Gov Sovereigns/Treasurys

Our Portfolio Allocation Summary for September 2024.

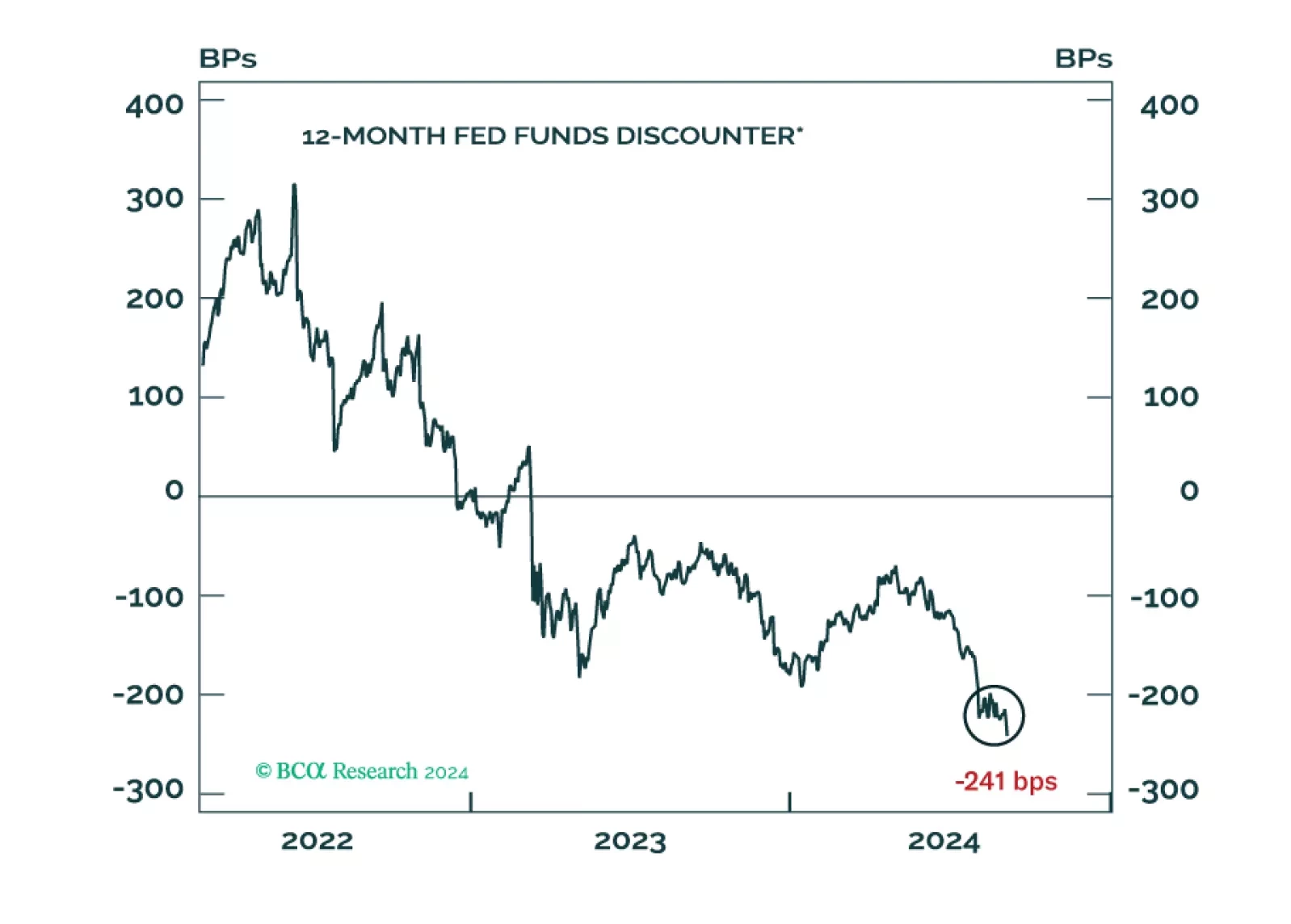

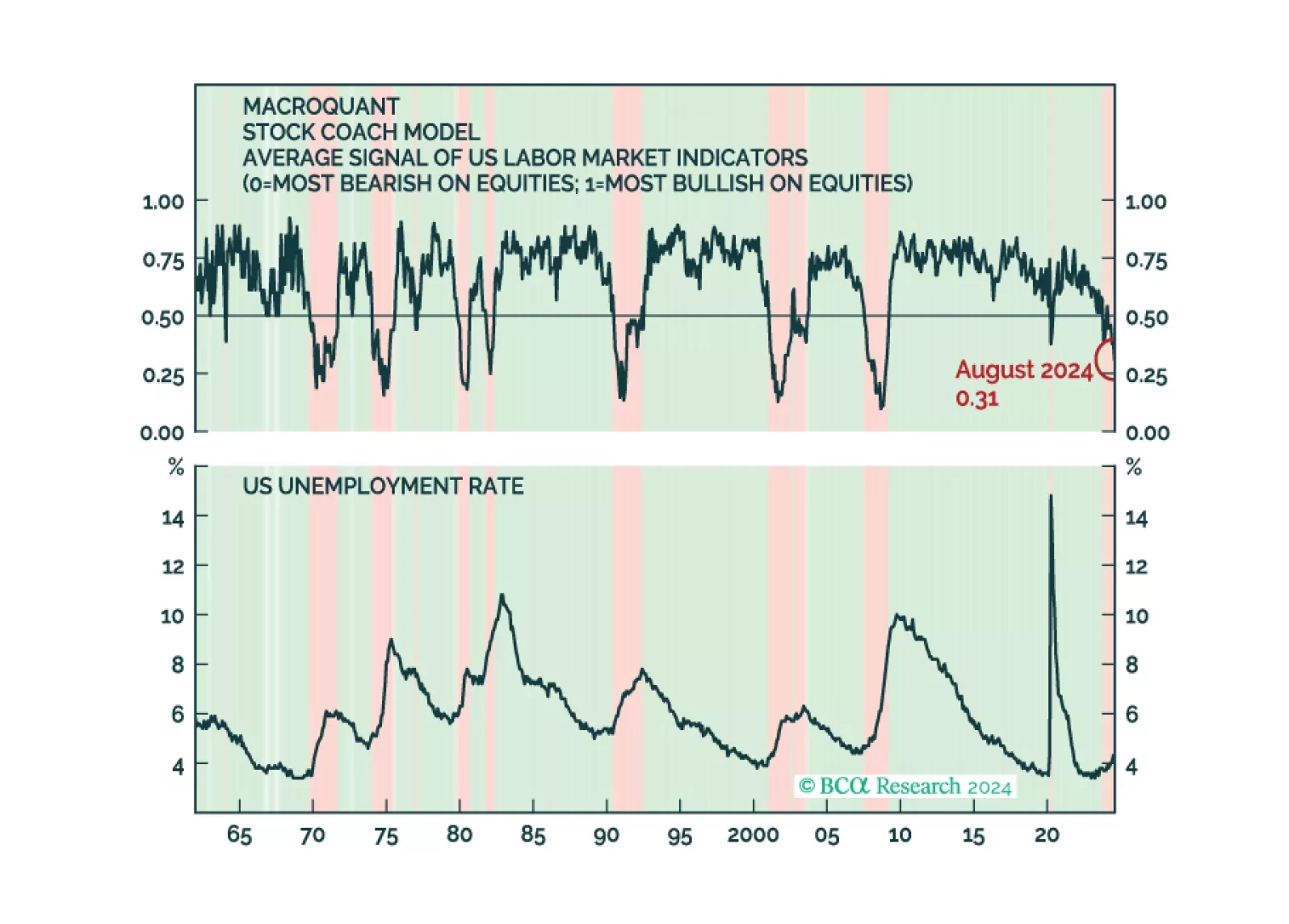

MacroQuant continues to recommend underweighting equities and overweighting bonds. This is consistent with the Global Investment Strategy Team's decision to downgrade global equities to underweight in late June.

