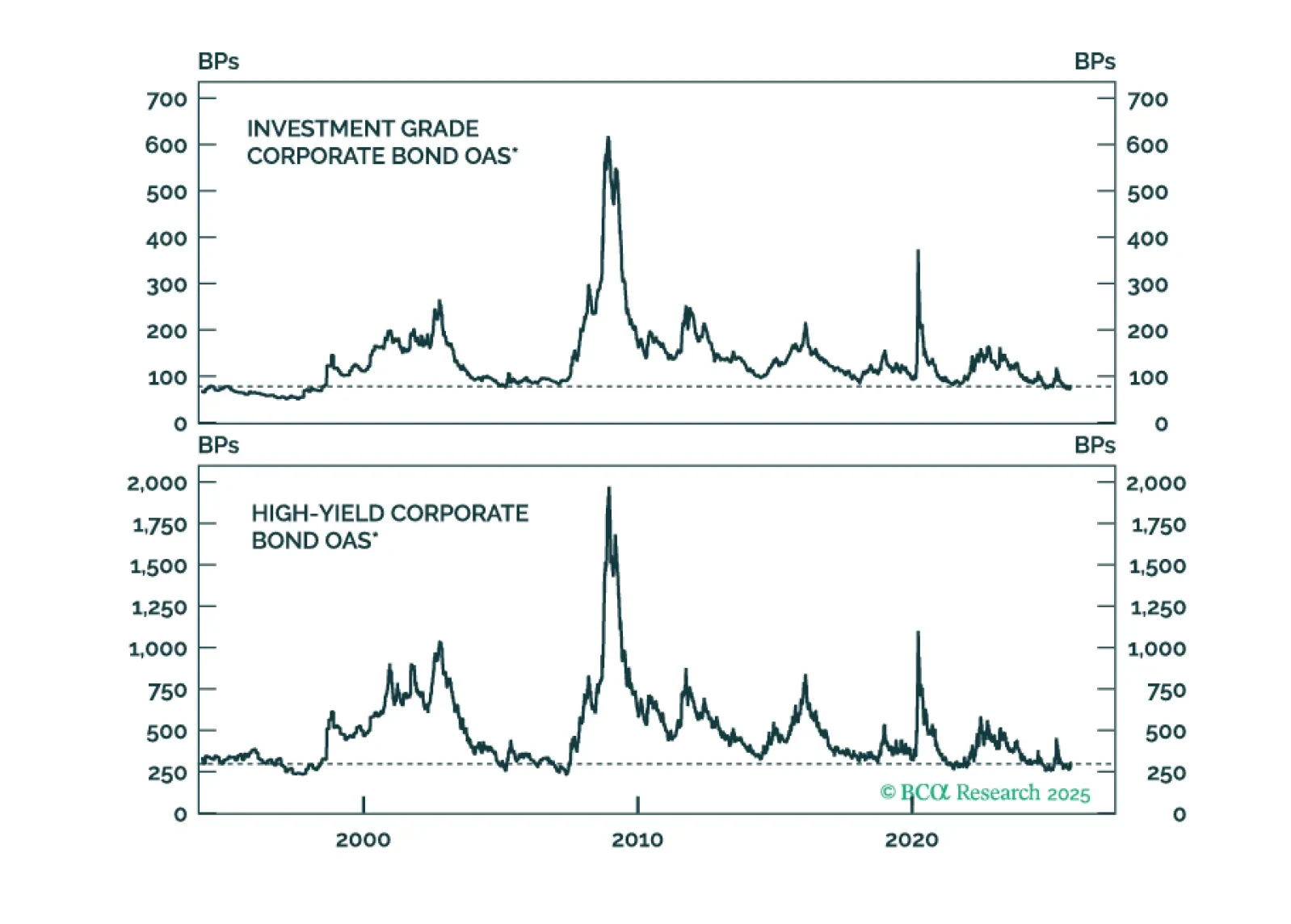

Our US Bond strategists find that neither IG nor HY spreads adequately compensate investors for risk, though the Ba credit tier offers the best relative trade-off. Expected excess returns across corporate credit are near multi-decade lows, with spreads for…

