Gov Sovereigns/Treasurys

Highlights The six-month increase in European bank credit flows amounts to an underwhelming $70 billion, compared to a record high $660 billion in the US and $550 billion in China. Underweight European domestic cyclicals versus their peers in the US and China. Specifically, underweight euro area banks versus US banks. Overweight equities on a long-term (2 years plus) horizon. The mid-single digit return that equities are offering makes them attractive versus ultra-low yielding bonds. But remain neutral equities on a 1-year horizon, until it becomes clear that we can prevent a second wave of the pandemic. Fractal trade: long bitcoin cash, short ethereum. Feature Chart I-1Bank Credit 6-Month Flow Up $70 Bn ##br##In The Euro Area…

Bank Credit 6-Month Flow Up $70 Bn In The Euro Area...

Bank Credit 6-Month Flow Up $70 Bn In The Euro Area...

Chart I-2…But Up $700 Bn ##br##In The US

...But Up $700 Bn In The US

...But Up $700 Bn In The US

Governments and central banks are dishing out an alphabet soup of stimulus. The question is: how much is reaching those that need it? Our preferred approach to assessing monetary stimulus is to focus on the evolution of bank credit flows and bond yields over a six-month period. Bank Credit Flows Have Surged In The US And China, Not In Europe On our preferred assessment, Europe’s monetary stimulus is underwhelming compared with that in the US and China. The six-month increase in US bank credit flows, at $660 billion, is the highest in a decade and not far from the highest ever. In China, the equivalent six-month increase is $550 billion. But in the euro area, the six-month increase in bank credit flows amounts to an underwhelming $70 billion (Charts I-1 - Chart I-4). Chart I-3Bank Credit 6-Month Flow Up $550 Bn In China…

Bank Credit 6-Month Flow Up $550 Bn In China...

Bank Credit 6-Month Flow Up $550 Bn In China...

Chart I-4...And Up ##br##Globally

...And Up Globally

...And Up Globally

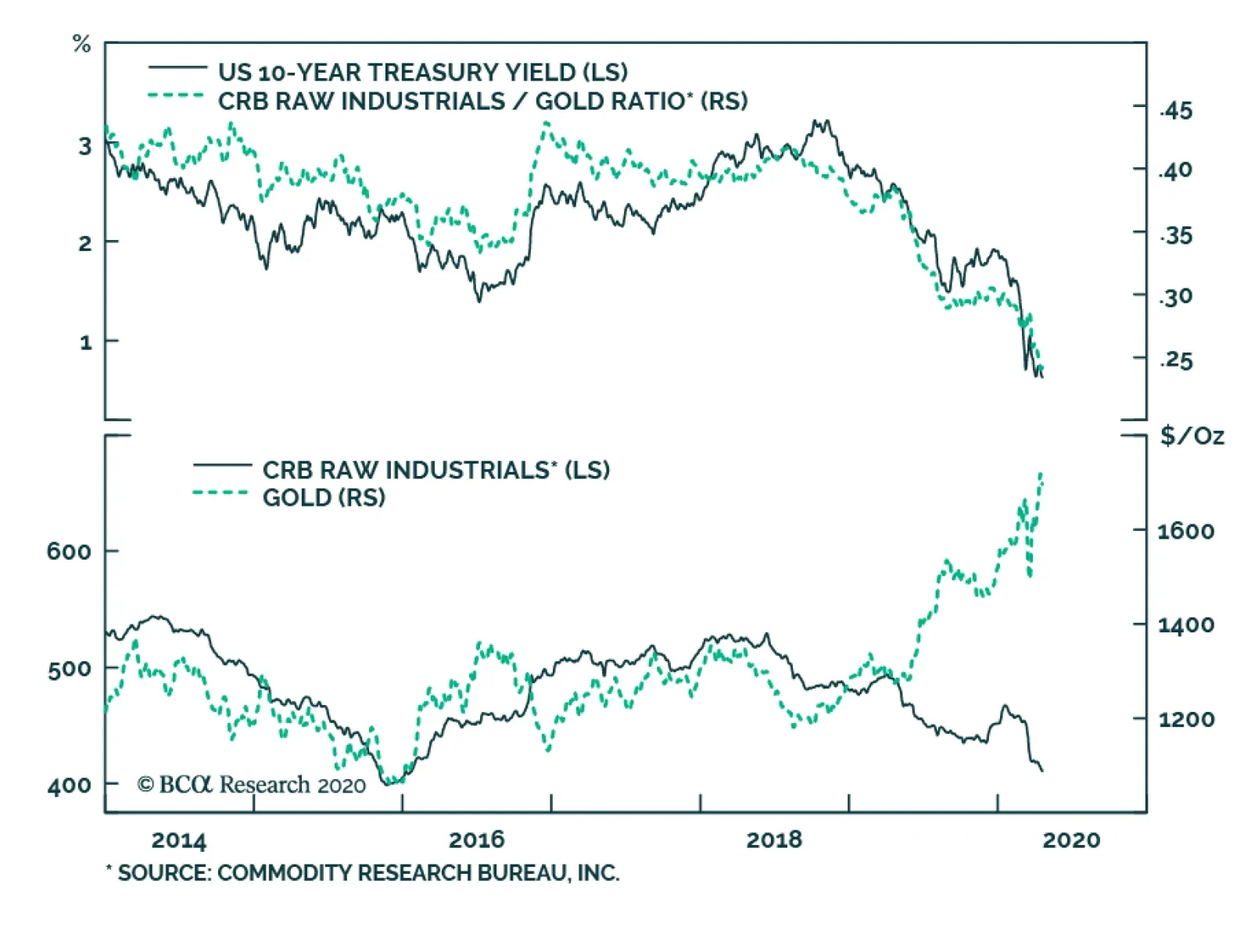

Admittedly, US firms are drawing on pre-arranged bank credit lines rather than taking out new loans. Furthermore, the link between bank credit flows and final demand might be compromised during the current economic shutdown. For example, if firms are borrowing to pay workers who are not producing any output, then the transmission of a credit flow acceleration to a GDP acceleration would be weakened. Europe’s monetary stimulus is underwhelming compared with that in the US and China. Nevertheless, some bank credit flows will still reach the real economy. And the US and China are creating more bank credit flows than Europe. Focus On The Deceleration Of The Bond Yield Turning to the bond yield, it is important to focus not on its level, and not on its decline. Instead, it is important to focus on its deceleration. The focus on the deceleration of the bond yield sounds counterintuitive, but it results from a fundamental accounting identity. The next two paragraphs may seem somewhat technical but read them carefully, as they are important for understanding the transmission of stimulus. GDP is a flow. It measures the flow of goods and services produced in a quarter. Hence, GDP receives a contribution from the flow of credit. The flow of credit, in turn, is established by the level of bond yields. When we talk about stimulating the economy, we mean boosting the GDP growth rate from, say, -1 percent to +1 percent, which is an acceleration of GDP. This acceleration in the GDP flow must come from an acceleration in the flow of credit. This acceleration in the flow of credit, in turn, must come from a deceleration of bond yields. In other words, the bond yield decline in the most recent period must be greater than the decline in the previous period. Banks tend to perform better after bond yields have decelerated. The good news is that in the US and China, bond yields have decelerated; the bad news is that in Europe, they have not. Over the past six months, the 10-year bond yield has decelerated by 40 bps in the US and by 65 bps in China. Yet in France, despite the coronavirus crisis, the 10-year bond yield has accelerated by 60 bps (Charts I-5 - Chart I-8).1 Chart I-5The Bond Yield Has Accelerated ##br##In The Euro Area...

The Bond Yield Has Accelerated In The Euro Area... CHART B

The Bond Yield Has Accelerated In The Euro Area... CHART B

Chart I-6...Decelerated ##br##In The US...

...Decelerated In The US...

...Decelerated In The US...

Chart I-7...Decelerated In China...

...Decelerated In China...

...Decelerated In China...

