Inflation/Deflation

Dear Client, Next week I will be hosting and attending client events, both virtual and in person. Our next report, on November 24 will be a recap of my observations from the meetings with our clients. Best regards, Jing Sima China Strategist Executive Summary Chart Of The DayThe Gap Between Chinese Manufacturing Input And Output Prices Reached Multi-Year High

The Gap Between Chinese Manufacturing Input And Output Prices Reached Multi-Year High

The Gap Between Chinese Manufacturing Input And Output Prices Reached Multi-Year High

Producer price inflation in China will likely peak in the next two quarters, but inflation could remain elevated well into 2022. Chinese producers will continue to pass on inflation to domestic and foreign consumers. Core CPI is only a notch below its pre-pandemic level; rising energy and food prices, along with improved service sector consumption, will push up headline consumer prices next year. Lack of meaningful policy easing is creating an air pocket for China’s economy, with significant near-term risks for a faster-than-expected economic slowdown. We continue to prefer the CSI500 Index over the broader onshore market.

In Limbo

In Limbo

Bottom Line: China’s business cycle has rapidly matured while inflation remains a risk. We are still underweight Chinese equities in a global portfolio. Within Chinese stocks, we continue to favor CSI500 Index which has a greater exposure to external demand. Feature Chart 1Persistently Negative Economic Surprises

Persistently Negative Economic Surprises

Persistently Negative Economic Surprises

China’s economic conditions deteriorated in the third quarter. Chart 1 shows that the nation’s economic surprise index remains in deep contraction. However, the combination of power shortages and persistent supply-side price pressures has limited policy choices, particularly the traditional measures used to stimulate the economy. We are closely monitoring the BCA China Play Index and the relative performance of domestic infrastructure stocks versus global equities as proxies for reflation; neither is signaling a significant improvement (Chart 2). The outlook for Chinese stocks in the next 6 to 12 months remains dim. Chinese corporate profit growth has peaked, and input cost pressure on domestic producers may prove to be stickier than the market has currently priced in (Chart 3). Chart 2Reflation Proxies Are Not Signaling A Major Economic Upturn

Reflation Proxies Are Not Signaling A Major Economic Upturn

Reflation Proxies Are Not Signaling A Major Economic Upturn

Chart 3Corporate Profit Growth Has Peaked

Corporate Profit Growth Has Peaked

Corporate Profit Growth Has Peaked

Producer Price Inflation Remains A Near-Term Risk China’s producer price index (PPI) inflation may stay high longer than the market is expecting. Supply-side pressures and bottlenecks will abate, but perhaps not as fast as investors expect. Moreover, energy prices will likely remain elevated into 2022 and labor shortages in the urban areas will further exacerbate inflationary pressures. As discussed in a previous report, the surge in China’s manufacturing output and prices has been driven by strong US consumer demand for goods. Robust external demand this year occurred as China’s industrial sector had gone through years of capacity reduction and domestic de-carbonization efforts gained momentum. Chart 4Expanding Mining Capacity Takes Time

Expanding Mining Capacity Takes Time

Expanding Mining Capacity Takes Time

Capacity in the mining sector will expand in the next 6 to 12 months if the power crunch persists. However, the 2015/16 supply-side reforms significantly reduced China’s upstream industry’s capability to produce. Given the capital-intensive nature of upstream industries, expanding production output often takes a long time. Chart 4 shows the significant lag between mining’s higher product prices, which indicate rising demand and tighter supply, and improved output and investment in the sector. The industrial sector’s capacity utilization rate remains elevated. China’s manufacturers can ramp up output more easily compared with mining enterprises. However, both manufacturing investment growth and output in volume have been falling (Chart 5). The wide gap between manufacturing input and output prices means that the profit margin among producers of manufacturing goods has been squeezed, giving them little incentive to expand business operations (Chart 6). Chart 5Manufacturing Investment Growth And Output Volume Have Been Falling

Manufacturing Investment Growth And Output Volume Have Been Falling

Manufacturing Investment Growth And Output Volume Have Been Falling

Chart 6The Gap Between Chinese Manufacturing Input And Output Prices Reached Multi-Year High

The Gap Between Chinese Manufacturing Input And Output Prices Reached Multi-Year High

The Gap Between Chinese Manufacturing Input And Output Prices Reached Multi-Year High

In addition, PPI inflation may be slow to decline for the following reasons: Coal futures prices have been clobbered since mid-October in the wake of government regulatory measures to curb speculation in the domestic commodity exchange market (Chart 7). However, the plunge does not solve the supply shortage issue. Coal prices at China’s major ports have been trending sideways and remain at historic highs (Chart 8). Chart 7Regulators Have Squashed Coal Price Speculations In Commodity Exchanges...

Regulators Have Squashed Coal Price Speculations In Commodity Exchanges...

Regulators Have Squashed Coal Price Speculations In Commodity Exchanges...

Chart 8...But Coal Prices At Ports Remain High

...But Coal Prices At Ports Remain High

...But Coal Prices At Ports Remain High

Regulators have allowed electricity producers to boost prices by as much as 20% to industrial users. We estimate that a 20% increase in electricity prices can add anywhere from half to one percentage point to PPI. The recovery in the global service sector will provide support to oil prices (Chart 9). BCA’s Commodity and Energy Strategy service expects energy prices to soften in the next 12 months, but not by as much as the markets are discounting. Our latest forecast sets Brent crude oil at an average $81/bbl in 2021Q4, $80/bbl in 2022 (versus market expectations of $77/bbl) and $81/bbl in 2023 (versus market expectations of $71/bbl) (Chart 10). Chart 9Oil Prices Find Support From Recovery In Global Service Activity

Oil Prices Find Support From Recovery In Global Service Activity

Oil Prices Find Support From Recovery In Global Service Activity

Chart 10

China’s domestic demand has weakened, particularly in the construction sector. Prices for steel rebar, iron ore and cooper have all rolled over and/or fallen sharply (Chart 11). Nonetheless, the prices remain well above pre-pandemic levels and policy-induced production cuts may limit the downside. Labor shortages in China’s urban areas have not improved. Reverse migration has increased since early last year when China imposed travel restrictions to contain domestic COVID transmission. Workers from rural areas opted to remain in their hometowns rather than return to work in urban areas. As of Q3 this year, there were still about 2 million fewer migrant workers than in the pre-COVID years, which has exacerbated an urban labor shortage that existed before the pandemic (Chart 12). Chart 11Commodity Prices In China Have Rolled Over, But Downside May Be Limited

Commodity Prices In China Have Rolled Over, But Downside May Be Limited

Commodity Prices In China Have Rolled Over, But Downside May Be Limited

Chart 12Migrant Workers Are Slow To Return To Urban Jobs

Migrant Workers Are Slow To Return To Urban Jobs

Migrant Workers Are Slow To Return To Urban Jobs

Bottom Line: PPI should peak in the next one to two quarters as supply bottlenecks ease and the base factor wanes. However, China’s industrial capacity and labor market remain tight. Producer inflationary pressures may sustain longer than investors expect. Passing On Costs To Consumers Chart 13Households Are Paying Higher Prices For Durable Goods And Daily Necessities

Households Are Paying Higher Prices For Durable Goods And Daily Necessities

Households Are Paying Higher Prices For Durable Goods And Daily Necessities

The weakness in demand from Chinese households has kept consumer price inflation subdued so far this year. Nonetheless, Chinese producers have started to pass on supply-side cost pressures to consumers, both domestic and foreign. Rising raw material costs have pushed up the price of Chinese consumer durable goods, such as home appliances (Chart 13). Consumer prices for fuel have reached the highest level since the data collection started in 2016. The cost of consumer daily necessities is also climbing: households are paying more for utilities (water, electricity and fuel) compared with pre-pandemic years and prices are at 2013 highs. Escalating electricity prices will further strengthen inflationary pressures on the CPI. While residential electricity costs are strictly regulated in China and are unlikely to rise in the near future, price inflation passthroughs will be mainly via higher costs on both consumer goods and services. If the 20% increase in electricity costs among Chinese manufacturers is passed onto consumers, it could potentially push up the CPI by about 0.2 -0.4 percentage points. The cost of food and vegetables has also jumped since early October. Given the high likelihood of La Niña this winter, food inflation could further mount and potentially push the headline CPI close to the PBoC’s 3% inflation target next year. The recovery in China’s service sector has lagged due to domestic COVID flareups and subsequent lockdowns (Chart 14A and 14B). However, service CPI has recovered to above its pre-pandemic level, with strong rebounds in tourism and transportation (Chart 15). Given that China is accelerating vaccine boosters, an improvement in the domestic COVID situation next year could further support the service sector’s consumption and prices. Chart 14AService Sector Recovery In China Has Lagged...

Service Sector Recovery In China Has Lagged...

Service Sector Recovery In China Has Lagged...

Chart 14BService Sector Recovery In China Has Lagged...

Service Sector Recovery In China Has Lagged...

Service Sector Recovery In China Has Lagged...

