Gov Sovereigns/Treasurys

In this insight, we calibrate our investment views based on the latest Bank of Canada decision.

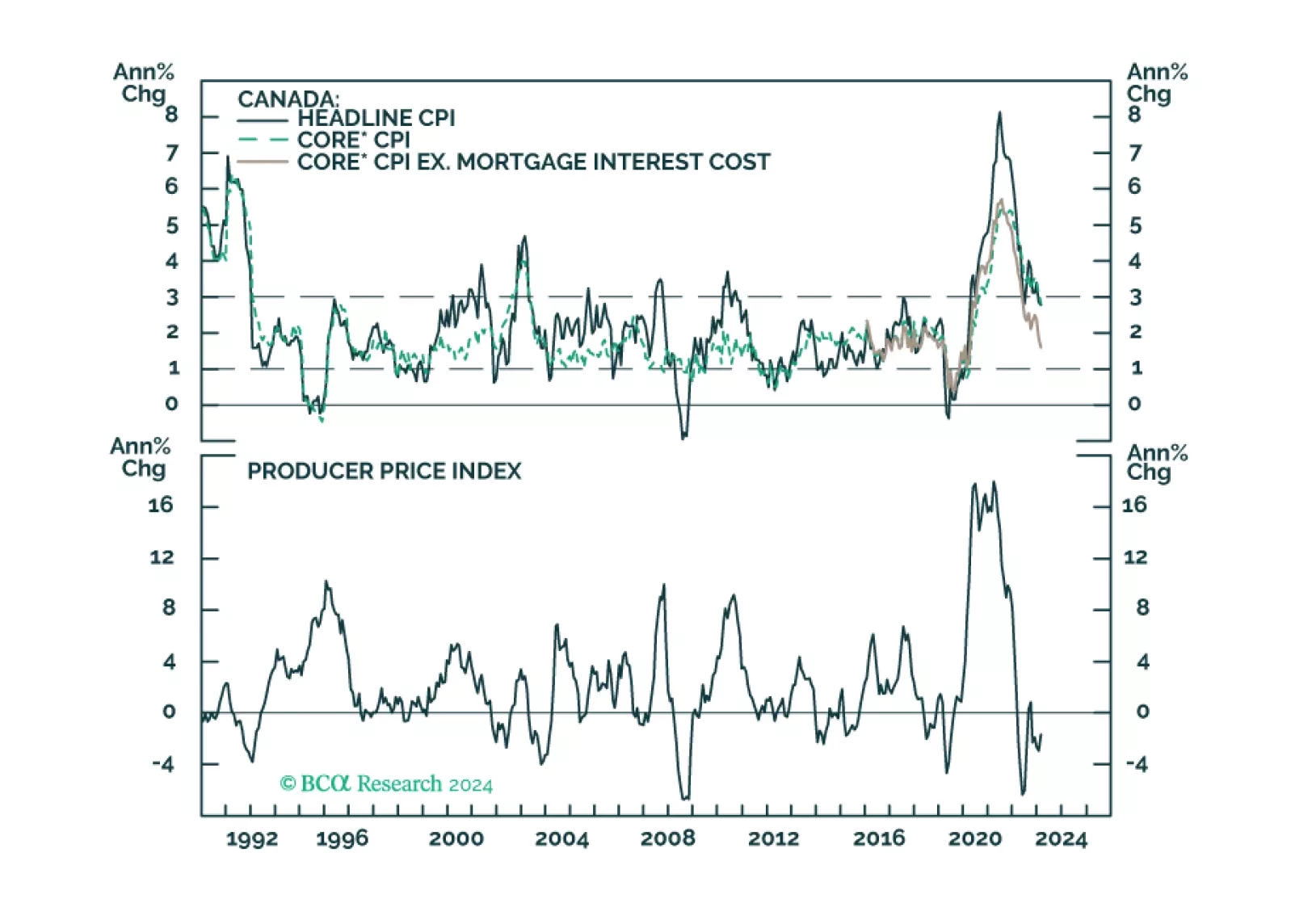

Our reaction to this morning’s CPI report and bond market moves.