Chart I-8...And Decelerated Globally

...And Decelerated Globally

...And Decelerated Globally

European bond yields are struggling to decelerate because of their proximity to the lower bound to bond yields, at around -1 percent. The inability to decelerate the bond yield constrains the monetary stimulus that Europe can apply compared to the US and China, whose bond yields are much further from the lower bound constraint. Compared to Europe, the US and China have much stronger decelerations in their bond yields and much stronger accelerations in their bank credit flows. This suggests underweighting European domestic cyclicals versus their peers in the US and China. Specifically, banks tend to perform better after bond yields have decelerated; and they tend to perform worse after bond yields have accelerated. On this basis, underweight euro area banks versus US banks (Chart I-9). Chart I-9Banks Perform Better After Bond Yields Have Decelerated, Worse After Bond Yields Have Accelerated

Banks Perform Better After Bond Yields Have Decelerated, Worse After Bond Yields Have Accelerated

Banks Perform Better After Bond Yields Have Decelerated, Worse After Bond Yields Have Accelerated

Long-Term Asset Allocation Is Straightforward, Shorter-Term Is Not The level of the bond yield, or of so-called ‘financial conditions’, does not drive the short-term oscillations in credit flows. To repeat, it is the acceleration and deceleration of the bond yield that matters. Yet when it comes to the long-term valuation of assets, the level of the bond yield does matter, and when the bond yield is ultra-low it matters enormously. An ultra-low bond yield justifies a much lower prospective return on competing long-duration assets, like equities. The reason is that when bond yields approach their lower bound, bond prices can no longer rise, they can only fall. This higher riskiness of bonds justifies an abnormally low (or zero) ‘risk premium’ on equities. In this world of ultra-low numbers – for both bond yields and equity risk premiums – the low to mid-single digit long-term return that equities are offering makes them attractive versus bonds (Chart I-10). Chart I-10Equities Are Offering Mid-Single Digit Long-Term Returns

Equities Are Offering Mid-Single Digit Long-Term Returns

Equities Are Offering Mid-Single Digit Long-Term Returns

But this long-term valuation argument only works for those with long-term investment horizons. What does long-term mean? There is no clear dividing line, but we would define long-term as two years at the very minimum. For a one-year investment horizon, the much more important question is: what will happen to 12-month forward earnings (profits)? In the stock market recessions of 2008-09 and 2015-16, the stock market reached its low just before forward earnings reached their low. Assuming the same holds true in 2020-21, we must establish whether forward earnings are close to their low or not. In 2008-09, world forward earnings collapsed by 45 percent. In the current recession, which is putatively worse, world forward earnings are down by less than 20 percent to date. To have already reached the cycle low in forward earnings with only half the decline of 2008, the current recession needs to be much shorter than the 2008-09 episode (Chart I-11 and Chart I-12). Chart I-11In The Global Financial Crisis, Forward Earnings Collapsed By 45 Percent

In The Global Financial Crisis, Forward Earnings Collapsed By 45 Percent

In The Global Financial Crisis, Forward Earnings Collapsed By 45 Percent

Chart I-12In The Current Crisis, Forward Earnings Are Down 20 Percent. Is That Enough?

In The Current Crisis, Forward Earnings Are Down 20 Percent. Is That Enough?

In The Current Crisis, Forward Earnings Are Down 20 Percent. Is That Enough?

Whether this turns out to be the case or not hinges on the pandemic and our response to it. A controlled easing of lockdowns will boost growth as more of the economy comes back to life. But too rapid an easing of lockdowns will unleash a second wave of the pandemic, requiring a second wave of economic shutdowns, a double dip recession and a new low in the stock market. Hence, if you have a long-term (2-year plus) investment horizon, the choice between equities and bonds is very straightforward: overweight equities. On this long-term horizon, German and Swedish equities are especially attractive versus negative-yielding bonds. On a 1-year investment horizon, the key question is: can we avoid a second wave of the pandemic? But if you have a 1-year investment horizon, the choice is less straightforward, because it hinges on whether we can avoid a second wave of the pandemic or not. Until it becomes clear that governments will not reopen economies too quickly, remain neutral equities on the 1-year horizon. Fractal Trading System* This week’s recommended trade is a pair-trade within the cryptocurrency asset-class. Long bitcoin cash / short ethereum. Set the profit target at 21 percent with a symmetrical stop-loss. The 12-month rolling win ratio now stands at 61 percent. Chart I-13Bitcoin Cash Vs. Ethereum

Bitcoin Cash Vs. Ethereum

Bitcoin Cash Vs. Ethereum

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 In the US, the 10-year bond yield has declined by 120 bps in the past six months compared with 80 bps in the preceding six months, which equals a deceleration of 40 bps; in China, the 10-year bond yield has declined by 73 bps in the past six months compared with 18 bps in the preceding six months, which equals a deceleration of 65 bps; but in France, the 10-year bond yield has increased by 12 bps in the past six months compared with a 48 bps decline in the preceding six months, which equals an acceleration of 60 bps. Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Yesterday we published a Special Report titled EM: Foreign Currency Debt Strains. We are upgrading our stance on EM local currency bonds from negative to neutral. Before upgrading to a bullish stance, we would first need to upgrade our stance on EM currencies. We recommend receiving long-term swap rates in Russia, Mexico, Colombia, China and India. EM central banks’ swap lines with the Fed could be used to fend off short-term speculative attacks on EM currencies. Nevertheless, they cannot prevent EM exchange rates from depreciation when fundamental pressures warrant weaker EM currencies. For the rampant expansion of US money supply to produce a lasting greenback depreciation, US dollars should be recycled abroad. This is not yet occurring. Domestic Bonds: A New Normal Chart I-1Performance Of EM Domestic Bonds In The Last Decade

Performance Of EM Domestic Bonds In The Last Decade

Performance Of EM Domestic Bonds In The Last Decade

In recent years, our strategy has favored the US dollar and, by extension, US Treasurys over EM domestic bonds. Chart I-1 demonstrates that the EM GBI local currency bond total return index in US dollar terms is at the same level as it was in 2011, and has massively underperformed 5-year US Treasurys. We are now upgrading our stance on EM local currency bonds from negative to neutral. Consistently, we recommend investors seek longer duration in EM domestic bonds while remaining cautious on the majority of EM currencies. Before upgrading to a bullish stance on EM local bonds, we would first need to upgrade our stance on EM currencies. Still, long-term investors who can tolerate volatility should begin accumulating EM local bonds on any further currency weakness. Our upgrade is based on the following reasons: First, there has been a fundamental shift in EM central banks’ policies. In past global downturns, many EM central banks hiked interest rates to defend their currencies. Presently, they are cutting rates aggressively despite large currency depreciation. This is the right policy action to fight the epic deflationary shock that EM economies are presently facing. There has been a fundamental shift in EM central banks’ policies. They are cutting rates aggressively despite large currency depreciation. Historically, EM local bond yields were often negatively correlated with exchange rates (Chart I-2, top panel). Similarly, when EM currencies began plunging two months ago, EM local bond yields initially spiked. However, following the brief spike, bond yields have begun dropping, even though EM currencies have not rallied (Chart I-2, bottom panel). This represents a new normal, which we discussed in detail in our October 24 report. Overall, even if EM currencies continue to depreciate, EM domestic bond yields will drop as they price in lower EM policy rates. Second, the monetary policy transmission mechanism in many EMs was broken before the COVID-19 outbreak. Even though central banks in many developing countries were reducing their policy rates before the pandemic, commercial banks’ corresponding lending rates were not dropping much (Chart I-3, top panel). Chart II-2EM Local Bond Yields And EM Currencies

EM Local Bond Yields And EM Currencies

EM Local Bond Yields And EM Currencies

Chart I-3EM ex-China: Monetary Transmission Has Been Impaired

EM ex-China: Monetary Transmission Has Been Impaired

EM ex-China: Monetary Transmission Has Been Impaired

Further, core inflation rates were at all time lows and prime lending rates in real terms were extremely high (Chart I-3, middle panels). Consequently, bank loan growth was slowing preceding the pandemic (Chart I-3, bottom panel). The reason was banks’ poor financial health. Saddled with a lot of NPLs, banks had been seeking wide interest rate margins to generate profit and recapitalize themselves. With the outburst of the pandemic and the sudden stop in domestic and global economic activity, EM banks’ willingness to lend has all but evaporated. Chart I-4 reveals EM ex-China bank stocks have plunged, despite considerable monetary policy easing in EM, which historically was bullish for bank share prices. This upholds the fact that the monetary policy transmission mechanism in EM is broken. Mounting bad loans due to the pandemic will only reinforce these dynamics. Swap lines with the Fed cannot prevent EM exchange rates from depreciation when fundamental pressures – global and domestic recessions – warrant weaker EM currencies. In brief, EM lower policy rates will not be transmitted to lower borrowing costs for companies and households anytime soon. Loan growth and domestic demand will remain in an air pocket for some time. Consequently, EM policy rates will have to drop much lower to have a meaningful impact on growth. Third, there is value in EM local yields. The yield differential between EM GBI local currency bonds and 5-year US Treasurys shot up back to 500 basis points, the upper end of its historical range (Chart I-5). Chart I-4EM ex-China: Bank Stocks Plunged Despite Rate Cuts