Chart 15...But Prices Have Not

...But Prices Have Not

...But Prices Have Not

Chart 16Chinese Export Growth Remained Buyout Through October

Chinese Export Growth Remained Buyout Through October

Chinese Export Growth Remained Buyout Through October

China’s exporters are passing on inflation to their foreign customers too. Newly released trade data highlights buoyant export growth through October (Chart 16). Even though goods consumption in the US will likely converge to its long-term trend next year, inventories are at multi-year lows while global industrial production growth remains well above trend (Chart 17). China’s export growth may stay strong in the next two quarters, as suggested by our regression-based modelling (Chart 18). Exporters have been charging US and global customers less than average prices (Chart 19). Robust demand for consumer and capital goods from the US and Europe should give China’s exporters sustained pricing power. Chart 17Extremely Low Inventories In The US Will Benefit Chinese Exports

Extremely Low Inventories In The US Will Benefit Chinese Exports

Extremely Low Inventories In The US Will Benefit Chinese Exports

Chart 18Above-Trend Growth In Global Industrial Production Will Also Support Chinese Exports

Above-Trend Growth In Global Industrial Production Will Also Support Chinese Exports

Above-Trend Growth In Global Industrial Production Will Also Support Chinese Exports

Bottom Line: China’s producers will continue to pass on inflation to their domestic and foreign customers. Chart 19Chinese Export Prices Are Below Global Average

Chinese Export Prices Are Below Global Average

Chinese Export Prices Are Below Global Average

Chart 20Favor CSI500 Index Over A-Shares

Favor CSI500 Index Over A-Shares

Favor CSI500 Index Over A-Shares

Investment Conclusions China’s authorities will unlikely use policy measures to cool domestic demand, but they will be constrained by lingering inflationary risks driven by external consumption and supply-side pressures in the next six months. Monetary and fiscal policies will ease to counter the slowdown in the economy, but reflationary measures will be gradual. We expect the money and credit impulse to bottom in Q4, but the rebound will be subdued. As such, domestic demand will remain sluggish and economic growth will likely decelerate faster than the onshore market has currently discounted. While we maintain a cautious stance on Chinese stocks in general, we continue to favor the CSI500 Index relative to the broader A-share market. External demand growth may remain above trend in the next six months. The CSI500 has a larger exposure to the global economy and lower valuation relative to China’s broad onshore market, and should still have some upside potentials. (Chart 20). Jing Sima China Strategist jings@bcaresearch.com Market/Sector Recommendations Cyclical Investment Stance

We will be holding our quarterly webcasts next Monday, November 15th at 10:00 a.m. Eastern time and Tuesday, November 16th at 8:00 a.m. Hong Kong time in lieu of publishing a Weekly Report. Please join us with your questions to make it a fully interactive event. We will resume our regular publication schedule on the 22nd. Highlights Economy – Wages could be on the rise if workers are able to exploit the considerable leverage they now enjoy: The labor market currently has no slack. Workers’ ability to derive a lasting advantage from today’s shortages will determine if the extended decline in labor’s share of income will reverse. Markets – Lengthy agreements in labor’s favor could give inflation an additional impetus: Investors are not prepared for a shift in the balance of power from management to labor and a range of assets will have to reprice if workers can achieve some durable victories. Strategy – Keep an eye on labor agreements, which could hasten a shift to more defensive positioning: The current economic backdrop, along with accommodative monetary and fiscal policy, support risk-friendly portfolio positioning, but a labor revival could prompt the Fed to engage in a disruptive tightening cycle that would halt the bull markets in equities and credit and possibly also short-circuit the expansion. Feature At the end of 2019, tiring of the market debates du jour, we began haunting the New York Public Library, reading all we could about US labor relations history. Several books and rolls of microfilm later, we published a three-part Special Report on workers’ past, present and future. While we concluded that organized labor would not regain the influence it wielded in the fifties, sixties and seventies, we thought that investors were underestimating the potential for workers to reverse the grinding decline in their fortunes that began in the early eighties. Public opinion seemed to be shifting in workers’ favor, especially among the young; the coming election held promise for the Democrats; and the pendulum had swung so far, for so long, that there was little scope for management to gain any more ground. We looked forward to countering the view that organized labor was as dead as a doornail, only to have COVID-19 render the topic irrelevant. Nearly two years later, however, dislocations caused by the pandemic have pushed negotiations over wages and labor conditions to the fore. Amidst a recent flurry of strikes against S&P 500 constituents, clients have been asking what the labor future holds. We refresh the themes we identified in our initial analysis, noting how conditions have shifted since early 2020. The investment takeaway is that increasing labor muscle could stoke inflation and push long-run inflation expectations higher, forcing the Fed to tighten monetary policy more abruptly than markets expect. The 2020 Election Went Labor’s Way A review of the historical record makes it crystal clear that employees cannot gain ground if government sides with employers. The 2020 election, which delivered both the White House and the Senate to Democrats, put some unexpected wind in labor’s sails. They did not mark a revival of the New Deal, however, as Democrats’ legislative majorities are precariously thin and unlikely to survive the 2022 midterms, their control of the presidency may not extend beyond 2024, and the federal judiciary will be inclined to see things management’s way for some time thanks to past conservative appointments. At the state level, the executive and legislative branches remain firmly in Republican control. A friendly executive branch can do a lot to reset the scales nonetheless. The Biden Department of Labor, National Labor Relations Board (NLRB), Occupational Safety and Health Administration (OSHA) and Department of Justice are certain to enforce existing worker protection laws more vigorously than their recent predecessors, while more actively challenging business combinations. Joe Biden began his election campaign at a Pittsburgh union hall and returned to the Steel City to end it, promising to be “the most pro-union president you’ve ever seen.” Labor leaders have generally given him high marks since taking office for supporting legislation to make it easier for workers to organize and he publicly offered moral support to John Deere’s UAW workers when they went on strike last month, saying, “My message is they have a right to strike and they have a right to demand higher wages.” Public Opinion Has Continued To Shift Toward Labor We noted two years ago that young Democratic voters overwhelmingly favored Bernie Sanders’ and Elizabeth Warren’s candidacies, suggesting that solidarity with workers might be on the rise. It is no surprise that students would be the most avid supporters of progressive campaigns, but Millennials, born between 1981 and 1996, and Generation Z might be viewed as the Inequality Generations, having entered the workforce after China’s admittance to the WTO, which coincided with a peak in labor’s share of income (Chart 1). Their lives have spanned the September 11th attacks, the financial crisis, a once-in-a-century pandemic and three equity market crashes, and many of them started adulthood with onerous student debt burdens and dim earnings prospects. They might find the notion of a union buffer from market forces especially alluring and therefore view unions favorably. The 2019 Gallup poll found that public approval for unions had reached nearly 20-year highs; two years on, it’s up to levels last reached over 50 years ago (Chart 2). Chart 1Workers' Share Of The Pie Shrank For 15 Years

Workers' Share Of The Pie Shrank For 15 Years

Workers' Share Of The Pie Shrank For 15 Years

Chart 2Extreme Makeover

Extreme Makeover

Extreme Makeover

Public opinion is crucially important to the outcome of labor negotiations because for-profit employers will seek the most favorable terms they can get, to the extent that they are socially acceptable. In our schematic of the 1980s vicious circle that initiated unions’ 40-year decline, public opinion made it possible for the Reagan administration to take a hard line against the air traffic controllers’ union and emboldened private employers to take more aggressive measures as well (Figure 1). Beyond the private sector, elected officials reliably deliver what their constituents want, and the courts do, too, albeit with a longer lag. The median voter theory advanced by our geopolitical strategists doesn’t just predict future outcomes, it directly influences them.

Chart

Striketober Another key takeaway from our original study was that successful strikes beget strikes. Strikes are the most potent weapon in workers’ arsenal – withholding their labor threatens to reduce their employer’s output and may halt it altogether – but they are fraught with risk for individual employees. Striking workers don’t get paid beyond the partial support that may be provided by their union strike fund and may find themselves entirely out of work if the strike fails. Workers should only strike when they have a good chance of winning or when their situation has become so intolerable that they have little to lose. Strikes (and lockouts) occur when labor and management cannot reach a mutually acceptable settlement, often because at least one side overestimates its bargaining power. It is easy to agree when labor and management hold similar views about each side’s relative position, as when both perceive that one of them is considerably stronger. In that case, a settlement favoring the stronger side can be reached quickly, especially if the stronger side exercises some restraint and does not seek to impose terms that the weaker side can scarcely abide. Restraint is rational in repeated games like employer-employee bargaining, and when both parties recognize that relative bargaining positions are fluid, they are likely to exercise it. Viewing labor negotiations through a game theory lens, we posit a simple framework in which each side can hold any of five perceptions of its bargaining power, resulting in a total of 25 possible joint perceptions. Labor (L) can believe it is way stronger than Management (M), L >> M; stronger than Management, L > M; roughly equal, L ≈ M; weaker than Management, L < M; or way weaker than Management, L << M. Management also holds one of these five perceptions, and the interaction of the two sides’ perceptions establishes the path negotiations will follow. Limiting our focus to today’s prevailing conditions, Figure 2 displays only the outcomes consistent with labor’s belief that it has the upper hand. For completeness, the exhibit lists all of management’s potential perceptions, but we deem the three away from the extremes to be most likely. Record job openings and job quits rates (Chart 3) should disabuse even the most rabidly anti-union managements from thinking they hold all the cards. On the other hand, four consecutive decades of victories will make it hard for all but the most objective management negotiators to believe that the tables have completely turned and that labor is fully in control.

