Inflation/Deflation

Dear Client, I will be holding a webcast next Friday, September 24th at 10:00 AM EDT (3:00 PM BST, 4:00 PM CEST, 11:00 PM HKT) with BCA Research’s Chief Emerging Markets Strategist Arthur Budaghyan where we will debate the outlook for EM stocks. As this week’s report conveys, I am bullish, while Arthur is in the bearish camp. Please join us for what is sure to be a fiery debate. Also, instead of our regular report next week, we will be sending you a Special Report written by Matt Gertken, BCA Research’s Chief Geopolitical Strategist, discussing the stability of the American political system. I hope you will find it insightful. We will be back the following week with the GIS Quarterly Strategy Outlook, where we will explore the major trends that are set to drive financial markets in the rest of 2021 and beyond. As always, I will hold a webcast discussing the outlook the week after, on Thursday, October 7th. Best regards, Peter Berezin Chief Global Strategist Highlights After lagging the global indices, EM stocks are set to outperform during the remainder of this year and into 2022. Go long the EM FTSE index versus the global benchmark (ETF proxy: VWO versus VT). Five factors will support EM assets over the coming months: 1) The vaccination campaign in emerging markets is in full swing; 2) Domestic EM inflation will crest; 3) China will stimulate its economy; 4) The US dollar will weaken; and 5) EM valuations have discounted a lot of bad news. Contrary to popular perception, the Chinese government has not launched an indiscriminate attack on tech companies. If anything, heightened geopolitical tensions have made it more important than ever for China to buttress its tech sector. Investors wanting to gain exposure to Chinese tech while still limiting risk should consider writing cash-covered puts. For example, a strategy of selling puts on Alibaba could generate a 9% annualized yield while giving investors access to the stock at a forward PE ratio of only 12.5. Go long an equally-weighted basket consisting of the Russian ruble and Brazilian real against the US dollar. Both currencies enjoy favorable interest rate differentials and will benefit from continued strength in commodity markets. Debating The EM Outlook BCA Research has some of the brightest, most creative strategists in the world. While we often agree on many issues, we sometimes disagree. The near-term outlook for emerging markets is a case in point. My colleague, Chief EM Strategist Arthur Budaghyan, is bearish on emerging markets over a 3-to-6 month horizon. In contrast, I am bullish. In this note, I explain why. I see five reasons why EM assets will do very well during the remainder of the year and into 2022: 1) The vaccination campaign in emerging markets is in full swing; 2) Domestic EM inflation will crest; 3) China will stimulate its economy; 4) The US dollar will weaken; and 5) EM valuations have discounted a lot of bad news. Let’s examine all five reasons in turn. Vaccine Access In Emerging Markets Is Improving The proportion of EM populations which have been vaccinated is rising rapidly (Chart 1). India is now vaccinating 10 million people per day, a number that would have seemed unimaginable just a few months ago. Chart 1EM Vaccination Rates Have Been Ramping Up Rapidly

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

Globally, about 10 billion doses of vaccine will be produced this year (Chart 2). This does not include potential new mRNA vaccines that China is developing. China-based Walvax Biotechnology is conducting late-stage trials in Nepal, with mass production of the vaccine expected to start in October. Sinopharm is also working on its own mRNA vaccine. Meanwhile, the number of new Covid cases in most EM economies has peaked, permitting a relaxation of lockdown measures (Chart 3). Goldman’s Effective Lockdown Index for China has eased significantly since mid-August, although this week’s outbreak in Fujian province could partially reverse that trend. Chart 2At Least 10 Billion Doses Of Vaccine Will Be Produced This Year

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

Chart 3EM Lockdown Measures Have Eased As The Number Of New Cases Has Peaked

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

It is true, as Arthur has pointed out, that vaccine hesitancy is a problem in some emerging markets. However, this may not be as significant an issue as previously believed. The huge spike in cases in highly vaccinated countries such as Israel and the UK shows that herd immunity is a pipe dream. Given this reality, as long as everyone who wants a vaccine is able to receive it, the political pressure to maintain lockdowns will dissipate. Pandemic-Induced Spike In Inflation Is Fading As in most developed economies, many emerging markets have experienced a post-pandemic rise in inflation (Chart 4). Whereas DM central banks generally looked through the inflation spike, many EMs did not have that luxury. Chart 4Inflation Across The EM Universe

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

Worried about an unmooring of inflation expectations and currency depreciation, central banks in such countries as Brazil, Mexico, Chile, Colombia, Peru, Russia, and Turkey have all raised rates this year. Higher rates have weighed on EM growth and financial markets. The good news is that inflationary pressures are starting to abate. This week’s US CPI report for August showed an absolute decline in prices in pandemic-related categories such as airfares, hotels, admissions, and vehicles (Chart 5). Things are even improving on the semiconductor front. Chart 6 shows that memory chip prices are in a clear downtrend. Chart 5Pandemic-Driven Inflation Is Cresting

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

Chart 6Chip Prices Are Off Their Highs

Chip Prices Are Off Their Highs

Chip Prices Are Off Their Highs

Chart 7Agricultural Prices Have Stabilized, Which Will Help Cool EM Inflation

Agricultural Prices Have Stabilized, Which Will Help Cool EM Inflation

Agricultural Prices Have Stabilized, Which Will Help Cool EM Inflation

Critically for emerging markets, agricultural prices have stabilized (Chart 7). Historically, food inflation has been a major driver of EM inflation. Chinese Stimulus On The Way Growth in China was quite weak in the first half of the year, averaging only 3.5% on a sequential annualized basis (Chart 8). The Bloomberg consensus estimate is for Q3 growth to hit 4.3%, reflecting the negative impact of lockdown measures and the lagged effect from policy tightening. Growth in the fourth quarter is expected to rebound to only 5.7%. This seems too low to us. Barring a major spike in Covid cases, Chinese industry will be saddled with fewer social distancing restrictions in the fourth quarter. Policy is also turning more stimulative. The PBOC cut bank reserve requirements in July. In the past, cuts in reserve requirements have been a reliable predictor of faster credit growth (Chart 9). Chart 8Chinese Growth Should Accelerate After A Disappointing First Half Of 2021

Chinese Growth Should Accelerate After A Disappointing First Half Of 2021

Chinese Growth Should Accelerate After A Disappointing First Half Of 2021

Chart 9Chinese Stimulus Is On The Way

Chinese Stimulus Is On The Way

Chinese Stimulus Is On The Way

With credit growth back to its 2018 lows, there is little need for further actions to reduce lending. On the contrary, the PBOC’s meeting with financial institutions on August 23rd revealed a desire to increase credit availability. Partly reflecting this development, new bank loans rose to RMB 1.22 trillion in August, up from RMB 1.08 trillion in the prior month. Chart 10EM Stocks Have Done Well When Global Industrial Stocks Have Outperformed

EM Stocks Have Done Well When Global Industrial Stocks Have Outperformed

EM Stocks Have Done Well When Global Industrial Stocks Have Outperformed

On the fiscal side, the Ministry of Finance stated on August 27th its intention to ramp up fiscal spending by increasing local government bond issuance. As of the end of August, local governments had used up only 50% of their annual debt issuance quota, compared to 77% at the same time last year and 93% in 2019. To reinforce the need for more stimulus, the authorities announced an additional RMB 300 billion in credit support for SMEs during the latest State Council meeting held on September 1st. Local Chinese government spending has typically flowed into infrastructure. Increased infrastructure spending should buttress metals prices while providing a tailwind for global industrial stocks. I agree with Arthur’s assessment that industrials will be a winning equity sector over the coming years. EM stocks have usually beaten the global benchmark during periods when global industrial stocks were outperforming (Chart 10). A Weaker US Dollar Will Benefit Emerging Markets EM stocks tend to perform best when the US dollar is on the back foot (Chart 11). We expect the greenback to weaken over the next 12 months. As a countercyclical currency, the dollar is likely to struggle in an environment of above-trend global growth (Chart 12). Chart 11EM Stocks Tend To Outperform The Global Benchmark When The Dollar Is Weakening

EM Stocks Tend To Outperform The Global Benchmark When The Dollar Is Weakening

EM Stocks Tend To Outperform The Global Benchmark When The Dollar Is Weakening

Chart 12The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Interest rate differentials have moved sharply against the dollar (Chart 13). The US trade deficit has surged over the past 16 months. The way the US has been financing its trade deficit – relying heavily on fickle equity inflows – also leaves the dollar in a vulnerable position (Chart 14). Chart 13Interest Rate Differentials Have Moved Against The Dollar

Interest Rate Differentials Have Moved Against The Dollar

Interest Rate Differentials Have Moved Against The Dollar

Chart 14Volatile Equity Inflows Have Been Financing The US Trade Deficit, Putting The Dollar In A Vulnerable Position

Volatile Equity Inflows Have Been Financing The US Trade Deficit, Putting The Dollar In A Vulnerable Position

Volatile Equity Inflows Have Been Financing The US Trade Deficit, Putting The Dollar In A Vulnerable Position

Go Long BRL And RUB Against a backdrop of broad-based dollar weakness, EM currencies will strengthen. Currently, the 12-month interest rate differential between Brazil and the US stands at 8.7%, up from a low of 2.1% last year. Russian rates have also risen rapidly relative to US rates (Chart 15). The Russian ruble will benefit from the cyclical recovery in oil prices. Bob Ryan and BCA’s commodity team project that the price of Brent will rise 5% to $80/bbl in 2023, whereas market expectations are for a 12% decline (Chart 16). Likewise, Brazil will gain from both higher oil prices and rising Chinese demand for metals. Chart 15Interest Rate Differentials Favor The RUB And BRL Versus The USD

