Global

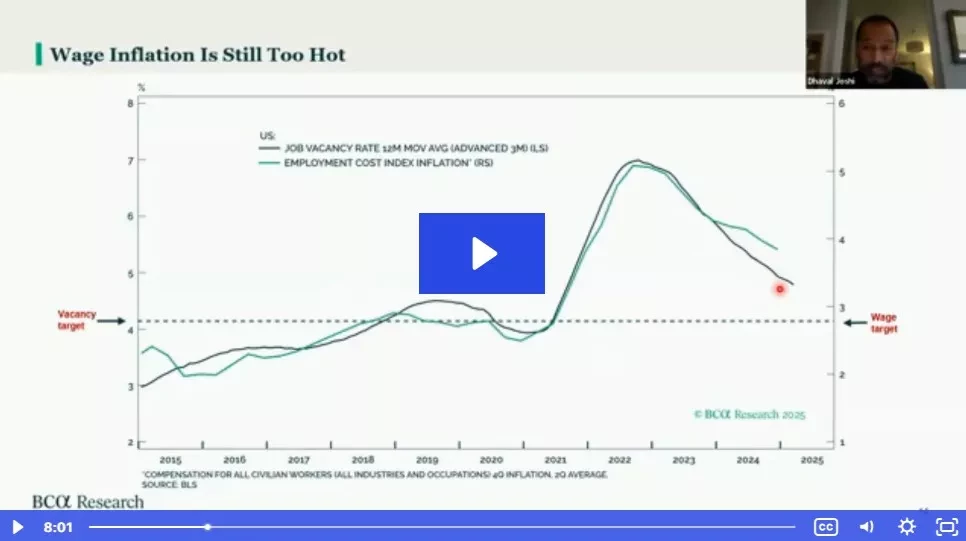

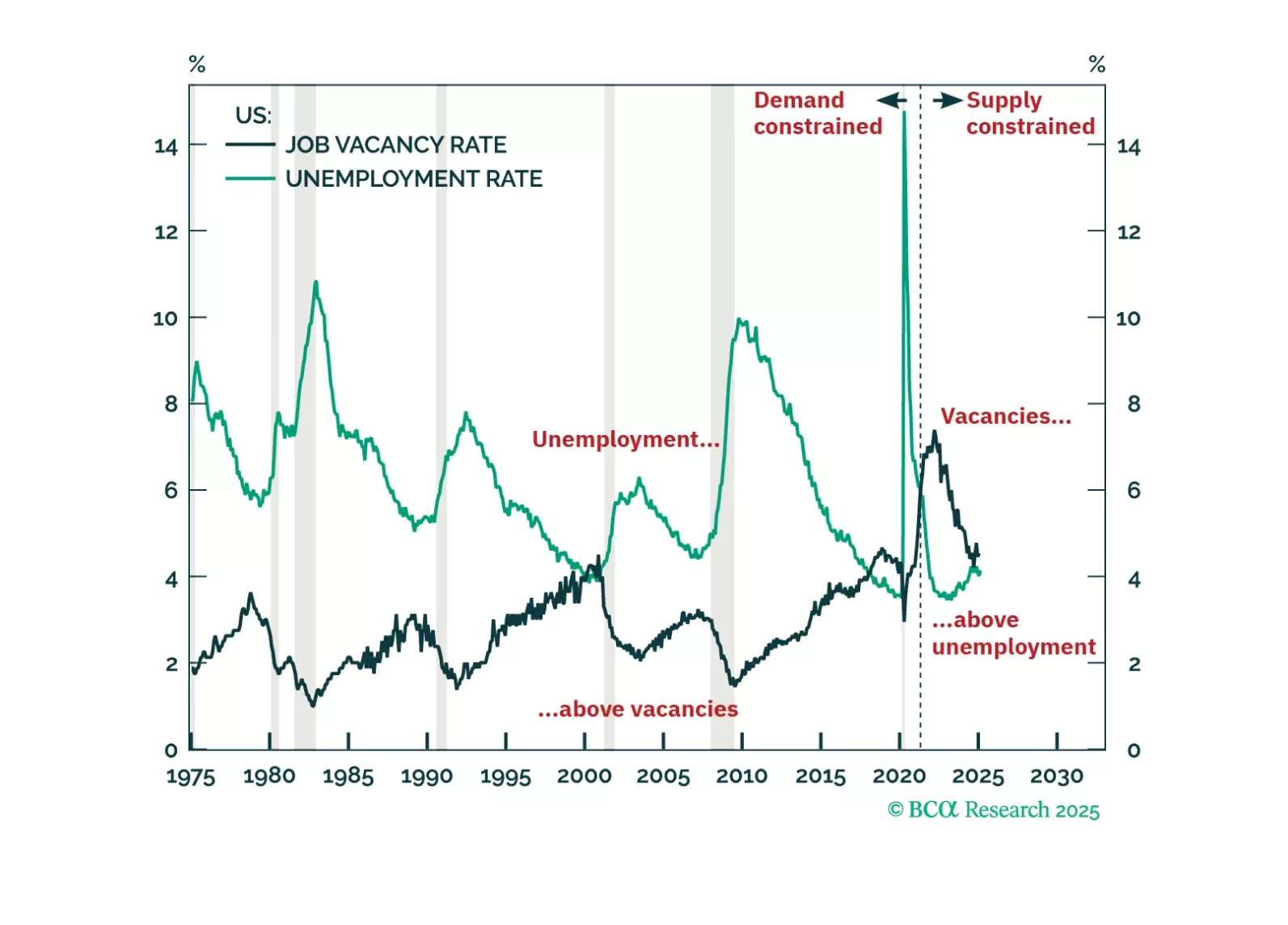

The US economy has never entered a demand-driven recession without labour demand running below labour supply and without the job vacancy rate running below the unemployment rate. Right now though, US labour demand is still running 1.7 million workers above labour supply, and the job vacancy rate is running comfortably above the unemployment rate. This suggests that the labour market