EM ex-China: Bank Stocks Plunged Despite Rate Cuts

EM ex-China: Bank Stocks Plunged Despite Rate Cuts

Chart I-5The EM Vs. US Yield Differential Is Attractive

The EM Vs. US Yield Differential Is Attractive

The EM Vs. US Yield Differential Is Attractive

Bottom Line: Odds favor further declines in EM local currency bond yields. Fixed-income investors should augment their duration exposure. We express this view by recommending receiving swap rates in the following markets: Russia, Mexico, Colombia, India and China. This is in addition to our existing receiver positions in Korean and Malaysian swap rates. For more detail, please refer to the Investment Recommendations section on page 8. Nevertheless, absolute-return investors should be cognizant of further EM currency depreciation. EM Currencies: At Mercy Of Global Growth Chart I-6EM Currencies Correlate With Commodities Prices

EM Currencies Correlate With Commodities Prices

EM Currencies Correlate With Commodities Prices

The key driver of EM currencies has been and remains global growth. The latter will remain very depressed for some time, warranting patience before turning bullish on EM exchange rates. We have long argued that EM exchange rates are driven not by US interest rates but by global growth. Industrial metals prices offer a reasonable pulse on global growth. Chart I-6 illustrates their tight correlation with EM currencies. Even though the S&P 500 has rebounded sharply in recent weeks, there are no signs of a meaningful improvement in industrial metals prices. Various raw materials prices in China are also sliding (Chart I-7). In a separate section below we lay out the case as to why there is more downside in iron ore and steel as well as coal prices in China. Finally, the ADXY – the emerging Asia currency index against the US dollar – has broken down below its 2008, 2016 and 2018-19 lows (Chart I-8). This is a very bearish technical profile, suggesting more downside ahead. This fits with our fundamental assessment that a recovery in global economic activity is not yet imminent. Chart I-7China: Commodities Prices Are Sliding

China: Commodities Prices Are Sliding

China: Commodities Prices Are Sliding

Chart I-8A Breakdown In Emerging Asian Currencies

A Breakdown In Emerging Asian Currencies

A Breakdown In Emerging Asian Currencies

What About The Fed’s Swap Lines? A pertinent question is whether EM central banks’ foreign currency reserves and the Federal Reserve’s swap lines with several of its EM counterparts are sufficient to prop up EM currencies prior to a pickup in global growth. The short answer is as follows: These swap lines will likely limit the downside but cannot preclude further depreciation. With the exception of Turkey and South Africa, virtually all mainstream EM banks have large foreign currency reserves. On top of this, several of them – Brazil, Mexico, South Korea and Singapore– have recently obtained access to Fed swap lines. Their own foreign exchange reserves and the swap lines with the Fed give them an option to defend their currencies from depreciation if they choose to do so. However, selling US dollars by EM central banks is not without cost. When central banks sell their FX reserves or dollars obtained from the Fed via swap lines, they withdraw local currency liquidity from the system. As a result, banking system liquidity shrinks, pushing up interbank rates. This is equivalent to hiking interest rates. The Fed’s outright money printing is the sole reason to buy EM risk assets and currencies at the moment. Yet, EM fundamentals – namely, its growth outlook – remain downbeat. Hence, the cost of defending the exchange rate by using FX reserves is both liquidity and credit tightening. In such a case, the currency could stabilize but the economy will take a beating. Since the currency depreciation was itself due to economic weakness, such a policy will in and of itself be self-defeating. The basis is that escalating domestic economic weakness will re-assert its dampening effect on the currency. Of course, EM central banks can offset such tightening by injecting new liquidity. However, this could also backfire and lead to renewed currency depreciation. Bottom Line: EM central banks’ swap lines with the Fed are primarily intended to instill confidence among investors in financial markets. They could be used to fend off short-term speculative attacks on EM currencies. Nevertheless, they cannot prevent EM exchange rates from depreciation when fundamental pressures – global and domestic recessions – warrant weaker EM currencies. What About The Fed’s Money Printing? Chart I-9The Fed Is Aggressively Printing Money

The Fed Is Aggressively Printing Money

The Fed Is Aggressively Printing Money

The Fed is printing money and monetising not only public debt but also substantial amounts of private debt. This will ultimately be very bearish for the US dollar. Chart I-9 illustrates that the Fed is printing money much more aggressively than during its quantitative easing (QE) policies post 2008. The key difference between the Fed’s liquidity provisions now and during its previous QEs is as follows: When the Fed purchases securities from or lends to commercial banks, it creates new reserves (banking system liquidity) but it does not create money supply. Banks’ reserves at the Fed are not a part of broad money supply. This was generally the case during previous QEs when the Fed was buying bonds mostly – but not exclusively – from banks, therefore increasing reserves without raising money supply by much. When the Fed lends to or purchases securities from non-banks, it creates both excess reserves for the banking system and money supply (deposits at banks) out of thin air. The fact that US money supply (M2) growth is now much stronger than during the 2010s QEs suggests the recent surge in US money supply is due to the Fed’s asset purchases from and lending to non-banks, which creates money/deposits outright. The rampant expansion of US money supply will eventually lead to the greenback’s depreciation. However, for the US dollar to depreciate against EM currencies, the following two conditions should be satisfied: 1. US imports should expand, reviving global growth, i.e., the US should send dollars to the rest of the world by buying goods and services. This is not yet happening as domestic demand in America has plunged and any demand recovery in the next three to six months will be tame and muted. 2. US investors should channel US dollars to EM to purchase EM financial assets. In recent weeks, foreign flows have been returning to EM due to the considerable improvement in EM asset valuations. However, the sustainability of these capital flows into EM remains questionable. The main reasons are two-fold: (A) there is huge uncertainty on how efficiently EM countries will be able handle the economic and health repercussions of the pandemic; and (B) global growth remains weak and, as we discussed above, it has historically been the main driver of EM risk assets and currencies. Bottom Line: The Fed’s outright money printing is the sole reason to buy EM risk assets and currencies at the moment. Yet, EM fundamentals – namely, its growth outlook – remain downbeat. Overall, we recommend investors to stay put on EM risk assets and currencies in the near-term. Investment Recommendations Chart I-10China: Bet On Lower Long-Term Yields

China: Bet On Lower Long-Term Yields

China: Bet On Lower Long-Term Yields

We have been recommending receiving rates in a few markets such as Korea and Malaysia. Now, we are widening this universe to include Russia, Mexico, Colombia, China, and India. In China, the long end of the yield curve offers value (Chart I-10, top panel). The People’s Bank of China has brought down short rates dramatically but the long end has so far lagged (Chart I-10, bottom panel). We recommend investors receive 10-year swap rates. Fixed-income investors could also bet on yield curve flattening. The recovery in China will be tame and the PBoC will keep interest rates lower for longer. Consequently, long-dated swap rates will gravitate toward short rates. We are closing three fixed-income trades: In Mexico, we are booking profits on our trade of receiving 2-year / paying 10-year swap rates – a bet on a steeper yield curve. This position has generated a 152 basis-point gain since its initiation on April 12, 2018. In Colombia, our bet on yield curve flattening has produced a loss of 28 basis points since January 17, 2019. We are closing it. In Chile, we are closing our long 3-year bonds / short 3-year inflation-linked bonds position. This trade has returned 2.0% since we recommended it on October 3, 2019. For dedicated EM domestic bond portfolios, our overweights are Russia, Mexico, Peru, Colombia, Korea, Malaysia, Thailand, India, China, Pakistan and Ukraine. Our underweights are South Africa, Turkey, Brazil, Indonesia and the Philippines. The remaining markets warrant a neutral allocation. Regarding EM currencies, we continue to recommend shorting a basket of the following currencies versus the US dollar: BRL, CLP, ZAR, IDR, PHP and KRW. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Chinese Steel, Iron Ore And Coal Markets: Heading South Chart II-1Steel, Iron Ore And Coal Prices: More Downside Ahead?