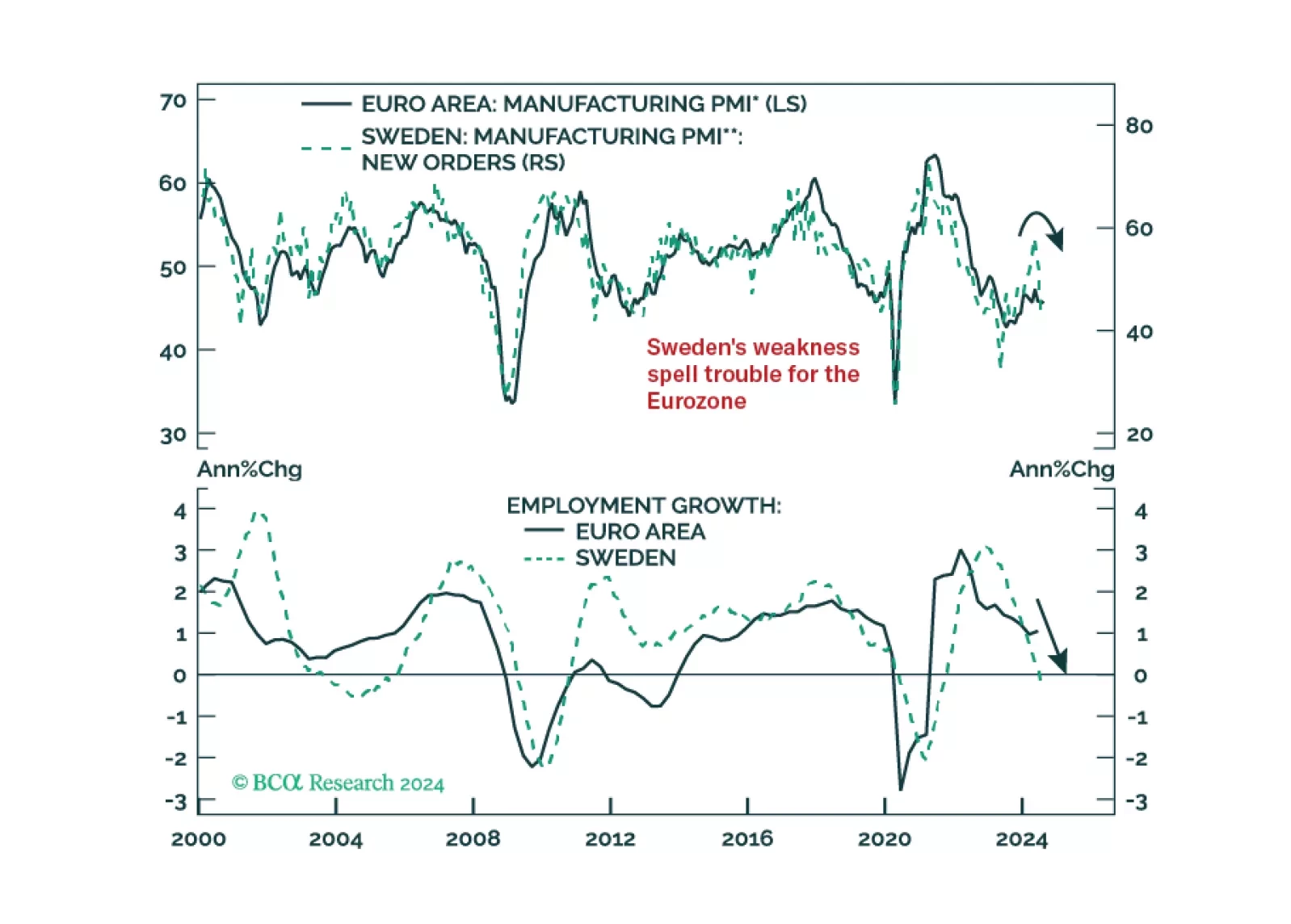

Our negative stance on European growth and assets is not devoid of risks. To gauge whether these risks warrant upgrading our growth outlook, we monitor Sweden closely. So, what is the current message from this Nordic economy?

