Government

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

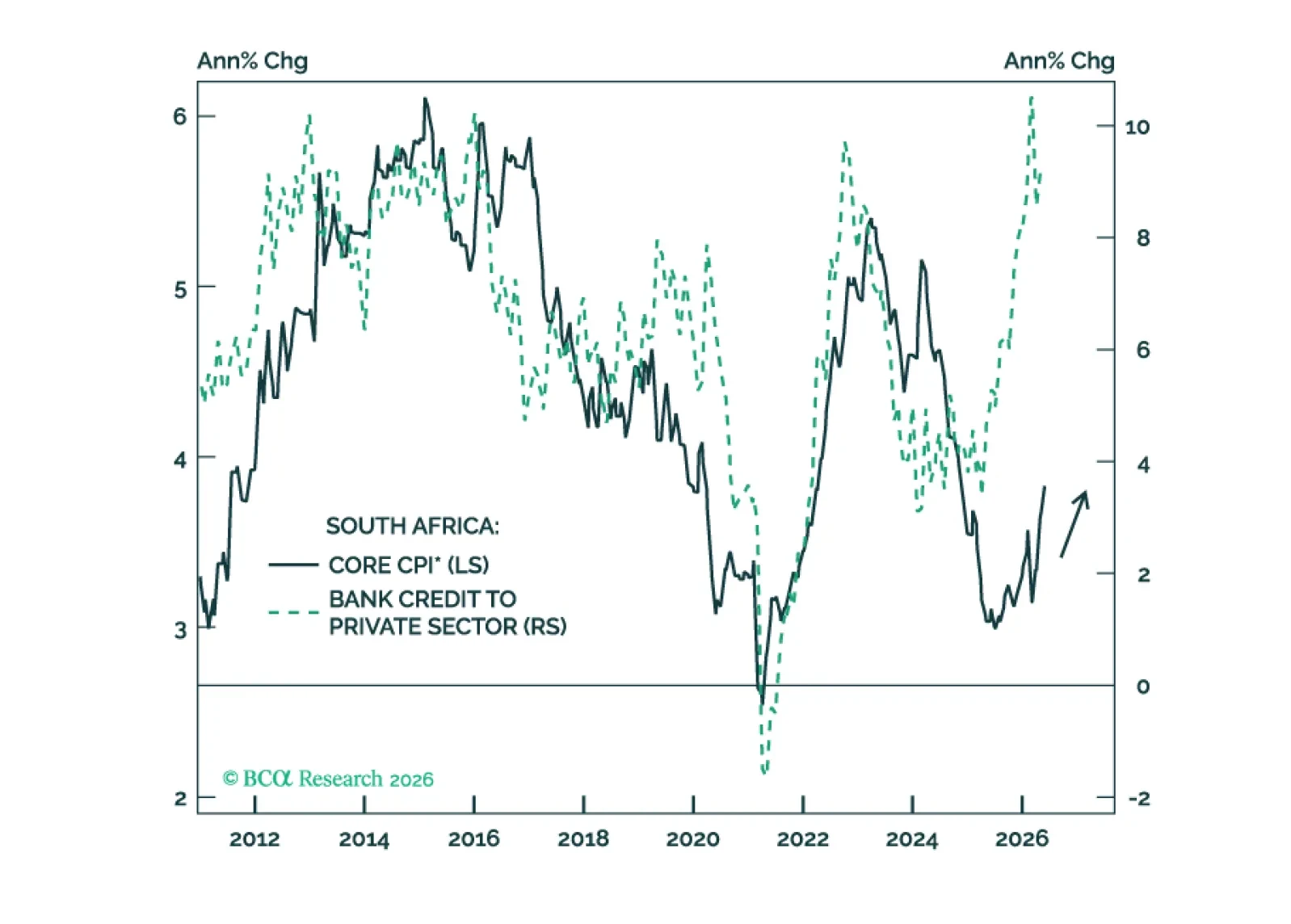

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

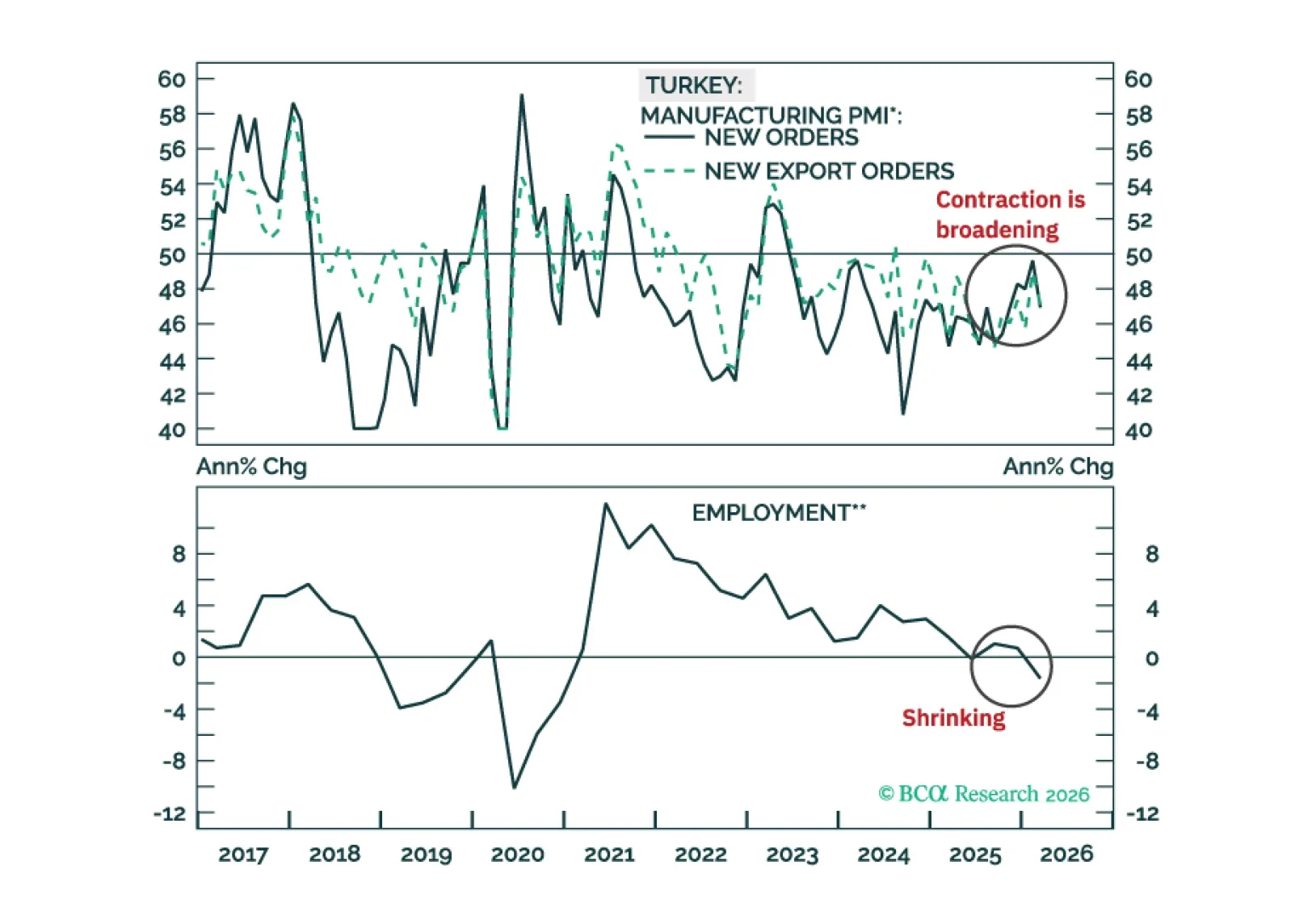

The Turkish financial markets will struggle in the very near term, but beyond that, the cyclical disinflation process will resume. Fixed-income investors should put Turkish 2-year local currencybonds on a ‘buy’ watch list.

