Government

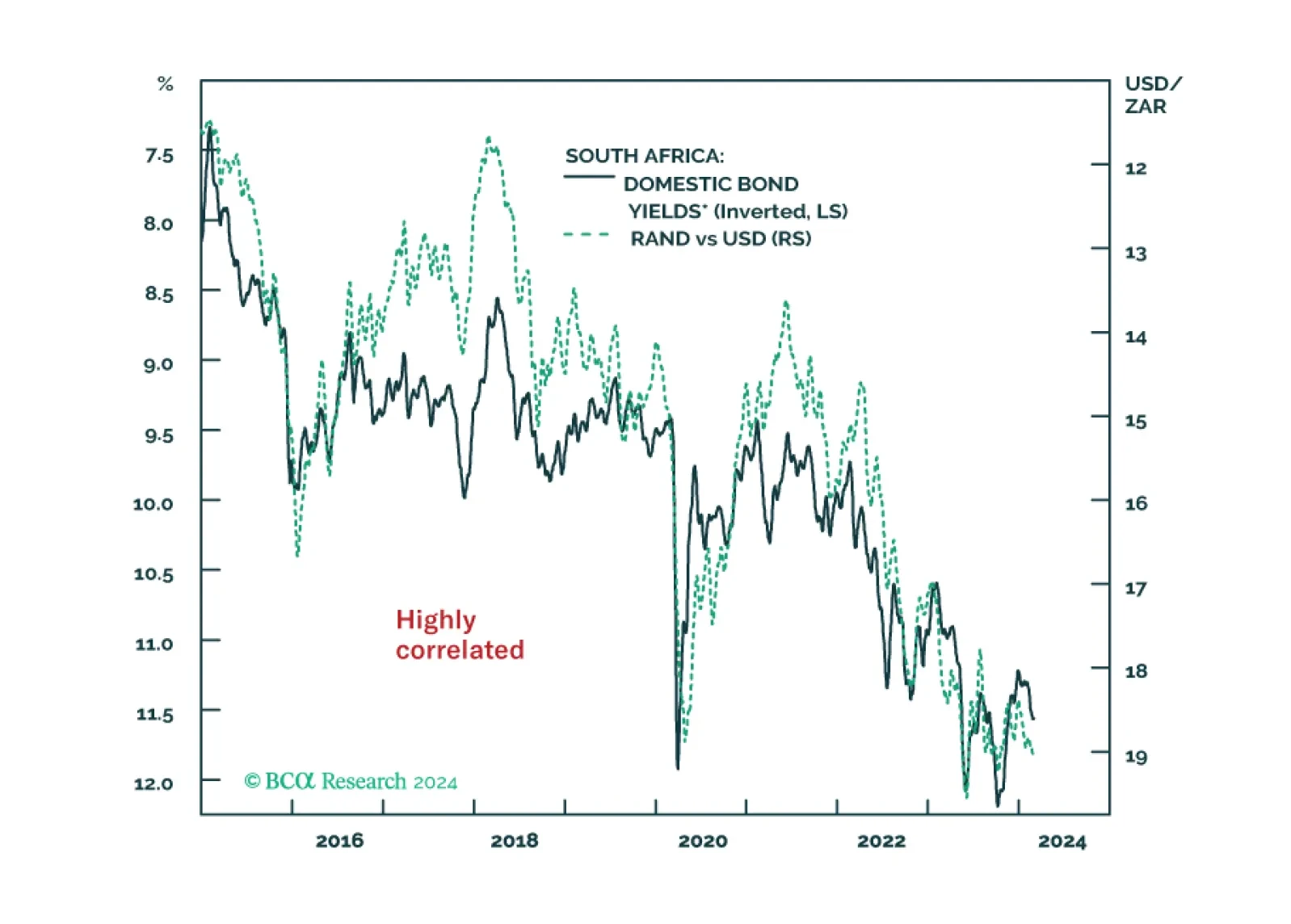

Despite the economy being on the verge of a recession, the South African Reserve Bank will not ease policy meaningfully. Doing so will accentuate the currency depreciation, which, in turn, will push up bond yields – an outcome the central bank would like to prevent.