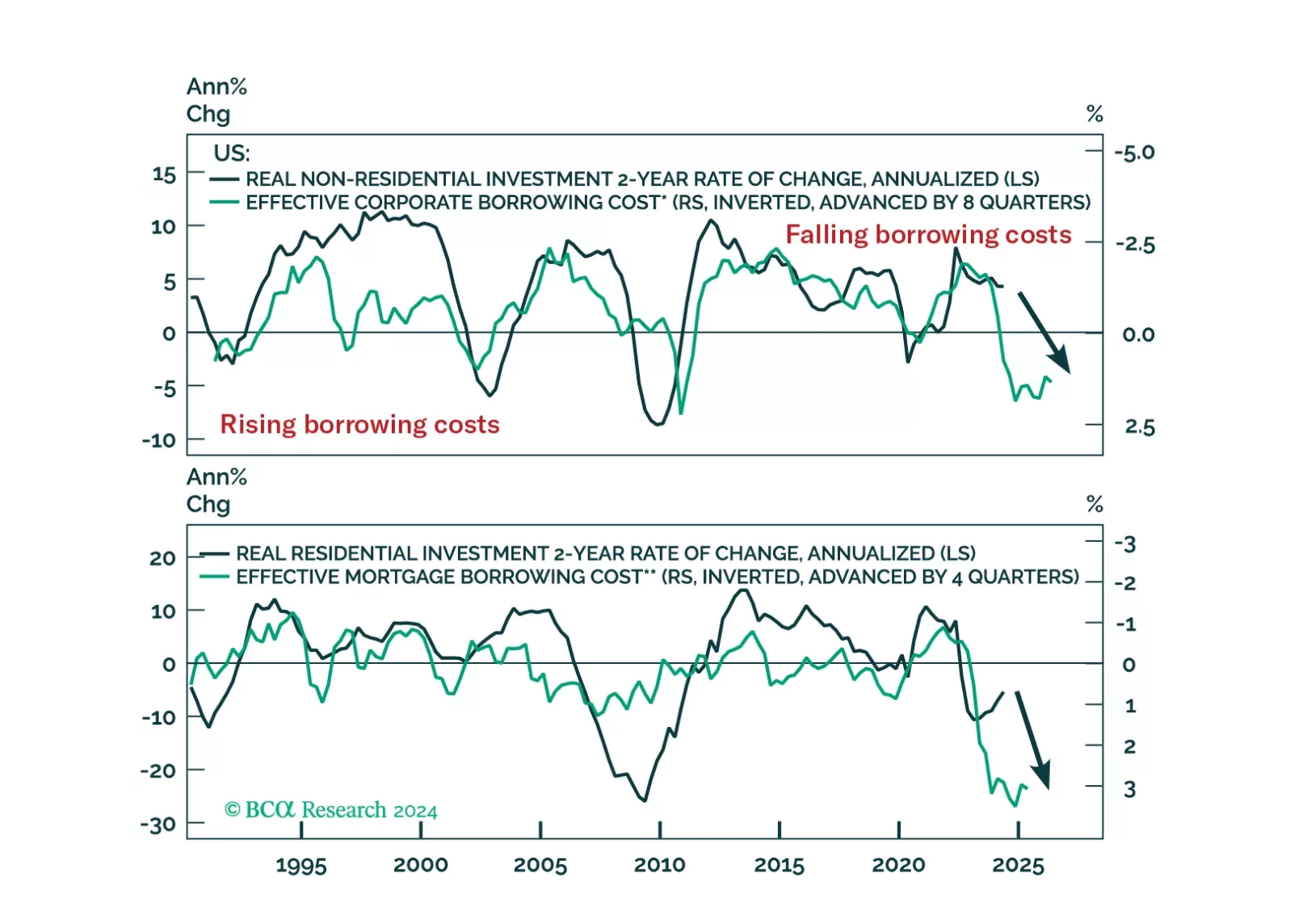

In this Special Report, we assess the impact of monetary policy tightening on major economies. Interest rate sensitive GDP already slowed significantly in response to the aggressive rate hiking cycle. Despite the beginning of policy easing, our forward-looking indicators suggest monetary policy will continue to weigh on the economy.

