Global

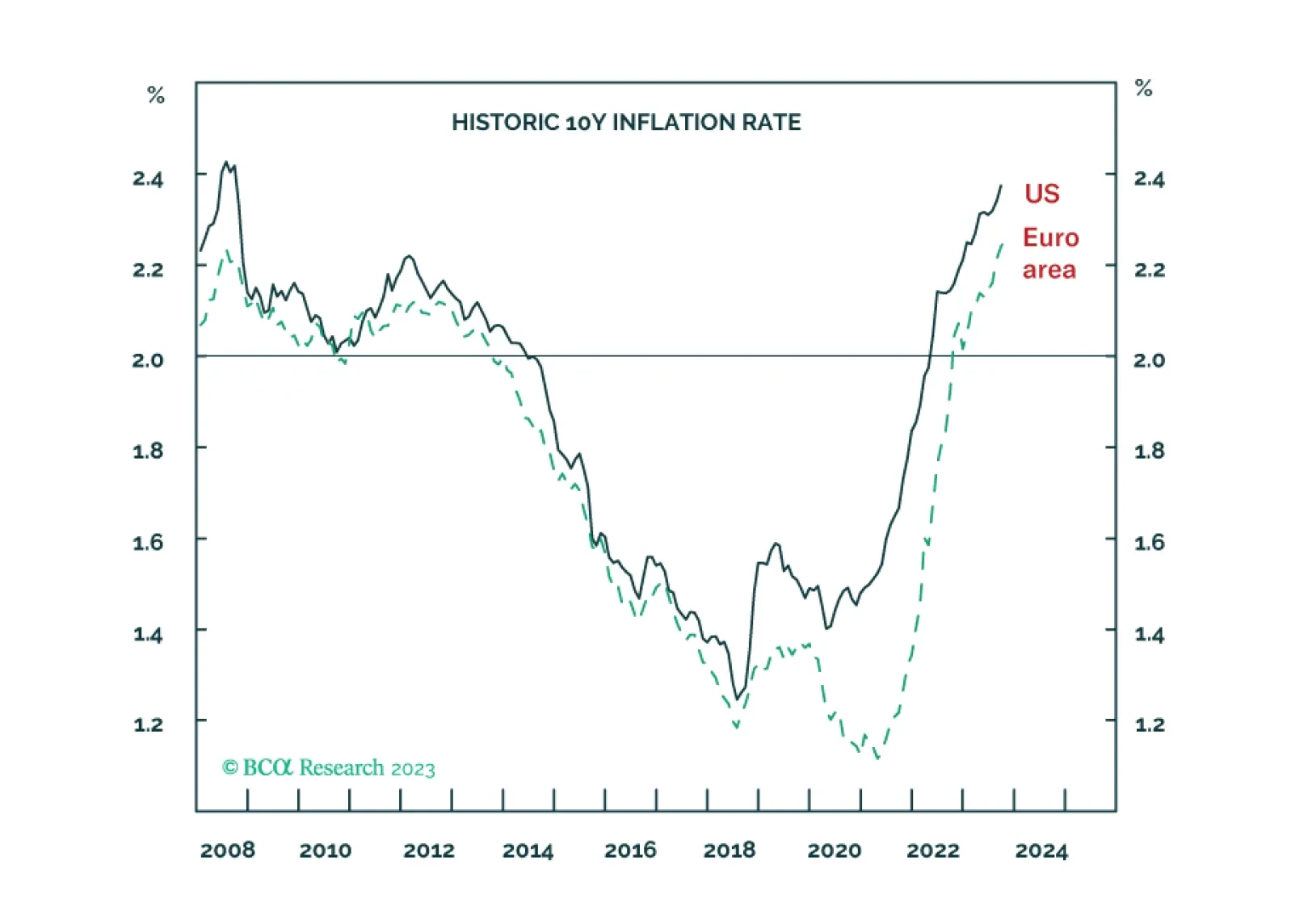

The fundamental component of long-term inflation expectations has climbed to its highest level since 2008 in both the US and the euro area. This means that both the Fed and the ECB will need to engineer inflation to undershoot 2 percent for an extended period if they are to maintain their 2 percent inflation targets. We explain what this means for investment strategy over the coming 6-12 months. Plus, we pinpoint what to focus on in this Friday’s US jobs report. And we identify food and beverages (PBJ) and the Indonesian rupiah (IDR/USD) as excellent rebound candidates.