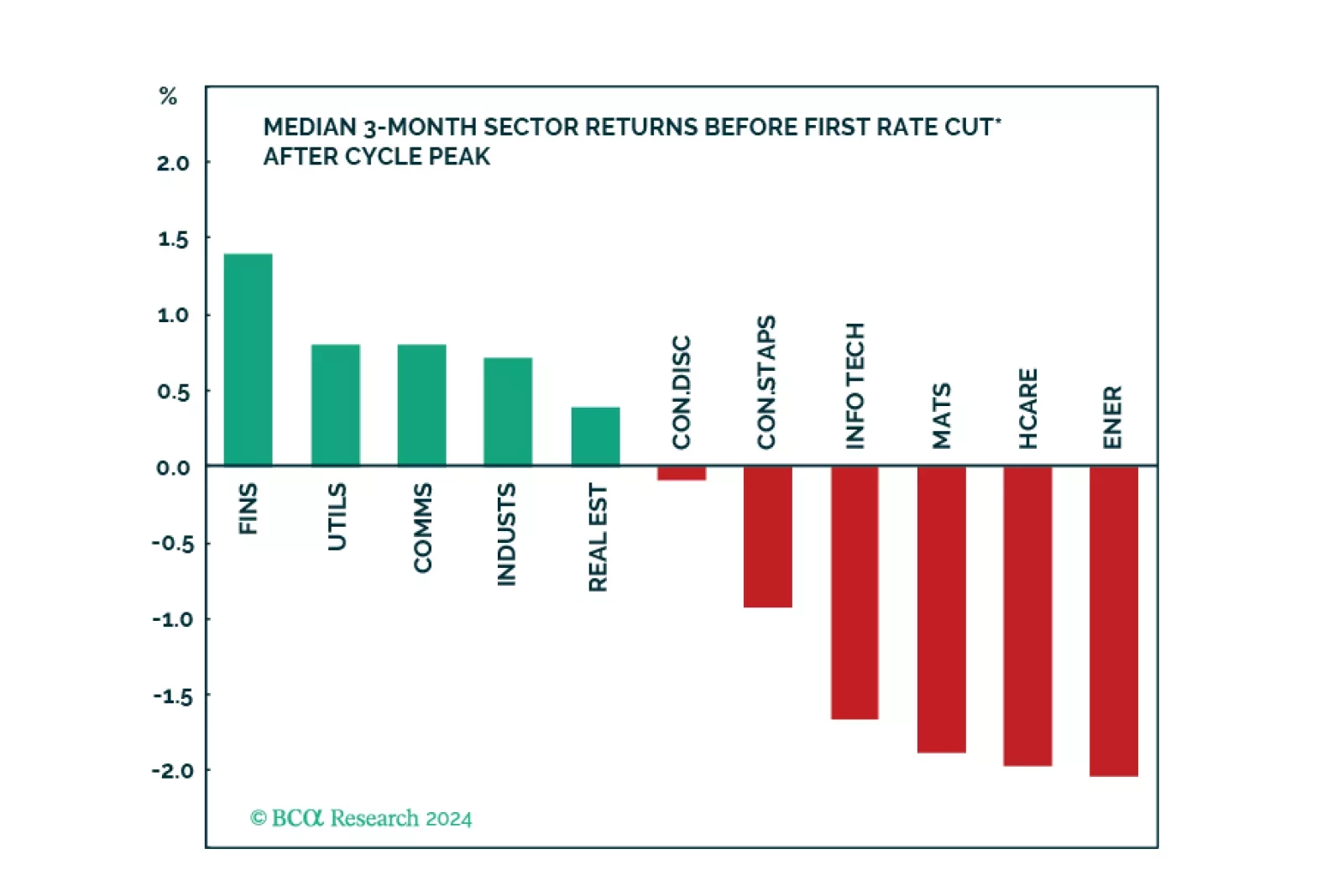

We created a sector selection scorecard based on performance of sectors under various macroeconomic regimes while taking into consideration revisions to expected earnings growth and valuations in a historical context. Our total sector selection scorecard suggests overweighting defensives such as Utilities, and Consumer Staples, and underweighting cyclicals such as Consumer Discretionary, Industrials, and Financials. Considering this analysis, we have adjusted our sector positioning accordingly.

