Gov Sovereigns/Treasurys

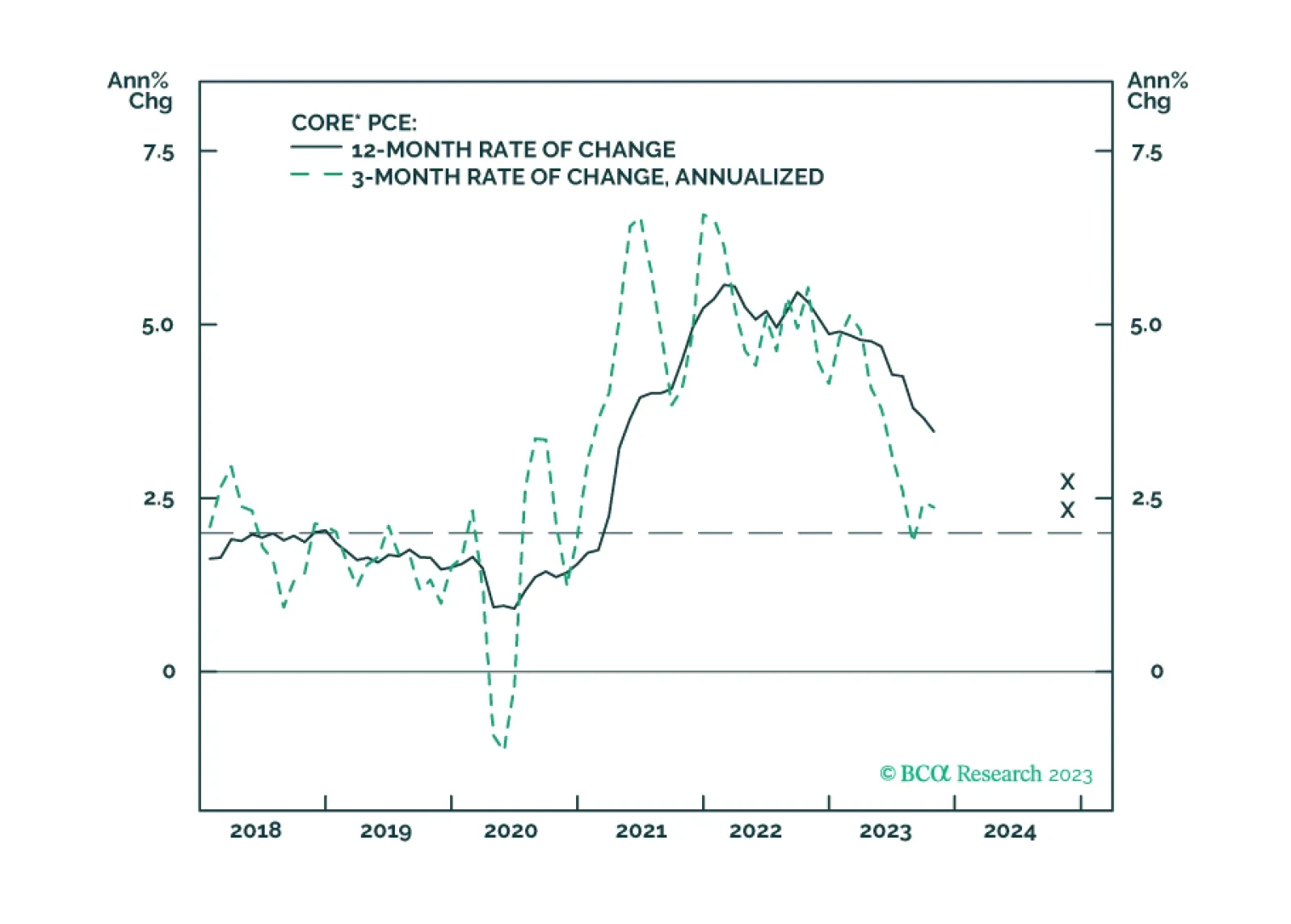

Our US bond team’s thoughts on this afternoon’s FOMC meeting and yesterday’s CPI release.

