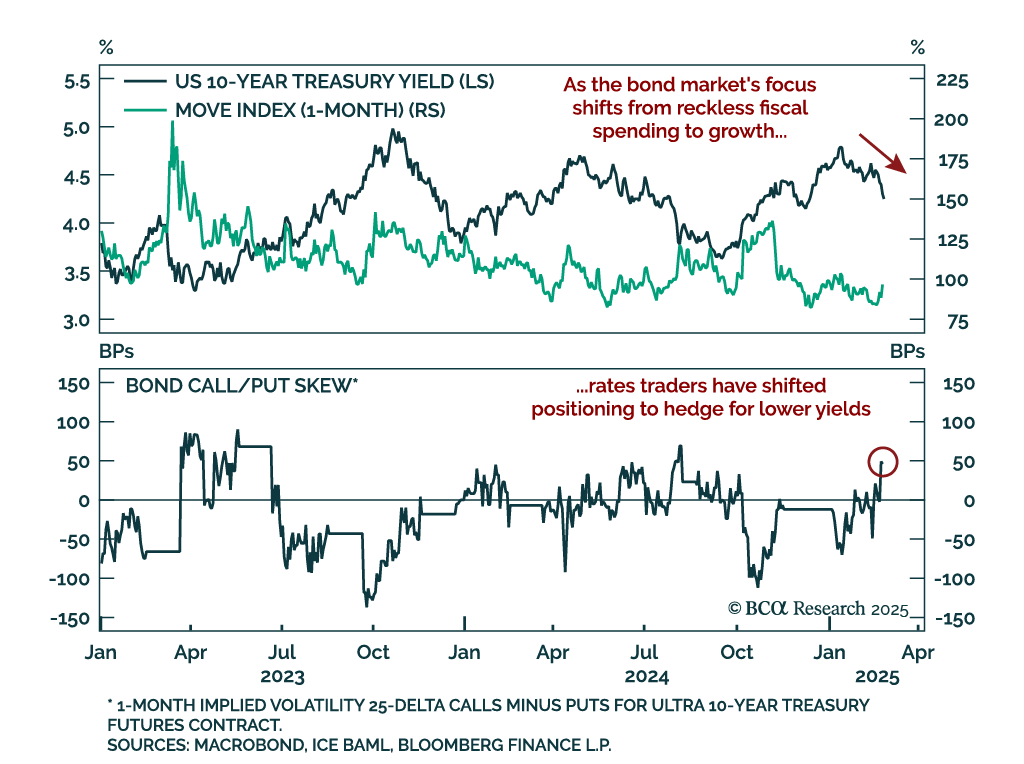

Gov Sovereigns/Treasurys

Core PCE inflation was tame this morning, but with large tariffs looming we anticipate loftier inflation readings in the months ahead.

