Gov Sovereigns/Treasurys

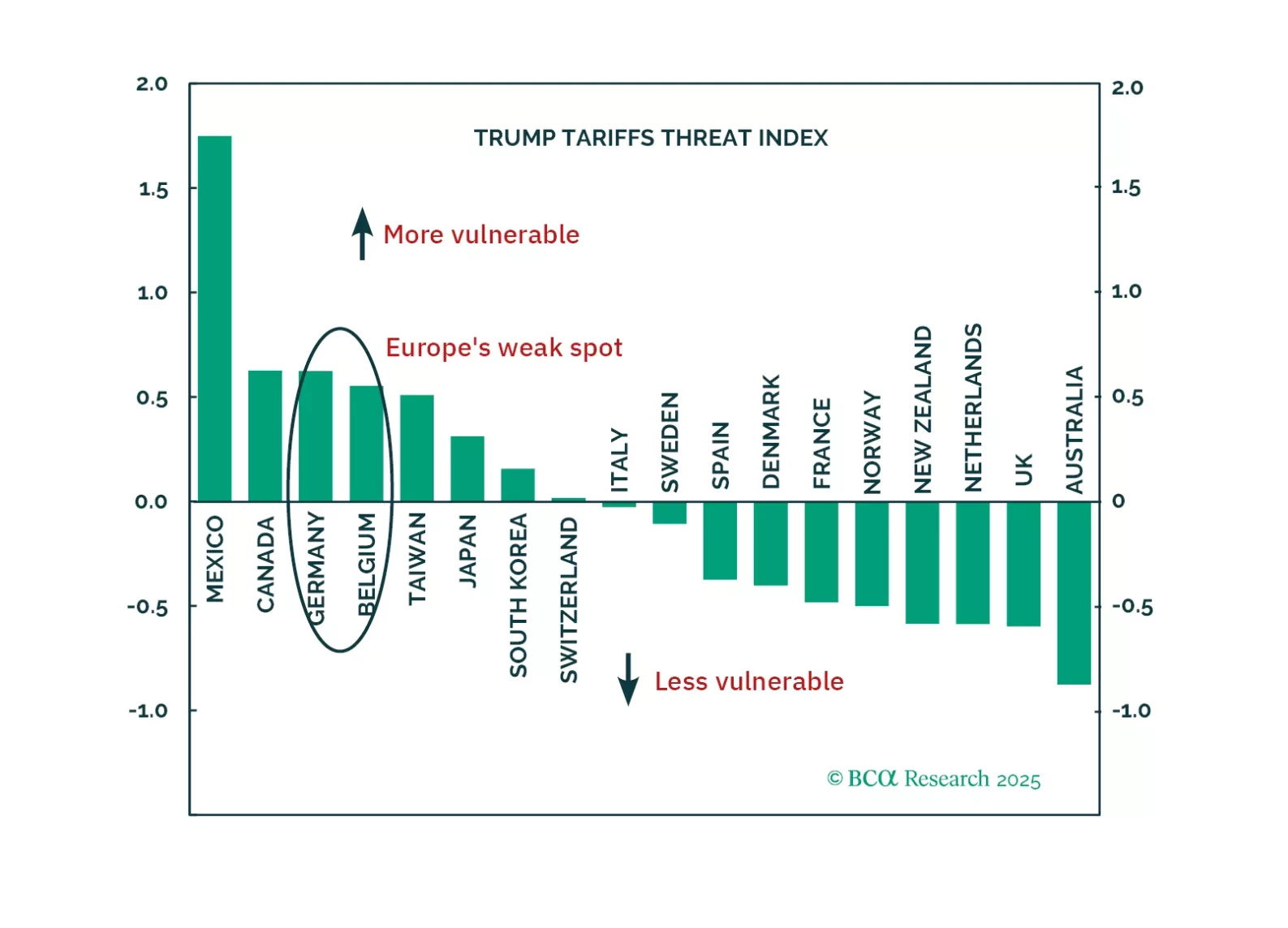

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

We examine Treasury market valuation and look for indicators that could help us time the next peak in yields. We also update the forecasts from our Treasury yield model.