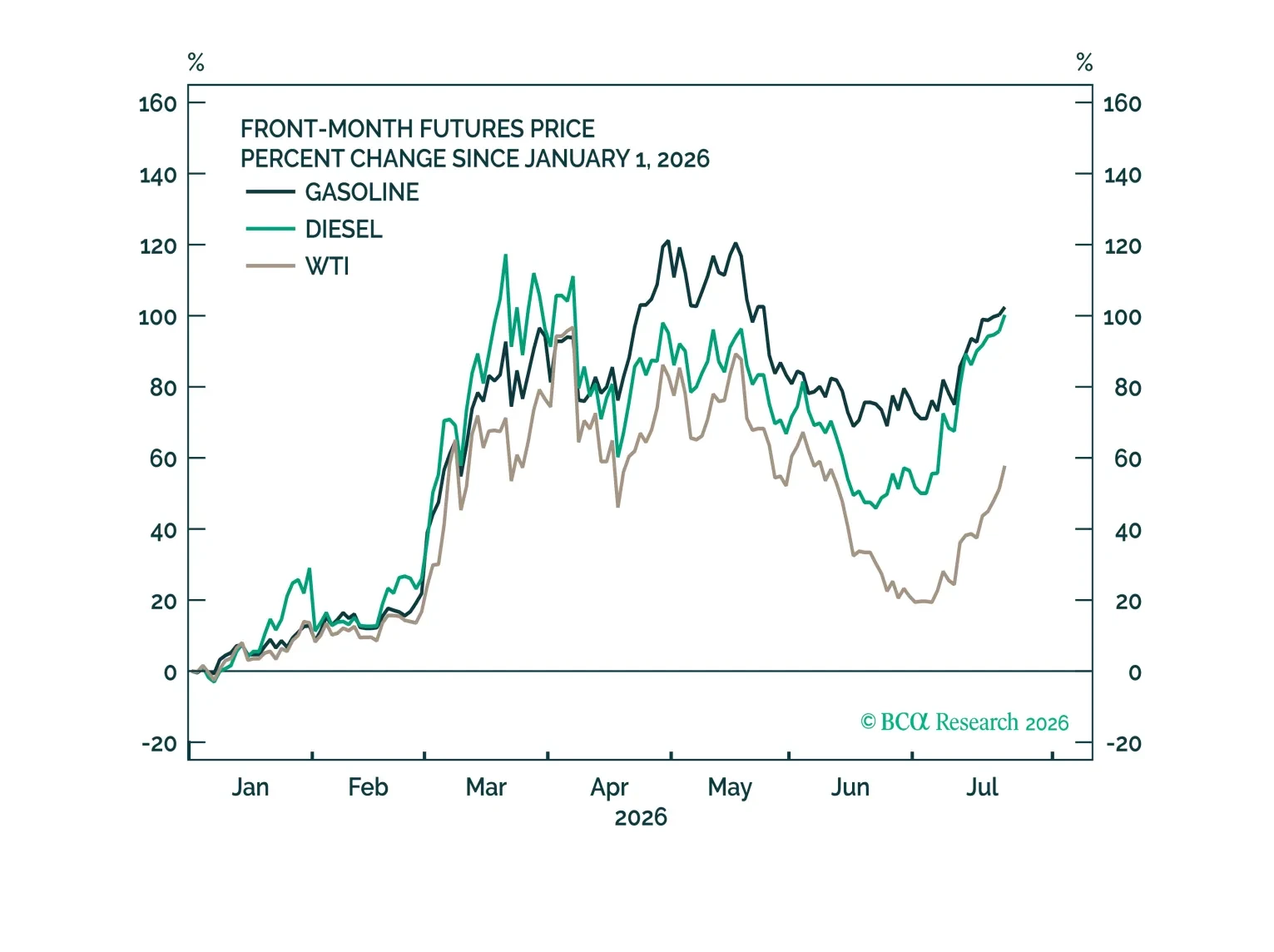

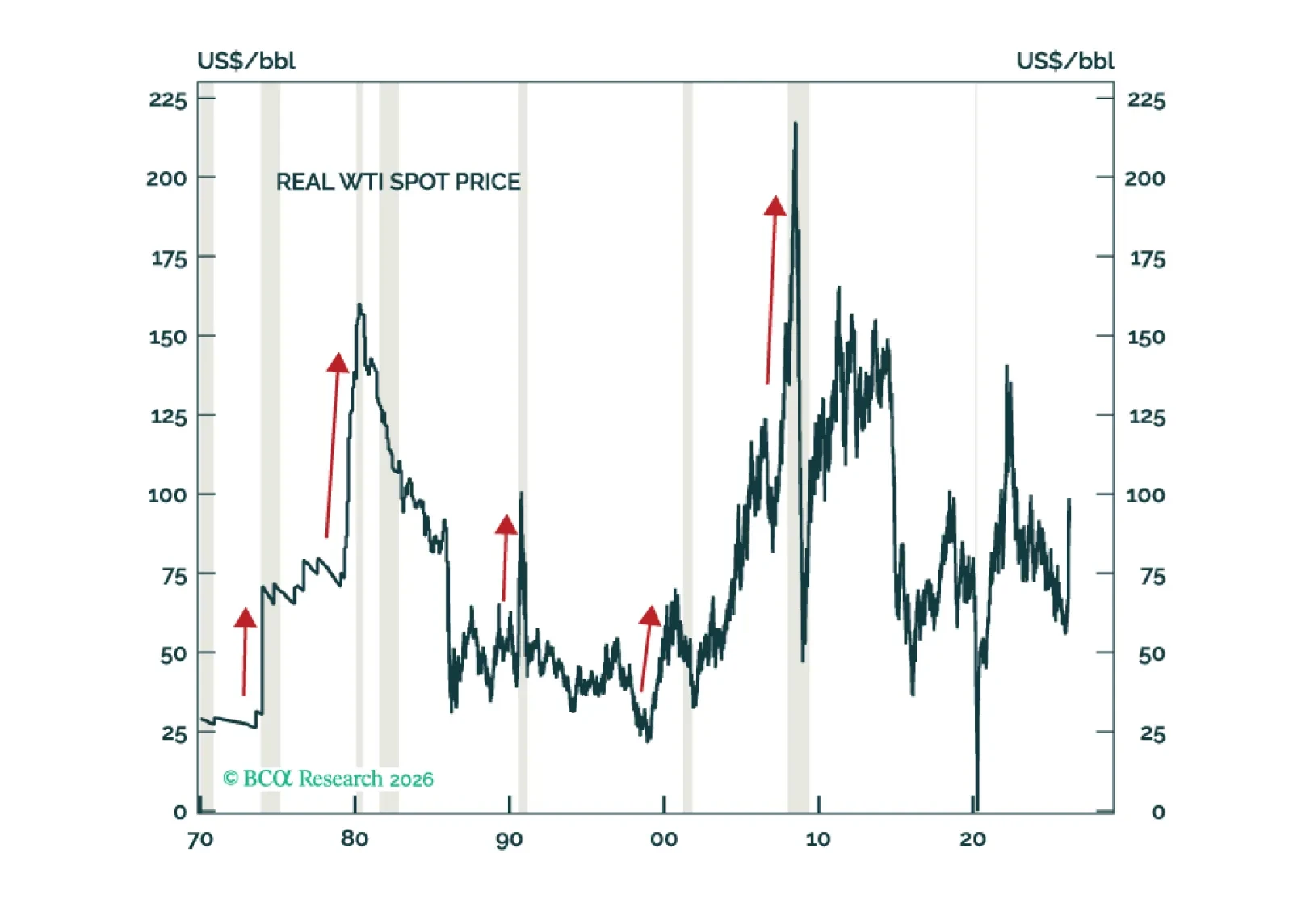

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