Steel, Iron Ore And Coal Prices: More Downside Ahead?

Steel, Iron Ore And Coal Prices: More Downside Ahead?

Odds are that iron ore, steel and coal prices will all continue heading south (Chart II-1). Lower prices will harm both Chinese and global producers of these commodities. Steel And Iron Ore The oversupplied conditions in the Chinese steel market will become even more aggravated over the next three to six months. First, Chinese output of steel products has not contracted even though demand plunged in the first three months of the year, creating oversupply. Despite falling steel prices and the demand breakdown resulting from the COVID-19 outbreak, Chinese crude steel output still grew at 1.5% and its steel products output only declined 0.6% between January and March from a year ago (Chart II-2). Chart II-2Steel Products Output In China: Still No Contraction

Steel Products Output In China: Still No Contraction

Steel Products Output In China: Still No Contraction

The profit margin of Chinese steel producers has compressed but not enough to herald a sizable cut in mainland steel production. Despite oversupply, Chinese steel producers are reluctant to curtail output to prevent layoffs. This year, there will be 62 million tons of new steel production capacity while 82 million tons of obsolete capacity will be shut down. As the capacity-utilization rate (CUR) of the new advanced production capacity will be much higher than the CUR on those soon-to-be-removed capacities in previous years, this will help lift steel output. Second, Chinese steel demand has plummeted, and any revival will be mild and gradual over the next three to six months. Construction accounts for about 55% of Chinese steel demand, with about 35% coming from the property market and 20% from infrastructure. Additionally, the automobile industry contributes about 10% of demand. All three sectors are currently in deep contraction (Chart II-3). Looking ahead, we expect that the demand for steel from property construction and automobile production will revive only gradually. Overall, it will continue contracting on a year-on-year basis, albeit at a diminishing rate than now. While we projected a 6-8% rise in Chinese infrastructure investment for this year, most of that will be back-loaded to the second half of the year. In addition, modest and gradual steel demand increases from this source will not be able to offset the loss of demand from the property and automobile sectors. The oversupplied conditions in the Chinese steel market will become even more aggravated over the next three to six months. Reflecting the disparity between weak demand and resilient supply, steel inventories in the hands of producers and traders are surging, which also warrants much lower prices (Chart II-4). Chart II-3Deep Contraction In Steel Demand From Major Users

Deep Contraction In Steel Demand From Major Users

Deep Contraction In Steel Demand From Major Users

Chart II-4Significant Build-Up In Steel Inventories

Significant Build-Up In Steel Inventories

Significant Build-Up In Steel Inventories

Chart II-5Chinese Iron Ore Imports Will Likely Decline In 2020

Chinese Iron Ore Imports Will Likely Decline In 2020

Chinese Iron Ore Imports Will Likely Decline In 2020

Regarding iron ore, mushrooming steel inventories in China and lower steel prices will eventually lead to steel output cutbacks in the country. This will be compounded by shrinking steel production outside of China, dampening global demand for iron ore. Besides, in China, scrap steel prices have fallen more sharply than iron ore prices have. This makes the use of scrap steel more appealing than iron ore in steel production. Chinese iron ore imports will likely drop this year (Chart II-5). Finally, the global output of iron ore is likely to increase in 2020. The top three producers (Vale, Rio Tinto and BHP) have all set their 2020 guidelines above their 2019 production levels. This will further weigh on iron ore prices. Coal Although Chinese coal prices will also face downward pressure, we believe that the downside will be much less than that for steel and iron ore prices. Coal prices have already declined nearly 27% from their 2019 peak. They recently declined below 500 RMB per ton – the lower end of a range that the government generally tries to maintain. Prices had not dropped below this level since September 2016. In the near term, prices could go down by another 5-10%, given that record-high domestic coal production and imports have overwhelmed the market (Chart II-6). Coal prices have already declined nearly 27% from their 2019 peak. They recently declined below 500 RMB per ton – the lower end of a range that the government generally tries to maintain. However, there are emerging supportive forces. China Coal Transport & Distribution Association (CCTD), the nation’s leading industry group, on April 18, called on the industry to slash production (of both thermal and coking coal) in May by 10%. It also proposed that the government should restrict imports. The CCTD stated that about 42% of the producers are losing money at current coal prices. The government had demanded producers make similar cuts for a much longer time duration in 2016, which pushed coal to sky-high prices. The outlook for a revival in the consumption of electricity and, thereby, in the demand for coal is more certain than it is for steel and iron ore. About 60% of Chinese coal is used to generate thermal power. Finally, odds are rising that the government will temporarily impose restrictions on coal imports as it did last December – when coal imports to China fell by 70% as a result. Investment Implications Companies and countries producing these commodities will be hurt by the reduction of Chinese purchases. These include, but are not limited to, producers in Indonesia, Australia, Brazil and South Africa. Iron ore and coal make up 10% of total exports in Brazil, 6% in South Africa, 18% in Indonesia and 32% in Australia. Investors should avoid global steel and mining stocks (Chart II-7). Chart II-6Chinese Coal Output And Imports Are At Record Highs

Chinese Coal Output And Imports Are At Record Highs

Chinese Coal Output And Imports Are At Record Highs

Chart II-7Avoid Global Steel And Mining Stocks For Now

Avoid Global Steel And Mining Stocks For Now

Avoid Global Steel And Mining Stocks For Now

We continue to recommend shorting BRL, ZAR and IDR versus the US dollar. Ellen JingYuan He Associate Vice President ellenj@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights The Chinese economy is recovering at a slower rate than the equity market has priced in. There is a high likelihood of negative revisions to Q2 EPS estimates and an elevated risk of a near-term price correction in Chinese stocks. We expect a meaningful pickup in credit growth in H1 to improve domestic demand gain tractions in H2. This supports our overweight stance on Chinese stocks in the next 6-12 months, in both absolute and relative terms. There is still a strong probability that the yield curve will flatten, and the 10-year government bond yield may even dip below 2% in the wake of disappointing economic data in Q2. But our baseline scenario suggests the 10-year government bond yield should bottom no later than Q3 of this year. Feature This week’s report addresses pressing concerns from clients in China’s post-Covid-19 environment. China’s economy contracted by 6.8% in Q1, the largest GDP growth slump since 1976. Furthermore, the IMF’s baseline scenario projects a 3% contraction in global economic growth in 2020, with the Chinese economy growing at a mere 1.2%.1 This dim annual growth outlook means that the contraction in China’s economy will likely extend to Q2, dragging down corporate profit growth. In our April 1st report2 we recommended that investors maintain a neutral stance on Chinese stocks in the next three months due to uncertainties surrounding the pandemic, the oversized passive outperformance in Chinese stocks, and heightened risks for further risk-asset selloffs. On a 6- to 12-month horizon, however, we have a higher conviction that Chinese stocks will outperform global benchmarks. Our view is based on a decisive shift by policymakers to a “whatever it takes” approach to boost the economy. We believe that the speed of China’s economic recovery in the second half of 2020 will outpace other major economies. Q: China’s economy is recovering ahead of other major economies. Why did you recently downgrade your tactical call on Chinese equities from overweight to neutral relative to global stocks? A: China’s economy is recovering, but it is recovering at a slower rate than the equity market has fully priced in (Chart 1A and 1B). We believe the likelihood of negative revisions to Q2 EPS estimates is high, and the risk of a near-term price correction in Chinese stocks remains elevated. Chart 1AElevated Chinese Equity Outperformance Relative To Global Stocks

Elevated Chinese Equity Outperformance Relative To Global Stocks

Elevated Chinese Equity Outperformance Relative To Global Stocks

Chart 1BChinese Stocks Largely Ignored Weakness In Domestic Economy

Chinese Stocks Largely Ignored Weakness In Domestic Economy

Chinese Stocks Largely Ignored Weakness In Domestic Economy

The lackluster March data suggests that the pace of China’s economic recovery in April and even May will likely disappoint, weighing on the growth prospects for Q2’s corporate earnings (Chart 2). Chart 2EPS Growth Estimates Likely To Capitulate In Q2