Interest Rate Differentials Favor The RUB And BRL Versus The USD

Interest Rate Differentials Favor The RUB And BRL Versus The USD

Chart 16Oil Prices Have More Upside

Oil Prices Have More Upside

Oil Prices Have More Upside

Accordingly, we are initiating a new trade going long an equally-weighted basket consisting of BRL/USD and RUB/USD. Are EMs A Value Trap? Emerging market stocks currently trade at a Shiller PE ratio of 14.7, compared to 36.8 for the US, 22.2 for Europe, and 24.1 for Japan. The EM discount to the global index is as large now as it was during the late 1990s. Other valuation measures tell a similar story (Chart 17). Chart 17AEM Equities Are Trading At A Large Discount (I)

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

Chart 17BEM Equities Are Trading At A Large Discount (II)

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

A low PE ratio for EM stocks could be justified based on weak expected earnings growth. However, it is far from clear that such an expectation is warranted. While EM earnings growth has lagged the US since 2011, this follows a decade when EM earnings grew much faster than in the US (Chart 18). Chart 18AEM Earnings Have Moved Sideways Since 2011 After Blazing Higher Over The Preceding Decade (I)

EM Earnings Have Moved Sideways Since 2011 After Blazing Higher Over The Preceding Decade (I)

EM Earnings Have Moved Sideways Since 2011 After Blazing Higher Over The Preceding Decade (I)

Chart 18BEM Earnings Have Moved Sideways Since 2011 After Blazing Higher Over The Preceding Decade (II)

EM Earnings Have Moved Sideways Since 2011 After Blazing Higher Over The Preceding Decade (II)

EM Earnings Have Moved Sideways Since 2011 After Blazing Higher Over The Preceding Decade (II)

Chart 19EM Stocks Underperformed Their US Peers By More Than What Is Suggested By Earnings

EM Stocks Underperformed Their US Peers By More Than What Is Suggested By Earnings

EM Stocks Underperformed Their US Peers By More Than What Is Suggested By Earnings

On that note, it is worth mentioning that US earnings have risen by only 6 percentage points more than EM earnings since mid 2019 (20% versus 14%), even as EM stocks have underperformed their US peers by 29% over this period (52% versus 23%) (Chart 19). China’s Regulatory Crackdown The regulatory crackdown on Chinese tech companies has weighed on the sector. Chinese tech stocks have underperformed their global tech peers by 48% since February (Chart 20). Chart 20Chinese Tech Stocks Have Been Underperforming Their Global Tech Peers

Chinese Tech Stocks Have Been Underperforming Their Global Tech Peers

Chinese Tech Stocks Have Been Underperforming Their Global Tech Peers

Chinese tech is 44% of the China investable index and 15% of the MSCI EM index. Thus, the outlook for Chinese stocks is relevant not just for China-focused investors, but for EM investors more broadly (especially those who invest in index products). The current crackdown bears some resemblance to the one in 2018, which saw Tencent lose $20 billion in market capitalization in a single day. Like other Chinese tech names, Tencent shares quickly recovered from that incident. Contrary to popular perception, the Chinese government has not launched an indiscriminate attack on tech companies. If anything, heightened geopolitical tensions have made it more important than ever for China to buttress its tech sector. Rather, what the government has done is restrain companies that it either perceives as working against the national interest (i.e., addictive video game makers and expensive after-school tutoring companies) or that have too much sway over the public. Private tech companies in sectors such as semiconductors or clean energy continue to receive government support. A plausible outcome is that China’s leading consumer-oriented internet companies will go out of their way to pledge allegiance to the Communist Party just as US companies have pledged allegiance to woke ideology. If that were to happen, the Chinese government may allow them to operate normally, cognizant of the fact that it is easier to monitor a few large internet companies than many small ones. While such an outcome is far from assured, current valuations offer enough cushion to prospective investors. As we go to press, Alibaba is trading at 16.4-times earnings, Baidu is trading at 17.9-times earnings, and Tencent is trading at 26.7-times current year earnings. In comparison, the NASDAQ 100 trades at nearly 30-times earnings. Investment Conclusions Sentiment towards EM stocks is very bearish (Chart 21). Investor angst towards China is especially elevated, with the media replete with stories about the tech crackdown and problems at Evergrande, the country’s largest property developer. Chart 21Sentiment Towards EM Stocks Is Highly Bearish

Sentiment Towards EM Stocks Is Highly Bearish

Sentiment Towards EM Stocks Is Highly Bearish

All these downside risks to EM assets are well known. What are less well known are the upside risks stemming from higher vaccination rates, an easing of domestic inflationary pressures, Chinese stimulus, a weaker US dollar, and favorable valuations. With that in mind, we are upgrading our rating on EM equities and currencies to strong overweight in the view matrix at the back of this report. We are also reinstating a long EM/Global equity trade (ETF proxy: VWO versus VT). The risk-reward of buying Chinese internet stocks is reasonably appealing. Investors who want to mitigate risk should consider writing cash-covered puts. For example, a BABA put with a strike price of $130 expiring on December 16th 2022 trades for about $16. If the price of BABA does not fall below $130, you will pocket the premium, realizing an annualized yield of 9%. If the price does fall to $130, you get the stock at an attractive PE ratio of 12.5 based on current forward earnings estimates. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Global Investment Strategy View Matrix

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

Special Trade Recommendations

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

Current MacroQuant Model Scores

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

The Best Trade For The Rest Of 2021: Long EM Equities And Currencies

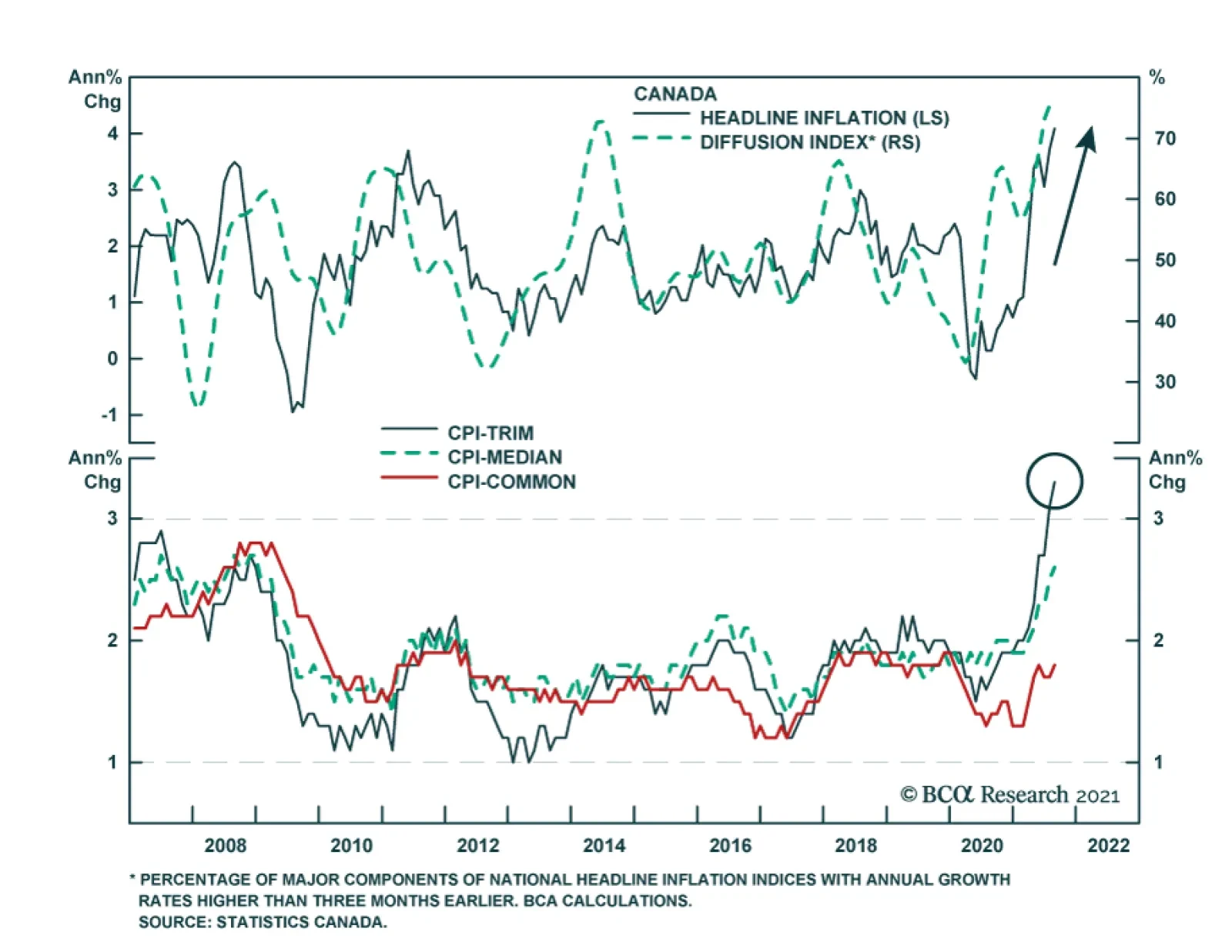

Inflationary pressures are likely to keep the Bank of Canada at least as hawkish - if not more hawkish - than the Fed. Headline CPI accelerated to a 18-year high of 4.1% y/y in August. The diffusion index's extremely elevated reading is in line with…