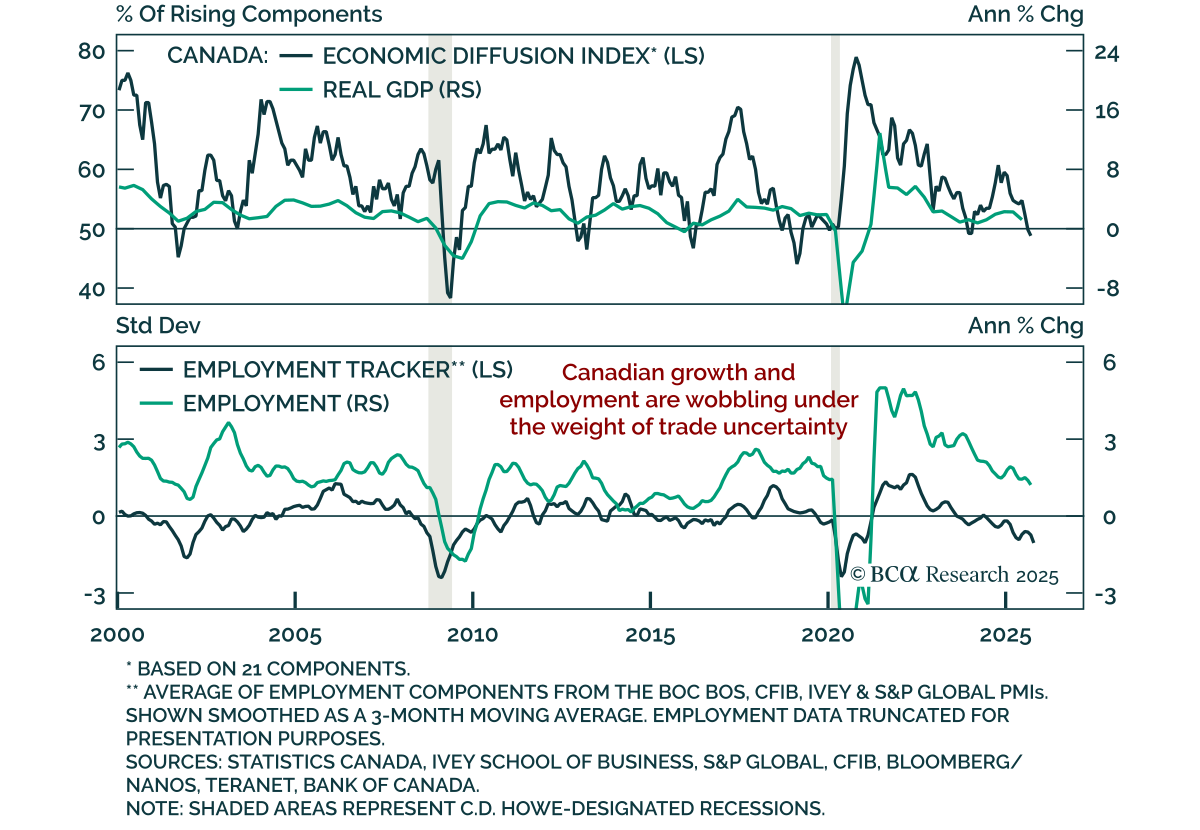

Recent Canadian data confirm slowing growth, reinforcing support for government bonds and steepeners. The October CFIB Business Barometer fell to 46.3 from 50.2, indicating contraction and underscoring the risk posed by small business weakness given their…

This week’s Special Report evaluates the reward and risk in corporate bonds. We address the question of whether low expected excess returns today are justified by low risk or an example of overvaluation.

Our GeoMacro strategists remain overweight equities and bonds for now but warn that markets will soon test their “melt-up” thesis, as the cycle transitions from cash- to leverage-driven growth. The dominant theme of 2025 is not AI, but USD debasement. While a…

