Inflation/Deflation

Dear Client, We had an error in our oil balances/forecasts report from 18 November 2021 resulting from a double counting of select US onshore production figures. This has been corrected below. Highlights Higher oil production will restrain price increases in the short term, and give the impression the burst in inflation is transitory. Re-opening of airline travel and releasing of pent-up demand will absorb much of the higher output by year-end 2022. We are doubtful a US SPR release is forthcoming, as its impact would be trivial. Likewise, we do not expect the US to limit or ban exports of crude oil again, as it would unbalance markets. We are maintaining our Brent forecasts for 2022 and 2023 at $80 and $81/bbl. We again include a caveat, noting upside price risk is increasing going forward, due to inadequate capex (Chart of the Week). Stronger inflation prints going into 1Q22 will test the conviction underpinning central bankers' view that the current bout of price increases is transitory. If inflation appears to be more persistent going into 2H22, the Fed and other systemically important central banks likely will signal earlier-than-expected policy-rate hikes. This would be negative for commodities, as it would raise debt-service costs and investment hurdle rates, and reduce consumption. Higher oil prices and tighter monetary policy will temper demand. If capex is not forthcoming, however, prices will have to rise sharply to destroy demand. Feature It hardly deserves mention that the US has been hectoring the leadership of OPEC 2.0 to increase oil production, in order to reduce the cost of gasoline and home-heating fuels going into the winter … And, there's a mid-term election next year. The Biden administration also has been threatening – if that is the proper term – to release barrels from the US Strategic Petroleum Reserve (SPR), and reportedly asked China to consider a similar release.1 The leadership of OPEC 2.0, on the other hand, is flagging the risk to stronger oil prices from higher production next year. Much to the chagrin of the Biden administration, the coalition led by the Kingdom of Saudi Arabia (KSA) and Russia will not be increasing output by more than the 400k b/d it agreed to earlier this year. OPEC 2.0 will keep this up until June or July 2022, when most of its output sidelined by the COVID-19 pandemic will have been returned to the market. We expect the core Gulf-state producers – mostly KSA – will want to maintain ~ 3mm b/d of spare capacity thereafter. Chart of the WeekStable Oil-Price Trajectory

Stable Oil-Price Trajectory

Stable Oil-Price Trajectory

Chart 2OPEC 2.0 Production Continues To Lift

OPEC 2.0 Production Continues To Lift

OPEC 2.0 Production Continues To Lift

Higher Oil Output Expected Overall OPEC 2.0 production is expected to total 52.3mm b/d next year and 53.1mm b/d in 2023 (Chart 2). Most of the increase in the coalition's production will be accounted for by its core producers – KSA, Russia, Iraq, the UAE and Kuwait (Table 1). The "Other Guys" – i.e., those producers in OPEC 2.0 that can only maintain existing output levels or are managing continual declines in output – will account for a decreasing share of the coalition's production (Chart 3).2

Chart 3

Table 1BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances) To Dec23

High Oil Prices, Low Capex, Inflation … Oh, My.

High Oil Prices, Low Capex, Inflation … Oh, My.

Including drilled-but-uncompleted wells (DUCs), we expect an additional 600k b/d from US shale-oil producers next year, which would take their output up to 8.39mm b/d, and another 350k b/d increase in their output in 2023. Output in the Lower 48 (L48) states of the US overall is expected to increase to 9.65mm b/d next year and 9.93mm b/d in 2023 (Chart 4). The increase in L48 output will continue to be led by higher shale-oil production, notably from the prolific Permian Basin play (Chart 5). US Gulf of Mexico and Alaska production tops up our total average output forecasts in the States to 11.89mm b/d next year and 12.20mm b/d in 2023. Chart 4US L48 Production Continues To Grow

US L48 Production Continues To Grow

US L48 Production Continues To Grow

Chart 5

Demand Continues To Expand On the demand side, we continue to expect 2021 consumption growth of ~ 5.0mm b/d this year. Our growth expectation for 2022 and 2023 remains close to ~ 4.6mm b/d and 1.3mm b/d, respectively. We also expect demand to cross back over 100mm b/d in the current quarter, as can be seen in Table 1. As has been our wont during the recovery from the pandemic, we expect DM demand to level off next year after a stout recovery, and for EM demand to pick up the baton and lead global oil-consumption growth in the next two years (Chart 6). We remain bullish re the rollout of COVID-19 vaccines using mRNA technology globally, which will allow EM economies to step up growth. Re-opening of DM and EM economies will continue, pushing refined-product demand above 2019 levels next year, including jet-fuel toward the end of 2H22. Chart 6EM Oil Demand Growth Will Take The Lead

EM Oil Demand Growth Will Take The Lead

EM Oil Demand Growth Will Take The Lead

Oil Market Remains Balanced Our supply-demand balances are largely unchanged from last month. This keeps global crude-oil markets in a physical deficit for most of next year. We expect OPEC 2.0's core producers will maintain their production-management strategy – i.e., keeping the level of supply below the level of demand. Producers in the price-taking cohort outside the coalition – chiefly the US, Canada and Brazil – will lift production subject to capital-market constraints on producing oil profitably (Chart 7). This supply-demand dynamic keeps inventories drawing through this year, then leveling off in 2022 and rebounding slowly in 2023 (Chart 8). Chart 7Global Crude Markets Mostly Balanced

Global Crude Markets Mostly Balanced

Global Crude Markets Mostly Balanced

Chart 8Crude Inventories Continue To Draw

Crude Inventories Continue To Draw

Crude Inventories Continue To Draw

Global crude-oil inventories could come under pressure during the 2021-22 winter, if natural-gas markets remain supply-constrained. This week, the Russian state-owned supplier and operator of Nord Stream 2 (NS2) pipeline delivering Russian gas to Germany was told it must comply with German law before its gas will be allowed to flow. It is unlikely this will be done this year.3 This could keep demand for oil higher at the margin, as we noted earlier.4 Oil's Known Unknowns: Capex, Inflation The big unknowns – and risks – to our view are when and how much capex is going to be deployed in the oil and gas exploration-and-production space, and what we can expect from the Fed and other systematically important central banks if inflation looks to be persistent. OPEC 2.0 leaders and officials from the price-taking cohort agree that the dearth of capex for the industry threatens to destabilize oil and gas markets in the near future. Among the 90 international oil and gas producers tracked quarterly by the US EIA capex has collapsed (Chart 9). The industry appears to have made shareholder and investor interests their priority, so as to be competitive in the pursuit of capital that all firms engage in. This also is true for state-owned entities, which also compete for capital and access to technology.