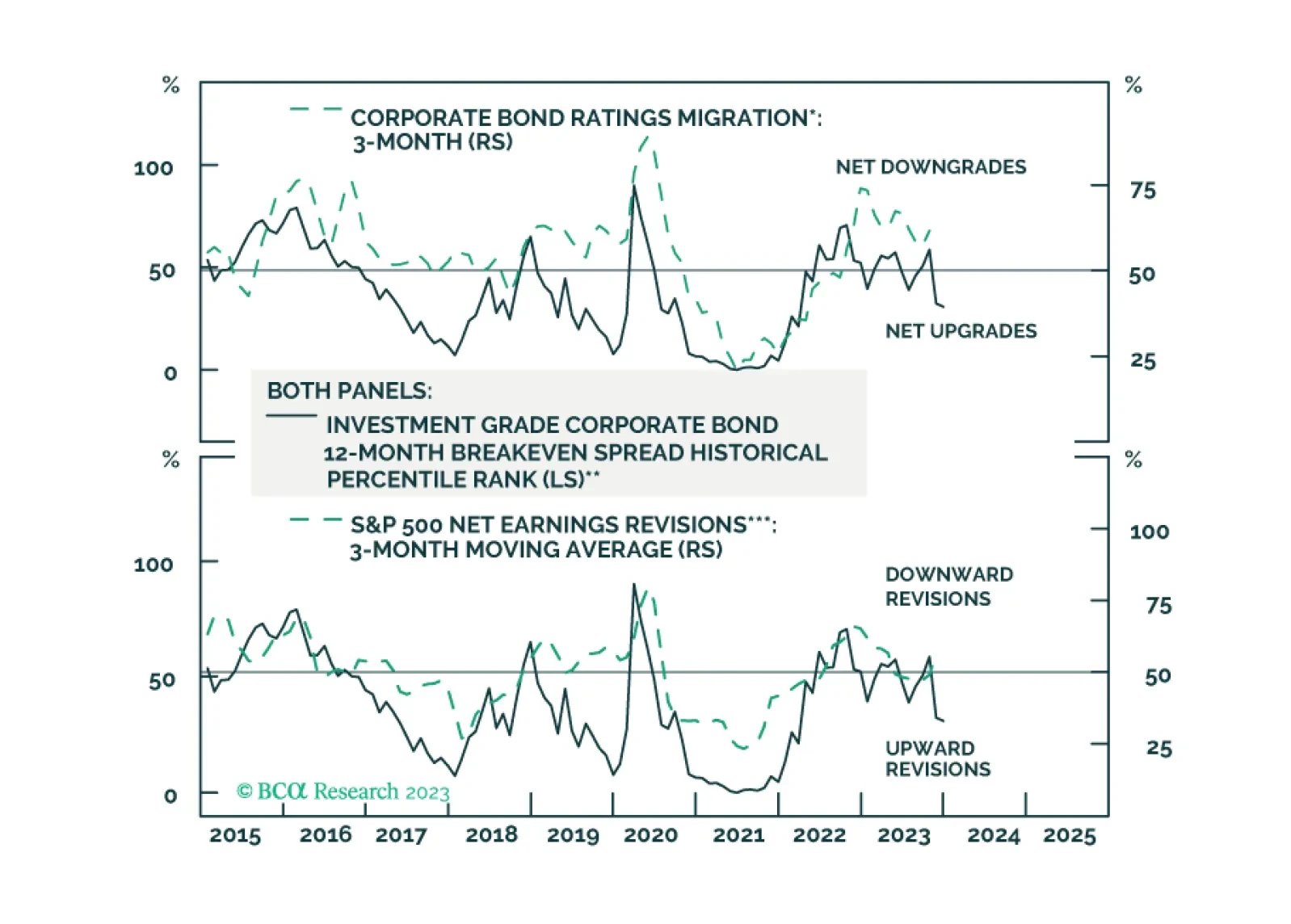

Our US fixed income team’s key investment views for 2024.

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.

