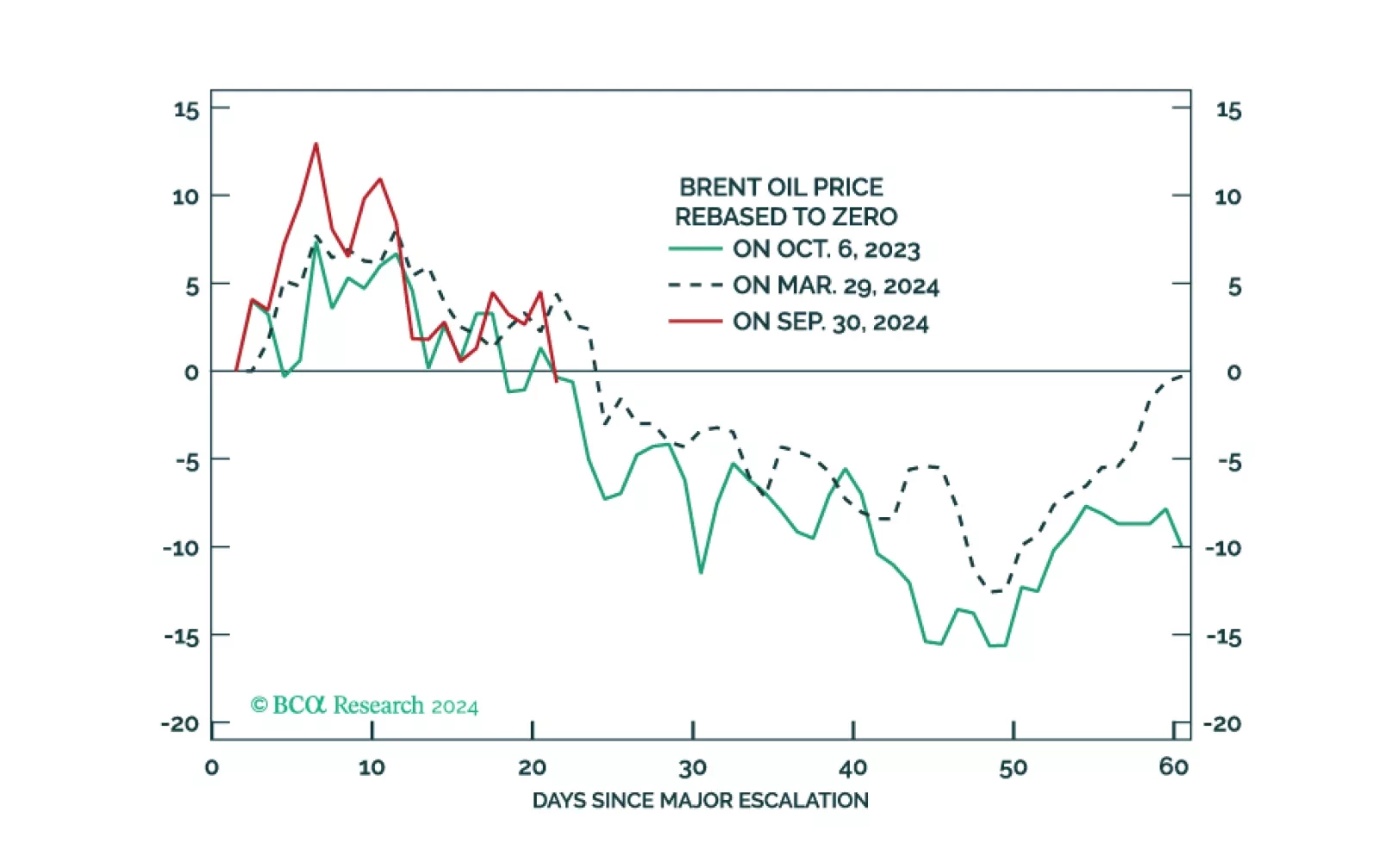

Geopolitics

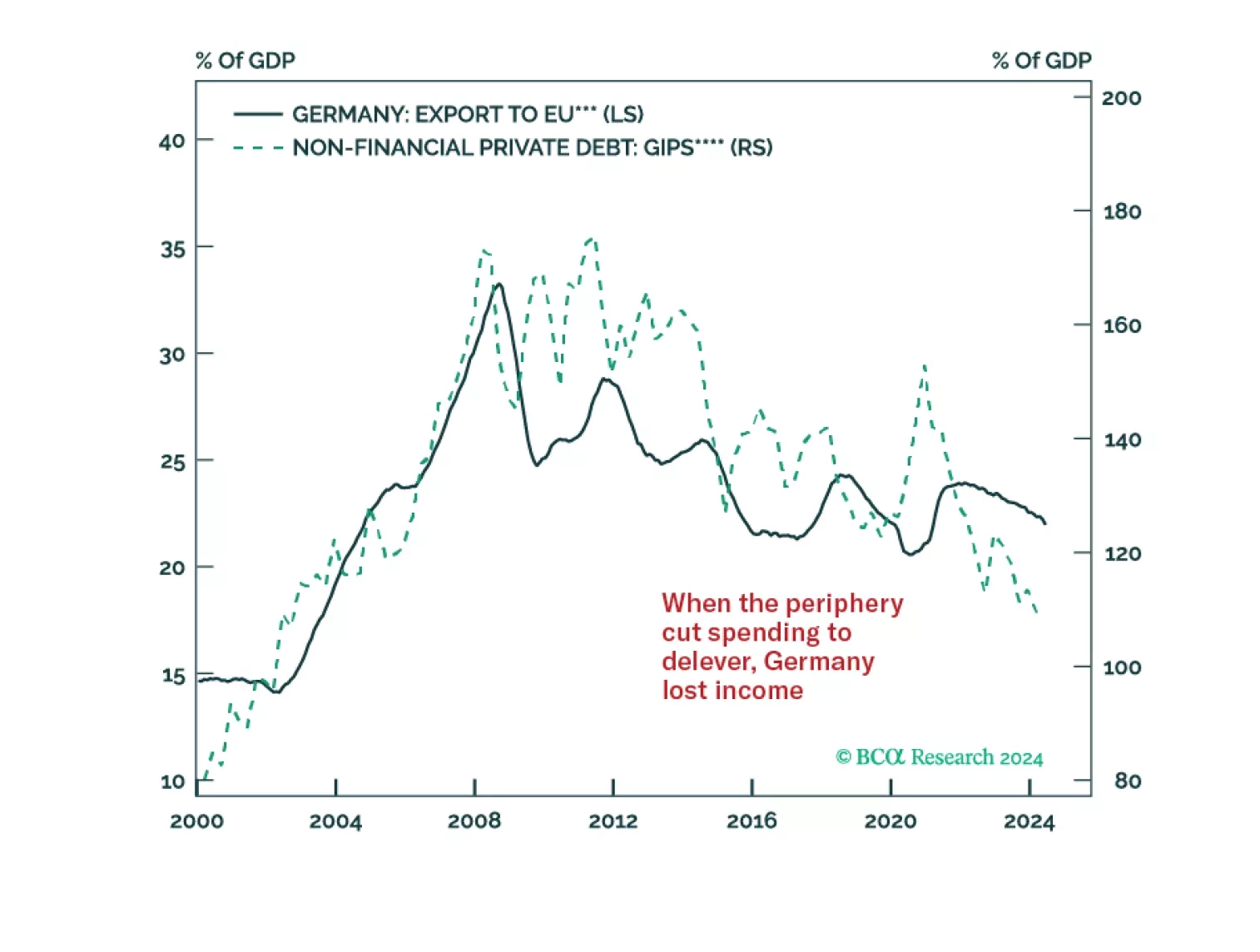

Germany’s economy has lagged that of the rest of Europe for nearly 10 years. So have German stocks. Investors are extrapolating these trends to bet on the country’s deindustrialization. Could Germany manage to beat dismal expectations?

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

Trump may be slightly favored for the White House but the US election is still extremely close. Odds of a contested or contingent election are rising, which should cause stock market volatility. A Republican sweep should cause more volatility. Democratic gridlock is next most likely but benign for stocks in the short run.

