Gov Sovereigns/Treasurys

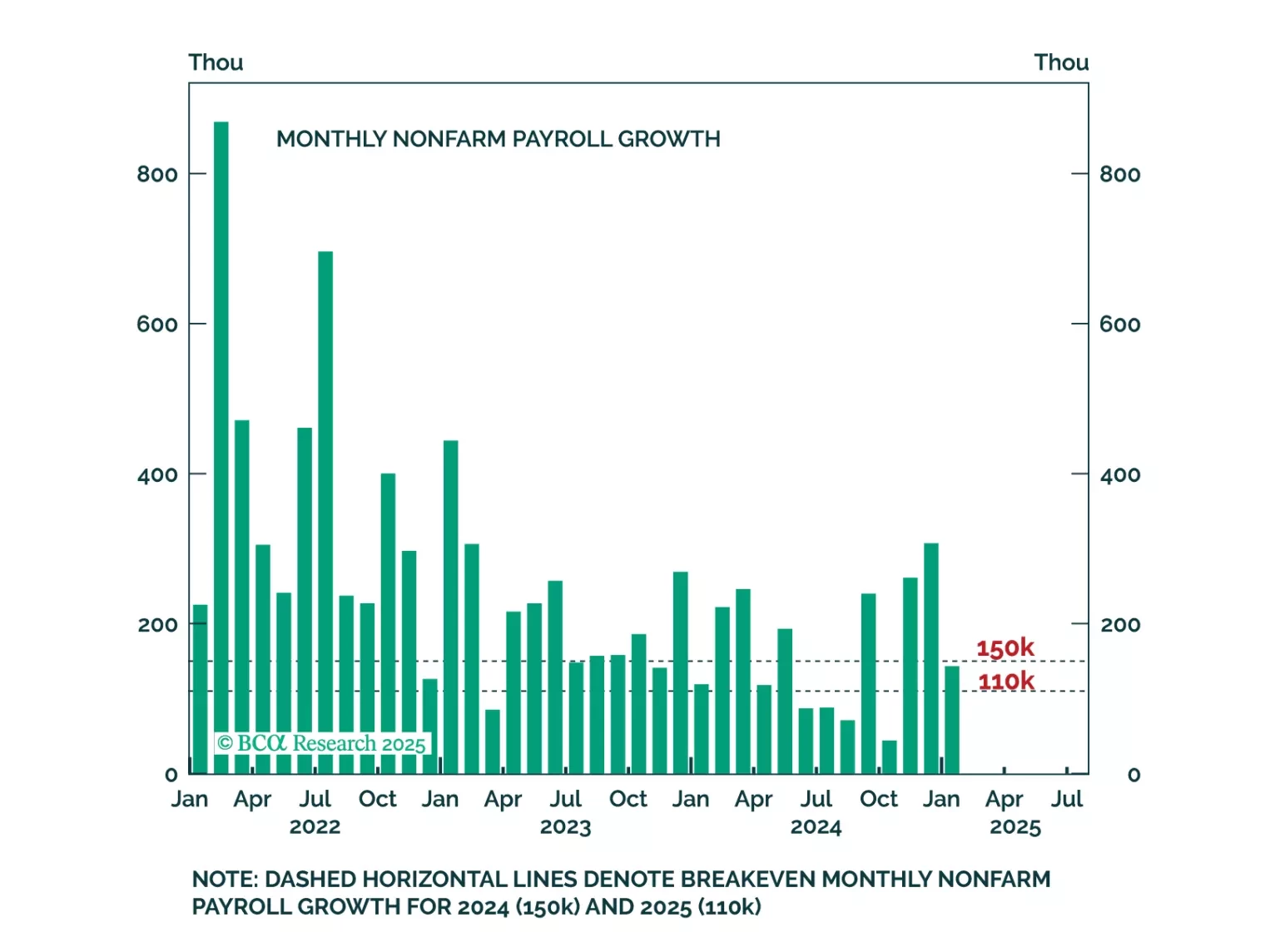

Some thoughts on this morning's employment data and Treasury Secretary Bessent's recent attempts to talk down the 10-year Treasury yield.