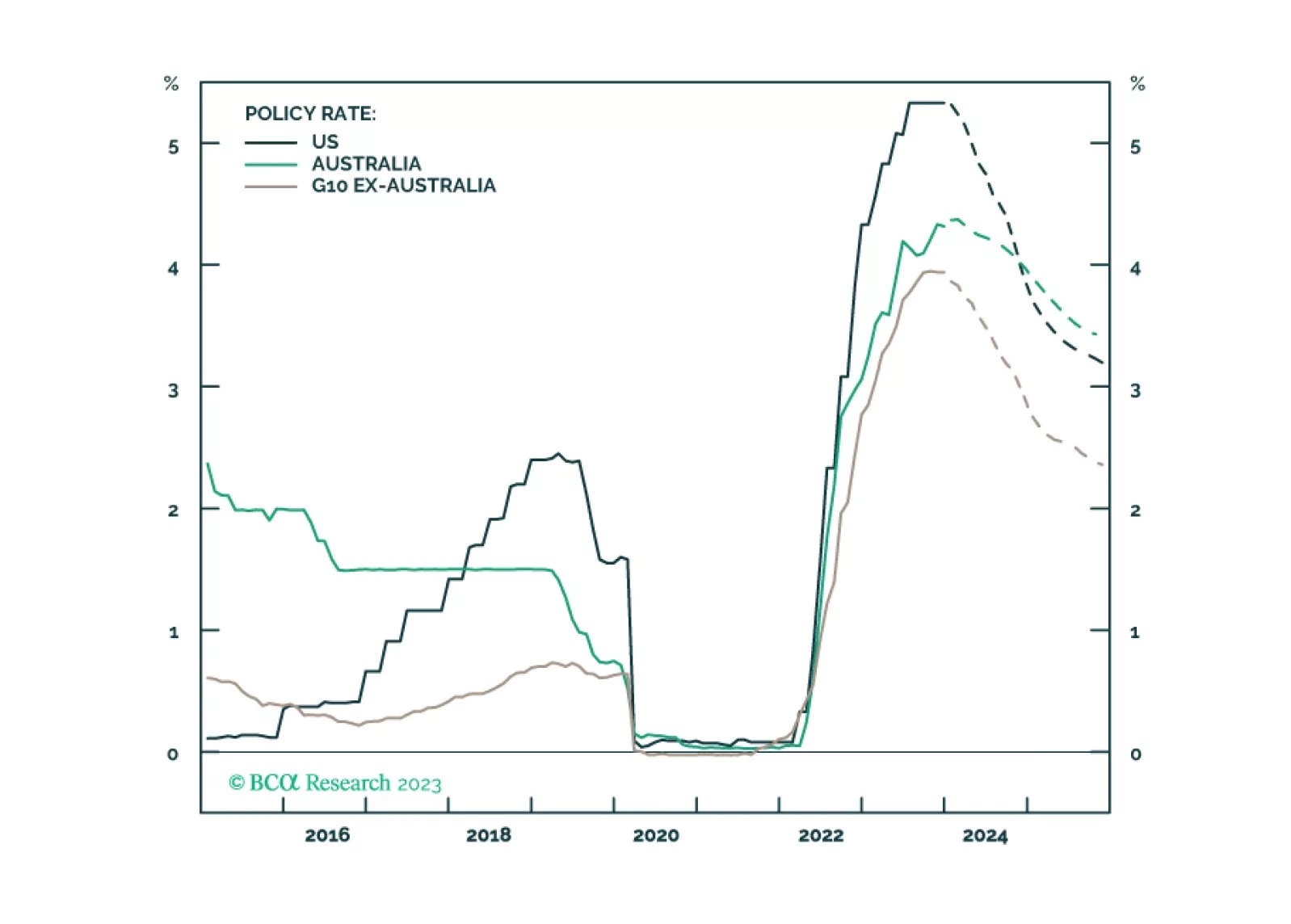

In this Special Report, we take an in-depth look at the outlook for monetary policy in Australia and discuss the impact of an elevated policy rate on the economy. We recommend an underweight country allocation to Australian government bonds and look for opportunities to go long the Australian dollar.