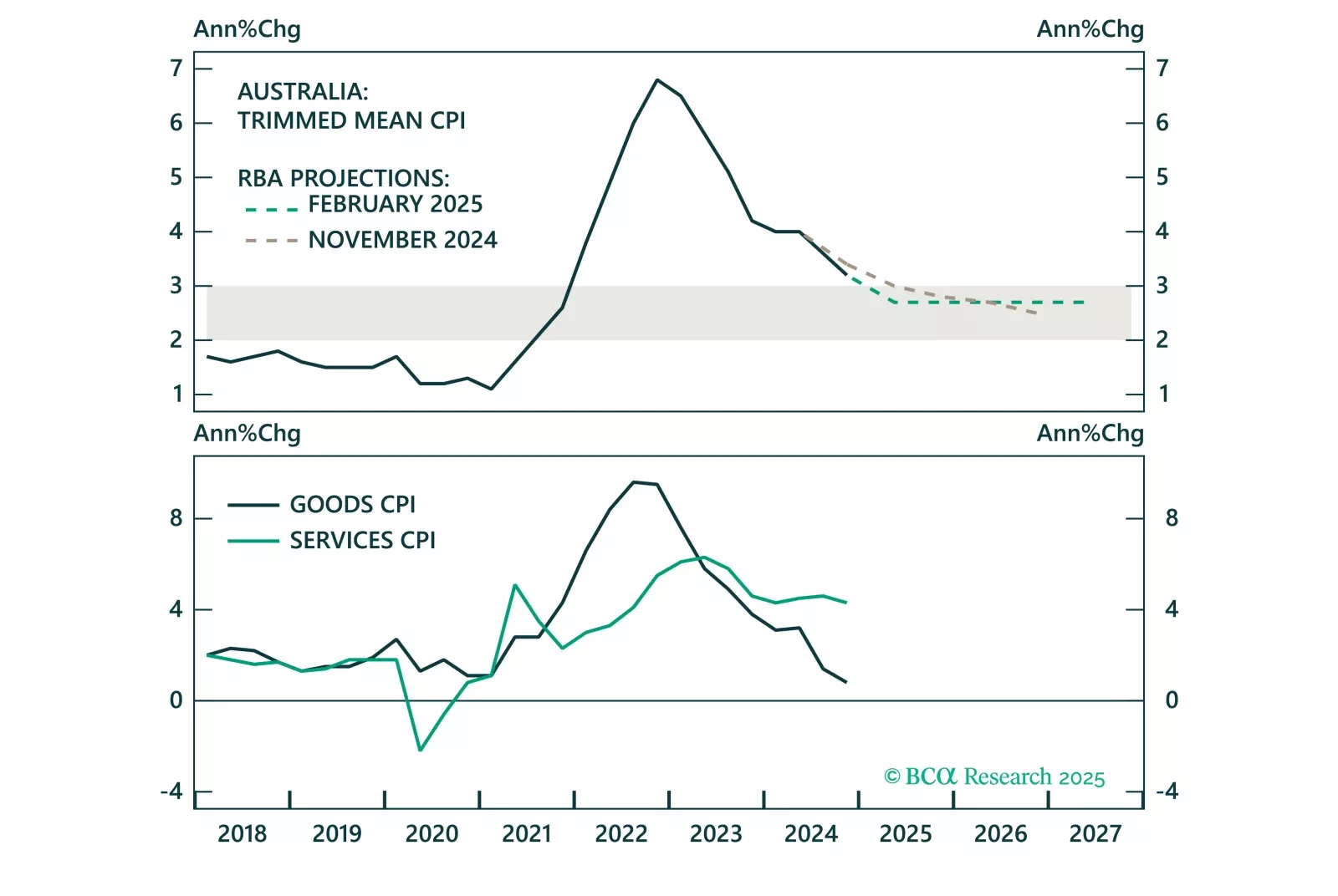

Overnight, the RBA cut the cash target rate for the first time since 2022, marking the beginning of the policy easing cycle in Australia. However, the RBA will proceed cautiously with further rate cuts, given a tight labor market and still elevated services inflation. This will keep Australian government bond yields elevated versus global yields, benefitting the Australian dollar.

In lieu of all the geopolitical and economic news in media, this report looks at where next the dollar is likely to trend in the next one-to-three months. Our view is down, though on a cyclical horizon (six-to-twelve months), we would not be short the dollar, for now.

