Global

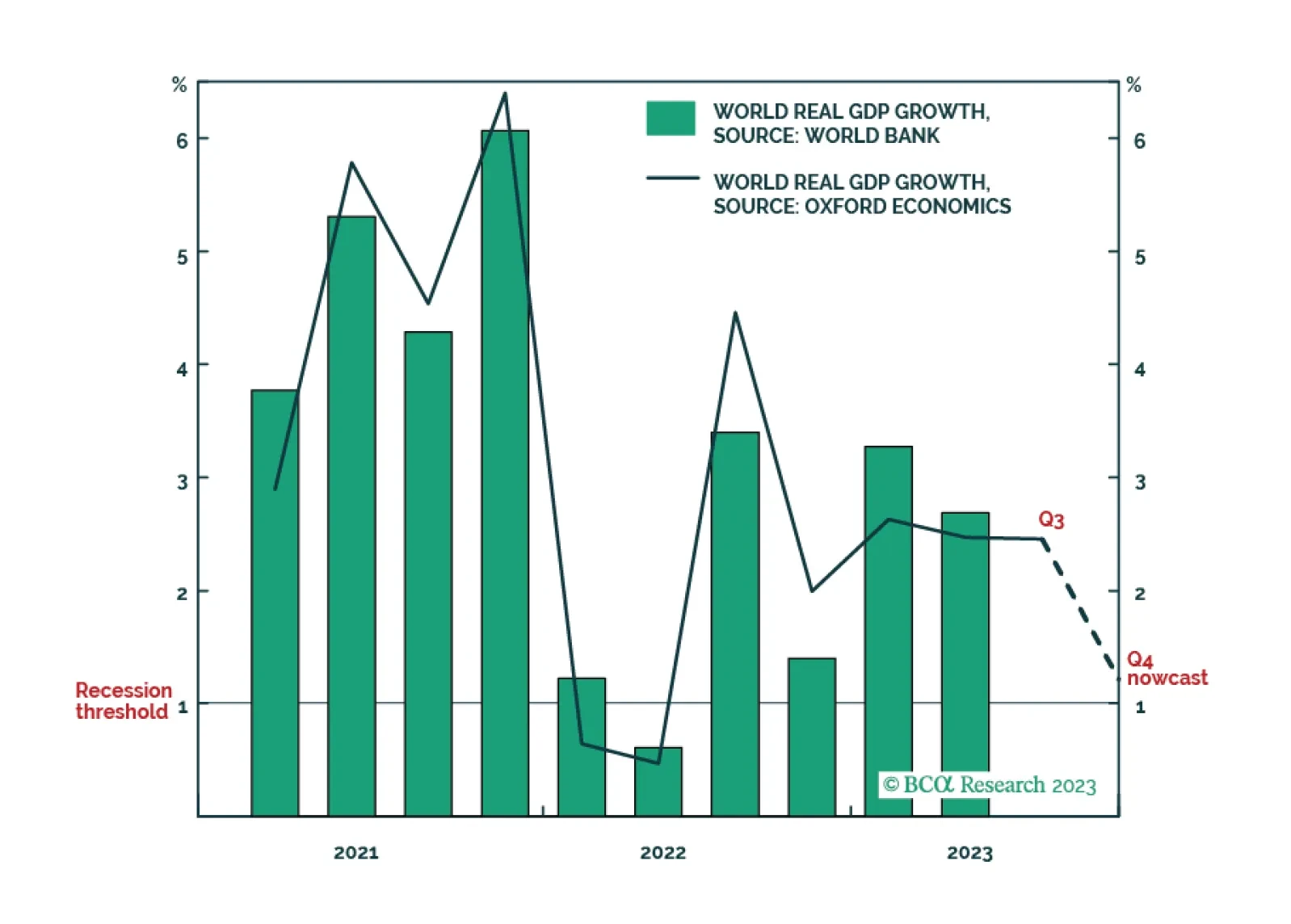

The latest ‘nowcast’ for world economic growth in the fourth quarter has plunged to just 1.2 percent, marking the cusp of another world recession. One important implication is that expectations for oil demand growth and industrial metal demand growth are way too optimistic.