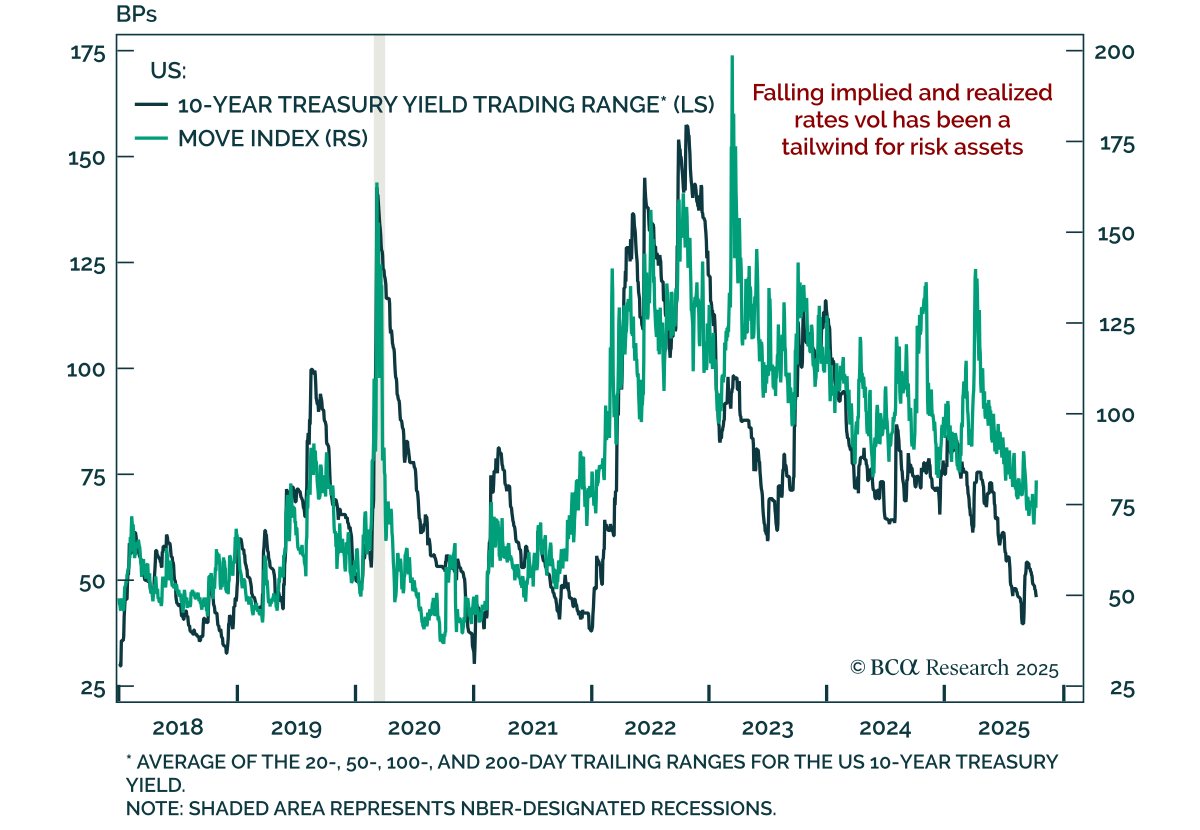

Cross-asset volatility fell in recent weeks, with lower rates volatility supporting risk assets. The MOVE index, which tracks implied USD rates volatility, recently dropped to its 20th percentile before rebounding. This decline reflects several forces. There…