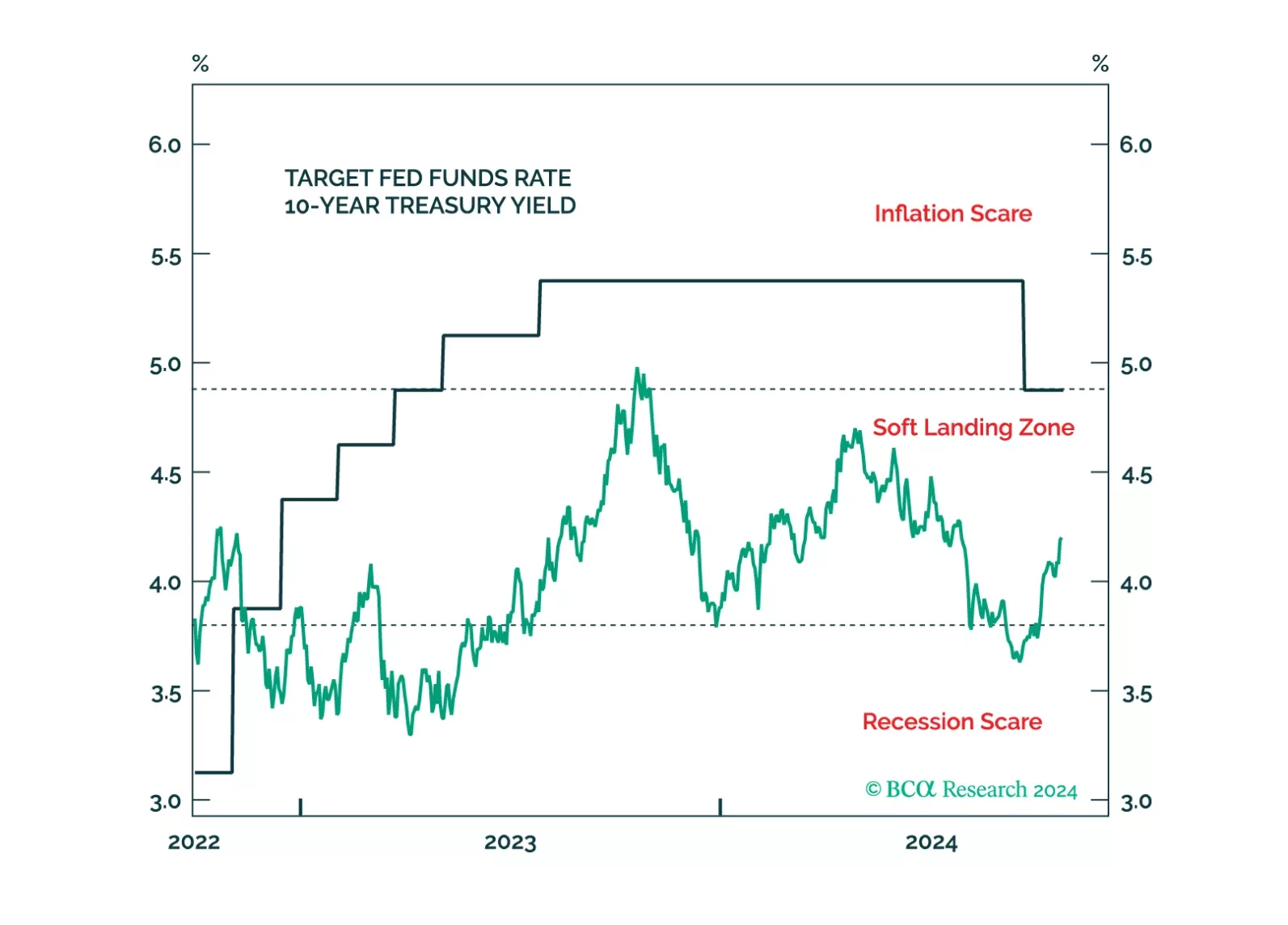

A Donald Trump victory would send bond yields higher during the next few weeks, but yields will fall in 2025 no matter the election outcome.