Dear Client, Next week, in lieu of our regular weekly report, I will be hosting two webcasts where I will discuss our view on China’s economy and financial markets. I will also address the topics that our clients are most concerned about, including China’s regulatory developments, inflation, and policy direction. The webcasts will be held on Wednesday, September 22 at 10:00 am EDT (English), and Thursday, September 23 at 9:00 am HKT (Mandarin). I look forward to discussing with you during the webcast. We will return to our regular publishing schedule on Wednesday, September 29. Best regards, Jing Sima, China Strategist Highlights China is facing cyclical inflationary pressures more than disinflationary ones. Prices of mining, raw materials and manufacturing goods have been rising at record rates. Chinese manufacturers are operating at close to full production, which suggests that there is little slack in demand. Despite soft headline readings in consumer prices, the costs of goods and services have rebounded to pre-pandemic levels. Prices for home durable goods, fuel and utilities have surged to multiyear highs. Measures to boost domestic demand will be limited as long as inflationary pressures continue and manufacturers produce at close to full capacity. Near-term policy support will likely focus on reducing costs for manufacturers and improving wage growth for lower-income households. We are initiating a trade: long industrial stocks/short A-shares. Feature China’s Producer Price index (PPI) registered a 13-year high in August, at the time when the domestic economy continued to slow. On the other hand, consumer prices (CPI) - both headline and core CPI - have been lackluster. The acceleration in producer inflation and the demand dynamics raise the question whether China is in a stagflation, a situation in which prices climb but wages and demand do not follow. Consequentially, economy policy faces a dilemma between boosting demand and containing inflation. Inflationary pressures have been driven by pandemic-related factors and the supply-side constraints will likely continue into Q1 next year. These inflationary pressures, and more importantly, undercurrents in the inflation prints, will constrain Chinese policymakers’ efforts to reflate the economy. The recent rebound in Chinese infrastructure stocks is overdone. Material stocks are also vulnerable to price setbacks. Global commodity prices will soften, although from very elevated levels. Meanwhile, we are initiating a trade: long Chinese industrial stocks relative to the A-share market. Despite falling profit growth in recent months, China’s leadership is increasing its support, both cyclically and structurally, to the manufacturing sector. Inflation Or Deflation? The details in both the PPI and CPI readings indicate that China is facing more inflationary pressures than disinflationary ones. Producers are raising prices across the board. Although consumer prices will likely remain well below the PBoC's 3% inflation target for the year mainly due to low food prices, prices in some of the key consumer goods segments are rising at an alarming pace. The inflationary pressures will continue for producers, at least through the first quarter of 2022. The strength in August’s PPI was concentrated in mining and raw materials (Chart 1, top panel). Robust global demand and tight supply conditions supported high oil and base metals prices, while pushing up coal prices. Chart 1Chinese Mining And Manufacturing Goods Prices Accelerated To Record Highs

Chinese Mining And Manufacturing Goods Prices Accelerated To Record Highs

Chinese Mining And Manufacturing Goods Prices Accelerated To Record Highs

Chart 2Commodity Prices Held Up Despite A Slowing China

Commodity Prices Held Up Despite A Slowing China

Commodity Prices Held Up Despite A Slowing China

We do not expect China’s infrastructure investment growth to pick up and support industrial metal prices. However, this year’s unsynchronized recovery in global demand and severe supply shortages have delayed the global commodity market’s price reaction to slowing Chinese demand (Chart 2). Moreover, as China’s environmental policy remains stringent during the upcoming winter, supply-side constraints from production cuts will partially offset the slowdown in China’s demand for mining and raw materials (Chart 3A and 3B). Chart 3ASupply-Side Constraints And Chinese Production Cuts Likely To Continue Into Early 2022

Supply-Side Constraints And Chinese Production Cuts Likely To Continue Into Early 2022

Supply-Side Constraints And Chinese Production Cuts Likely To Continue Into Early 2022

Chart 3BSupply-Side Constraints And Chinese Production Cuts Likely To Continue Into Early 2022

Supply-Side Constraints And Chinese Production Cuts Likely To Continue Into Early 2022

Supply-Side Constraints And Chinese Production Cuts Likely To Continue Into Early 2022

Manufacturing goods inflation registered its topmost annual growth since data collection started in 1996 (Chart 1, bottom panel). Moreover, capacity utilization rates in the industrial and manufacturing sectors are at the highest levels since 2007, well above their means (Chart 4). Changes in manufacturing capacity are highly correlated with China’s export growth and tightly linked to PPI (Chart 5). Therefore, manufacturing goods prices will remain lofty as long as external demand stays robust and China’s manufacturers continue to produce near maximum output. Chart 4Chinese Manufacturers Are Producing Near Their Max Capacity

Chinese Manufacturers Are Producing Near Their Max Capacity

Chinese Manufacturers Are Producing Near Their Max Capacity

Chart 5Robust Exports Have Been Supporting Strong Chinese Manufacturing Output

Robust Exports Have Been Supporting Strong Chinese Manufacturing Output

Robust Exports Have Been Supporting Strong Chinese Manufacturing Output

The PPI’s weakest component has been consumer goods, which inched up by a mere 0.3% from a year ago (Chart 6). However, consumer goods only account for 25% of PPI, whereas industrial and manufacturing producer goods are 75%. In addition, the underlying data shows that among the four sub-components in the PPI’s consumer goods, only food prices have remained below their pre-pandemic levels (Chart 7, top panel). Prices in durable goods have rebounded strongly since March last year and clothing and daily sundry articles have recovered to their end-2019 rate of growth (Chart 7, mid and bottom panels). Chart 6Producer Prices For Consumer Goods Remain Soft...

Producer Prices For Consumer Goods Remain Soft...

Producer Prices For Consumer Goods Remain Soft...

Chart 7...But Food Prices Have Been The Main Drag

...But Food Prices Have Been The Main Drag

...But Food Prices Have Been The Main Drag

The PPI’s price forces are consistent with the CPI, in which food has been the main drag. Core CPI, along with prices for consumer goods and services, have returned to pre-pandemic growth rates (Chart 8). Durable goods prices, such as home appliances, increased to a multiyear high in August. Fuel and utilities costs have also risen. This suggests that despite the soft CPI readings, inflation has flowed from producers to Chinese consumers through manufacturing goods. The passthrough will likely intensify into Q4 when domestic COVID-cases have been largely brought under control and the September – October holiday season will boost consumption for both goods and services. Chart 8Prices For Other Consumer Goods Categories Have Recovered

Prices For Other Consumer Goods Categories Have Recovered

Prices For Other Consumer Goods Categories Have Recovered

Table 1A Look At China’s CPI Basket – Food Dominates

Inflation, Deflation, Or Stagflation?

Inflation, Deflation, Or Stagflation?

We still expect that headline CPI will remain below the PBoC’s 3% inflation target for the year. Consumer durable goods prices are lightly weighted in China’s CPI, therefore, an acceleration in inflation passthroughs in this component is unlikely to significantly push up the CPI aggregates (Table 1). Chart 9Prices For Healthcare And Education Services On A Structural Downshift

Prices For Healthcare And Education Services On A Structural Downshift

Prices For Healthcare And Education Services On A Structural Downshift

In addition, there are some structural headwinds that will affect prices in the education and healthcare and medical services components, which together account for about 15% of the CPI. Healthcare prices have been on a policy-driven structural downshift since late 2017 and recent regulatory changes in the education industry will depress pricing power in that sector (Chart 9). Despite sluggish aggregate consumer prices, climbing prices in consumer durable goods, services and particularly, fuel and utilities, will likely force China’s leadership to take action on policy. Bottom Line: Price pressures for Chinese producers remain intense and consumers will feel the heat of escalating prices in durable goods, fuel and utilities. Inflation is threatening domestic demand, which is already slowing from its peak earlier this year. Implications On Policy Response Inflation readings –even though they are lagging economic indicators –bear significant forward-looking market implications because changes in inflation dynamics herald various policy responses. Despite slower economic growth, higher inflation coupled with accommodative monetary and fiscal policies may indicate that the economy is in a “goldilocks” stage and corporate profits can still benefit (Chart 10). Chinese onshore stocks reached record high recently (Chart 11). Chart 10Are Chinese Corporates In A 'Sweet Spot'?

Are Chinese Corporates In A 'Sweet Spot'?

Are Chinese Corporates In A 'Sweet Spot'?

