Geopolitics

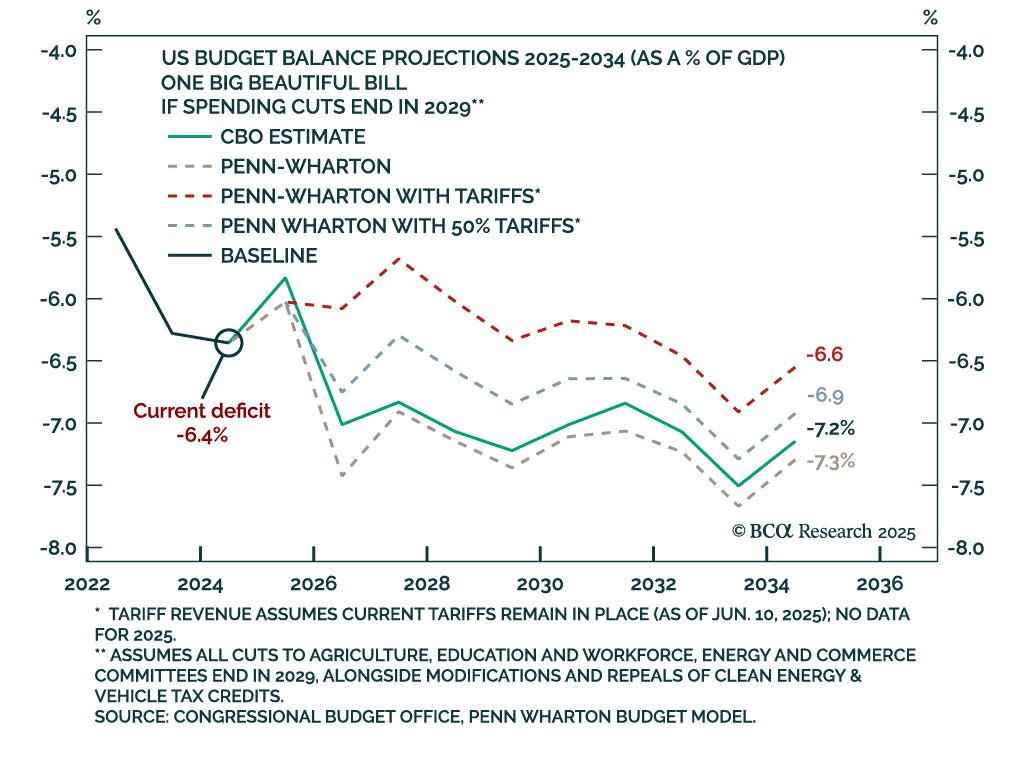

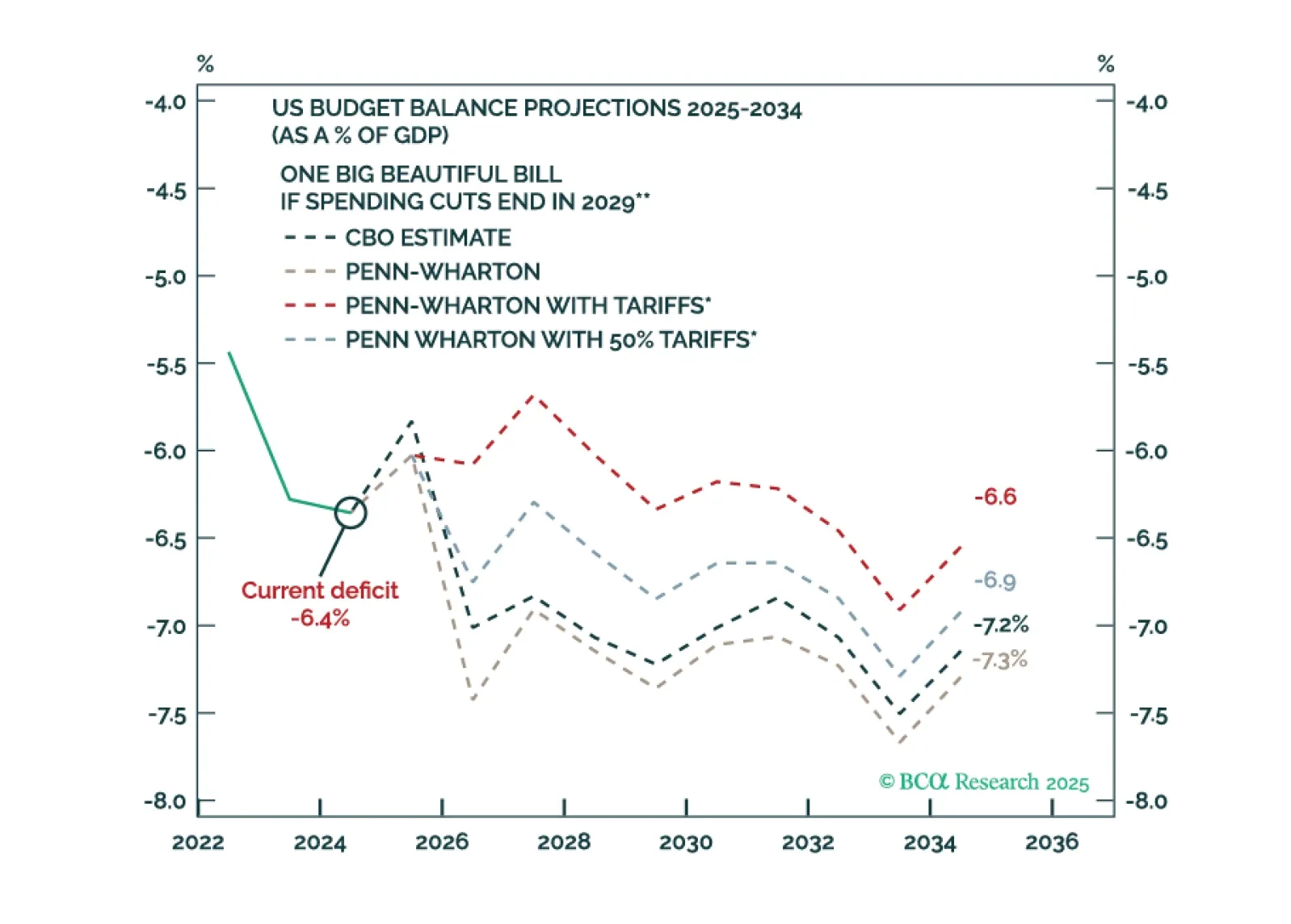

Bond market volatility will spike again in the near term. The Fed is committed to an easing cycle yet the Trump administration’s signature fiscal policy action will stimulate the economy. Tariffs are supposed to keep the budget deficit contained but they are inflationary.