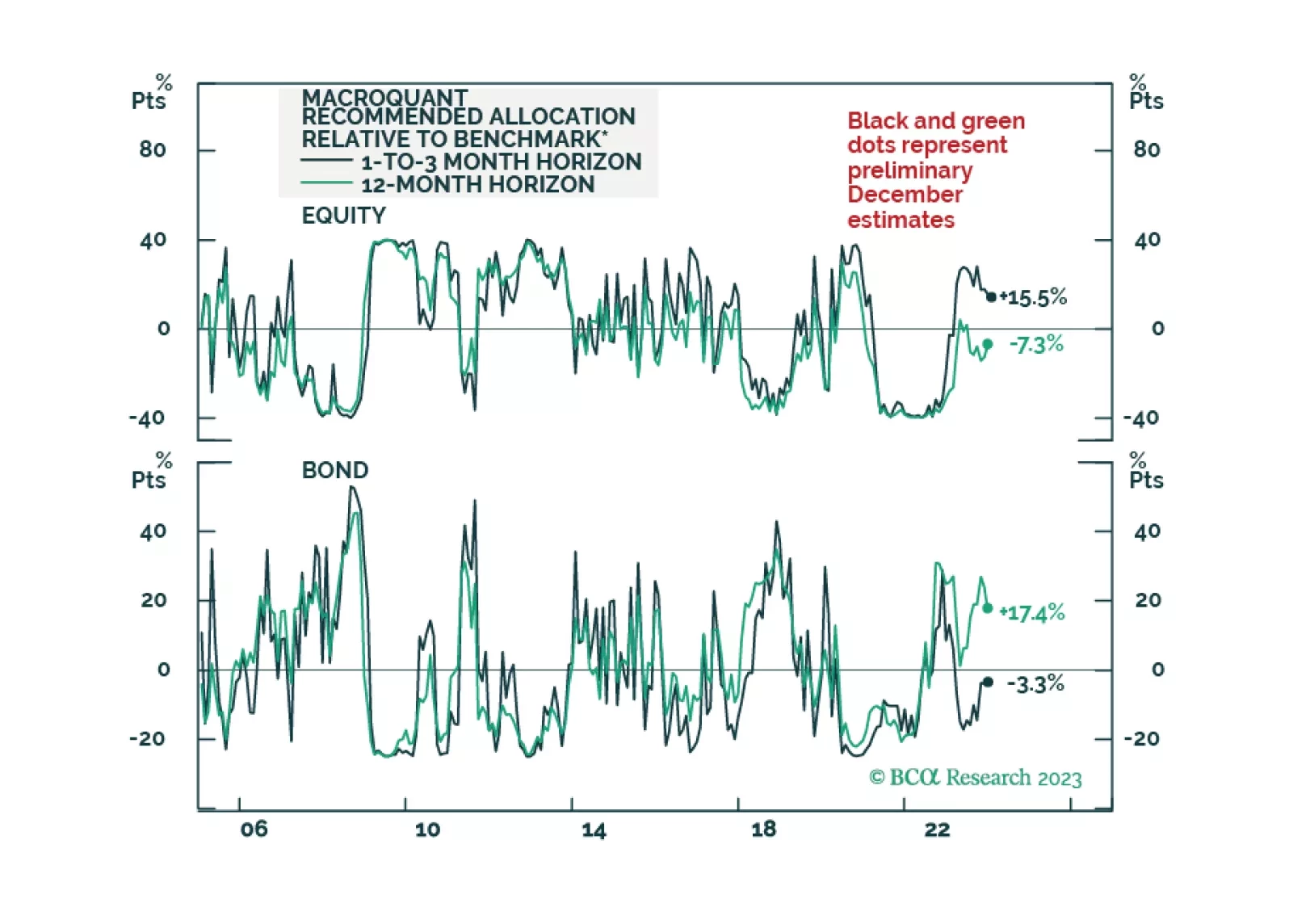

Our Portfolio Allocation Summary for December 2023.

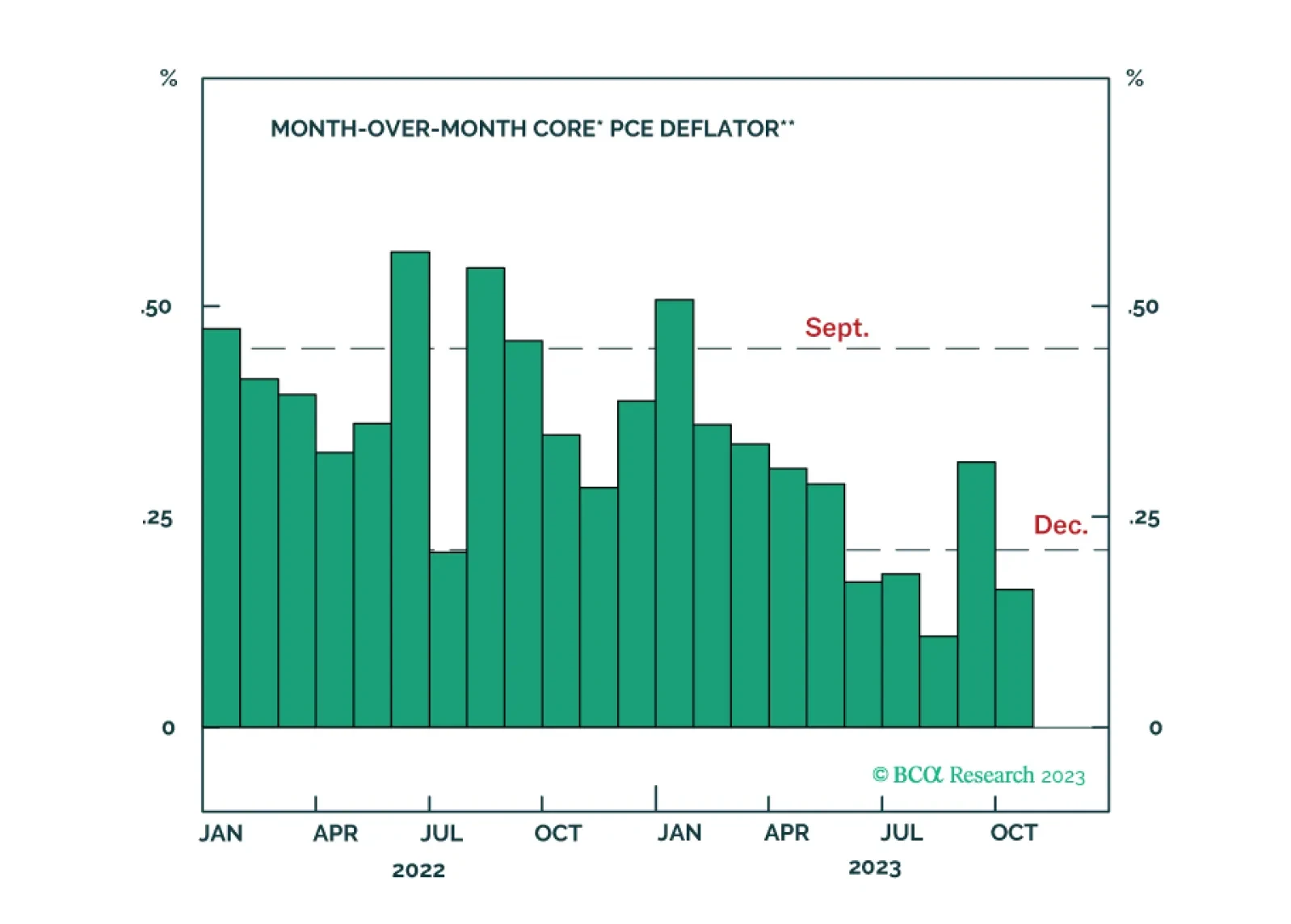

Treasury yields will sketch out a range between now and Q1 2024, with the upside determined by inflation and the downside determined by labor markets.