Chart

Chart 3It's A Labor Seller's Market ...

It's A Labor Seller's Market ...

It's A Labor Seller's Market ...

Strike outcomes turn on which side has overestimated its leverage. The broad factors we use to assess leverage are overall labor market slack; economic concentration; regulatory and legal trends; and the sustainability of either side’s accumulated advantage, which we describe as the labor-management rubber band. Other factors that matter on a case-by-case basis, but are beyond the scope of our analysis, include industry-level slack, a labor input’s susceptibility to automation, and the degree of labor specialization/skill involved in that input. For these micro-level factors, a given group of workers’ leverage is inversely related to the availability of substitutes for their input. Labor Market Slack Though we hold the view that labor force participation is likely to revive in coming months because inequality and a comparatively thin social safety net will compel many lower-income workers to return to the work force, no one knows for sure where the workers have gone or when they will return, if at all. It is abundantly clear from accelerating wage gains (Chart 4), the openings and quits rates, and small businesses’ historic inability to fill job openings (Chart 5) that the labor market is extremely tight right now. A difference of opinion about whether and how long the worker shortages will persist could make finding common ground in contract negotiations a challenge. Chart 4... As Rising Wages ...

... As Rising Wages ...

... As Rising Wages ...

Chart 5... And Frantic Employers Confirm

... And Frantic Employers Confirm

... And Frantic Employers Confirm

Economic Concentration We previously noted that the trend toward economic concentration has strengthened management’s hand in labor negotiations as it has made an increasing share of local labor markets tend toward monopsony. A monopsony is a market with a single buyer, the mirror image of a monopoly, which is a market with a single seller. Unfortunately for labor, monopsonies restrain prices just as monopolies inflate them. The trend toward economic concentration is well established and we think the probability that it will reverse is low – Congress may shake its fist at Big Tech and the Biden Justice Department will more vigorously contest mergers on anti-trust grounds, but there is an ocean of liquidity available to support acquisitions and robust CEO confidence suggests it will be deployed. Regulatory And Legal Trends Over the last four decades, unions have endured a near-constant drubbing from statehouses, federal agencies and the courts, as union and labor protections have been under siege from all sides. But the regulatory and legal tide has been such a huge benefit for employers since the beginning of the Reagan administration that it simply cannot continue to maintain its pace. Furthermore, as our Global Investment Strategy colleagues have observed, the Republican party’s lurch toward populism may leave Big Business without a champion in Washington, DC. The regulatory and legal winds are shifting and management teams that have spent their entire careers in an environment in which labor has perpetually been on the back foot may be the last to know, leading to an uptick in the number and contentiousness of labor disputes. A change in Fed policy, as unveiled in the August 2020 revision to the FOMC’s statement on longer-run monetary policy goals, has also tilted the playing field in workers’ favor. The Fed has sworn off preemptively tightening monetary policy when the labor market appears to be getting tight. The new direction contrasts with 40-plus years of Fed policy that were predicated on taking away the punch bowl before upward wage pressures could build momentum. The tacit pledge in the revised statement on monetary policy implies that the Fed will prioritize its full employment mandate over its price stability mandate in the near term. That’s not an unalloyed positive for workers, who will only be better off if their nominal wage gains outpace inflation, but it will help give them more of a head start than they would have gotten if the FOMC had stuck with the proposition that tight labor markets stoke inflation. The Labor-Management Rubber Band Employees and employers have a deeply symbiotic relationship, and we like to think of labor and management as being linked by an elastic tether with a finite range. Since neither side can indefinitely thrive if the other is suffering, the tether pulls the two sides closer together when the gap between them threatens to become too wide. When labor does too well for too long at management’s expense, profit margins shrink and the company’s viability as a going concern is threatened. When management does too well, deteriorating living standards drive the best employees away, undermining productivity and profitability. One does not have to be a card-carrying socialist to believe that the band is near its limit and that some sort of mean reversion is inevitable, given how badly real hourly wages have lagged gains in hourly output over the last 50 years (Chart 6). Chart 6Testing How Far The Labor-Management Rubber Band Can Stretch

Testing How Far The Labor-Management Rubber Band Can Stretch

Testing How Far The Labor-Management Rubber Band Can Stretch

What Comes Next Steady concentration across industries and a persistently hospitable legal and regulatory climate has given management the upper hand for four decades. Going forward, however, labor should see its fortunes improve as the legal and regulatory climate cannot get materially better for employers, and the labor-management rubber band becomes less stretched in management’s favor (Figure 3).

Chart

The major uncertainty pertains to the ongoing level of slack in the labor market and how employment agreements should account for it. All parties recognize there is no slack right now and employers are duly offering generous inducements to attract workers. Sign-on bonuses for new employees in unskilled services positions are ubiquitous and negotiations with unionized employees include ratification bonuses for signing new contract packages. Because wages are sticky on the downside – it’s difficult to get employees to swallow outright pay cuts – employers prefer making one-time concessions like bonuses to increasing wage rates across the board, which is tantamount to locking in higher long-term input costs. The duration of concessions appears to be a sticking point in the negotiations to settle the current strikes. Over the last two decades, several large companies with unionized workforces have instituted a two-tier employment track distinguishing legacy employees from new hires. The legacy employees remain on their existing salary path and retain their retirement and health insurance benefits, while new employees are subject to a lower salary scale and are entitled to fewer benefits, if any. The result has been to bend the human resources cost curve lower in the future as natural attrition shrinks the share of employees on the more costly legacy path. The two-tier employment classification has proven to be an effective way for employers to bend the cost curve to their liking, as it protects the interests of a considerable majority of employee voters at the expense of a largely hypothetical future employee constituency. It is presumably difficult to empathize with workers who aren’t yet coming to the plant every day and legacy employees haven’t dwelled on their plight when participating in contract ratification votes. An interesting feature of the ongoing John Deere strike is that the UAW rejected what appeared to be a strikingly generous package partially in the interest of defending current and future employees who have no path to reach legacy employees’ all-in compensation level. The recent strikes against S&P 500 constituents have been concentrated in industries that faced demand spikes during the pandemic. The bakery worker’s union (BCTGM) representing Kellogg’s workers struck against Frito-Lay (owned by Pepsi) for three weeks in July and Nabisco (a unit of Mondelez) for five weeks in August and September. A significant motivation for the BCTGM workers’ actions seemed to be frustration over intense pandemic workloads. Their plants ramped up capacity to fill kitchen cabinets while consumers were cooped up at home and they are now seeking redress for the emergency hours they were asked to work. (All of the bakery workers who struck, as well as the John Deere workers, were considered essential workers.) Management, on the other hand, might take the view that their employees’ sacrifices are in the past, and are not likely to be repeated if product demand settles back into its pre-pandemic trend. Viewing ongoing negotiations from our game theory perspective, there is ample room for divergent perceptions of relative negotiating strength, based on differing opinions about the persistence of pandemic trends. The divergence might make for increasingly contentious labor negotiations going forward, with strikes exacerbating supply bottlenecks and ramping up near-term inflation pressures. If ongoing rounds of labor negotiations result in workers achieving longer-term victories, it will pressure corporate profit margins. Labor gains will also potentially feed into inflation if capacity is not poised to meet the ensuing increase in aggregate demand. We will keep close tabs on labor negotiations as the economy works its way back to a post-pandemic steady state. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com