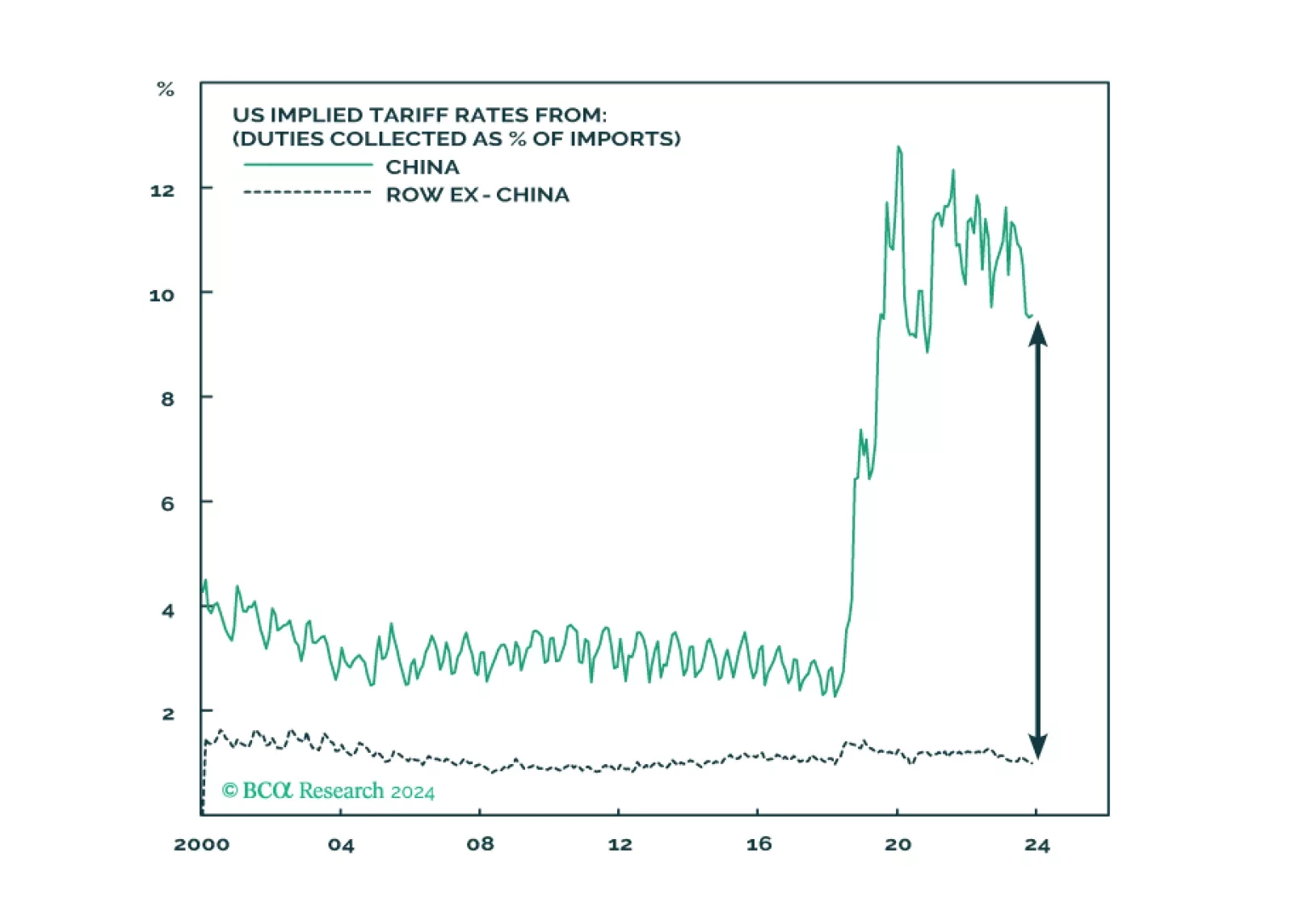

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.