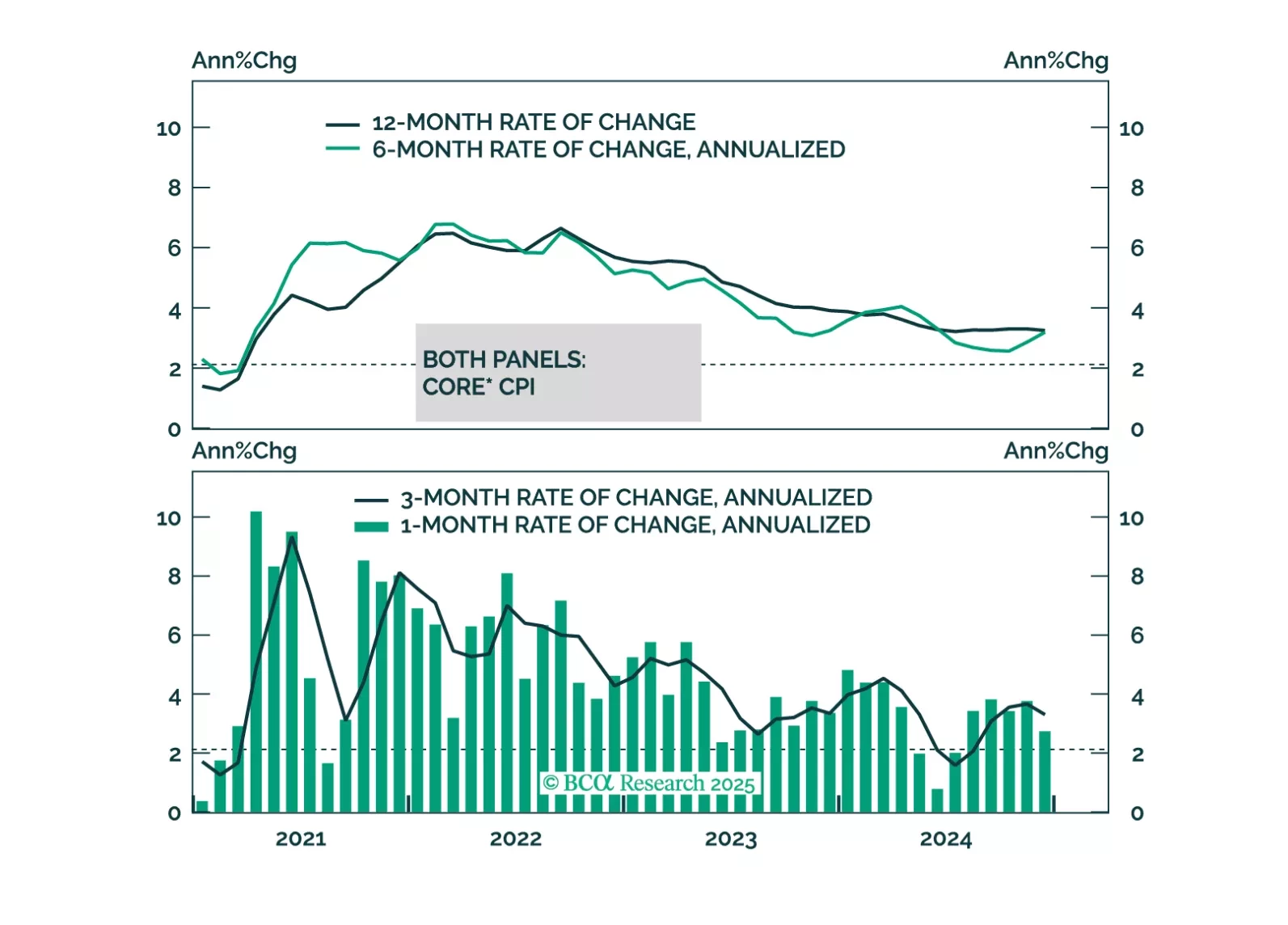

Our thoughts on this morning’s CPI release and some upside risks to inflation that could flare up in the months ahead.