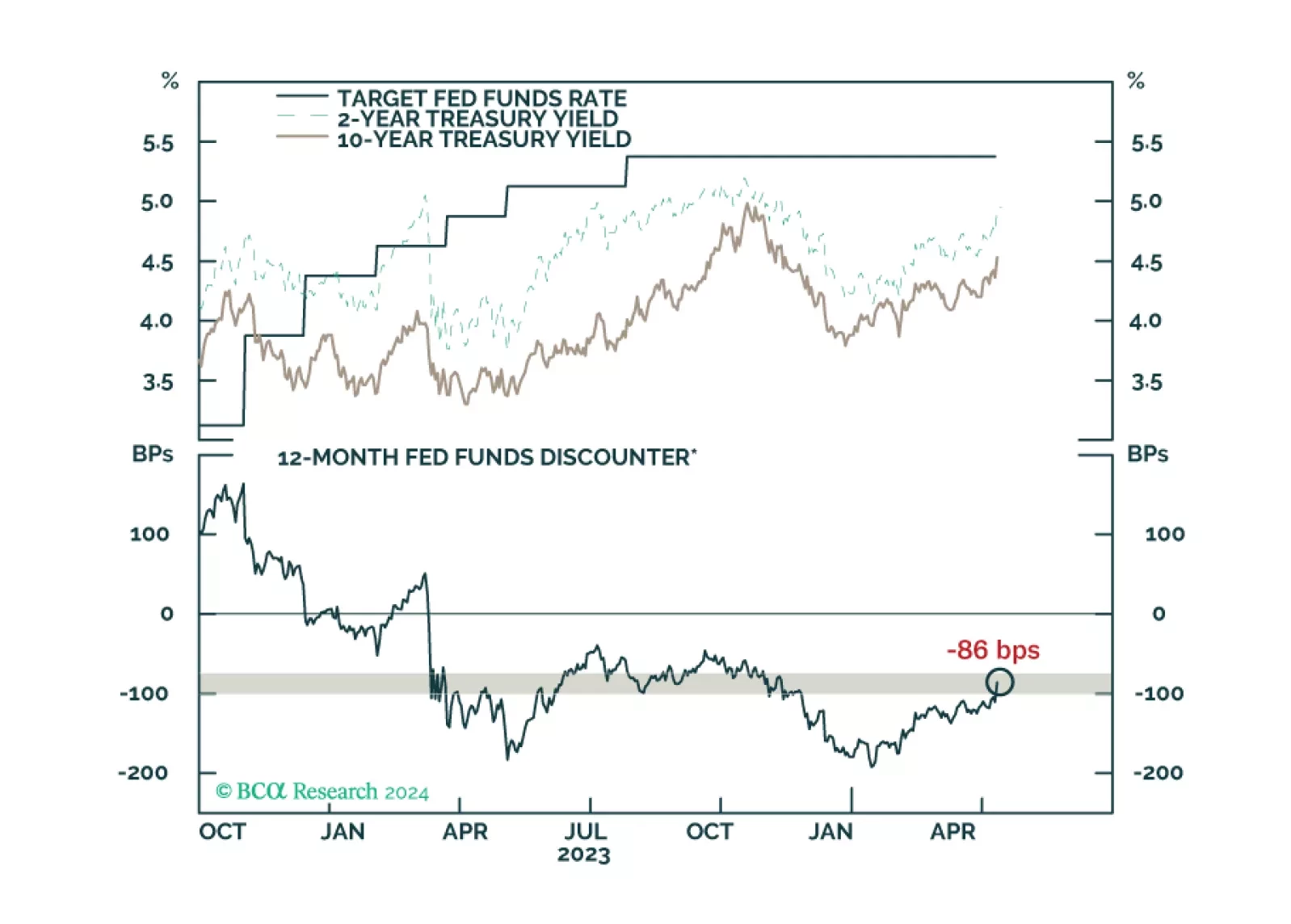

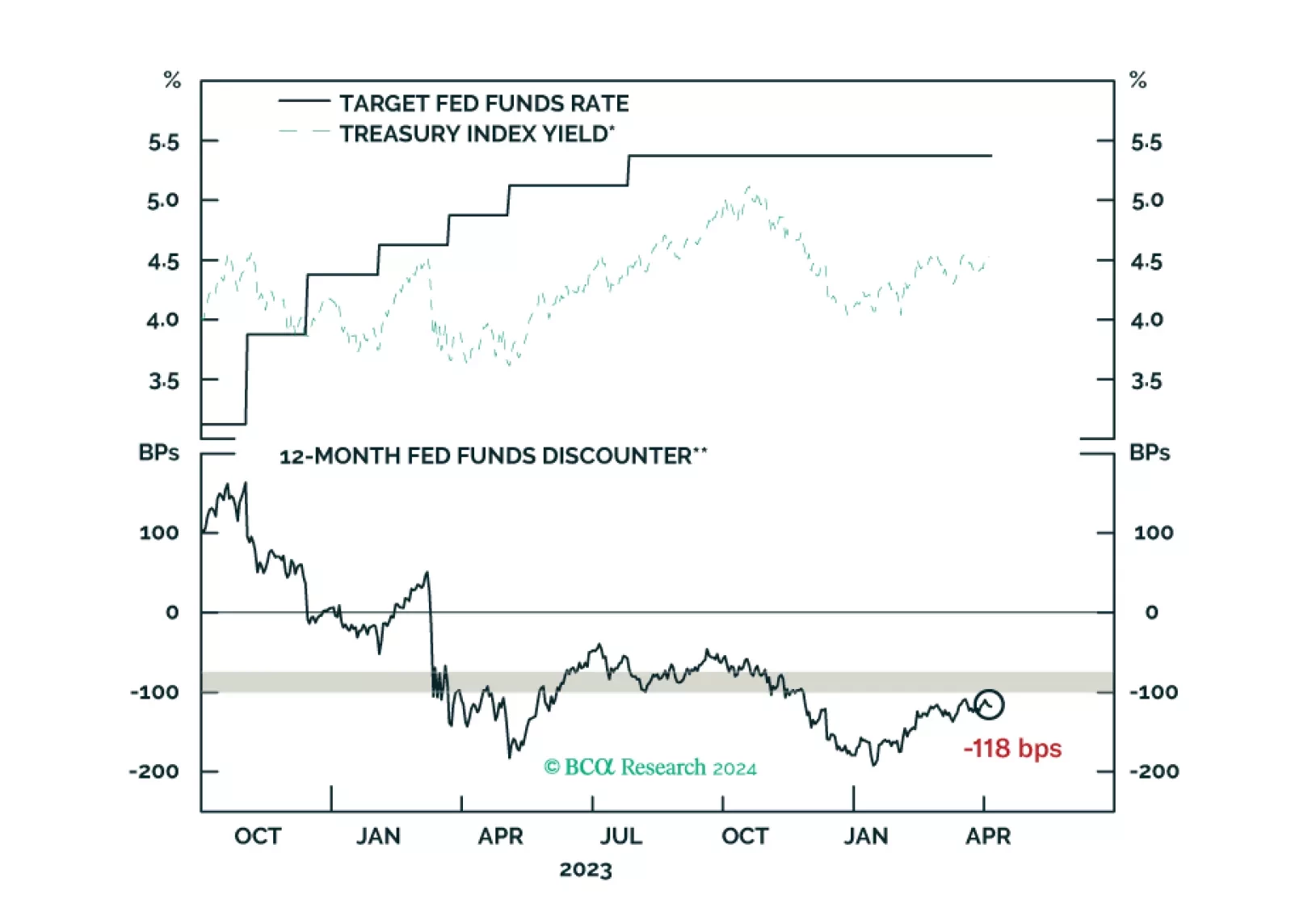

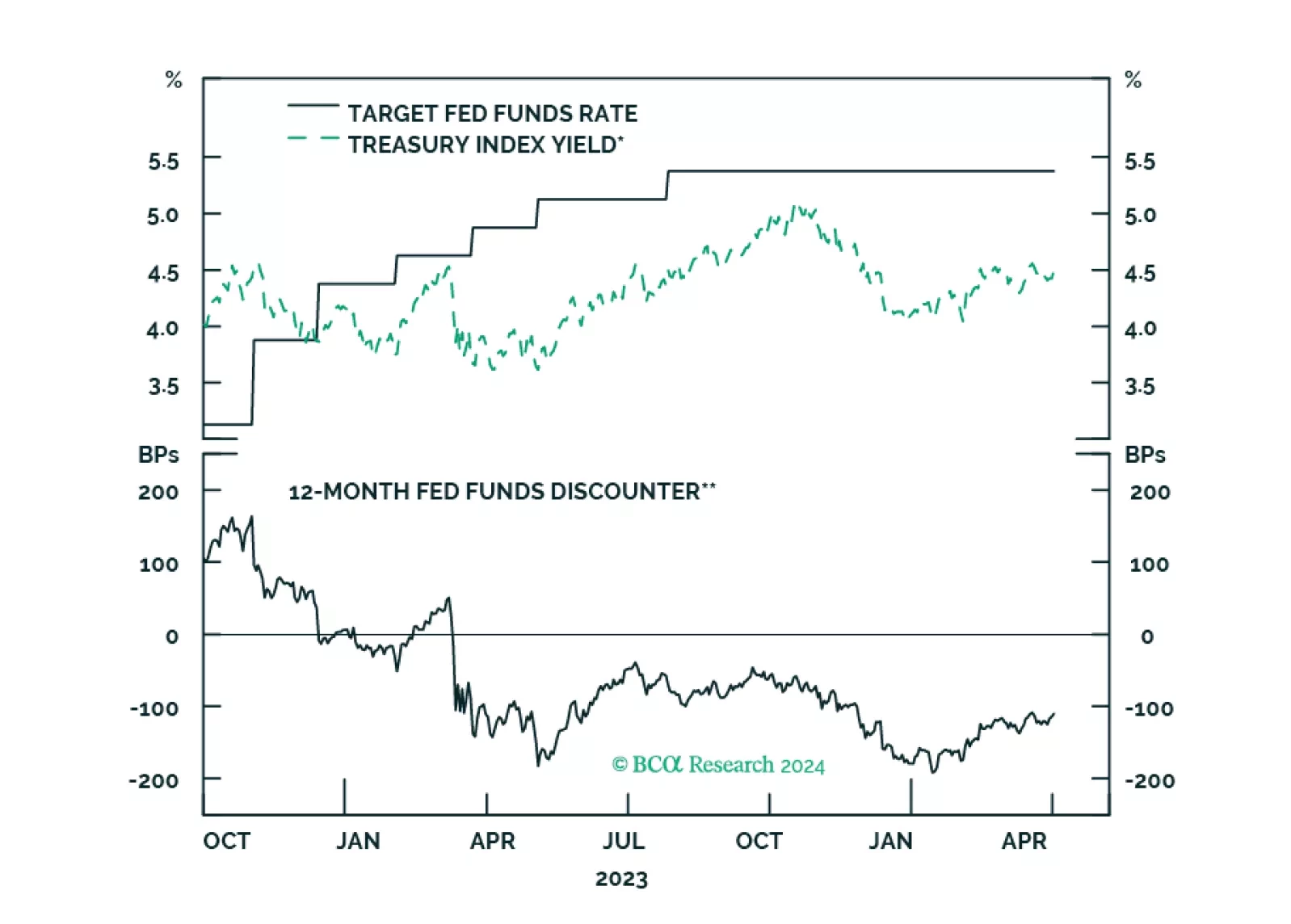

Our reaction to this morning’s