Chart 9

These firms and producers will continue to work to produce oil and gas profitably. Still, they likely will continue to find an unreceptive audience to invest in these energy sources; Governments and policymakers are actively discouraging investment in fossil fuels. This risks setting in motion a process in which supply erodes much faster than demand – similar to what is happening in coal markets presently – and prices for fossil fuels rocket higher. This is not a strategy, particularly as it disregards the fact there is insufficient renewables capacity and storage to cover the energy from hydrocarbons that is being lost because of the lack of a transition policy at any level. Recent strong inflation prints are a small-scale example of how this process could play out over the next decade or longer. When China eliminated Australian coal imports earlier this year in favor of Indonesian supplies, and forced its coal mines to shut as part of its dual-circulation policy to become more self-reliant, the resulting shortages set off chain reactions in global natural gas markets. European gas prices shot higher, which, along with higher Asian and American natgas prices, sent food prices soaring on the back of higher fertilizer prices.5 Shipping bottlenecks and container shortages worldwide exacerbated these problems. CBs' Inflation View Challenged Going into 2022, central bankers' view that the current bout of price increases is transitory is going to be put to the test. If inflation appears to be more persistent going into 2H22 – after hoped-for one-offs in coal, gas, oil and food markets are worked out – the Fed and other systemically important central banks likely would start signaling earlier-than-expected policy-rate hikes. This would be negative for commodities generally, as it would raise debt-service costs and investment hurdle rates, and reduce consumption. Higher oil prices and tighter monetary policy will temper demand. These inflationary pressures can be addressed, but this will require a serious re-thinking of the strategy the world needs to pursue if it is to pull off a successful energy transition. Such a strategy will have to give greater consideration to the role of fossil fuels in this transition. If capex is not forthcoming, however, oil prices will have to rise to destroy demand. This will feed into inflation, and ultimately could result in stagflation, as economic growth grinds lower. Investment Implications The level of uncertainty surrounding oil and gas prices remains elevated, given the background condition of 90% odds we see a La Niña in the Northern Hemisphere's winter (Nov21 – Mar22), and ~ 50% chance it persists into the Spring (March-May22). This could leave markets with colder-than-normal temperatures past the end of winter, as it did last year. Given this uncertainty, we remain long the S&P GSCI and the COMT ETF, to keep our exposure to higher prices and a return to higher backwardation. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Paula Struk Research Associate Commodity & Energy Strategy paula.struk@bcaresearch.com Commodities Round-Up Energy: Bullish Natural-gas price volatility in Europe and the EU exploded higher once again, following reports the German government would not certify Nord Stream 2 (NS2) unless and until it complies with German law (Chart 10). The European Commission also is setting conditions for its approval. Lastly, outgoing Chancellor Angela Merkel said further sanctions against Russia were possible if the pipeline was used against Ukrainian interests.6 The EU's TTF natural gas benchmark is up 24% this week alone, on the back of this news, while the UK's benchmark Balancing Point index is up 7%. These higher costs will feed into food costs, given the importance of natural gas to fertilizer markets, accounting for ~ 70% of fertilizer costs.7 Given the higher likelihood of another La Niña in the Northern Hemisphere (90% odds from the US Climate Prediction Center), we expect continued volatility in gas prices. Base Metals: Bullish Steel demand in China has been contracting after the government began tightening the supply of credit to the property sector following the Evergrande debt crisis. Construction makes up approximately one-fourth of total Chinese steel demand. At the same time, supply has been falling as, in addition to government regulation to curb carbon emissions, steel mills have voluntarily cut output due to decreasing margins on the back of soft demand. The fact that Chinese steel prices have been falling since their highs in May this year indicates that demand is dropping faster than supply (Chart 11). Reduced Chinese steel demand is feeding through to demand for iron ore – the main steel input in China – while disruptions in the top two iron ore exporters, Australia and Brazil are easing, increasing the possibility of an oversupplied market. Precious Metals: Bullish Gold ended last Thursday above $1,860/oz for the first time since mid-June after the October CPI data release showed that the US had its biggest inflation surge in nearly 30 years. As long as the Federal Reserve does not turn more hawkish, consecutive months of high CPI prints will mean low real rates well into 2022, which will reduce the opportunity cost of holding gold. The high US twin deficits – which as of Q3 2021 was 17.44% of GDP – support the long-term dollar bearish view our colleagues at BCA's Foreign Exchange Strategy hold. A weak dollar over the next 12-18 months will increase the inflation-hedge appeal of the yellow metal relative to the greenback.

Chart 10

Chart 11

GENERIC 1ST MONTH STEEL REBAR FUTURES PRICE LEVEL GOING DOWN

GENERIC 1ST MONTH STEEL REBAR FUTURES PRICE LEVEL GOING DOWN

Footnotes 1 We note in passing the Biden administration has been mostly successful in getting massive fiscal and monetary stimulus deployed into the US economy, which has increased household savings and potential spending power dramatically, as our colleagues in BCA's US Investment Strategy noted in their 1 November 2021 report Half-Empty Or Half-Full?: "Massive fiscal transfers and an unprecedented increase in household wealth will support consumption and keep the economy from stagnating." We cannot view higher gasoline prices in the wake of this stimulus and growth as an economic emergency of the sort the SPR is designed to address. Nor can we view the pick-up in mobility – particularly in air travel expected shortly with the re-opening of routes closed due to the pandemic – as a supply-side emergency. 2 It's worthwhile mentioning here that OPEC 2.0 has been returning less than the 400k b/d every month it agreed due to shortfalls in production outside the core group broken out in Table 1. Reduced capex and maintenance is responsible for this. Higher oil prices might allow this group within the coalition to attract additional capex, but, given the uncertain long-term support for such exploration-production-maintenance investment, this will remain a long-term challenge to these producers. Lastly, we continue to expect Iran to return to markets as a bona fide exporter; we expect its production to return to 3.70-3.85mm b/d by 2H22. 3 Please see Nord Stream 2: Germany halts approval of Russian gas link published on November 16, 2021. 4 Please see last month's oil balances and price-forecast report Short-Term Oil-Price Risk Moves To The Downside, published 21 October 2021. 5 Please see our October 14, 2021 report entitled Inflation Surges, Slows, Then Grinds Higher, and last week's report entitled Risk Of Persistent Food-Price Inflation for additional discussion. 6 Please see fn 3 above. 7 Please see fn 5 above. Investment Views and Themes Strategic Recommendations

Highlights China’s slowdown will deepen, and US bond yields will likely rise. This augurs well for the US dollar but will produce a toxic cocktail for EM. The recent weakness in the commodity complex will continue. EM markets are at risk in absolute terms and will continue to underperform their DM counterparts. From a global macro perspective, the US dollar’s appreciation will be a re-balancing act. In a world where China is exporting economic weakness/deflation and the US is experiencing genuine inflation, a strong US dollar is desirable. The latter will redistribute inflation away from the US to the rest of the world and will redirect disinflationary pressures from the rest of the world to the US. Feature Chart 1DXY Breakout, EM FX Breakdown

DXY Breakout, EM FX Breakdown

DXY Breakout, EM FX Breakdown

The US dollar is breaking out and EM currencies are breaking down (Chart 1). This will set in motion a number of responses in global financial markets. These include but are not limited to selloffs in EM equities, domestic bonds and EM credit markets and a setback in the commodity complex. Hence, we reiterate our negative stance on EM stocks and fixed-income markets. We continue to recommend shorting a basket of EM currencies versus the US dollar. Please refer to the end of this report for detailed investment recommendations. Why The Greenback Is Set To Strengthen Since early in the year, our investment strategy has been based on two macro themes: China’s slowdown and rising US inflation. We concluded early on that these dynamics are positive for the US dollar. Both macro themes have played out fairly well, yet until recently the broad trade-weighted US dollar’s advance has been hesitant. Odds are that the rally in the greenback is about to accelerate. Chart 2China's Slowdown = US Dollar Rally

China's Slowdown = US Dollar Rally

China's Slowdown = US Dollar Rally

The fundamental case for the US dollar rally remains as follows: China’s slowdown will weigh more on emerging Asia, Japan, Europe, and/or commodity producing, developing and developed economies than it will on the US. The basis is that US exports to China make up only 0.7% of its GDP. The same ratio is much higher for the rest of the world. Hence, the US economy will outperform many advanced and emerging economies. Chart 2 illustrates that, historically, whenever China has slowed down, the US dollar has rallied. The mainland’s property construction is shrinking, and traditional infrastructure investment is also extremely weak (Chart 3). Beijing is easing its regulatory and macro policies but only by degrees. For now, policy support will be insufficient to reverse the business cycle downturn. In the meantime, the US economy is overheating. Specifically, all core type inflation measures have surged to well above 2% (Chart 4). Critically, nominal wages are rising at the fastest rate seen in the past 35 years (Chart 5). Chart 3China: Infrastructure Investment Is Very Weak

China: Infrastructure Investment Is Very Weak

China: Infrastructure Investment Is Very Weak

Chart 4US Core Inflation Is Broad-Based And High

US Core Inflation Is Broad-Based And High

US Core Inflation Is Broad-Based And High

Given that the employee quit rate is very high, employers will have to grant notable wage increases to both new and current employees. Thus, wage growth will accelerate further. Recent wage gains have not been offset by productivity growth. As a result, unit labor costs are rising (Chart 6). This will push businesses to raise their selling prices. So long as household income and consumption remain robust, businesses will likely succeed in raising their prices. In short, US inflation is acute and genuine, and, hence, it will persist unless the economy slows considerably. Chart 5US Nominal Wage Growth Is At Its Fastest In 35 Years

US Nominal Wage Growth Is At Its Fastest In 35 Years

US Nominal Wage Growth Is At Its Fastest In 35 Years

Chart 6US Unit Labor Costs Are Rising Fast

US Unit Labor Costs Are Rising Fast

US Unit Labor Costs Are Rising Fast

The rise in US inflation will initially be bullish for the US dollar. The reason is that fixed-income markets will move to price in higher Fed funds rates and the Fed will also acknowledge the need to hike rates given that core inflation is well above its target range. At some point in future, however, high inflation will start hurting the US dollar. This will happen when the Fed eschews rate hikes and falls behind the inflation curve. We believe we are still in a window where US bond yields could rise further. Rising US interest rates will support the dollar. Finally, the US economy, but not necessarily its equity and credit markets, is better positioned to handle central bank tightening than are other DM and EM economies. American consumers have substantially deleveraged and there are shortages in US housing and cars. Even as US borrowing costs rise, interest rate sensitive sectors like housing and autos will still do well because of pent-up demand. In particular, the US housing market is sensitive to long-term (30-year) mortgage rates and not the front end of curve. On the contrary, many EM and other DM economies and their housing sectors are sensitive to domestic short-term rates. In percentage terms, the rise in US mortgage rates will likely be smaller than those in DM and EM economies. In short, the US economy will not slow sharply in the response to rates while EM and other DM economies will. This augurs well for the dollar. The key US vulnerability from higher interest rates stems from its equity and credit markets, not the real economy. US equities and credit markets are very richly priced, so the rising cost of capital could trigger a major selloff. In turn, wealth effects and tightening financial conditions will pose a risk to the real economy. However, even in this case, the US dollar will initially appreciate because it always rallies during risk-off phases. The greenback’s depreciation will resume when the Fed turns dovish again. From a big picture macro perspective, the US dollar’s appreciation will be a re-balancing act. In a world where China is exporting economic weakness/deflation and the US is experiencing genuine inflation, a strong US dollar is desirable. The latter will redistribute inflation away from the US to the rest of the world and will redirect disinflationary pressures from the rest of the world to the US. In this period of US dollar strength, EM financial markets will be hurt because foreign investors always flee EM when their currencies depreciate. Bottom Line: China’s slowdown will deepen, and US bond yields will likely rise. This will produce a toxic cocktail for EM. Watch Out Commodity Prices Chart 7Reduced Financing For Property Developers = Less Construction