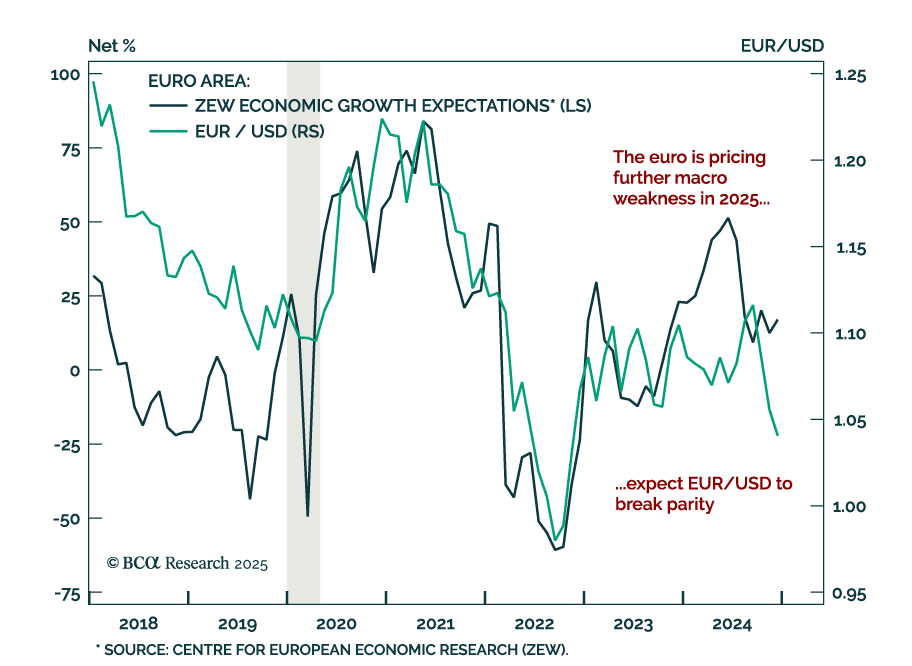

This month, our Here, There, And Everywhere chartpack reiterates our main thesis for 2025: the three main narratives driving markets today – fiscal profligacy, trade war, and geopolitical conflict – will peak at some point in 2025. Why does this matter? All three have been tailwinds to US assets, and their peak should help usher in the peak in US outperformance relative to RoW. We conclude with some slides on our bullish Europe thesis.