employment report and bond market moves.

Our Portfolio Allocation Summary for April 2024.

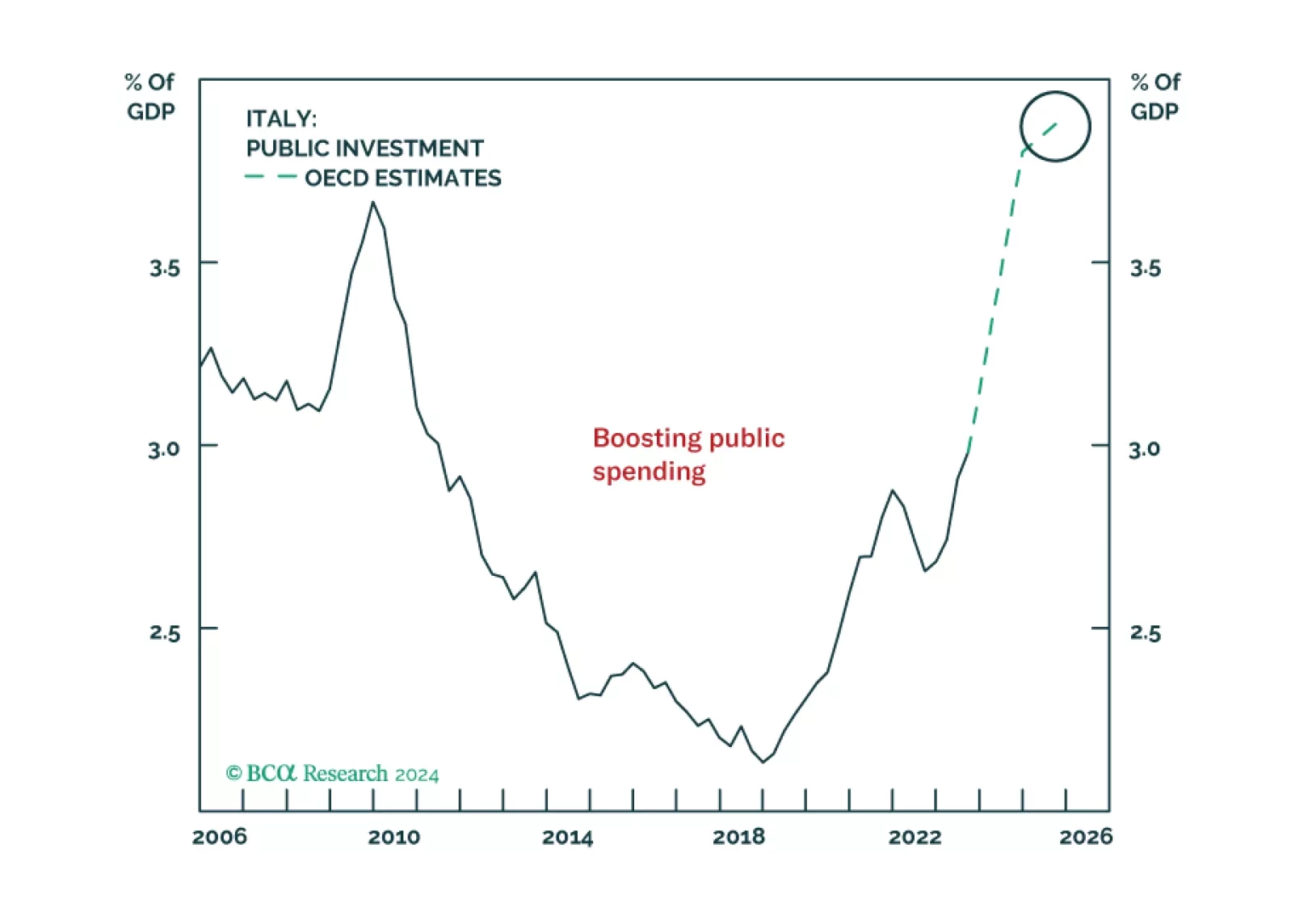

Italy is no longer Europe’s problem child. Investors will be better off reassessing their views of Italian assets, which represent a buying opportunity on a structural time horizon.