Reduced Financing For Property Developers = Less Construction

Reduced Financing For Property Developers = Less Construction

The downturns in China’s property construction and traditional infrastructure spending are bad for raw material prices. The following points offer an explanation as to why commodity prices will relapse in spite of the fact that they have thus far resisted China’s slowdown. Although Chinese property sales and starts have been shrinking, floor area completed (construction work) has been very strong. However, the liquidity crunch that many real estate developers are experiencing will lead them to halt or cut back on their construction work (Chart 7, top panel). The latter will weigh on raw material prices (Chart 7, bottom panel). Taiwan’s new export orders PMI for the basic materials sector has dropped below 50, indicating plunging regional demand for raw materials (Chart 8). Ongoing weakness in Chinese demand is the culprit behind this drop. Due to electricity shortages, mainland production of industrial metals has plunged (Chart 9, top panel). Yet, the prices of these metals have recently corrected (Chart 9, bottom panel). Falling prices amid shrinking supply are a sign of major demand relapse. Chart 8Greater China: Orders For Basic Materials Are Already Shrinking

Greater China: Orders For Basic Materials Are Already Shrinking

Greater China: Orders For Basic Materials Are Already Shrinking

Chart 9Base Metal Price Falling Despite Production Shutdowns In China

Base Metal Price Falling Despite Production Shutdowns In China

Base Metal Price Falling Despite Production Shutdowns In China

The Baltic Dry index – the price of shipping bulk commodities – has rolled over decisively. It has reasonable correlation with industrial metal prices. Oil is much less exposed than base metals to China’s property and infrastructure contraction. In the case of crude, the key risks are the US and China releasing their strategic reserves and the US dollar strength. Bottom Line: The recent weakness in the commodity complex will continue. Other Considerations Chart 10China's Onshore Stock-to_Bond Ratio Is Breaking Down

China's Onshore Stock-to_Bond Ratio Is Breaking Down

China's Onshore Stock-to_Bond Ratio Is Breaking Down

There are a number of other considerations and indicators that lead us to maintain a negative stance on EM financial markets: China’s onshore stock-to-bond ratio has broken below its 200-day moving average (Chart 10). This signifies a deepening growth slump in China. EM equity underperformance has been broad-based. Both the market cap-weighted and equal-weighted EM equity indexes have been underperforming their respective DM indexes. Further, not only have TMT (technology, media and telecom) stocks been underperforming their DM peers, but non-TMT stocks have also lagged their counterparts substantially (Chart 11). Last but not least, EM TMT stocks remain at risk. First, share prices of Chinese internet companies will continue derating due to structurally lower profitability going forward as the government exercises more control over them. We have discussed this in previous reports. In addition, consumer spending online has slowed sharply while smartphone sales are plunging (Chart 12). Chart 11EM Equity Underperformance Is Broad-Based

EM Equity Underperformance Is Broad-Based

EM Equity Underperformance Is Broad-Based

Chart 12China: Online Spending Is Very Weak

China: Online Spending Is Very Weak

China: Online Spending Is Very Weak

Second, DRAM (memory chip) prices are deflating and the value of DRAM sales is shrinking (Chart 13). This is weighing on Korean semiconductor share prices like Samsung and SK Hynix. These stocks have a large market cap in the KOSPI index. Finally, demand for semiconductors produced by Taiwanese companies has been booming but it is presently showing signs of moderation (Chart 14). Chart 13Falling DRAM Prices Are Weighing On Korean Semi Stocks

Falling DRAM Prices Are Weighing On Korean Semi Stocks

Falling DRAM Prices Are Weighing On Korean Semi Stocks

Chart 14Taiwanese Semiconductor Industry: Moderating Orders

Taiwanese Semiconductor Industry: Moderating Orders

Taiwanese Semiconductor Industry: Moderating Orders

Importantly, geopolitical risks around Taiwan in general and TSMC in particularly are enormous. The latter is literally at the center of the US-China confrontation. The timing of a diplomatic or even military crisis is uncertain but our Geopolitical Strategy team expects geopolitical risks over Taiwan to escalate substantially. The recent summit between Presidents Joe Biden and Xi Jinping does not change this assessment. Investment Recommendations Chart 15EM Credit Markets: Prepare For A Broad Selloff