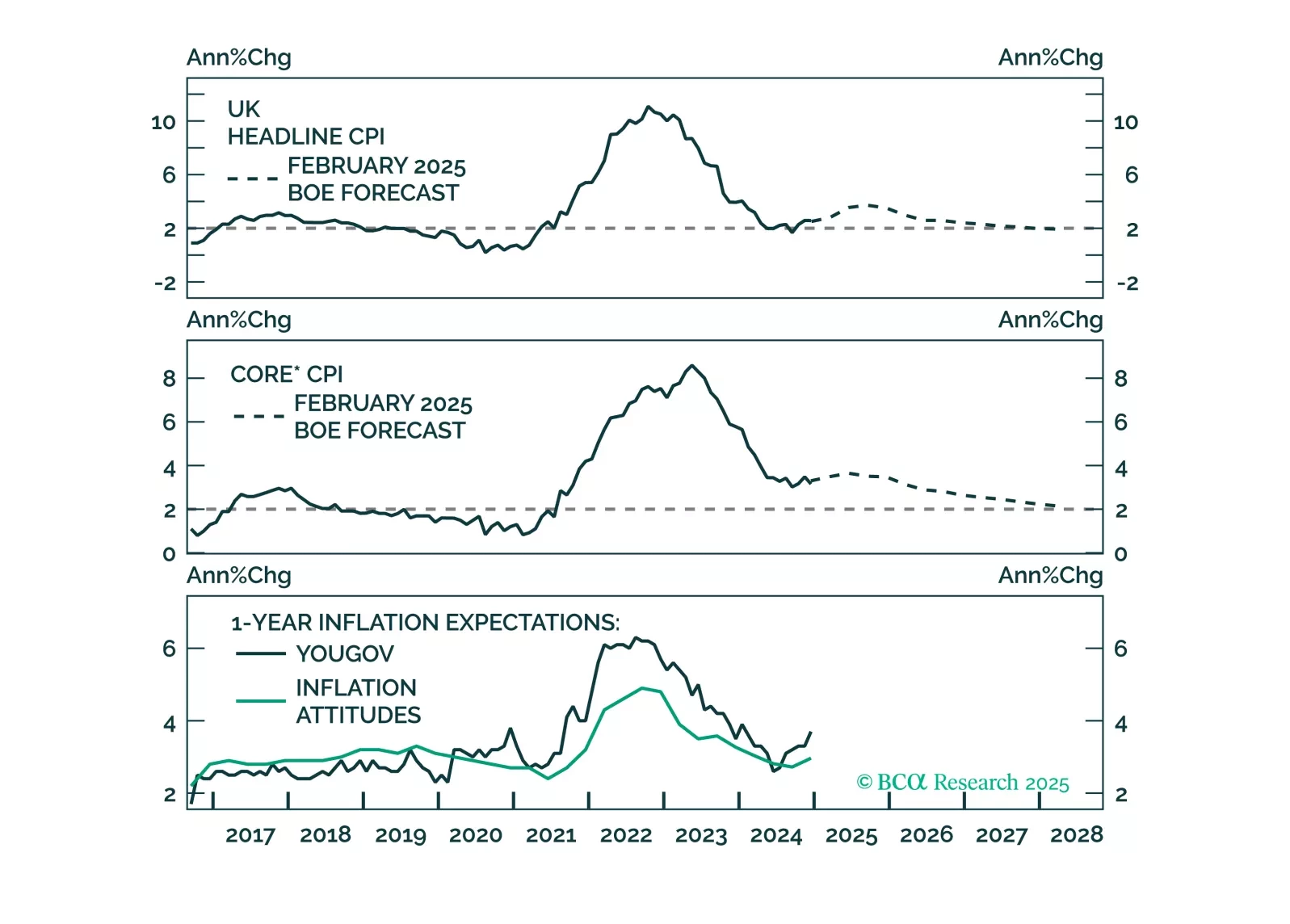

Following today’s Bank of England’s policy meeting, at which the policy rate was cut by 25 bps, we discuss our outlook for monetary policy in the UK. We expect the gradual easing to continue and discuss the investment implications for UK gilts and sterling.

