Geopolitics

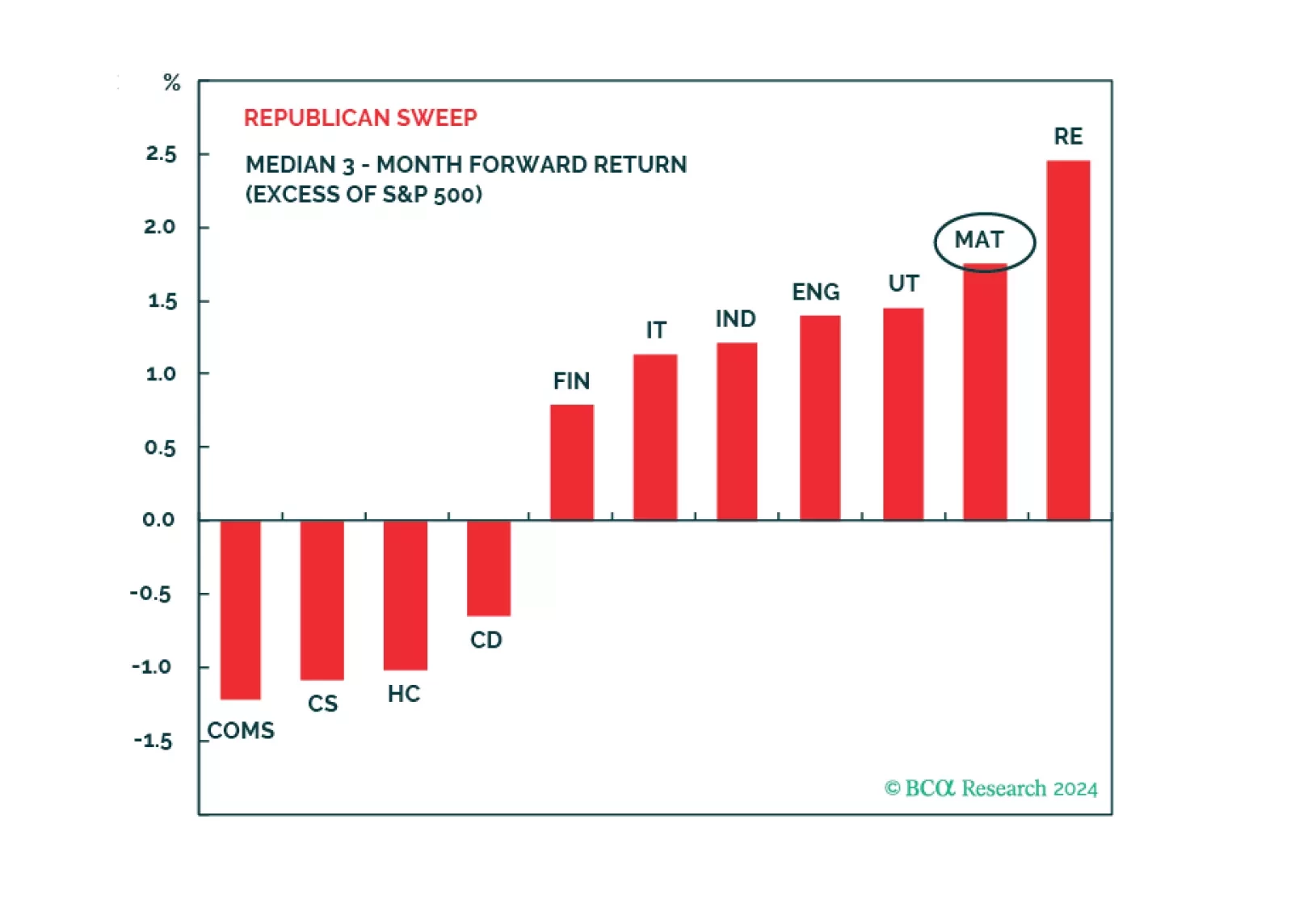

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.