EM Credit Markets: Prepare For A Broad Selloff

EM Credit Markets: Prepare For A Broad Selloff

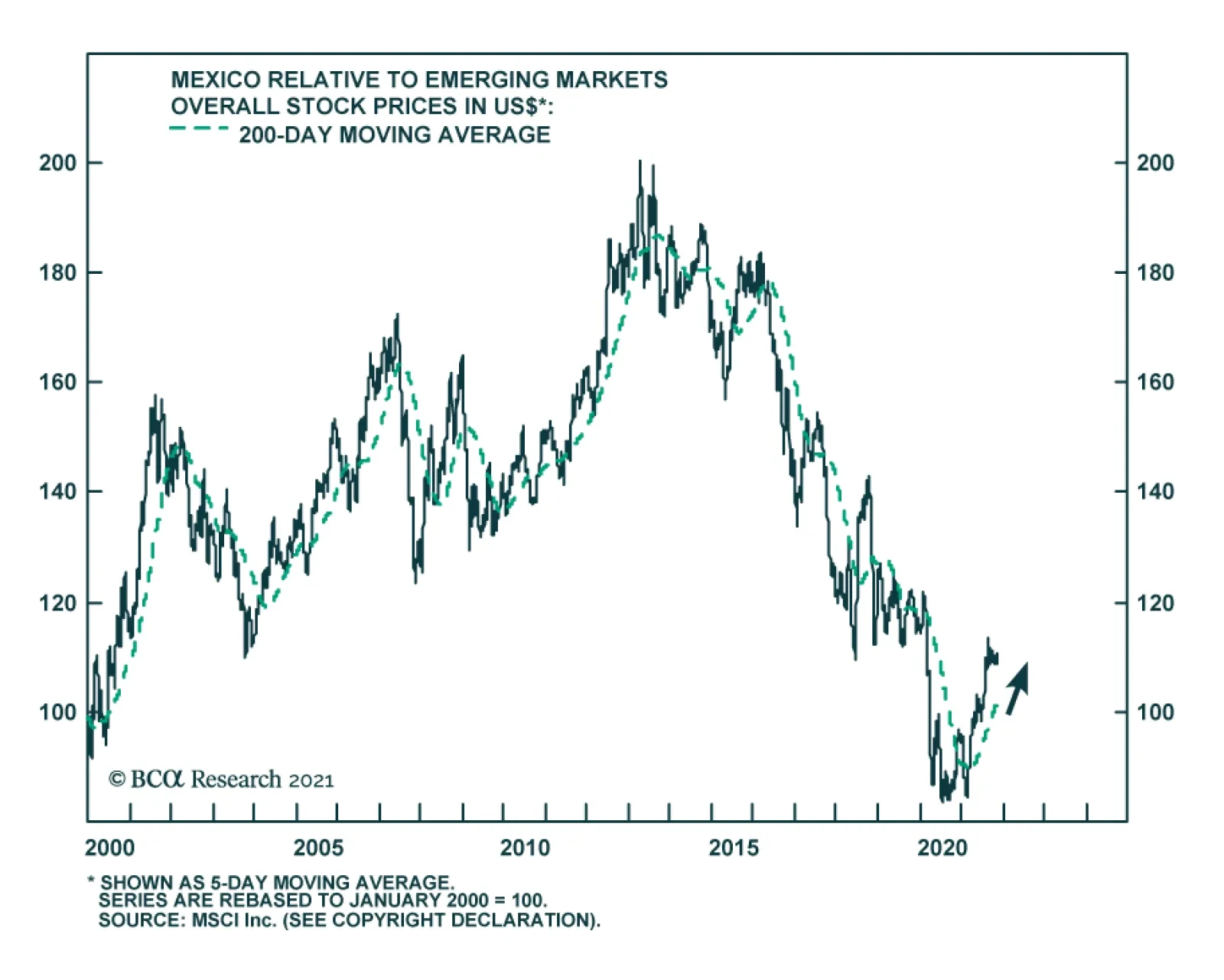

Continue underweighting EM equities in a global equity portfolio. Within the EM space, our overweights are Korea, Singapore, China (favoring A shares over investable stocks), Vietnam, Russia, central Europe and Mexico. Concerning EM equity sectors, we reiterate the short EM banks / long DM banks and short EM banks / long EM consumer staples positions. In line with our US dollar breakout thesis, we continue to recommend a short position in a basket of the following EM currencies versus the US dollar: BRL, CLP, COP, PEN, ZAR, TRY, THB, PHP and KRW. EM exchange rate depreciation is bad for EM domestic bonds. Currency weakness could lead central banks in Latin America to hike rates further. In brief, the risk-reward of EM local currency bonds is still unattractive. In this space, we recommend the following positions: bet on yield curve flattening in Mexico and Russia (pay 1-year/receive 10-year swap rates); pay Czech 10-year swap rates; receive Chinese and Malaysian 10-year swap rates. We reiterate our underweight in EM credit (both sovereign and corporate) markets versus US corporate credit, quality adjusted. As EM exchange rates depreciate, EM credit spreads will widen (Chart 15). Chinese high-yield corporate US dollar bonds are not yet a buy because the mainland property market’s travails are far from over, as was discussed in our recent Special Report. For a complete list of our recommendations across all asset classes and country strategy within each asset class, please see below or visit our web site. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Dear Client, The next two BCA Research Global Fixed Income Strategy reports will be jointly published with other BCA services, which will impact the publishing dates. Our next report will be a joint Special Report on Australia, published with our colleagues at Foreign Exchange Strategy, which you will receive this Friday, November 19. The following report will be a joint Special Report published with European Investment Strategy, which you will receive on November 29. -Rob Robis Highlights High realized inflation rates are pushing up longer-term inflation expectations toward all-time highs, while also weighing on consumer confidence, in the US and the UK. The inflation overshoot has not been as severe in the euro area, but consumer confidence appears to be rolling over there too. Over the next year, central banks will have to manage around the communications challenges posed by a rise in inflation that is perceived to be more supply-driven than demand-driven and, hence, beyond the full control of monetary policy. Public opinion surveys are showing eroding satisfaction with the Fed and Bank of England, while similar surveys in the euro area show public trust in the ECB remains strong despite higher euro area inflation. We continue to favor overweights in euro area government bonds (both core and periphery) versus US Treasuries and UK Gilts, given the far greater likelihood of multiple rate hikes in the UK and US in 2022/23, compared to the euro area, in order to restore central bank credibility. Feature Rapidly accelerating inflation has become front-page news around the world. It is also increasingly becoming a political issue and not just an economic one. After the release of the October US consumer price index (CPI) report, where headline inflation came in at a 30-year high of 6.2%, US President Joe Biden had to issue a formal White House statement acknowledging that inflation “hurts Americans’ pocketbooks, and reversing this trend is a top priority for me.” Biden also pulled off the neat trick of both committing to, and subtly challenging, the Fed’s independence when he noted that “I want to reemphasize my commitment to the independence of the Federal Reserve to monitor inflation, and take necessary steps to combat it.” The Great Inflation Of 2021 (and 2022?) has raised a new risk for both politicians and investors. As long as the high inflation persists, and for as long as central banks seem unwilling or unable to respond to try and bring down inflation with tighter monetary policy, consumer confidence will be negatively impacted – even if job growth remains reasonably healthy. Confidence & Inflation: A Matter Of Trust Chart of the WeekHigh Inflation Weighing On Consumer Confidence

High Inflation Weighing On Consumer Confidence

High Inflation Weighing On Consumer Confidence

The preliminary read on US consumer confidence for November from the University of Michigan survey showed sentiment hitting a ten-year low, largely on worries about the impact of rising inflation on household spending power. This effect of high inflation eroding consumer confidence is not just a US phenomenon (Chart of the Week). UK consumer sentiment is also falling due to what has been described as “a potential cost of living crisis” by consumer research firm GfK. In the euro area, however, consumer sentiment is still relatively elevated, but is starting to roll over as headline inflation reaches a 13-year high of 4.1% in October. From the point of view of financial markets, surging inflation is still expected to be a short-lived phenomenon, although conviction on that view is starting to wane. Market-based inflation expectations curves for the US, UK and euro area are all currently inverted, with shorter-maturity expectations above longer-maturity ones (Chart 2). Yet the upward momentum of those measures across all maturity points is showing little sign of ebbing, especially in the US. The 2-year TIPS breakeven rate now sits at a 16-year high of 3.51%, the 5-year breakeven is at an all-time high of 3.22%, while the 10-year breakeven of 2.77% is now just a single basis point below its all-time high reached in 2005. The story is similar in the UK, where RPI swap rates for the 2-year, 5-year and 10-year maturities are 5.3%, 4.8% and 4.3%, respectively – all hovering near all-time highs (as are breakevens on index-linked Gilts). Euro area inflation expectations are not so historically elevated, and the inflation curve is not as inverted, but the 2-year euro CPI swap rate is still at a 15-year high of 2.4% compared to a 9-year high of 2.0% - right at the ECB’s inflation target - for the 10-year CPI swap rate. In the US, the survey-based measures of inflation expectations are telling a similar story. The New York Fed’s Consumer Survey shows that median 3-year expectations are now at 4.2% with 1-year expectations even higher at 5.7% (Chart 3). Meanwhile, the early November read on inflation expectations from the University of Michigan survey showed that 1-year-ahead expectations climbed to a 13-year high of 4.9%, while the longer-term 5-10 year inflation expectations were unchanged from the October reading of 2.9%. Chart 2Rising Inflation Expectations, Both Short- & Long-Term

Rising Inflation Expectations, Both Short- & Long-Term

Rising Inflation Expectations, Both Short- & Long-Term

Chart 3A Broad-Based Surge In US Inflation

A Broad-Based Surge In US Inflation

A Broad-Based Surge In US Inflation

The latter figure may provide some comfort to the Fed, with surging shorter-term expectations not fully leaking through into longer-term expectations. However, the longer the inflation upturn persists, the more likely it will be that US consumers begin to factor in a higher rate of longer-term inflation, just as TIPS traders are doing. After all, the Michigan 5-10 year measure has still climbed by 0.7 percentage points from the pre-COVID low. Even more worrying from the Fed’s perspective is that inflation expectations are rising for essentially all Americans. The New York Fed Consumer Survey shows that 3-year-ahead inflation expectations are rising across all levels of education (Chart 4) and income cohorts (Chart 5). Chart 4US Inflation Expectations Are Rising For All Education Levels...

US Inflation Expectations Are Rising For All Education Levels...

US Inflation Expectations Are Rising For All Education Levels...

Chart 5...And Income Levels

...And Income Levels

...And Income Levels

The New York Fed also compiles a measure of consumer inflation uncertainty (bottom panels of both charts on page 5). Survey participants are asked to provide probabilities of inflation falling within certain ranges, with the gap between the top and bottom quartiles of those expected inflation outcomes representing the “uncertainty” over future US inflation. Perhaps unsurprisingly, the dispersion of inflation forecasts is typically much wider for those earning lower incomes and with less education. Yet even highly educated, high earning Americans are reporting wider gaps in possible inflation outcomes, in sharp contrast to the pre-COVID years where their expectations were low and stable. Americans Are Having Second Thoughts About The Fed Any way you cut it – TIPS breakevens or survey-based measures - US inflation uncertainty and volatility have increased. This appears to be starting to erode public confidence with the Fed. Along with its consumer confidence surveys, the University of Michigan also publishes a periodic survey of Confidence In Financial Institutions like commercial banks, asset managers and, most importantly, the Fed. The last survey was just conducted for the September/October 2021 period and showed that 43% of respondents reported a loss of confidence in the Fed compared to five years ago (Chart 6). That is up from 36% reporting a loss of confidence in the last such survey conducted in 2019, and is approaching the +50% levels seen in 2008 (the Financial Crisis) and in 2011 (the Taper Tantrum) – episodes where the Fed had difficulty maintaining economic and financial stability.