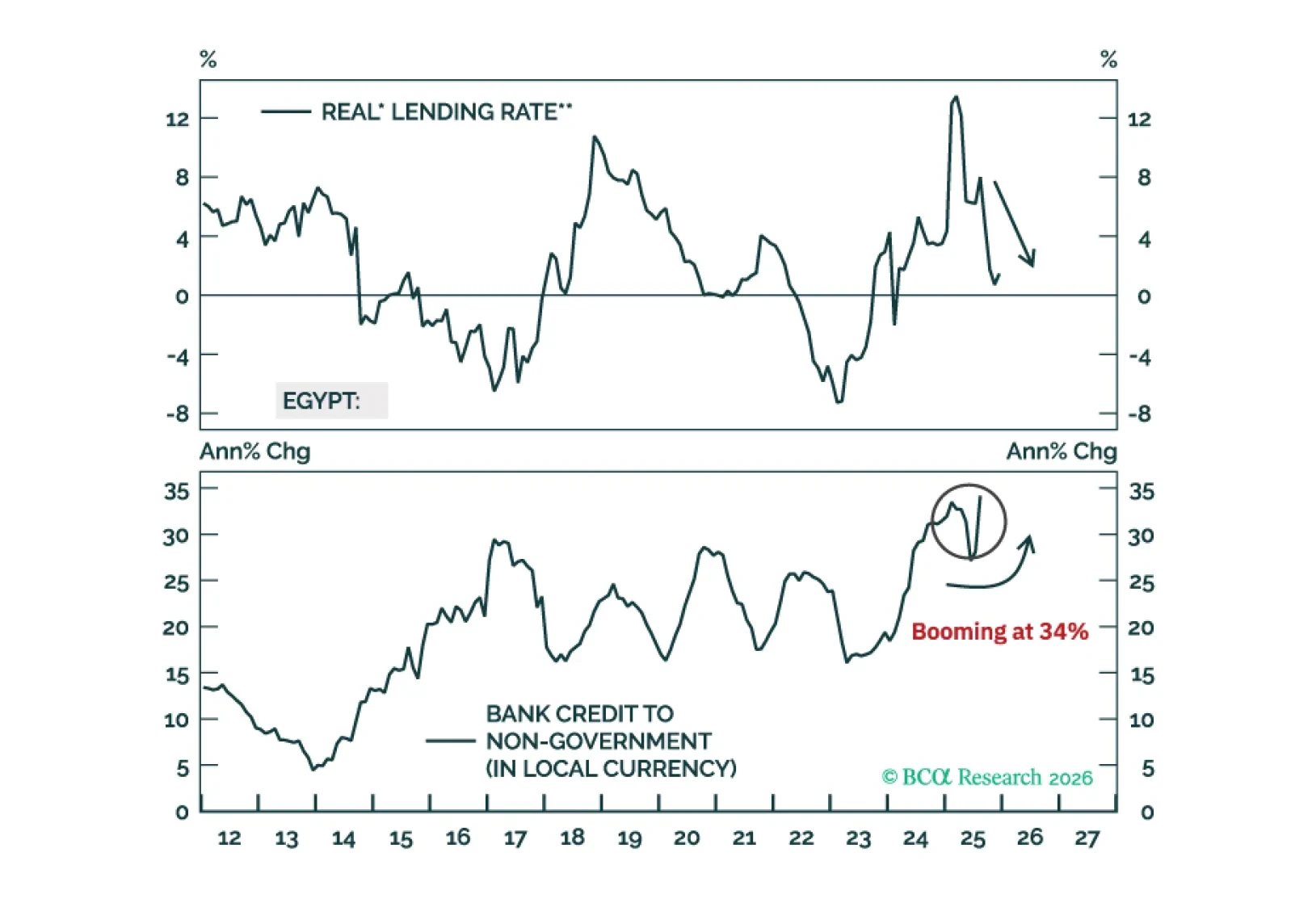

Egypt’s underlying inflation pressures are much higher than the headline CPI numbers imply. Real interest rates have plunged. As such, domestic bond yields have stayed high for a reason. Steer clear.