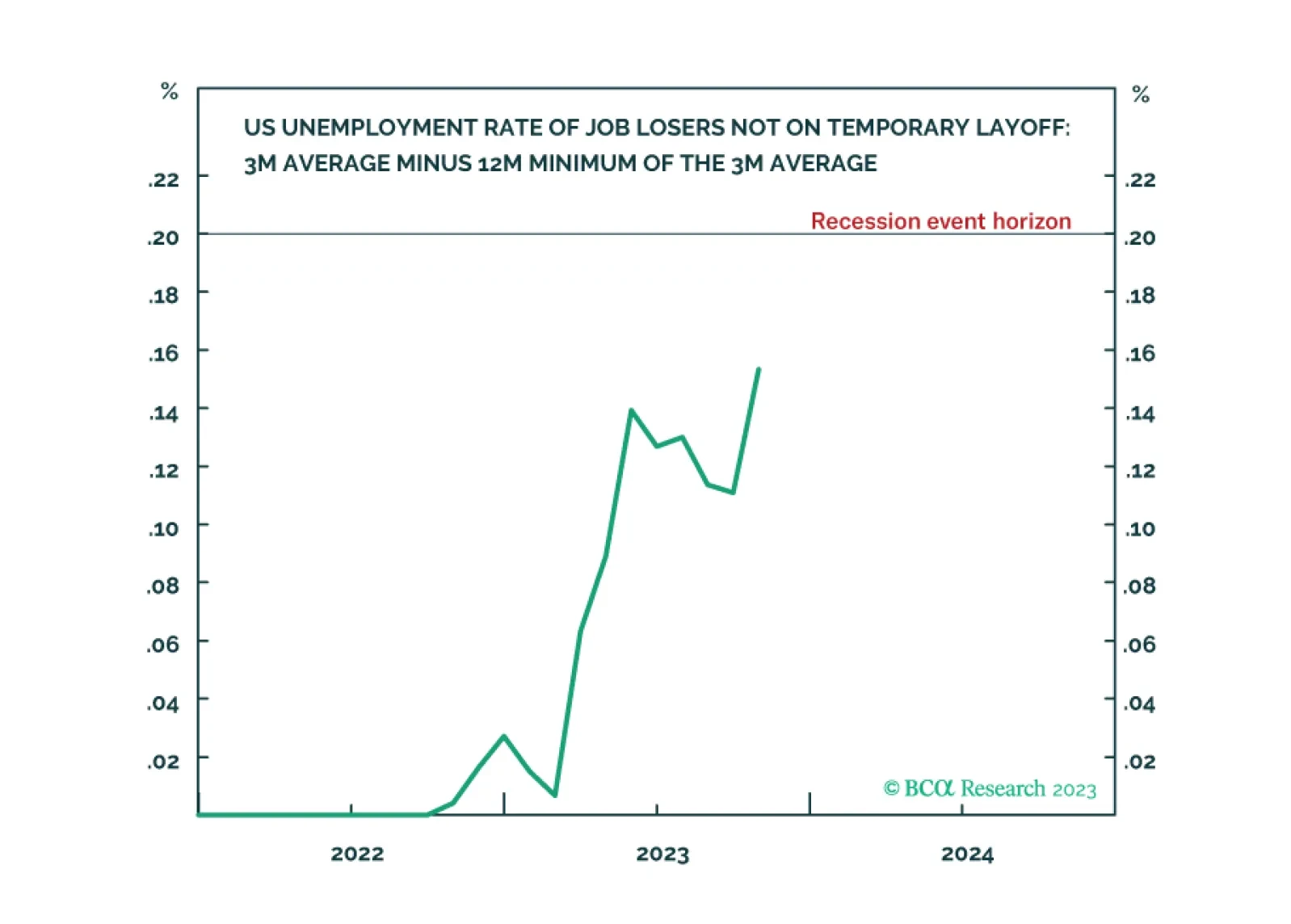

Following the October US jobs data, the ‘Joshi rule’ real-time US recession indicator increased from 0.11 to 0.15, meaning that it is fast approaching its event horizon of 0.20. We go through the investment implications. We also highlight a new long-term recommendation. Plus, the Norwegian krone is close to a potential rebound.

Economic growth has little to no relationship with long-term country returns. But if GDP doesn’t drive long-term equity returns, then what does? To find out, we break down equity total returns of 33 countries from 1997 to 2022 into seven components. In line with other academic research, we find that, over our sample, net buybacks were a crucial factor for long-term country performance. Our research suggests that equity issuance is an underestimated driver of returns that investors should pay more attention to.