EPS Growth Estimates Likely To Capitulate In Q2

EPS Growth Estimates Likely To Capitulate In Q2

The work resumption rate in China’s 36 provinces jumped sharply between mid-February and mid-March. However, since that time, the resumption rate among large enterprises has hovered around 80% of normal capacity (Chart 3). Chart 3Work Resumption Hardly Improved Since Mid-March

Three Questions Following The Coronacrisis

Three Questions Following The Coronacrisis

The flattening of the work resumption rate curve is due to a lack of strong recovery in demand. Chart 4So Far No Strong Recovery In Domestic Demand

So Far No Strong Recovery In Domestic Demand

So Far No Strong Recovery In Domestic Demand

The flattening of the resumption rate curve is due to a lack of strong recovery in demand. Although there was a surge in Chinese imports in crude oil and raw materials, the increase was the result of China taking advantage of low commodity prices. This surge cannot be sustained without a pickup in domestic demand. The March bounce back in domestic demand from the manufacturing, construction, and household sectors has all been lackluster (Chart 4). External demand, which growth remained in contraction through March, will likely worsen in Q2 (Chart 5). Exports shrunk by 6.6% in March, up from a deep contraction of 17.2% in January-February. Export orders can take more than a month to be processed, therefore, March’s data reflects pent-up orders from the first two months of the year. The US and European economies started their lockdowns in March, so Chinese exports will only feel the full impact of the collapse in demand from its trading partners in April and May. The work resumption rate will advance only if the momentum in domestic demand recovery increases to fully offset the collapse in external demand. The current 83% rate of work resumption implies that industrial output growth in April will remain in contraction on a year-over-year basis (Chart 6). Chart 5External Demand Will Worsen In Q2

External Demand Will Worsen In Q2

External Demand Will Worsen In Q2

Chart 6Will Q2 Industrial Output Growth Remain In Contraction?

Will Q2 Industrial Output Growth Remain In Contraction?

Will Q2 Industrial Output Growth Remain In Contraction?

Although we maintain a constructive outlook on Chinese risk assets in the next 6 to 12 months, the short-term picture remains volatile in view of the emerging economic data. As such, we recommend investors to maintain short-term hedges for risk asset positions. Q: China’s policy response to mitigate the economic blow from COVID-19 has been noticeably smaller than programs rolled out in key developed economies, especially the US. Why do you think such measured stimulus from China warrants an overweight stance on Chinese stocks in the next 6-12 months relative to global benchmarks? A: It is true that the size of existing Chinese stimulus, as a percentage of the Chinese economy, is smaller than that has been announced in the US. But this is due to a different approach China is taking in stimulating its economy. In addition, both the recent policy rhetoric and PBoC actions suggest a large credit expansion is in the works. This will likely overcompensate the damage on China’s aggregate economy, and generate an outperformance in both Chinese economic growth and returns on Chinese risk assets in the next 6 to 12 months. China’s policy responses have an overarching focus on stimulating new demand and investment, which is a different approach from the programs offered by its Western counterparts. In the US, the combination of fiscal and monetary stimulus amounts to 11% of GDP as of April 16, with almost all policy support targeted at keeping companies and individuals afloat. In comparison, China’s policy response accounts for a mere 1.2% of its GDP.3 However, this direct comparison understates the enormous firepower in the Chinese stimulus toolkit, specifically a credit boom. As noted in our February 26 report,4 China has largely resorted to its “old economic playbook” by generating a huge credit wave to ride out the economic turmoil. Our prediction of the policy shift towards a significant escalation in stimulus was confirmed at the March 27 Politburo meeting. Moreover, the April 17 Politburo meeting reinforced a “whatever it takes” policy shift with direct calls on more forceful central bank policy actions, a first since the global financial crisis in 2008.5 Since 2008, the overnight repo rate’s breaking into the IORR-IOER corridor has been a reliable indicator leading to impressive credit upcycles. The PBoC’s recent aggressive easing measures have pushed down the interbank repo rate below the central bank’s interest rate on required reserves (IORR). The price for interbank borrowing is now near the lower range of the rate corridor, between the IORR and the interest rate on excess reserves (IOER). Since 2008, the overnight repo rate’s breaking into the IORR-IOER corridor has been a reliable indicator leading to impressive credit upcycles (Chart 7). Such credit super cycles, in turn, have led to both economic booms and an outperformance in Chinese stocks. Chart 7Another Credit Super Cycle Is In The Works

Another Credit Super Cycle Is In The Works

Another Credit Super Cycle Is In The Works

Chart 8Financial Conditions Were Extremely Tight In 2011-2014

Financial Conditions Were Extremely Tight In 2011-2014

Financial Conditions Were Extremely Tight In 2011-2014

The 2012-2015 cycle was an exception to the relationship between the overnight interbank repo rate, credit growth and Chinese stock performance. A steep pickup in credit growth in 2012 coincided with a leap in the overnight interbank repo rate, and the credit boom did not help boost demand in the real economy or improve Chinese stock performance. This is because corporate borrowing was severely curtailed by high lending rates during a four-year monetary tightening cycle from 2011 to 2014 (Chart 8). The credit boom during that cycle was largely driven by explosive growth in short-term shadow-bank lending and wealth management products (WMP), and did not channel into the real economy.6 We do not think such an extreme phenomena will replay under the current circumstances. Monetary stance will likely remain tremendously accommodative through the end of the year to facilitate a continuous rollout of medium- to long-term bank loans and local government bonds. Chinese financial institutions’ “animal spirits” may have been unleashed. But under the scrutiny of the Macro-Prudential Assessment Framework and the New Asset Management Rules,7 the "animal spirits" are unlikely to run up enough risks to prompt the PBoC to prematurely tighten liquidity conditions in the interbank market. Marginal propensity in China is pro-cyclical, which tends to lag credit cycles by 6 months. Chart 9Marginal Propensity In China Is Pro-Cyclical

Marginal Propensity In China Is Pro-Cyclical

Marginal Propensity In China Is Pro-Cyclical

Both corporate and household marginal propensity, a measure of the willingness to spend, will pick up as well. Marginal propensity is pro-cyclical, which tends to lag credit cycles by 6 months (Chart 9). In other words, when interest rates are low and credit growth improves, corporates and households tend to spend more. The meaningful expansion in credit growth, which started in Q1 and will sustain in the coming two to three quarters, will help corporate and household spending gain tractions in H2. This constructive view on Chinese stimulus and economic recovery supports our overweight stance on Chinese stocks in the next 6-12 months, in both absolute and relative terms. Q: The yield curve in Chinese government bonds has steepened following PBoC’s aggressive monetary easing announcements. Has the Chinese 10-year bond yield bottomed? A: No, we do not think the 10-year bond yield has bottomed. There is probability the 10-year government bond yield may briefly dip below 2% in Q2. However, barring a multi-year global economic recession, we think the 10-year government bond yield will bottom no later than Q3 this year. Chart 10A Wide Gap Between The Long and Short

A Wide Gap Between The Long and Short

A Wide Gap Between The Long and Short

The short end of the yield curve dropped disproportionally compared with the long end, following the PBoC’s announcement to place its first IOER cut since 2008 (Chart 10). This led to a rapid steepening in the yield curve. While our view supports a flattening of the yield curve in Q2 and even a 50bps drop in the 10-year government bond yield, we think that the capitulation will be brief. In order for the 10-year government bond yield to remain below 2% for an extended period of time, the market needs to believe one or more of the following will happen: The pandemic will cause a multi-year global economic recession, preventing the PBoC from normalizing its policy stance in the foreseeable future. The duration and depth of the economic impact from the pandemic are still moving targets. Our baseline scenario suggests that the Chinese economic recovery will pick up momentum in H2 this year. The PBoC will not normalize its policy stance even when the economy has stabilized. The PBoC has a track record as a reactive central bank rather than a proactive one. Still, during each of the past three economic and credit cycles, the PBoC has started to normalize its interest rate on average nine months following a bottom in the business cycle (Chart 11). The tightening of interest rate even applied to the prolonged economic downturn and deep deflationary cycle in 2015/16 (Chart 12). Chart 11The 'Old Faithful' PBoC Policy Normalization Pattern

The 'Old Faithful' PBoC Policy Normalization Pattern

The 'Old Faithful' PBoC Policy Normalization Pattern

Chart 12Policy Normalized Even After A Long Economic Downturn

Policy Normalized Even After A Long Economic Downturn

Policy Normalized Even After A Long Economic Downturn

Chart 132008 Or 2015?