We expand our risk/reward analysis of US investment grade corporate bonds to focus on the 44 industry groups included in the Bloomberg index.

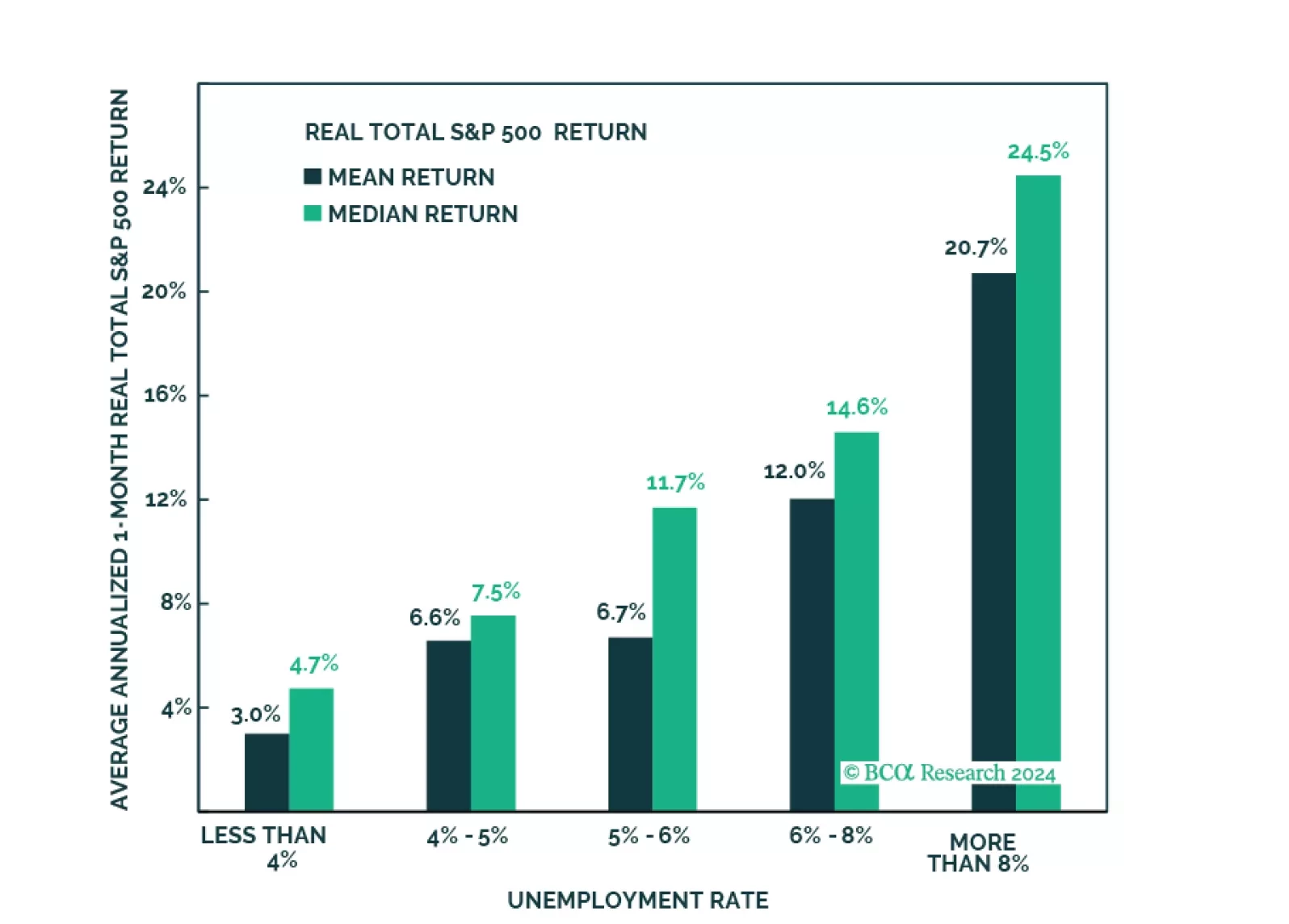