is still supply-constrained, and that a demand-driven recession is not imminent. We discuss the investment implications. Plus, more about our ‘trade of the century’: long cotton versus coffee.

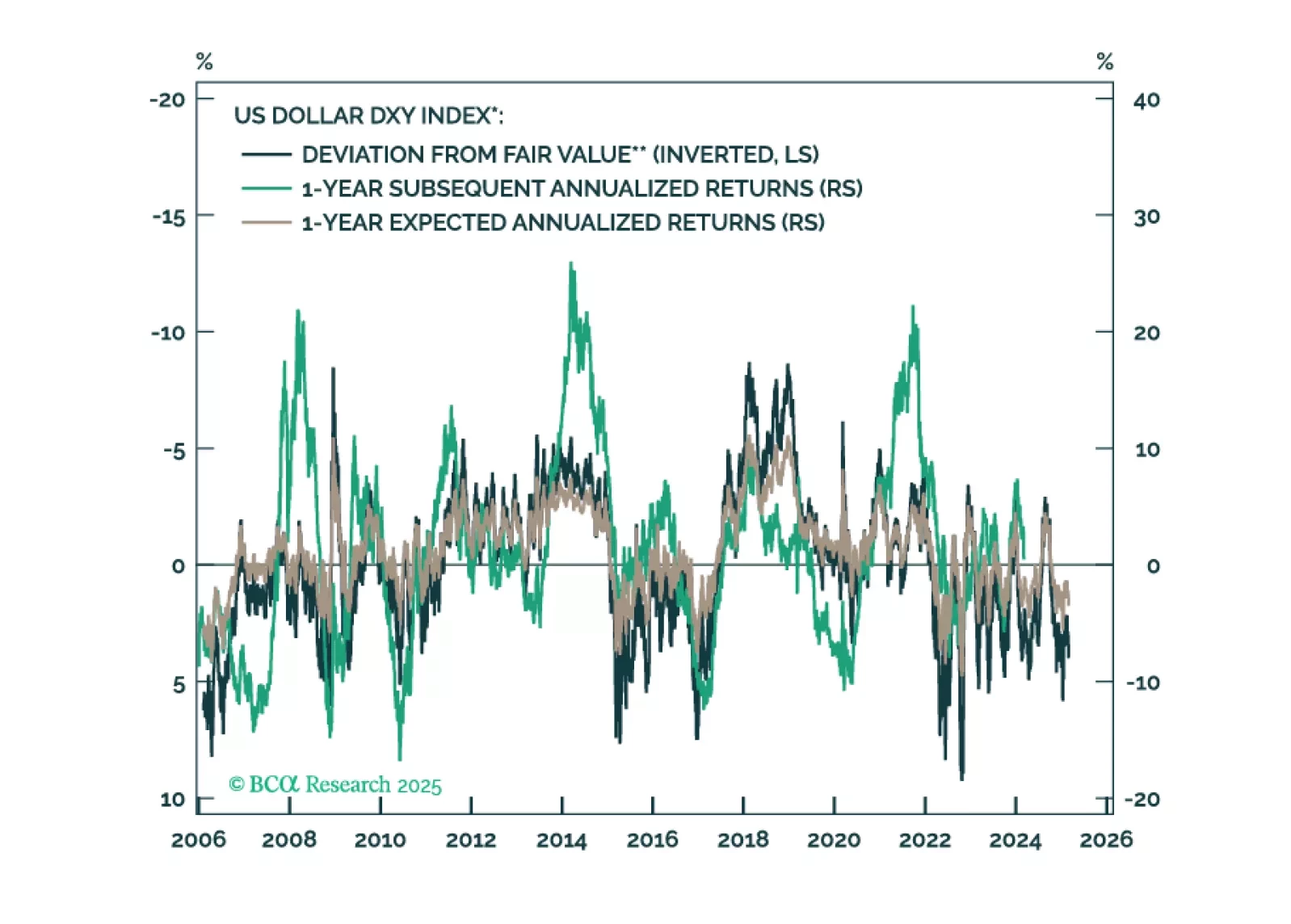

This report is our Part III series on valuation and subsequent returns, where we recalibrate our short-term models to emphasize signals over the next nine-to-twelve months. We will henceforth call these models STTM: Short Term Timing Models.