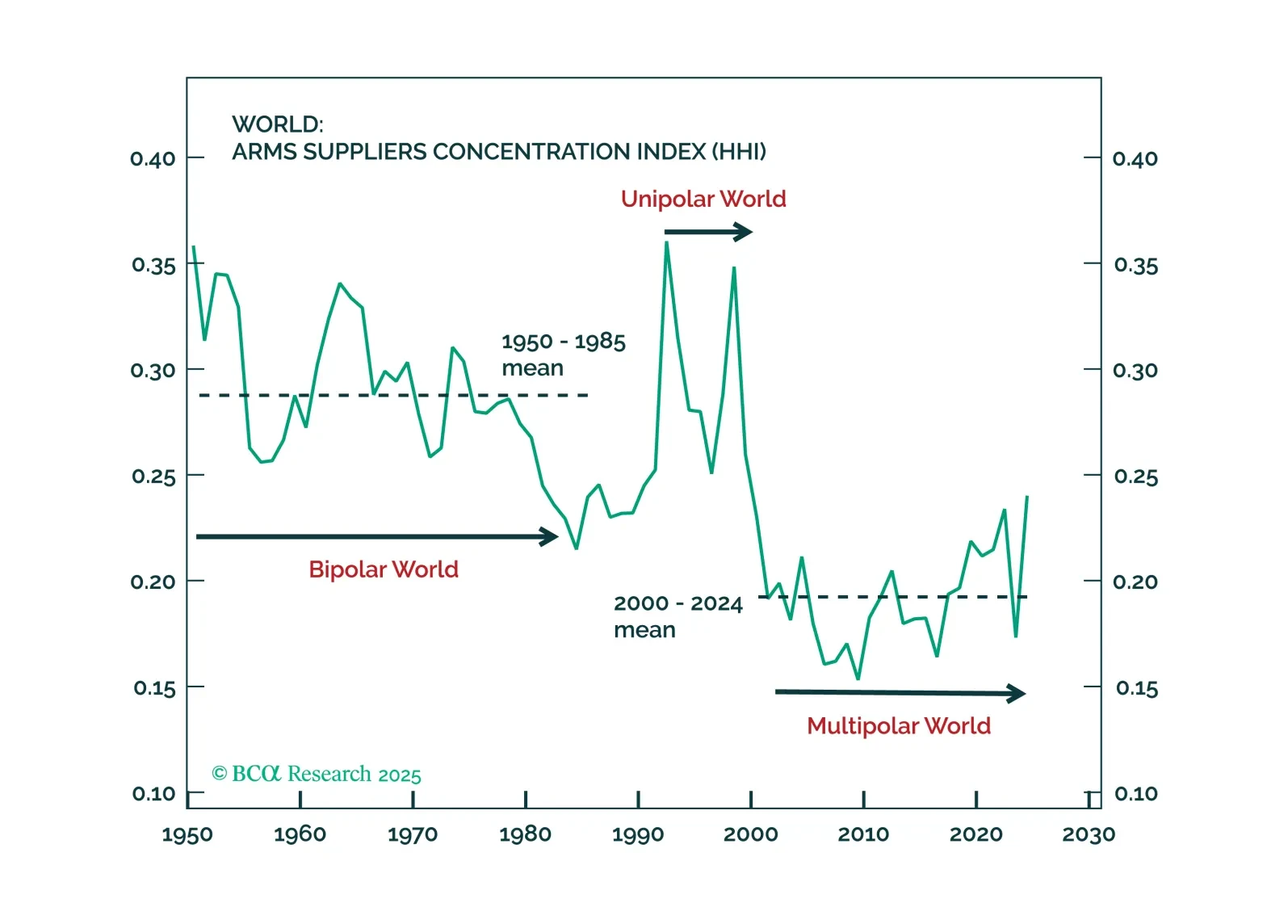

In our Beta report, we focus on our decade view. Many of our global allocator clients are scrambling to incorporate geopolitics into their strategic asset allocation. For most, this means thinking about war… or about future end-states. This is a mistake. We consider the next five years (maybe a decade) as the transition to the new era, a transition away from American unipolarity. And the transition itself is investment relevant. A transition to a multipolar world – which we think is occurring – will crush the USD and favor non-US assets. A transition to a bipolar world – not our base case, but still possible – would do the opposite.

President Trump faces new restrictions on his trade powers coming from the US judicial branch, but they will not prevent him from continuing to restrict trade and investment with China. Rather, they will establish some curbs against entirely arbitrary executive tariffs, especially when wielded against US allies and partners.

