Geopolitics

This report provides our framework for interpreting the messages from last week’s Third Plenum, and the potential implications for the economy and investors.

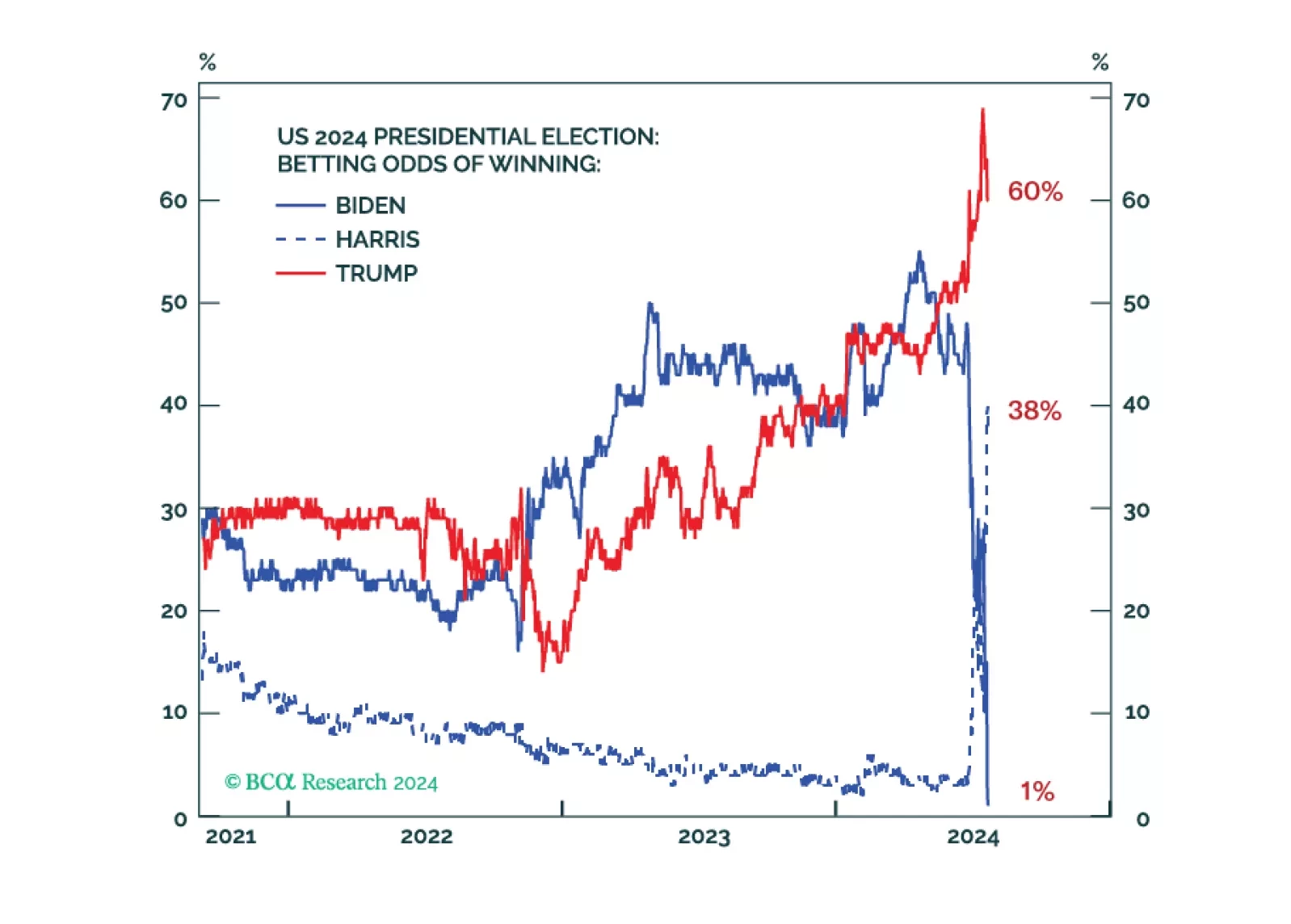

Investors should focus on growth concerns rather than the “Trump trade.” Bond yields will fall in the short run due to cyclically disinflationary economic slowdown, rather than rise in anticipation of a Republican full sweep and inflationary policies, which are likely but not yet a done deal.