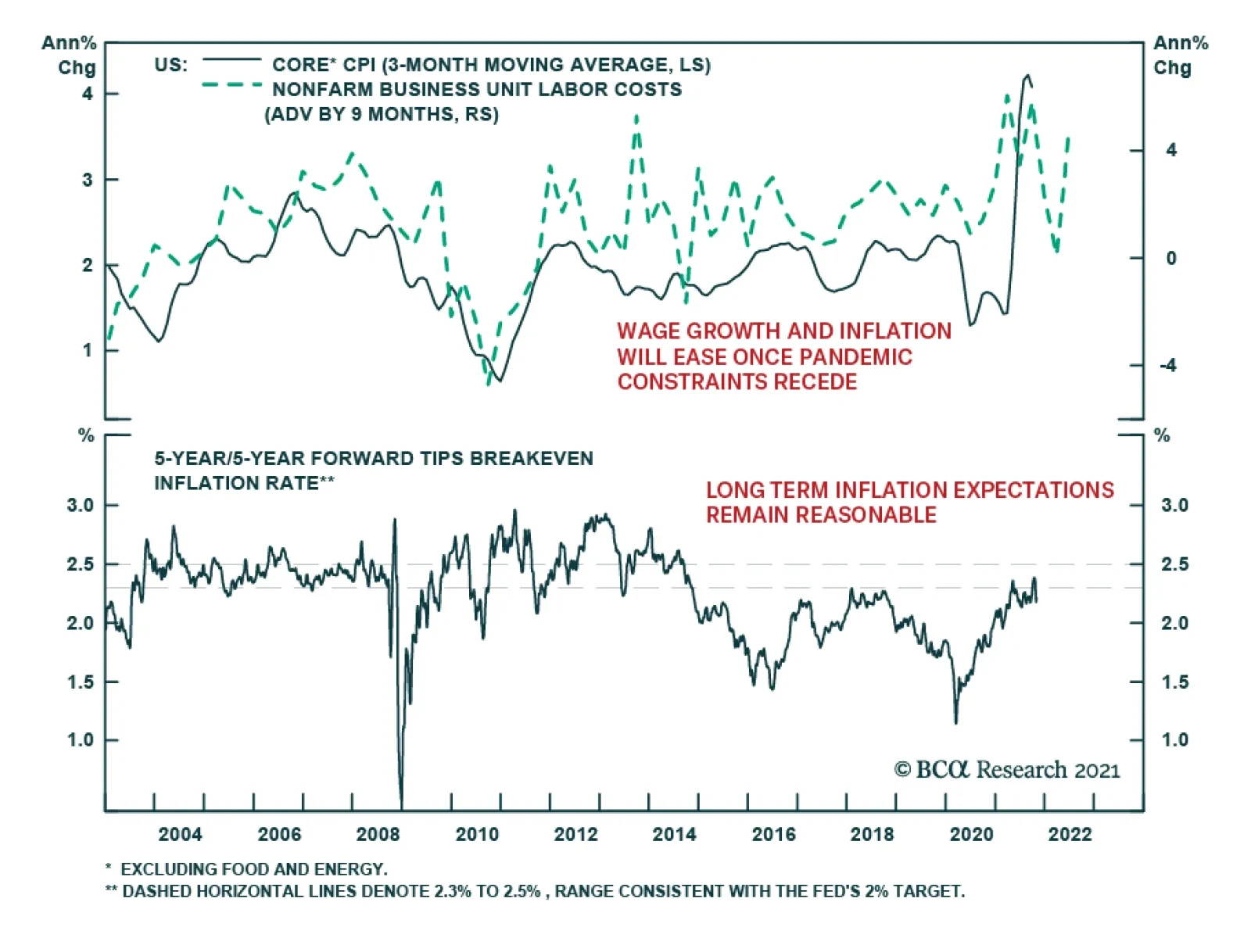

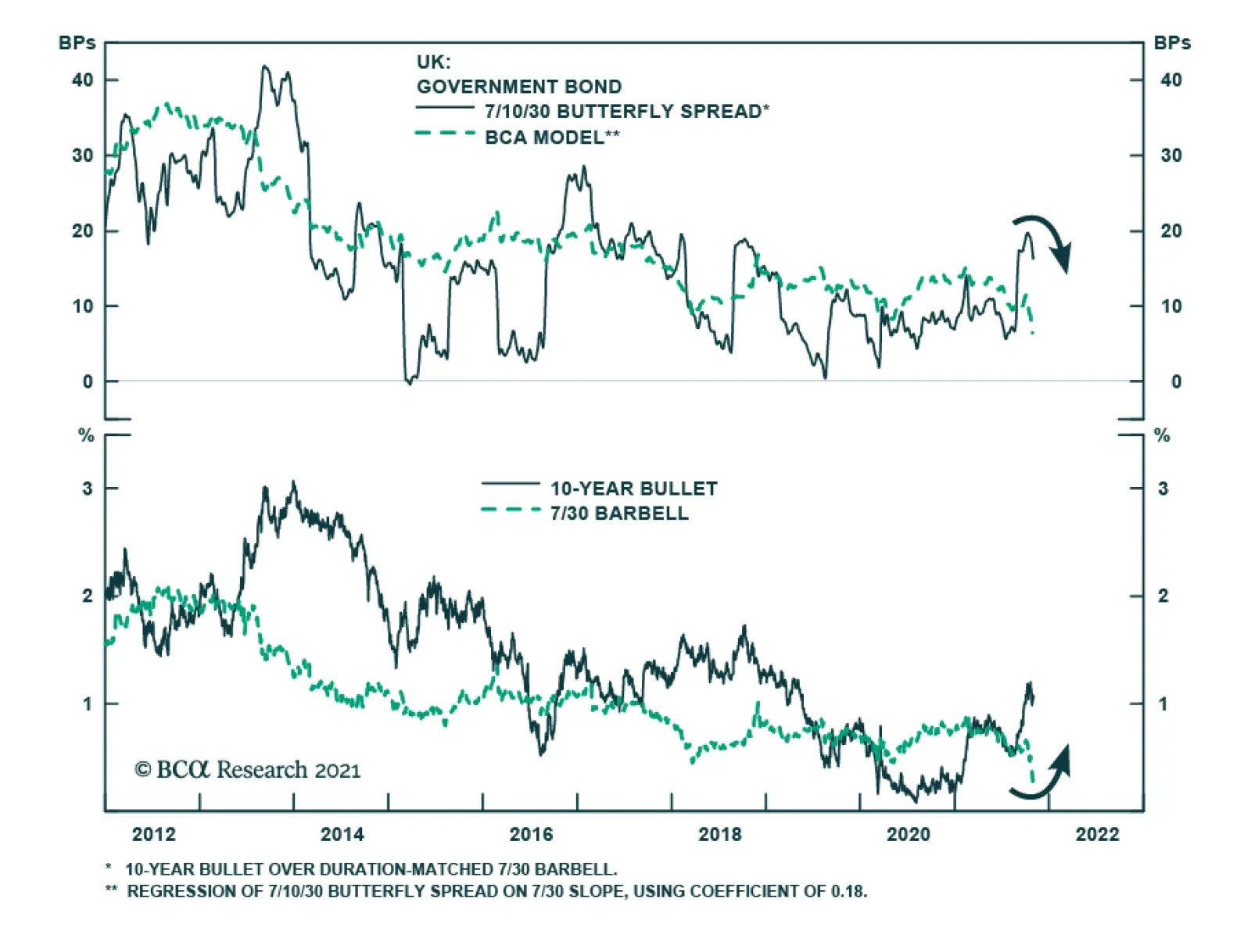

Highlights Supply-side pressures should abate over the coming months as semiconductor availability improves, transportation bottlenecks ease, energy prices recede, and more workers enter the labor force. The respite from inflation will be temporary, however. The combination of easy fiscal and monetary policies will cause unemployment to fall below its equilibrium level in the US, and eventually, in most major economies. Unlike in the late 1990s, when rising wages were counterbalanced by robust productivity gains, most of the recent rebound in US productivity growth will prove to be illusory. US inflation will follow a “two steps up, one step down” trajectory. We are currently at the top of those two steps, but rising unit labor costs will eventually drive inflation higher. Rather than fretting that the Federal Reserve will keep rates too low for too long, investors are worried that the Fed will tighten too much. This is a key reason why the 20-year/30-year Treasury slope has inverted. Such an inversion does not make sense to us. Hence, we are initiating a trade going long the 20-year bond versus the 30-year bond. Go short the 10-year Gilt on any break below 0.85%. UK real bond yields are amongst the lowest in the world. The Bank of England will eventually have to turn more hawkish, which will support the beleaguered pound. Structurally higher bond yields will benefit value stocks. Banks stand to gain from rising bond yields while tech could suffer. The eventual re-emergence of supply-side pressures will catalyze more investment spending. This will bolster industrial stocks. The Supply Side Matters, Again Savings glut, secular stagnation; call it what you will, but for the better part of two decades, the global economy has faced a chronic shortfall of aggregate demand. Times are changing, however. The predominant problem these days is not a lack of spending; it is a lack of production. Unlike during the Global Financial Crisis – when worries about moral hazard complicated efforts to bail out homeowners and banks – the victims of the pandemic elicited sympathy. As a result, governments in developed economies rolled out a slew of measures to support workers and businesses. Thanks to bountiful fiscal transfers, households in the US have accrued $2.2 trillion in income since the start of the pandemic, about $1.2 trillion more than one would have expected based on the pre-pandemic trend (Chart 1). With many services unavailable, consumers diverted spending towards manufactured goods. At first, sellers were able to dip into their inventories to meet rising demand. By early this year, however, inventories had been depleted (Chart 2). Shortages began to pop up across much of the global supply chain. Chart 1Stimulus-Supported Income Growth Boosted Goods Consumption

Stimulus-Supported Income Growth Boosted Goods Consumption

Stimulus-Supported Income Growth Boosted Goods Consumption

Chart 2The Pandemic Depleted Inventories

The Pandemic Depleted Inventories

The Pandemic Depleted Inventories

While today’s empty warehouses can be largely attributed to surging demand for goods, supply-side disruptions have also played an important role. Four disruptions stand out: 1) semiconductor shortages; 2) transportation bottlenecks; 3) inadequate energy supplies; and 4) reduced labor force participation. Let us examine all four in turn. Semiconductor Shortages Chart 3Car Prices Have Jumped