Chart 11Accommodative Monetary Conditions Propelled Chinese Stock Prices To Highest Since 2015

Accommodative Monetary Conditions Propelled Chinese Stock Prices To Highest Since 2015

Accommodative Monetary Conditions Propelled Chinese Stock Prices To Highest Since 2015

However, underlying trends in China’s producer and consumer inflation prints raise the risks that policymakers may not deliver the ingredients needed for a “just right” scenario. Even though China has kept a loose monetary policy that we expect to extend into next year, inflationary pressures may force policymakers to either delay or reduce the magnitude of stimulus. Recent policy moves show that the authorities are focused on reducing input cost burdens and bumping up support for small- and medium-sized enterprises (SMEs), which are highly concentrated in mid- to downstream manufacturing and services sectors. In our view, the recent rhetoric from policymakers further reduces the odds of any broadly based stimulus to boost demand. Our view is based on the following observations: The elevated global input costs and limited price passthroughs to consumers are depressing Chinese manufacturers’ profit margins and incentives to expand production capacity. Despite strong exports and production, manufacturing investment has lagged that in infrastructure and real estate this year (Chart 12). Consumers, particularly lower-income households, are bearing most of the burdens; rising costs and slow wage growth are weakening their propensity to spend (Chart 13). Chart 12Slower Manufacturing Investment Recovery Than Infrastructure And Real Estate So Far This Year

Slower Manufacturing Investment Recovery Than Infrastructure And Real Estate So Far This Year

Slower Manufacturing Investment Recovery Than Infrastructure And Real Estate So Far This Year

Chart 13Slow Wage Growth Limits The Pace Of Consumption Recovery

Slow Wage Growth Limits The Pace Of Consumption Recovery

Slow Wage Growth Limits The Pace Of Consumption Recovery

The inflation prints came at the time when China’s top leadership shifted its structural policy goals to reduce income inequality and stabilize manufacturing share in the aggregate economy. The structural goals will likely be reflected in policy responses to the cyclical challenge. Moreover, this year’s manufacturing production volume was growing twice as fast as producer prices, a reversal from 2017 when price increases outpaced production (Chart 14). Price changes are much more important to corporate profits than volume changes. A strong RMB and sharply escalating shipping costs have also reduced exporters’ pricing power and profits (Chart 15). In contrast, mounting prices across various commodities have allowed the upstream industrial sectors, which are dominated by SOEs, to deliver much stronger profits than the downstream and private sector (Chart 16). Chart 14Growth In Manufacturing Output And Prices Starting To Converge

Growth In Manufacturing Output And Prices Starting To Converge

Growth In Manufacturing Output And Prices Starting To Converge

Chart 15Strong RMB And Rising Shipping Costs Have Reduced Chinese Exporters' Profitability

Strong RMB And Rising Shipping Costs Have Reduced Chinese Exporters' Profitability

Strong RMB And Rising Shipping Costs Have Reduced Chinese Exporters' Profitability

It is unsurprising that authorities are increasing support to the private sector in order to maintain manufacturing share in the economy and keep the export sector competitive (Chart 17). A boost in infrastructure investment, on the other hand, would exacerbate upward pressure on commodity prices and mostly benefit upstream SOEs. Chart 16Upstream Industries Disproportionally Benefited From Surging Commodity Prices

Upstream Industries Disproportionally Benefited From Surging Commodity Prices

Upstream Industries Disproportionally Benefited From Surging Commodity Prices

Chart 17Private Sector: Lower Profit Margin, Higher Costs

Private Sector: Lower Profit Margin, Higher Costs

Private Sector: Lower Profit Margin, Higher Costs

Furthermore, stimulating the traditional sectors would not revive household consumption. The subdued recovery in consumption and prices for consumer staple goods is due to slow growth in lower-income household wages and a disrupted recovery in the services sector. Ramping up infrastructure investment can support headline GDP growth, but will do little to provide jobs and wages since China’s private sector provides 80% of all jobs and 90% of annual job creations. Lower-income households have a higher marginal propensity to consume. We expect the government to accelerate fiscal support measures to fortify wages among lower-income households. Bottom Line: Ongoing inflationary pressures and the underlying forces will likely thwart policymakers from stepping up their efforts to stimulate the old economy sectors. Investment Conclusions Chart 18Rebound In Infrastructure Stocks Should Be Short-Lived

Rebound In Infrastructure Stocks Should Be Short-Lived

Rebound In Infrastructure Stocks Should Be Short-Lived

Chinese onshore stocks in the infrastructure, materials, and industrial sectors recently advanced strongly in the expectation that policymakers will ramp up their fiscal support in the old economy sectors, particularly infrastructure. Although we agree that infrastructure investment will improve, we maintain our view that a sizable rebound is highly unlikely this year. Hence, we do not expect that the rally in infrastructure stocks will be long-lasting (Chart 18). We are probably too late in the cycle to re-initiate our long material/broad market trade in the onshore and offshore equity markets (Chart 19). We closed the trade in December last year when Chinese policymakers started pulling back stimulus, and in expectations that raw material prices would tumble. However, we underestimated the intensity of China’s de-carbonization efforts and protracted global supply-side constraints. Although global commodity prices will remain elevated into 2022, the price rallies from this year are not sustainable on a cyclical (6- to 12-month) basis. Therefore, we do not recommend material stocks as a cyclical play. Chart 19Price Rally In Materials Stocks Unlikely To Sustain

Price Rally In Materials Stocks Unlikely To Sustain

Price Rally In Materials Stocks Unlikely To Sustain

Chart 20Industrial Stocks May Be On A Structural Upcycle

Industrial Stocks May Be On A Structural Upcycle

Industrial Stocks May Be On A Structural Upcycle

Instead, we recommend a long industrial/broad A-share market trade (Chart 20). Even though China is in a late business cycle and the upcoming stimulus will be mediocre at best, we think that the industrial sector will benefit from policy support for investment in the manufacturing sector and a faster pace in the sector’s capacity expansion. Jing Sima China Strategist jings@bcaresearch.com Footnotes Market/Sector Recommendations Cyclical Investment Stance

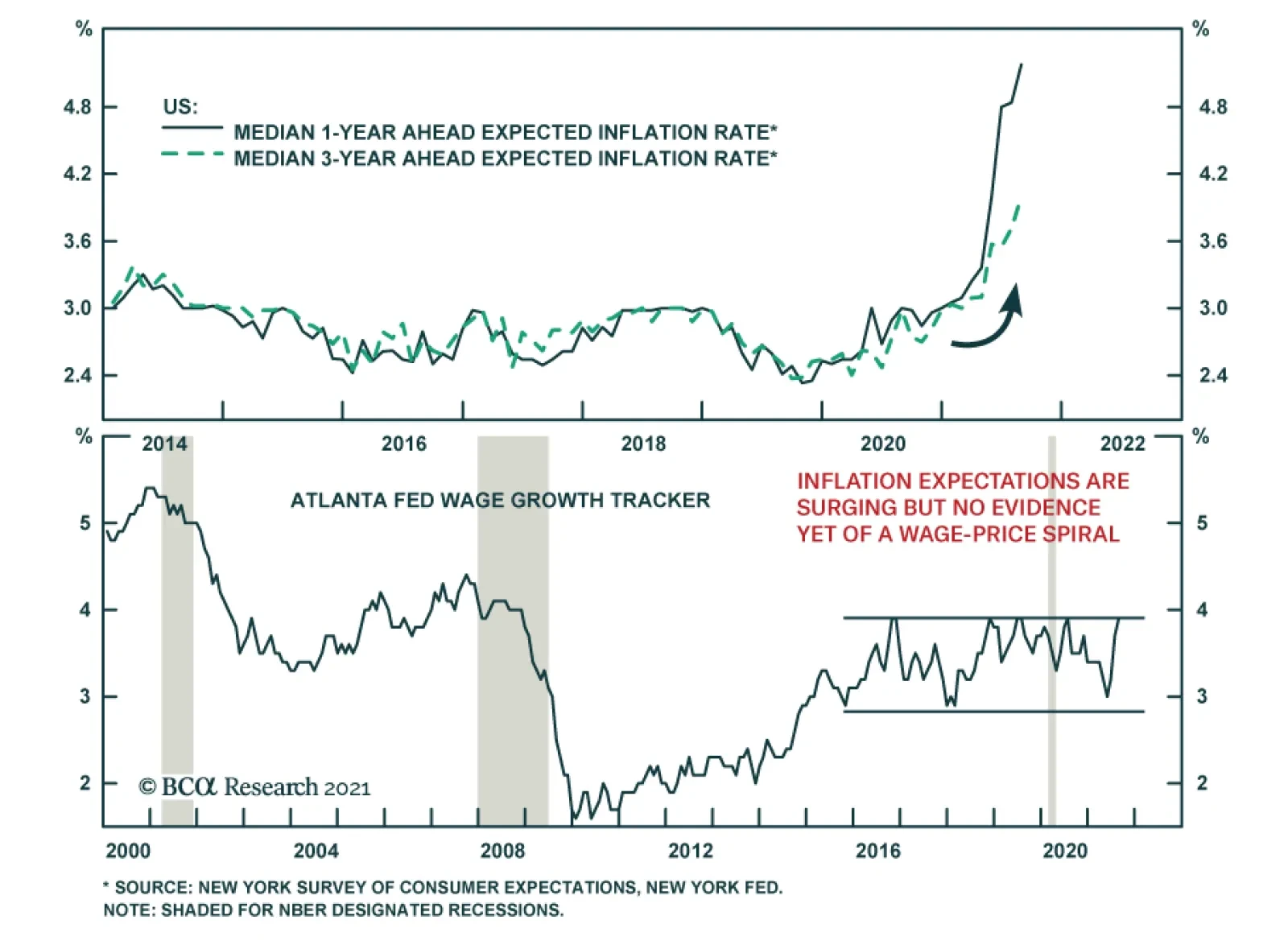

According to the New York Fed’s Survey of Consumer Expectations, the median 1-year ahead and 3-year ahead expected inflation rates rose to fresh series highs in August. Survey respondents expect the inflation rate to be 5.2% in a year’s time and ease to a…

BCA Research’s US Bond Strategy service expects employment data to take a back seat to the inflation data in the minds of bond investors in 2022. The Fed has successfully convinced markets that it will not lift rates until “maximum employment” is achieved,…