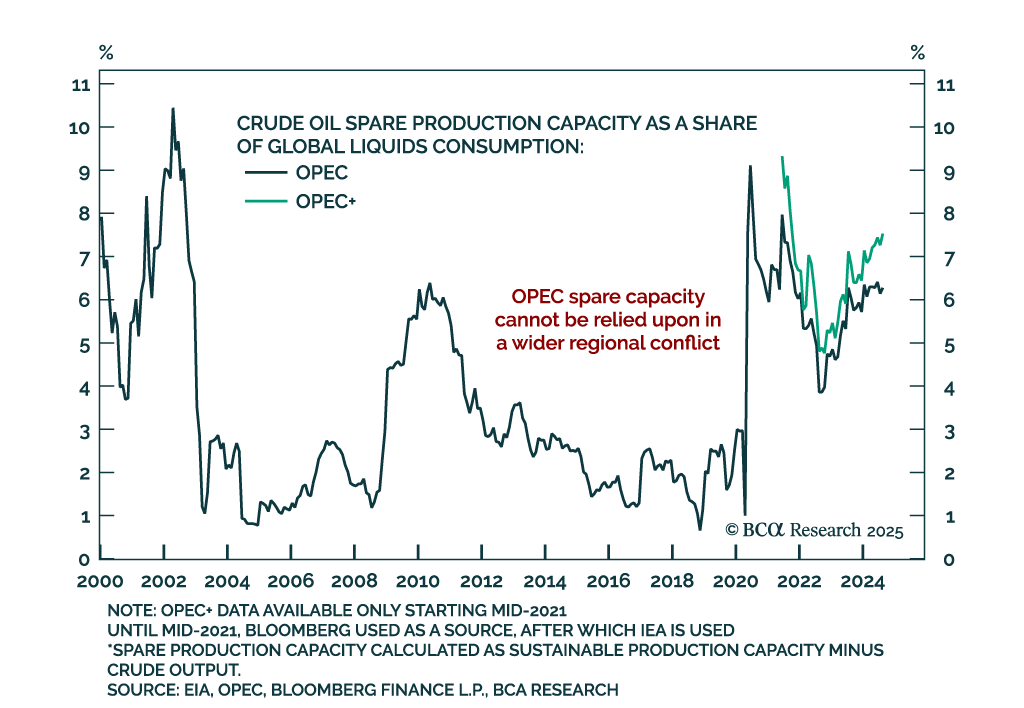

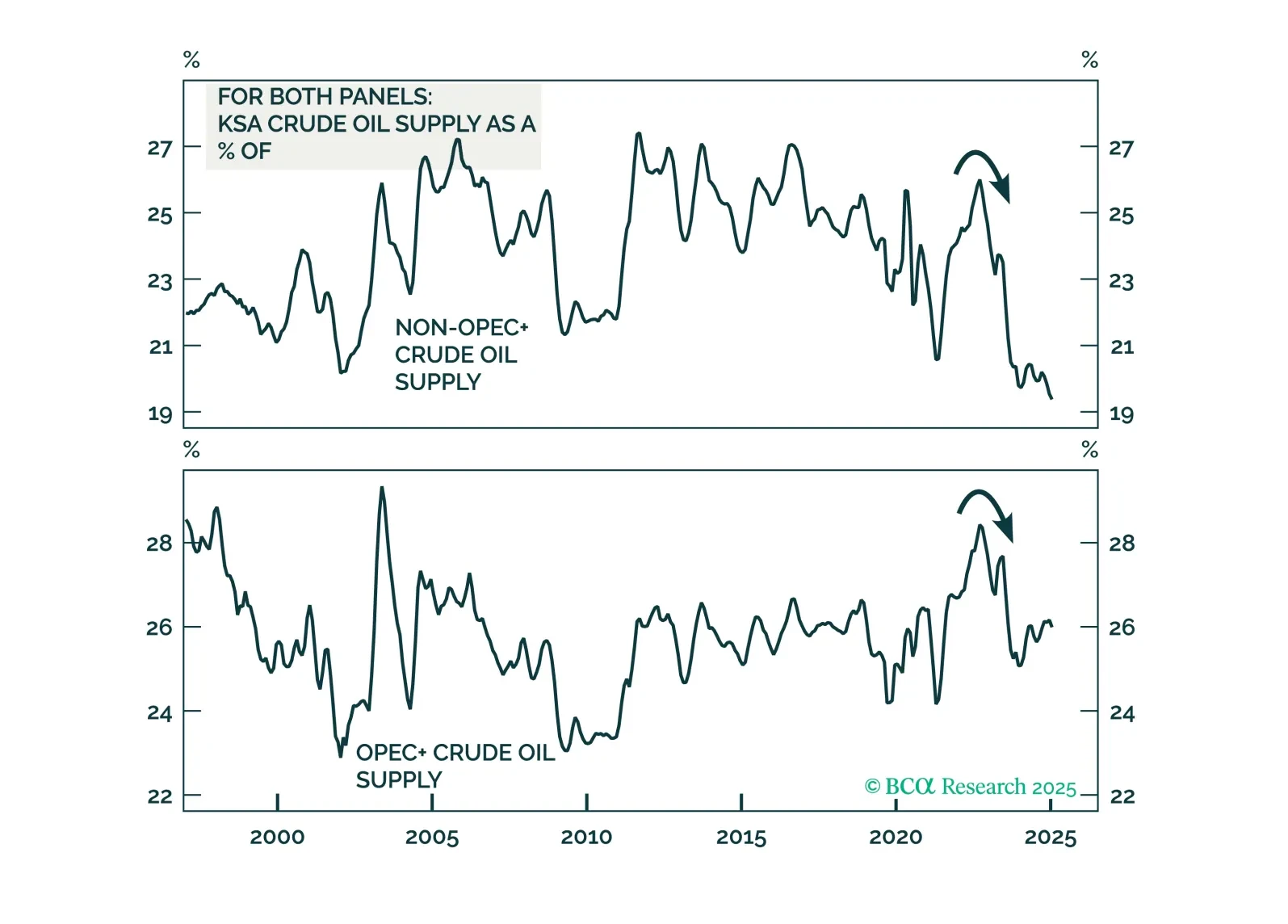

OPEC+ recently announced another outsized oil production hike, tripling its planned June output increase to 411k b/d for the second consecutive month. Our take on why KSA is boosting crude output at a time of heightened downside demand risks is that it is pursuing an oil price war lite. President Trump is not only blessing this strategy but also depending on it.