Chart 6

The University of Michigan also noted that reported consumer confidence was much lower for those claiming to have less confidence in the Fed, and vice versa (Chart 7).

Chart 7

Taken at face value, this survey shows that the Great Inflation of 2021 has shaken the public’s faith in the Fed’s ability to maintain economic stability. Combined with the message from the New York Fed Consumer Survey on the growing instability of American inflation expectations, this shows that the Fed may be facing an uphill climb to restore some of the credibility it has lost this year. Much like all aspects of American life these days, political partisanship must be factored in the analysis of US confidence data. The regular monthly University of Michigan sentiment survey for November noted that various measures of US confidence were consistently higher for respondents who reported to be Democrats compared to Republicans since President Biden took office (Chart 8). This is a mirror image of the years under President Trump (pre-pandemic), where Republicans consistently reported greater optimism than Democrats.

Chart 8

Chart 9Americans Can Agree On One Thing - High Inflation Is Bad

Americans Can Agree On One Thing - High Inflation Is Bad

Americans Can Agree On One Thing - High Inflation Is Bad

The University of Michigan Confidence in Financial Institutions survey also noted that less trust in the Fed was reported more frequently by Republicans (67%) than Democrats (27%) in 2021, the first year under Biden. This compares to 2017, the first year of the Trump Administration, where more Democrats (41%) reported less trust with the Fed compared to Republicans (30%). The Michigan survey described this “partisan identification” as being a “significant correlate of consumer assessments of the Federal Reserve, treating the Fed as part of the administration rather than an independent body.” Consumer confidence among reported Democrats has been falling since April of this year, although there is still room to catch up to the complete collapse of sentiment seen among Republican consumers (Chart 9, top panel). High US inflation is hitting everyone hard. The surge in inflation expectations is overwhelming income expectations for the next year, according to the New York Fed Consumer Survey (middle panel). High realized inflation has also eroded real spending power, with real average hourly earnings having contracted in year-over-year terms since April of this year (bottom panel). Even with that fall in real income growth perceptions, the plunge in the University of Michigan US consumer confidence has not been matched by other measures like the Conference Board US consumer confidence index, which remains well above pandemic era lows. Even more importantly, US consumer spending has held up well, with nominal retail sales expanding by +1.7% in October following a +0.8% gain in September. Some of those increases were due to rising prices, but were still significantly above inflation in both months, suggesting a solid pace of real consumer spending (the headline US CPI index rose +0.9% and +0.4% in October and September, respectively). For the Fed, the case is building to begin preparing Americans for higher interest rates in 2022. This is true both from an economic perspective – the US economy is likely to continue growing above trend next year, further tightening the US labor market – and in response to the high inflation that has caused some damage to the Fed’s credibility. What About The UK And Euro Area? Looking across the Atlantic, survey-based measures of inflation expectations have also climbed steadily higher (Chart 10). The YouGov/Citigroup survey of UK consumer inflation expectations is now at 4.4% for the 1-year-ahead measure and 3.7% for the longer-run 5-10 year ahead measure, both well above the BoE’s 2% inflation target. The European Commission surveys show a rapidly rising share of European Union businesses and consumers expect higher prices in the coming months. Yet while inflation expectations are rising in both the UK and Europe, only the UK shows the sort of deterioration in central bank confidence that is evident in the US. 48% of Europeans expressed confidence in the ECB, according to the Eurobarometer public opinion surveys – the highest share since 2007 and well above the 36% level seen after the Global Financial Crisis and European Debt Crisis (Chart 11). Some of that improvement in perceptions of the ECB mirrors better sentiment over the euro currency itself, as evidenced by that fact that both Germans and Italians now express similar levels of ECB confidence. Chart 10High Inflation Is Also A Problem Outside The US

High Inflation Is Also A Problem Outside The US

High Inflation Is Also A Problem Outside The US

Chart 11Europeans Have Not Lost Confidence In The ECB

Europeans Have Not Lost Confidence In The ECB

Europeans Have Not Lost Confidence In The ECB

High levels of public trust in the ECB play an important role in anchoring European inflation expectations. The ECB introduced its own Consumer Expectations Survey as a pilot project last year, and the latest reading from October 2021 shows that 1-year-ahead inflation expectations are now at 3% and 3-year-ahead expectations are at 2%. Both measures were at 2% a year earlier, and have generally stayed close to ECB’s 2% inflation target since the survey began. Chart 12High Inflation Is Worsening Public Satisfaction With The BoE

High Inflation Is Worsening Public Satisfaction With The BoE

High Inflation Is Worsening Public Satisfaction With The BoE

A recent research report from the Bank of Finland concluded that European consumers who have high trust in the ECB adjust their medium-term inflation expectations more slowly than those with low trust. The high public confidence in the ECB seen in the Eurobarometer surveys, combined with the stability of medium-term inflation expectations (both survey-based and market-based) around the ECB’s 2% target – even with realized euro area inflation now at 3.4% - fits with the conclusions of that report. We read this as a sign that the ECB is not under the same growing pressure to tighten policy in the face of rising inflation as the Fed, which is facing an erosion of public confidence that is showing up in steadily rising inflation expectations. In the UK, the Bank of England (BoE) is facing a situation more akin to that of the Fed. The BoE’s Inflation Attitudes Survey has been showing a steady erosion of UK consumers reporting satisfaction with how the BoE has been setting policy to fight inflation (Chart 12). The “net satisfied” index fell to +18% in the last survey published in September – similarly low levels of BoE satisfaction coincided with major spikes in longer-term UK inflation expectations in 2008 and 2011 (bottom panel). Our conclusion from the UK consumer surveys, along with measures of inflation expectations that are well above the BoE medium-term target, is similar to that in the US. The UK public is losing faith in the BoE’s ability, or willingness, to tackle the high inflation “problem” – even if much of the inflation is caused by high energy prices and global supply chain disruptions that are beyond the immediate control of monetary policy. The BoE will likely need to follow through on the rate hikes markets expect in 2022 to help restore public trust and credibility, even if realized inflation slows from current elevated levels. This is especially true after the debacle of the November 4 BoE meeting where a widely-signaled rate hike did not occur. If the BoE continues to delay the start of tightening while inflation expectations are accelerating, this will only put more pressure on the central bank to tighten faster, and by more than expected, in a bid to stabilize inflation expectations. Investment Conclusions Chart 13Favor European Government Bonds Over US & UK Equivalents

Favor European Government Bonds Over US & UK Equivalents

Favor European Government Bonds Over US & UK Equivalents

Our read of the various surveys shows that public trust in central banks has deteriorated in the US and UK, but not in Europe, because of surging inflation in 2021. This compounds the existing trends of tightening labor markets and accelerating wage growth in the US and UK that are more traditional reasons to tighten monetary policy. We continue to favor strategic overweights in euro area government bonds (both core and periphery) versus US Treasuries and UK Gilts, given the far greater likelihood of multiple rate hikes in the UK and US in 2022/23 in order to restore public trust in the Fed and BoE (Chart 13). The ECB can continue to be patient on responding to higher euro area inflation, given more stable euro area inflation expectations and with limited evidence that higher realized inflation is boosting European wage growth. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Recommendations Duration Regional Allocation Spread Product Tactical Trades GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Image

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Dear Client, This week, the US Bond Strategy service is hosting its Quarterly Webcast (November 16 at 10:00 AM EST, 15:00 PM GMT, 16:00 PM CET and November 17 at 9:00 HKT, 11:00 AEST). In addition, we are sending this Quarterly Chartpack that provides a recap of our key recommendations and some charts related to those recommendations and other areas of interest for US bond investors. Please tune in to the Webcast and browse the Chartpack at your leisure, and do let us know if you have any questions or other feedback. To view the Quarterly Chartpack PDF please click here. Best regards, Ryan Swift, US Bond Strategist

The Bank of Mexico raised rates by 25 bps on Thursday, marking the fourth consecutive rate increase this year and bringing the benchmark rate to 5%. These hikes come as the central bank attempts to temper rising inflation. At 6.24% y/y, CPI headline inflation…