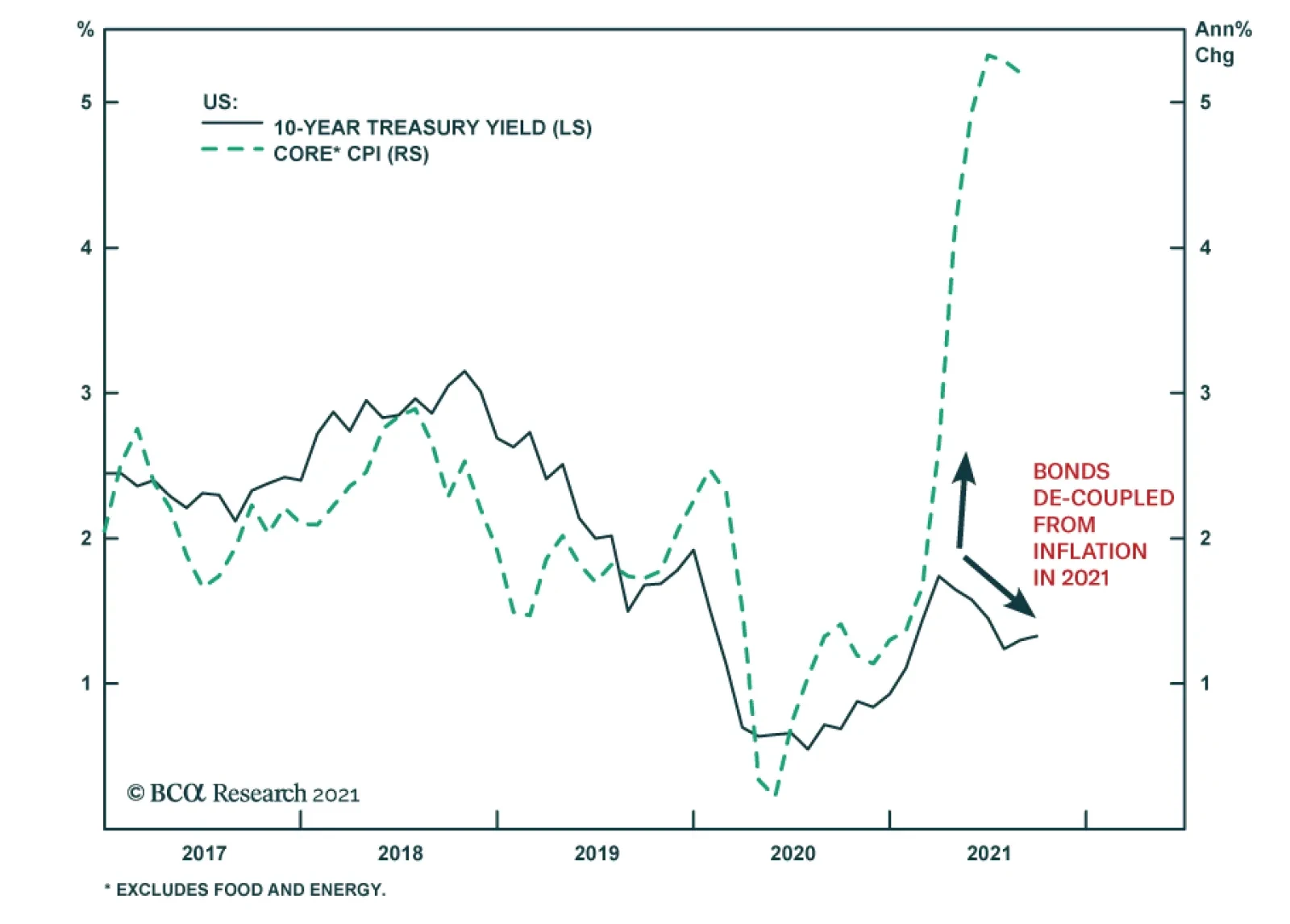

Highlights Fed: The Fed will be forced to clarify its definition of “maximum employment” in 2022, and the path of inflation will ultimately dictate how far the Fed tries to push the labor market. We expect Fed rate hikes to start in December 2022 and that the pace of hikes will proceed more quickly than is currently priced in the yield curve. Duration: Investors should maintain below-benchmark portfolio duration in anticipation of a rate hike cycle starting in December 2022. Yield Curve: Investors should position in Treasury curve flatteners. Specifically, we recommend shorting the 5-year Treasury note versus a duration-matched barbell consisting of the 2-year and 10-year notes. Feature Chart 1Bonds De-Coupled From Inflation In 2021

Bonds De-Coupled From Inflation In 2021

Bonds De-Coupled From Inflation In 2021

One of our themes this year is that US bond investors should pay more attention to the employment data than the inflation data.1 This is because the Fed has successfully convinced markets that it will not lift rates until “maximum employment” is achieved, even if inflation is strong.2 This story has played out during the past few months as bond yields have remained low despite surging prices (Chart 1). Our view is that the muted reaction in bonds is due to the widespread belief that the labor market remains far from “maximum employment” and that rate hikes are therefore a long way off. In this environment, only surprisingly strong employment prints can upset the market’s narrative and send bond yields higher. This playbook for the bond market will continue to function for the next few months. Strong employment data will pull bond yields higher and disappointing employment data will push them down. Inflation prints will be largely irrelevant for the market. But this will change next year. In fact, we see the employment data taking a back seat to the inflation data in the minds of bond investors in 2022. A More Explicit Definition of “Maximum Employment” Must Emerge In 2022 Almost everyone agrees that the US labor market is far from “maximum employment” today, but that will no longer be the case in 2022. The Appendix to this report shows the average monthly nonfarm payroll growth that is required to reach different possible definitions of “maximum employment” by a few specific future dates. For example, we calculate that average monthly nonfarm payroll growth of 414 thousand would cause the unemployment rate to reach 3.8% and the labor force participation rate to reach 63% by the end of 2022. Our sense is that the US economy will be able to add more than 414 thousand jobs per month between now and December 2022. This means that if Fed officials believe that an unemployment rate of 3.8% and a participation rate of 63% meet the definition of “maximum employment”, then they will start to lift interest rates by then. This example sets the scene for what will become next year’s most important monetary policy debate. What constitutes “maximum employment”? Does our example of a 3.8% unemployment rate and a 63% participation rate meet the definition? Or does the Fed have different targets in mind? The Fed will be forced to clarify its position on the topic as the labor market gets closer to reasonable definitions of “maximum employment”. Our sense is that, as of now, there are a range of views on the committee with some FOMC participants taking a more hawkish view of how much slack is left in the labor market and some adopting a more dovish posture. We outline the differences between the hawkish and dovish positions below, but ultimately the path of inflation in 2022 will determine which camp wins out. If inflation remains high next year, then the Fed will be quicker to declare that the labor market is at “maximum employment”, and vice-versa. The Fed’s reliance on the inflation data to settle the argument of what constitutes “maximum employment” will make inflation the most important economic indicator for bond yields in 2022. Labor Market Slack: The Hawkish Case Chart 2The Unemployment Rate Is Falling Fast

The Unemployment Rate Is Falling Fast

The Unemployment Rate Is Falling Fast

The hawkish case for the US labor market reaching “maximum employment” sooner rather than later was outlined nicely last month by our own Bank Credit Analyst.3 First, the Bank Credit Analyst points out that the US labor market was likely beyond “maximum employment” before COVID-19 struck. The implication being that the Fed may move to lift interest rates before the unemployment and participation rates fully recover their pre-pandemic levels. Notice that the unemployment rate (adjusted for the post-COVID surge in people employed but absent from work) was 3.5% in February 2020, well below the Congressional Budget Office’s 4.5% estimate of the natural rate of unemployment (Chart 2).4 Today, the adjusted unemployment rate is 5.5%, not that far above the 3.5%-4.5% range of FOMC participant estimates of the natural rate. If this year’s rate of decline continues, the unemployment rate will hit 4.5% by January 2022 and 3.5% by May 2022. Of course, we know that the Fed takes a broader view of labor market utilization than just the unemployment rate. In particular, we observed sharp declines in labor force participation rates across a wide range of demographic groups when the pandemic struck last year (Chart 3). While the Fed will want to see some improvement in labor force participation, it might be unrealistic to expect the overall labor force participation rate to return to its pre-pandemic level. This is because the aging of the US population imparts a structural downtrend to the participation rate. The dashed line in Chart 4 shows where the participation rate would be if the rate of labor force participation of every individual age cohort remained constant at its February 2020 level. Even in this case, the greater flow of people into the older age groups causes the part rate to fall over time. The message from Chart 4 is that even if the participation rates of every age cohort tracked by the Bureau of Labor Statistics rebound to their February 2020 levels, we would still only expect an overall participation rate of 62.8% by the end of 2022, significantly below the 63.3% seen in February 2020. Chart 3Labor Force Participation By Age Cohort

Labor Force Participation By Age Cohort

Labor Force Participation By Age Cohort

Chart 4The Demographic Downtrend In Participation

The Demographic Downtrend In Participation

The Demographic Downtrend In Participation

On top of the demographic argument, we also notice that the pandemic led to a surge in the number of retired people last year, a number that continues to rise quickly (Chart 5). While we should probably expect some increase in the flow of people coming out of retirement to re-join the labor force as the economy recovers, it’s also logical to assume that there will be at least some hysteresis among the retired population. That is, the longer someone is retired, the less likely they are to re-enter the labor force at all. To the extent that the increase in retired people is sticky, it may be ambitious to expect a full convergence of the 55-year+ part rate back to February 2020 levels (Chart 3, bottom panel). All else equal, this will cause the labor market to reach “maximum employment” more quickly than even our demographic trendline for participation suggests. Chart 5A Surge In Retirees