2008 Or 2015?

2008 Or 2015?

How the yield curve has historically behaved also depended on the market’s expectations on the speed of the economic recovery, and the timing of the subsequent monetary policy normalization. The yield curved spiked in the wake of substantial monetary easing and pickup in credit growth, in both 2008 and 2015 (Chart 13). While in 2008 the yield curve moved in lockstep with the 3-month SHIBOR with a perfect reverse correlation, in the 2015/16 cycle the yield curve spiked initially but quickly flattened. The long end of the yield curve capitulated as soon as the market realized the economic slowdown was a prolonged one. The 10-year government bond yield, after trending sideways in early 2016, only truly bottomed after the nominal output growth troughed in Q1 2016 (Chart 13, bottom panel). Will the yield curve behave like in 2008, or more like in 2015 in this cycle? We think it will be somewhere in between. The current economic cycle bottomed in Q1, but the economy is only recovering slowly and we expect a U-shaped economic recovery rather than a 2008-style V-shaped one. At the same time, our baseline scenario does not suggest the current environment will evolve into a 4-year deflationary cycle as in the 2012-2016 period. Therefore, we expect the low interest rate environment to endure for another two to three quarters before the PBoC starts to reverse its policy stance back to the pre-COVID-19 range. As such, the yield on 10-year government bonds will fall, possibly by as much as 50bps, when the economic data disappoint in Q2 and more rate cuts are forthcoming. But it will bottom when the economic recovery starts to gain traction in H22020 and the market starts to price in a subsequent monetary policy normalization. When growth slows and debt rises sharply, the PBoC will need to join its western counterparts to permanently maintain an ultra-low interest rate policy to accommodate its high debt level. We acknowledge the fact that China’s potential output growth is trending down (Chart 14). But it has been trending downwards since 2011. A structurally slowing rate of economic growth has not prevented the PBoC from cyclically raising its policy rate. Hence, unless we see evidence that the pandemic is meaningfully lowering China’s potential growth on par with growth rates in the DMs, our baseline scenario does not support a structural ultra-low interest rate environment in China. China’s debt-to-GDP ratio will most likely rise substantially this year, given that the credit impulse will gain momentum and GDP will grow very modestly. However, this rapid rise in the debt-to-GDP ratio will most likely not be sustained beyond this year. Even if we assume that credit impulse will account for 40% of GDP in 2020 (the same magnitude as in 2008/09), a sharp reversal in the output gap in 2021, as predicted by IMF,8 will flatten the debt-to-GDP ratio curve (Chart 15). Moreover, following every credit super cycle in the past, Chinese authorities have put a brake on the debt-to-GDP ratio. Chart 14China's Potential Growth Is Likely To Trend Lower...

China's Potential Growth Is Likely To Trend Lower...

China's Potential Growth Is Likely To Trend Lower...

Chart 15...But Has Not Stopped PBoC From Flattening The Debt Curve

...But Has Not Stopped PBoC From Flattening The Debt Curve

...But Has Not Stopped PBoC From Flattening The Debt Curve

All in all, while we see a high possibility for the 10-year government bond yield to fall in Q2, the decline will be limited in terms of duration. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1IMF World Economic Outlook, April 2020 2Please see China Investment Strategy Weekly Report "Investing During A Global Pandemic," dated April 1, 2020, available at cis.bcaresearch.com 3IMF, Policy Responses To COVID-19 https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19#U 4Please see China Investment Strategy Weekly Report "China: Back To Its Old Economic Playbook?" dated February 26, 2020, available at cis.bcaresearch.com 5“Stable monetary policy must become more flexible” and “use RRR reductions, lower interest rates, re-lending and other measures to preserve adequate liquidity and guide the loan prime rate downwards.” Statements from Xi Jinping, April 17, 2020 Politburo Meeting. http://www.gov.cn/xinwen/2020-04/17/content_5503621.htm 6 Bankers’ acceptances - short-term debt instruments guaranteed by commercial banks - swelled by 887% between end-2008 and 2012. The outstanding amount of WMPs jumped from 1.7 trillion RMB in 2009 to more than 9 trillion RMB by H12013. In contrast, the amount of RMB-denominated bank loans increased by only 67% during the same period. 7The Macro-Prudential Assessment Framework and the New Asset Management Rules were implemented in 2016 and 2018, respectively. They are designed to create additional restrictions to curb shadow-bank lending and broaden the PBoC’s oversight on banks’ WMP holdings. 8The April IMF World Economic Outlook predicts a 1.2% Chinese GDP growth in 2020 and a 9.2% GDP growth in 2021. Cyclical Investment Stance Equity Sector Recommendations

Highlights Social distancing makes it impossible to do jobs that require close personal interaction, yet these are the very job sectors that have kept jobs growth alive in recent decades. If social distancing persists, then AI will penetrate these job sectors too. Aggregate wage inflation is set to collapse – not just temporarily, but structurally. Structurally overweight US T-bonds versus the core European bonds in Germany, France, Netherlands, Switzerland and Sweden. Structurally overweight big technology, structurally underweight banks. Structurally overweight S&P 500 versus Euro Stoxx 50. Fractal trade: long Australian 30-year bond versus US 30-year T-bond. Feature Social distancing will feature large in our lives for the foreseeable future, and it carries a profound consequence. Social distancing really means physical distancing. And physical distancing diminishes the ways that we can interact with other humans – through the qualities of empathy, sympathy, the ability to recognise and respond to emotional cues, and to express ourselves through complex movements. You cannot hug someone on Facetime. Social distancing makes it impossible to do jobs that require close personal interaction. From an economic perspective, social distancing makes it impossible to do jobs that require close personal interaction. It follows that in the recent bloodbath of job losses, the biggest casualties have been in employment sectors that rely on this close personal interaction: food services and drinking places (waitresses, bartenders, and baristas), ambulatory healthcare services, hotels, and social assistance (Table I-1). Table I-1Social Distancing Is Destroying Jobs That Require Close Personal Interaction

Social Distancing Is Good For Robots, Bad For Humans

Social Distancing Is Good For Robots, Bad For Humans

A profound consequence arises because these are the very sectors that have kept jobs growth alive in recent decades (Table I-2). Millions of new jobs that rely on close personal interaction have more than offset the structural job destruction in manufacturing and finance. As well as being export-proof, jobs that require this close personal interaction have been ‘artificial intelligence (AI) proof’. That is, until now. Table I-2Jobs That Require Close Personal Interaction Have Been The Engine Of Jobs Growth

Social Distancing Is Good For Robots, Bad For Humans

Social Distancing Is Good For Robots, Bad For Humans

One UK doctor told the New York Times “we’re basically witnessing 10 years of change in one week”. Before the virus, online consultations made up only 1 percent of doctors’ appointments. But now, three in four UK patients are seeing their doctor remotely. Moravec’s Paradox + Social Distancing = A Very Tough Jobs Market Regular readers will know that one of our mega-themes is the far-reaching societal and economic implications of Moravec’s Paradox. Named after the professor of robotics, Hans Moravec, the paradox points out that: For AI the hard things are easy, but the easy things are hard. By the hard things, we mean things that require ‘narrow-frame pattern recognition’ within a defined body of knowledge. For example, playing chess, translating languages, diagnosing medical conditions, and analysing legal problems. We find these tasks hard, but AI finds them effortless. By the easy things, we mean our social skills: empathy, sympathy, the ability to recognise and respond to emotional cues, and to express ourselves through complex movements. To us, all these things are second nature, but AI finds them very hard to replicate. The reason, it turns out, is that the higher brain that enables us to learn and play chess and solve similar abstract problems evolved relatively recently. Whereas the ancient lower brain that enables complex movement and the associated giving and receiving of emotional signals took much longer to evolve. As AI is just reverse engineering the human brain, AI has found it easy to replicate the less-evolved higher brain functions, but very difficult to replicate the skills that emanate from the deeply evolved lower brain. Millions of new jobs that rely on close personal interaction have more than offset the structural job destruction in manufacturing and finance. The far-reaching societal and economic implication is that we have misunderstood and mispriced what is difficult and what is easy. By reverse engineering the brain, AI is correcting this mispricing. So far, AI has been most disruptive to high-paying jobs requiring abstract problem-solving skills, such as in finance. AI has been less disruptive to jobs requiring close personal interaction (Table I-3). But if social distancing persists, then AI will disrupt those jobs too, especially during a recession. Table I-3New Jobs That Require Close Personal Interaction Have Offset Lost Jobs In Manufacturing And Finance