Car Prices Have Jumped

Car Prices Have Jumped

The global supply chain was not equipped to handle the dislocations caused by the pandemic. The combination of just-in-time inventory systems and far-flung supplier networks ensured that bottlenecks in one part of the global economy quickly filtered down to other parts of the economy. Few industries are as important as semiconductors. The auto sector has felt the brunt of the chip shortage. Both new and used vehicle prices have soared as dealer lots have emptied out (Chart 3). The drop in vehicle spending alone shaved 2.4 percentage points off US real GDP growth in the third quarter. Semiconductor makers have ramped up production to meet growing demand. The US Census Bureau’s Quarterly Survey of Plant Capacity Utilization showed that semiconductor plants operated an average of 73 hours per week in the first half of this year, up from around 45-to-50 hours prior to the pandemic (Chart 4). Chip production in Northeast Asia has rebounded (Chart 5). Southeast Asian production dropped in August due to Covid lockdowns, with semiconductor exports falling by over a third in Malaysia and Vietnam. Fortunately, since then, a decline in Covid cases and rising vaccination rates have spurred a recovery throughout the region. Chart 4Chipmakers Are Working Overtime

Chipmakers Are Working Overtime

Chipmakers Are Working Overtime

Chart 5Semiconductor Production Has Accelerated In Northeast Asia

Semiconductor Production Has Accelerated In Northeast Asia

Semiconductor Production Has Accelerated In Northeast Asia

Chart 6Memory Chip Prices Are Declining

Memory Chip Prices Are Declining

Memory Chip Prices Are Declining

Commentary from semiconductor companies and automakers suggest that the chip shortage will ease over the coming months. In an auspicious sign, US auto sales jumped to 13.1 million in October from 12.3 million in September. Memory chip prices are also falling (Chart 6). Nevertheless, the overall chip market is unlikely to return to balance until 2023. Transportation Bottlenecks Unlike semiconductors and high-end electronics, which usually arrive by air, bulkier items such as furniture, sporting goods, and housing appliances typically arrive by sea. Port congestion, insufficient warehouse capacity, and a lack of truck chassis on which to place containers have all contributed to transportation bottlenecks. Chart 7Transportation Bottlenecks: Past The Worst?

Transportation Bottlenecks: Past The Worst?

Transportation Bottlenecks: Past The Worst?

As with the semiconductor shortage, we are probably past the worst point in the shipping crisis. Drewry’s composite World Container Index has edged down 11% from its highs, although it is still up more than three-fold from mid-2020 levels (Chart 7). The easing in container shipping costs follows a dramatic 47% decline in the Baltic Dry Index since early October. The number of ships waiting to unload cargo off the coast of Los Angeles and Long Beach remains near record highs (Chart 8). Port congestion should ease over the next few months. US port throughput usually falls starting in the late fall and remains weak during the winter months, bottoming shortly after the Chinese New Year. If throughput remains elevated near current levels this year, this should be enough to clear much of the backlog. Looking further out, shipping costs could face additional downward pressure. Chart 9 shows that the number of container ships on order has risen to a 10-year high; these new ships will be delivered over the next two years. Chart 8Port Congestion Should Ease Over The Coming Months

Port Congestion Should Ease Over The Coming Months

Port Congestion Should Ease Over The Coming Months

Chart 9Shipbuilders Are Busy

Shipbuilders Are Busy

Shipbuilders Are Busy

Inadequate Energy Supplies After a torrid rally since the start of the year, energy prices have come off their highs. The price of Brent oil has dipped 6% from its October peak. US natural gas prices have retreated 11%. Natural gas prices in Europe have fallen 37%.

Chart 10

The biggest move has been in coal prices, which have dropped 36% over the past two weeks alone. Futures curves are pricing in further declines in key energy prices (Chart 10). BCA’s Commodity and Energy Strategy service expects energy prices to soften over the next 12 months, but not as much as markets are discounting. Their latest forecast calls for the price of Brent crude to average $81/bbl in 2021Q4, $80/bbl in 2022 (versus market expectations of $77/bbl), and $81/bbl in 2023 (versus market expectations of $71/bbl). As we discussed a few weeks ago, years of underinvestment have led to tight supply conditions across the entire energy complex (Chart 11). Proven global oil reserves increased by only 6% between 2010 and 2020, having risen by 26% over the preceding decade. Gas reserves followed a similar trajectory, increasing by only 5% between 2010 and 2020 compared to 30% over the prior ten years (Chart 12).

Chart 11

Chart 12

With little spare capacity, energy markets have become increasingly vulnerable to shocks. A cold snap across the Northern Hemisphere this spring depleted natural gas supplies, while a lack of wind reduced energy production by European wind farms. Increased gas imports from Russia could have mitigated the problem, but the dispute over the Nord Stream 2 pipeline prevented that from happening. The pipeline is popular with German voters (Chart 13). BCA’s geopolitical team expects it to be approved, a welcome development given that La Niña is highly likely to lead to colder-than-normal temperatures across northern Europe this winter.

Chart 13

China has also restarted 170 coal mines and will probably begin re-importing Australian coal. Beijing is also allowing utilities to charge higher prices, which should help stave off bankruptcies across the sector. These measures should help mitigate China’s energy crisis. Chart 14US Rig Count Has Risen From Low Levels

US Rig Count Has Risen From Low Levels

US Rig Count Has Risen From Low Levels

A bit more oil production will also help. The US rig count, while still far below its 2014 highs, has doubled since last year (Chart 14). BCA’s commodity strategists expect output in the Lower 48 states to average 9.5mm b/d in 2022 and 10mm b/d in 2023, versus 2021 production levels of 9.0mm b/d. Nevertheless, shale producers are a lot more disciplined these days. Debt reduction and cash flow generation are now the top priorities. This implies that fairly high oil prices may be necessary to catalyze additional investment in the industry. Reduced Labor Force Participation Despite the rapid economic recovery, US employment remains 5 million below its pre-pandemic peak. One would not know this from the survey data, however. A record 51% of small businesses expressed difficulty finding qualified workers in the October NFIB survey. The share of households reporting that jobs are plentiful versus hard-to-get has returned to its 2000 highs. Both the quits rate and the job openings rate are well above their pre-pandemic levels (Chart 15). A wave of early retirement accounts for some of the apparent labor market tightness. About 1.3 million more workers have retired since the pandemic began than one would have expected based on demographic trends. Yet, there is more to the story than that. The labor force participation rate for workers aged 25-to-54 has not fully recovered; the employment-to-population ratio for that age cohort is still 2.5 percentage points below pre-pandemic levels (Chart 16).

Chart 15

Chart 16Labor Force Participation Has Room To Rise

Labor Force Participation Has Room To Rise

Labor Force Participation Has Room To Rise

There is considerable uncertainty about how many workers will re-enter the labor force over the coming months. On the one hand, the expiration of enhanced unemployment benefits could prod more workers into the job market. Diminished anxiety about the virus should help. While the number has fallen by half, there are still 2.5 million people not working due to concerns about getting or spreading Covid-19 (Chart 17). According to Boston College’s Center for Retirement Research, the retirement rate rose more for older lower-income workers than higher-income workers (Chart 18). Some of these retirees may decide to re-enter the labor force. Chart 17Less Anxiety About The Coronavirus Should Increase Labor Supply

Poorer Older Workers Were More Likely To Retire Last Year

Poorer Older Workers Were More Likely To Retire Last Year

Chart 18

On the other hand, the imposition of vaccine mandates could reduce labor supply. About 100 million US workers are currently subject to the mandates. According to the Census Household Pulse Survey, about 8 million of them are unvaccinated and attest that “they will definitely not get the vaccine.” Perhaps the biggest question mark is over whether the pandemic will lead to permanent changes in peoples’ perspectives on the optimal work/life balance. High burnout rates (especially in the health care sector), a reluctance to restart the daily commute to the office, and the desire to spend more time with family have all contributed to what some commentators have dubbed The Great Resignation. Ultimately, the deciding factor may be wages. Wage growth accelerated during the late 1990s as the labor market tightened (Chart 19). This drew a lot of people – especially less-skilled workers – into the labor force. Recently, wage growth has exploded at the bottom end of the income distribution, and our guess is that this will entice more people to seek employment (Chart 20). Chart 19Wage Growth Accelerated During The Late 1990s As The Labor Market Tightened

Wage Growth Accelerated During The Late 1990s As The Labor Market Tightened

Wage Growth Accelerated During The Late 1990s As The Labor Market Tightened

Chart 20Wages At The Bottom End Of The Income Distribution Are Rising Briskly

Wages At The Bottom End Of The Income Distribution Are Rising Briskly

Wages At The Bottom End Of The Income Distribution Are Rising Briskly

Will Higher Productivity Growth Mitigate Supply-Side Pressures? The late 1990s saw a resurgence in productivity growth. This helped restrain unit labor costs in the face of rising wages.