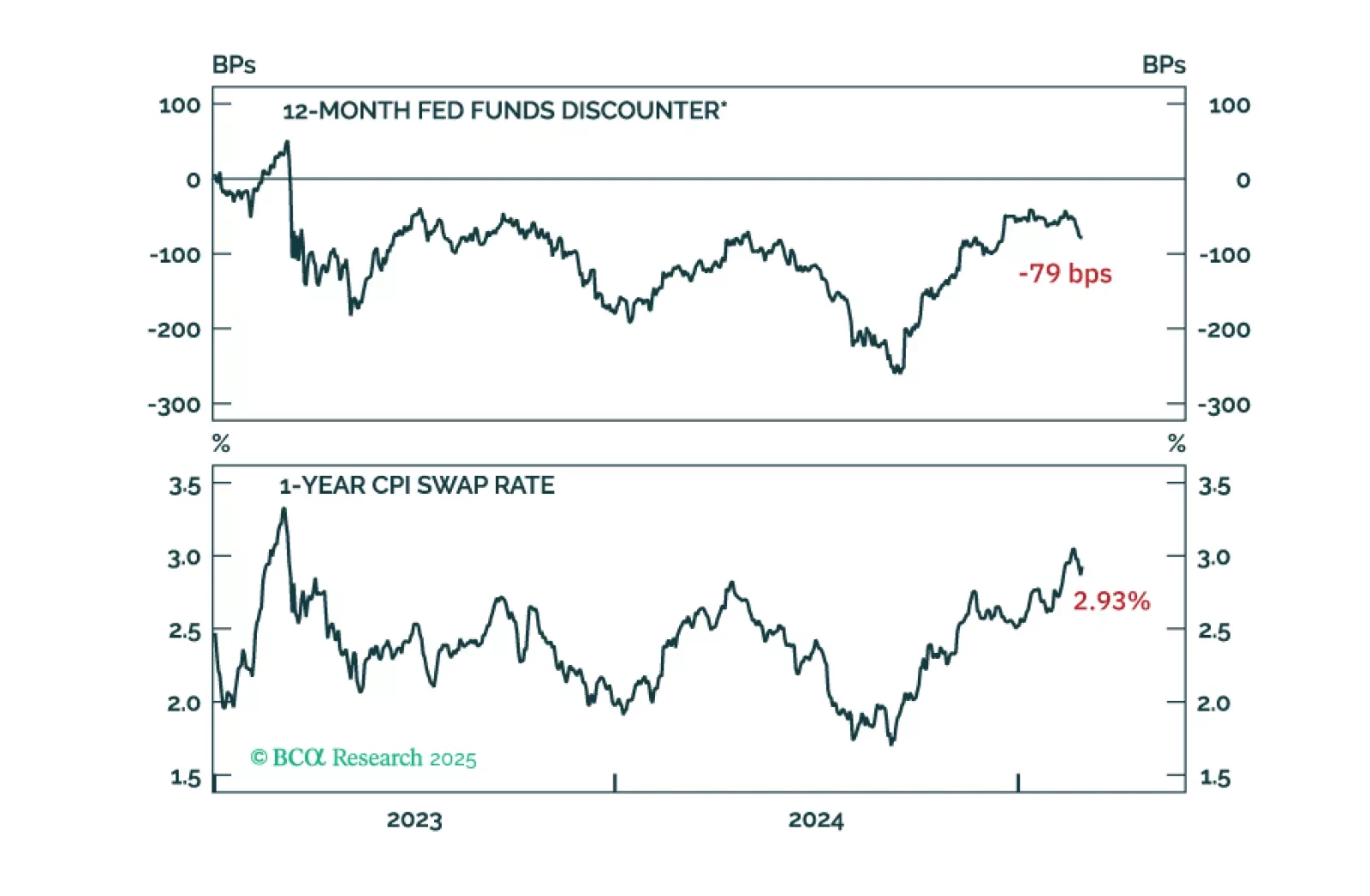

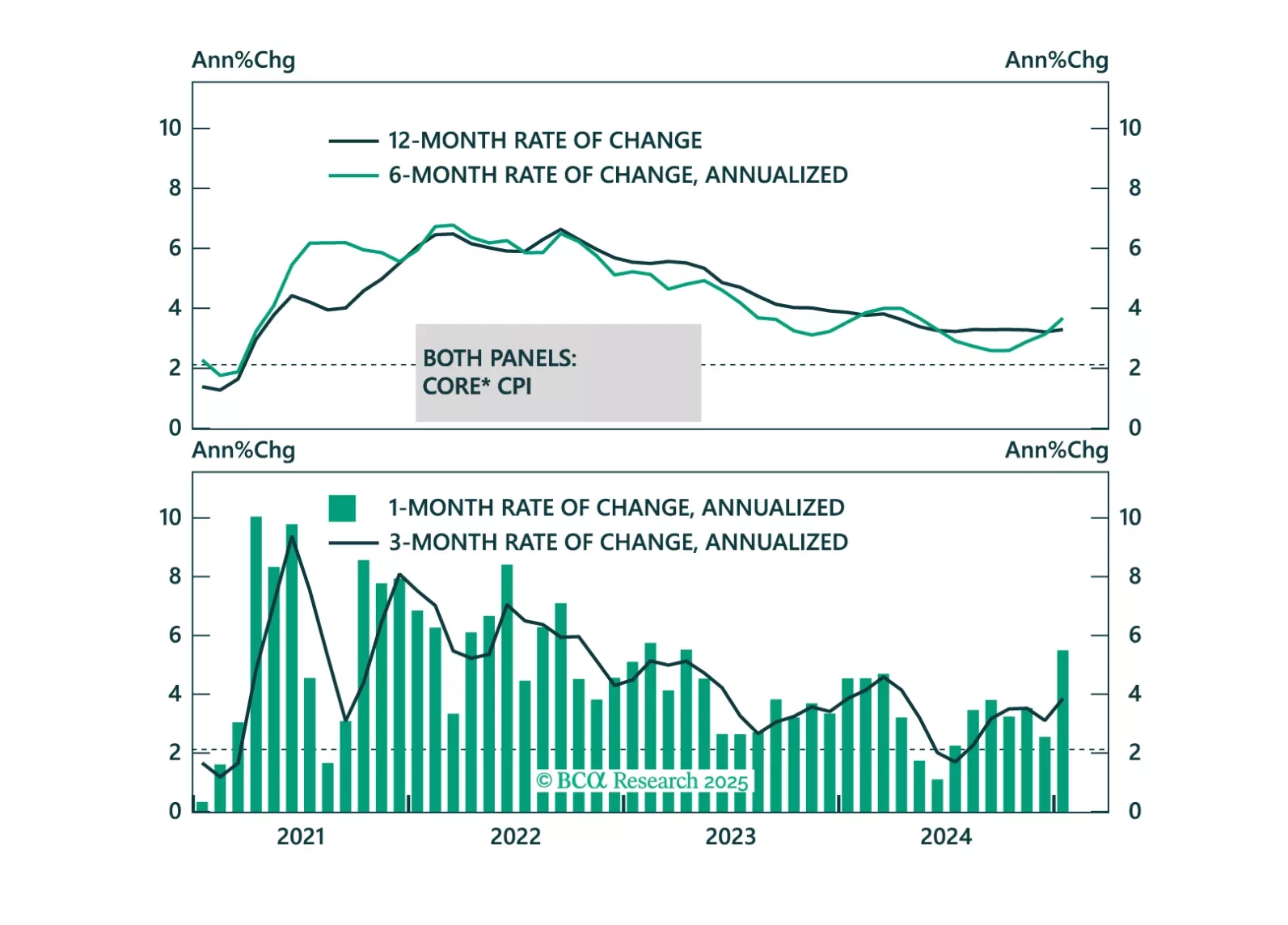

Some thoughts on this morning’s CPI report and its