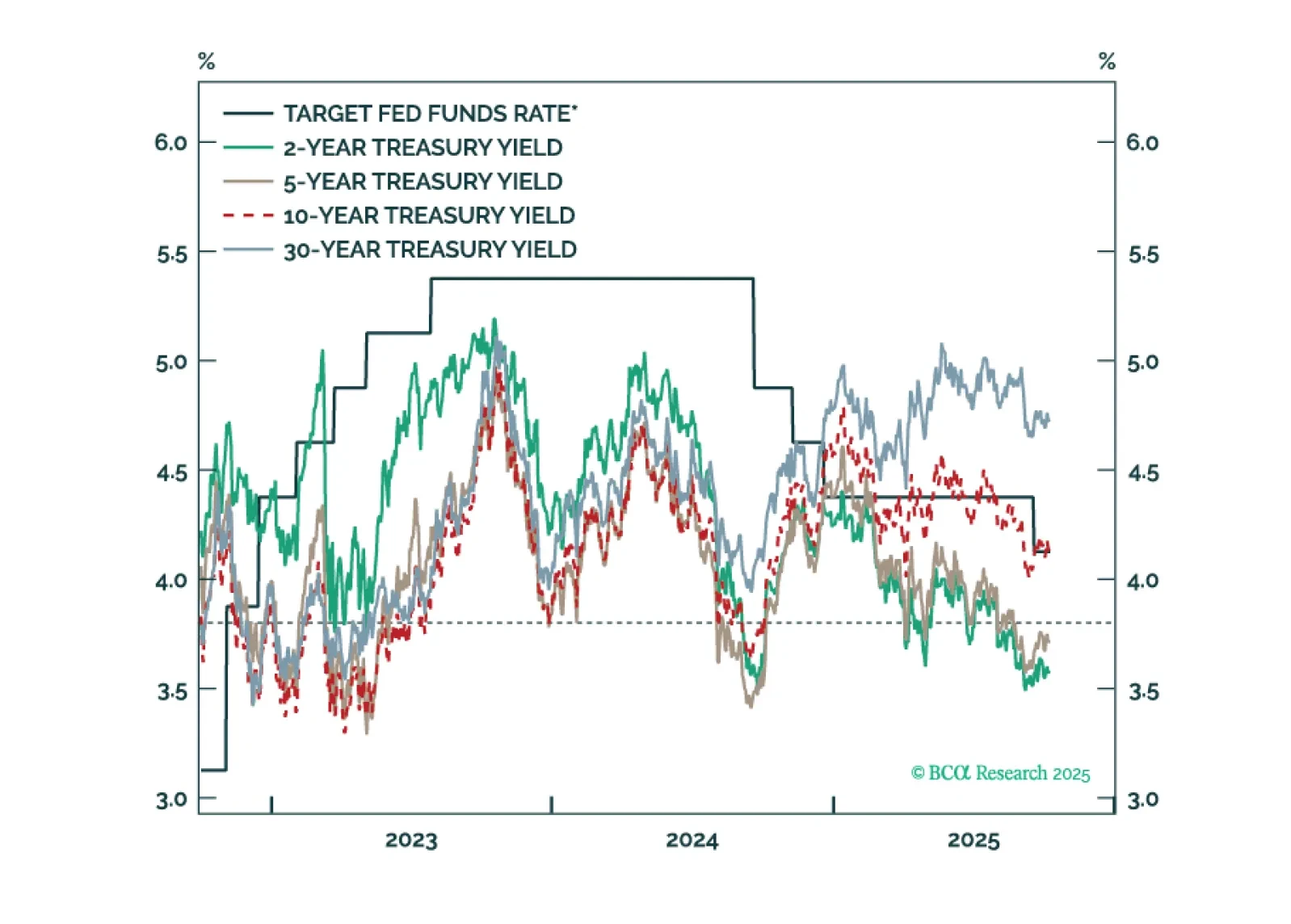

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

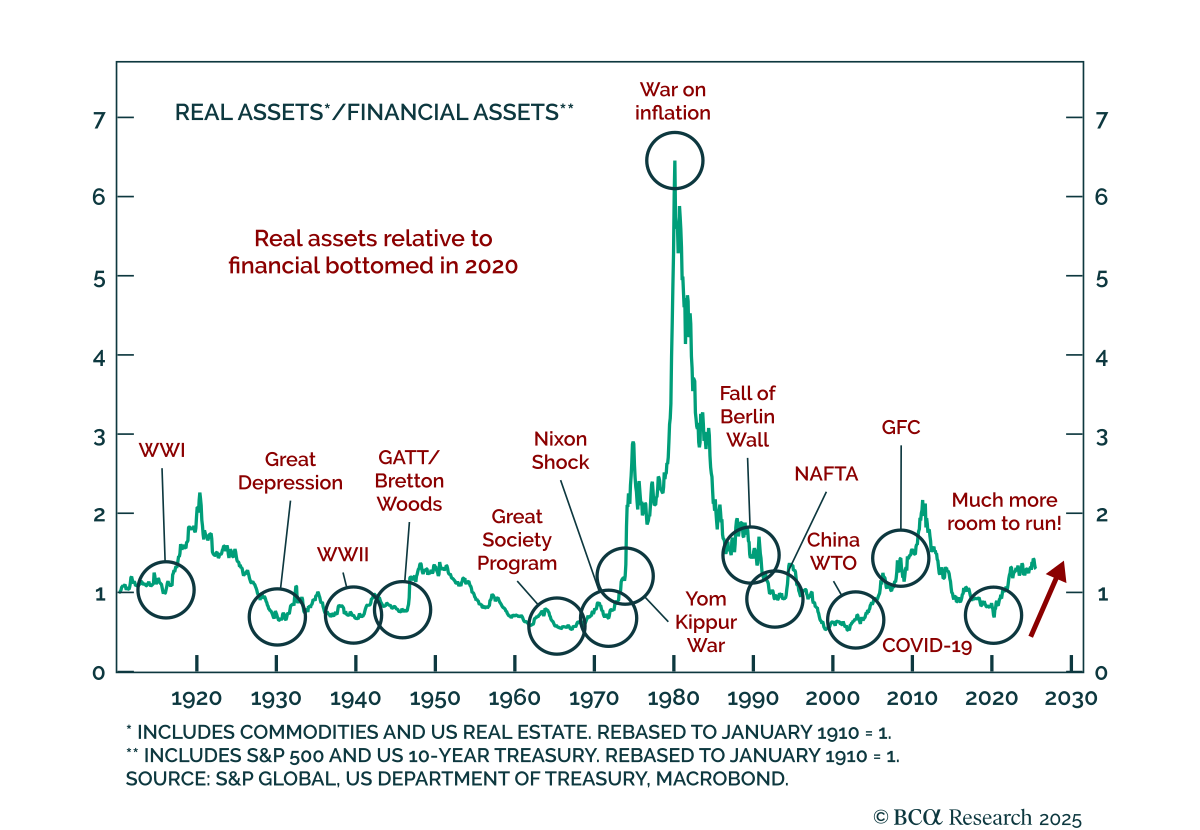

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

Japanese markets reacted sharply to Sanae Takaichi’s election as the leader of the ruling Liberal Democratic Party and the frontrunner to become Japan’s next Prime Minister. The Nikkei surged 4.8% and the yen plunged nearly 2% across major pairs. Seen as a…