High interest rates will eventually cause growth to slow. Signs of stress are already starting to show. Stay cautiously positioned.

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.

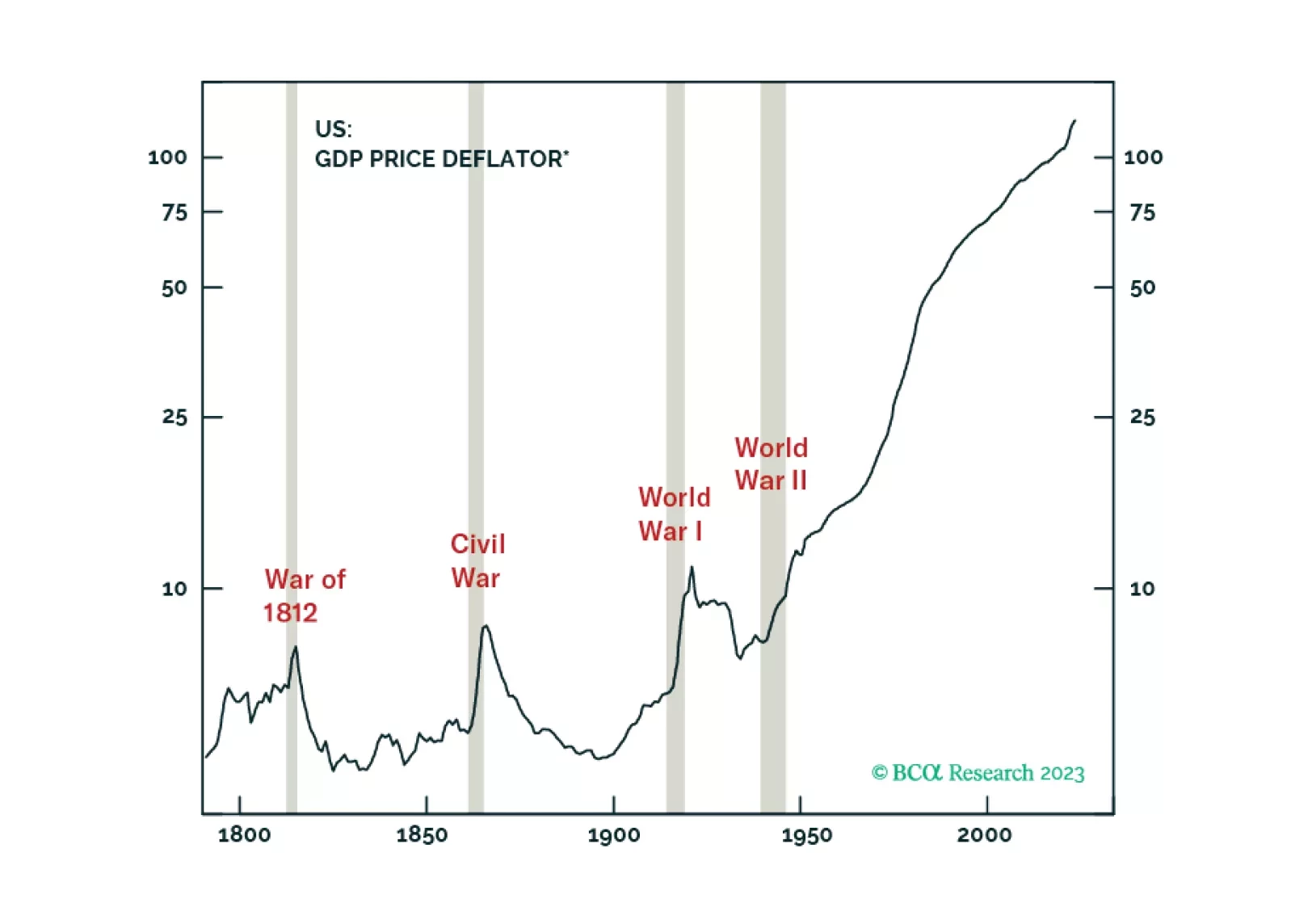

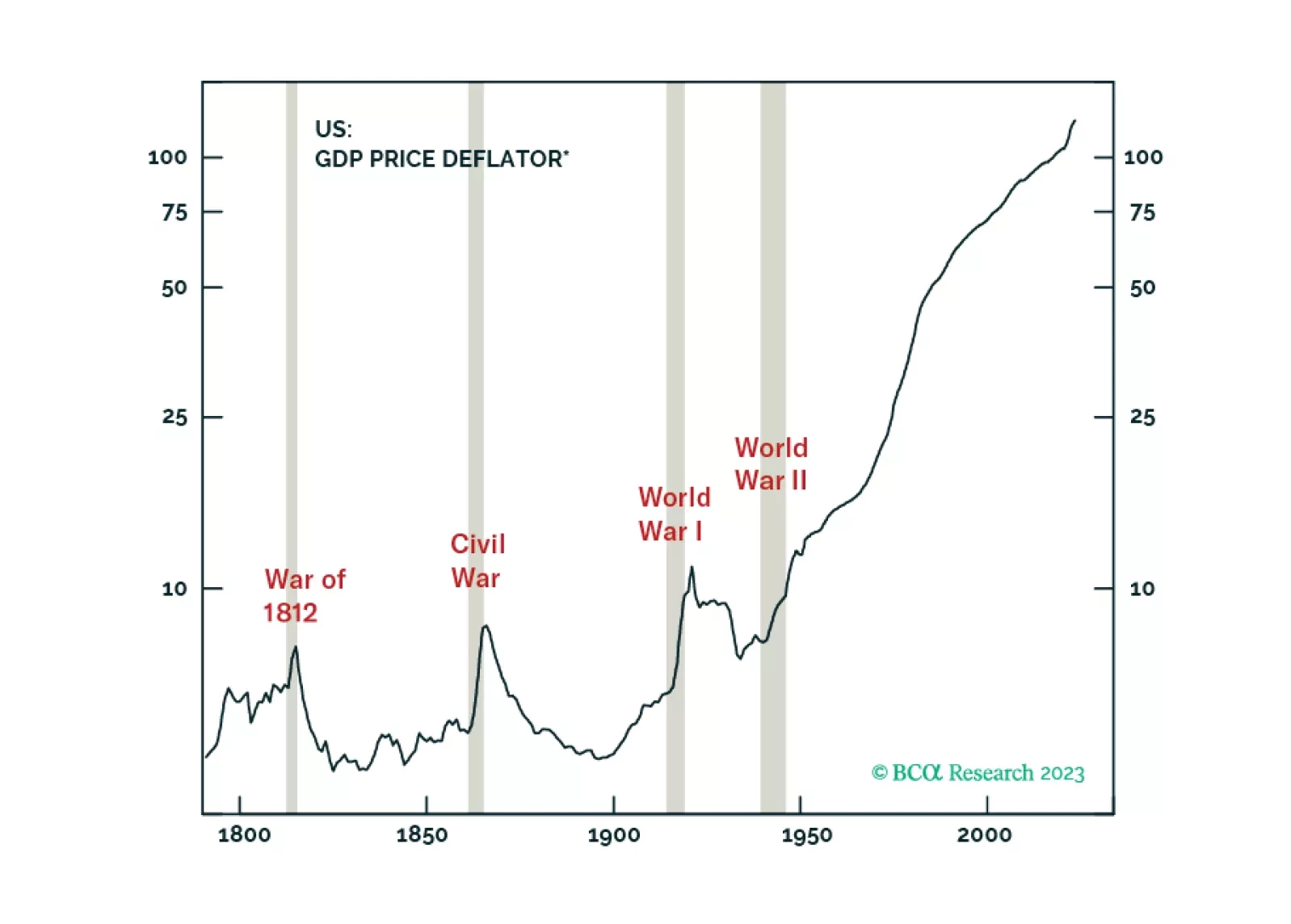

The Hamas attack against Israel, timed almost 50 years to the day after a similar surprise attack on Yom Kippur of 1973, has evoked parallels with the 1970s. Parallels not only with Middle Eastern geopolitics then and now, but also with inflation, economics, and financial markets. In this report, we explain what went wrong in the 1970s and whether the mistakes will be repeated. Plus: the sharp sell-offs in some Latin American currencies are reaching a potential turning-point.