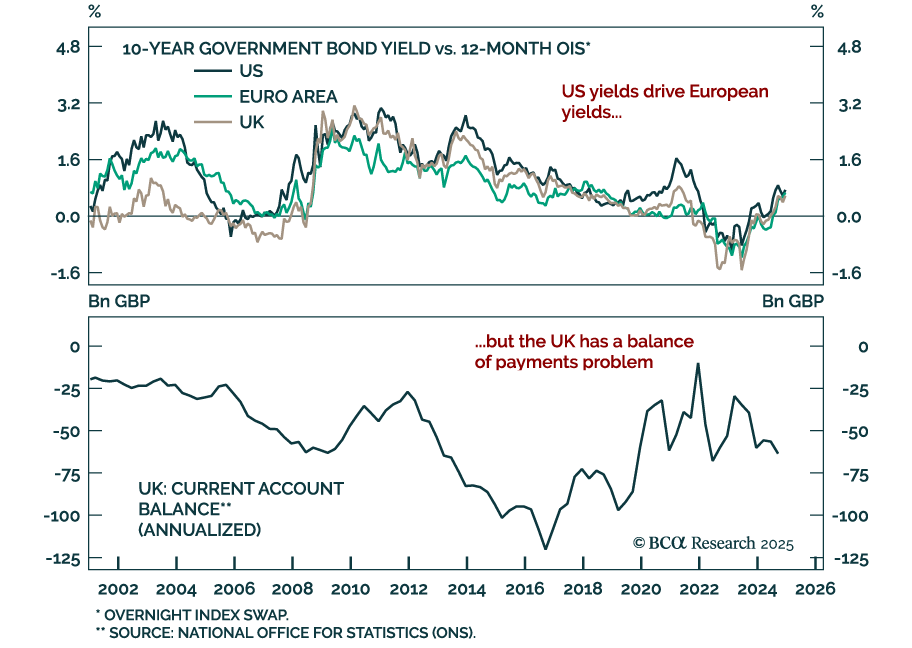

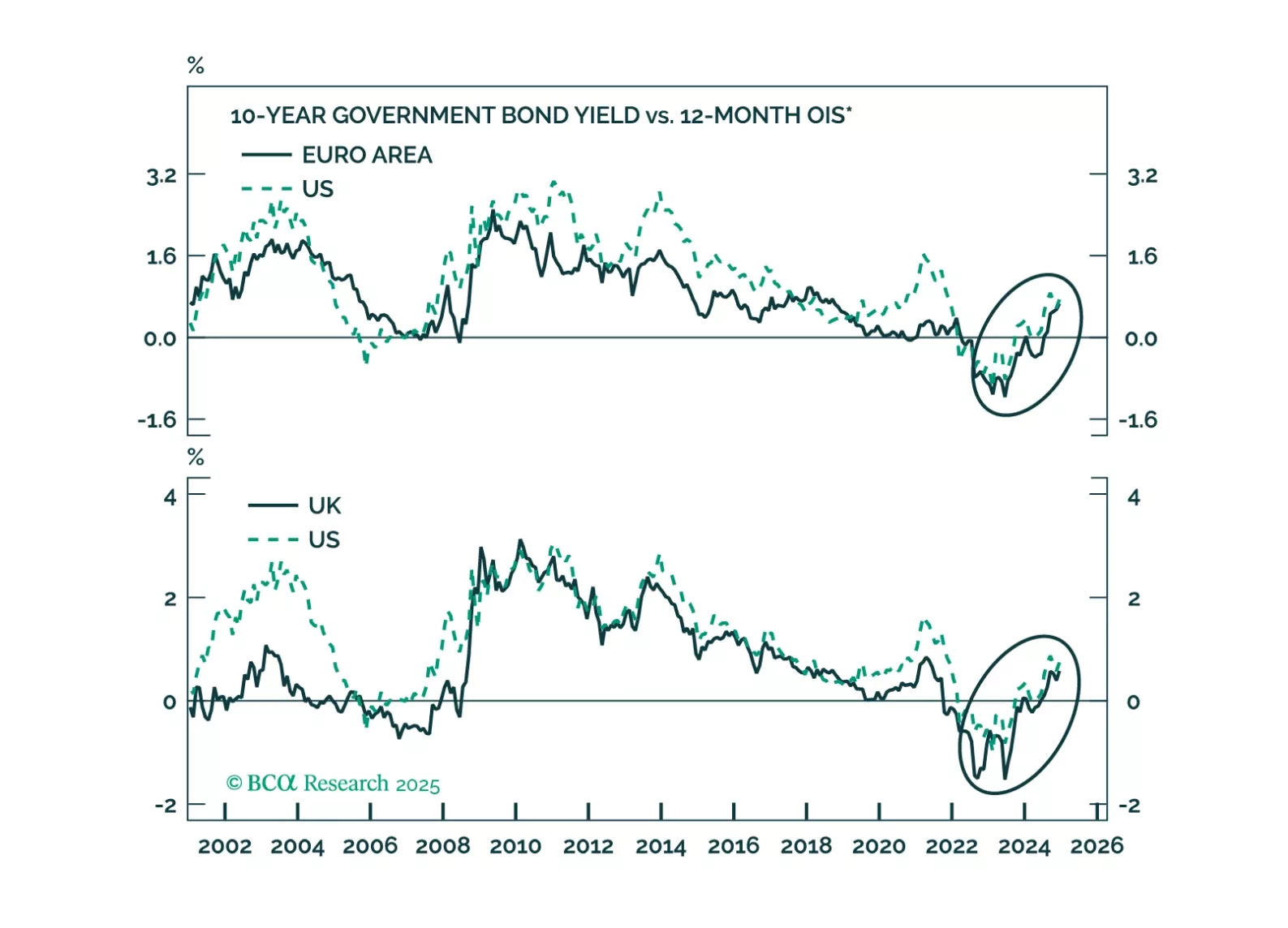

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?

