Fixed Income

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.

The Fed’s actions tell us that it has chosen to avoid a recession at the cost of moving its inflation goalposts to 3 percent. Thus begins the slippery slope to price instability. Long-term investors should underweight the dollar, own some gold, but better than gold is bitcoin. Plus, a new tactical trade is short GOOGL vs. SPY.

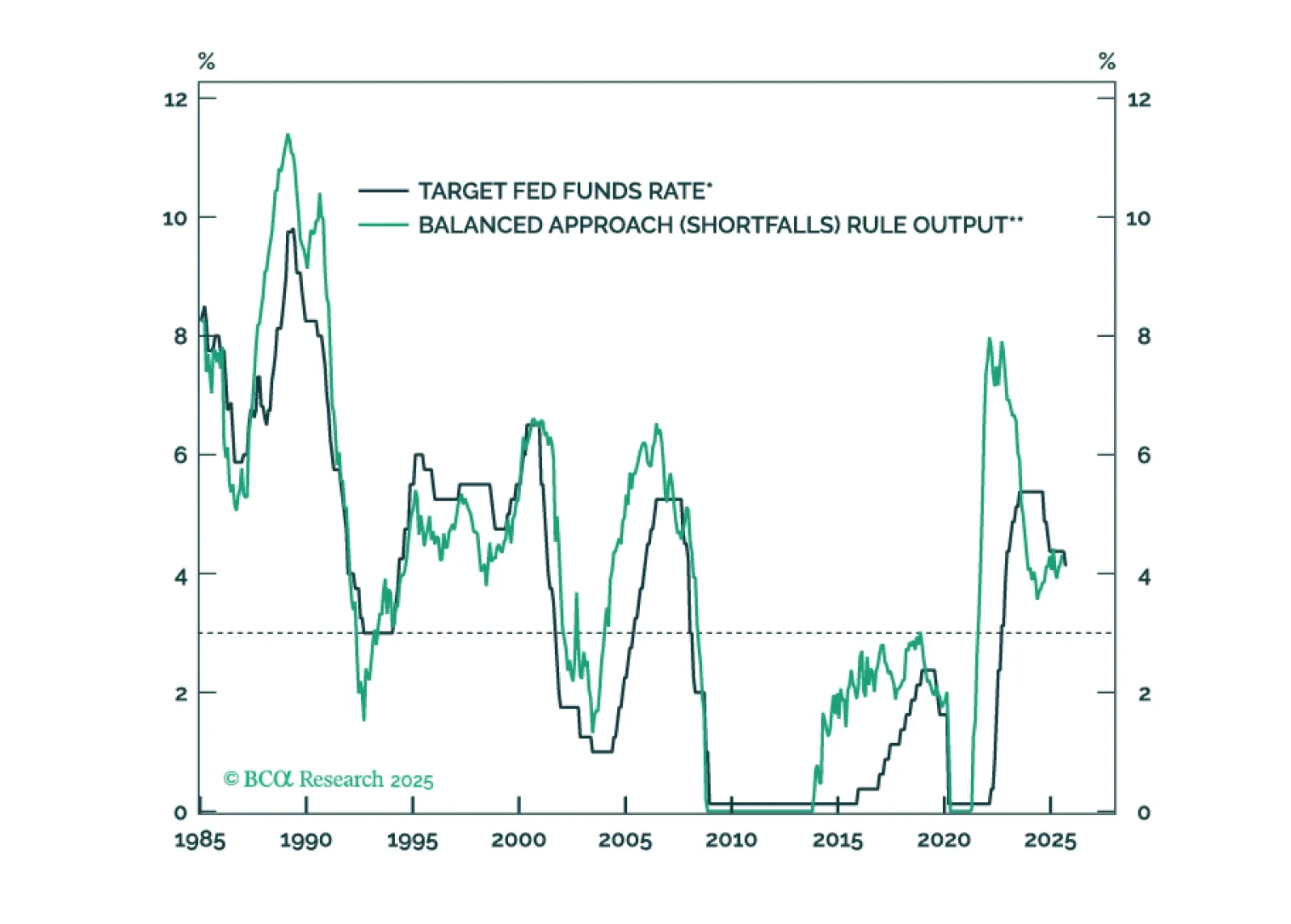