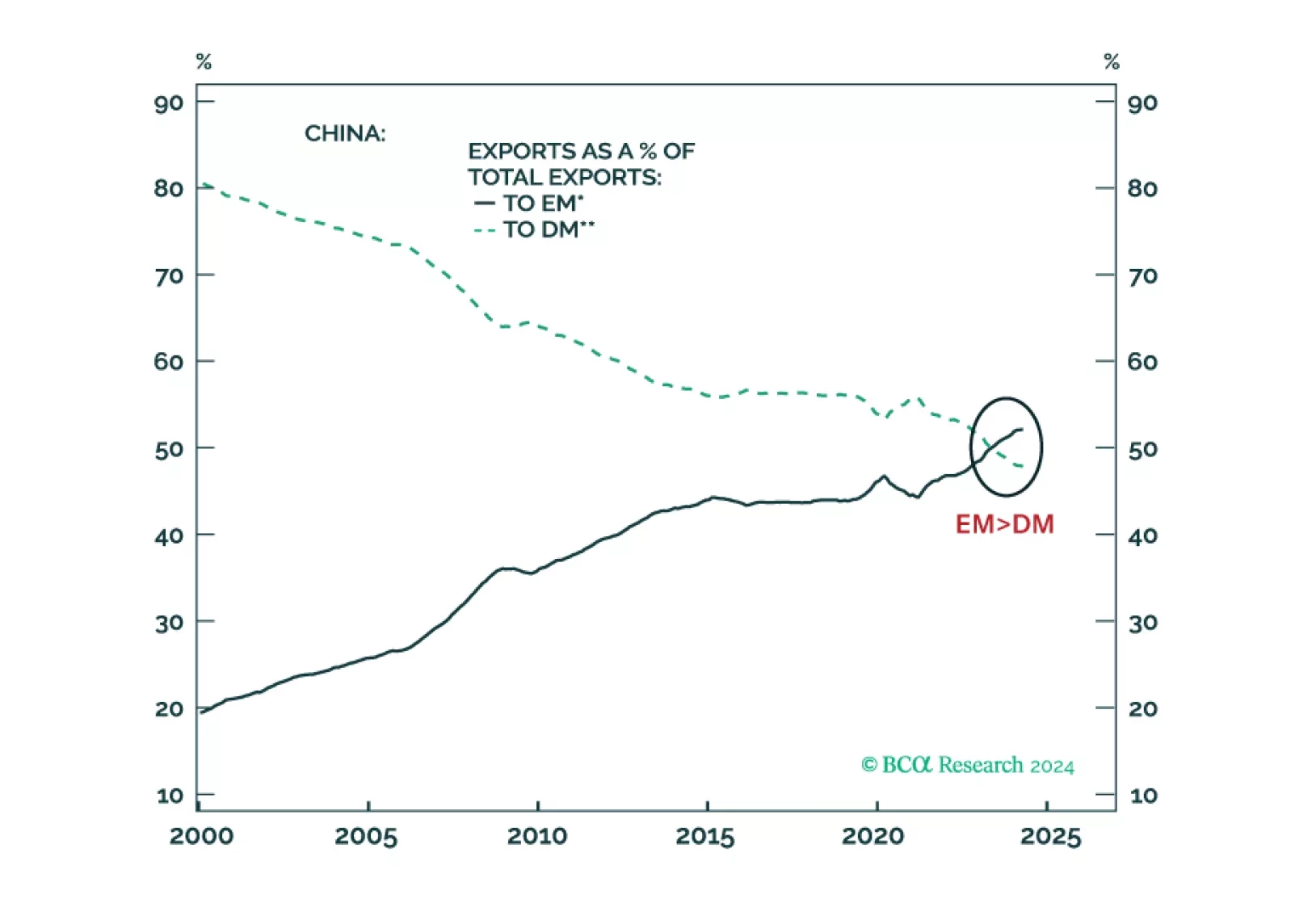

China has become less reliant on exports to advanced economies, and its products have successfully penetrated developing economies. Exports to the US make up 3% of Chinese GDP, while exports to all developing economies account for 10% of its GDP. China’s trade pivot from advanced to developing economies has economic, political, and geopolitical ramifications.

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.

China missed the chance to change course on economic policy and now it faces rising social instability and western protectionism. This policy approach implies it is not afraid of escalating strategic conflicts in East Asia. Investors should continue to underweight Greater Chinese assets. Any US-China détente will come later rather than sooner.