implications for the Fed and Treasury yields.

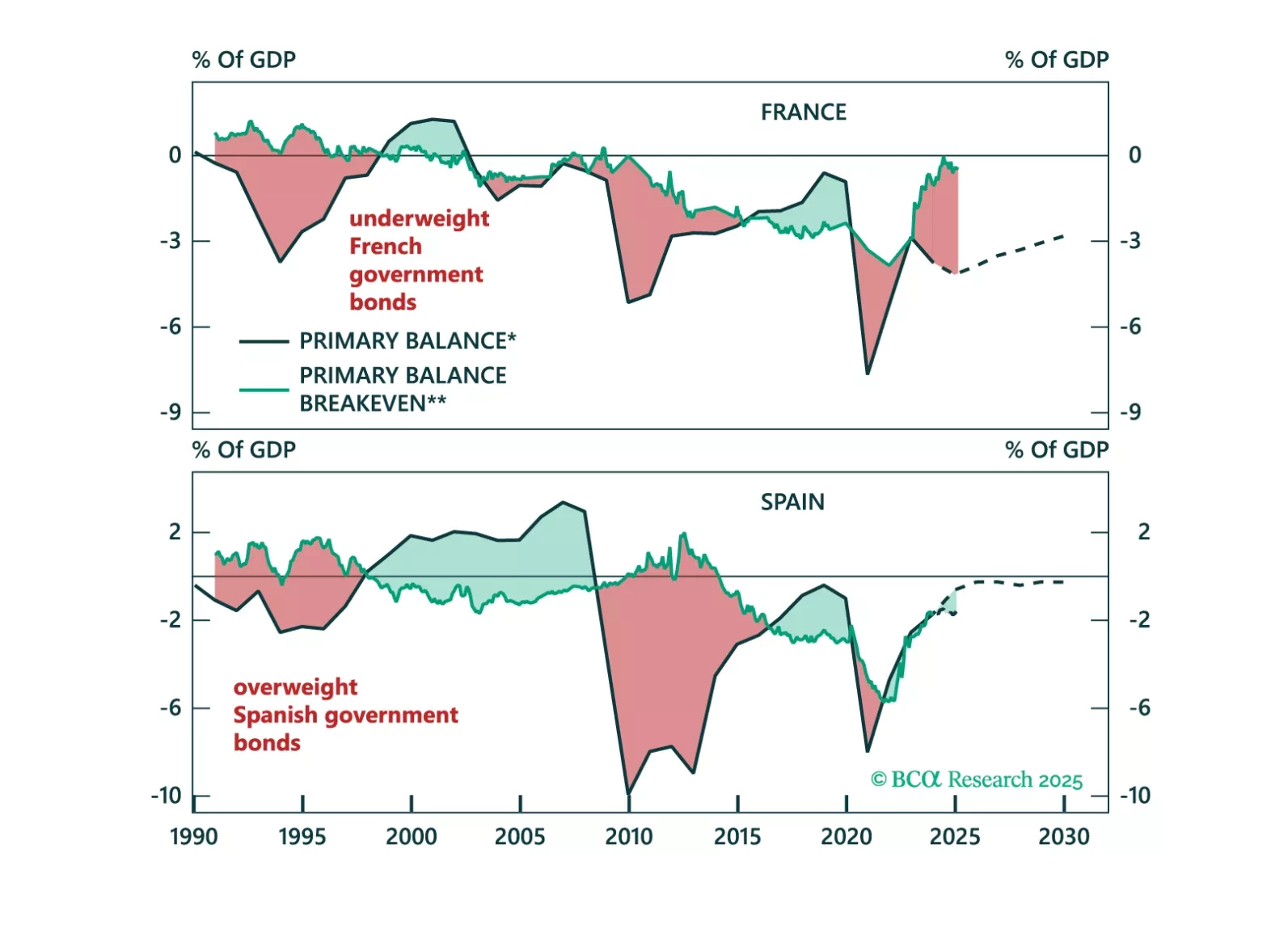

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.