Our Portfolio Allocation Summary for January 2025.

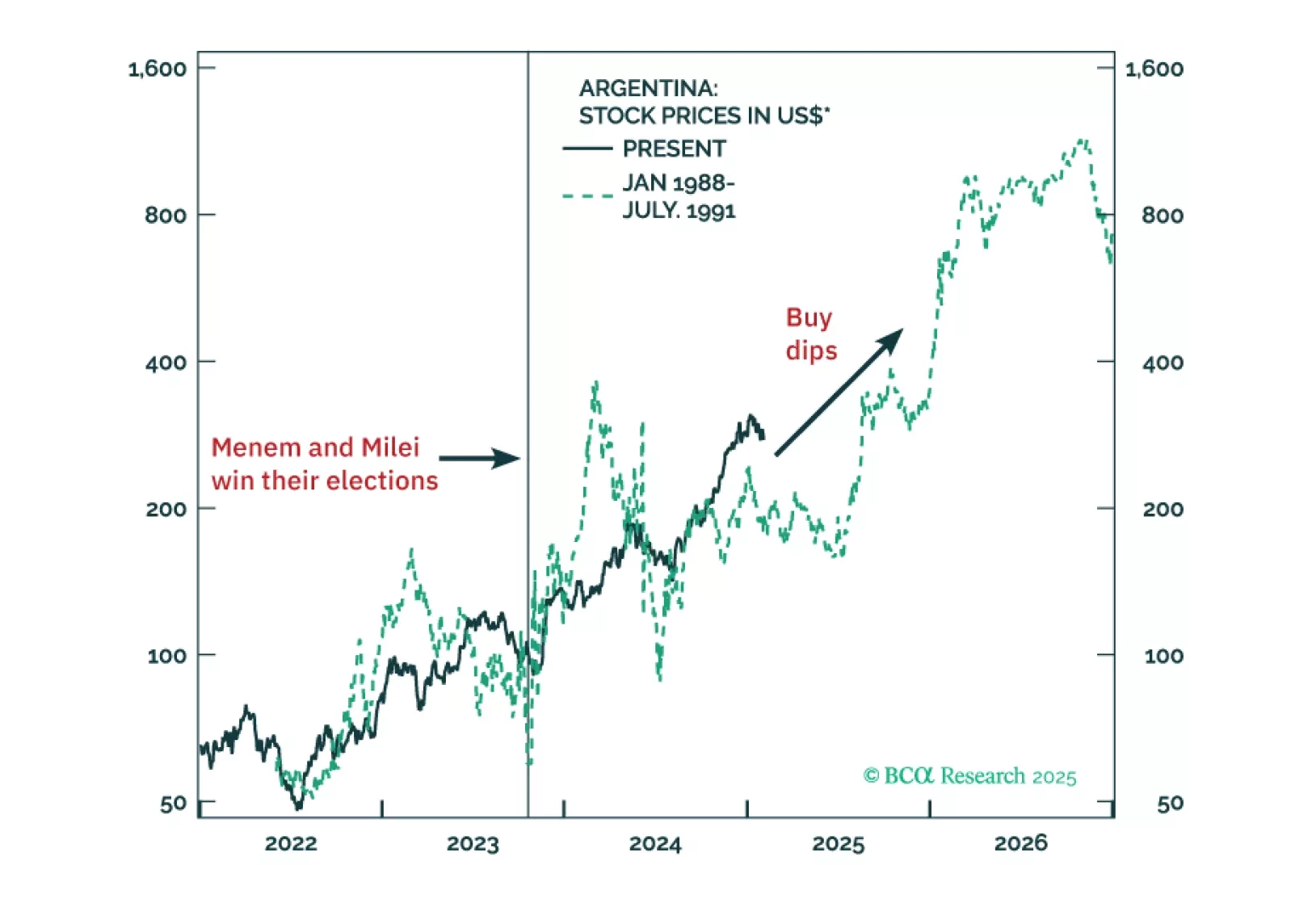

Argentina is entering a regime shift from the traditional short boom-bust cycles of the past 50 years. Profound structural reforms will result in a productivity boom, leading to a more durable economic expansion while keeping with the disinflation trend. Authorities will likely lift capital and currency controls in the second quarter of this year. All in all, odds are that Argentinian assets have entered a multi-year bull market.