A Surge In Retirees

A Surge In Retirees

The question of how many FOMC participants agree with the above arguments remains open, but our sense is that there are some who will be eager to declare that “maximum employment” has been achieved before we see a full rebound in the unemployment and participation rates back to pre-COVID levels. For example, Fed Vice-Chair Richard Clarida mentioned the “demographic trend” in labor force participation in his most recent speech.5 Also, Dallas Fed President Robert Kaplan said the following in a recent interview: We’ve had 3 million retirements since February 2020. […] Some of these workers will come back into the workforce, but some of these workers are 55 and older and they’re in reasonably good financial shape and COVID has caused them to re-think whether they really want to re-enter the workforce.6 Labor Market Slack: The Dovish Case There are also good arguments on the side of those who think that an appropriate definition of “maximum employment” involves an unemployment rate closer to 3.5% than 4.5% and a participation rate that does return to pre-COVID levels, and maybe even moves higher. First, a study from the Federal Reserve Bank of Kansas City noted that the bulk of the recent increase in the number of retired people is explained, not by an increase in the number of retirements, but by a reduction in the flow of people from retirement back into the workforce (Chart 6).7 This suggests that pandemic-related health risks are the likely culprit behind the increase in the number of retired people, casting doubt on the idea that the increase in retired people will be sticky. Chart 6Increased Retirees: A Closer Look

2022 Will Be All About Inflation

2022 Will Be All About Inflation

Second, there is a strong case to be made that even the February 2020 labor force participation rate is not high enough to meet the definition of “maximum employment”. If we look at the participation rates for 25-54 year old men and women, we see that both were in strong uptrends prior to the pandemic (Chart 7), and there is every reason to believe that they would have continued to move higher if COVID hadn’t cut the recovery short. Chart 7Part Rates Were Rising Pre-Pandemic

Part Rates Were Rising Pre-Pandemic

Part Rates Were Rising Pre-Pandemic

Consider what some FOMC participants were saying prior to the pandemic: The strong labor market is also encouraging more people in their prime working years – ages 25 to 54 – to rejoin or remain in the labor force, […] So far, we have made up more than half the loss in the Great Recession, which translates to almost 2 million more people in the labor force. But prime age participation could still be higher. - Jerome Powell, November 20198 Whether participation will continue to increase in a tight labor market remains to be seen. But I note that male prime-age participation still remains below levels seen in previous business cycle expansions. - Richard Clarida, November 20199 In a more recent interview, Minneapolis Fed President Neel Kashkari expressed skepticism about the idea that labor force participation is destined to remain in a long-run structural downtrend and said that he’s “not convinced we were actually at maximum employment before the COVID shock hit us.” He also said: Getting [labor force participation] and employment-to-population at least back to where they were before [the pandemic], but not necessarily even declaring victory when we do that. I think that’s a reasonable thing for us to try to achieve.10 Inflation: The Ultimate Argument Settler What the above arguments make clear is that there are good reasons to think that the US labor market will reach some policymakers’ definitions of “maximum employment” perhaps by as early as the middle of next year. However, there are also some policymakers who will adopt a more dovish view of what constitutes “maximum employment”. Ultimately, the path of inflation will determine which camp wins out. This is because the entire concept of “maximum employment” is only meaningful when viewed alongside inflation. If employment is pushed beyond its “maximum”, it definitionally means that labor market tightness is leading to unwanted inflationary pressures. With that in mind, the Fed will increasingly refer to the inflation data next year as it tries to make its definition of “maximum employment” more precise. Crucially, what will matter for the Fed (and for the bond market) is where inflation is next year, not where it is right now. Right now, core inflation is well above the Fed’s price stability target, but it is well known that the recent increase in inflation is concentrated in a few sectors – COVID-impacted services and autos – where prices will decelerate as post-pandemic bottlenecks ease (Chart 8). Just as the Fed ignored surging prices in those sectors this year, it will ignore plunging prices in those sectors next year. What will matter for monetary policy is whether core inflation excluding COVID-impacted services and autos remains contained or rises above levels consistent with the Fed’s target (Chart 8, bottom panel). The Fed will also be inclined to declare that “maximum employment” has been achieved if wage growth is accelerating. Currently, there is some evidence of rising wages but also some major supply bottlenecks in the labor market, as evidenced by the all-time high in job openings (Chart 9). Labor supply constraints should ease next year, but the Fed will be watching closely to see if wage growth moderates in kind or continues to increase. Chart 8Watch CPI (ex. COVID-Impacted Services And Autos) In 2022

Watch CPI (ex. COVID-Impacted Services And Autos) In 2022

Watch CPI (ex. COVID-Impacted Services And Autos) In 2022

Chart 9Watch Wages In 2022

Watch Wages In 2022

Watch Wages In 2022

Finally, the Fed will keep a close eye on inflation expectations next year. In particular, it will monitor the Common Inflation Expectations Index and the 5-year/5-year forward TIPS breakeven inflation rate (Chart 10). If either of these indicators break above levels consistent with the Fed’s 2% inflation target, then policymakers will be more inclined to think that “maximum employment” has been attained. Chart 10Watch Inflation Expectations In 2022

Watch Inflation Expectations In 2022

Watch Inflation Expectations In 2022

Bottom Line: The Fed will be forced to clarify its definition of “maximum employment” in 2022, and the path of inflation will ultimately dictate how far the Fed tries to push the labor market. The key indicators to monitor to decide when the Fed will declare that “maximum employment” has been attained are: core inflation excluding COVID-impacted services and autos, wage growth, inflation expectations and the prime-age (25-54) labor force participation rate (Chart 3, panel 2). Investment Implications For bond markets, the question of when the Fed decides that the labor market has reached “maximum employment” is crucial because it will determine the start of the next rate hike cycle. At present, the overnight index swap curve is priced for Fed liftoff in January 2023 and for a total of 78 bps of rate hikes by the end of 2023 (Chart 11). Chart 11Rate Hike Expectations

Rate Hike Expectations

Rate Hike Expectations

Our expectation is that the Fed will start lifting rates in December 2022 and that rate hikes will proceed more quickly than what is currently priced in the market. The unemployment rate will be close to 3.5% by December 2022 and inflation will be sufficiently above the Fed’s target that policymakers will be inclined to view the labor market as at “maximum employment”. Investors should run below-benchmark duration in US bond portfolios to profit from this outcome. We also recommend that investors position for a flatter yield curve by the end of 2022. Specifically, we recommend shorting the 5-year Treasury note versus a duration-matched barbell consisting of the 2-year and 10-year notes. Table 1A shows fair value estimates for the 2-year, 5-year and 10-year yields as of the end of 2022 assuming the market moves to price-in the following path for the fed funds rate: The first 25 bps rate hike occurs in December 2022 Rate hikes proceed at a pace of 100 bps per year The fed funds rate levels-off at a terminal rate of 2.08%11 Table 1ATreasury Curve Fair Value Estimates: December 2022 Liftoff Scenario

2022 Will Be All About Inflation

2022 Will Be All About Inflation

In that example, the 2-year and 5-year yields both rise by much more than the 10-year yield and both exceed the change that is priced into the forward curve by more than the 10-year yield. Table 1B shows the results from a similar scenario, the only difference is that the liftoff date is pushed back to March 2023. Both the 2-year and 5-year yields also rise by more than the 10-year yield in this scenario, though the delayed liftoff dampens the relative upside in the 2-year yield. Table 1BTreasury Curve Fair Value Estimates: March 2023 Liftoff Scenario

2022 Will Be All About Inflation

2022 Will Be All About Inflation

Bottom Line: Investors should maintain below-benchmark portfolio duration and position in Treasury curve flatteners in anticipation of a rate hike cycle that will start in December 2022. Appendix: How Far From “Maximum Employment” And Fed Liftoff? Chart A1Defining “Maximum Employment”

Defining "Maximum Employment"

Defining "Maximum Employment"

The Federal Reserve has promised that the funds rate will stay pinned at zero until the labor market returns to “maximum employment”. The Fed has not provided explicit guidance on the definition of “maximum employment”, but we deduce that “maximum employment” means that the Fed wants to see the U3 unemployment rate within a range consistent with its estimates of the natural rate of unemployment, currently 3.5% to 4.5%, and that it wants to see a more or less complete recovery of the labor force participation rate back to February 2020 levels (Chart A1). Alternatively, we can infer definitions of “maximum employment” from the New York Fed’s Surveys of Primary Dealers and Market Participants. These surveys ask respondents what they think the unemployment and labor force participation rates will be at the time of Fed liftoff. Currently, the median respondent from the Survey of Market Participants expects an unemployment rate of 3.5% and a participation rate of 63%. The median respondent from the Survey of Primary Dealers expects an unemployment rate of 3.8% and a participation rate of 62.8%. Tables A1-A4 present the average monthly nonfarm payroll growth required to reach different combinations of unemployment rate and participation rate by specific future dates. For example, if we use the definition of “maximum employment” from the Survey of Market Participants, then we need to see average monthly nonfarm payroll growth of +414k in order to hit “maximum employment” by the end of 2022. Table A1Average Monthly Nonfarm Payroll Growth Required For The Unemployment To Reach 4.5% By The Given Date