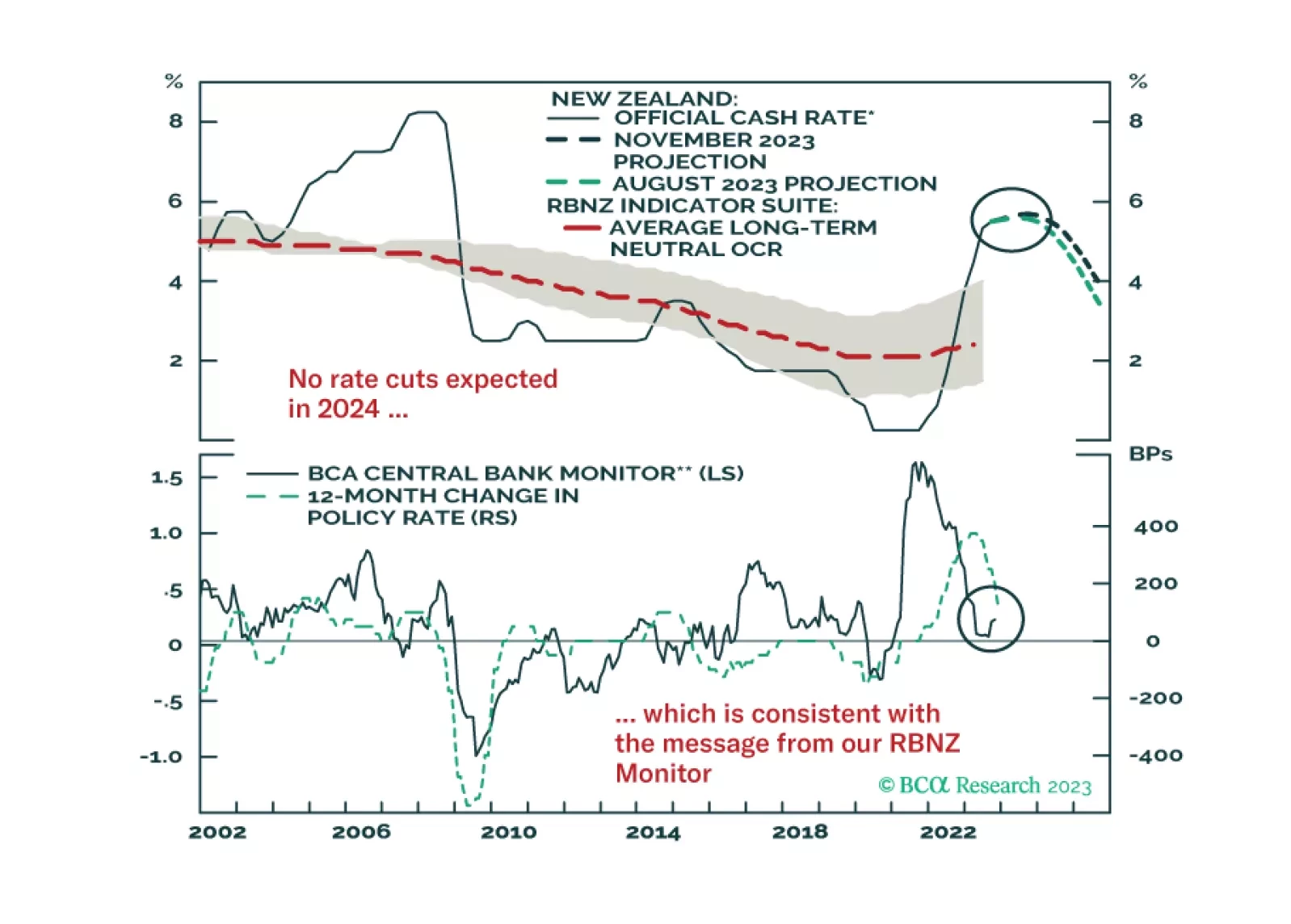

In this Insight, we discuss the outlook for monetary policy in New Zealand after this week’s RBNZ policy meeting, and introduce related fixed income and currency trade ideas.