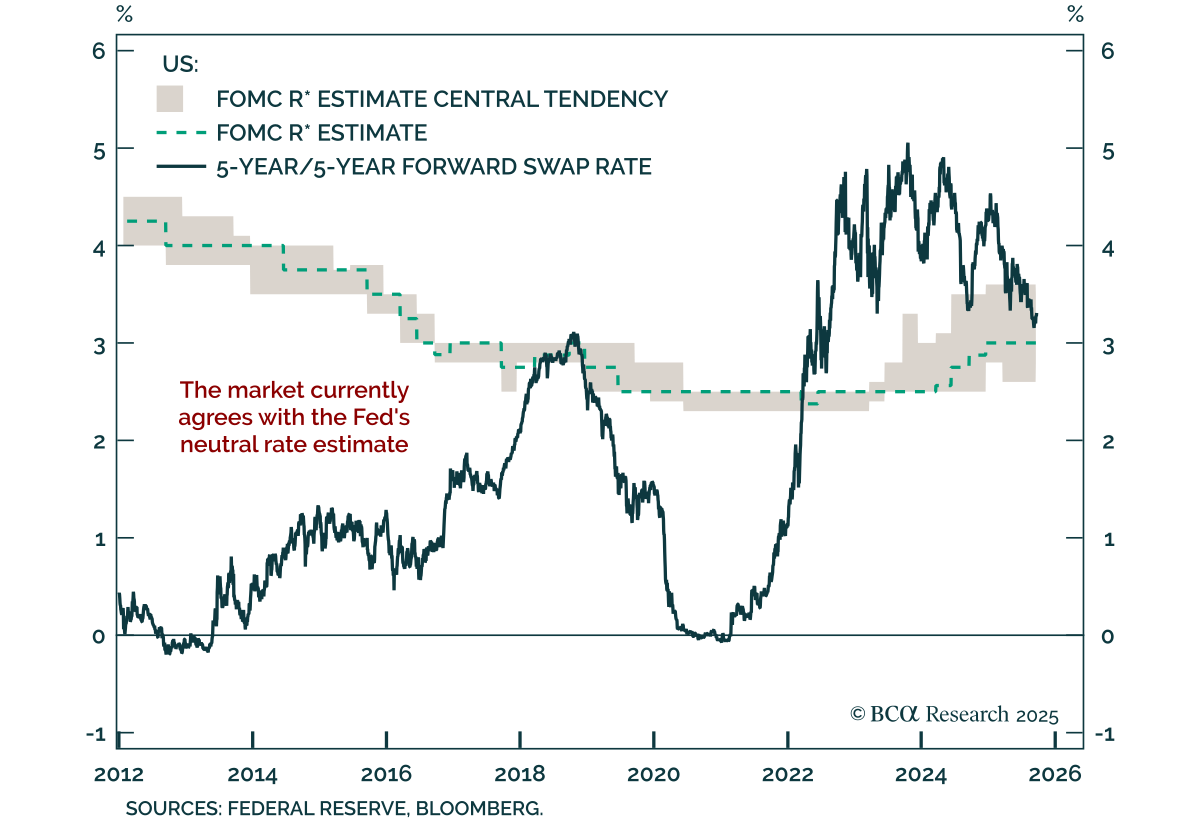

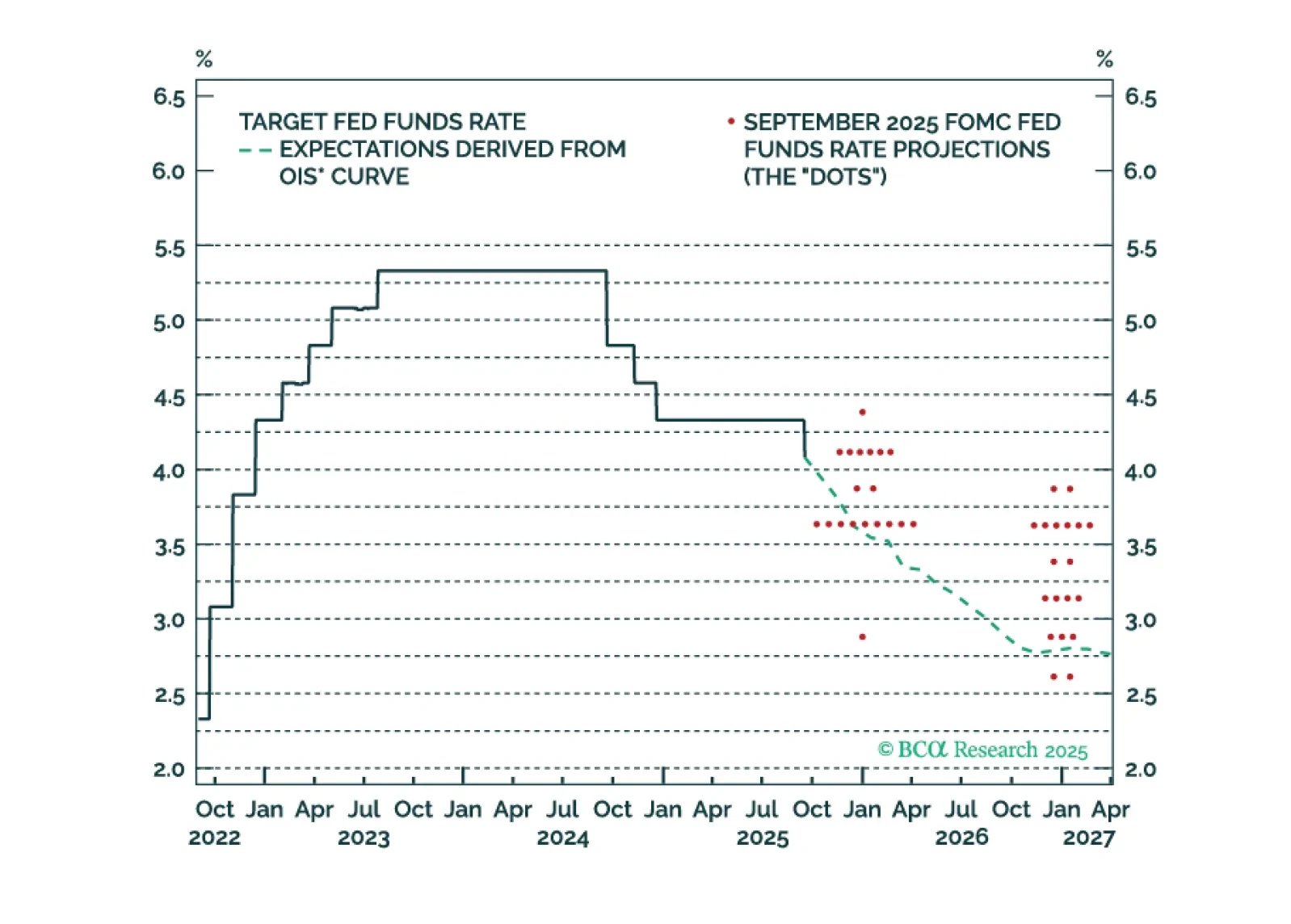

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

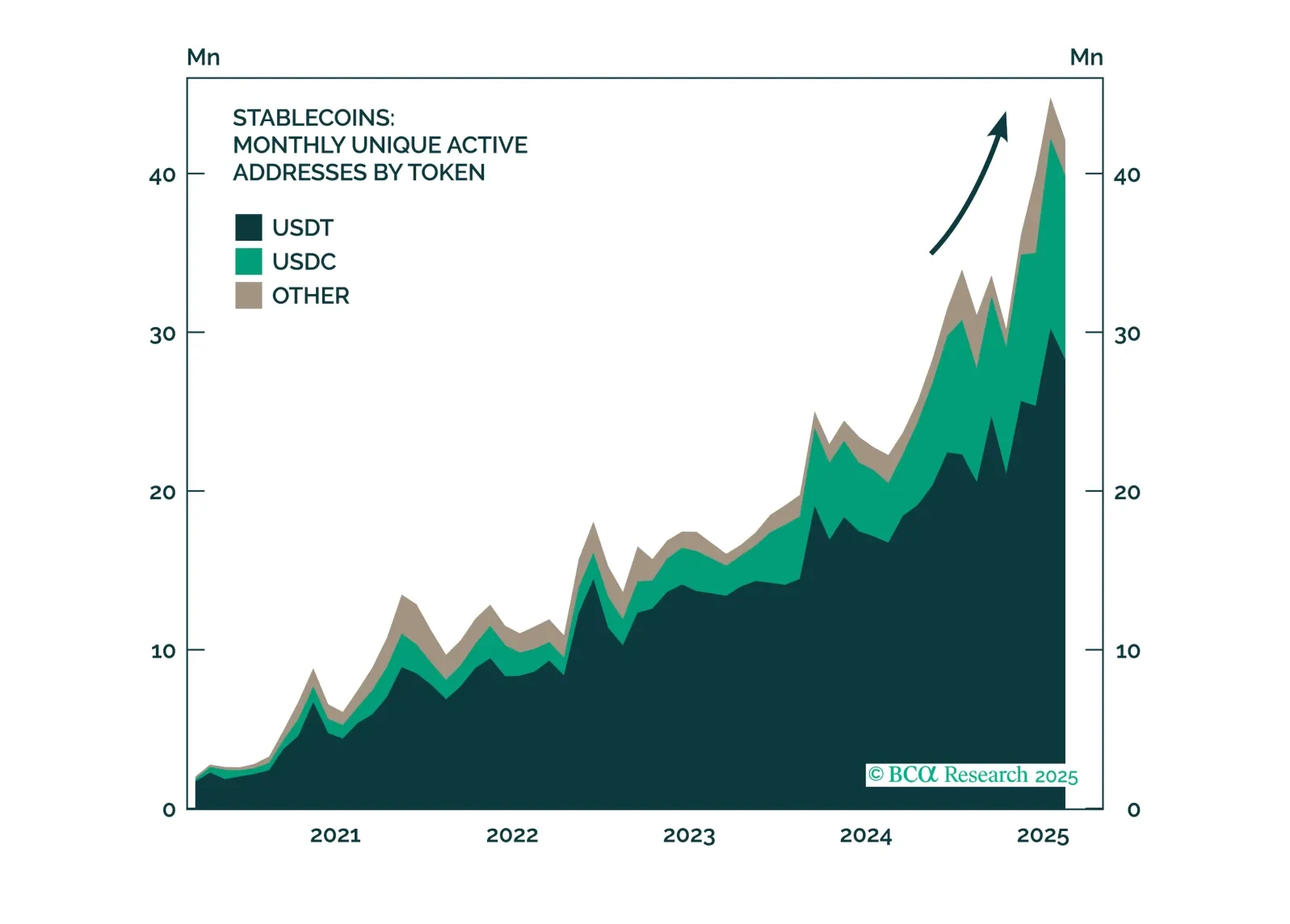

From Treasurys to tokenization, stablecoins are quietly becoming one of the most disruptive forces in global finance, with the power to compress yields, deepen dollar penetration, and shift the balance within crypto markets. Explore BCA’s latest insights on their growing impact.