2022 Will Be All About Inflation

2022 Will Be All About Inflation

Table A2Average Monthly Nonfarm Payroll Growth Required For The Unemployment To Reach 4% By The Given Date

2022 Will Be All About Inflation

2022 Will Be All About Inflation

Table A3Average Monthly Nonfarm Payroll Growth Required For The Unemployment To Reach 3.5% By The Given Date

2022 Will Be All About Inflation

2022 Will Be All About Inflation

Table A4Average Monthly Nonfarm Payroll Growth Required To Reach “Maximum Employment” As Defined By Survey Respondents

2022 Will Be All About Inflation

2022 Will Be All About Inflation

Chart A2 presents recent monthly nonfarm payroll growth along with target levels based on the Survey of Market Participants’ definition of “maximum employment”. This chart is to help us track progress toward specific liftoff dates. For example, if monthly nonfarm payroll growth continues to print at the same level as last month, then we could anticipate a Fed rate hike by June 2022. Chart A2Tracking Toward Fed Liftoff

Tracking Toward Fed Liftoff

Tracking Toward Fed Liftoff

We will continue to track these charts and tables in the coming months, and will publish updates after the release of each monthly employment report. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “Watch Employment, Not Inflation”, dated June 15, 2021. 2 Specifically, the Fed’s forward guidance states that it will not lift interest rates until (i) inflation is above 2%, (ii) inflation is expected to remain above 2% for some time and (iii) the labor market has reached “maximum employment”. 3 Please see Bank Credit Analyst Special Report, “The Return To Maximum Employment: It May Be Faster Than You Think”, dated August 26, 2021. 4 For details on the adjustment we make to the unemployment rate please see US Bond Strategy Weekly Report, “Overreaction”, dated July 13, 2021. 5 https://www.federalreserve.gov/newsevents/speech/clarida20210804a.htm 6 https://www.bloomberg.com/news/articles/2021-08-09/dallas-fed-president-rob-kaplan-on-the-economy-and-monetary-policy-right-now?sref=Ij5V3tFi 7 https://www.kansascityfed.org/research/economic-bulletin/what-has-driven-the-recent-increase-in-retirements/ 8 https://www.federalreserve.gov/newsevents/speech/powell20191125a.htm 9 https://www.federalreserve.gov/newsevents/speech/clarida20191114a.htm 10 https://www.bloomberg.com/news/articles/2021-08-16/neel-kashkari-on-the-fed-s-quest-to-get-to-full-employment?srnd=oddlots-podcast&sref=Ij5V3tFi 11 We assume a target range of 2% to 2.25% for the terminal fed funds rate. We also assume that the effective fed funds rate trades 8 bps above the lower-end of its target band, as is presently the case. Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

9 September 2021 at 10:00 EDT Emerging Markets Strategy/Webcast EM/China: See The Forest For The Trees 9 September 2021 at 21:00 EDT Emerging Markets Strategy/Webcast Emerging Asia: See The Forest For The Trees Highlights Structural inflation in India has abated noticeably since the mid-2010s. The cyclical inflation outlook is also benign (Chart 1). As such, the specter of inflation does not pose a material threat to this stock market. Indian stocks’ high valuation is a risk; yet this bourse’s structurally high premium relative to EM will likely continue as India’s earnings growth will stay strong and its volatility low. Investors should stay overweight Indian stocks in an EM equity portfolio, and local currency bonds in an EM domestic bond portfolio. Feature Chart 1India's Cyclical Inflation Outlook Is Benign

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

In a recent Emerging Markets Strategy report we showed that India stands out as the only country in Asia with rather high inflation. Indeed, core CPI in India, at about 6%, is higher than all other major EM and DM countries, save Turkey and Russia. The question is, with the economy re-opening, will Indian inflation rise further and thus derail the rally in Indian equities? Our research indicates that both the structural and cyclical inflation outlook for India remains benign. Our models for headline and core CPI both point to lower inflation in the coming months (Chart 1). As such, inflation is unlikely to pose any major threat to Indian assets in the foreseeable future. Investors should remain overweight Indian stocks in an EM equity portfolio. Fixed-income investors should also continue to overweight Indian local bonds in an EM domestic bond portfolio. Currency traders should favor the rupee versus its EM peers. Inflation Outlook: Structural … The first of the two principal drivers of India’s structural inflation trend is the country’s productivity. The stronger the productivity gains, the more contained has been its structural inflation. The second major driver is broad money supply. The higher the money growth, the steeper have been inflationary pressures – especially during those periods when productivity gains were timid. Top panel of Chart 2 shows that up until the early-2000s, India’s average productivity gains used to be rather low: of the order of 3% annually. That period was also marked by very strong broad money growth: at times, the latter would rise to 20% annually (Chart 2, bottom panel). This growth was due to chronically high fiscal deficits that were monetized, coupled with intermittent surges in bank credit. Chart 2Slower Money Supply Amid Decent Productivity Led To A Structural Decline In Inflation

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

The consequence of persistently low productivity gains amid strong money supply was structurally high inflation, with occasional flare-ups well into double digits (Chart 2). Chart 3Steady Fall In Budget Deficits In Post-GFC Era

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

From the early 2000s, however, that dynamic began to change. A surge in capital spending in infrastructure and other productive capacity propelled India’s productivity trend up by several notches. In the past 15 years, the productivity growth rate has averaged around 6% a year; even though more recently that rate has slowed. In the post-GFC period, both major sources of money creation were stymied. First, successive Indian governments, regardless of political affiliation, adopted a rather tight fiscal policy. They reined in fiscal outlays substantially. Non-interest expenditures of the central government fell from 14% of GDP in 2010 down to 9% by 2019, just before the pandemic (Chart 3, top panel). As a result, during that period, fiscal and primary deficits narrowed significantly: from almost 7% of GDP to 3%, and from almost 4% of GDP to nearly zero, respectively (Chart 3, bottom panel). In addition, a myriad of reasons1 caused commercial bank credit to decelerate materially – from as high as 30% before the GFC to a mere 6% by 2019. The upshot of all this was a secular decline in broad money growth. That eventually led India’s inflationary pressures to decline structurally since the mid-2010s (Chart 2, bottom panel, above). Going forward, those major drivers (both productivity and money growth) will warrant a benign inflation outlook. The country has been continuing its high capital spending for over a decade now (around 30% to 35% of GDP, a rate second only to China). This year, India’s capital spending has already revived. Other corroborating indicators such as imports of capital goods have also recovered robustly. This indicates a new capex cycle is unfolding. Therefore, odds are that the productivity growth rate will stay decent. Prudent fiscal policy, on the other hand, will keep the money growth in check. Chart 4Low Wages Will Help Keep Inflation Subdued

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Finally, wage pressures in India will also stay muted. In rural areas, both farm and non-farm nominal wages have been growing at a very slow pace; and are now flirting with outright contraction (Chart 4, top panel). Industrial wage expectations have also been tepid over the past several years (Chart 4, bottom panel). The broader picture is unlikely to change in the future as tens of millions of young people continue to join the work force every year. Taken together, these factors point to subdued structural inflation ahead. … And Cyclical The chance that inflation in India will flare up over a cyclical horizon (12 months) is also low: First, one of the major cyclical drivers of inflation in India, the government’s food procurement prices (called Minimum Support Price or MSP) have stayed low for the past several years. The announced MSPs for some of the crops for the 2021-22 agriculture season (July-June) have also shown no marked increase. This will surely help keep the wholesale prices for food in check, which, in turn, will keep a lid on consumer inflation expectations and ultimately on both headline and core consumer inflation (Chart 5). Second, the country’s money growth is also unlikely to witness an immediate, major boom. While the budget deficit has swelled over the past year or so, odds are that the government will revert to the tighter fiscal stance that prevailed over the past decade – as soon as the pandemic is brought under control. Chart 6 shows that government non-interest spending leads core CPI. Reduced expenditure growth will cap inflation. Chart 5Low Food Prices Will Keep A Lid On Inflation Expectations

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Chart 6Slowing Fiscal Spending Will Cap Core Inflation

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Chart 7Fuel Price Inflation Is Set To Decelerate

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

The other contributor to money growth, bank credit, is expected to accelerate; but its expansion will not be rapid as banks are still suffering from elevated NPLs. Third, fuel price inflation has likely peaked in India. Last year authorities imposed substantial new taxes on local gasoline and diesel prices, which artificially raised consumer inflation (Chart 7). Since there is little chance of new fuel levies this year and given that crude prices are unlikely to rise much from the current levels (which is EMS’s view), fuel inflation will subside materially next year. And as fuel costs often eventually spill into core inflation, this deceleration will help check the latter as well. Finally, given the massive negative output gap that opened up in the economy during the pandemic-related lockdowns, it will take a while before the economy overheats again. Odds are therefore low that India’s inflation will accelerate much in the coming months. Notably, our cyclical inflation models for both headline and core CPI – built using the drivers discussed above – also vouch for a modest decline in inflation (Chart 1, on page 1). Does Inflation Hurt Stocks? Currently, the Indian economy is not plagued by any major excesses and therefore has no major macro vulnerability. The only potential vulnerability that the economy and stock markets face stem from any possible rise in inflation. Notably, the primary driver of Indian stocks is economic growth and corporate profits. Historically, inflation (CPI) in low- and mid-single digits did not hurt Indian stocks. However, once inflation approached a high-single digit mark (usually 8%), a sell-off in stocks typically occurred. Chart 8 shows that, during India’s high-inflation era (from 1994 to 2013), every time CPI breached the 8% mark (the dotted line in the chart), stocks fell in absolute USD terms, or at the minimum, were weak. Chart 8Indian Stocks Faced Major Headwinds When Headline CPI Approached 8%