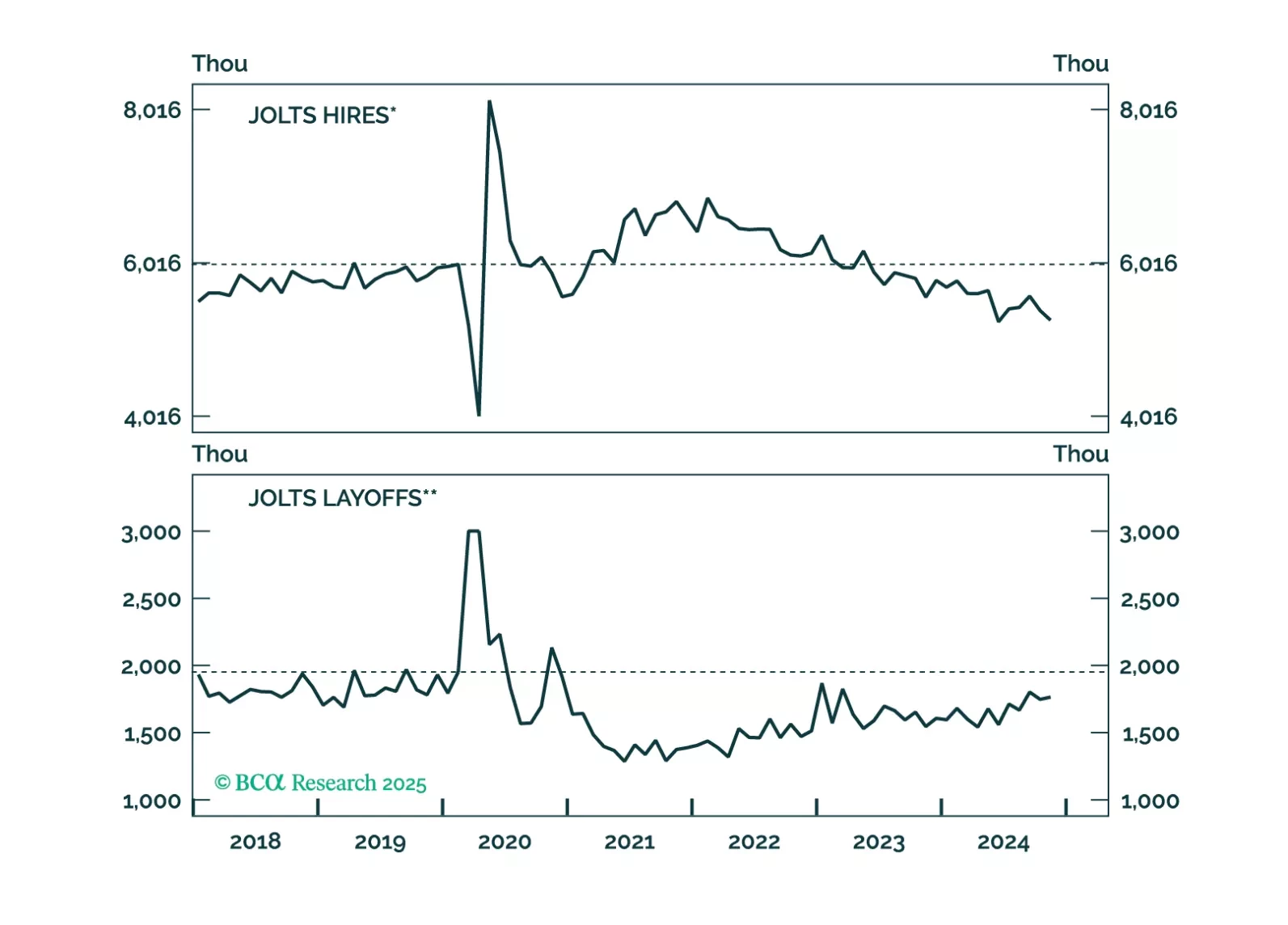

Thoughts on the increase in bond yields and this morning’s employment data.