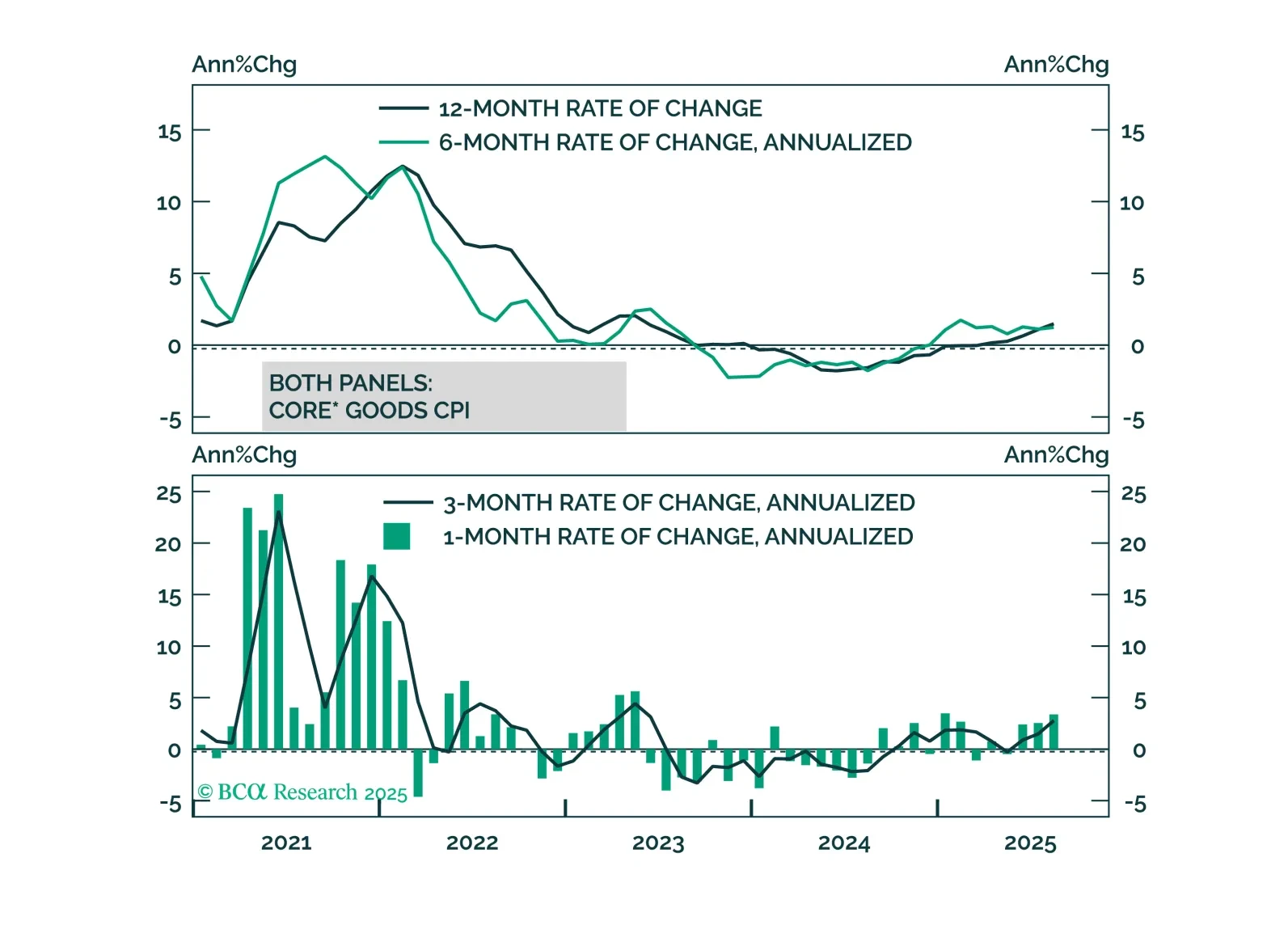

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.