Social Distancing Is Good For Robots, Bad For Humans

Social Distancing Is Good For Robots, Bad For Humans

Labour Market Disruption Intensifies During A Recession To paraphrase Ernest Hemingway, industries adopt labour-saving technologies gradually then suddenly. And the suddenly tends to be during a recession. This is because once an industry has already shed many workers, it is easier to restructure the industry with a new labour-saving technology that reduces labour input permanently. At the start of the Great Depression a substantial part of the US automobile industry was still based on skilled craftsmanship. These smaller, less productive craft-production plants were the ones that shut down permanently, while plants that had adopted labour-saving mass production had the competitive advantage that enabled them to survive. The result was a major restructuring of the auto productive structure. Likewise, until the late 1990s, the ‘typing pool’ was a ubiquitous feature of the office environment. But once the 2000 downturn arrived, these typing jobs became extinct to be replaced by the wholesale roll-out of Microsoft Word. After the 2008-09 recession, UK economic power became focussed in a few large firms that could access the finance to ensure their survival. As small firms went by the wayside, job growth came disproportionately from self-employment and the ‘gig economy’. In this case, the labour market disruption hurt productivity as an army of freelancers ended up doing their own sales, marketing and accounts in which they had no specialism (Chart I-1 and Chart I-2). Chart I-1The 1990s UK Recovery Produced No Increase In Self-Employment...

The 1990s UK Recovery Produced No Increase In Self-Employment...

The 1990s UK Recovery Produced No Increase In Self-Employment...

Chart I-2...But The 2010s UK Recovery Produced A Huge Increase In Self-Employment

...But The 2010s UK Recovery Produced A Huge Increase In Self-Employment

...But The 2010s UK Recovery Produced A Huge Increase In Self-Employment

The point is that all recessions produce major structural changes in the labour market and the current recession will be no different. If social distancing persists, it will nullify the social skill advantage that humans have over AI. Therefore, one structural change will be that AI disrupts the more ‘human’ job sectors that have so far escaped its penetration. All recessions produce major structural changes in the labour market. To repeat, labour market disruption arrives suddenly. Within the space of a few weeks, most UK patients have switched to receiving their medical care online or by telephone. Admittedly, the patients are still ‘seeing’ a human doctor, but the question and answer consultations are a classic example of narrow-frame pattern recognition. Meaning that it would be a small step to upgrade the human doctor to the superior diagnosis from AI. And if AI can produce a superior diagnosis to your human doctor, why can’t AI also produce a a superior legal analysis to your human lawyer? The Investment Implications Even when the labour market seemed to be humming and unemployment rates were at multi-decade lows, aggregate wage inflation was anaemic (Chart I-3 and Chart I-4). A major reason was the hollowing out of high paying jobs and substitution with low paying jobs. Now that unemployment rates are surging, and AI is penetrating even more job sectors, aggregate wage inflation is set to collapse – not just temporarily, but structurally. Chart I-3Unemployment Rates Have Been At Multi-Decade Lows...

Unemployment Rates Have Been At Multi-Decade Lows...

Unemployment Rates Have Been At Multi-Decade Lows...

Chart I-4...But Wage Inflation Has Been ##br##Anaemic

...But Wage Inflation Has Been Anaemic

...But Wage Inflation Has Been Anaemic

This leads to the following investment implications: 1. All bond yields will gravitate to their lower bound, so any bond yield that can go lower will go lower. 2. It follows that bond investors should continue to overweight US T-bonds versus the core European bonds in Germany, France, Netherlands, Switzerland and Sweden (Chart I-5). Chart I-5Any Bond Yield That Can Go Lower Will Go Lower

Any Bond Yield That Can Go Lower Will Go Lower

Any Bond Yield That Can Go Lower Will Go Lower

3. Underweight banks structurally. Depressed and flattening yield curves combined with shrinking demand for private credit constitutes a strong headwind. Banks are now underperforming in both up markets and in down markets (Chart I-6). Chart I-6Banks Are Underperforming In Both Up Markets And Down Markets

Banks Are Underperforming In Both Up Markets And Down Markets

Banks Are Underperforming In Both Up Markets And Down Markets

4. Overweight technology structurally. As AI penetrates even more job sectors, the superstar companies of big tech will continue to thrive. The duopoly of Apple and Google are designing proximity-tracking apps for every smartphone in the world. Big tech is laying down the law to governments, and there is not even a hint of antitrust suits. Tech is now outperforming in both up markets and in down markets (Chart I-7). Chart I-7Tech Is Outperforming In Both Up Markets And Down Markets

Tech Is Outperforming In Both Up Markets And Down Markets

Tech Is Outperforming In Both Up Markets And Down Markets

5. Finally, if big tech outperforms banks, the sector composition of the S&P 500 versus the Euro Stoxx 50 makes it inevitable that the US equity market will structurally outperform the euro area equity market (Chart I-8). Chart I-8If Big Tech Outperforms Banks, The S&P 500 Must Outperform The Euro Stoxx 50

If Big Tech Outperforms Banks, The S&P 500 Must Outperform The Euro Stoxx 50

If Big Tech Outperforms Banks, The S&P 500 Must Outperform The Euro Stoxx 50

Fractal Trading System* The steep decline in the US 30-year T-bond yield means that it has crossed below the Australian 30-year bond yield for the first time in recent history. Resulting from this dynamic, this week’s recommended trade is long the Australian 30-year bond versus the US 30-year T-bond. Set the profit target at 9 percent with a symmetrical stop-loss. Chart I-930-Year Govt. Bonds: Australia Vs. US

30-Year Govt. Bonds: Australia Vs. US

30-Year Govt. Bonds: Australia Vs. US

In other trades, long IBEX versus Euro Stoxx 600 hit its 3 percent stop-loss, while long nickel versus copper is half way to its 11 percent profit target. The rolling 12-month win ratio now stands at 63 percent. When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Yesterday. BCA Research's US Bond Strategy service's analysis concluded that it is premature to call the bottom in Treasury yields. We are seeing the bad US economic data, which raises the possibility that we are close to the trough in US economic growth.…

Highlights Q1/2020 Performance Breakdown: Our recommended model bond portfolio underperformed the custom benchmark by -40bps during the first quarter of the year – a number that would have been far worse if not for the changes in exposures for duration (increased) and spread product (decreased) made in early March. Winners & Losers: Underperformance was concentrated in sovereign debt, US Treasuries in particular (-94bps), as yields plummeted. This detracted from the outperformance in spread product (+51bps) led by US investment grade corporates (+34bps) and emerging markets (+20bps). Scenario Analysis For The Next Six Months: Given the ongoing uncertainty over when the COVID-19 pandemic and economy-crushing global lockdown will end, we are sticking close to benchmark on overall duration and spread product exposure. Instead, we recommend focusing more on country allocation and spread product relative value to generate outperformance, favoring markets where there is direct involvement from central banks. Feature Global bond markets were roiled in the first quarter of 2020 by the economic fallout from the COVID-19 pandemic. Government bond yields crashed to all-time lows while volatility reached extremes across both sovereign debt and credit. The quick, coordinated policy response from global monetary and fiscal authorities – which includes unprecedented levels of direct central bank asset purchases, both in terms of size and the breadth across markets and counties - has helped stabilize global credit spreads and risk assets, more generally. The outlook remains highly uncertain, however, with many governments worldwide looking to reopen their collapsed economies, risking the potential resurgence of a virus still lacking effective treatment or a vaccine. We are focusing more on relative value between counties and sectors. In this report, we review the performance of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio during the eventful first quarter of 2020. We also present our updated recommended positioning for the portfolio for the next six months. The main takeaway there is that we are focusing more on relative value between counties and sectors while staying close to benchmark on both overall global duration and spread product exposure versus government bonds (Table 1). Table 1GFIS Model Bond Portfolio Recommended Positioning For The Next Six Months