Our Portfolio Allocation Summary for October 2025.

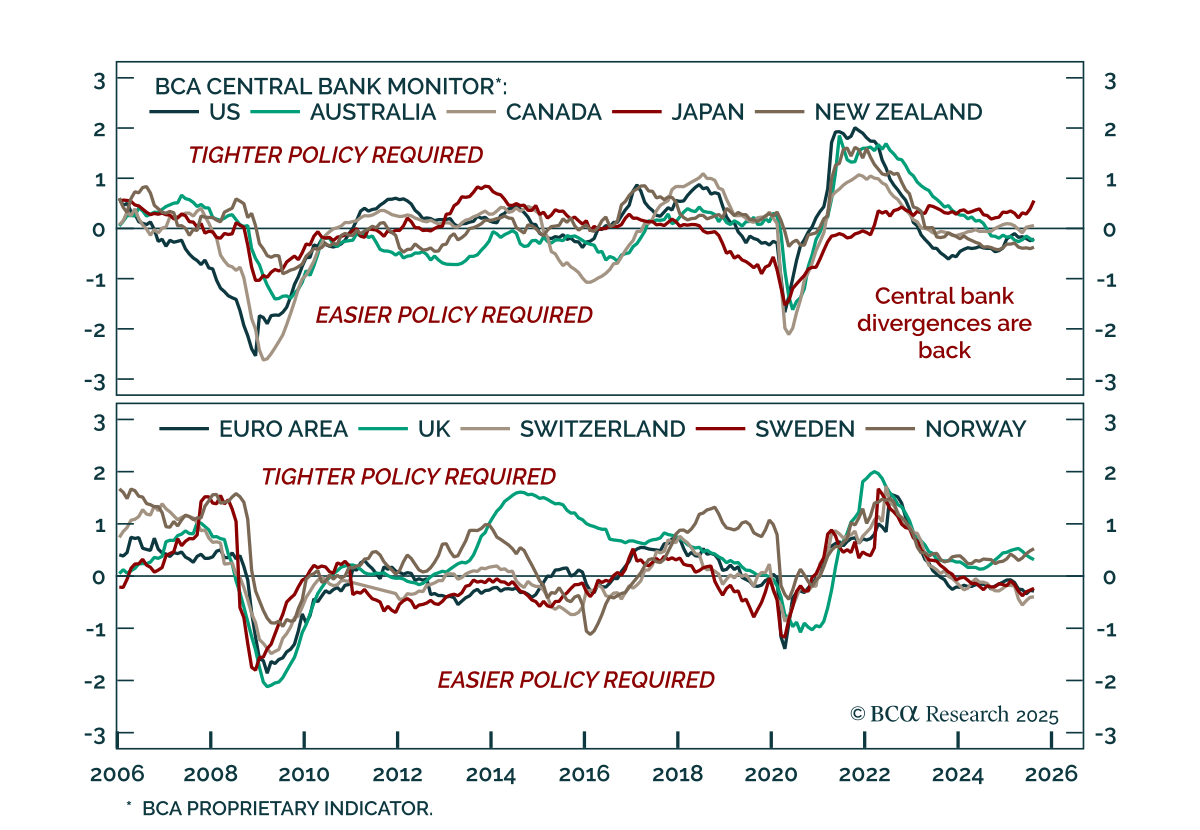

Our DM strategists recommend regional bond overweights in the UK, Canada, and Sweden, and express policy divergence through tactical FX trades: long USD, underweight GBP and SEK, and long JPY vs. EUR. Most G10 central banks are nearing neutral, but their next…