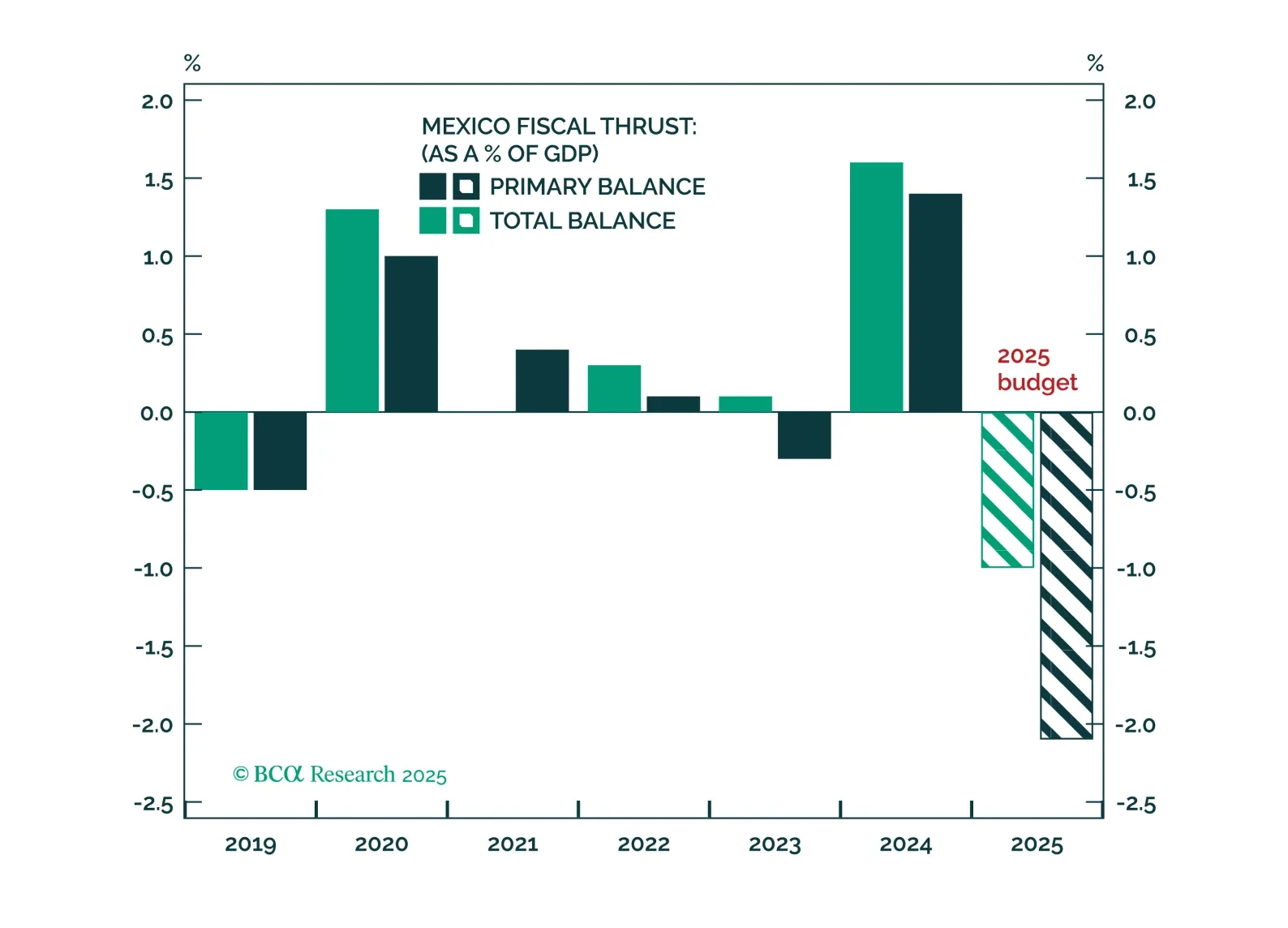

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.