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Chart 9In Recent Years Inflation Has Ceased To Be A Headwind For Indian Stocks

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Interestingly, the above correlations have changed dramatically since 2014. The top panel of Chart 9 shows that core CPI does not have any steady correlation with stock prices anymore. And core PPI, in fact, has developed a strong positive correlation with stocks (Chart 9, bottom panel) – in complete reversal of the dynamics that prevailed in the previous two decades. The adverse impact of inflation on stock prices is via multiple compression, as rising interest rates lead to equity de-rating. What’s notable is that the multiple compressions do not begin as soon as a rate hike cycle commences. Rather, it takes a meaningful rise in interest rates before it starts to hurt multiples (Chart 10). Given the above, one can expect a material multiple compression only if inflation rises a few notches above the central bank’s target (Chart 11). The odds of that happening now are low. Therefore, policy rates will remain lower for longer, and stock valuations will remain at a higher level than usual. Chart 10Interest Rates Usually Needed To Rise Several Points Before Stock Multiple Compression Began

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Chart 11India's Inflation Remains Within RBI Target Bands

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Incidentally, thanks to material rate cuts, real interest rates paid by Indian firms – deflated by both core producer and core consumer prices – have plummeted. Lower real rates benefit the borrowers (i.e., non-financial listed companies) (Chart 12). The bottom line is that, with India’s inflation now being both structurally low (by Indian history) and cyclically tame, it is unlikely to be a cause of any major equity sell-off. Are Indian Equity Valuations Justified? With a trailing P/E of 31, and P/Book of 3.9, there is no doubt that Indian stocks are expensive. Yet, part of the multiple expansion in India, like most other DM countries, has been a direct outcome of a sharply lower policy rate, as discussed above. Incidentally, if one were to look at the cyclically adjusted valuation measures (CAPE), Indian markets appear to be only moderately expensive (Chart 13, top panel). Chart 12Lower Real Rates Boost Firms' Profits And Warrant Higher Stock Prices

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Chart 13Cyclically-Adjuted P/E Ratio

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Chart 14Relative Equity Multiples: India vs. EM

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

In terms of relative valuation vis-à-vis the rest of the EM, Indian stocks continue to command a high premium: around 90% in the case of P/E and P/Book multiples. (Chart 14). In terms of cyclically adjusted valuation (CAPE) relative to the EM, India also appears to be quite pricey (Chart 13, bottom panel). The bottom line is that Indian stocks are expensive; and that is a risk to this bourse. A pertinent question here is whether India still merits the structurally high premium that it has enjoyed over the years relative to its peers. Our answer is in the affirmative. One reason this bourse has continued to enjoy a high premium, especially since the mid-2000s, is because the growth of Indian corporate earnings has been superior to those of most other EM countries. But more importantly, the volatility of those earnings has been much lower than its peers. These strong, yet less volatile earnings are what investors have been willing to pay a premium for. Going forward, we see both traits remaining intact. Long-term growth in India will likely stay as one of the highest in the EM world. Earnings volatility is also unlikely to change anytime soon. The reason is, first, lower inflation going forward will entail relatively lower interest rate volatility, and therefore, lower business cycle / earnings volatility. Second, India’s currency volatility will also likely stay lower. Part of the reason is the near absence of foreign investors on government bonds in India. This has precluded India from suffering a major currency sell-off during global risk-off episodes – as few bond investors head for the exit. We discussed this and several other issues related to Indian bond markets and the rupee in much greater detail in our last report on India. Taken together, lower volatility in both local currency earnings and the exchange rate entails lower overall volatility for US dollar-denominated earnings. That will help Indian stocks’ premium to stay elevated beyond any short-term fluctuations. Inflation And The Rupee Chart 15The Rupee Strengthens When Relative Inflation In India Versus US Decelerates

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

The impact of inflation on the rupee is nuanced. It’s not the absolute level of India’s CPI or PPI that affects the rupee-dollar exchange rate; it’s the relative inflation between these two economies that does so. Chart 15 shows that the rupee usually strengthens versus the dollar when inflation in India falls relative to that of US (shown in inverted scale in the chart). These relative inflation dynamics could also provide insight into the exchange rate outlook. Chart 16 shows that the rupee is currently 10% cheaper when measured against what would be its “fair value” (Chart 16, bottom panel). The fair value has been derived from a regression analysis of the exchange rate on the manufacturers’ relative producer prices of the two countries. Investment Recommendations Indian stocks have decisively broken out both in absolute terms and relative to their EM counterparts (Chart 17). Notably, the outperformance is not just due to a sell-off in Chinese TMT stocks. It is even more impressive relative to the ‘mainstream EM’ bourses (i.e., EM excluding China, Taiwan and Korea). Given India’s relatively superior structural and cyclical backdrops, this outperformance should continue for a while (Chart 17, bottom two panels). Investors should stay overweight this bourse in an EM equity portfolio. Chart 16The Indian Rupee Is Now About 10% Below Its Fair Value Versus The US Dollar

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Chart 17Indian Stocks' Breakout Is Decisive And The Relative Outperformance Is Broad-based

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

Chart 18Higher Carry And A Better Currency Outlook Will Lead To Indian Domestic Bonds' Outperformance

Can Inflation Upset The Indian Applecart?

Can Inflation Upset The Indian Applecart?

The medium-term outlook for the rupee is also positive. The currency is cheap and competitive –an added incentive for both foreign direct investors and portfolio investors. Finally, Indian domestic bonds offer value – both relative to their EM peers and the US treasuries. 10-year government bonds yields, at 6.2%, offer an enticing 480 basis points over similar duration US Treasuries. Given the sanguine rupee and inflation outlooks, Indian bonds will likely continue to outperform EM local bonds (Chart 18). Investors should stay on with our recommendation of overweighting India in an EM local currency bond portfolio. Rajeeb Pramanik Senior EM Strategist rajeeb.pramanik@bcaresearch.com Footnotes 1 The reasons include a surge in bank NPLs, lack of bankable projects, a kind of policy paralysis resulting in delay in various regulatory clearances for capital projects etc.

Highlights Economy – Goldilocks remains our base-case macro backdrop for the next twelve months: The transitory inflation narrative is still intact, despite persistently high consumer price increases, suggesting that the economy will not overheat. The Delta wave has roiled many communities, but COVID is unlikely to spark a growth outage unless a vaccine-resistant variant emerges. Markets – Above-trend growth and extraordinarily accommodative monetary policy is a sweet spot for risk assets: As long as the Fed’s novel policy of adding monetary stimulus to an economy growing way above trend doesn’t give rise to unnervingly high inflation, the combination will be conducive to continued equity and credit outperformance. Strategy – Continue to overweight risk assets within multi-asset portfolios: There’s more to investment returns than the state of the business, credit and monetary policy cycles but they make a powerful case against turning defensive in the near term. Feature We had several virtual meetings with clients in August and inflation, the Fed and the growth outlook were frequently recurring themes. In this week’s report, we share some of the most common questions, along with our take on them, so that all clients can see what we’ve been discussing with their peers. In the interest of space, we confine the discussion to our base-case scenarios, but future outcomes appear to be even more uncertain than they normally are against a backdrop of unprecedented policy settings. We advise investors to remain vigilant and be prepared to hold positions for shorter-than-usual durations in the event circumstances change. Inflation prints remain high, pressuring the Fed’s transitory narrative. What will happen to markets if investors reject it? Chart 1Losing Steam?

Losing Steam?

Losing Steam?

Inflation prints do remain high, with headline CPI rising 0.5% month-over-month and 5.3% year-over-year in July and core CPI rising 0.3% and 4.2%. Both series modestly exceeded expectations, though they recorded their smallest sequential gains since February and their year-over-year increases came in just below the peaks recorded in June (Chart 1). It is possible that consumer price increases have begun to decelerate though it will take more data to confirm the existence of a new trend. Reports of continued bottlenecks driven by component shortages, transport challenges and the Delta infection wave suggest that even if the factors that have pushed inflation higher are beginning to abate, they may linger in some form for longer than initially expected. The transitory narrative remains intact, however. Drilling into the components of the elevated core CPI reveals that a handful of categories that have been particularly impacted by the pandemic are exerting outsized influence over the index. When we published the initial version of Table 1 in late May, nine categories powered April’s reported core inflation. This time there are eight, as the five shaded components have come off the boil and the four components shown in an indented font have newly begun to run hot. Table 1Temporary Irritants

Discussing Inflation, Growth And Market Implications

Discussing Inflation, Growth And Market Implications

Excepting historically volatile recreational services and water, sewer and trash services, which have been increasing in price far faster than other goods and services for a while, the hot categories’ moves have been extreme relative to their own history. Unless their spaces have undergone lasting structural changes, we expect their two-plus standard deviation moves will not be sustained. The biggest outliers, lodging and new vehicles, can be explained entirely by the pandemic and once hotels are able to return to full capacity and an end to the semiconductor shortage allows automakers to resume normal production levels, they will come back to earth. The turnover among the outliers supports the transitory narrative, as price spikes in categories that have long lagged the overall basket, like airfares and used cars, or have experienced long deflationary skids, like furniture and bedding, appear to have been fleeting. Chart 2Back To The Early Nineties

Back To The Early Nineties

Back To The Early Nineties