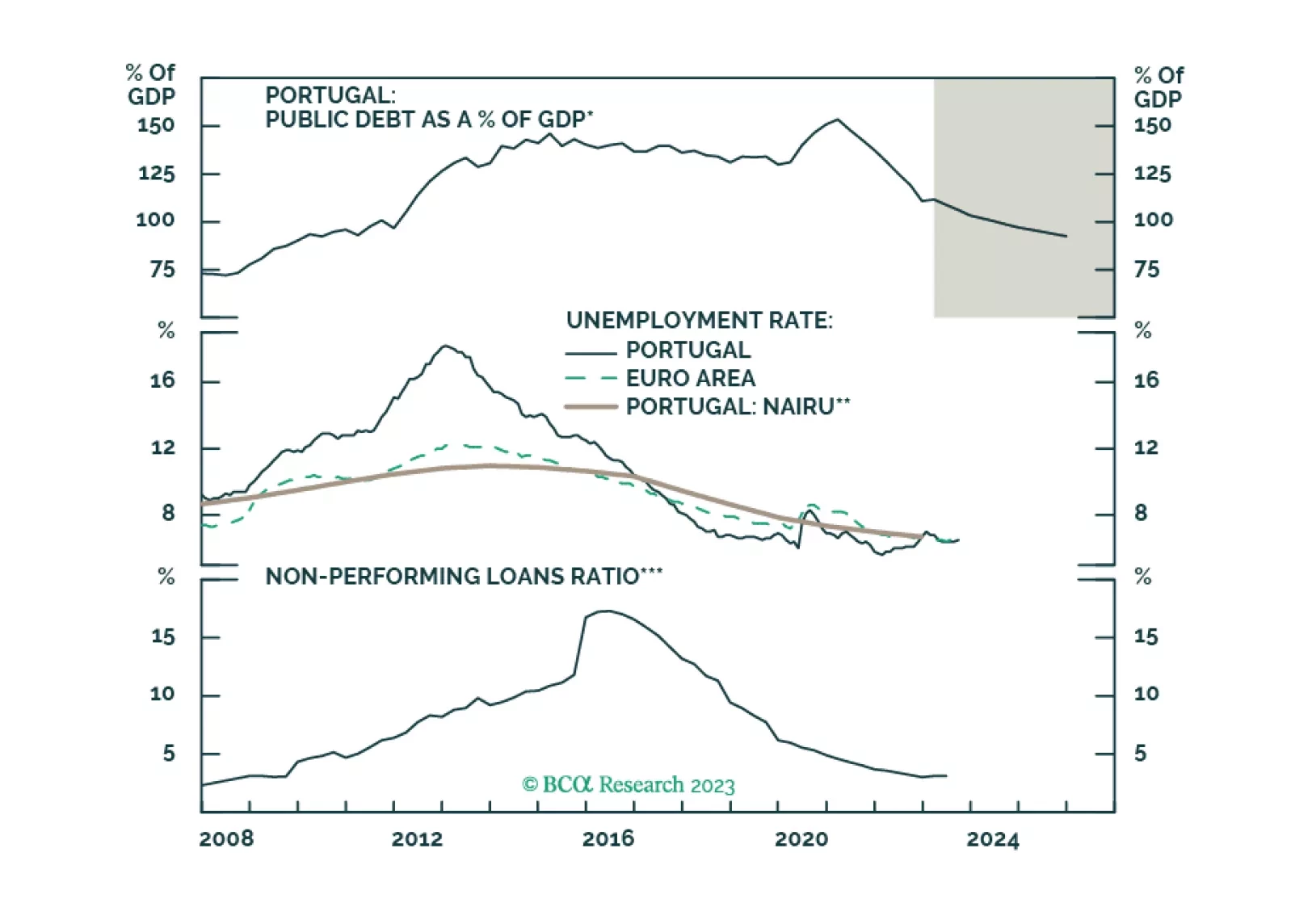

The first stop of the EIS Special Series: PIGS Have Wings takes us to Portugal.