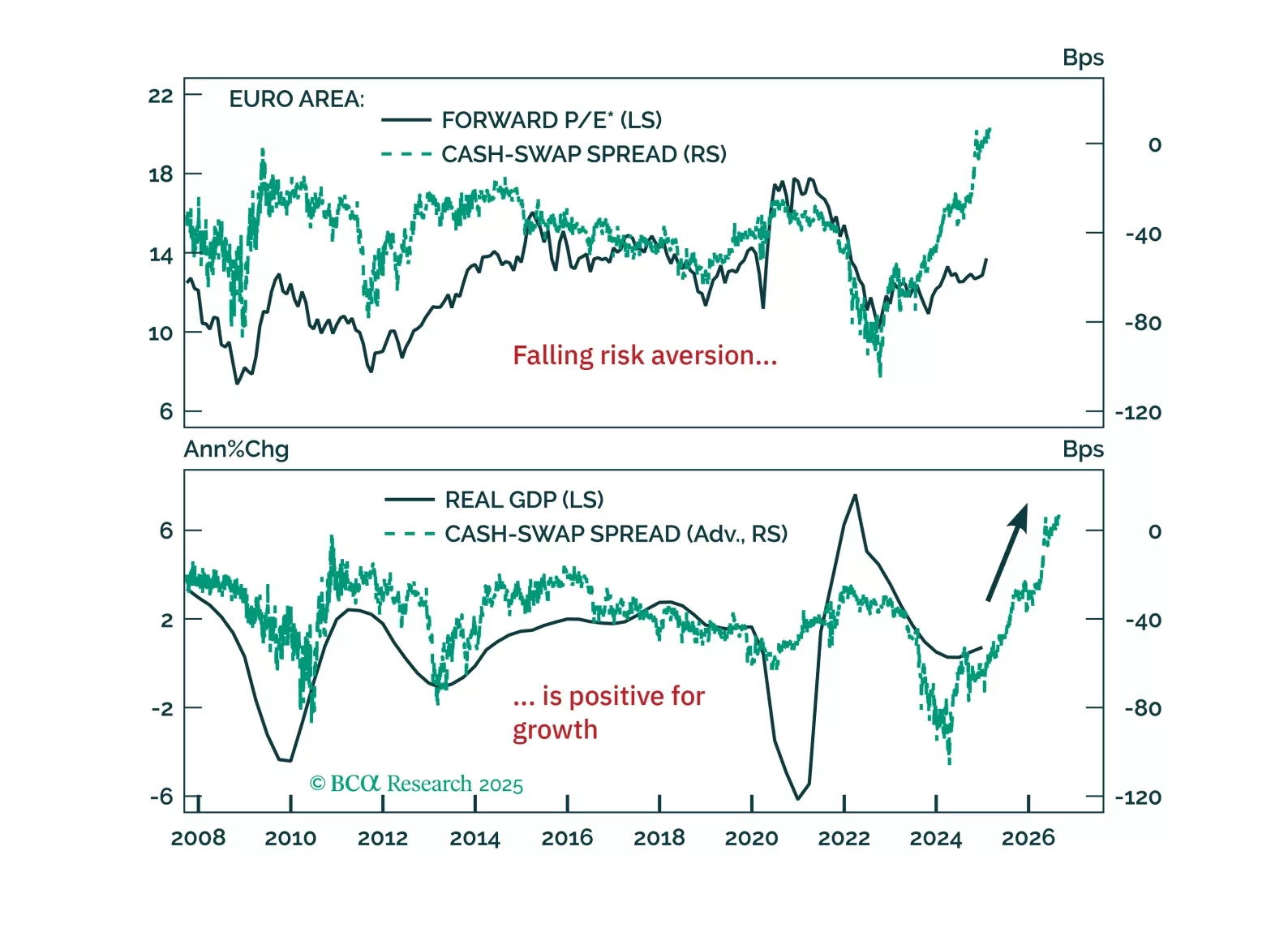

Europe’s resilience to global liquidity deterioration isn’t a fluke—it signals a structural shift. Our latest report explains why the decline in precautionary money demand marks the end of Europe’s liquidity trap and what it means for investors.