Chart 21

While US productivity did jump during the pandemic, we are sceptical of claims that this can be attributed to efficiency gains from digitalization and work-from-home practices. A recent study of 10,000 skilled professionals at a major IT company revealed that work-from-home policies decreased productivity by 8%-to-19%, mainly because people ended up working longer. It is telling that productivity outside of the US generally declined during the pandemic (Chart 21). This suggests that last year’s productivity gains stemmed mainly from increased operating leverage, a common feature of post-recession US recoveries (Chart 22). Supporting this view is the fact that productivity growth slowed from 4.3% in Q1 to 2.4% in Q2 on a quarter-over-quarter annualized basis. Productivity declined by 5% in Q3, leading to an 8.3% increase in unit labor costs. Chart 22US Productivity Tends To Jump After Recessions

US Productivity Tends To Jump After Recessions

US Productivity Tends To Jump After Recessions

Chart 23Capital Goods Orders Have Soared

Capital Goods Orders Have Soared

Capital Goods Orders Have Soared

The only saving grace is that core capital goods orders have soared (Chart 23). This should translate into increased business capital spending next year and higher productivity down the road. Investment Implications Supply-side pressures should abate over the coming months as semiconductor availability improves, transportation bottlenecks ease, energy prices recede, and more workers enter the labor force. The respite from inflation will be temporary, however. The combination of easy fiscal and monetary policies will cause unemployment to fall below its equilibrium level in the US, and eventually, in most major economies. This is consistent with our “two steps up, one step down” projection for US inflation. We are probably near the top of those two steps at present. This implies that the next move for inflation is to the downside, even if the longer-term trend is still to the upside. The US 10-year Treasury yield should stabilize at around 1.8% in the first half of 2022, before moving higher later in the year. As we discussed last week, markets are understating the true level of the neutral rate of interest. Rather than fretting that the Federal Reserve will keep rates too low for too long, investors are worried that the Fed will tighten too much. This is a key reason why the 20-year/30-year Treasury slope has inverted (Chart 24). Such an inversion does not make sense to us. Hence, as of this week, we are initiating a trade going long the 20-year bond versus the 30-year bond. We would also go short the 10-year Gilt on any break below 0.85%. The Bank of England’s “surprising hold” knocked the yield down 14 basis points to 0.93%. UK real bond yields are amongst the lowest in the world (Chart 25). Growth is strong and will remain buoyant as Brexit headwinds fade. The BoE will eventually have to turn more hawkish, which will support the beleaguered pound. Chart 24Go Long US 20-Year Bonds Versus 30-Year Bonds

Go Long US 20-Year Bonds Versus 30-Year Bonds

Go Long US 20-Year Bonds Versus 30-Year Bonds

Chart 25UK Real Bond Yields Are Amongst The Lowest In The World

UK Real Bond Yields Are Amongst The Lowest In The World

UK Real Bond Yields Are Amongst The Lowest In The World

Structurally higher bond yields will benefit value stocks. Chart 26 shows that there has been a close correlation between the US 30-year Treasury yield and the relative performance of global value versus growth stocks. Banks stand to gain from rising bond yields while tech could suffer (Chart 27). Chart 26Higher Bonds Yields Favor Value Stocks

Higher Bonds Yields Favor Value Stocks

Higher Bonds Yields Favor Value Stocks

Chart 27

The re-emergence of supply-side pressures could affect companies in a variety of unexpected ways. For example, Facebook and Google both rely heavily on revenue from advertising. But what is the point of trying to boost demand for your product if you already cannot produce enough of it? Companies such as Hershey and Kimberly-Clark are already cutting ad spending in response to supply-chain bottlenecks. Finally, tight supply conditions will catalyze more investment spending. This will benefit industrial stocks. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Global Investment Strategy View Matrix

Chart 28

Special Trade Recommendations

The Supply Side Strikes Back

The Supply Side Strikes Back

Current MacroQuant Model Scores

Chart 29

Unit labor costs in the US nonfarm business sector surged 8.3% in Q3 following Q2’s 1.1%, beating expectations of 7.0%. T increase in unit labor costs reflects both lower productivity and higher hourly compensation. Nonfarm productivity fell 5.0% – the…

The Bank of England kept policy unchanged at its meeting on Thursday. The Monetary Policy Committee voted by a majority of 6-3 to maintain UK bond purchases and a majority of 7-2 to keep the Bank Rate at 0.1%. Governor Bailey borrowed a page from Jerome…

Image

The markets were deluged by a lot of information in late October. Several central banks made surprise moves towards tightening (the Bank of Canada, for example, ended asset purchases, and the Reserve Bank of Australia effectively abandoned its yield-curve control). Inflation continued to surprise on the upside (headline CPI in the US is now 5.4% year-on-year). But, at the same time, there were signs of faltering growth with, for example, US real GDP growth in Q3 coming in at only 2.0% quarter-on-quarter annualized, compared to 6.7% in Q2. This caused a flattening of the yield curve in many countries, as markets priced in faster monetary tightening but lower long-term growth (Chart 1). Nonetheless, equities shrugged off the barrage of news, with the S&P500 ending the month at a new high. All this highlights what we discussed in our latest Quarterly: That the second year of a bull market is often tricky, resulting in lower (but still positive) returns from equities and higher volatility. For risk assets to continue to outperform, our view of a Goldilocks environment needs to be “just right”: The economy must not be too hot or too cold. We think it will be – and so stay overweight equities versus bonds. But investors should be aware of the risks on either side. How too hot? Inflation is broadening out (at least in the US, UK, Australia and Canada, though not in the euro zone and Japan) and is no longer limited to items which saw unusually strong demand during the pandemic but where supply is constrained (Chart 2). Chart 1What Is The Message Of Flattening Yield Curves?

What Is The Message Of Flattening Yield Curves?

What Is The Message Of Flattening Yield Curves?

Chart 2Inflation Is Broadening Out In The US

Inflation Is Broadening Out In The US

Inflation Is Broadening Out In The US

There is a risk that this turns into a wage-price spiral as employees, amid a tight labor market, push for higher wages to offset rising prices. We find that wages tend to follow prices with a lag of 6-12 months (Chart 3). The Atlanta Fed Wage Tracker (good for gauging underlying wage pressures since it looks only at employees who have been in a job for 12 months or more) is already at 3.5% and looks set to rise further. On the back of these inflationary moves, the market has significantly pulled forward the date of central bank tightening. Futures now imply that the Fed will raise rates in both July and December next year (Chart 4) and that other major developed central banks will also raise multiple times over the next 14 months (Table 1). Breakeven inflation rates have also risen substantially (Chart 5). Chart 3Wages Tend To Rise After Prices Rise

Wages Tend To Rise After Prices Rise

Wages Tend To Rise After Prices Rise

Chart 4Will The Fed Really Hike This Soon?

Will The Fed Really Hike This Soon?

Will The Fed Really Hike This Soon?

Table 1Futures Implied Path Of Rate Hikes

Monthly Portfolio Update: The Risks To Goldilocks

Monthly Portfolio Update: The Risks To Goldilocks

Chart 5Breakevens Suggest Higher Inflation

Breakevens Suggest Higher Inflation

Breakevens Suggest Higher Inflation

We think these moves are a little excessive. There are several reasons why inflation might cool next year. Companies are rushing to increase capacity to unblock supply bottlenecks. For example, semiconductor production has already begun to increase, bringing down DRAM prices over the past few months (Chart 6). Another big contributor to broad-based inflation has been a 126% increase in container shipping costs since the start of the year (Chart 7). But currently the number of container ships on order is at a 10-year high; these new ships will be delivered over the next two years. Such deflationary forces should pull down core inflation next year (though we stick to our longstanding view that for multiple structural reasons – demographics, the end of globalization, central bank dovishness, the transition away from fossil fuels – inflation will trend up over the next five years). Chart 6DRAM Prices Falling As Production Ramps Up

DRAM Prices Falling As Production Ramps Up

DRAM Prices Falling As Production Ramps Up

Chart 7All Those Ships On Order Should Bring Down Shipping Costs

All Those Ships On Order Should Bring Down Shipping Costs

All Those Ships On Order Should Bring Down Shipping Costs

The Fed, therefore, will not be in a rush to raise rates. It does not see the labor market as anywhere close to “maximum employment” – it has not defined what it means by this, but we would see it as a 3.8% unemployment rate (the median FOMC dot for the equilibrium unemployment rate) and the prime-age participation rate back to its 2019 level (Chart 8). We continue to expect the first rate hike only in December next year. The Fed will feel the need to override its employment criterion only if long-term inflation expectations become unanchored – but the 5-year 5-year forward breakeven rate is only at 2.3%, within the Fed’s effective CPI target range of 2.3-2.5% (Chart 5). We remain comfortable with our view of only a moderate rise in long-term rates, with the US 10-year Treasury yield at 1.7% by end-2021, and reaching 2-2.25% at the time of the first Fed rate hike. It is also worth emphasizing that even a fairly sharp rise in long-term rates has historically almost always coincided with strong equity performance (Chart 9 and Table 2). This has again been evident in the past 12 months: When rates rose between August 2020 and March 2021, and then from July 2021, equities performed strongly. Chart 8We Are Not Back To "Maximum Employment"