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

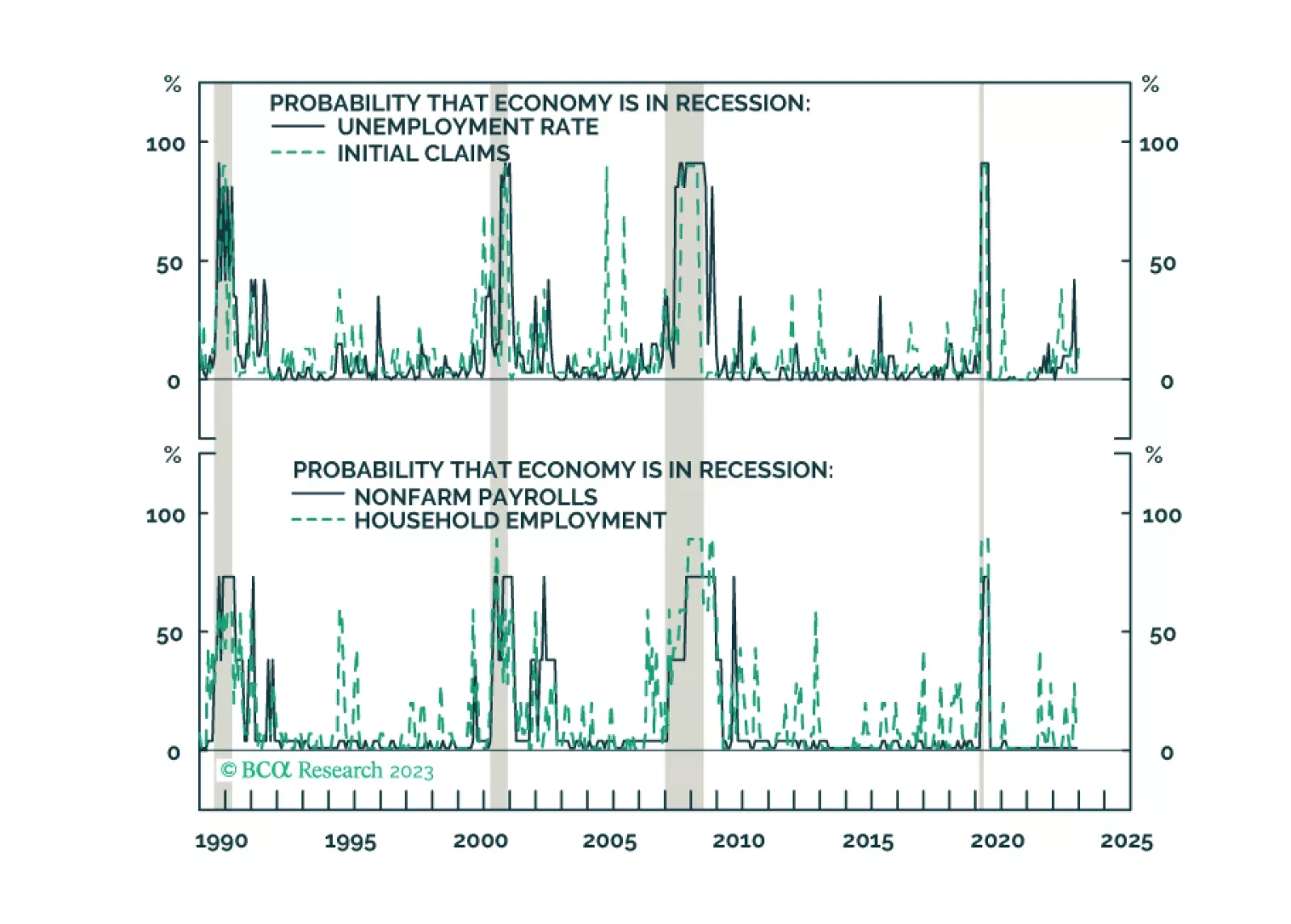

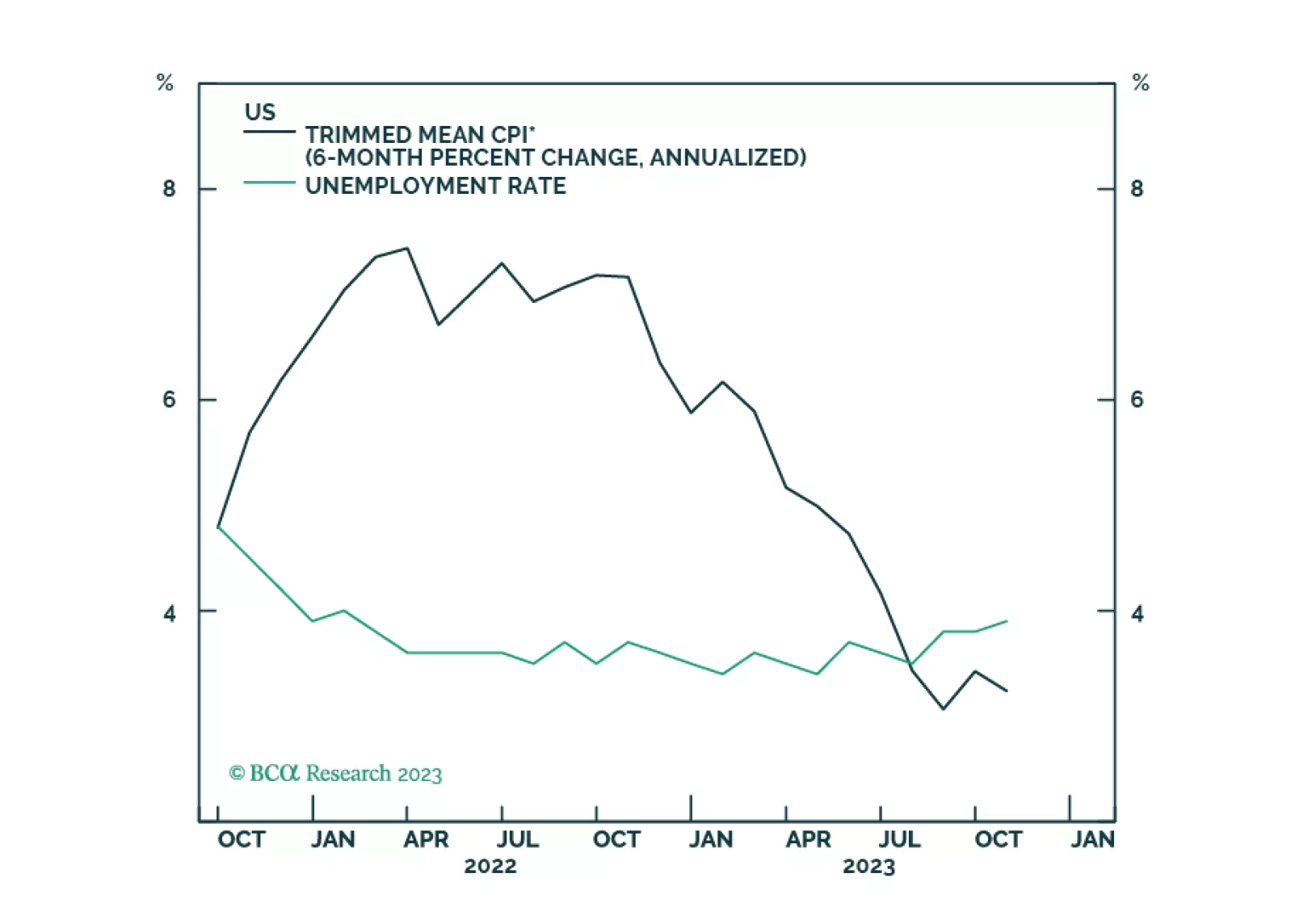