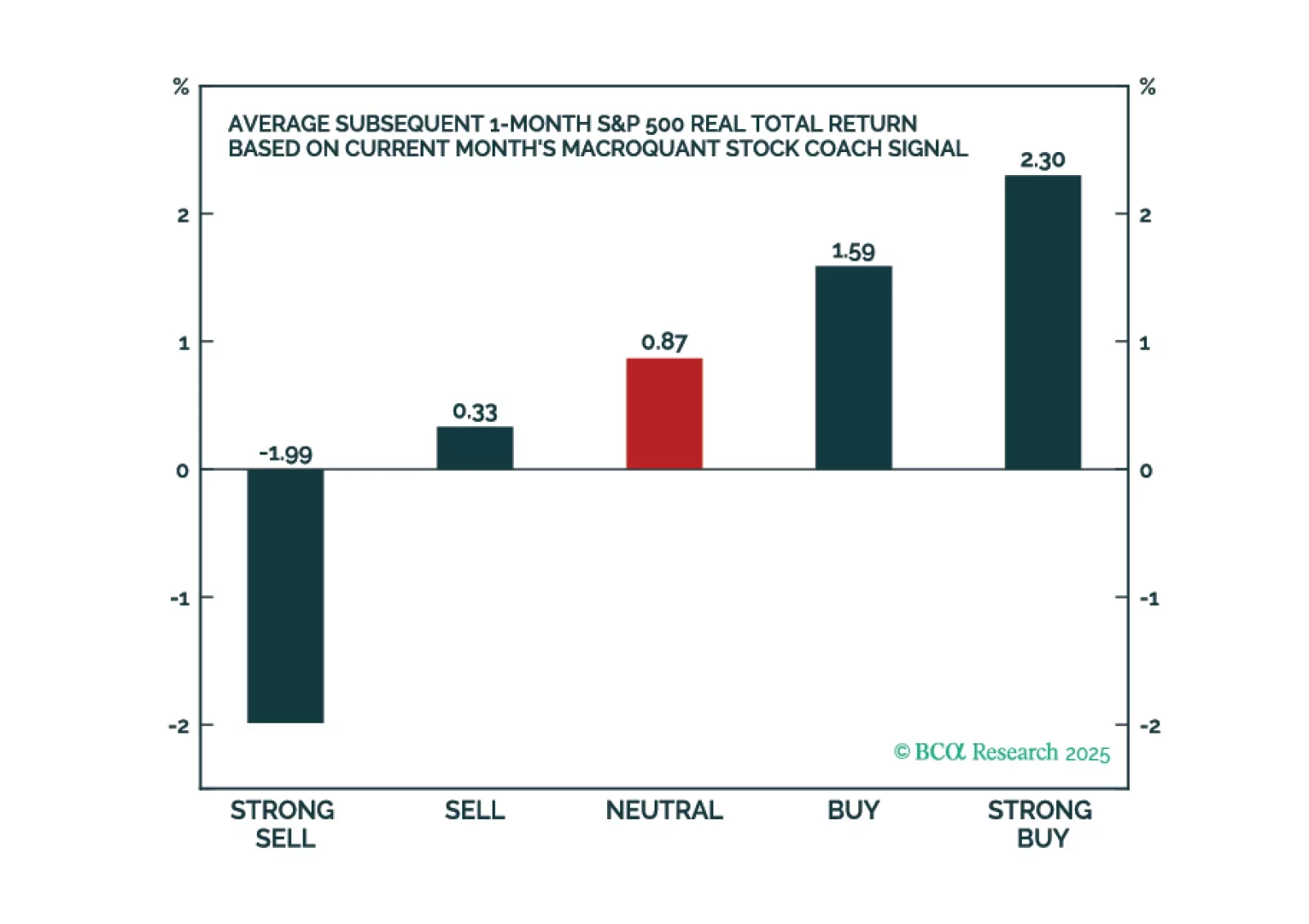

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

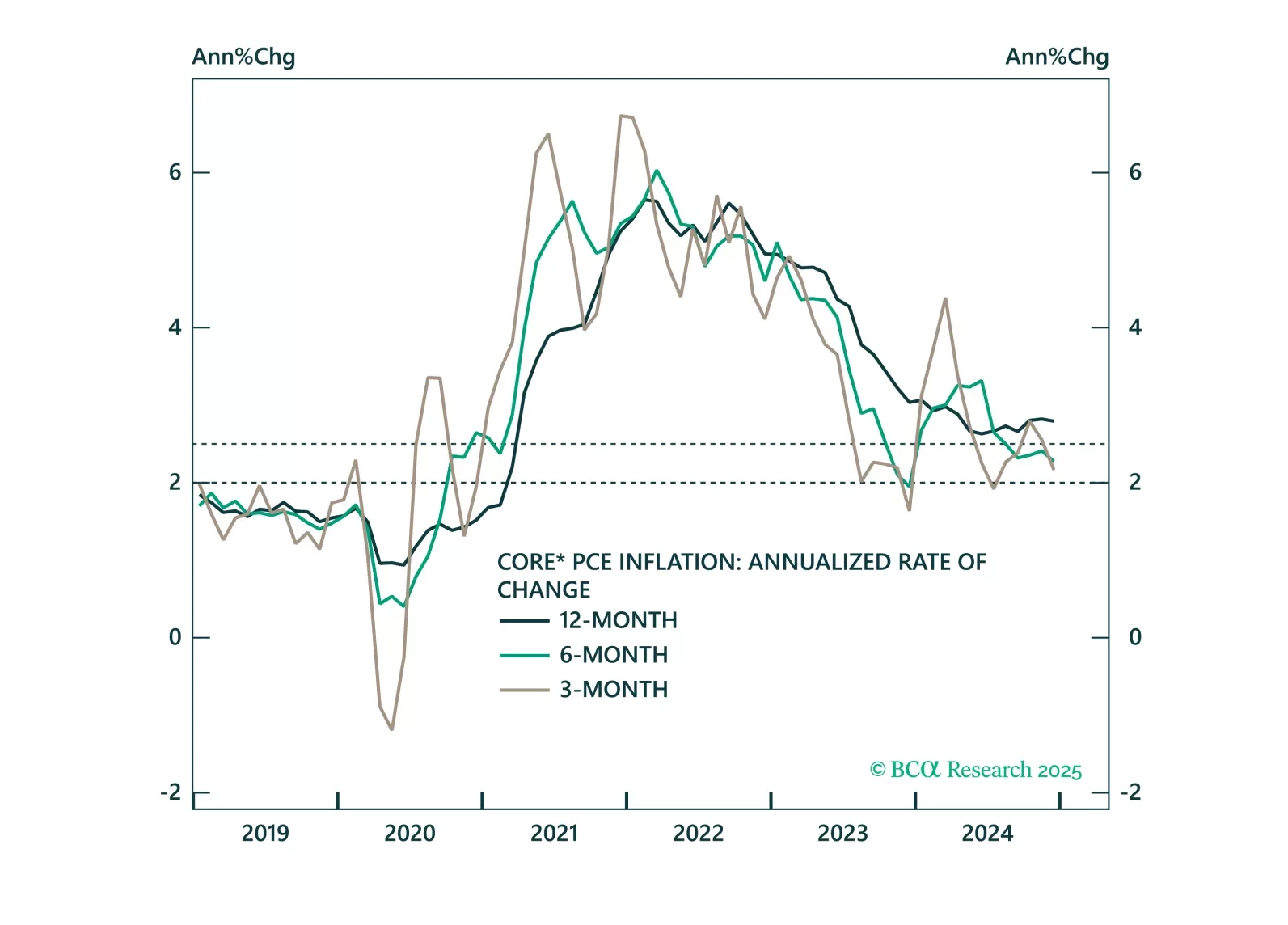

Core PCE inflation came in soft this morning and is tracking well below the Fed’s 2025 forecast. We highlight three upside risks to inflation and preview next week’s employment report.