We Are Not Back To "Maximum Employment"

We Are Not Back To "Maximum Employment"

Chart 9Rising Rates Are Usually Accompanied By A Rising Stock Market

Rising Rates Are Usually Accompanied By A Rising Stock Market

Rising Rates Are Usually Accompanied By A Rising Stock Market

Table 2Episodes Of Rising Long-Term Rates Since 1990

Monthly Portfolio Update: The Risks To Goldilocks

Monthly Portfolio Update: The Risks To Goldilocks

But could the economy get too cold? We would discount the weak US GDP reading: It was mostly due to production shortages, especially in autos, which pushed down consumption on durable goods by 26% QoQ annualized, and by some softness in spending on services due to the delta Covid variant, the impact of which is now fading. US growth should continue to be supported by a combination of the $2.5 trillion of excess household savings, strong capex as companies boost their production capacity, and a further 5% of GDP in fiscal stimulus that should be passed by Congress by year-end. Similar conditions apply in other developed economies. Chart 10Real Estate Is A Big Part Of Chinese GDP

Real Estate Is A Big Part Of Chinese GDP

Real Estate Is A Big Part Of Chinese GDP

We see three principal risks to this positive outlook: A new strain of Covid-19 that proves resistant to current vaccines – unlikely but not impossible. Our geopolitical strategists worry about Iran, which may have a nuclear bomb ready by December, prompting Israel to bomb the country. Iran would likely react by hampering oil supplies, even blocking the Strait of Hormuz, through which 25% of global oil flows. Chinese growth has been slowing and the impact from the problems at Evergrande is still unclear. Real estate is a major part of the Chinese economy, with residential investment comprising 10% of GDP (Chart 10) and, broadly defined to include construction and building materials, real estate overall perhaps as much as one-third. Our China strategists don’t expect the government to launch a major stimulus which would bail out the industry, since it is happy with the way that property-related lending has been shrinking in recent years (Chart 11). We expect the slowdown in Chinese credit growth to bottom out over the coming few months, but economic activity may have further to slow (Chart 12), and there is a risk that the authorities are unable to control the fallout from the property market. Chart 11Chinese Authorities Are Happy To See Slowing Property Lending

Chinese Authorities Are Happy To See Slowing Property Lending

Chinese Authorities Are Happy To See Slowing Property Lending

Chart 12When Will Credit Growth Bottom?

When Will Credit Growth Bottom?

When Will Credit Growth Bottom?

Fixed Income: Given the macro environment described above, we remain underweight bonds and short duration. If we assume 1) a Fed liftoff in December 2022, 2) 100 basis points of rate hikes over the following year, and 3) a terminal Fed Funds Rate of 2.08% (the median forecast from the New York Fed’s Survey of Market Participants), 10-year US Treasurys will return -0.2% over the next 12 months, and 2-year Treasurys +0.3%.1 TIPs have overshot fair value and, although we remain neutral since they a tail-risk hedge against high inflation over the next five years, we would especially avoid 2-year TIPS which look very overvalued. We see some pockets of selective value in lower-quality high-yield bonds, specifically US Ba- and Caa-rated issues, which are still trading at breakeven spreads around the 35th historical percentile, whereas higher-rated bonds look very expensive (Chart 13). For US tax-paying investors, municipal bonds look particularly attractive at the moment, with general-obligation (GO) munis trading at a duration-matched yield higher than Treasurys even before tax considerations (Chart 14). Our US bond strategists have recently gone maximum overweight.

Chart 13

Chart 14Muni Bonds Are A Steal

Muni Bonds Are A Steal

Muni Bonds Are A Steal

Equities: We retain our longstanding preference for US equities over other Developed Markets. US equities have outperformed this year, irrespective of whether rates were rising or falling, or how US growth was surprising relative to the rest of the world, emphasizing the much stronger fundamentals of the US market (Chart 15). Analysts’ forecasts for the next few quarters look quite cautious, and so earnings surprises can push US stock prices up further (Chart 16). We reiterate the neutral on China but underweight on Emerging Markets ex-China that we initiated in our latest Quarterly. Our sector overweights are a mixture of cyclicals (Industrials), rising-interest-rate plays (Financials), and defensives (Heath Care). Chart 15US Equites Outperformed This Year Whatever Happened

US Equites Outperformed This Year Whatever Happened

US Equites Outperformed This Year Whatever Happened

Chart 16Analysts Are Pessimistic About The Next Couple Of Quarters

Analysts Are Pessimistic About The Next Couple Of Quarters

Analysts Are Pessimistic About The Next Couple Of Quarters

Currencies: We continue to expect the US dollar to be stuck in its trading range and so stay neutral. Recent moves in prospective relative monetary policy bring us to change two of our currency recommendations. We close our underweight on the Australian dollar. The recent rise in Australian inflation (with both trimmed mean and 10-year breakevens now above 2% – Chart 17) has brought forward the timing of the first rate hike and should push up relative real rates (Chart 18). We lower our recommendation on the Japanese yen from overweight to neutral. The Bank of Japan will not raise rates any time soon, even when other central banks are tightening. This will push real-rate differentials against the yen (Chart 18, panel 2). Chart 17Australian Inflation Is Picking Up

Australian Inflation Is Picking Up

Australian Inflation Is Picking Up

Chart 18Real Rates Moving In Favor Of The AUD And Against The JPY

Real Rates Moving In Favor Of The AUD And Against The JPY

Real Rates Moving In Favor Of The AUD And Against The JPY

Chart 19Chinese-Related Metals' Prices Are Falling

Chinese-Related Metals' Prices Are Falling

Chinese-Related Metals' Prices Are Falling

Commodities: We remain cautious on those industrial metals which are most sensitive to slowing Chinese growth and its weakening property market. The fall in iron ore prices since July is now being followed by aluminum. However, metals which are increasingly driven by investment in alternative energy, notably copper, are likely to hold up better (Chart 19). We are underweight the equity Materials sector and neutral on the commodities asset class. The Brent crude oil price has broadly reached our energy strategists’ forecasts of $80/bbl on average in 2022 and $81 in 2023 (Chart 20). Although the forward curve is lower than this, with December-22 Brent at only $75/bbl, it is a misapprehension to characterize this as the market forecasting that the oil price will fall. Backwardation (where futures prices are lower than spot) is the usual state of affairs for structural reasons (for example, producers hedging production forward). The market typically moves to contango only when the oil price has fallen sharply and reserves are high (Chart 21). We remain neutral on the equities Energy sector. Chart 20Brent Has Reached Our 2022 And 2023 Forecast Level

Brent Has Reached Our 2022 And 2023 Forecast Level

Brent Has Reached Our 2022 And 2023 Forecast Level

Chart 21Lower Oil Futures Don't Mean Oil Price Is Forecast To Fall

Lower Oil Futures Don't Mean Oil Price Is Forecast To Fall

Lower Oil Futures Don't Mean Oil Price Is Forecast To Fall

Garry Evans, Senior Vice President Global Asset Allocation garry@bcaresearch.com GAA Asset Allocation

In this report we examine the risk of stagflation by comparing the current environment to that of the late-1960s and 1970s. Today, investors cannot rule out the possibility of a stagflationary outcome, for four reasons: long-term household inflation expectations have risen significantly over the past year; fiscal policy has been expansionary; monetary policy will remain expansionary at the Fed’s projected terminal Fed funds rate; and component shortages and price increases linked to energy market and supply chain disruptions may persist or worsen over the coming year. However, the strong demand-pull inflationary dynamics that existed in the late-1960s were mostly absent in the lead-up to the pandemic, supply-chain issues are in part due to strong goods demand and supply disruptions that will eventually dissipate, and economic agents do not expect severe price pressures to persist beyond the pandemic. On balance, this points to a stagflationary outcome over the coming 6-24 months as a risk, but not a likely event. Investors should use the Misery Index, which is the sum of the unemployment rate and headline PCE inflation, as a real-time stagflation indicator. The Misery Index underscores that the US economy is unlikely to experience true stagflation unless the unemployment rate rises. A portfolio of the US dollar, the Swiss Franc, and industrial commodities may serve as a useful hedge for investors who are concerned about absolute return prospects in a world in which long-maturity bond yields are rising and risks of stagflationary dynamics are present. Chart II-1The Misery Index Reflects The Risk Of Stagflation

The Misery Index Reflects The Risk Of Stagflation

The Misery Index Reflects The Risk Of Stagflation

Over the past several weeks, concerns about a possible return to 1970s-style stagflation have re-emerged significantly in the minds of many investors. These investors have pointed toward similarities between the current environment and that of the 1970s, including shortages limiting output, a snarled global trade and logistical system, and rising energy prices. Chart II-1 highlights that the US “Misery Index” – the sum of the unemployment rate and headline PCE inflation – rose again over the past several months to high single-digit territory, after having fallen dramatically from April 2020 to February of this year. Panel 2 of Chart II-1 highlights that last year's rise in the Misery Index was driven almost entirely by the unemployment rate, whereas the current level is due to a combination of a modestly elevated unemployment rate and a pronounced acceleration in inflation. The headline PCE deflator has risen above 4%, a level that has not been reached since 1991 during the First Gulf War. In this report, we examine the risk of stagflation by comparing the current environment to that of the late 1960s and 1970s. We conclude that while investors cannot rule out the possibility of a stagflationary outcome, there are important differences that point toward a stagflation outcome over the coming 6-24 months as a risk, not a likely event. We conclude by highlighting assets that may produce absolute returns in a world in which long-maturity bond yields are rising and risks of stagflationary dynamics are present. Revisiting The 1960s And 70s Chart II-2The 1960s Laid The Groundwork For Elevated Inflation