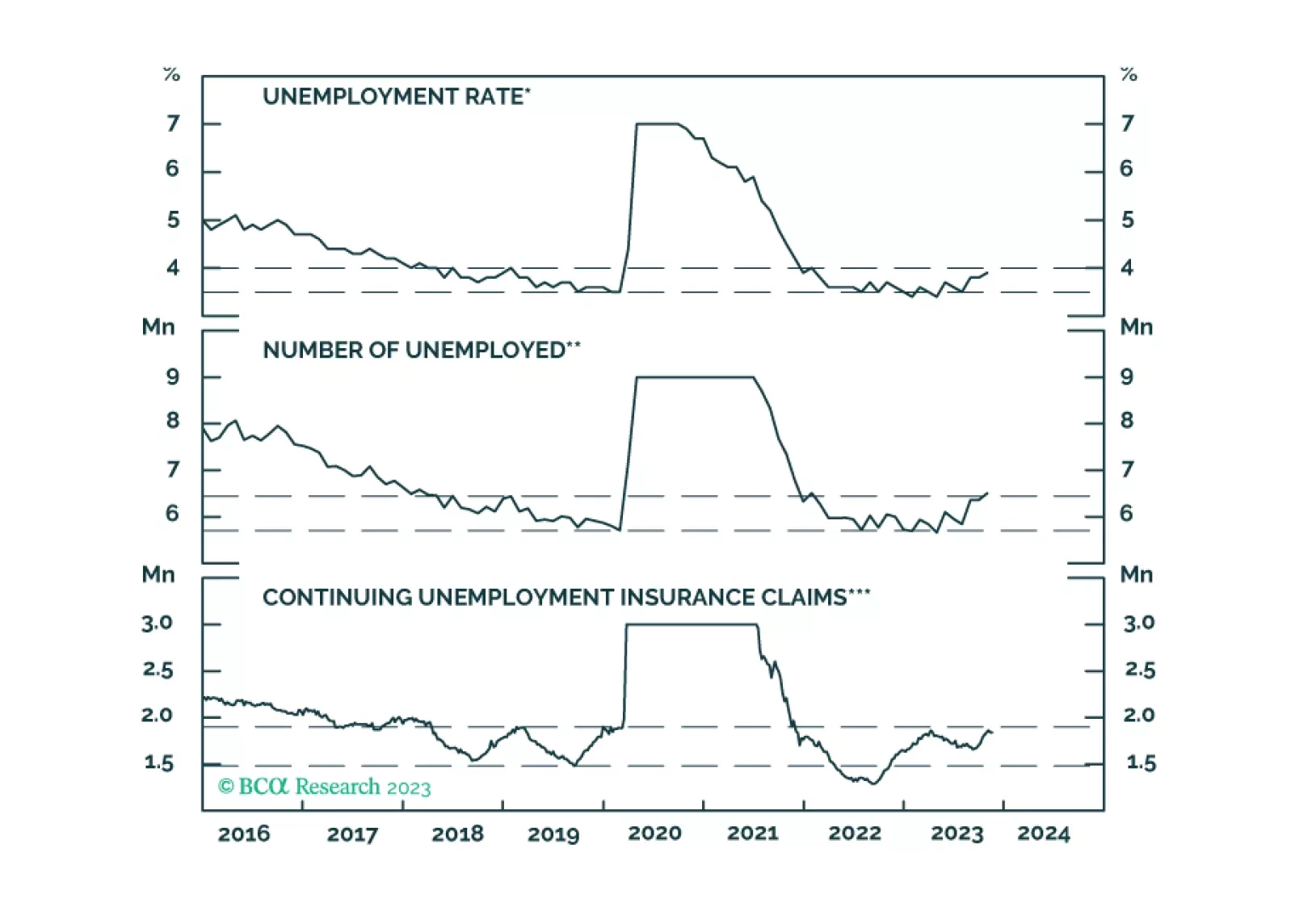

We investigate the recent increase in unemployment with the goal of determining whether it is flagging an imminent US recession.