Highlights US growth will slow next year, not because demand will falter, but because supply-side constraints will prevent the economy from producing as much output as households and businesses want to buy. If aggregate demand exceeds aggregate supply, the price level will rise. We argue that the US aggregate demand curve is currently quite steep. This implies that the price level may need to rise a lot to restore balance to the economy. In fact, if the aggregate demand curve is not just steep but upward-sloping, which is quite possible, there may be no price level that brings aggregate demand in line with supply; the US economy could go supernova. When supply is the binding constraint to growth, investors need to throw the old playbook for dealing with growth slowdowns out the window. Rather than positioning for lower bond yields, investors should position for higher yields. Rather than expecting a stronger dollar, investors should expect a weaker one. Rather than favoring growth stocks, large caps, and defensives, investors should favor value stocks, small caps, and cyclicals. The Binding Constraint To Growth Is Now Supply After a post-Delta wave rebound in Q4, the US economy is expected to slow over the course of 2022. The Bloomberg consensus is for US growth to decelerate from 4.9% in 2021Q4 to 4.1% in 2022Q1, 3.9% in 2022Q2, 3.0% in 2022Q3, and 2.5% in 2022Q4. Growth in the first quarter of 2023 is expected to dip further to 2.3%. We agree that US growth will slow next year but think the market narrative around this slowdown is misguided. Chart 1Plenty Of Pent-Up Demand

Plenty Of Pent-Up Demand

Plenty Of Pent-Up Demand

The standard market playbook for dealing with an economic slowdown is to position for lower bond yields, a stronger US dollar, and a decline in commodity prices. On the equity side, the playbook calls for shifting equity exposure from cyclicals to defensives, favoring large caps over small caps, and growth stocks over value stocks. There are two major problems with this narrative. First, growth is peaking at much higher levels than before and is unlikely to return to trend at least until the second half of 2023. Second, and more importantly, US growth will slow due to supply-side constraints rather than inadequate demand. US final demand will remain robust for the foreseeable future. Households are sitting on $2.3 trillion in excess savings, equivalent to 15% of annual consumption (Chart 1). The household deleveraging cycle is over. After initially plunging during the pandemic, credit card balances are rising (Chart 2). Banks are falling over themselves to make consumer loans (Chart 3). Chart 2Revolving Credit On The Rise Again

Revolving Credit On The Rise Again

Revolving Credit On The Rise Again

Chart 3Banks Are Easing Credit Standards For Consumers

Banks Are Easing Credit Standards For Consumers

Banks Are Easing Credit Standards For Consumers

Chart 4A Record Rise In Household Net Worth

A Record Rise In Household Net Worth

A Record Rise In Household Net Worth

Household net worth has risen by over 100% of GDP since the start of the pandemic (Chart 4). As we discussed two weeks ago, the wealth effect alone could boost annual consumer spending by up to 4% of GDP. Investment demand should remain strong. Business inventories are near record low levels (Chart 5). Core capital goods orders, a leading indicator for corporate capex, have soared (Chart 6). Chart 5Business Inventories Are Near Record Low Levels

Business Inventories Are Near Record Low Levels

Business Inventories Are Near Record Low Levels

Chart 6Rise In Durable Goods Orders Bodes Well For Capex

Rise In Durable Goods Orders Bodes Well For Capex

Rise In Durable Goods Orders Bodes Well For Capex

Chart 7The Homeowner Vacancy Rate Is Signaling The Need For More Homebuilding

The Homeowner Vacancy Rate Is Signaling The Need For More Homebuilding

The Homeowner Vacancy Rate Is Signaling The Need For More Homebuilding

The Dodge Momentum Index, which tracks planned nonresidential construction, rose to a 13-year high in October. The homeowner vacancy rate is at multi-decade lows, signifying the need for more homebuilding (Chart 7). While increased investment will augment the nation’s capital stock down the road, the short-to-medium term effect will be to inflate demand. Policy Won’t Tighten Enough To Cool The Economy What is the mechanism that will push down aggregate demand growth towards potential GDP growth? It is unlikely to be policy. While budget deficits will narrow over the next few years, the IMF still expects the US cyclically-adjusted primary budget deficit to be nearly 3% of GDP larger between 2022 and 2026 than it was between 2014 and 2019 (Chart 8).

Chart 8

Chart 9The Fed And Investors Still Believe In Secular Stagnation

The Fed And Investors Still Believe In Secular Stagnation

The Fed And Investors Still Believe In Secular Stagnation

As Matt Gertken, BCA’s Chief Geopolitical Strategist, writes in this week’s US Political Strategy report, the passage of the $550 billion infrastructure bill has increased, not decreased, the odds of President Biden and the Democrats passing their social spending bill via the partisan budget reconciliation process. On the monetary side, the Federal Reserve will finish tapering asset purchases next June and begin raising rates shortly thereafter. However, the Fed has no intention of raising rates aggressively. Most FOMC members see the Fed funds rate rising to only 2.5% this cycle (Chart 9). The “dots” call for only one rate hike in 2022 and three rate hikes in both 2023 and 2024. Investors expect rates to rise even less by end-2024 than the Fed foresees (Chart 10).

Chart 10

The Inflation Outlook Hinges On The Slope Of The Aggregate Demand Curve If policy tightening will not suffice in cooling demand, the economy will overheat and inflation will rise. But by how much will inflation increase? The answer is of great importance to investors. It also hinges on a seemingly technical question: What is the slope of the aggregate demand curve? As Chart 11 illustrates, prices will rise more if the aggregate demand curve is steep than if it is flat.

Chart 11

Chart 12Wages Rose Faster Than Prices During The Inflationary Late-60s and 70s

Wages Rose Faster Than Prices During The Inflationary Late-60s and 70s

Wages Rose Faster Than Prices During The Inflationary Late-60s and 70s

It is tempting to think of the aggregate demand curve in the same way one might think of the demand curve for, say, apples. When the price of apples rises, there is both a substitution and an income effect. An increase in the price of apples will cause shoppers to substitute away from apples towards oranges. In addition, if apples are so-called “normal goods,” shoppers will buy fewer apples in response to lower real incomes. This chain of reasoning breaks down at the aggregate level. When economists say the price level has risen, they are referring to all prices; hence, there is no substitution effect. Moreover, since one person’s spending is another’s income, rising prices do not necessarily translate into lower overall real incomes. Granted, if nominal wages are sticky, as they usually are in the short run, an unanticipated increase in prices will reduce real wage income. However, this will be offset by higher business income. Over time, wages tend to catch up with prices. In fact, wage growth usually outstrips price growth during inflationary periods. For example, real wages rose during the late-1960s and 70s but fell during the disinflationary 1980s (Chart 12). Textbook Reasons For A Downward-Sloping Aggregate Demand Curve According to standard economic theory, there are three main reasons why aggregate demand curves are downward-sloping: The Pigou Effect: Higher prices erode the purchasing power of money, resulting in a negative wealth effect. The Keynes Effect: Higher prices reduce the real money supply. This pushes up real interest rates, leading to lower investment spending. The Mundell-Fleming Effect: Higher real rates push up the value of the currency, causing net exports to decline. None of these three factors are particularly important for the US these days. Chart 13Base Money Has Swollen Since The Subprime Crisis

Base Money Has Swollen Since The Subprime Crisis

Base Money Has Swollen Since The Subprime Crisis

Strictly speaking, the Pigou wealth effect applies only to “base money,” also known as “outside money.” Outside money includes cash notes, coins, and bank reserves. Inside money such as bank deposits are not included in the Pigou effect because while an increase in consumer prices decreases the real value of bank deposits, it also decreases the real value of commercial bank liabilities.1 In the US, the monetary base has swollen from 6% of GDP in 2008 to 28% of GDP as a result of the Fed’s QE programs (Chart 13). Nevertheless, even if one were to generously assume a wealth effect of 10% from changes in monetary holdings, this would still imply that a 1% increase in consumer prices would reduce spending by only 0.03% of GDP. Simply put, the Pigou effect is just not all that big.

Chart 14

In contrast to the Pigou effect, the Keynes effect has historically had a significant impact on the business cycle. However, the importance of the Keynes effect faded following the Global Financial Crisis as the Fed found itself up against the zero lower bound on interest rates. When interest rates are very low, there is little to distinguish money from bonds. Rather than holding money as a medium of exchange (i.e., for financing transactions), households and businesses end up holding money mainly as a store of wealth. In the presence of the zero bound, the demand for money becomes perfectly elastic with respect to the interest rate (Chart 14). As a result, changes in the real money supply have no effect on interest rates, and by extension, interest-rate sensitive spending. And if a decline in the real money supply does not push up interest rates, this undermines the Mundell-Fleming effect as well. Could The Aggregate Demand Curve Be Upward-Sloping? The discussion above, though rather theoretical in nature, highlights an important practical point: The aggregate demand curve may be quite steep. This means that the price level might need to rise a lot to equalize aggregate demand with aggregate supply. Chart 15US Real Bond Yields Hitting Record Lows