The 1960s Laid The Groundwork For Elevated Inflation

The 1960s Laid The Groundwork For Elevated Inflation

The first step in judging the risk of a return to 1970s-style stagflation is to review, in a detailed way, what caused those conditions. Investors are well aware of the role that two separate energy price shocks played in raising prices and damaging output during this period, but they are less cognizant of the impact that a persistent period of above-trend output and significant labor market tightness had in setting up the conditions for sharply higher inflation. This focus of investors on energy prices partially reflects the fact that the Misery Index increased most visibly in the 1970s and that policymakers in the 1960s may not have realized how extensively economic output was running above its potential. With the benefit of hindsight, Chart II-2 illustrates the extent to which inflationary pressures built up in the 1960s, well before the first oil price shock in 1973. The chart shows that the unemployment rate was below NAIRU – the non-accelerating inflation rate of unemployment – for 70% of the time during the 1960s, and that inflation had already responded to this in the latter half of the decade. Annual headline PCE inflation was running just shy of 5% at the onset of the 1970 recession; it fell to 3% in the aftermath of the recession, but had already begun to reaccelerate in the first half of 1973. Following the 1973/1974 recession, inflation did decelerate significantly, falling from 11-12% to 5% in headline terms, and from 10% to 6% in core terms. But the pace of price appreciation did not fall below 5-6% in the second half of the 1970s, despite a significant and sustained rise in the unemployment rate above its natural rate. The 1975 to 1978 period is especially important for investors to understand, because it is arguably the clearest period of true stagflation in the 1970s. The fact that the Misery Index rose sharply during two major oil price shocks is not particularly surprising in and of itself, given the direct impact of energy prices on headline consumer prices; it is the fact that the index remained so elevated between these shocks, the result of persistently high inflation in the face of significant labor market slack, that is most relevant to investors. There are two reasons that both inflation and unemployment remained high during this period. First, labor market slack was sizeable during these years because the US economy was more energy-intensive in the 1970s than it is today. Chart II-3 highlights that goods-producing employment lagged overall employment growth from late 1973 to late 1977, underscoring that the rise in oil prices significantly impacted jobs growth in energy-intensive industries.

Chart II-3

Second, it is clear that the combination of demand-pull inflation in the late 1960s and the predominantly cost-push inflation of the 1970s led to expectations of persistent inflation among households and firms. The original Phillips Curve, as formulated by New Zealand economist William Phillips in the late 1950s, described a negative relationship between the unemployment rate and the pace of wage growth. Given the close correlation between wage and overall price growth at the time, the Phillips Curve was soon extended and generalized to describe an inverse relationship between labor market slack and overall price inflation. But the experience of the 1970s highlighted that inflation expectations are also an important determinant of inflation, a realization that gave birth to the expectations-augmented (i.e. “modern-day”) Phillips Curve (more on this below). The Stagflation Era Versus Today

Chart II-

Table II-1 presents a stagflation “threat matrix,” representing the Bank Credit Analyst service’s assessment of the various factors that could potentially contribute to a stagflationary environment today, relative to what occurred in the 1960s and 1970s. While we acknowledge that there are some similarities today to what occurred five decades ago, the most threatening factors have been present for a shorter period of time and appear to have a smaller magnitude than what occurred during the stagflationary era. In addition, key factors, such as the visibility available to policymakers and investors about household inflation expectations and the potential output of the economy, would appear to reduce significantly the risk of a stagflationary outcome today. We discuss each of the factors presented in Table II-1 below: Fiscal & Monetary Policy Chart II-4Government Spending Last Cycle Looked Nothing Like The 1960s

Government Spending Last Cycle Looked Nothing Like The 1960s

Government Spending Last Cycle Looked Nothing Like The 1960s

The persistently tight labor market that contributed to the inflationary buildup in the 1960s occurred as a result of easy fiscal and monetary policy. Chart II-4 highlights that the contribution to real GDP growth from government expenditure and investment was very elevated in the 1960s. Chart II-5 shows that a positive output gap in the late 1960s and the first half of the 1970s is well explained by the fact that 10-year US government bond yields were persistently below nominal GDP growth. The relationship between the stance of monetary policy and the output gap only meaningfully diverged in the latter half of the 1970s, during the true stagflationary era that we noted above. Chart II-5Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Chart II-6Monetary Policy Today Is Extremely Easy

Monetary Policy Today Is Extremely Easy

Monetary Policy Today Is Extremely Easy

Today, it is clear that the stance of fiscal policy has recently been extraordinarily easy, and 10-year US government bond yields have remained well below nominal GDP growth for the better part of the last decade. Relative to estimates of potential nominal GDP growth, 10-year Treasury yields are the lowest they have been since the 1970s (Chart II-6). Ostensibly, this supports concerns that policy might contribute to a stagflationary outcome. These concerns were raised by Larry Summers in March, when he described the Biden administration’s fiscal policy as the “least responsible” that the US has experienced in four decades and warned of the potential inflationary consequences of overheating the economy.1 But there are two important counterpoints to these concerns. First, easy fiscal policy this cycle has followed a period during the last economic cycle in which government spending contributed to the most sustained drag on economic activity since the 1950s. Unlike the 1960s, the unemployment rate has been below NAIRU for only a third of the time over the past decade. In addition, Chart II-7 highlights that fiscal thrust will turn to fiscal drag next year, underscoring the temporary nature of the massive burst in fiscal spending that has occurred in response to the pandemic. Under normal circumstances, the fiscal drag implied by Chart II-7 would substantially raise the risks of a recession next year, but we have noted in previous reports that a significant amount of excess savings remain to support spending and employment. The net impact of these two factors results in a reasonable expectation that the US economy will return to maximum employment next year, but this is a far cry from the 1960s when the unemployment rate was below its natural rate for 70% of the decade.

Chart II-7

Based on conventional measures, US monetary policy has been easy for a decade, but easy monetary policy did not begin to contribute positively to a rise in household sector credit growth last cycle until 2014/2015. This underscores that the natural rate of interest (“R-star”) did fall during the early phase of the last economic expansion. However, we argued in an April report that R-star was likely rising in the latter half of the last expansion,2 and we believe that the terminal Fed funds rate is likely higher than what the Fed is currently projecting, barring any additional negative policy shocks. Thus, while we do not believe that the duration of easy monetary policy over the past decade has laid the groundwork for a major rise in prices, it is now clearly positively contributing to aggregate demand and does risk a future overshoot in prices if long maturity bond yields remain well below the pace of economic growth for a sustained period of time. The Impact Of Shortages Chart II-8Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline shortages occurred during the oil shocks of the 1970s and are a key similarity that some investors point toward when comparing the situation today with the stagflationary era. Chart II-8 highlights that the annual growth in real personal consumption expenditures on energy goods and services fell into negative territory on six occasions in the 1970s, although it was most pronounced during the two oil price shocks and their resulting recessions. Today, the impact of shortages appears to be broader than what occurred in the 1970s, but less impactful and not likely to be as long-lasting. Chart II-9 highlights that the OPEC oil embargo of 1973 raised the global oil bill by 2.4% of global GDP and permanently raised the price of oil. The global oil bill will only be fractionally above its pre-pandemic level in 2022, with oil prices at $80/bbl, and, while it is true that US gasoline prices have risen significantly, they are not higher than they were from 2011-2014 (Chart II-10). Chart II-9$80/bbl Oil Is Not Onerous

$80/bbl Oil Is Not Onerous

$80/bbl Oil Is Not Onerous

Chart II-10US Gasoline Prices Are High, But They Have Been Higher

US Gasoline Prices Are High, But They Have Been Higher

US Gasoline Prices Are High, But They Have Been Higher

It is certainly true that global shipping costs have skyrocketed and that this is contributing to the increase in US consumer prices. We estimate, however, that this increase in shipping costs as a share of GDP is no more than a quarter of the impact of the 1973 increase in oil prices, without the attendant negative effects on US goods-producing employment that occurred in the 1970s. If anything, surging shipping costs create an incentive to re-shore manufacturing production, which would contribute positively to US goods-producing employment. We also do not expect the rise in shipping costs to be meaningfully permanent, i.e., shipping costs may ultimately settle at a higher level than they were in late-2019, but at a much lower level than what prevails today. Chart II-11A Tight Labor Market Is Causing Wage Growth To Pick Up

A Tight Labor Market Is Causing Wage Growth To Pick Up

A Tight Labor Market Is Causing Wage Growth To Pick Up