Jay Powell didn’t say much at this afternoon’s FOMC press conference, and monetary policy will continue to take a back seat to fiscal for the next few months.

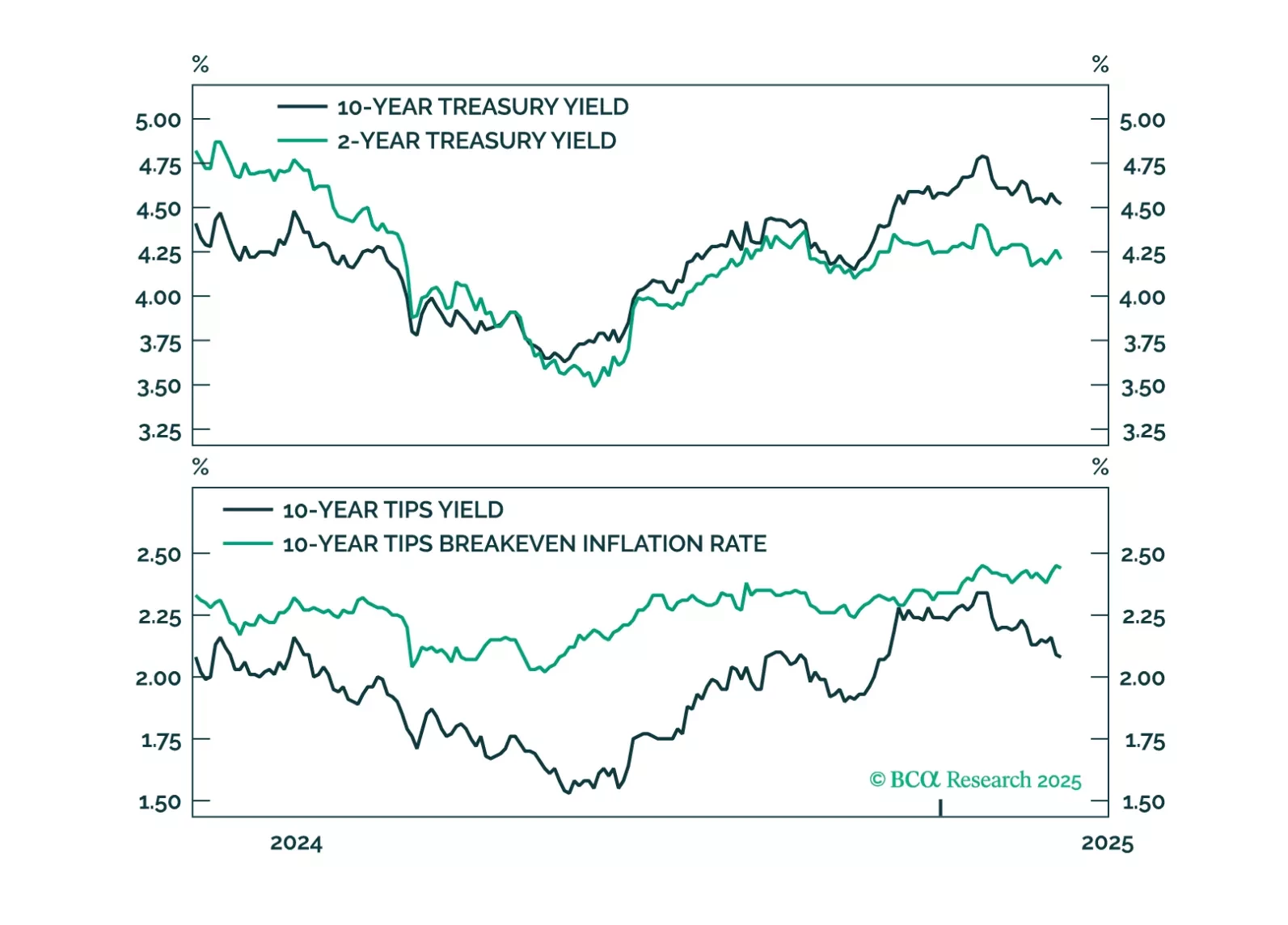

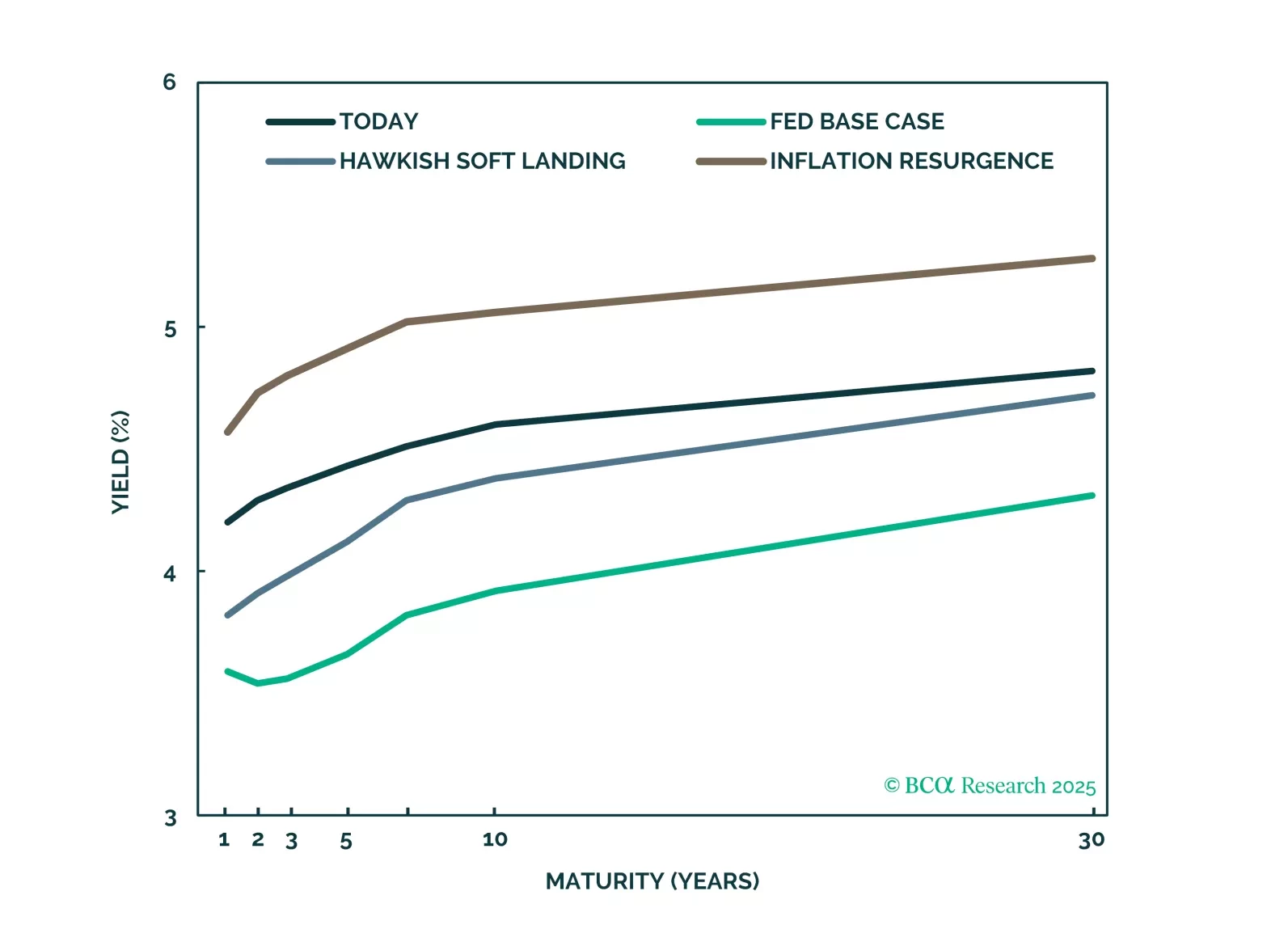

We forecast Treasury and corporate bond returns in three different economic scenarios. This report focuses on what returns might look like in a scenario where inflation is sticky and the Fed makes a hawkish pivot.