US Real Bond Yields Hitting Record Lows

US Real Bond Yields Hitting Record Lows

In fact, one can easily envision a scenario where a rising price level boosts spending; that is, where the demand curve is not just steep but upward-sloping. One normally assumes that higher inflation will prompt central banks to raise rates by more than inflation has risen, leading to higher real rates. However, if the Fed drags its feet in hiking rates, as it is wont to do given its concerns about the zero bound, rising inflation will translate into a decline in real rates. Lower rates will boost demand, leading to higher inflation, and even lower real rates. In addition, lower real rates will benefit debtors, who tend to have a higher marginal propensity to spend than creditors. This, too, will also boost aggregate demand. It is striking in this regard that real bond yields hit a record low this week, with the 10-year TIPS yield falling to -1.17% and the 30-year yield drooping to -0.57% (Chart 15). Black Holes Vs. Supernovas

Chart 16

In the case where the aggregate demand curve is upward-sloping, there is no stable equilibrium (Chart 16). If demand falls short of supply, demand will continue to shrink as the price level declines, leading to ever-rising unemployment. Unless policymakers intervene with stimulus, the economy will sink into a deflationary black hole. In contrast, if demand exceeds supply, demand will continue to rise as the price level increases exponentially. The economy will go supernova. Tick Tock Young stars fuse hydrogen into helium, releasing excess energy in the process. After the star has run out of hydrogen, if it is big enough, it will start fusing helium into heavier elements such as carbon and oxygen. The process of nucleosynthesis continues until it reaches iron. That is the end of the line. Fusing elements heavier than iron requires a net input of energy. Unable to generate enough external pressure through fusion, the star loses its battle to gravity. The core collapses, spewing material deep into interstellar space (a good thing since your body is mainly made from this stardust). Observing the star from afar, one would be hard-pressed to see anything abnormal until it explodes. The path to becoming a supernova is highly non-linear. The same is true for inflation. Just like a star with an ample supply of hydrogen, the Fed can burn through its credibility for a while longer. During the 1960s, it took four years for inflation to take off after the economy had reached full employment (Chart 17). By that time, the unemployment rate was two percentage points below NAIRU. Most of today’s inflation is confined to durable goods. This is not a sustainable source of inflation. The durable goods sector is the only part of the CPI where prices usually fall over time (Chart 18). Chart 17Inflation Spiked In The 1960s Only Once The Unemployment Rate Had Fallen Far Below Equilibrium

Inflation Spiked In The 1960s Only Once The Unemployment Rate Had Fallen Far Below Equilibrium

Inflation Spiked In The 1960s Only Once The Unemployment Rate Had Fallen Far Below Equilibrium

Chart 18Inflation Has Been Concentrated In Durable Goods, A Sector Where Prices Usually Fall Over Time

Inflation Has Been Concentrated In Durable Goods, A Sector Where Prices Usually Fall Over Time

Inflation Has Been Concentrated In Durable Goods, A Sector Where Prices Usually Fall Over Time

To get inflation to go up and stay up in modern service-based economies, wages need to rise briskly. While US wage growth has picked up, the bulk of the increase has been among low-wage workers, particularly in the services and hospitality sector (Chart 19). Chart 19Wage Growth Has Picked Up, But Mainly At The Bottom Of The Income Distribution

Wage Growth Has Picked Up, But Mainly At The Bottom Of The Income Distribution

Wage Growth Has Picked Up, But Mainly At The Bottom Of The Income Distribution

The most likely scenario for next year is that firms will simply ration output, fearful that raising prices too quickly will hurt brand loyalty and trigger accusations of price gouging. Shortages will persist, but this time they will be increasingly concentrated in the service sector. Such a state of affairs will not last, however. Competition for workers will cause wages to rise much more than they have so far. Keen to protect profit margins, firms will start jacking up prices. A wage-price spiral will develop. The US economy could go supernova. Investment Conclusions Chart 20Long-Term Inflation Expectations Are Near The Bottom End Of The Fed's Comfort Zone

Long-Term Inflation Expectations Are Near The Bottom End Of The Fed's Comfort Zone

Long-Term Inflation Expectations Are Near The Bottom End Of The Fed's Comfort Zone

US growth will slow next year, not because demand will falter, but because supply-side constraints will prevent the economy from producing as much output as households and businesses want to buy. This means that the old playbook for dealing with growth slowdowns needs to be thrown out the window. Rather than positioning for lower bond yields, investors should position for higher yields. Rather than expecting a stronger dollar, investors should expect a weaker one. Rather than favoring growth stocks, large caps, and defensives, investors should favor value stocks, small caps, and cyclicals. While inflation expectations have recovered from their pandemic lows, the 5-year/5-year forward TIPS breakeven inflation rate is still near the bottom end of the Fed’s comfort zone (Chart 20). Rising inflation expectations will lift long-term bond yields, justifying a short duration stance in fixed-income portfolios. Higher bond yields will benefit value stocks. Chart 21 shows that there has been a strong correlation between the relative performance of growth and value stocks and the 30-year bond yield this year. Rising input prices will make the US export sector less competitive, leading to a weaker dollar. Historically, non-US stocks have done well when the dollar has been weakening (Chart 22). Chart 21The Relative Performance of Value Stocks Has Closely Tracked Bond Yields This Year

The Relative Performance of Value Stocks Has Closely Tracked Bond Yields This Year

The Relative Performance of Value Stocks Has Closely Tracked Bond Yields This Year

Chart 22Non-US Stocks Tend To Do Best When The US Dollar Is Weakening

Non-US Stocks Tend To Do Best When The US Dollar Is Weakening

Non-US Stocks Tend To Do Best When The US Dollar Is Weakening

As for the overall stock market, with the Fed still in the dovish camp, it is too early to turn negative on equities. An equity bear market is coming, but not until rising inflation forces the Fed to step up the pace of rate hikes. That will probably not happen until mid-2023. Short Gilt Trade Activated We noted last week that we would go short the 10-year UK Gilt if the yield broke below 0.85%. Our limit order was activated on November 5th and we are now short this security. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Footnotes 1 To distinguish between inside and outside money, one should ask where the liability resides. If the liability resides within the private sector, it is inside money. By convention, central bank reserves are classified as outside money. However, one could argue that since taxpayers ultimately own the central bank, an increase in the price level will benefit taxpayers by eroding the real value of the central bank’s liability. If one were to take this view, the Pigou effect would be even weaker. Global Investment Strategy View Matrix

Image

Special Trade Recommendations

Image

Current MacroQuant Model Scores

Image

Highlights Geopolitical conflicts point to energy price spikes and could add to inflation surprises in the near term. However, US fiscal drag and China’s economic slowdown are both disinflationary risks to be aware of. Specifically, energy-producers like Russia and Iran gain greater leverage amid energy shortages. Europe’s natural gas prices could spike again. Conflict in the Middle East could disrupt oil flows. President Biden’s $1.75 trillion social spending bill is a litmus test for fiscal fatigue in developed markets. It could fail, and even assuming it passes it will not prevent overall fiscal drag in 2022-23. However, it is inflationary over the long run. China’s slowdown poses the chief disinflationary risk. But we still think policy will ease to avoid an economic crash ahead of the fall 2022 national party congress. We are closing this year’s long value / short growth trade for a loss of 3.75%. Cyclical sectors ended up being a better way to play the reopening trade. Feature Equity markets rallied in recent weeks despite sharp upward moves in core inflation across the world (Chart 1). Inflation is fast becoming a popular concern and we see geopolitical risks that could drive headline inflation still higher in the short run. We also see underrated disinflationary factors, namely China’s property sector distress and economic slowdown. Several major developments have occurred in recent weeks that we will cover in this report. Our conclusions: Biden’s domestic agenda will pass but risks are high and macro impact is limited. Congress passed Biden’s infrastructure deal and will probably still pass his signature social spending bill, although inflation is creating pushback. Together these bills have little impact on the budget deficit outlook but they will add to inflationary pressures. Energy shortages embolden Russia and Iran. Winter weather is unpredictable, the energy crisis may not be over. But investors are underrating Russia’s aggressive posture toward the West. Any conflict with Iran could also cause oil disruptions in the near future. US-China relations may improve but not for long. A bilateral summit between Presidents Joe Biden and Xi Jinping will not reduce tensions for very long, if at all. Climate change cooperation is an insufficient basis to reverse the cold war-style confrontation over the long run. Chart 1Inflation Rattles Policymakers

Inflation Rattles Policymakers

Inflation Rattles Policymakers

The investment takeaway is that geopolitical tensions could push energy prices still higher in the short term. Iran and Russia need to be monitored. However, China’s economic slowdown will weigh on growth. China poses an underrated disinflationary risk to our views. US Congress: Bellwether For Fiscal Fatigue While inflation is starting to trouble households and voters, investors should bear in mind that the current set of politicians have long aimed to generate an inflation overshoot. They spent the previous decade in fear of deflation, since it generated anti-establishment or populist parties that threatened to disrupt the political system. They quietly built up an institutional consensus around more robust fiscal policy and monetary-fiscal coordination. Now they are seeing that agenda succeed but are facing the first major hurdle in the form of higher prices. They will not simply cut and run. Inflation is accompanied by rising wages, which today’s leaders want to see – almost all of them have promised households a greater share of the fruits of their labor, in keeping with the new, pro-worker, populist zeitgeist. Real wages are growing at 1.1% in the US and 0.9% across the G7 (Chart 2). Even more than central bankers, political leaders are focused on jobs and employment, i.e. voters. Yet the labor market still has considerable slack (Chart 3). Almost all of the major western governments have been politically recapitalized since the pandemic, either through elections or new coalitions. Almost all of them were elected on promises of robust public investment programs to “build back better,” i.e. create jobs, build infrastructure, revitalize industry, and decarbonize the energy economy. Thus while they are concerned about inflation, they will leave that to central banks, as they will be loathe to abandon their grand investment plans. Chart 2Higher Wages: Real Or Nominal?