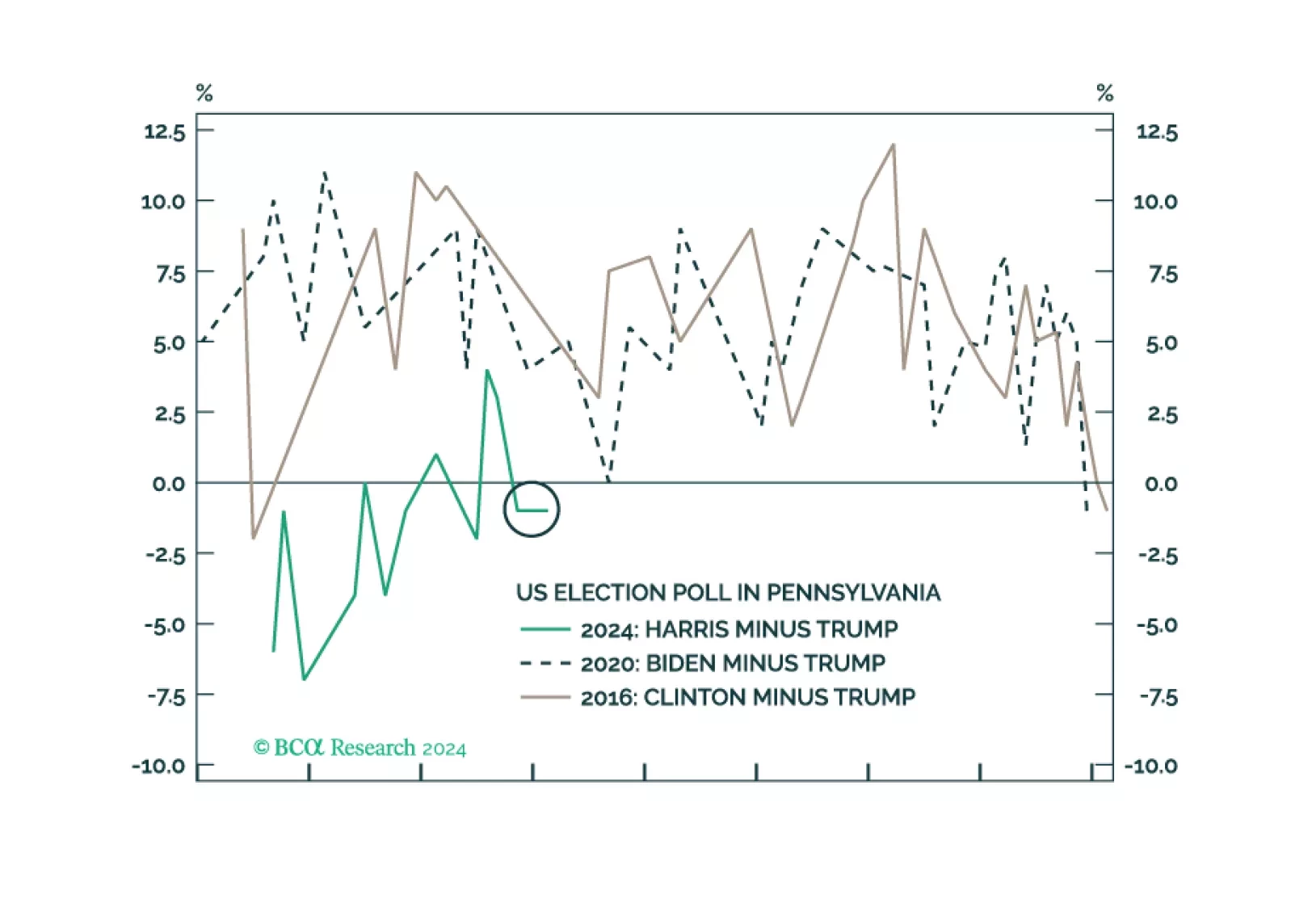

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

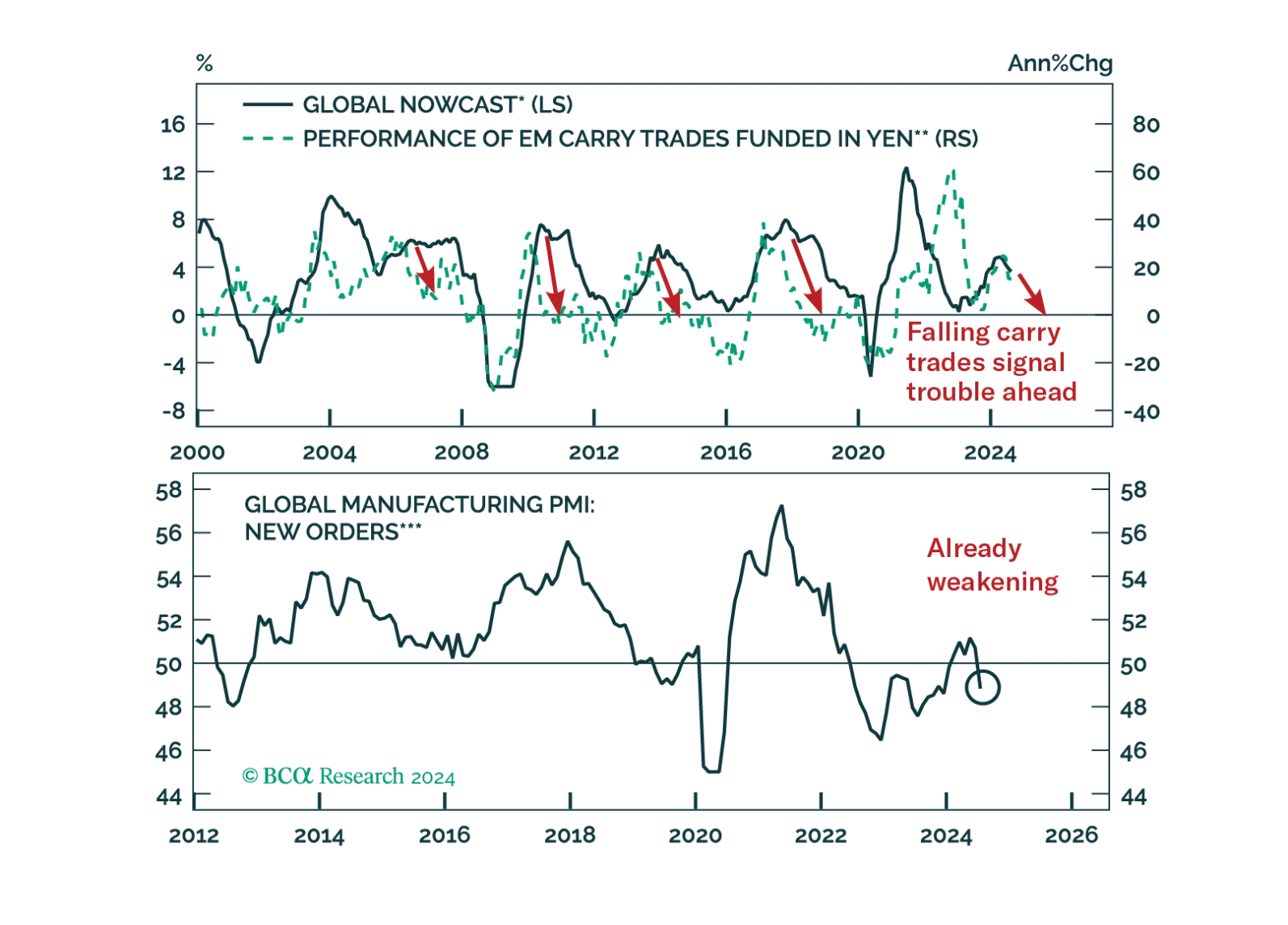

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

Our Portfolio Allocation Summary for August 2024.