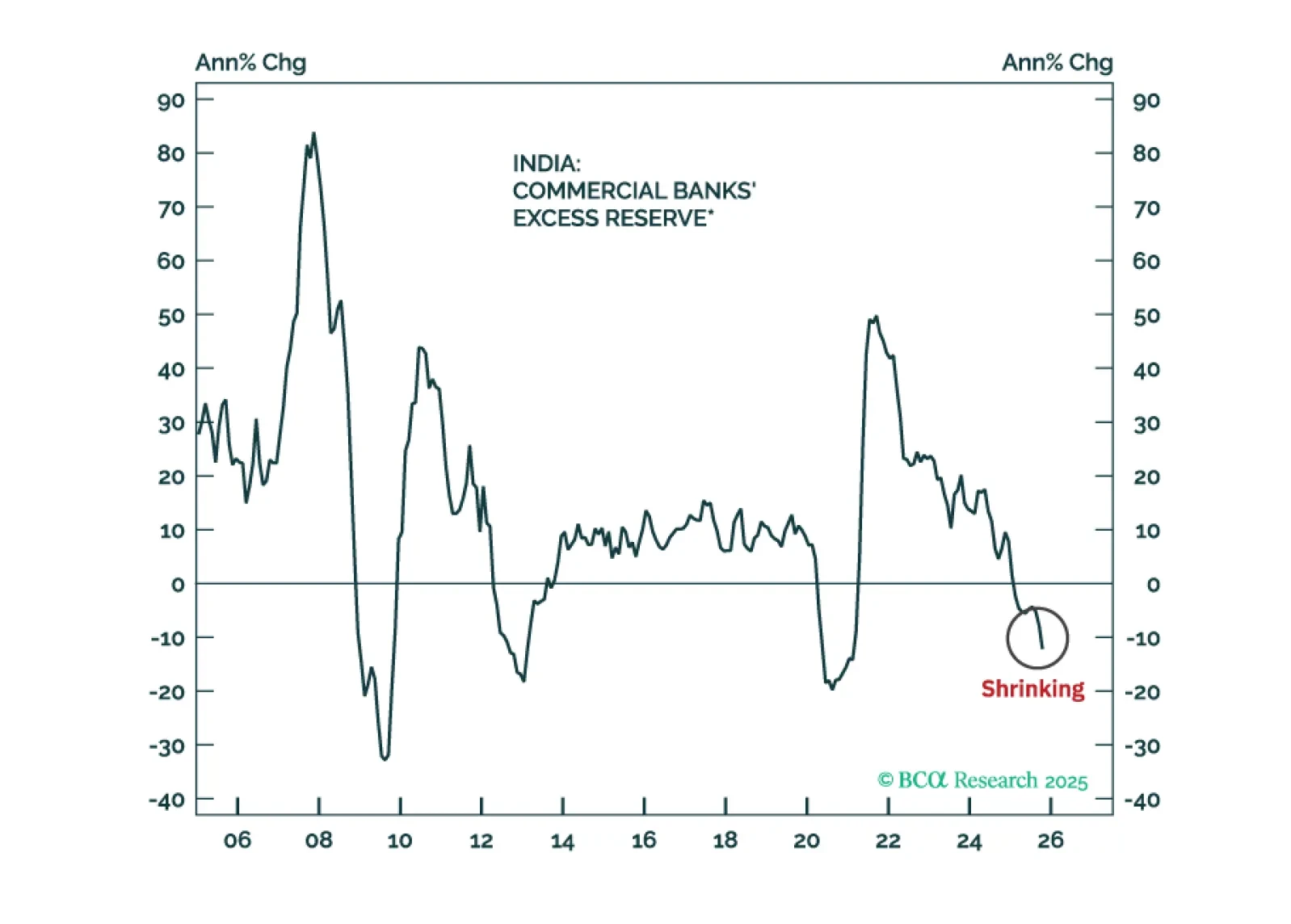

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.