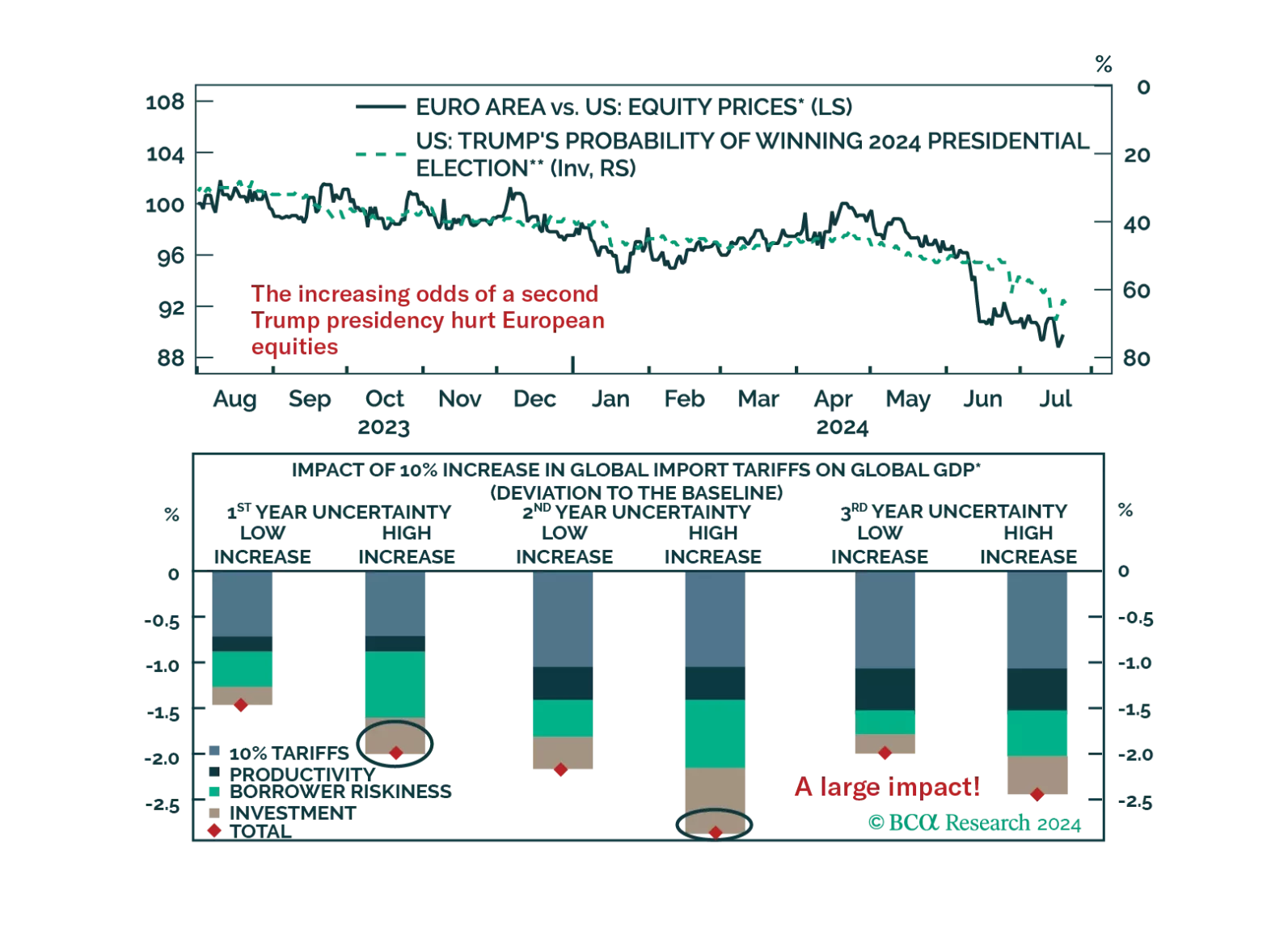

As Trump’s victory odds rise, the underperformance of European equities deepens. How negative would a global trade war be for European assets?

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.