Higher Wages: Real Or Nominal?

Higher Wages: Real Or Nominal?

Still, there will be a breaking point at which inflation forces governments to put their spending plans on hold. The US Congress is the immediate test of whether today’s inflation will trigger fiscal fatigue and force a course correction. Chart 3Policymakers Fear Populism, Focus On Employment

Policymakers Fear Populism, Focus On Employment

Policymakers Fear Populism, Focus On Employment

President Biden’s $550 billion infrastructure bill passed Congress last week and will be signed into law around November 15. Now he is worried that his signature $1.75 trillion social spending bill will falter due to inflation fears. He cannot spare a single vote in the Senate (and only three votes in the House of Representatives). Odds that the bill fails are about 35%. Democratic Party leaders will not abandon the cause due to recent inflation prints. They see a once-in-a-generation opportunity to expand the role of government, the social safety net, and the interests of their constituents. If they miss this chance due to inflation that ends up being transitory then they will lose the enthusiastic left wing of the party and suffer a devastating loss in next year’s midterm elections, in which they are already at a disadvantage. Biden’s social bill is also likely to pass because the budget reconciliation process necessary to pass the bill is the same process needed to raise the national debt limit by December 3. A linkage of the two by party leaders would ensure that both pass … and otherwise Democrats risk self-inflicting a national debt default. The reconciliation bill is more about long-term than short-term inflation risk. The bill does not look to have a substantial impact on the budget outlook: the new spending is partially offset by new taxes and spread out over ten years. The various legislative scenarios look virtually the same in our back-of-the-envelope budget projections (Chart 4).

Chart 4

However, given that the output gap is virtually closed, this bill combined with the infrastructure bill will add to inflationary pressures. The fiscal drag will diminish by 2024, not coincidentally the presidential election year 2024, not coincidentally the presidential election year. The deficit is not expected to increase or decrease substantially between 2023 and 2024. From then onward the budget deficit will expand. The increased government demand for goods and services and the increased disposable income for low-earning families will add to inflationary pressures. Other developed markets face a similar situation: inflation is picking up, but big spending has been promised and normalizing budgets will marginally weigh on growth in the next few years (Chart 5). True, growth should hold up since the private economy is rebounding in the wake of the pandemic. But politicians will not be inclined to renege on campaign promises of liberal spending in the face of fiscal drag. The current crop of leaders is primed to make major public investments. This is true of Germany, Japan, Canada, and Italy as well as the United States. It is partly true in France, where fiscal retrenchment has been put on hold given the presidential election in the spring. The effect will be inflationary, especially for the US where populist spending is more extravagant than elsewhere.

Chart 5

The long run will depend on structural factors and how much the new investments improve productivity. Bottom Line: A single vote in the US Senate could derail the president’s social spending bill, so the US is now the bellwether for fiscal fatigue in the developed world. Biden is likely to pass the bill, as global fiscal drag is disinflationary over the next 12 months. Yet inflation could stay elevated for other reasons. And this fiscal drag will dissipate later in the business cycle. Russia And Iran Gain Leverage Amid Energy Crunch The global energy price spike arose from a combination of structural factors – namely the pandemic and stimulus. It has abated in recent weeks but will remain a latent problem through the winter season, especially if La Niña makes temperatures unusually cold as expected. Rising energy prices feed into general producer prices, which are being passed onto consumers (Chart 6). They look to be moderating but the weather is unpredictable. There is another reason that near-term energy prices could spike or stay elevated: geopolitics. Tight global energy supply-demand balances mean that there is little margin of safety if unexpected supply disruptions occur. This gives greater leverage to energy producers, two of which are especially relevant at the moment: Russia and Iran. Russia’s long-running conflict with the West is heating up on several fronts, as expected. Russia may not have caused the European energy crisis but it is exacerbating shortages by restricting flows of natural gas for political reasons, as it is wont to do (Chart 7). Moscow always maintains plausible deniability but it is currently flexing its energy muscles in several areas: Chart 6Energy Price Depends On Winter ... And Russia/Iran!

Energy Price Depends On Winter ... And Russia/Iran!

Energy Price Depends On Winter ... And Russia/Iran!

Ukraine: Russia has avoided filling up and fully utilizing pipelines and storage facilities in Ukraine, where the US is now warning that Russia could stage a large military action in retaliation for Ukrainian drone strikes in the still-simmering Russia-Ukraine war. Belarus: Russia says it will not increase the gas flow through the major Yamal-Europe natural gas pipeline in 2022 even as Belarus threatens to halt the pipeline’s operation entirely. Belarus, backed by Russia, is locked in a conflict with Poland and the EU over Belarus’s funneling of migrants into their territory (Chart 8). The conflict could lead not only to energy supply disruptions but also to a broader closure of trade and a military standoff.1 Russia has flown two Tu-160 nuclear-armed bombers over Belarus and the border area in a sign of support. Moldova: Russia is withholding natural gas to pressure the new, pro-EU Moldovan government.

Chart 7

Chart 8

Russia’s main motive is obvious: it wants Germany and the EU to approve and certify the new Nord Stream II pipeline. Nord Stream II enables Germany and Russia to bypass Ukraine, where pipeline politics raise the risk of shortages and wars. Lame duck German Chancellor Angela Merkel worked with Russia to complete this pipeline before the end of her term, convincing the Biden administration to issue a waiver on congressional sanctions that could have halted its construction. However, two of the parties in the incoming German government, the Greens and the Free Democrats, oppose the pipeline. While these parties may not have been able to stop the pipeline from operating, Russia does not want to take any chances and is trying to force Germany’s and the EU’s hand. The energy crisis makes it more likely that the pipeline will be approved, since the European Commission will have to make its decision during a period when cold weather and shortages will make it politically acceptable to certify the pipeline.2 The decision will further drive a wedge between Germany and eastern EU members, which is what Russia wants. EU natural gas prices will likely subside sometime next year and will probably not derail the economic recovery, according to both our commodity and Europe strategists. A bigger and longer-lasting Russian energy squeeze would emerge if the Nord Stream II pipeline is not certified. This is a low risk at this point but the next six months could bring surprises. More broadly, the West’s conflict with Russia can easily escalate from here. First, President Vladimir Putin faces economic challenges and weak political support. He frequently diverts popular attention by staging aggressive moves abroad. There is no reason to believe his post-2004 strategy of restoring Russia’s sphere of influence in the former Soviet space has changed. High energy prices give him greater leverage even aside from pipeline coercion – so it is not surprising that Russia is moving troops to the Ukraine border again. Growing military support for Belarus, or an expanded conflict in Ukraine, are likely to create a crisis now or later. Second, the US-Germany agreement to allow Nord Stream II explicitly states that Russia must not weaponize natural gas supply. This statement has had zero effect so far. But when the energy shortage subsides, the EU could pursue retaliatory measures along with the United States. Of course, Russia has been able to weather sanctions. But tensions are already escalating significantly. After Russia, Iran also gains leverage during times of tight energy supplies. With global oil inventories drawing down, Iran is in the position to inflict “maximum pressure” on the US and its allies, a role reversal from the 2017-20 period in which large inventories enabled the US to impose crippling sanctions on Iran after pulling out of the 2015 nuclear deal (Chart 9). Iran is rapidly advancing on its nuclear program and a new round of diplomatic negotiations may only serve to buy time before it crosses the “breakout” threshold of uranium enrichment capability as early as this month or next. In a recent special report we argued that there is a 40% chance of a crisis over Iran in the Middle East. Such a crisis could ultimately lead to an oil shock in the Persian Gulf or Strait of Hormuz. Chart 9Now Iran Can Use 'Maximum Pressure'

Now Iran Can Use 'Maximum Pressure'

Now Iran Can Use 'Maximum Pressure'