Our Portfolio Allocation Summary for January 2025.

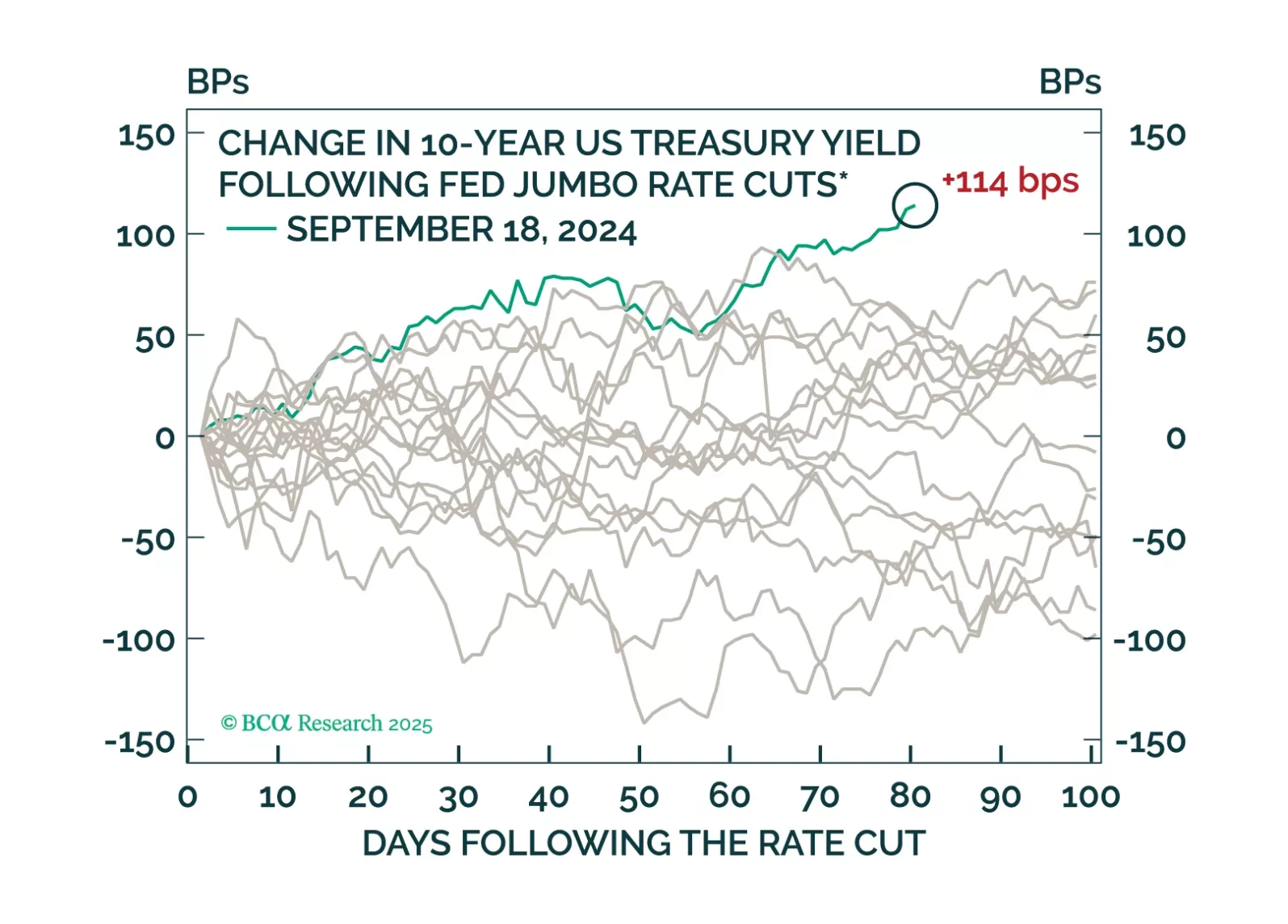