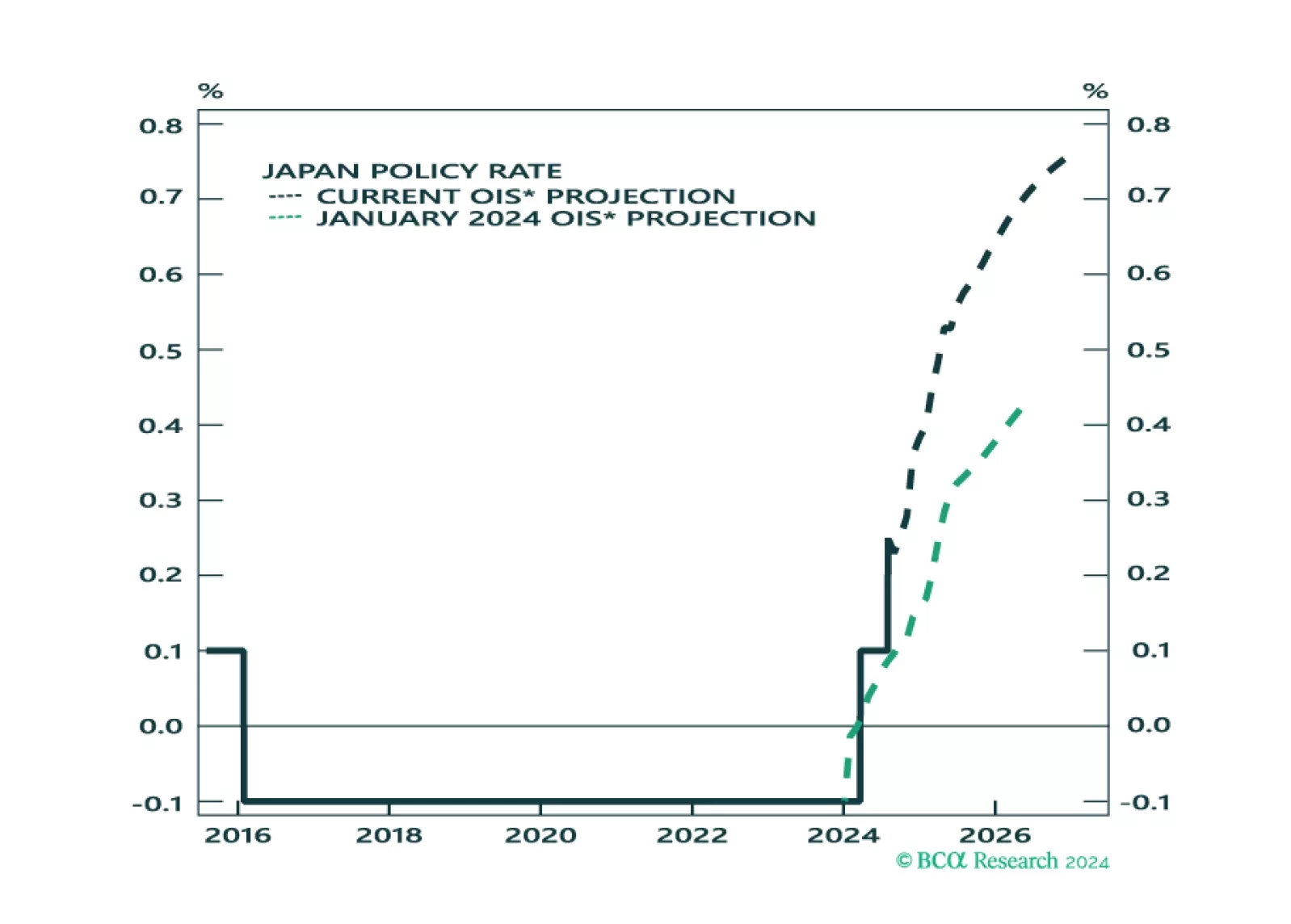

We assess the investment implications of the BoJ and Fed meetings, and give our take on the next policy moves. We also assess the impact on asset markets.