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

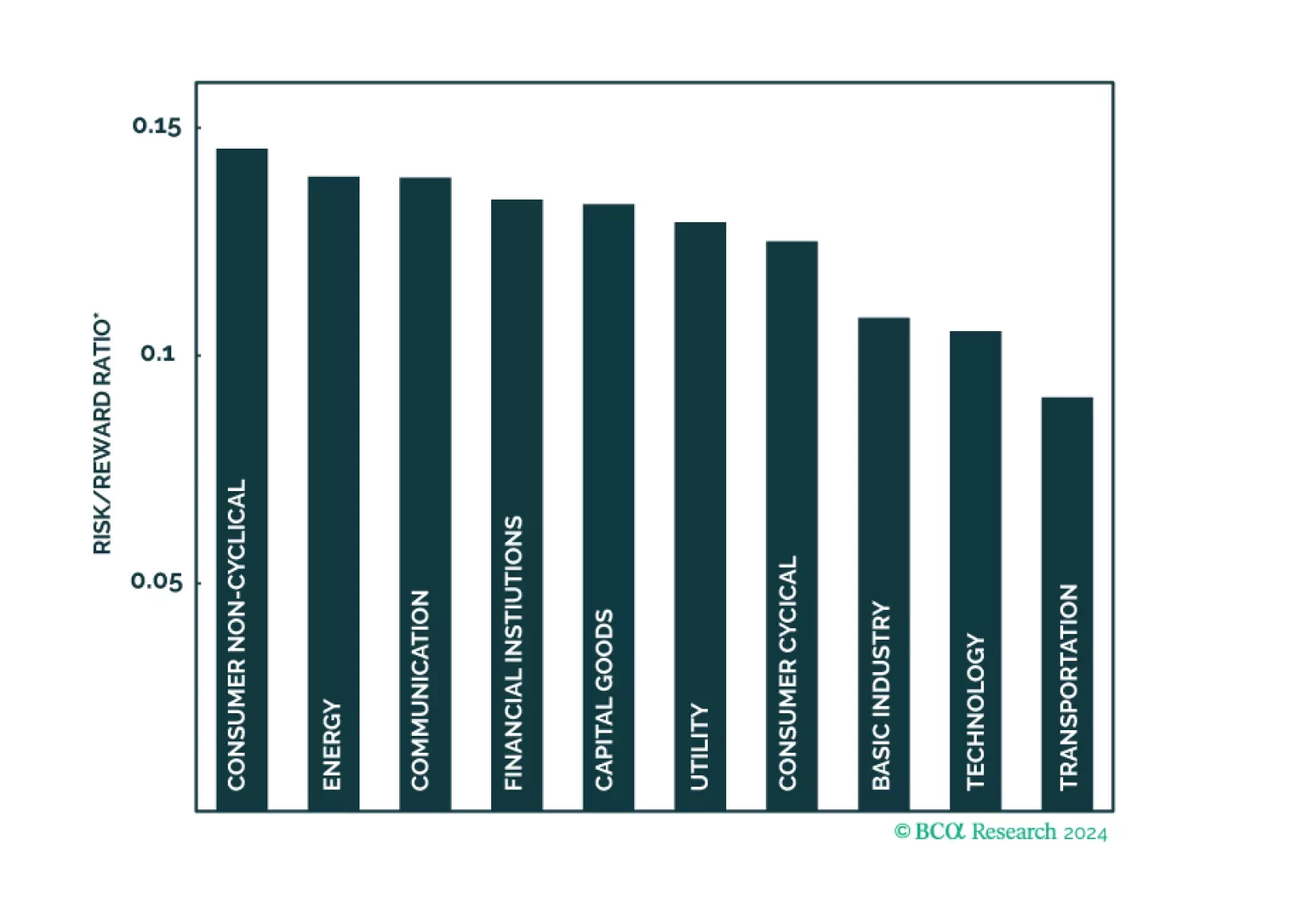

A risk/reward ranking of the 10 major US investment grade corporate bond sectors.