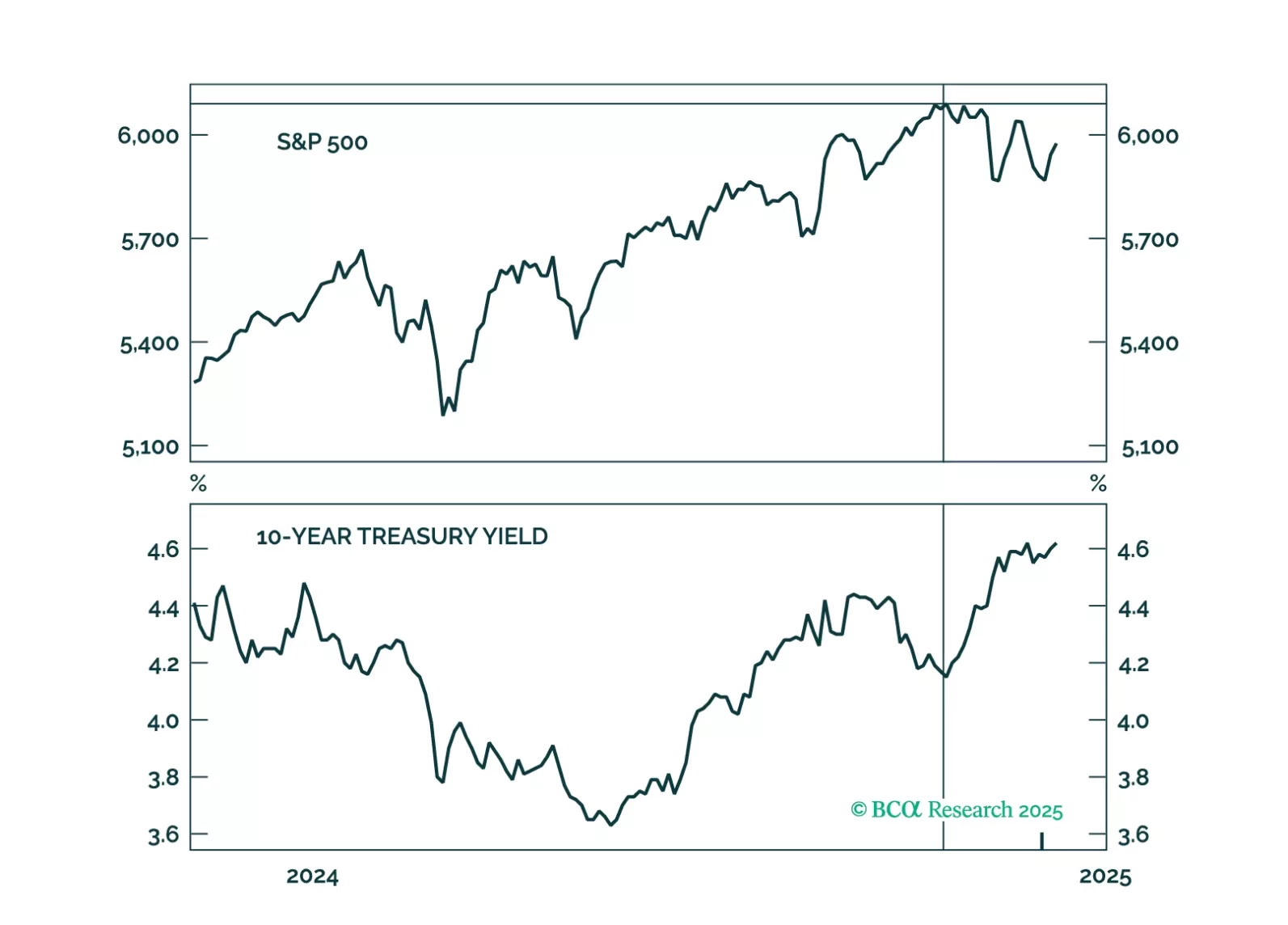

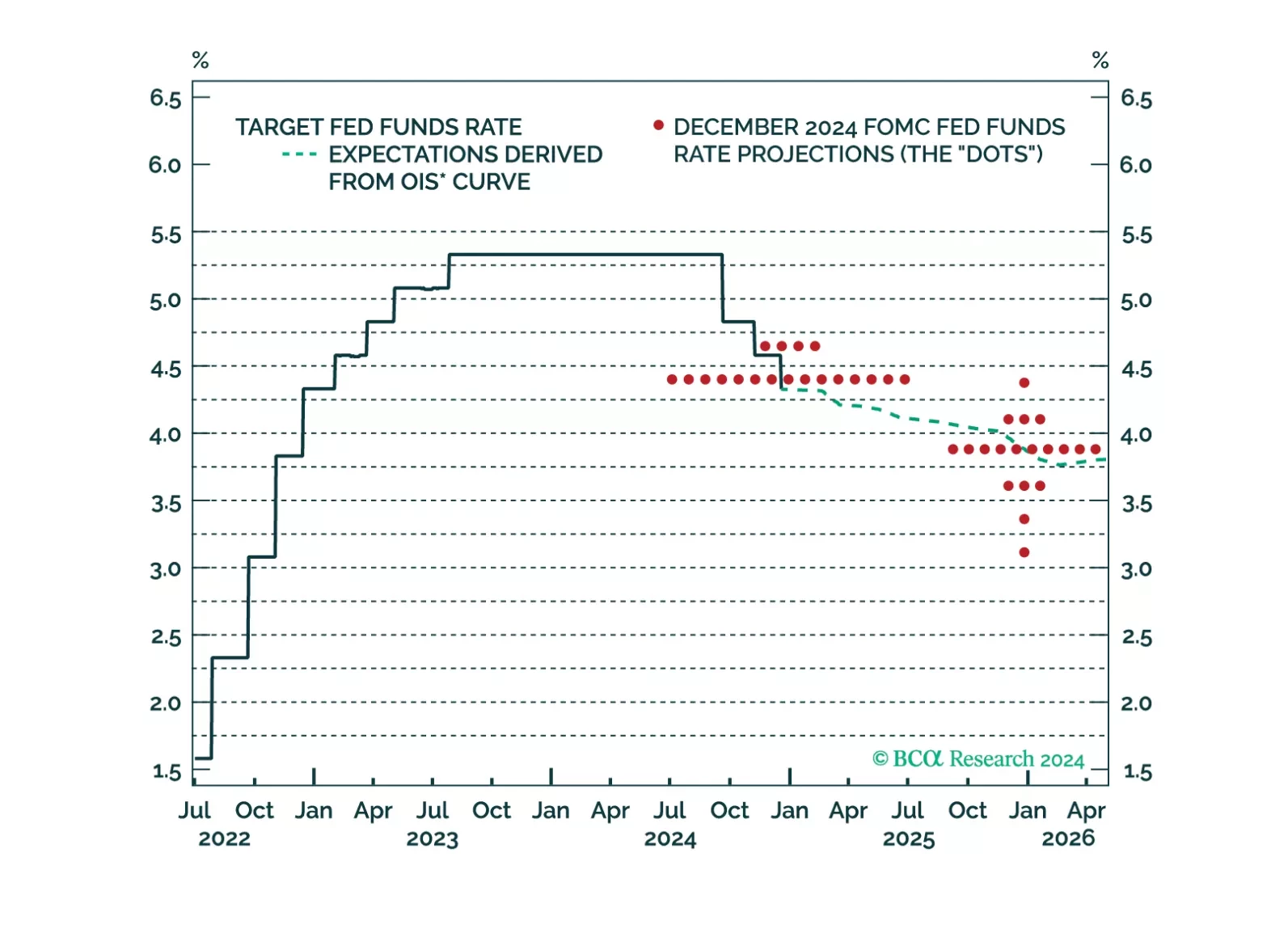

Our thoughts on this afternoon’s Fed decision and the bond market reaction.