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

Chart 1Q1/2020 Performance: Lagging, But It Could Have Been Much Worse

Q1/2020 Performance: Lagging, But It Could Have Been Much Worse

Q1/2020 Performance: Lagging, But It Could Have Been Much Worse

As a reminder to existing readers (and to new clients), the model portfolio is a part of our service that complements the usual macro analysis of global fixed income markets. The portfolio is how we communicate our opinion on the relative attractiveness between government bond and spread product sectors. This is done by applying actual percentage weightings to each of our recommendations within a fully invested hypothetical bond portfolio. Q1/2020 Model Portfolio Performance Breakdown: A Missed Rally In Sovereigns, Outperformance In Credit The total return for the GFIS model portfolio (hedged into US dollars) in the first quarter was -0.1%, underperforming the custom benchmark index by -40bps (Chart 1).1 That relative underperformance came from the government bond side of the portfolio, while our spread product allocation outperformed the benchmark. US Treasuries underperformed the most (-91bps) with losses concentrated in the +10 year maturity bucket. (Table 2). After US Treasuries, euro area high-yield corporates were the second worst performer, underperforming the benchmark by -10bps. Outperformance in spread product was driven by US investment grade industrials (+22bps) and EM credit (+20bps). Table 2GFIS Model Bond Portfolio Q1/2020 Overall Return Attribution

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

The potential losses to our model portfolio were greatly mitigated by changes in positioning during the quarter. Our decision to raise overall global duration exposure to neutral at the beginning of March helped shield the portfolio as yields plummeted.2 We followed this by upgrading sovereign debt in the US and Canada, both higher-beta countries, to overweight while moving to an underweight stance on US high-yield debt, euro area investment-grade and high-yield debt, and emerging market (EM) USD-denominated sovereign and corporate debt.3 In an environment of rampant uncertainty, these allocation changes helped prevent catastrophic losses in the model portfolio that had previously been positioned for a pickup in global growth. The potential losses to our model portfolio were greatly mitigated by changes in positioning during the quarter. In terms of the specific breakdown between the government bond and spread product allocations in our model portfolio, the former generated -91bps of underperformance versus our custom benchmark index while the latter outperformed by +51bps. The bar charts showing the total and relative returns for each individual government bond market and spread product sector are presented in Charts 2 and 3. Chart 2GFIS Model Bond Portfolio Q1/2020 Government Bond Performance Attribution

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

Chart 3GFIS Model Bond Portfolio Q1/2020 Spread Product Performance Attribution By Sector

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

The most significant movers were: Biggest Outperformers Overweight US investment grade industrials (+22bps) Underweight euro area investment grade corporate bonds (+16bps) Underweight EM USD-denominated corporates (+12bps) Overweight US investment grade financials (+10bps) Underweight Japanese government bonds with maturity greater than 10 years (+8bps) Biggest Underperformers Underweight US government bonds with maturity greater than 10 years (-36bps) Underweight US government bonds with maturity of 3-5 years (-17bps) Underweight US government bonds with maturity of 5-7 years (-16bps) Underweight US government bonds with maturity of 1-3 years (-13bps) Underweight US government bonds with maturity of 7-10 years (-12bps) Chart 4 presents the ranked benchmark index returns of the individual countries and spread product sectors in the GFIS model bond portfolio for Q1/2020. The returns are hedged into US dollars (we do not take active currency risk in this portfolio) and are adjusted to reflect duration differences between each country/sector and the overall custom benchmark index for the model portfolio. We have also color-coded the bars in each chart to reflect our recommended investment stance for each market during Q1/2020 (red for underweight, dark green for overweight, gray for neutral).4 Ideally, we would look to see more green bars on the left side of the chart where market returns are highest, and more red bars on the right side of the chart were returns are lowest. Predictably, government debt performed the best in Q1/2020 as global bond yields fell and monetary authorities raced to support economies and inject liquidity. UK, US, and Canadian government debt delivered the best returns this quarter. While we started the year neutral or underweight those assets, we moved to an overweight allocation in March, which helped salvage some returns. Also worth noting is that Australian government debt, where we have maintained a structural overweight stance, was one of the top performing markets during the first quarter. The deepest losses were sustained in EM USD-denominated sovereign and corporate debt, and euro area high-yield. Although it seems a distant memory at this point, we did start this quarter on an optimistic note and expected spreads on these products to narrow as global growth picked up. However, we were able to shield our portfolio against excessive losses in these products by moving to an underweight stance in March once the severity of the COVID-19 global economic shock become apparent. Bottom Line: Our recommended model bond portfolio underperformed the custom benchmark index during the first quarter of the year. The underperformance was concentrated in government bonds, which rallied on the back of the global pandemic. However, the portfolio outperformed the benchmark in spread products, where the combination of massive fiscal/monetary easing and direct central bank asset purchases have brought credit spreads under control. Future Drivers Of Portfolio Returns Typically, in these quarterly performance reviews of our model bond portfolio, we attempt to make return forecasts for the portfolio based off scenario analysis and quantitative predictions of various fixed income asset classes. In the current unprecedented economic and financial market environment, however, we are reluctant to rely on model coefficients and correlations to estimate expected returns. Instead, in this report, we will focus on discussing the logic behind our current model portfolio positioning and how those allocations should expect to contribute to the overall portfolio performance over the next six months. Looking ahead, the performance of the model bond portfolio will be driven by three main factors: Our recommended overweight stance on US spread product that is backstopped by the Fed—US investment grade corporates, Agency CMBS, and Ba-rated high-yield; Our recommended overweight stance on relatively higher-yielding sovereigns like the US and Italy; Our recommended underweight stance on EM USD-denominated corporates and sovereigns, where the specter of defaults and liquidity crunches looms. In terms of specific weightings in the GFIS model bond portfolio, we have moderated our stance on global spread product since our previous review of the portfolio.5 While the monetary liquidity backdrop is highly bullish, with central banks aggressively buying bonds and keeping policy rates at the zero lower bound, it is still unclear if and when economies will be able to successfully reopen and put an end to the COVID-19 recession. We are now recommending only a small relative overweight of two percentage points for spread product versus the benchmark index (Chart 5), leaving room to add more should the news on the virus and global growth take a turn for the better. Chart 5Overall Portfolio Allocation: Slightly Overweight Credit

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

GFIS Model Bond Portfolio Q1/2020 Performance Review & Current Allocations: Traversing The Turmoil

We also remain neutral on overall portfolio duration exposure. Our Global Duration Indicator, which contains growth data like our global leading economic indicator and the global ZEW expectations index, has plunged and is signaling bond yields will stay depressed over the next six months (Chart 6). Yet at the same time, yields in most countries have been unable to hit new lows after the panic-driven bond rally in late February and early March, even as global oil prices have collapsed and inflation expectations remain depressed, suggesting that yields already discount a lot of bad news. Chart 6Our Duration Indicator Is Signaling Government Bond Yields Will Stay Low

Our Duration Indicator Is Signaling Government Bond Yields Will Stay Low

Our Duration Indicator Is Signaling Government Bond Yields Will Stay Low

We do not see much value in taking a big directional bet on yields through overall duration exposure at the present time. We also think it is far too early to contemplate reducing duration – even with many global equity and credit markets having rallied sharply off the lows – given the persistent uncertainty over the timing of a recovery in global growth. Thus, we are maintaining a neutral overall portfolio exposure (Chart 7). Chart 7Overall Portfolio Duration: At Benchmark

Overall Portfolio Duration: At Benchmark

Overall Portfolio Duration: At Benchmark

Chart 8Country Allocation: Favor Those With Higher Betas To Global Yields

Country Allocation: Favor Those With Higher Betas To Global Yields

Country Allocation: Favor Those With Higher Betas To Global Yields