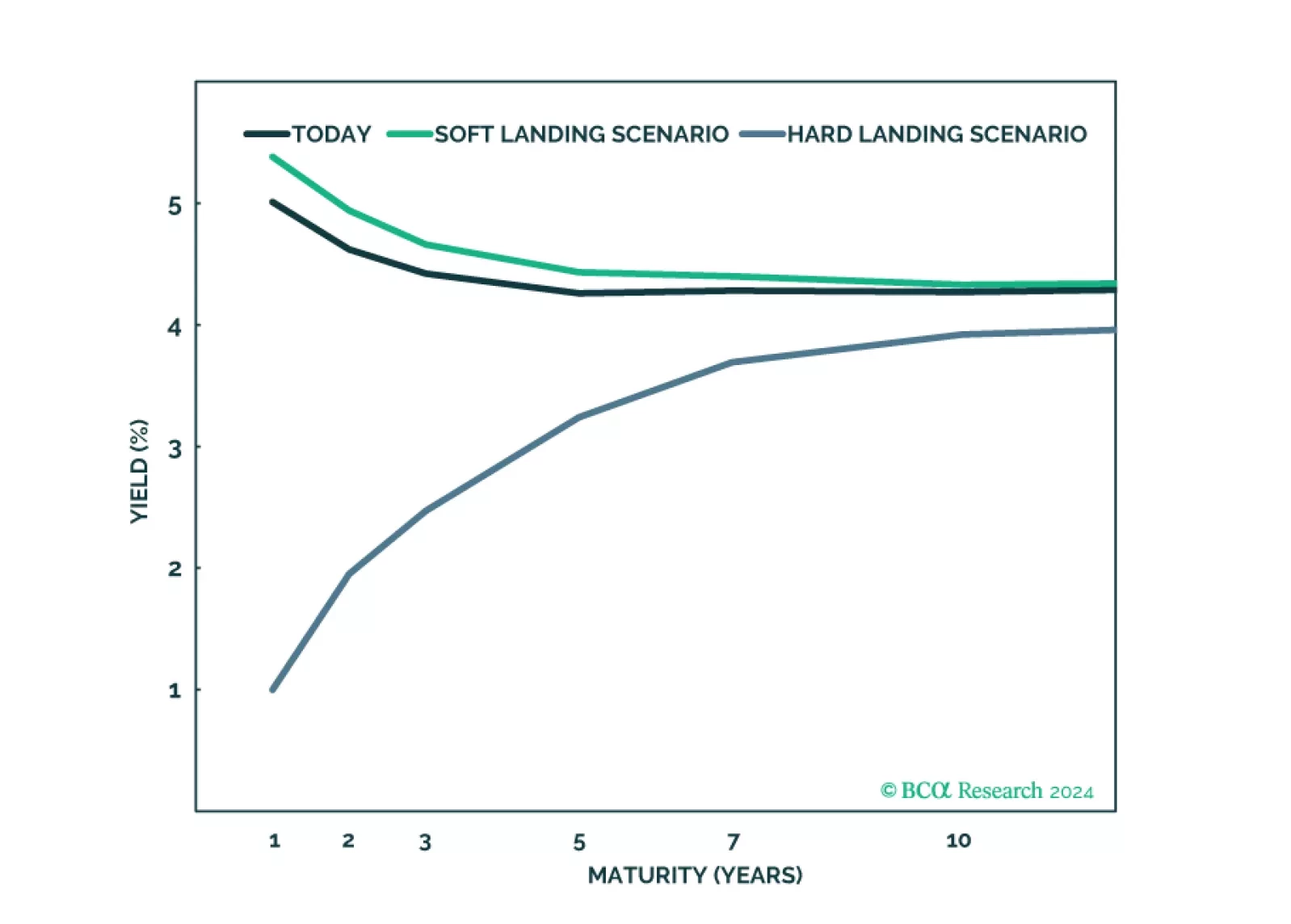

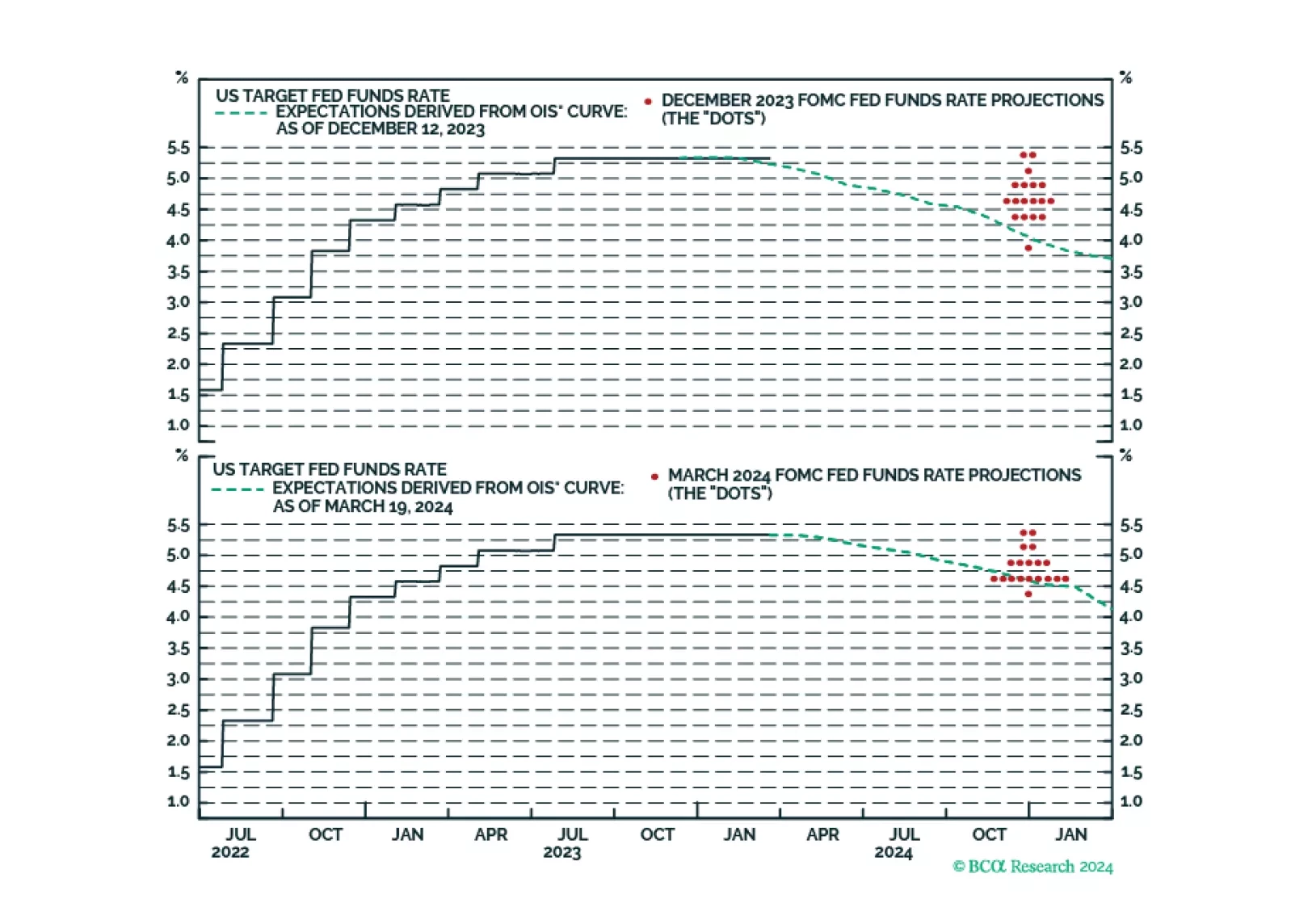

Our takeaways from this afternoon’s FOMC meeting.

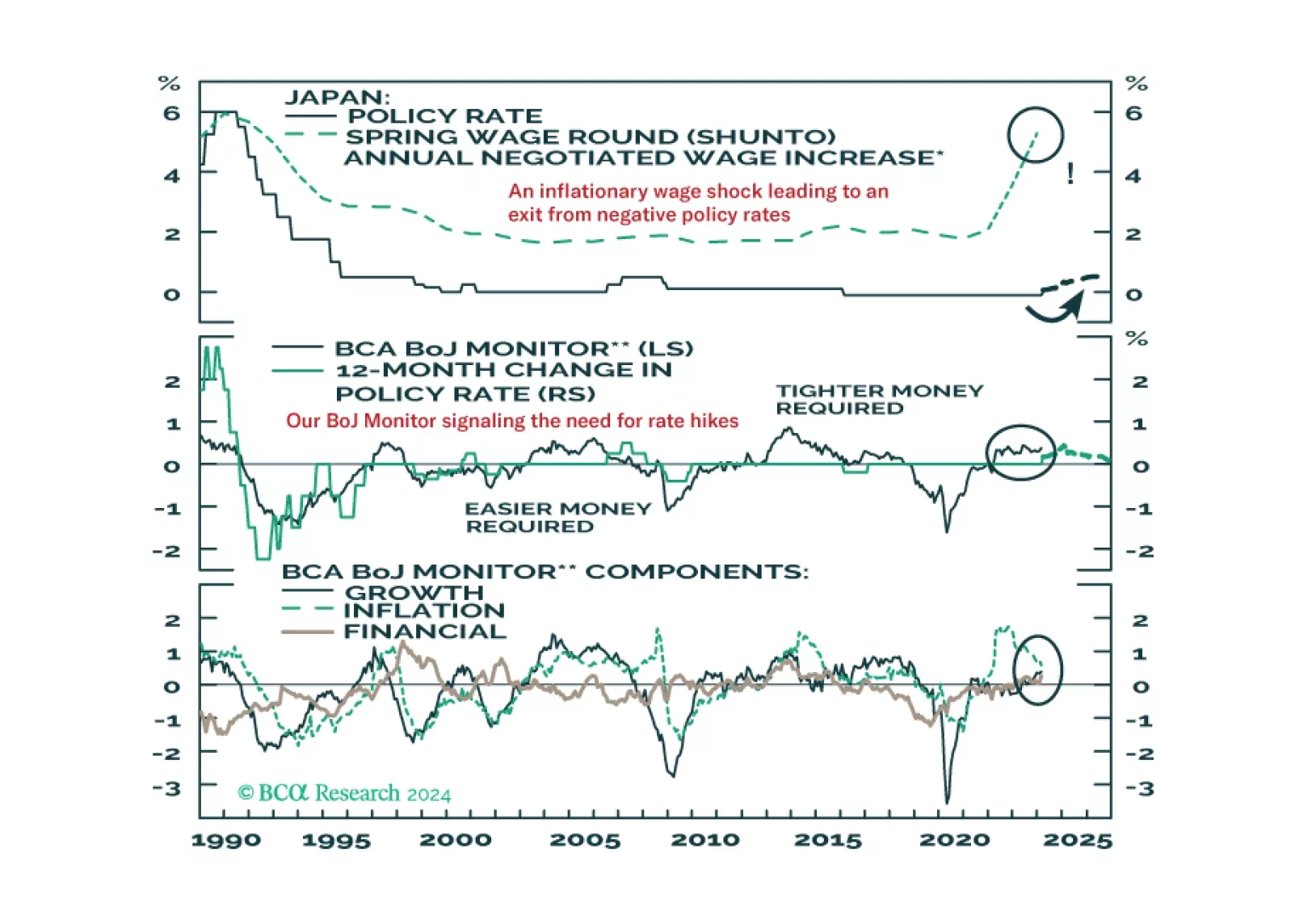

The Bank of Japan delivered a historic policy adjustment this week, ending both negative interest rates and Yield Curve Control. In this Insight, BCA’s global fixed income and currency strategists discuss the immediate implications of the move for Japanese bond yields and the yen, and the potential for additional tightening actions.